Sample Category Title

EUR/USD Test Of Resistance, GBP/USD Pushing Higher, USD/JPY Weak Bounce.

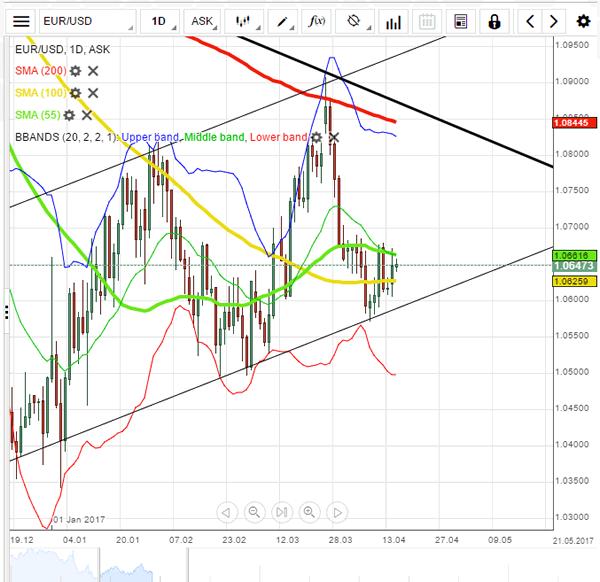

EUR/USD Test of resistance.

EUR/USD has improved, yet failure to break resistance suggest a reversal. Monitor the resistances area given by 1.0679. Hourly support can be found at 1.0650 (intraday base) then 1.0570 (11.04.2017 low). Stronger support can be found at 1.0494 (22/02/2017 low). A key resistance stands at 1.0874.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

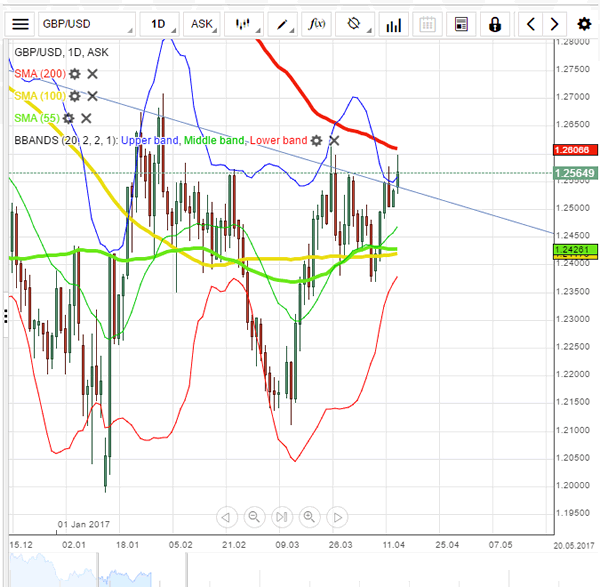

GBP/USD Pushing higher.

GBP/USD has rallied off key support at 1.2334, suggesting a potential short-term base formation. Key resistance stands at 1.2605 (27/03/2017 high). An hourly support can be found at 1.2581 (12/04/2017 base) then 1.2405 (11/04/2017 low).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

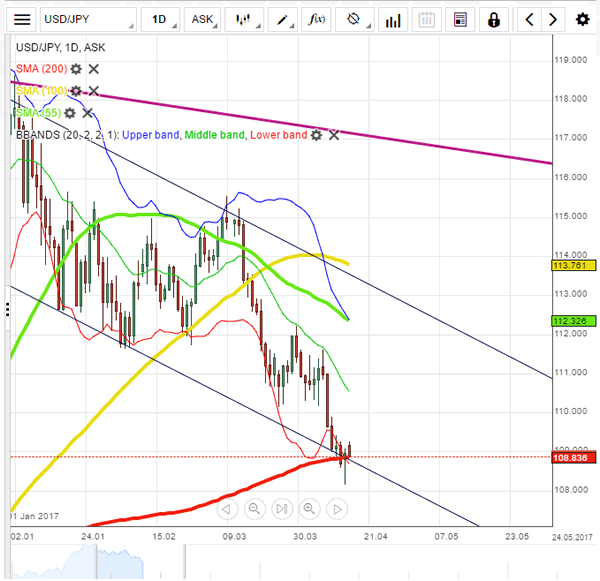

USD/JPY Weak bounce.

USD/JPY has broken to the downside out of the horizontal support at 110.11 confirming a bearish bias. Next support can be located at 108.22 (intraday low). Other key supports lie at a distant 106.04 (11/11/2016 low). Resistance can be found at 110.11, while a key resistance stands at 112.20 (31/03/2017 high).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Commodities Fall As Mnuchin Trumps The Dollar

Treasury Secretary Mnuchin's strong dollar comments saw the greenback rally across most asset classes.

