Sample Category Title

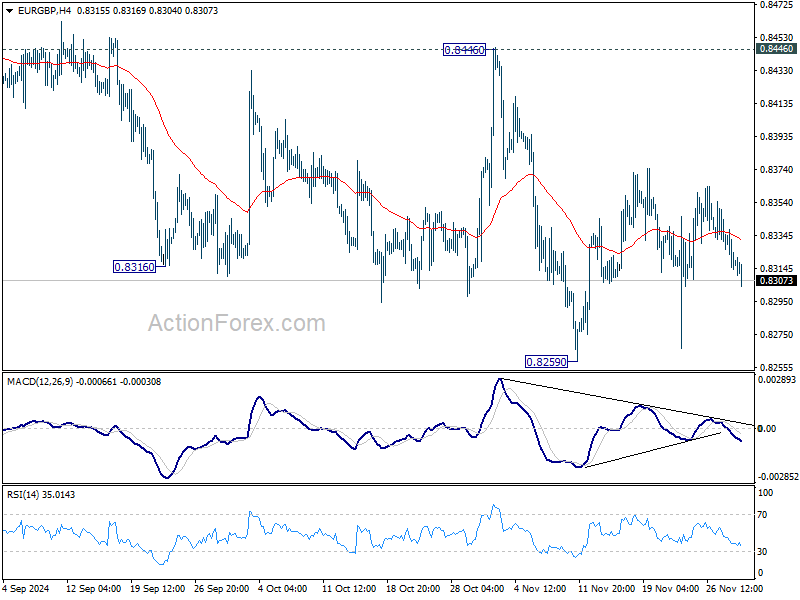

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8310; (P) 0.8324; (R1) 0.8334; More...

Outlook in EUR/GBP remains unchanged as range trading continues. Intraday bias stays neutral and further decline is expected with 0.8446 resistance intact. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

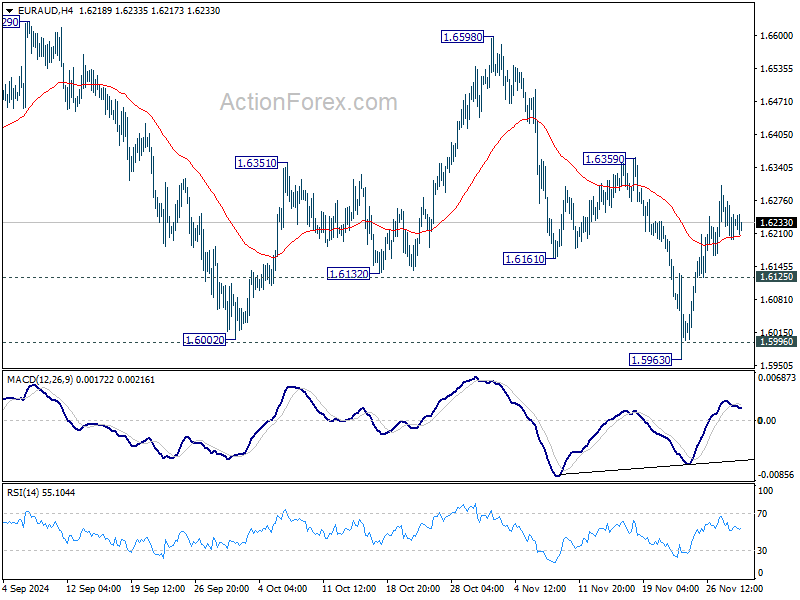

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6198; (P) 1.6241; (R1) 1.6282; More...

Intraday bias in EUR/AUD remains neutral for the moment, and outlook is unchanged. . On the upside, firm break of 1.6359 resistance will be the first sign of bullish reversal and target 1.6598 resistance for confirmation. On the downside, though, below 1.6125 minor support will bring retest of 1.5963 low.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

