Sample Category Title

WTI Crude Oil Slips: Is The Market Headed for Further Losses?

Key Highlights

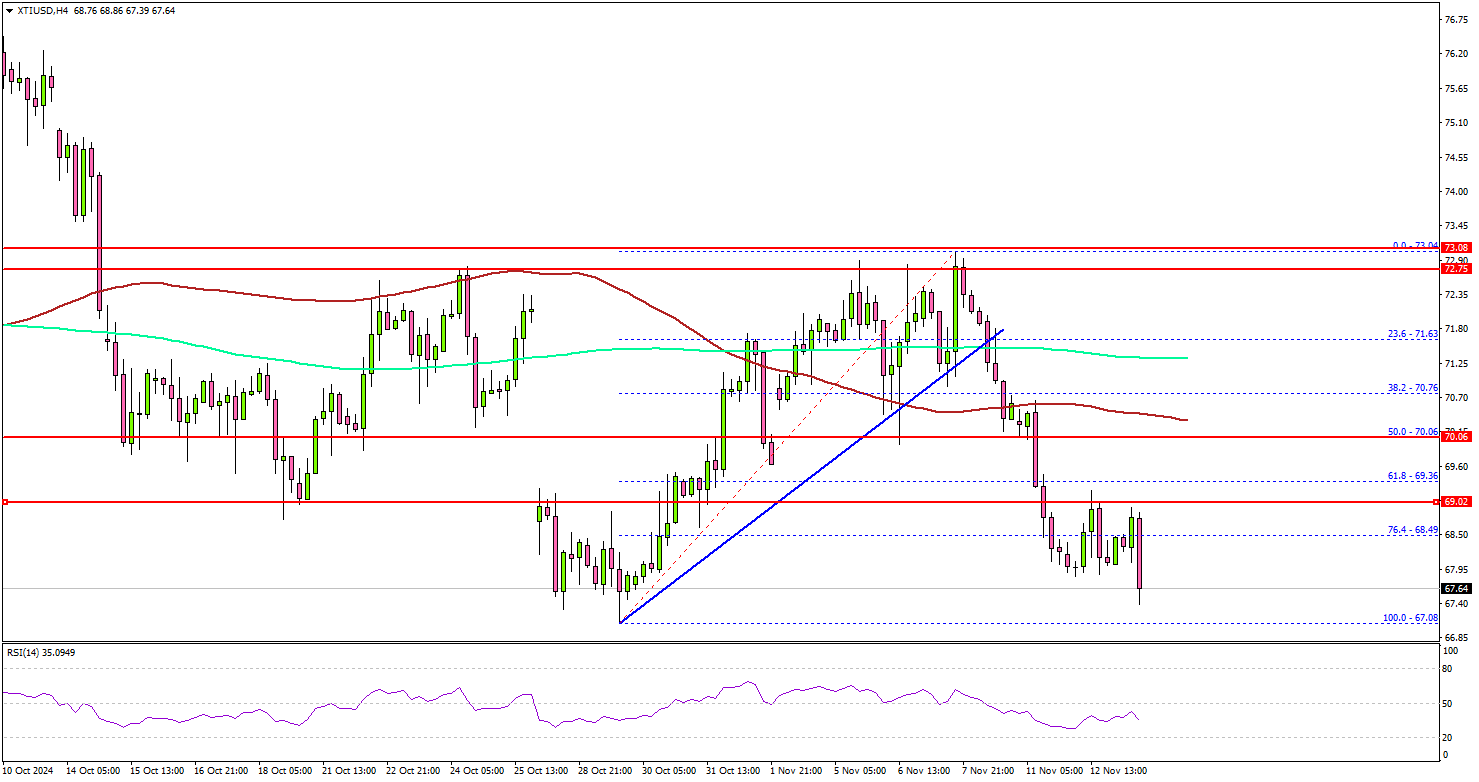

- WTI Crude Oil price started a fresh decline from the $73.00 resistance zone.

- It traded below a key bullish trend line with support at $71.80 on the 4-hour chart.

- EUR/USD could gain bearish momentum below the 1.0580 support.

- Gold prices might struggle to recover and could continue lower.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price failed to extend gains above $73.80 and $74.00. It started a fresh decline and traded below the key support at $72.00.

Looking at the 4-hour chart of XTI/USD, the price traded below a key bullish trend line with support at $71.80. There was a clear move below the 50% Fib retracement level of the upward move from the $67.08 swing low to the $73.04 high.

The price even settled below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the downside, the first major support sits near the $67.00 zone.

