Sample Category Title

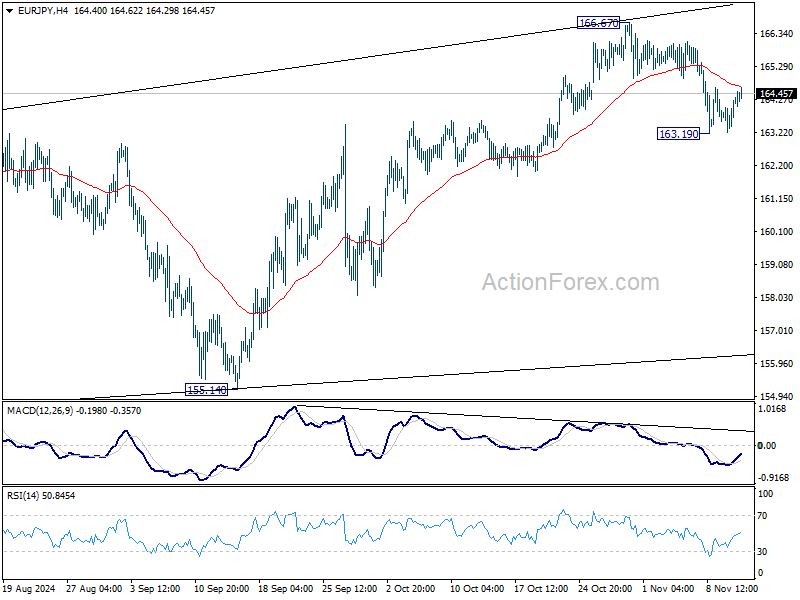

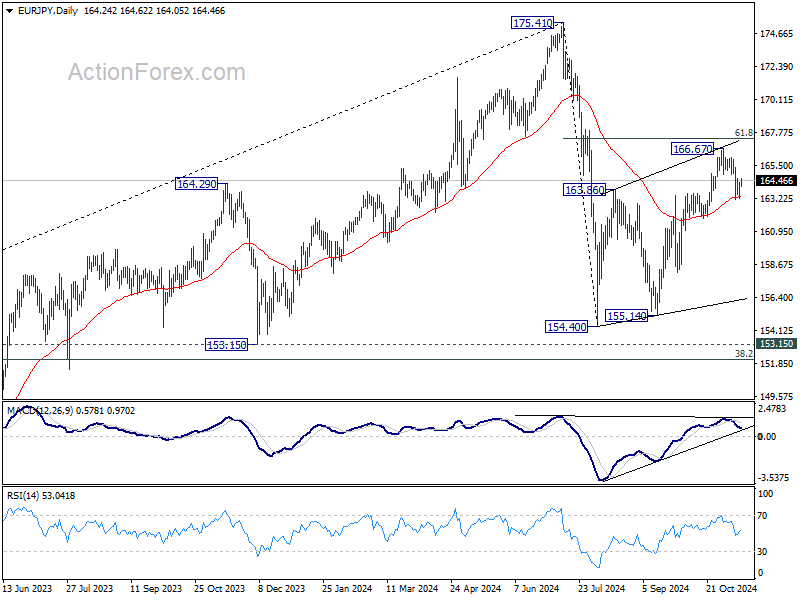

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.56; (P) 163.95; (R1) 164.64; More....

EUR/JPY turned sideway after drawing support from 55 D EMA (now at 163.34), and intraday bias is turned neutral first. On the downside, sustained trading below 55 D EMA will argue that whole corrective rise from 154.40 has completed with three waves up to 166.67. Deeper decline should then be seen back to 154.40/155.14 support zone. On the upside, break of 166.67 will target 61.8% retracement of 175.41 to 154.40 at 167.38 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