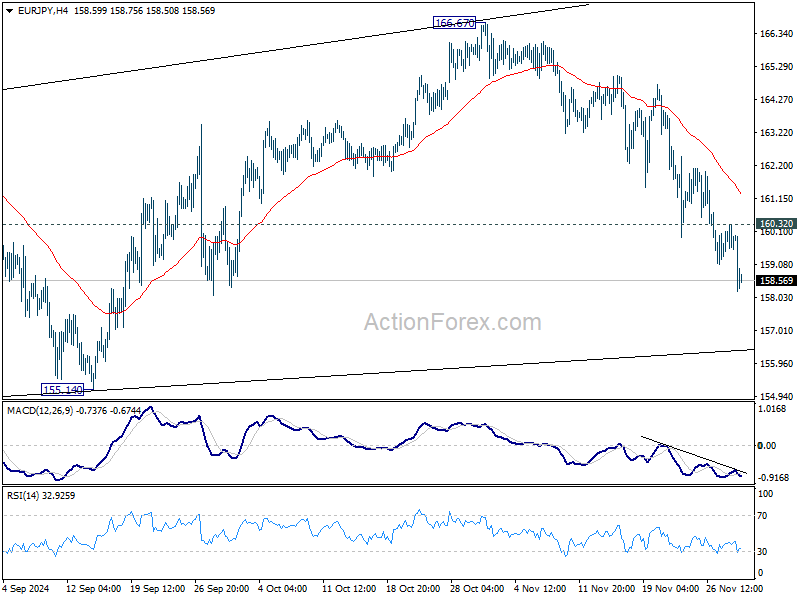

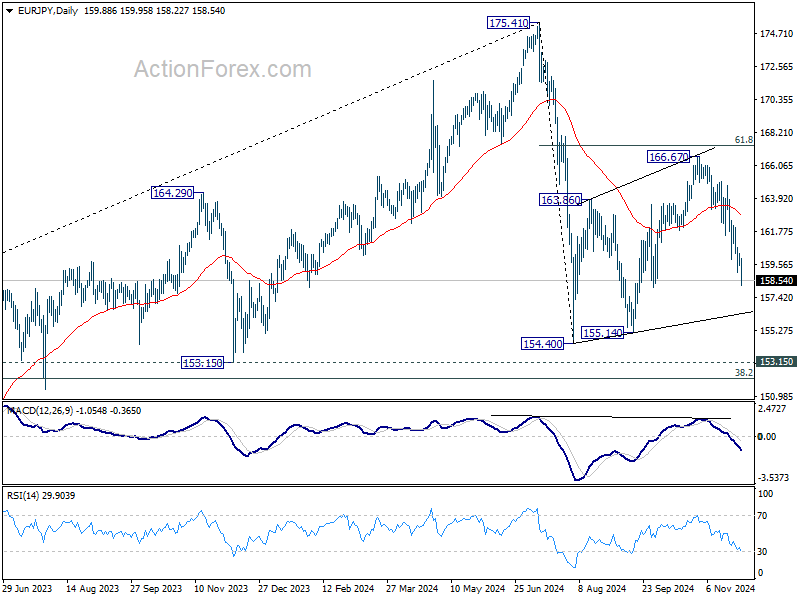

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.49; (P) 159.92; (R1) 160.36; More....

EUR/JPY's fall from 166.67 is in progress today and intraday bias stays on the downside. As noted before, corrective rebound from 154.40 could have completed with three waves up to 166.67. Deeper decline would be seen to 155.14 support next. On the upside, above 160.32 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 55 D EMA (now at 162.78) holds, in case of recovery.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

USD/JPY Tips a Toe Below 150.00 Euro CPI in Focus

The chip makers around the world felt the relief of a rumour suggesting that the sales curb to China could be less severe than previously expected. But the news didn’t necessarily translated in a strong rally. ASML - Europe’s biggest chip equipment maker that predicted a 30% fall to its Chinese revenue next year - closed 0.22% lower yesterday, while Tokyo Electron – which was up by more than 6% yesterday - couldn’t extend gains at today’s session.

With US markets paused for the Thanksgiving break, France was at the heart of the attention yesterday. The political drama, there, only got worst as Michel Barnier gave concessions to Marine Le Pen – who only asked more of them. Barnier dropped plans to increase taxes on electricity, but Le Pen’s party also wants him to drop the plans to reduce drug reimbursement, help small and medium companies compete better and index pensions on inflation starting from January 1st. The demands are nice - and they have the merit to please the French voters who, as everyone else, are dealing with inflation and cost-of-living crisis - but Le Pen’s demands cost money. And the growing French deficit doesn’t allow the French government to spend that money, please or not. The country’s debt-to-GDP stands near 5.5% today, well above the EU’s 3% target. Pushing for spending the money that you don’t have doesn’t always bode well with investors – except if you’re named after the US. Remember, Liz Truss wanted to offer the Brits significant tax cuts two years ago, and all she got was a mini financial crisis. This is what we sense from the market reaction to Le Pen’s threats that she would vote Barnier’s government down if he doesn’t give Le Pen what she wants. The French 10-year yield eased while CAC 40 was in a better mood. But the political uncertainties in France will certainly keep volatility high across French-denominated assets into the year end.