A daily close below $67.00 could open the doors for a larger decline. The next major support is $65.50. Any more losses might send oil prices toward $62.00 in the coming days.

On the upside, it faces resistance near the $69.00 level. The next major resistance is near the $70.00 zone and the 100 simple moving average (red, 4-hour). The main hurdle is still near the $73.00 zone, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $75.00 resistance. Any more gains might call for a test of the $76.50 resistance zone in the near term.

Looking at EUR/USD, the pair is consolidating losses, and the bears seem to be aiming for more downsides toward 1.0520.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 223K, versus 221K previous.

- US Producer Price Index for Oct 2024 (YoY) – Forecast +2.3%, versus +1.8% previous.

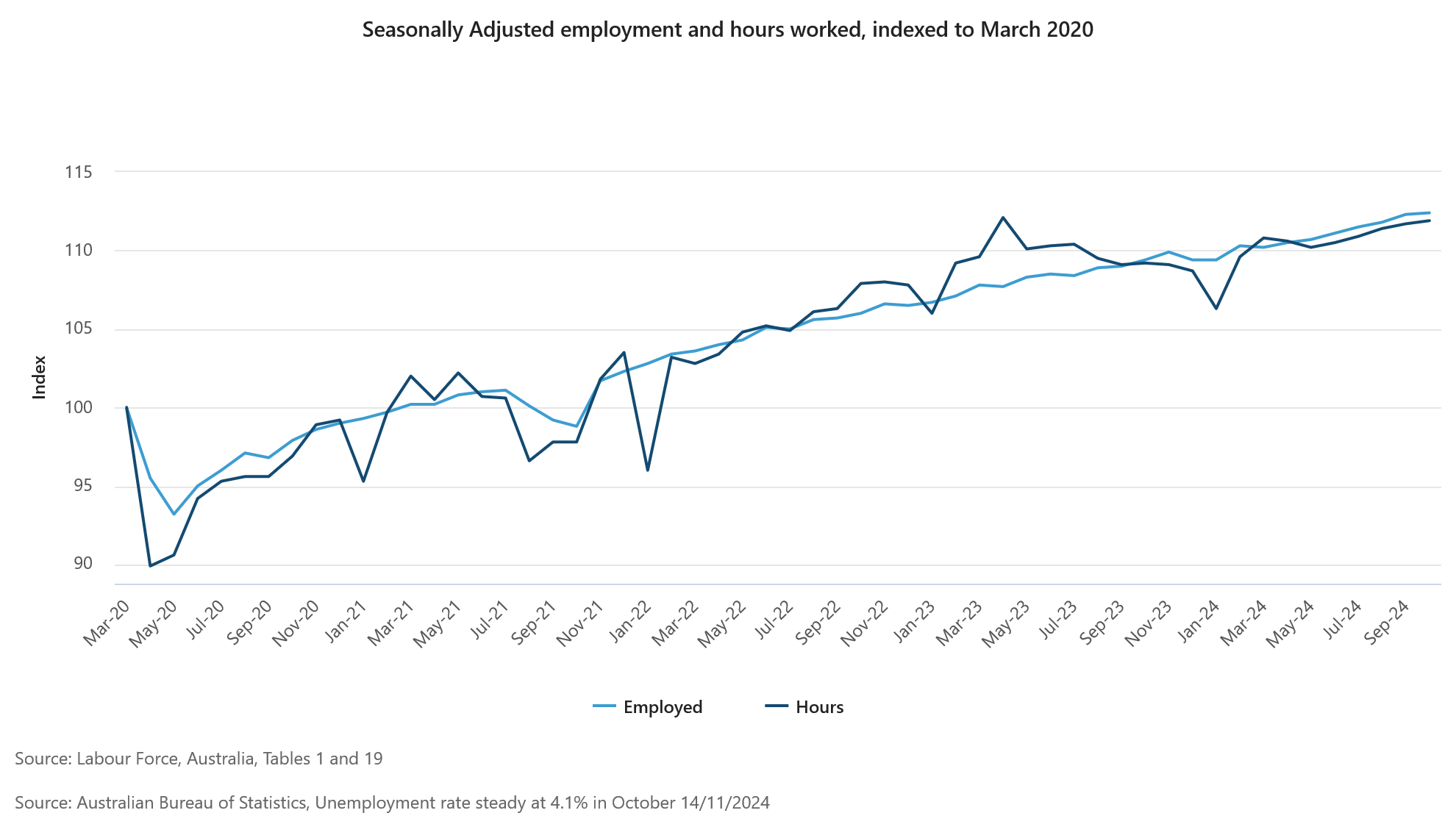

Australia’s employment growth 15.9k in Oct, slowest rate in recent months

Australia's employment grew modestly in October, rising by 15.9k or 0.1% mom, falling short of the anticipated 25k increase. This represents the slowest pace of employment growth in recent months, following a period of more robust gains averaging 0.3% per month over the last six months. Full-time positions rose by 9.7k, while part-time jobs increased by 6.2k, both contributing to the incremental rise.