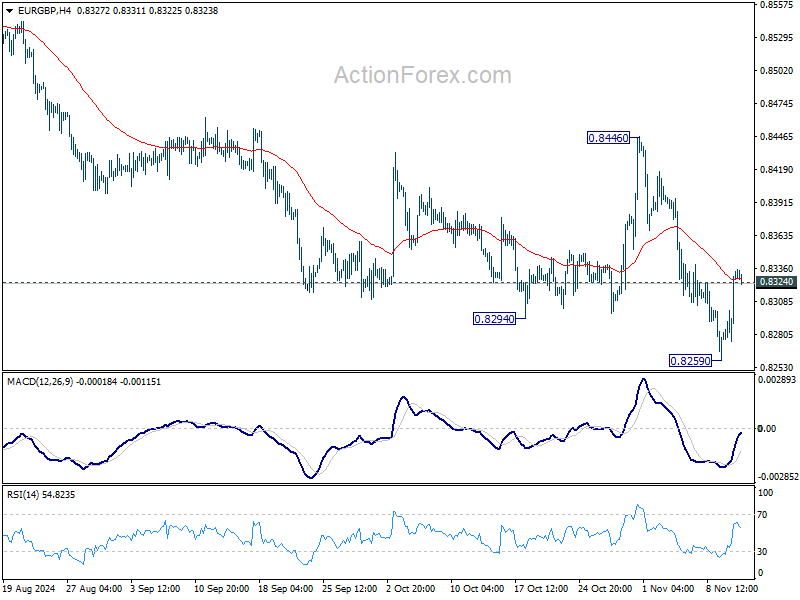

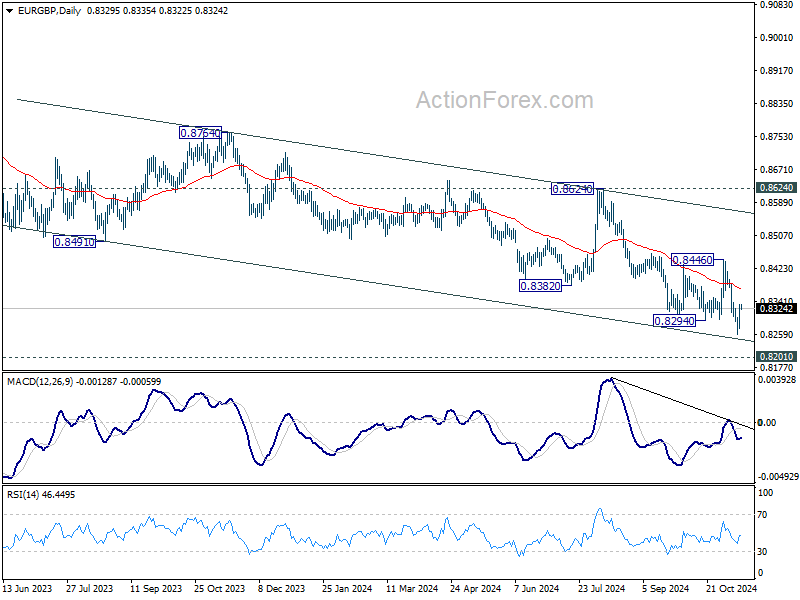

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8294; (P) 0.8315; (R1) 0.8354; More...

Intraday bias in EUR/GBP is turned neutral again with break of 0.8324 minor resistance. Some consolidations could be seen but further decline is expected as long as 0.8446 resistance holds. Break of 0.8259 will resume larger down trend to 0.8201 key support.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