For the euro, we don’t yet see a major impact of French political shenanigans, but the French touch is not necessarily a positive one. The EURUSD swung between gains and losses yesterday, caught between mixed inflation data from Spain and Germany. Inflation in Spain ticked higher – from 1.8% to 2.4% in November, while price pressures in Germany came in softer-than-expected thanks to softer food prices. This divergence in the bloc's largest economies left traders uncertain about the European Central Bank’s (ECB) next moves. Dues this morning, the EZ aggregate inflation data is expected to print an uptick in price pressures. A softer-than-expected read will certainly keep the ECB doves in charge of the market and cap the euro appetite limited into the 1.06 psychological level, while a stronger-than-expected number should encourage the euro bulls to push for a further recovery. But in both cases, the EURUSD will remain in a bearish trend below 1.0672 – the major 38.2% Fibonacci retracement on September to November selloff.

Speaking of inflation, inflation in Tokyo came in stronger than expected in November, industrial production advanced 3%, almost the double of expectations but came in lower than expected, while retail sales grew sensibly softer than expected. But traders focuses on Tokyo inflation that backed the growing expectation that the Bank of Japan (BoJ) would hike rates in the December meeting. As such, the rise of the hawkish BoJ expectations shortly pushed the USDJPY below the 150 mark. I believe that a sustainable move below this level is possible, if the BoJ goes ahead and hikes rates in its December 18-19 meeting.

In energy, there is hesitation about what to do at the current levels. The latest news suggests that OPEC+ will delay its decision time from Sunday to December 5th. It appears that the cartel members need more time to discuss about what to do about their plans to restore production. It is clear that extending production cuts deep into next year is the only option to prevent boosting the supply gut in global markets – and keep the downside in prices limited at a time of easing geopolitical tensions in the Middle East.

Euro Area Inflation Out Today

In focus today

In the euro area, we will get the full euro area inflation print for November, after the local prints yesterday. In the light of yesterday's local prints, we expect euro area inflation to come in at 2.2%, a bit lower than the 2.3% indicated beforehand. German CPI inflation increased less than expected to 2.2% y/y (cons: 2.3% y/y) in November from 2.0% in October. Spanish inflation rose to 2.4% y/y in November from 1.8% y/y in October as expected. Core CPI inflation rose less than expected to 2.4% y/y (consensus: 2.6%) from 2.5% y/y in October.

In Sweden, we receive data for Q3 GDP. Yesterday's NIER confidence data indicated an improvement in economic sentiment, hinting that the October decline in the NIER survey might have been an anomaly. The NIER release, along with production and consumption data, also indicates that the Q3 GDP figures might be more favorable than the GDP indicator suggested (-0.1% q/q, -0.1% y/y). A stronger GDP reading today for Q3 would be a bit of a paradox, as the weaker NIER survey and GDP indicator were contributing factors to the Riksbank's decision to cut rates by 50bp earlier this month. Additionally, we receive October's retail sales data. It is noteworthy that sentiment among households and in the retail trade sector continued to improve in yesterday's NIER survey, which suggests that retail sales will recover from here.

Over the weekend we get Chinese PMIs for November. In the past two months we saw a decent increase in the official PMI manufacturing from NBS rising to 50.1 in October. We expect to see a flat reading reflecting somewhat better activity after the recent round of stimulus. We also look for a small rise in Caixin PMI manufacturing (Monday) coming from 50.3 in October.

Economic and market news

What happened overnight

In Japan, the Tokyo CPI excl. fresh foods came in higher than expected at 2.2% (consensus: 2.1%, prior: 1.8%). The print fuelled expectations for a potential 25bp rate hike in Japan in one of the upcoming meetings. USD/JPY dropped from around 150.3 before the meeting to 149.80 after the release. Since it has strengthened a bit and is now trading around 150. We expect Bank of Japan to deliver a 25bp hike at the December meeting.

