Sample Category Title

US: Inflation Progress Grinds to a Halt in October

The Consumer Price Index (CPI) rose 0.2% month-on-month (m/m) in October, in line with the consensus forecast. On a twelve-month basis, CPI ticked up to 2.6% (from 2.4% in September).

- Energy prices were flat last month, as a pullback in gasoline prices (-0.9% m/m) was offset by an uptick in electricity costs (+1.0% m/m). Food prices rose 0.2% m/m, following a sharp 0.4% m/m gain in September.

Excluding food and energy, core prices rose 0.3% m/m, matching the two prior-months' gains. The twelve-month change held steady at 3.3%, while the three-month annualized shot higher to 3.6% (from 3.1% in September).

- Price growth on core services were up 0.35% m/m, in line with September's gain. On a year-ago basis, services prices are up 4.8% or roughly two percentage points above its pre-pandemic pace of growth when inflation was running closer to 2%.

- Primary shelter costs rose 0.4% m/m, following a gain of 0.3% m/m in September. While well off its 2023 highs of over 8%, primary shelter costs remain elevated at 5.1% y/y.

Price growth of non-housing services inflation (aka "supercore") remained firm, rising 0.3% m/m – roughly in line with the average gain recorded over the past three months. The continued strength was primarily driven by another strong gain in airline fares (+3.2% m/m), recreational services (+0.7% m/m) and to a lesser extent, medical care services (+0.4% m/m).

Core goods prices were flat in October, after registering a gain the month prior. A pullback in apparel (-1.5% m/m) and education & communication goods (-1.1% m/m) helped to offset a sharp gain in used vehicle prices (+2.7% m/m).

Key Implications

Progress on the inflation front has slowed to a snail's pace in recent months as services inflation is looking increasingly sticky, while much of the disinflationary pressure from fallings goods prices is now in the rear-view mirror. All of this suggests that the last leg lower on returning inflation to the Fed's 2% target is going to occur much more gradually.

From the Fed's standpoint, there was little in this morning's data to get excited about. The three-month annualized rate of change on core inflation jumped to a six-month high, while the six-and-twelve-month rates of change held steady at 2.6 and 3.3% respectively. With inflation progress stalling but the economy still holding up, November's employment report will carry added significance for whether the FOMC continues cutting at its next meeting in December or opts to pause. Following this morning's release, markets are pricing a 70% probability that the Fed cuts next month.

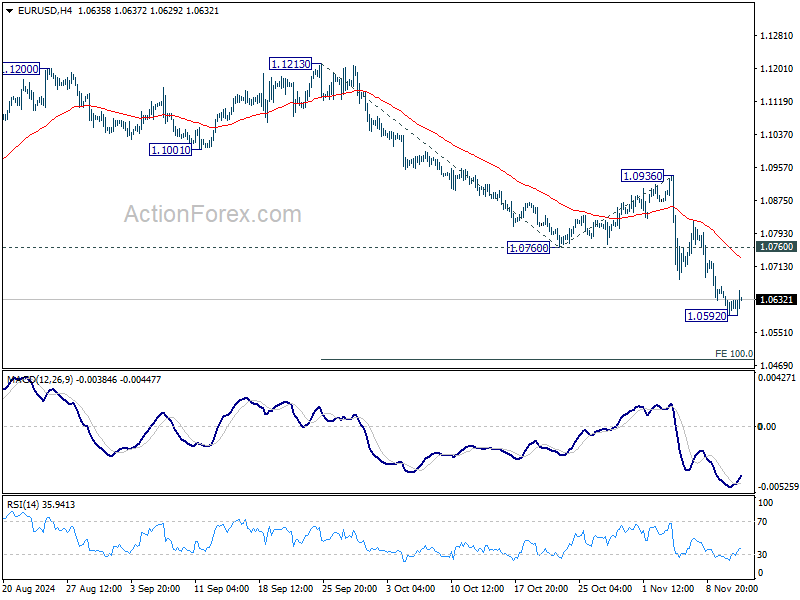

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0591; (P) 1.0627; (R1) 1.0659; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. But further decline is expected as long as 1.0760 support turned resistance holds. Break of 1.0592 temporary low will resume the fall from 1.1213 to 100% projection of 1.1213 to 1.0760 from 1.0936 at 1.0483.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

Dollar Softens Slightly Post-CPI; Focus Turns to Aussie Employment Data

US stock futures have jumped in a relief rally following release of October US CPI data, which, while showing an uptick in headline inflation and steady core inflation, stayed within expectations. This in-line report eases fears of an inflation surprise that could disrupt Fed's gradual easing path. Market sentiment has therefore strengthened, with Fed fund futures still pricing a 70% likelihood of a 25bps rate cut at the December FOMC meeting, indicating that the Fed’s near term rate-cut path remains intact for now.

