Sample Category Title

GOLD: Biased To Upside In The Short Term

GOLD - The commodity strengthened further the past week leaving risk of more gains on the cards on the cards. On the downside, support comes in at the 1,280.00 level where a break will turn attention to the 1,270.00 level. Further down, a cut through here will open the door for a move lower towards the 1,260.00 level. Below here if seen could trigger further downside pressure targeting the 1,250.00 level. Conversely, resistance resides at the 1,290.00 level where a break will aim at the 1,300.00 level. A turn above there will expose the 1,310.00 level. Further out, resistance stands at the 1,320.00 level. Its weekly RSI is bullish and pointing higher suggesting further up[side pressure. All in all, GOLD looks to strengthen further.

Stocks, Dollar and Yields under Geopolitical and Economic Pressure

Monday April 17: Five things the markets are talking about

Global equities and the 'mighty' dollar have again dipped overnight while U.S Treasury yields have fallen to new five-month lows after soft U.S data on Friday hurts investor sentiment already in distress by worries over North Korea and upcoming French elections.

Note: U.S. retail sales dropped more than expected in March (+0.0% vs. +0.2%) while annual core inflation slowed to +2.0%, the smallest advance since November 2015, from +2.2% in Feb.

A raft of Chinese economic data (see below) beat market expectations, but did not produce a notable market reactions, as investors had been already optimistic following a recent string of positive China numbers.

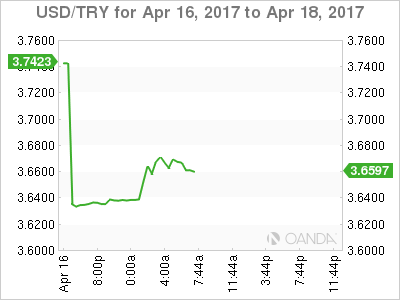

In Turkey, President Erdogan snatched a victory in a referendum Sunday to grant him sweeping powers in the biggest overhaul of modern Turkish politics.

Note: Markets in Australia, New Zealand and Hong Kong, as well as most European exchanges, are closed for Easter Monday.

1. Global equities under pressure

Stock markets across Asia ended mostly lower overnight, as China's securities regulator urged tighter supervision of listed companies, while geopolitical tensions in Korea continued to discourage investors from buying.

Japan's Nikkei Stock Average opened lower, but later recouped the declines to end up +0.1%, snapping a four-session losing streak - the yen (¥108.76) spiked to new yearly highs (¥108.13).

In China, investor market sentiment has worsened over an escalating regulatory crackdown on stock manipulation, despite stronger-than-expected economic data for the Q1. The Shanghai Composite Index ended down -0.7%, while the Shenzhen Composite Index lost -1.4%.

Elsewhere, Singapore's Straits Times Index lost -0.9%, while Taiwan's Taiex ended down -0.2%.

In Turkey, the Borsa Istanbul 100 Index climbed +0.6% - the highest level in more than two-years after President Erodgan's referendum victory yesterday (see below).

In Europe, markets remain closed due to Easter Monday holiday.

U.S stocks are set to open in the 'red' (-0.1%).

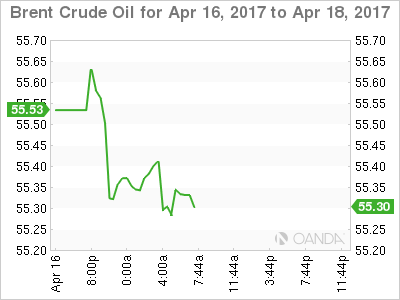

2. Oil falls after failed North Korean missile test, U.S rig count gains

Crude oil prices are again under pressure overnight in quiet trading after the Easter break on signs that the U.S continues to add output, undermining OPEC efforts to support prices, and as the market digest North Korea's failed missile launch yesterday.

Ahead of the U.S open, Brent crude futures are down -56c at +$55.33, while West Texas Intermediate (WTI) crude futures are down -51c at +$52.67 a barrel.

Note: Both benchmarks last week rose for a third consecutive week, with Brent adding +1.2% over the four days (Good Friday holiday) while WTI was up +1.8%.

Last Thursday's Baker Hughes (energy services) report indicated that drillers added +11 oil rigs in the week to April 13, bringing the count up to 683, highest in about two-years.

Note: The latest EIA report shows that U.S crude oil production has climbed to +9.24m barrels per day (bpd), making it the world's third-largest producer after Russia and Saudi Arabia.