What happened yesterday

In the euro area, ECB's Villeroy said that ECB should keep its options open for a bigger than 25bp rate cut at the next monetary policy meeting. Furthermore, he added that the policy rate could be on a path where it ends below the neutral rate, such that monetary policy once again stimulates growth. We still see the most realistic case that ECB cut the interest rate by 25bp at the December meeting.

EU commissioner Von der Leyen presented a new EU commission. The new Commission leans centre-right and will prioritize competition, defence, and the green transition. However, as the Greens lack a commissioner, there is likely less emphasis on climate issues in favour of competitiveness and industrial policies. A notable change under the second term of President von der Leyen is the redistribution of responsibilities among commissioners, ensuring that basically no single commissioner has full autonomy. Hence, von der Leyen will gain much more influence this time and the picks of commissioners show this already as it was the first time no commissioner was ousted by Parliament.

Von der Leyen also presented that she is establishing a task force to implement the recommendations from the Draghi report, which highlights the focus on competitiveness. Although her statements were somewhat unclear, the substantial aspect is the formation of a team, including some individuals who assisted Draghi in drafting his confidential report. This team will support the Commission's departments in ensuring the report's recommendations are executed effectively.

Equities: Global equities were higher yesterday despite the guiding star of the US being out for celebrating Thanksgiving. With the US markets closed, it was a rather quiet session, but this did not deter Europe from posting gains of approximately 0.5%, led by cyclicals. Although macro factors are not the sole focus currently, we received a favourable combination of news, with inflation figures coming in even more benign than anticipated and the Ecofin data surprisingly strong. The US is back for only half a day today following yesterday's celebrations, yet this has not prevented China from pushing markets higher, while the rest of Asia remains more subdued. It is important to consider the currency effect for Japan again this morning. Both European and US futures are trending upwards this morning.

FI: Yesterday, the OAT-Bund spread saw a 4bp tightening to 82bp following French PM Barnier's concession to National Rally's demands, which could allow the 2025 budget to be approved by parliament. EGB yields continued moving lower throughout Thursday, as markets added to ECB rate cut expectations for 2025 following a string of weaker-than-expected core inflation prints out from Germany, Spain and Belgium. The 5y5y EUR inflation swap rate dropped below 2% for the first time since August 2022, highlighting the non-negligible risk that inflation could settle below the target. US was closed for Thanksgiving.

FX: Apart from the politically induced sell-off to the BRL yesterday's FX session was rather quiet and dominated by the US Thanksgiving holiday season. The USD was the general underperformer while the MXN, NOK and JPY all did well albeit gains were relatively limited.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.58; (P) 192.03; (R1) 192.73; More...

GBP/JPY's decline from 199.79 continues today and intraday bias stays on the downside. As noted before, corrective rise from 180.00 could have completed with three waves up to 199.79. Deeper decline would be seen to 183.70 support next. On the upside, above 192.45 minor resistance will turn intraday bias neutral first. But risk will now stay on the downside as long as 55 D EMA (now at 194.88) holds, in case of recovery.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

Yen Rally Resumes on Tokyo CPI, Swiss GDP and Eurozone Inflation Watched

Yen resumed its broad-based rally during the Asian session, lifted by stronger-than-expected Tokyo inflation data. The accelerated inflation figures have reignited market speculation about another rate hike by BoJ as early as December. Overnight index swaps now suggest there is over 60% probability of a 25bps increase at this upcoming meeting.

A key highlight from the inflation report is the continued uptick in services inflation, indicating that price pressures are becoming more entrenched in the domestic economy. The rise in core-core CPI also signaled that underlying inflation is gaining momentum beyond volatile food and energy prices.

However, the less-than-stellar retail sales growth raises questions about the robustness of domestic demand. This softness in retail activity may temper BoJ's urgency to act immediately, as policymakers might seek more concrete evidence of sustained demand-pull inflation before making a policy shift.

Nevertheless, a recent Bloomberg poll showed that over 80% of economists surveyed expect BoJ to adjust its policy by January. Similarly, a Reuters survey showed that 90% of economists anticipate an increase in the policy rate from the current 0.25% to 0.50% by the end of March. This widespread expectation suggests that while the exact timing remains uncertain, a rate hike is likely to occur within the next few months.

