Sample Category Title

Germany’s Inflation Confirmed At 0.2% In March

For the 24 hours to 23:00 GMT, the EUR rose 0.2% against the USD and closed at 1.0641.

On Thursday, data showed that Germany's final consumer price index (CPI) advanced 0.2% MoM in March, meeting market expectations and following a similar rise in the prior month.

In the US, the NAHB housing market index dropped more-than-anticipated to a level of 68.0 in April, from a nearly twelve-year high level of 71.0 in the preceding month and compared to market expectations for the index to edge down to a level of 70.0.

On Friday, data indicated that consumer prices in the US surprisingly dropped 0.3% on a monthly basis in March, dropping for the first time in thirteen months. The CPI had registered a gain of 0.1% in the prior month, while markets anticipated for a flat reading. Moreover, the nation's advance retail sales declined for a second consecutive month, after it eased 0.2% in March, in line with market expectations and following a revised drop of 0.3% in the preceding month. In contrast, the nation's business inventories advanced 0.3% in February, following a similar gain in the previous month.

On Thursday, data revealed that the US flash Reuters/Michigan consumer sentiment index unexpectedly rose to a level of 98.0 in April, as Americans remained increasingly optimistic over the nation's current economic conditions. The index had recorded a reading of 96.9 in the previous month, while market participates were expecting for a fall to a level of 96.5. Moreover, the nation's initial jobless claims unexpectedly fell to a level of 234.0K in the week ended 08 April, while investors had envisaged for an advance to a level of 245.0K and after registering a revised reading of 235.0K in the preceding month.

In the Asian session, at GMT0300, the pair is trading at 1.0651, with the EUR trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.0619, and a fall through could take it to the next support level of 1.0588. The pair is expected to find its first resistance at 1.0676, and a rise through could take it to the next resistance level of 1.0702.

With no major economic releases in the Euro-zone today, investors would look forward to a batch of economic releases in the US, consisting of housing starts, building permits, industrial production as well as manufacturing production data, all for March, scheduled to release later today.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.18% against the USD and closed at 1.2557.

On Thursday, the Bank of England, in its quarterly credit conditions survey report, disclosed that growth in corporate lending moderated in the first quarter and lenders are expected to tighten supply of unsecured consumer credit in the next three months.

In the Asian session, at GMT0300, the pair is trading at 1.2566, with the GBP trading 0.07% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.2530, and a fall through could take it to the next support level of 1.2494. The pair is expected to find its first resistance at 1.2599, and a rise through could take it to the next resistance level of 1.2632.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.79% against the JPY and closed at 109.03.

On Friday, data showed that Japan’s final industrial production climbed 3.2% MoM in February, compared to a rise of 2.0% in the preliminary print.

In the Asian session, at GMT0300, the pair is trading at 108.96, with the USD trading 0.06% lower against the JPY from yesterday’s close.

The pair is expected to find support at 108.31, and a fall through could take it to the next support level of 107.66. The pair is expected to find its first resistance at 109.41, and a rise through could take it to the next resistance level of 109.86.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD traded flat against the CHF and closed at 1.0042.

On Thursday, data indicated that Switzerland's producer and import price index climbed 0.1% MoM in March, in line with market expectations. In the previous month, the index had fallen 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.0034, with the USD trading 0.08% lower against the CHF from yesterday's close.

The pair is expected to find support at 1.0011, and a fall through could take it to the next support level of 0.9987. The pair is expected to find its first resistance at 1.0055, and a rise through could take it to the next resistance level of 1.0075.

Amid a lack of economic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Loonie Reverses Its Losses In The Asian Session, Ahead Of Canada’s Existing Home Sales Data

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CAD and closed at 1.3324.

On Thursday, data revealed that Canada's new housing price index advanced 0.4% on a monthly basis in February, more than market expectations for a rise of 0.2% and following a gain of 0.1% in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.3322, with the USD trading marginally lower against the CAD from yesterday's close.

The pair is expected to find support at 1.3277, and a fall through could take it to the next support level of 1.3232. The pair is expected to find its first resistance at 1.3350, and a rise through could take it to the next resistance level of 1.3378.

Ahead in the day, traders would keep a close watch on Canada's existing home sales data for March.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Is The EURCHF Ready For A Breakout?

Key Points:

- Narrowing wedge likely coming to an end.

- Technical bias shifting towards bullish in the near-term.

- Resulting rally could extend to around the 1.0725 level.