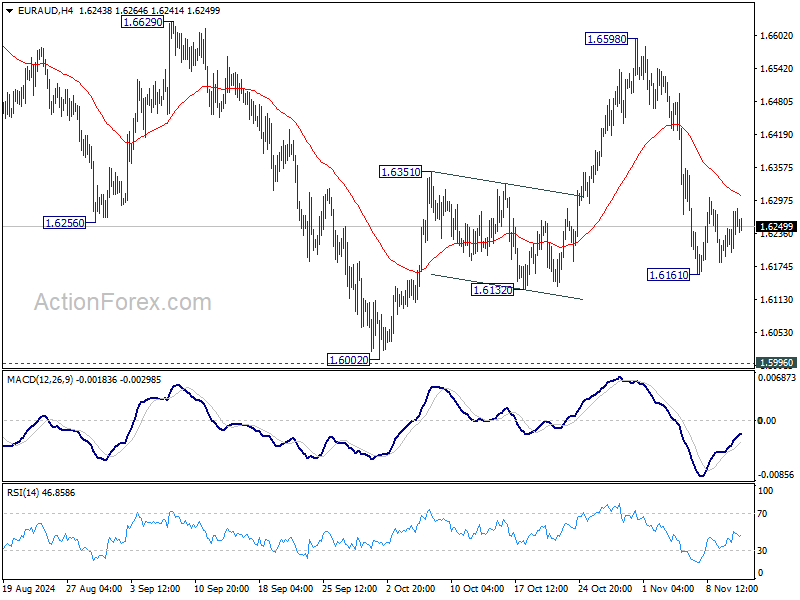

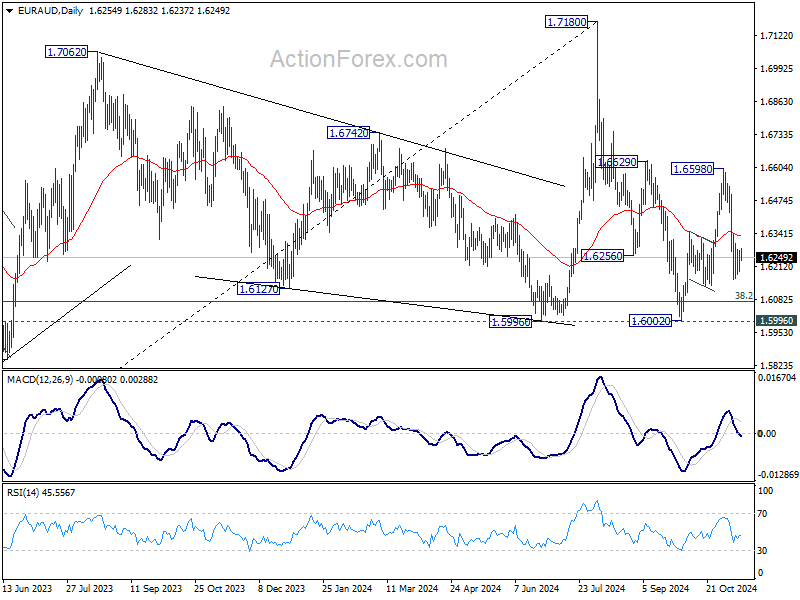

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6211; (P) 1.6245; (R1) 1.6293; More...

Intraday bias in EUR/AUD remains neutral, and risk will stay mildly on the downside as long as 1.6598 holds, in case of stronger rebound. On the downside, break of 1.6161 will resume the decline from 1.6590 to target a test on 1.5996/6002 key support zone.

In the bigger picture, as long as 1.5996 cluster support , up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