Unemployment rate remained steady at 4.1%, matching expectations, although the participation rate saw a slight dip from 67.2% to 67.1%. The number of unemployed rose by 1.3% mom, adding 8.3k to the job-seeking pool. In terms of labor utilization, monthly hours worked inched up by 0.1% mom, reflecting only minimal expansion in total labor demand.

This marks the third consecutive month with an unemployment rate of 4.1%, which stands 0.6% points higher than June 2023 low of 3.5%. Nonetheless, this rate remains 1.1% below the pre-pandemic level of 5.2% in March 2020.

The deceleration in employment growth could indicate a stabilizing labor market, aligning with recent RBA commentary on maintaining a restrictive policy stance until clear demand cooling is observed.

RBA’s Bullock: Policy to stay restrictive until demand cools to sustainable levels

RBA Governor Michele Bullock commented at a panel discussion today on Australia's economic and labor market conditions, noting that the economy is still operating at a level that risks fueling inflation.

According to Bullock, while labor market tightness has eased slightly, “it’s still not easy to get staff,” indicating persistent hiring challenges for businesses.

Bullock attributed the resilience in the job market to strong "demand" and "population growth". These factors, she noted, continue to support employment levels despite some easing in labor market constraints.

Comparing RBA’s policy stance with other central banks, Bullock remarked that while others have already moved to lower rates, RBA remains "not as restrictive."

Nevertheless, she emphasized that the bank considers its policy "restrictive enough" to address inflation risks and is committed to maintaining this stance until there’s clear evidence of a sustained "downward trajectory in demand."

Fed’s Musalem: To cut judiciously and patiently as inflation risks rising

St. Louis Fed President Alberto Musalem stated in a speech overnight that he expects inflation to converge toward the Fed's 2% target over the medium term. His baseline scenario anticipates a cooling labor market that remains within the range of full employment, alongside moderating compensation growth.

Musalem emphasized that this outlook depends on monetary policy staying "appropriately restrictive" while inflation exceeds 2%, a situation that would allow Fed to "judiciously and patiently" continue lowering interest rates.

However, Musalem expressed concerns that recent information indicates the risk of inflation failing to converge toward 2%, or even moving higher, "has risen."

Simultaneously, he noted that the risk of an unwelcome deterioration in the labor market "has remained unchanged or possibly fallen."

Although he is "attuned to the possibility of rising layoffs going forward," Musalem believes the overall strength of the economy "provides some confidence that a disorderly labor market deterioration is unlikely."

Fed’s Schmid: Rate cut depth unclear, productivity holds key

Kansas City Fed President Jeffrey Schmid highlighted overnight Fed’s confidence that inflation is on track to reach its 2% target, attributing this progress to "signs that both labor and product markets have come into better balance in recent months."

Schmid acknowledged that conditions are right to begin easing the Fed’s restrictive monetary policy but stressed that "it remains to be seen how much further interest rates will decline or where they might eventually settle."

He added that sustained gains in productivity could enable the economy to grow robustly without significant inflation. However, Schmid cautioned that economic growth could be dampened if the energy supply fails to meet the increasing demands, such as those driven by AI development.

“As an optimist, my hope is that productivity growth can outrun both demographics and debt," yet as a central banker, he remains committed to the Fed’s dual mandate, ensuring price stability and full employment, guided by data.