PRECIOUS METALS

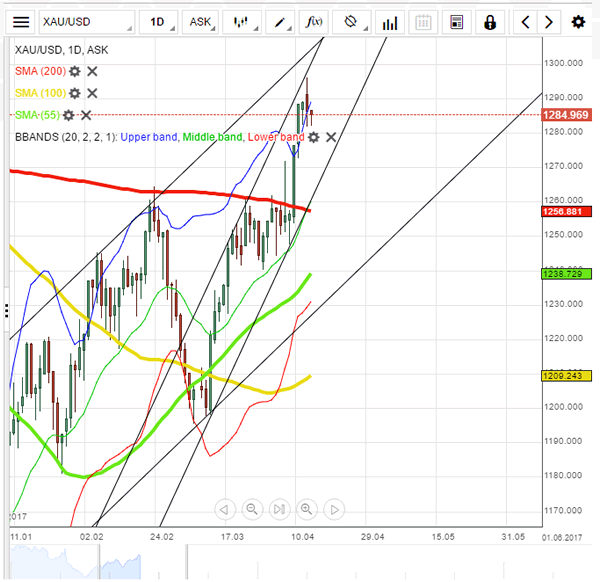

Gold fell from its high above 1295 to 1280 overnight, but gold has made a sprightly start in Asian trading, up five dollars to the 1285 level in the early part of the session, before drifting back to 1283.

This reinforces the view that gold is trading as a function of safe haven demand, with ongoing geopolitical tensions meaning that dips will be eagerly sought by investors and traders alike. This weekend's French Presidential first round elections are looking increasingly murky, and this will most likely fan those haven fires.

Gold has initial support at 1280 with major support at the 1255/60 region, the break-out and the 200-day moving average. Above, gold has resistance at 1296, 1300 and 1308. In all likelihood though, it will be news headlines and opinion polls that drive gold's short-term direction.

Silver suffered much the same fate as gold overnight and for exactly the same reasons. Silver fell from 18.6600 to close at 18.4100 for the New York session. More concerningly, silver has traced an outside reversal day on the daily charts which are a bearish formation in this case. However one could qualify this, as the move has occurred in a low liquidity holiday market. One suspects that silver will trade on the news as well and not technicals.

Silver has support at 18.3500 initially with possibly some weak long liquidation if it breaks. Behind this, we have support at 18.2500 and then the 200-day moving average at 18.0500.

Resistance lies intra-day at 18.4500 and then yesterday's high at 18.6550.

OIL

Both Brent Crude and WTI fell by approximately one percent overnight to leave both hovering just above short-term support in early Asian trading. In a holiday-thinned market, Treasury Secretary Mnuchin's comments were the start of the rot. As the USD rallied across the board, this prompted short-term profit taking in crude as well.

Traders will be eyeing the $55.00 and $52.50 levels for Brent and WTI spot nervously this morning, with a break of either possibly prompting another wave of selling to flush out weak longs. As liquidity is still below average following the Easter break, short term moves could be exacerbated.

The above levels aside, Brent spot has support at $54.00, it's 100-day moving average, with resistance at $56.00 and then $56.50.

WTI spot has support at $51.40, its 100-day moving average, with resistance at the $53.60 region.

Summary

Despite the comments by Mnuchin causing dollar strength, its effect may be temporary given the event risk around the world at the moment. After pausing for breath, precious metals may find support along with oil as the street trades of news headlines this week.

Technical Outlook: USDJPY – Strong Bearish Sentiment Sees Limited Recovery Before Fresh Downside

The pair is holding around 109.00 handle in early European trading, after hitting fresh recovery high at 109.20 in Asia and being so far supported by 200SMA, which reverted to support after recovery broke and close above it.

Monday’s long-tailed daily candle that was formed after strong downside rejection (the pair hit fresh five-month low at 108.11 on Monday) underpins and may spark stronger correction as slow stochastic is emerging from oversold territory and daily RSI is on the border of oversold zone.

However, negative daily studies see limited upside action, before bears resume, as general sentiment is firmly bearish on geopolitical tensions that favor yen’s safe haven buying.

Falling 10SMA offers strong barrier (currently at 109.74) which should ideally cap and keep intact upper pivots at 110.00/25 (psychological barrier/Fibo 61.8% of 111.56/108.11 downleg), break of which is needed to signal stronger recovery.

Conversely, early recovery rejection and return below 200SMA would signal an end of corrective phase and shift near-term focus lower again.

Res: 109.20, 109.74, 110.00, 110.25

Sup: 108.82, 108.55, 108.11, 107.84

Technical Outlook: Cable Cracked 1.2600 Barrier, Eyes Pivotal 200SMA / Trendline Resistance

Cable cracked psychological 1.2600 on fresh strength from correction low at 1.2548, hit in Asia, after Monday's rally stalled at 1.2594.