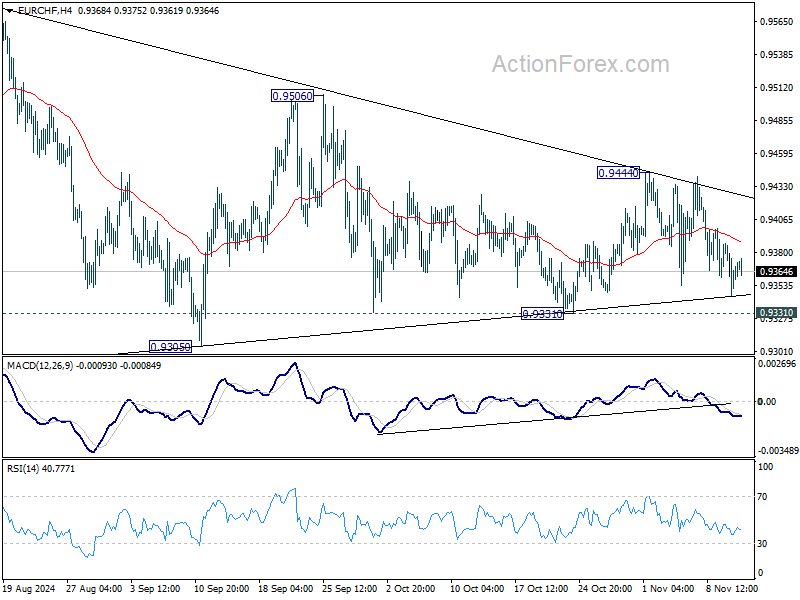

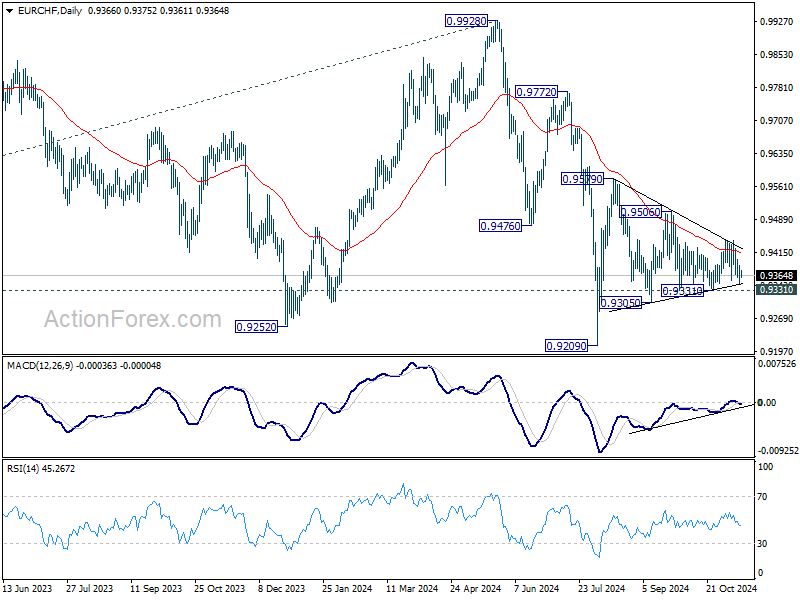

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9346; (P) 0.9368; (R1) 0.9389; More....

No change in EUR/CHF's outlook as range trading continues inside converging triangle. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9419) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

Greenback Strengthens Once More Against All Major Peers

Markets

US bond yields surged after having had the day off on Monday for Veteran’s Day. Net daily changes varied between 8.7 and 13.1 bps across the curve spectrum as President-elect Trump’s reflationary politics continue to reverberate. Expectations for a (much) looser fiscal policy lift those for US growth at a time when CPI inflation has yet to hit the 2% central bank target. With Germany now having set the election date at February 23, we’ll be looking for the fiscal narrative to gain traction in the country and more broadly in Europe as well. US CPI not being at target will still have been the case in October. Numbers are released later today. Headline inflation is seen to accelerate from 2.4% to 2.6% y/y. Core inflation would match September’s 3.3%. Any beat, however small, would cast further doubt on another December 25 bps rate cut. Markets already pared the odds sharply to about 60%. Minneapolis Fed Kashkari yesterday said that “if we saw inflation surprises to the upside between now and then, that might give us pause” when asked what could cause the Fed not to cut rates next month, deviating from the September dot plot. Kashkari is live commenting at Bloomberg when the CPI numbers come out. Stock markets succumbed to the yield pressure. Wall Street eased off the record highs, the Dow Jones underperforming. Europe’s Stoxx50 slipped 2.25%. A technical acceleration kicked in after the index lost support around 4800. Widening interest rate differentials (European swap rates rose between 0.7-4.6 bps) and the risk-off created the perfect environment for the USD. The greenback strengthened once more against all major peers. EUR/USD tested the 1.06 big figure. It avoided a break yesterday (1.062) but continues to trade on the backfoot this morning (1.061), suggesting ongoing, by default dollar strength. USD/JPY extends its meteoric rise that’s been going on since mid-September to beyond 155 currently. We expect to see some Japanese government and central bank officials to become increasingly vocal about the matter. Gilts underperformed Bunds on “sticky” (BoE chief economist Pill) wage growth but sterling couldn’t benefit. Perhaps the UK currency is eying other important data that’s upcoming, including Friday’s GDP numbers and next week’s CPI. EUR/GBP jumped back above 0.83 but the technical picture remains a fragile one.

News & Views

The Federal Reserve Bank of New York consumer survey showed households’ inflation expectations declined slightly across the whole spectrum of horizons in October. One-year ahead inflation expectations eased 0.1%pt to 2.9%, three-year ahead expectations declined 0.2%pt to 2.5% and the 5-y gauge softened to 2.8%. Home price growth expectations (3.0%) were unchanged and stayed in a tight band since August 2023. Labor market expectations improved with households reporting a lower likelihood of higher unemployment (-1.7%pt to 34.5%, the lowest since Feb 2022) and personal job loss (-0.3%pt to 13.0%). Consumers see a higher likelihood of finding a job if they were laid off. Median expected household income growth as unchanged at 3.0%. That was also the case for spending growth 4.9%, but this parameter stays well above pre-pandemic levels. Perceptions of credit access compared to a year ago improved in October. The average perceived probability of missing a minimum debt payment over the next three months decreased by 0.3%pt to 13.9%, the first decrease since May 2024. Perceptions about households’ current financial situations compared to a year ago improved.