The EURCHF could be destined for a near-term breakout over the coming sessions and its recent decline is likely to be put on hold for a short while. Specifically, the pair is now testing the upside of a rapidly narrowing wedge and, unlike like prior challenges, this one could be the real deal. As a result, a closer look at the technical bias could be warranted as we move ahead.

As is shown on the chart below, price action over the past few weeks has been predisposed to the downside but it is also oscillating within a narrowing wedge. As a result, it is tempting to assume that we are now likely to see a repeat performance, specifically, a near-term slip that ends as the pair draws near to the downside of the structure. Nevertheless, this time, there could be some doubt cast on such a prediction as the technical bias seems to be shifting slightly.

For one, both the stochastics and the RSI readings are firmly neutral which means there is little resistance being applied by fears of moving into overbought territory. In addition to this, the MACD oscillator is creeping closer to the signal line which indicates that the recent decline is beginning to run short on momentum. By themselves, these instruments may not instantly signal that the well tested trend line is in much danger of being broken. However, there are two other technical factors that hint that this challenge could be more successful than previous ones.

Namely, the Parabolic SAR and Bollinger Bands are now signalling that a near-term breakout is actually a fairly likely prospect. Starting with the Parabolic SAR, as of last session, the indicator finally inverted its bias to bullish. Importantly, this is the first time it has been bullish whilst the EURCHF has been challenging the upside of the wedge. Moving onto the Bollinger Bands, the upper and lower bands have begun to converge on the basis line which would typically indicate that chances of a breakout are increasing somewhat.

If we do indeed see a breakout, it should extend to around the 1.0725 mark at most. This is largely a result of the long-term trend line which remains staunchly bearish but resistance will also be supplied by a number of other sources. In particular, the 100 day moving average and the 38.2% Fibonacci levels which also intersect around the 1.0725 level.

Ultimately, a lack of much news on either side of the quote should leave the pair somewhat exposed to technical influence over the coming 24 hours but it could still be impacted by headline risk. Notably, the CHF will be reacting to developments in the Syrian and North Korean dramas whilst the EUR still has Brexit and the Greek Debt crises hanging over it. Regardless, we do still expect to see the above forecasted correction take place moving forward, even if a fundamental upset could delay such a rally by a few sessions.

Crude Oil Shows Key Reversal Point

Key Points:

- Crude Oil fails to break through recent high.

- RSI Oscillator retreating from overbought levels.

- Downside targets likely to fall around the 10EMA at $52.10 and 50EMA at $51.20.

Crude Oil prices have been trending strongly higher through most of April as the commodity was buoyed by the ongoing OPEC production cuts, as well as plenty of geo-political risk. Subsequently, we have seen the West Texas Intermediate (WTI) prices leap to around the $53.74 before slipping lower to trade around its present level at $52.61/barrel. However, despite its overall bullishness, the recent pullback could just be a key reversal point for the commodity.

In particular, Wednesday’s failure to rally has been seen by many as a negative signal with price action now languishing near the recent lows. Also, the breach of the $53.00 handle has left the commodity exposed to a retracement back towards the 23.6% Fibonacci level at $52.10. This should be regarded as the abject minimum level that price action will retreat to. In extension, we are likely to see further downside action with targeted levels around the 38.2% Fibonacci level at $51.20. This key level also forms around the 50EMA which is a highly important technical factor for crude oil. Additionally, the RSI Oscillator, is also trending lower away from overbought levels, suggesting that there is plenty of room to move on the downside.

Subsequently, there are plenty of technical reasons to suggest that the highly traded commodity will continue its march lower, at least to around the $51.00 handle, before it discovers some support. However, the elephant in the room is clearly OPEC with the latest ruminations seemingly suggesting that the cartel will look to extend their latest round of production cuts through their next meeting. However, an agreement is never a sure thing with most members willing, able, and incentivised to cheat on any output caps or cuts. This may especially be the case given the heightening levels of U.S. and Canadian production in response to firmer crude prices.

Ultimately, technical analysis is suggesting that the commodity is heading in only one direction and that is clearly lower. In particular, crude’s inability to rally back above the recent high is a strong indication of its present malaise. Subsequently, the most likely scenario is a breakdown over the coming week and a retreat back towards the $51.00 handle in short order. However, keep a close watch on OPEC and any potential geo-political risk emanating from North Korea.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

EUR/USD

During the course of yesterday's sessions, we saw the pair advance. In spite of this, as the market entered into the US segment, H4 price whipsawed through April's opening level at 1.0659 and tagged in offers sitting around a nearby H4 supply zone at 1.0677-1.0665. This move was also bolstered by the fact that the US dollar (see US dollar index) tapped a H4 demand base coming in at 99.93-100.09.