Overall in the currency markets, Yen continues to outperform its peers, maintaining its position as the best performer of the week. Swiss Franc ranks as the second strongest currency, while Euro holds the third spot. Conversely, Loonie remains the weakest. Dollar has slipped to the second weakest position, while Aussie follows as the third weakest. Sterling and Kiwi continue to occupy middle positions.

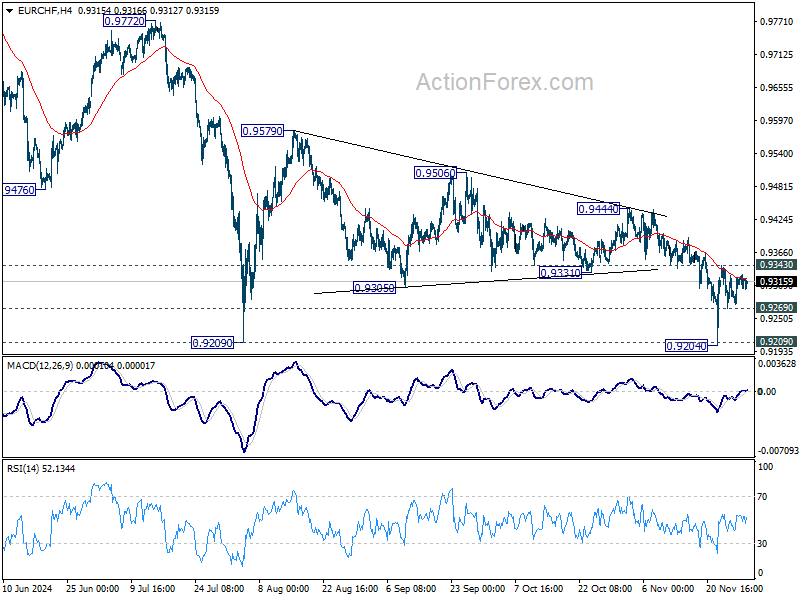

Looking ahead, Swiss GDP and Eurozone CPI flash are set to take center stage. These data could determine whether Swiss Franc or Euro finishes the week stronger.

Technically, break of 0.9269 minor support in EUR/CHF will indicate another rejection by 55 4H EMA and bring retest of 0.9204/9 support zone. Firm break there will resume larger down trend. However, firm break of 0.9343 resistance will argue the near term down trend might be reversing, and target 0.9444 resistance and possibly above.

In Asia, at the time of writing, Nikkei is down -0.40%. Hong Kong HSI is down -0.15%. China Shanghai SSE is up 0.87%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is down -0.0005 at 1.057.

Tokyo CPI core accelerates to 2.2%, boosting speculation of BoJ rate hike

Tokyo's November CPI data pointed to resurgence of inflation pressures in Japan, raising expectations for BoJ to tighten policy further.

Tokyo Core CPI, excluding food, climbed from 1.8% yoy to 2.2% yoy, beating expectations of 2.1%, driven largely by the reduction in energy subsidies.

Core-core CPI, excluding food and energy, edged higher from 1.8% yoy to 1.9% yoy from 1.8%. Services prices, a key indicator of domestic demand-driven inflation, also increased, rising from 0.8% yoy to 0.9% yoy.

Headline CPI surged significantly, jumping from 1.8% yoy to 2.6% yoy.

Japan's industrial output grows 3% mom in Oct, but contractions expected ahead

Japan's industrial production rose by 3.0% mom in October, marking the second consecutive month of growth but falling short of market expectations of a 3.9% mom increase. This uptick is nonetheless an improvement from September's 1.6% mom growth.

Out of the 15 industrial sectors surveyed, 11 sectors—including production machinery and motor vehicles—reported increased output, while four sectors, such as electronic parts and devices, experienced declines.

The Ministry of Economy, Trade and Industry maintained its previous assessment, stating that industrial production is fluctuating "indecisively."

Looking ahead, the ministry projects that industrial output will decrease for two consecutive months, by -2.2% mom in November and a further -0.5% mom in December, likely dragged down by sectors like production machinery and transport equipment.

A ministry official expressed concern over "downside risks from overseas demand," which could significantly impact the output of products like semiconductor manufacturing equipment and motor vehicles.