Australian quarterly wage growth figures for Q3 for the third consecutive quarter printed at 0.8% Q/Q. The Y/Y measure eased to 4.1% to 3.5%. The rise was slightly more modest than expected. Annual growth in the private sector was 3.5% in the September quarter 2024. This is the lowest private sector annual growth since the September quarter 2022. Public sector annual growth (+3.7%) was higher than in the same quarter last year (+3.5%), but lower than the recent peak (+4.2%) seen in December quarter 2023. The Reserve bank of Australia expects wage growth to ease to 3.4% at the end of the 2024 and 3.2% end 2025. However, for these kinds of wage growth levels to be compatible with inflation sustainably returning to 2-3% a further rise in productivity is probably needed. Money markets currently still only fully discount a first RBA rate cut in the summer of next year. The Aussie dollar remains under pressure from USD strength (AUD/USD 0.6525) but in this move recently outperformed the likes of the euro (EUR/AUD 1.626).

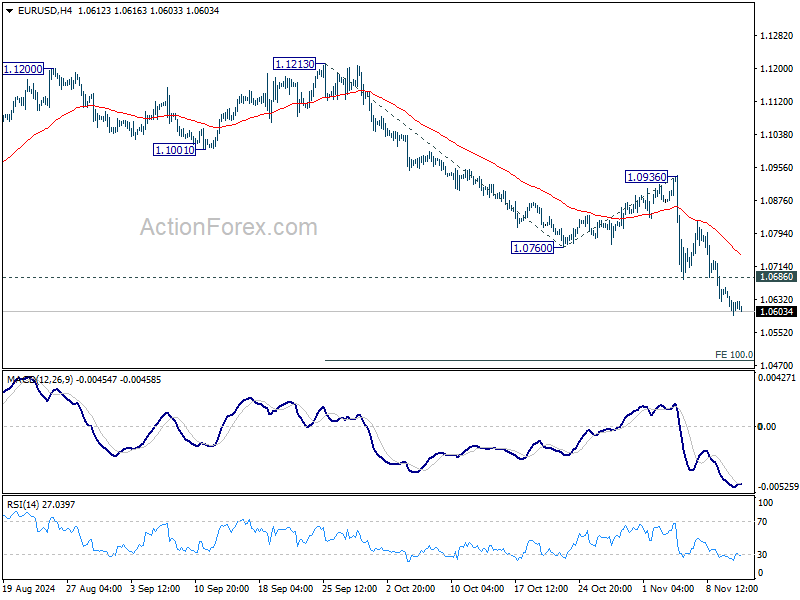

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0591; (P) 1.0627; (R1) 1.0659; More...

Intraday bias in EUR/USD remains on the downside for the moment. Fall from 1.1213 should target 100% projection of 1.1213 to 1.0760 from 1.0936 at 1.0483. On the upside, above 1.0686 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0760 support turned resistance holds.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