Despite yesterday's action, weekly price, in our opinion, continues to suggest the unit could eventually shake hands with the 2017 yearly opening level at 1.0515/support area at 1.0333-1.0502 sometime this week. Moving down to the daily timeframe, we can see that the candles are somewhat capped between a resistance area at 1.0714-1.0683 and a demand base drawn from 1.0525-1.0576 (positioned ten pips above the aforementioned 2017 yearly opening level).

Our suggestions: Right now, we do not see much to hang our hat on at the moment. The H4 Quasimodo support at 1.0604 did initially catch our eye, as it fuses nicely with the 1.06 handle. However, it shows little connection to higher-timeframe structures which is something we generally look for in a setup. Therefore, opting to stand on the sidelines today may be the better path to take.

Data points to consider: US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

GBP/USD

Recent action shows that the GBP extended Friday's bounce from the 1.25 handle, and drove itself into the jaws of a H4 supply at 1.2596-1.2568, more specifically, February's opening level at 1.2586. For those who read Monday's report you may recall our desk highlighting the possibility of a bounce being seen from this monthly level. It warranted attention for the following reasons:

Submerged within H4 supply at 1.2596-1.2568.

Seen just below the 1.26 handle.

Positioned nearby daily resistance at 1.2582.

Located below the weekly trendline resistance extended from the high 1.2774.

Well done to any of our readers who managed to take advantage of the bounce seen from here!

Our suggestions: At the time of writing, the bears seem to have the upper hand. Before our team looks to consider shorts, however, April's opening level needs to be consumed. Should this come to fruition, an intraday short could be considered on the retest of this line, targeting 1.25 as an initial take-profit zone. To achieve the best possible risk/reward here given the distance to 1.25, we would advise drilling down to the lower-timeframe structure and looking for a sell signal (see the top of this report for ideas on how to do this).

Data points to consider: US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to engulf 1.2541 and look to trade any retest seen thereafter ([waiting for a lower-timeframe confirming signal is advised] stop loss: dependent on where one confirms this level).

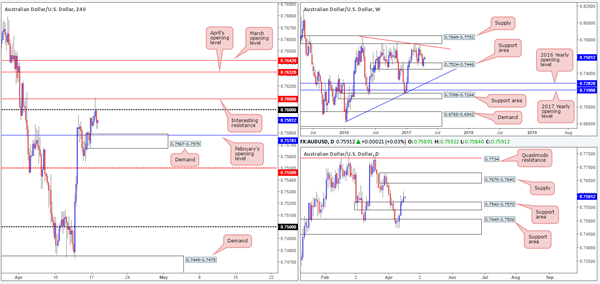

AUD/USD

Chinese data offered the pair support early on in the day yesterday, forcing the commodity currency to whipsaw through the 0.76 handle and touch base with H4 resistance at 0.7609, which, as you can see, held firm. The downside move seen from here was strengthened by the US dollar (see US dollar index) tapping a H4 demand base at 99.93-100.09 and lower gold prices. While H4 bears now look poised to challenge February's opening level at 0.7578/H4 demand at 0.7567-0.7579, the bigger picture shows the bulls to be in the driver's seat.

During the course of last week's segment, weekly bulls staged a modest rebound from the support area at 0.7524-0.7446. This zone can be seen offering support and resistance as far back as mid-2016. Should the currency extend last week's bullish rotation, the next upside hurdle can be seen at a trendline resistance taken from the high 0.7835, followed closely by supply at 0.7849-0.7752. Zooming in and looking at the daily picture reveals that price recently engulfed the resistance area penciled in at 0.7540-0.7570, potentially opening up the path north for the candles to challenge supply at 0.7679-0.7640.

Our suggestions: Given that the current H4 demand is positioned on top of the daily support area at 0.7540-0.7570, and holds a monthly opening level within, there's a reasonable possibility that the bulls could defend this barrier today. Risk/reward considerations, however, would argue against taking a long from here, due to how close 0.76 is. While we would agree that the trade is tight, we believe there is still room. Providing that the bears drive into the demand zone, touching the 0.7570 neighborhood, and a lower-timeframe confirming buy signal is seen (see the top of report for ideas on how to find this), the risk/reward will very likely be at least 1:1 up to 0.76. This essentially gives traders the option to either take partial profit or move stops to breakeven in the hope of more pips as suggested by the higher timeframes.