The pair extends rally from 1.2500 higher base and pressures targets at 1.2613 (27 Mar high) and 1.2620 (200SMA / bear-trendline connecting 06 Dec/ 02 Feb tops).

Technical studies are bullish on all timeframes and favor final break above 1.2613/20 pivots for extension towards 1.2704 (02 Feb high).

Overbought slow stochastic on daily chart suggests consolidation, but without firmer bearish signals for now.

Session low at 1.2548 marks initial support ahead of Monday's low at 1.2521 and higher base at 1.2500, reinforced by 10/20SMA bull-cross at 1.2488.

Res: 1.2605, 1.2613, 1.2620, 1.2671

Sup: 1.2548, 1.2521, 1.2500, 1.2488

Technical Outlook: EURUSD – 10SMA And Rising Daily Cloud Underpin But Close Above 55SMA Is Needed To Signal Further...

The Euro is holding above a cluster of good supports which lay between 1.0628 and 1.0614, consisting of 10/100SMA's and daily cloud top and underpinning near-term action. Monday's break above 10SMA and acceleration to 1.0669 was bullish signal, however, the rally failed to close above 55SMA (1.0657) and confirm bullish continuation. Bullishly aligned near-term studies are supportive for renewed attempts higher and attack at key barriers at 1.0676 (12/13 Apr double recovery rejection) and 1.0700 (Fibo 38.2% of 1.0905/1.0568 descend) break of which would signal fresh extension of recovery phase from 1.0568 (10 Apr low). Caution on probes below 10/100SMA's which may soften near-term structure, as daily technicals are in mixed mode and show no clear direction for now.

Res: 1.0651, 1.0669, 1.0676, 1.0700

Sup: 1.0628, 1.0614, 1.0601, 1.0583

EUR/USD Analysis: Trades Near 1.0650 Mark

'France's presidential race enters its final stretch with no clear winner in sight as the main contenders scrap for votes in a flurry of campaign rallies.' – Geraldine Amiel and Vidya Root, Bloomberg

Pair's Outlook

On Tuesday morning the common European currency fluctuated against the US Dollar just above the 23.60% Fibonacci retracement level, which is located at the 1.0639 level. The rate had retreated to the retracement level due to bouncing off from the resistance put up by the weekly R1, which is located at the 1.0672 level. It is most likely that the currency exchange rate will rebound against the Fibonacci retracement level and continue on its path higher. However, the strong resistance cluster just above it, near the 1.0680 mark, will hinder the rates surge.

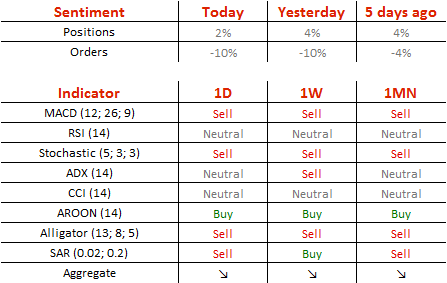

Traders' Sentiment

Traders are almost neutral, as 51% of open positions are long. Meanwhile, 55% of set up orders are to sell the Euro.

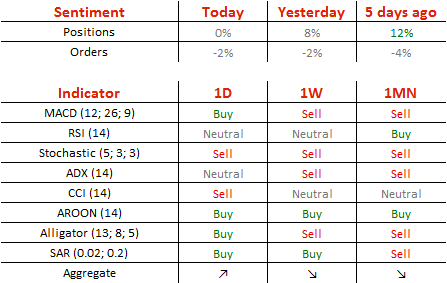

GBP/USD Analysis: Keeps Climbing Up

'There's significant resistance for GBP/USD between 1.25 and 1.2630.' – BK Asset Management (based on PoundSterlingLive)

Pair's Outlook

Monday ended with the British Pound outperforming the US Dollar, which resulted in the six-month bearish trend-line getting pierced. The Cable, however, now faces another strong resistance, namely the cluster around 1.2610, represented by the upper Bollinger band, the weekly R1 and the 200-day SMA. Technical indicators keep pointing to another potential rally today, in which case the Sterling would have the opportunity to reclaim 1.26. Nevertheless, there is no impetus present that could help the GBP/USD pair overcome the 200-day SMA at 1.2626, not yet at least.

Traders' Sentiment

Market sentiment reached a perfect equilibrium today, but the portion of orders to sell the Pound remained unchanged, still taking up 51% of the market.