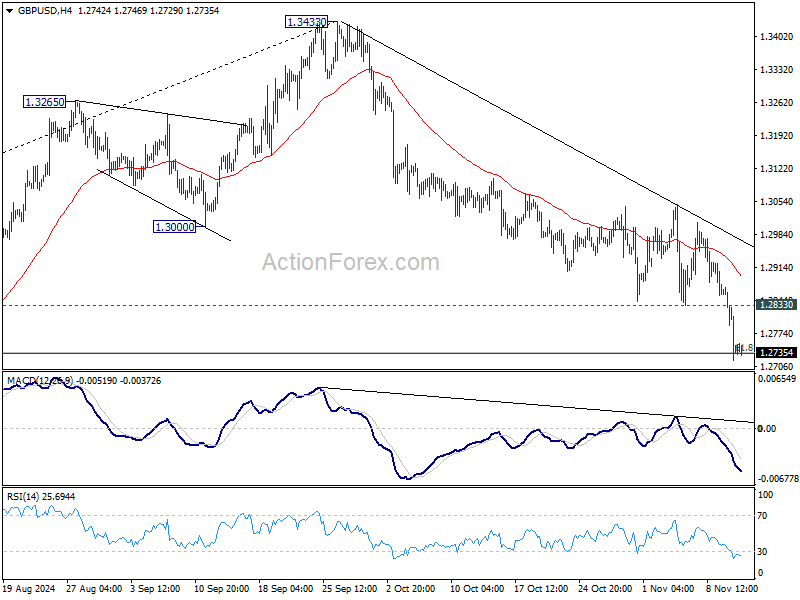

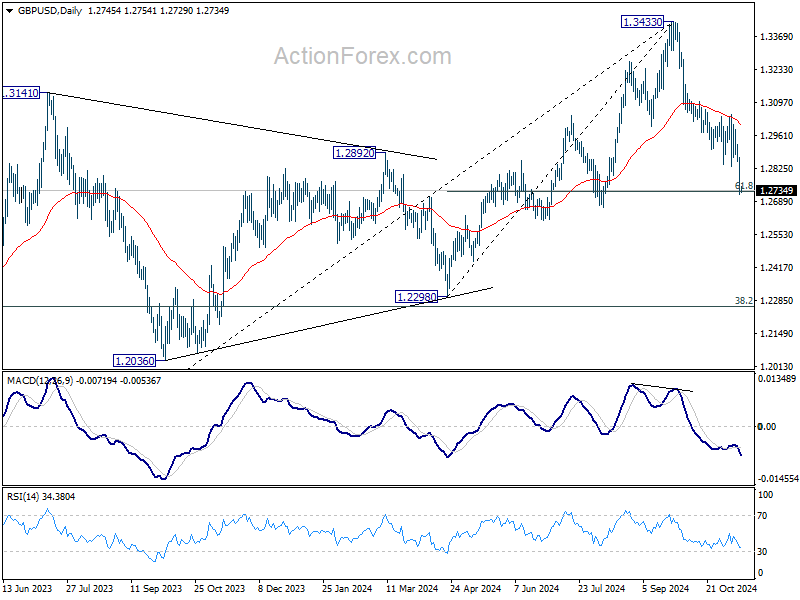

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2685; (P) 1.2781; (R1) 1.2843; More...

Intraday bias in GBP/USD stays on the downside at this point. Decisive break of 61.8% retracement of 1.2298 to 1.3433 at 1.2732 will extend the decline from 1.3433 to 1.2298 key support. On the upside, above 1.2833 support turned resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