Data points to consider: Aussie monetary policy meeting minutes at 2.30am. US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: 0.7567-0.7579 ([waiting for additional lower-timeframe confirming price action is advised] stop loss: dependent on where one confirms this area).

- Sells: Flat (stop loss: N/A).

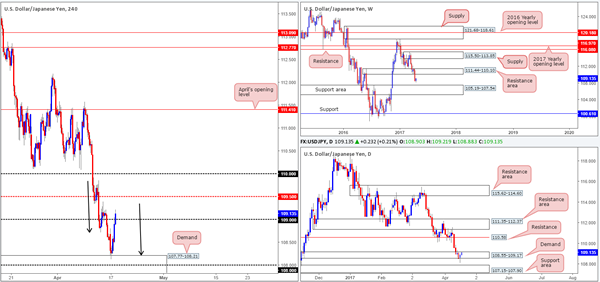

USD/JPY

For those who read Monday's report you may remember our team mentioning to keep an eye on the H4 demand at 107.77-108.21 for potential long opportunities. The reasons for selecting this zone were as follows:

H4 AB=CD bullish convergence taken from the high 109.86 (see black arrows).

108 psychological handle.

Bolstered by the daily support area at 107.15-107.90, which itself is supported by a weekly support area at 105.19-107.54.

Well done to any of our readers who managed to enter long from here. Price has rallied beautifully so far.

With H4 price now seen peeking its head above the 109 barrier, and daily price recently chalking up a nice-looking bullish tail within the walls of demand at 108.55-109.17, is there room for additional longs?

Our suggestions: Given the H4 demand is reinforced by a weekly and daily support area, we feel the move from here has potential. As such, providing that H4 price retests 109 and holds firm, a buy trade, targeting the H4 mid-level resistance at 109.50 as an initial take-profit target, is certainly something to consider.

Data points to consider: US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: 109 region ([watch for H4 price to retest this number and hold] stop loss: ideally beyond the rejection candle's tail).

- Sells: Flat (stop loss: N/A).

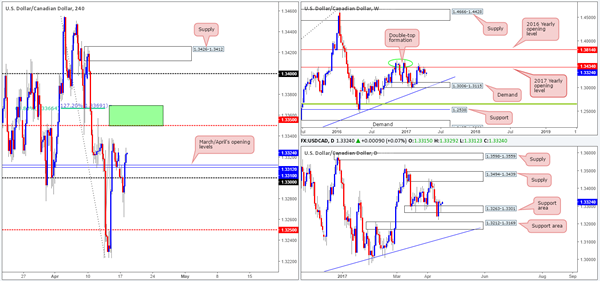

USD/CAD

Weekly price remains in a rather negative climate, as the candles have spent the best part of a month and a half teasing the underside of the 2017 yearly opening level at 1.3434. Reinforcing this line is a well-defined double-top formation seen around the 1.3588 neighborhood (green circle). On the other side of the coin, nonetheless, daily flow is seen holding firm around a support area fixed at 1.3263-1.3301. Assuming that the bulls continue to bolster this market, the next upside hurdle in view is supply printed at 1.3494-1.3439.

In recent hours, H4 price crossed back above March/April's opening levels at 1.3310/1.3312. Although there's some wood seen to chop through around the 1.3320/1.3340ish neighborhood, the next line of interest to the upside can be seen at the H4 mid-level resistance drawn from 1.3350.

Our suggestions: As you can see on the H4 chart, we've drawn a green box to represent a potential reversal zone. The lower edge is denoted by the said H4 mid-level resistance, while the top edge is formed from a 61.8% Fib resistance at 1.3366 (taken from the high 1.3455) and a Fib extension at 1.3369 drawn from the low 1.3223.

Of course, selling from here would mean going against potential daily buyers. However, let's not forget that weekly bears show lower prices could be on the cards! To be safe though, we would highly recommend waiting for a reasonably sized H4 bearish candle to form before committing to any shorts.