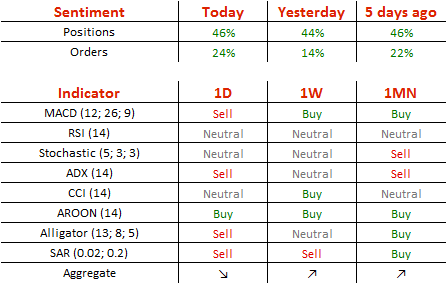

USD/JPY Analysis: Attempts To Preserve The Channel Pattern

'It is unclear whether the situation over North Korea will escalate into military action, but uncertainty is increasing and the dollar continues to edge lower. The dollar also looks shaky technically, after slipping below the 200-day moving average of 108.80 yen.' – Mizuho Securities (based on Reuters)

Pair's Outlook

Despite initial sharp downside volatility, the US Dollar managed to end the day in the green zone yesterday, adding 14 pips against the Japanese Yen. The recovery suggests that the channel pattern remains in play, but with the lower bounder now being significantly weaker. A successful rally today could be the first step towards reaching the pattern's resistance line near 112.00, but technical indicators are unable to confirm this scenario. Downside risks are also present due to the recent breach, but the US fundamental data could provide the required boost for the given pair to stabilise above 109.00.

Traders' Sentiment

The Buck remains overbought, as 73% of all open positions are long (previously 72%). The number of orders to acquire the Greenback inched up from 57 to 62%.

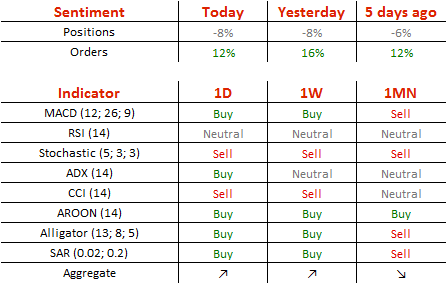

Gold Analysis: Retreats On Tuesday

'The U.S. dollar steadied after Treasury Secretary Steven Mnuchin said U.S. President Donald Trump's recent remarks that the dollar is getting too strong were about the short term.' – Nallur Sethuraman, Reuters

Pair's Outlook

After hitting a five month high level the gold price began a period of consolidation, which became a decline due to fundamental events. The main reason for the decline of the bullion's price was the comments made by the Treasury Secretary of the US Steven Mnuchin, who expressed that the US President sees the strong US Dollar only as a problem in the short term. It is most likely that the bullion will continue its surge, as turmoil around the world drives the run to safety. Moreover, a new medium term ascending channel pattern seems to have revealed itself due to the recent decline of the commodity price.

Traders' Sentiment

SWFX gold traders remain bearish, as 54% of open positions are short. However, 56% of set up orders are to buy the metal.

Investors Turn To Safe Havens On Rising Regional Tensions

Recent US military actions, such as the airstrike in Syria, the movement of an aircraft carrier strike group toward the Korean Peninsula and the dropping of 'the mother of all bombs' on ISIS in Afghanistan has led to rising tensions amongst some of the world superpowers.

The rising regional tensions have lifted the markets' risk aversion sentiment. Investors are turning away from riskier assets towards safe havens, resulting in the weakening of US equity markets. Monday April 17, saw spot gold surge to the highest level of 1295.37 since November 9, it has rallied 2.6% since Syria strike on April 7.

The first round of the French election is to be held this Sunday April 23. The latest polls conducted between April 12-14 showed a tightening race: Macron, Le Pen are both 22%, Macron and Le Pen got a lower share of the vote compared to 23% from a previous poll. The far-left candidate Jean-Luc Melenchon, has slipped to third position, with 20% of voters, which surpassing Fillion's 19%. Jean-Luc Melenchon is the only candidate among the four whose share of vote saw an increase recently. The difference of votes between the 4 candidates is less than 3% which poses more uncertainty to the election.

The US retail sales and CPI data for March released last Friday both underperformed. Retail sales (MoM) fell to -0.2%, retail sales for February was revised downward to -0.3% from 0.1%, marking the first decline since August 2016. The drop was partially caused by the recent decline in automobile and petrol sales. However, consumer electronics and clothing sectors saw a growth. Retail sales exclude autos for March (MoM) fell to 0.0%, marking the lowest growth since August 2016.

US CPI and core CPI (YoY) for March were 2.4% and 2.0% respectively, marking the lowest growth since January 2017 and November 2015. Per CME's FedWatch tool, after the release of US retail sales and CPI data for March, the probability of a rate hike in June has dropped to 50.7%.

The Bank of Japan Governor Kuroda stated on Monday April 17 that employment and wages are improving steadily, consumer spending saw a pickup. The positive economic indicators continue to strengthen JPY ahead of the upcoming BoJ's meeting on April 27. Monday USDJPY hit the lowest level of 108.12 since November 15.