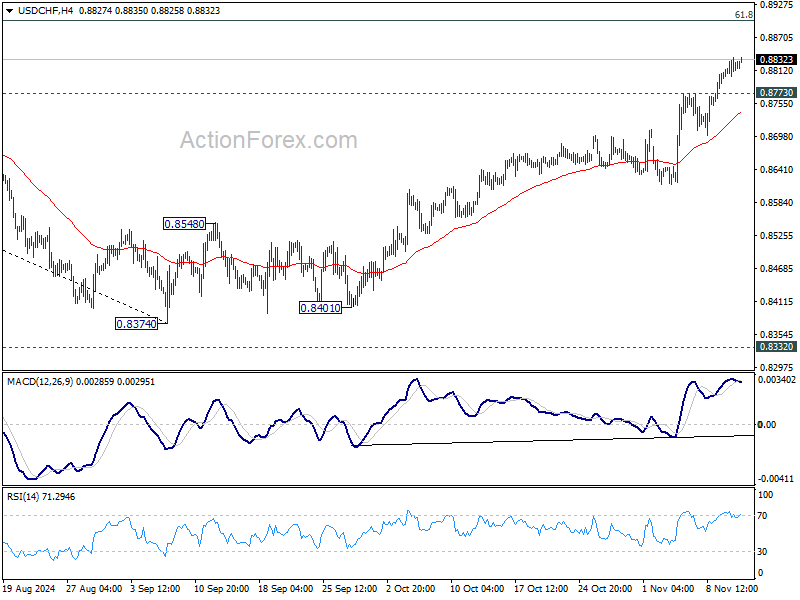

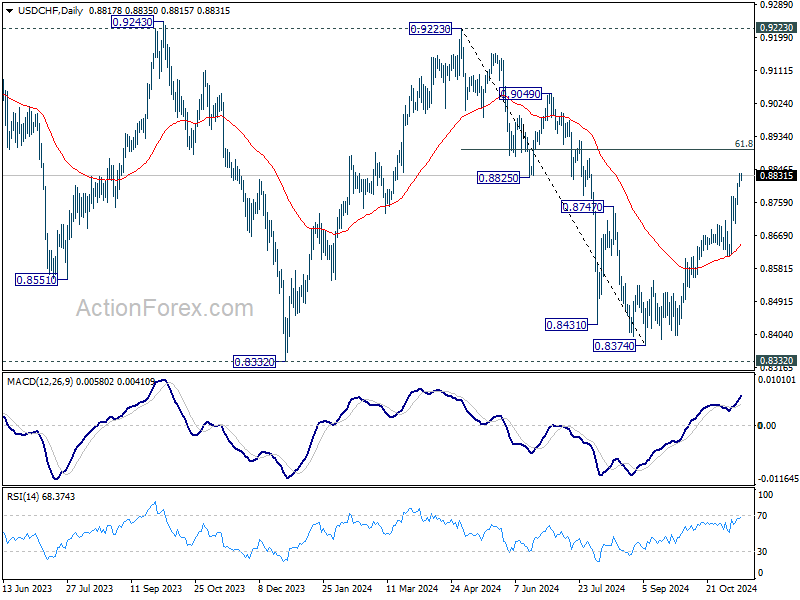

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8780; (P) 0.8808; (R1) 0.8845; More…

Intraday bias in USD/CHF stays on the upside for the moment. Current rise from 0.8374 should target 61.8% retracement of 0.9223 to 0.8374 at 0.8899. Sustained trading above there will pave the way towards 0.9223 high. On the downside, below 0.8773 support will turn intraday bias neutral again and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

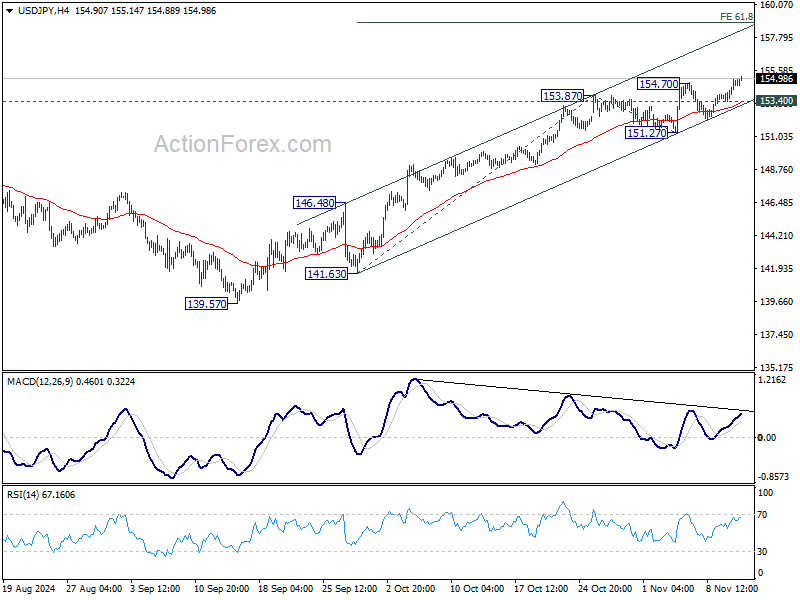

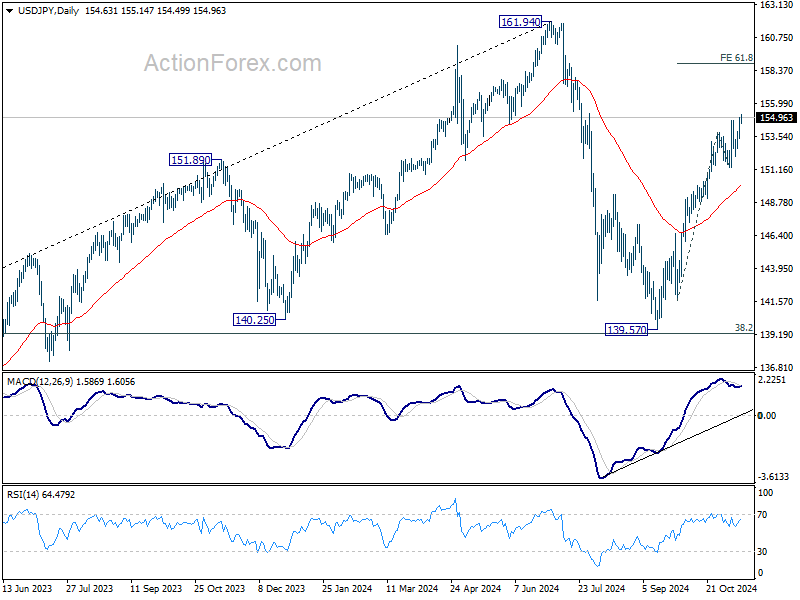

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.72; (P) 154.32; (R1) 155.23; More...