Data points to consider: US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1.3369/1.3350 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

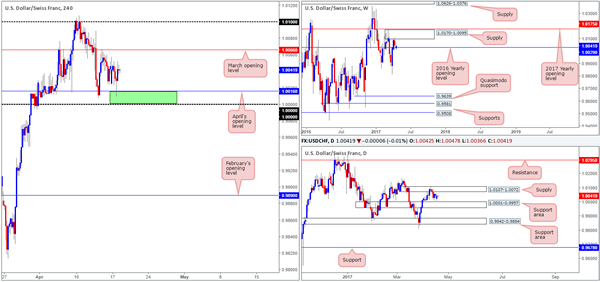

USD/CHF

Leaving parity (1.0000) unchallenged, H4 price, once again, found a pocket of bids around April's opening line at 1.0016 yesterday. Through the simple lens of a technical trader, this has placed the candles in somewhat of a ranging environment amid the said April opening line and March's opening level at 1.0066.

Up on the weekly chart, we can see that the buyers and sellers are currently battling for position around the 2016 yearly opening level at 1.0029. On the daily chart, price is also seen capped between a supply base drawn from 1.0107-1.0072 and a support area logged at 1.0001-0.9957.

Our suggestions: As far as we can see, there's equal opportunity trade this pair both long and short today. The upper edge of the current H4 range is positioned just a few pips beneath the aforementioned daily supply, which itself is supported by a weekly supply area at 1.0170-1.0095.

The lower edge of the current H4 range is located nearby parity (see green box), which represents the top edge of the daily support area mentioned above at 1.0001-0.9957, and also happens to also be located nearby the above said 2016 yearly opening level.

Therefore, we'll be keeping a close eye on the H4 consolidation today. Should price shake hands with either extreme, we'll drill down to the lower-timeframe action (see the top of this report) in an attempt to find potential setups to trade this range to the opposite end.

Data points to consider: US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: 1.0000/1.0016 ([waiting for additional lower-timeframe confirming price action is advised] stop loss: dependent on where one confirms this area).

- Sells: 1.0066 region ([waiting for additional lower-timeframe confirming price action is advised] stop loss: dependent on where one confirms this area).

DOW 30

US equities added close to 200 points in light trading yesterday, bringing H4 price up to within shouting distance of April's opening level at 20669. Also accomplished during Monday's advance was daily price whipsawing back into the daily range fixed between a resistance area at 20714-20821 and a demand base coming in at 20527-20626. What's also notable from a technical perspective is that the daily candles formed a nice-looking bullish engulfing formation.

According to the daily timeframe, we may see H4 price breach April's opening line today to connect with the resistance area seen at 20754-20717. This is simply due to this resistance base being lodged within the said daily resistance area.

Our suggestions: In view of how responsive the current H4 resistance area has been over the past month, taking a short from here is certainly an option. However, the other key thing to note here is that weekly price seems to be basing around 20416 after the index pulled back from record highs of 21170. This means we could eventually see price strike fresh highs in the near future, effectively continuing this market's trend which began back in early 2009. As a result of this, we would only consider a sell from the noted H4 resistance area on the condition that we are able to pin down lower-timeframe confirming price action (see the top of this report).

Data points to consider: US housing figures at 1.30pm, US Industrial production and Capacity utilization rate at 2.15pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 20754-20717 ([waiting for additional lower-timeframe confirming price action is advised] stop loss: dependent on where one confirms this area).

GOLD

Kicking this morning's report off from the weekly chart, we can see that the bears are beginning to make an appearance within the area formed from the Fibonacci extensions 161.8/127.2% at 1313.7/1285.2 taken from the low 1188.1 (green zone). In the event that the bears remain energetic, the support at 1263.7 could see a retest soon. Of particular interest on the daily timeframe is that the said weekly support is seen lodged within a daily support area marked at 1265.2-1252.1.

With H4 price seen topping at a high of 1295.3 in early trading on Monday, the unit has been grinding lower since. According to our technical markings on the H4 chart, there's little support standing in the way until we reach demand penciled in at 1271.8-1275.2, followed closely by support at 1270.7.

Our suggestions: With both weekly and daily structure suggesting that price could stretch lower, short setups are preferred. The best we've been able to come up with is a possible sell at the 61.8% Fib retracement at 1289.9 that's housed within a minor H4 supply at 1292.5-1289.2.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 1292.5-1289.2 ([waiting for a reasonably sized H4 bear candle to form before pulling the trigger is advised] stop loss: ideally beyond the candle's wick).