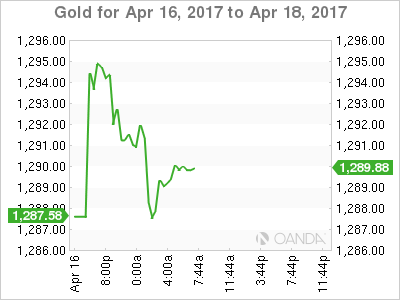

Gold prices hit a five-month high overnight (+$1,295.42 an ounce) as the dollar weakened with investors taking refuge in safe-haven assets in the wake of rising geopolitical tensions over North Korea.

The 'yellow' metal last week rose +2.5%, posting its biggest weekly gain in 10-months.

3. Global yield curves flatten

Last Friday's disappointing U.S data (retails sales and CPI) has helped to drive down the U.S 10-year Treasury yield to +2.20%, its lowest level since mid-Nov.

In March, U.S 10's were trading atop of +2.6% on expectations of a Trump stimulus package. However, with Trump expected to struggle to push any tax cuts and fiscal spending programs through Congress has supported the markets unwinding of the "Trump" trade.

Current Fed fund futures for June are now pricing in less than a +50% chance of a rate hike in its June 13-14 meeting for the first time in about a month.

Elsewhere, geopolitical and French Presidential election risks have seen the yield on 10-year Bunds fall over -33 bps from its mid-March peak of +0.51% to +0.18%.

The gap between French and German 10-year borrowing costs, an indicator of concerns over the election, is at +71.4 bps, +4 points off one-month highs hit earlier last week.

4. Dollar under geopolitical pressure

The Turkish Lira (TRY) has rallied over +2.4% outright in the wake of this weekend's referendum to expand the executive powers of President Erdogan.

While the "Yes" vote was deemed victorious, the margin of victory at 51.3% vs. 48.7% opposed was well below the 55% mandate predicted by Erdogan and is expected to be challenged by the opposition.

Note: Under upcoming constitutional changes, the winner of next election in 2019 will "gain full control of the government, ending the current parliamentary system, which treated office of the president as a role without full executive authority."

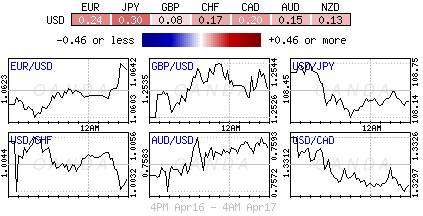

The 'mighty' USD is trading a tad softer across the board after last week's release of March CPI and retail sales data both underwhelmed. Fixed income dealers are paring back the probability of another Fed rate hike in June.

The EUR is trading +0.2% higher at €1.0630 in quiet trading with most European markets remaining closed for Easter Monday holiday. USD/JPY is trading softer, down -0.3% at ¥108.32. Expect geopolitical worries to continue to support the yen's strength.

5. China data beats expectations

Over the weekend, China economic data offered some positive surprises - GDP, industrial output, and retail sales for Q1 all topped consensus to hit multi-month rates of growth.

Note: The world's second-biggest economy accounted for about one-third of global growth last year and, given the strong Q1, is on track to contribute at least as much this year.

Digging deeper, Q1 GDP y/y rallied to a six-quarter high of +6.9%. Consumption accounted for +77.2% of that growth, up from +64.6% in 2016. Fixed asset investment rose over +10% as property investment value rose +9%, sales value rose +25% and construction up +11%.

Industrial output growth was similarly impressive, rising at the fastest pace in three-years. Power generation was up +7%, while coal and steel output were both up +2% despite the recent production curbs. While March retail sales y/y was +10.9% vs. +9.7%e (3-month high).

GBP/JPY 1H Chart: Falling Wedge

Comment: GBP/JPY has set a strong downward trend-line to guide it away from 147.45, the December 2016 high. The pair has additionally formed a falling wedge on the hourly time-frame, meaning that the trend-line might be luring it closer again. The cross is trading mid-pattern with risks skewed to the upside until 136.16, the upper boundary of the pattern. A set of levels will provide resistance outside of the pattern causing the motion to become flatter and potentially lead to a retracement before a more prominent rally. Immediate support lies at 135.63 and will come into play if the pair makes another wave before breaking the pattern.

EUR/GBP 1H Chart: Falling Wedge

Comment: After an unsuccessful attempt at forming a head and shoulders pattern at 0.9125, EUR/GBP entered a correction phase with distinct waves on the weekly and daily time-frames. The recent developments, however, show some bullish potential again on the hourly chart, suggesting that another solid wave might be coming up. The pair is currently on the edge of the pattern at 0.8478 and might possess enough momentum to push through the area if tested consistently. The break would open the way for tests of 0.8481 and most likely give in to the area with a retracement before more ambitious movements emerge.

Gold Analysis: Reaches 1,295 Mark

"Gold will likely retain a measure of strength heading into the French elections in about one week's time, while ongoing tensions in North Korea should also keep the markets rather nervous."