USD/JPY's rally resumed by breaking 154.70 and intraday bias is back on the upside. Current rise from 139.57 will 61.8% projection of 141.63 to 153.87 from 151.27 at 158.8. On the downside, below 153.40 minor support will turn intraday bias neutral again first. But further rally is expected as long as 151.27 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

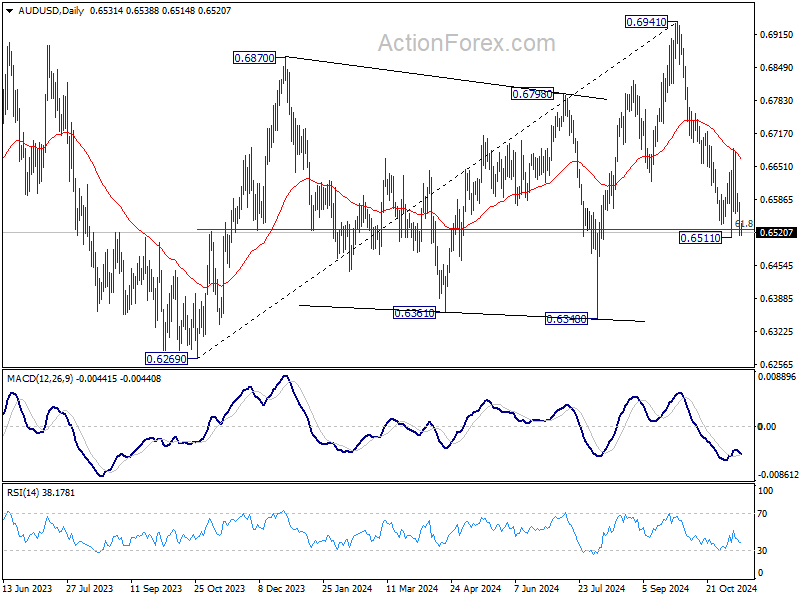

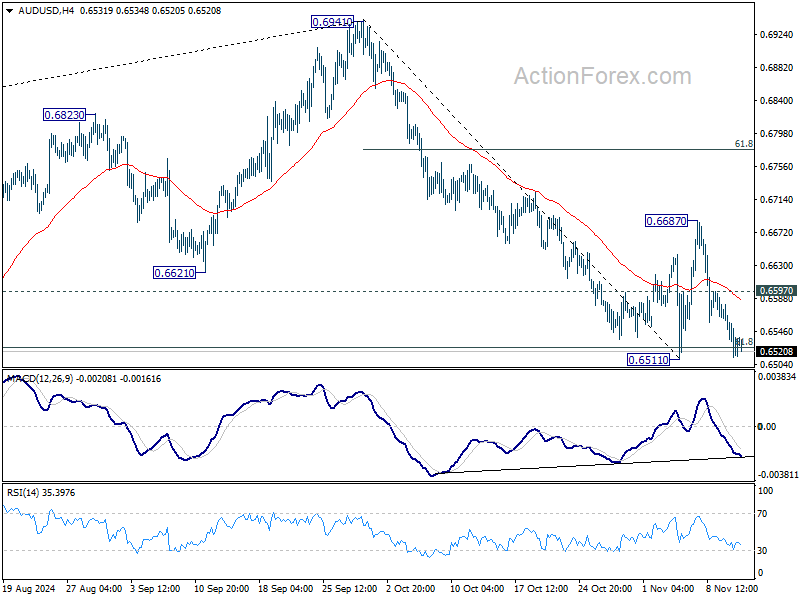

AUD/USD Daily Report

Daily Pivots: (S1) 0.6505; (P) 0.6543; (R1) 0.6573; More...

Intraday bias in AUD/USD remains neutral for the moment. On the upside, above 0.6597 minor resistance will turn bias back to the upside for 0.6687 first. Firm break there will target 61.8% retracement of 0.6941 to 0.6511 at 0.6777. On the downside, break of 0.6511 will resume the fall from 0.6941 instead.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.