In additional economic data, retail sales increased by 1.6% yoy in October, missing expectations of a 2.1% yoy rise. Unemployment rate edged up from 2.4% to 2.5%, matching forecasts.

Looking ahead

Swiss GDP and KOF economic barometer will be released in European session. Eurozone CPI flash is another focus. Germany import prices, retail sales and unemployment France GDP revision, and UK M4 money supply will also be featured. Later in the day, Canada's GDP data is the only focus.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.58; (P) 192.03; (R1) 192.73; More...

GBP/JPY's decline from 199.79 continues today and intraday bias stays on the downside. As noted before, corrective rise from 180.00 could have completed with three waves up to 199.79. Deeper decline would be seen to 183.70 support next. On the upside, above 192.45 minor resistance will turn intraday bias neutral first. But risk will now stay on the downside as long as 55 D EMA (now at 194.88) holds, in case of recovery.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

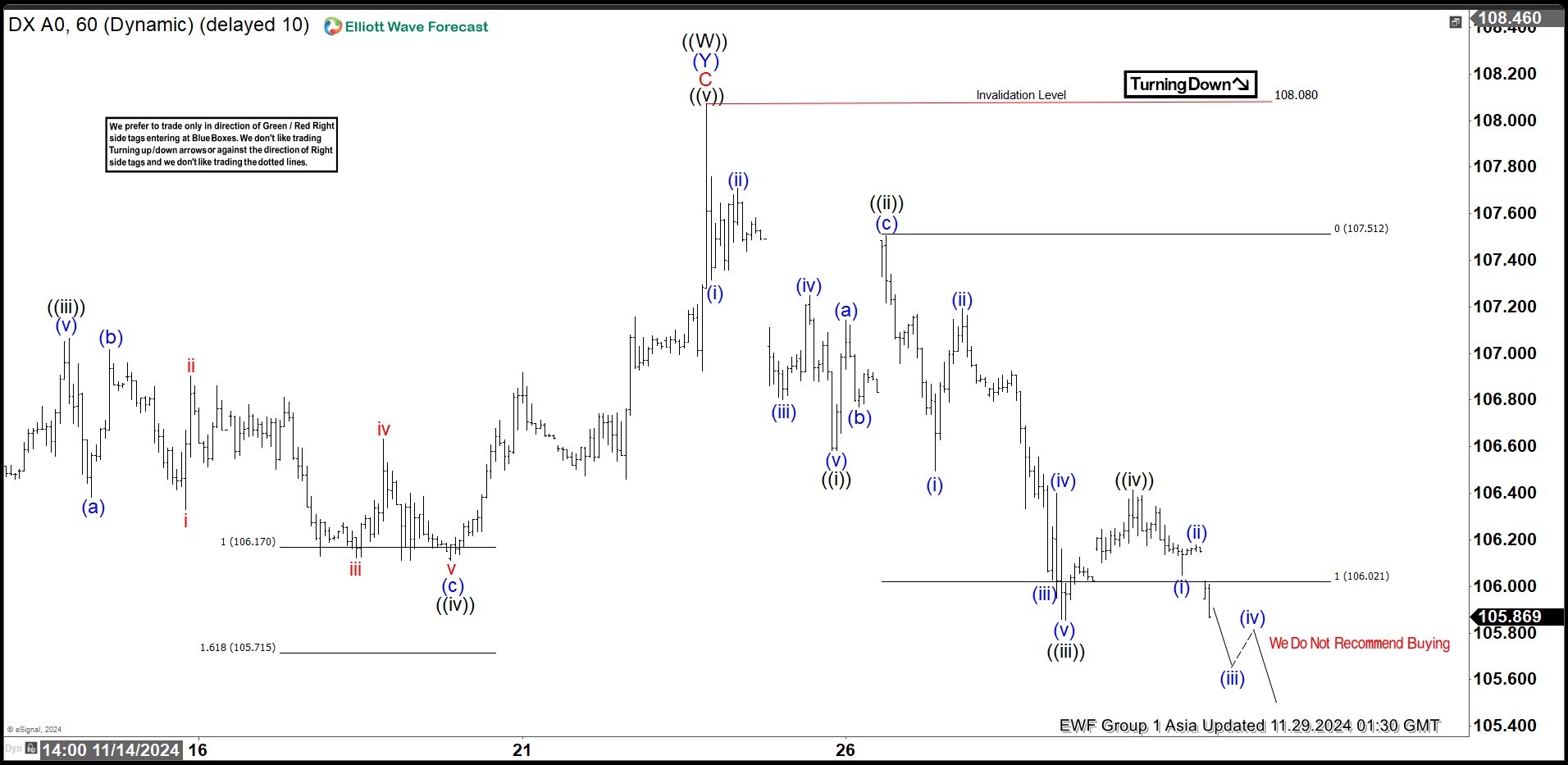

Elliott Wave View: US Dollar Index Turning Lower

Dollar Index (DXY) has reached 100% Fibonacci extension from 7.17.2023 low and ended the cycle. The rally is unfolding as a double three Elliott Wave structure. Up from 7.17.2023 low, wave (W) ended at 107.34 and wave (X) pullback ended at 100.15. Wave (Y) higher ended at 108 which completed wave ((W)) in higher degree as the 1 hour chart below shows. Wave ((X)) is currently in progress with a possible zigzag structure. Down from wave ((X)), wave (i) ended at 107.31 and wave (ii) ended at 107.71. Wave (iii) lower ended at 106.8 and rally in wave (iv) ended at 107.24.

Final leg wave (v) ended at 106.58 which completed wave ((i)). Wave ((ii)) rally ended at 107.5 with internal subdivision as a zigzag. Up from wave ((i)), wave (a) ended at 107.14 and wave (b) ended at 106.77. Wave (c) higher ended at 107.5 which completed wave ((ii)). The Index has resumed lower again in wave ((iii)). Down from wave ((ii)), wave (i) ended at 106.49 and wave (ii) ended at 107.19. Wave (iii) lower ended at 106 and wave (iv) ended at 106.4. Final wave (v) ended at 105.85 which completed wave ((iii)). Wave ((iv)) rally ended at 106.41. Expect Index to extend lower in wave ((v)) before turning higher in 3 waves. Near term, as far as pivot at 108.08 high is intact, expect rally to fail in 3, 7, or 11 swing for further downside.