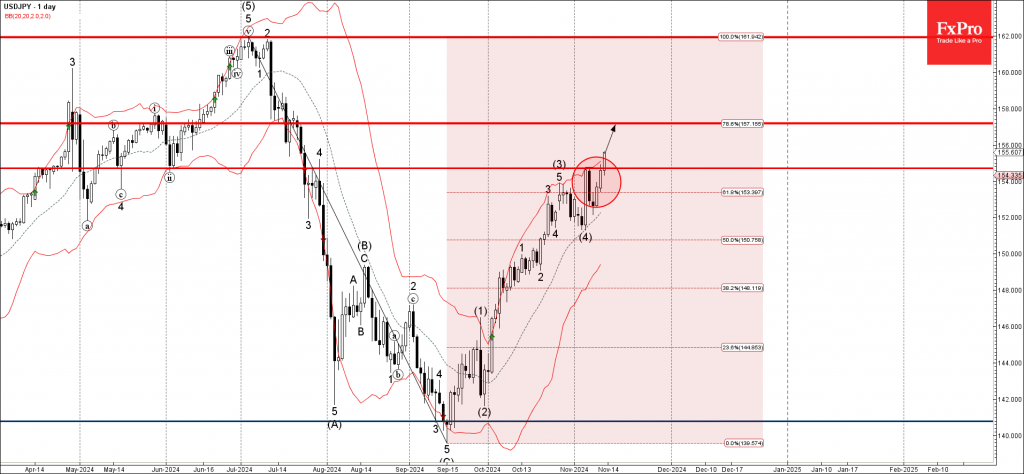

USDJPY Wave Analysis

- USDJPY broke key resistance level 154.70

- Likely to rise to resistance level 157.20

USDJPY currency pair recently broke the key resistance level 154.70 (former stern support from June, which has been reversing the price from the end of July).

The breakout of the resistance level 154.70 should accelerate the active medium-term impulse wave (5) from the start of November.

Given the clear daily uptrend and the bullish US dollar sentiment, USDJPY currency pair can be expected to rise to the next resistance level 157.20.

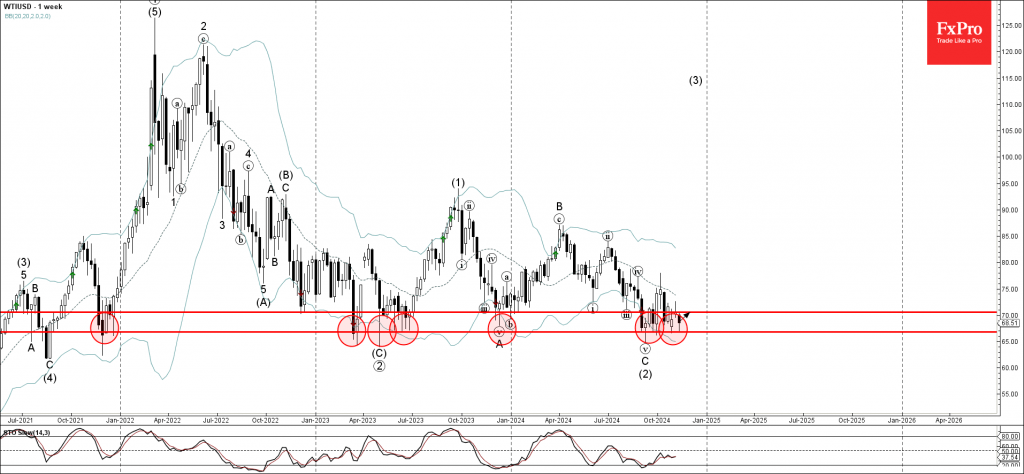

WTI Crude Wave Analysis

- WTI crude oil reversed from the multi-year support level 66.70

- Likely to rise to resistance level 70.00

WTI crude oil recently reversed up from the powerful multi-year support level 66.70 (which has been repeatedly reversing WTI from the end of 2021, as seen from the weekly WTI chart below).

The support level 66.70 was strengthened by the nearby lower daily and the weekly Bollinger Bands.

Given the strength of the nearby support level 66.70 and the bullish divergence on the weekly Stochastic indicator, WTI crude oil can be expected to rise to the next resistance level 70.00.

Dallas Fed’s Logan cites uncertainty on timing and extent of rate cuts

Dallas Fed President Lorie Logan emphasized today that while additional rate cuts will likely be necessary, "it’s difficult to be sure how many cuts may be needed and how soon they may need to happen.”

Logan also reiterated that the “neutral” rate—the level at which the interest rate neither stimulates nor restricts the economy—may be higher than initially estimated.

She suggested that the current rate is close to this neutral level, though precise measurement is challenging.

Fed’s Kashkari confident on inflation path, urges patience before policy decisions

Minneapolis Fed President Neel Kashkari conveyed optimism about the current direction of inflation but emphasized the importance of waiting for additional economic data before making any policy changes.

Speaking to Bloomberg TV shortly after release of October CPI, Kashkari mentioned that although he hadn't yet examined the details, the headline figures reinforced his confidence that inflation is moving favorably.

"I think that inflation is headed in the right direction. I’ve got confidence about that, but we need to wait,” he said. “We’ve got another month or six weeks of data to analyze before we make any decisions.”