RBA’s April Minutes Revealed Concerns Over Labor And Housing Markets

RBA minutes for the April meeting came in less upbeat than the March one, underpinning concerns over developments in Australia's labor and housing market. Policymakers concluded by noting that "developments in the labour and housing markets warranted careful monitoring over coming months". Note, however, that the meeting was held ahead of the release of the March employment report which showed that full-time payrolls rose the most in nearly 30 years. Aussie slumped after the minutes to a 3-day low 0.552.

Softer conditions in the labour market

Policymakers acknowledged that low interest rates had continued to support moderate growth in Australia at the beginning of 2017. However, they cautioned over the weaker than expected indicators of household consumption, attributing them to the "softer conditions in the labour market". The members were concerned over the employment market, noting that positive forward-looking indicators of labour demand had failed to lead to an improvement in labour market conditions.

We have to point out that this judgment was made before the release of the March employment report which did depict encouraging developments in the job market. Employment rose +60.9K from February, beating expectations of a +20K increase. Of which full-time jobs jumped +74.5K, the biggest increase since December 1987 while part-time jobs dropped -13.6K.

The unemployment rate steadied at 5.9% with participation rate adding +0.2 percentage point to 64.8%.

Increasing concern on housing market

Another big concern haunting the members is the housing market. The minutes suggested that “growth in housing credit continued to outpace growth in household incomes, suggesting that the risks associated with the housing market and household balance sheets had been rising”. Policymakers were apparently concerned that soft income growth has led to an increase in household debt ratios, despite modest slowdown in household credit growth. The minutes added that the current “developments needed to be kept under review and depending on how the system responds to the various measures” and “the Council of Financial Regulators would consider further measures if needed”.

Less upbeat than March

Policymakers refrained from delivering an upbeat forward guidance as it was in March. In the March minutes, RBA suggested that "year-ended growth was expected to pick up gradually to be above its potential rate over the forecast period". However, it only noted this month that "Australian economy had continued to grow moderately at the beginning of 2017, supported by the low level of interest rates". This apparently sounded less confident over the growth outlook. In the concluding statement, it was added that that "developments in the labour and housing markets warranted careful monitoring over coming months".

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 03 May 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 3 May 2016

• Trend bias: Sideways

EUR/USD – 1.0645

As the single currency found support at 1.0570 and recovered last week, suggesting consolidation above this level would be seen and another bounce to 1.0678 resistance cannot be ruled out, however, still reckon upside would be limited to 1.0700 and bring another decline, below said support at 1.0570 would signal the fall from 1.0906 top is still in progress and extend fall to 1.0525 support but a daily close below key support at 1.0493 is needed to confirm early erratic rise from 1.0340 low (this year’s low) has ended at 1.0906, bring further fall to 1.0440-50 and possibly towards 1.0390-00, having said that, said support at 1.0340 should remain intact.

On the upside, although consolidation is seen with initial upside bias, reckon 1.0700 would limit upside and bring another decline. A daily close above the Kijun-Sen (now at 1.0738) would abort and suggest first leg of decline from 1.0906 has ended instead, risk a stronger rebound to 1.0765-70 but upside should be limited to 1.0800 and price should falter well below 1.0870-75, bring another selloff later this month.

Recommendation: Hold short entered at 1.0670 for 1.0500 with stop above 1.0770.

On the weekly chart, although the single currency found support at 1.0570 and recovered, as the selloff from 1.0906 suggests top is possibly formed there, reckon upside would be limited to the Tenkan-Sen (now at 1.0700) and bring another decline, below said support at 1.0570 would extend weakness to 1.0525. Looking ahead, only a break of indicated pivotal support at 1.0493 would signal the rebound from 1.0340 has ended at 1.0906, bring further fall to key support at 1.0454, a sustained breach below this level would provide confirmation, then further fall to 1.0390-00 and later retest of this January low would follow.

On the upside, expect recovery to be limited to the Tenkan-Sen (now at 1.0700) and brig another decline. Above 1.0730-40 would bring test of 1.0780, however, reckon upside would be limited to 1.0825-30 and price should falter well below said resistance at 1.0906, bring another decline later. Only a break of 1.0906 would revive near term bullish view for the erratic rise from 1.0340 low to bring retracement of recent decline to 1.0930-35 (61.8% Fibonacci retracement of 1.1300-1.0340) and possibly 1.1000, however, reckon upside would be limited to 1.1050-60 and price should falter below 1.1100-10, risk from there is seen for a retreat to take place later.