Dollar Index (DXY) 60 Minutes Elliott Wave Chart

DXY Elliott Wave Video

https://www.youtube.com/watch?v=7VynFiFPPqU

Japan’s industrial output grows 3% mom in Oct, but contractions expected ahead

Japan's industrial production rose by 3.0% mom in October, marking the second consecutive month of growth but falling short of market expectations of a 3.9% mom increase. This uptick is nonetheless an improvement from September's 1.6% mom growth.

Out of the 15 industrial sectors surveyed, 11 sectors—including production machinery and motor vehicles—reported increased output, while four sectors, such as electronic parts and devices, experienced declines.

The Ministry of Economy, Trade and Industry maintained its previous assessment, stating that industrial production is fluctuating "indecisively."

Looking ahead, the ministry projects that industrial output will decrease for two consecutive months, by -2.2% mom in November and a further -0.5% mom in December, likely dragged down by sectors like production machinery and transport equipment.

A ministry official expressed concern over "downside risks from overseas demand," which could significantly impact the output of products like semiconductor manufacturing equipment and motor vehicles.

In additional economic data, retail sales increased by 1.6% yoy in October, missing expectations of a 2.1% yoy rise. Unemployment rate edged up from 2.4% to 2.5%, matching forecasts.

Tokyo CPI core accelerates to 2.2%, boosting speculation of BoJ rate hike

Tokyo's November CPI data pointed to resurgence of inflation pressures in Japan, raising expectations for BoJ to tighten policy further.

Tokyo Core CPI, excluding food, climbed from 1.8% yoy to 2.2% yoy, beating expectations of 2.1%, driven largely by the reduction in energy subsidies.

Core-core CPI, excluding food and energy, edged higher from 1.8% yoy to 1.9% yoy from 1.8%. Services prices, a key indicator of domestic demand-driven inflation, also increased, rising from 0.8% yoy to 0.9% yoy.

Headline CPI surged significantly, jumping from 1.8% yoy to 2.6% yoy.

This inflation data has heightened market anticipation of a policy change from BoJ. Overnight swaps now indicate over 60% probability of a rate hike at the December meeting. Meanwhile, more than 80% of economists surveyed recently forecasting an adjustment by January.

With the BoJ's current policy rate at 0.25%, the decision appears imminent, likely within the next two months.