- Edward Meir, INTL FCStone (based on investing.com)

Pair's Outlook

As it was forecasted, the yellow metal began Monday's trading session higher and surged above the 1,295 level. However, afterwards profit taking occurred and the bullion began a retreat from the achieved heights. Meanwhile, it is still expected that the commodity price will soon reach the 1,300 level, as the only resistance level up to that mark was the upper Bollinger band, which fluctuated near the 1,291 level. At the 1,300 mark the yellow metal's price is most likely set to change its direction, as a strong resistance cluster surrounds that level.

Traders' Sentiment

Traders remain bearish, as 54% of open positions are short. Meanwhile, 58% of pending commands are to buy the metal.

USD/JPY Analysis: Sets Eye on 108.00

"It is unclear whether the situation over North Korea will escalate into military action, but uncertainty is increasing and the dollar continues to edge lower. The dollar also looks shaky technically, after slipping below the 200-day moving average of 108.80 yen."

- Mizuho Securities (based on Reuters)

Pair's Outlook

The US Dollar weakened against the Japanese Yen again on Friday, amid soft US fundamentals weighing on the Greenback. As a result, the pair failed to rebound from the descending channel's support line, breaching the tough demand area around 108.90, which resulted in more weakness earlier today. The Buck is now expected to approach the 108.00 level, where support could be sufficient for the bullish momentum to be regained. A failure to recover this weak might lead to a slump towards July-September 2016 lows, namely closer to the 100.00 handle. However, longer-term technical studies point to a potential recovery by April's end.

Traders' Sentiment

There are 72% of traders holding long positions today, whereas 57% of all pending orders are to acquire the US Dollar.

GBP/USD Analysis: Risks Breaking the Down-Trend

"We believe there is scope for GBP/USD to benefit from a further softening of the US dollar, most likely in response to a further scaling back in US stimulus prospects. As such, we forecast the currency pair to move towards 1.30 by end-2017."

- Lloyds Bank (based on FXStreet)

Pair's Outlook

Poor US fundamentals on Friday allowed the British Pound to erase most of Thursday's losses against the US Dollar, causing the six-month down-trend to be put to the test again today. From the technical perspective the GBP/USD currency pair should now undergo another decline, with the weekly pivot point and the 20-day SMA circa 1.2490 limiting the losses, assuming the 1.25 major level is breached. However, technical indicators keep giving bullish signals in the daily timeframe, suggesting the trend-line might be pierced soon. A breach would not imply a complete trend reversal, as the 200-day SMA near 1.2930 is required to be overcome for that to occur.

Traders' Sentiment

Bulls barely remain in control, as 54% of all open positions are long. At the same time, 51% of all pending orders are to sell the Sterling.

EUR/USD Analysis: Faces resistance on Monday

"Trading flows are quite modest after European trading centers shut down for the long weekend."

- Alexandria Arnold and Dennis Pettit, Bloomberg

Pair's Outlook

On Monday morning the common European currency began the day against the US Dollar by facing a combined resistance cluster of the weekly PP at 1.0621 and the 100-day SMA at 1.0627. During the early hours of the day's trading the currency pair already bounced off the resistance once and went in for another try. If the resistance levels are broken, the pair would surge up to the 23.60% Fibonacci retracement level, which is located at the 1.0639 level. On the other hand, if a failure occurs, the exchange rate might retreat to the long term trend line, which on Monday was located at 1.0585.

Traders' Sentiment

SWFX traders remain neutral bullish, as 52% of open positions are long. Meanwhile, 55% of trader set up orders are to sell the Euro.

Geopolitical Worries Over the Korean Peninsula also Contributed to a Firmer Yen

Notes/Observations

- China economic data offered some positive surprises as Annual Q1 GDP pace, Mar Retail Sales and Industrial Production all beat expectations

- Situation on the Korean peninsula remained tense even though there was no activity at the nuclear test site over the weekend; North Korea said to have failed in a ballistic missile launch early on Sunday

- Softer US CPI and Retail Sales data has market participants rethink the probability of another Fed rate hike in June

Overnight:

Asia:

- China Q1 GDP YoY: 6.9% v 6.8%e (fastest growth since the third quarter of 2015)

- China Mar Industrial ProductionYoY: 7.6% v 6.3%e (highest since Dec 2014)

- China Mar Retail Sales YoY: 10.9% v 9.7%e (3-month high)

- (JP) Japan PM Abe: Need to pressure North Korea for a sincere dialogue; Working for China to play a larger role in North Korea

- US carrier USS Vinson to reach South Korea east coast on Apr 25th

- (JP) Japan to seeking to revive Trans-Pacific Partnership (TPP) without the US

Europe:

- Turkey passed its referendum on changing the constitution to replace its parliamentary system with the executive presidency with 51.5% v 48.7%; opposition to challenge result

- EU's Piri: Will suspend EU accession talks with Turkey if referendum package not changed

- France presidential candidate Mélenchon (far left, communist) is rapidly rising in the polls

Americas:

- US Mar CPI (released Friday) saw its 1st MoM negative reading since Feb 2016 and by its largest amount since Jan 2010

- US Mar Advance Retail Sales (released Friday) registered its 2nd straight decline (M/M: -0.2% v -0.2%e

Energy:

- (US) Weekly Baker Hughes US Rig Count: 847 v 839 w/w (+1%)(13th straight weekly rise)

Economic Data

- (IN) India Mar Wholesale Prices (WPI) Y/Y: 5.7% v 6.0%e

- (TR) Turkey Jan Unemployment Rate: 13.0% v 13.0%e (highest level since Feb 2010)

- (TR) Turkey Mar Central Gov't Budget Balance (TRY): -19.5B v -6.8B prior

**Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Equities**

- European markets closed for Easter Monday holiday

Speakers

- Turkey Dep PM Simsek reiterated view that double digit inflation is unacceptable and that it will fall to single digits

- Various global leaders react to Turkey's "Yes' outcome for its Constitutional Referendum

- German Chancellor Merkel called for respectful dialogue with Turkey

- BOJ Gov Kuroda reiterated that ist needed to continue with its easy monetary policy because consumer prices were still distant from its 2 percent inflation target. Domestic economy had continued its moderate recovery trend; exports and production are recovering

- BOJ Dep Gov Nakaso: BOJ should explain exit strategy as they near 2% inflation target. Bank was naturally holding internal discussions on its exit strategy from monetary easing, including the methods and impact on the bank's profitability.

- South Korea acting President Hwang stated that it had agreed with US to tighten global network of pressure on North Korea - comments alongside US VP Pence

- US VP Pence stated US was 100% commitment to South Korea and would meet any attack

- Saudi Oil Min Al-Falih noted that it aimed to double gas output by 2030 and planned to produce energy from nuclear sources

Currencies

- The USD was on soft footing after Friday's release of Mar CPI and retail sales data underwhelmed and had participants rethink the probability of another Fed rate hike in June.

- EUR/USD was higher by 0.2% at 1.0630 area in quiet trading with European markets closed for Easter Monday holiday.

- USD/JPY was softer by 0.3% and hovered near 5-month lows. Geopolitical worries over the Korean Peninsula also contributed to a firmer yen on safe-haven flows.

Looking Ahead

- 07:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 07:00 (BR) Brazil Apr FGV Inflation IGP-10 M/M: -0.6%e v 0.1% prior

- 07:00 (BR) Brazil Central Bank (BCB) Apr COPOM Minutes

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 07:30 (BR) Brazil Feb Economic Activity Index (Monthly GDP) M/M: +0.5%e v -0.3% prior; Y/Y: -2.4%e v -0.8% prior

- 07:30 (TR) Turkey TCMB Turkey Survey of Expectations

- 08:30 (US) Apr Empire Manufacturing: 15.0e v 16.4 prior

- 10:00 (US) Apr NAHB Housing Market Index: 70e v 71 prior

- 11:30 (US) Treasury to sell 3-Month and 6-month Bills

- 15:00 (CO) Colombia Feb Industrial Production Y/Y: -1.3%e v -0.2% prior

- 15:00 (CO) Colombia Feb Retail Sales Y/Y: -1.6%e v -2.2% prior

- 16:00 (US) Feb Total Net TIC Flows: No est v $110.4B prior; Net Long-term TIC Flows: No est v $6.3B prior

- 16:00 (US) Weekly Crop Progress Report

Technical Outlook: GBPUSD Trading Within Narrow Range on Low Volumes

Cable is trading within narrow range on low volumes in early Monday, as Europe is closed for holiday, but remains positive above 1.2500 handle, where the pair is attempting to form a higher base.

Last week's strong recovery rally from 1.2364 that peaked at 1.2572, looks for final push towards targets at 1.2613 (27 Mar high) and 1.2623 (200SMA), supported by bullish daily studies which are gaining fresh momentum.

Bullishly aligned near-term technicals also support scenario, with 1.2500 support zone (also Fibo 38.2% of 1.2363/1.2572 rally) required to hold.

Otherwise, risk of deeper correction could be expected on loss 1.2500 handle that would open next pivotal support at 1.2468 (daily Tenkan-sen) and trigger further easing on break.

Res: 1.2547; 1.2572; 1.2594; 1.2613

Sup: 1.2521; 1.2500; 1.2468; 1.2443