Following the CPI release, Dollar eased across the board as risk appetite returned, although it maintains its lead as the week's top performer. Canadian Dollar follows as the second strongest, while New Zealand Dollar rounds out the strongest three. Meanwhile, Sterling is the week’s weakest performer, overshadowed by continued caution despite comments from BoE’s top hawk. Euro and Yen also softened. Australian Dollar and Swiss Franc occupy middle ground.

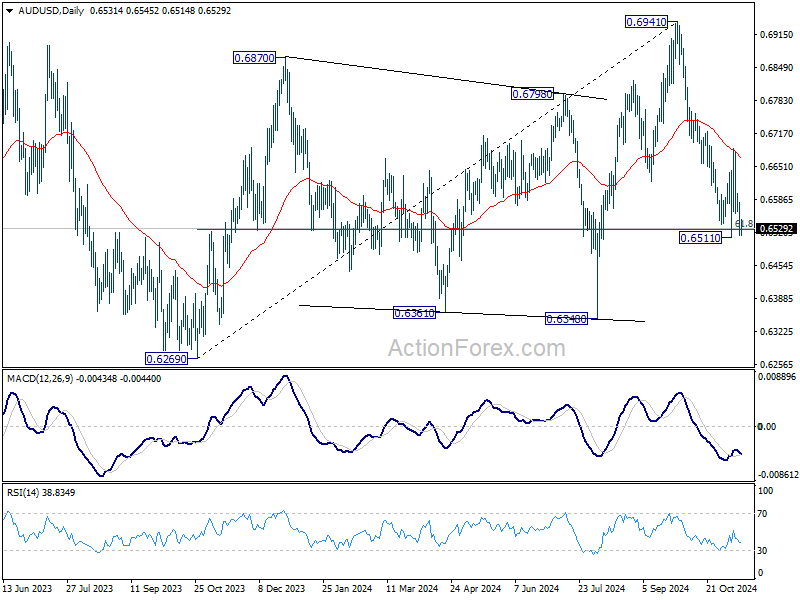

Australia's employment data will be a major focus in the upcoming Asian session while RBA Governor Michele Bullock is scheduled to speak too. Technically, AUD/USD is so far still holding on to 61.8% retracement of 0.6269 to 0.6941 at 0.6526. But prior rejection by falling 55 D EMA is a near term bearish sign. Sustained break of 0.6526 will extend the fall from 0.6941 towards 0.6269/6348 support zone.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is down -0.38%. CAC is down -0.37%. UK 10-year yield is down -0.0419 at 4.469. Germany 10-year yield is up 0.006 at 2.375. Earlier in Asia, Nikkei fell -1.66%. Hong Kong HSI fell -0.12%. China Shanghai SSE rose 0.51%. Singapore Strait Times rose 0.24%. Japan 10-year JGB yield rose 0.0323 to 1.042.

US CPI rises to 2.6% yoy in Oct, core CPI unchanged at 3.3% yoy

US CPI rose 0.2% mom in October while core CPI (ex food and energy) rose 0.3% mom, matched expectations. The index for shelter rose 0.4 mom, accounting for over half of the monthly all items increase. Food index increased 0.2% mom. Energy index was unchanged.

Over the last 12 months, CPI accelerated from 2.4% yoy to 2.6% yoy, matched expectations. Core CPI was unchanged at 3.3% yoy. Energy index decreased -4.9 yoy. Food index increased 2.1% yoy.

BoE's Mann advocates 'activist' approach as inflation not yet been vanquished

BoE MPC member Catherine Mann reiterated her hawkish stance on inflation during a panel discussion today, emphasizing the need for an "activist" approach to monetary policy. Mann expressed that she prefers to wait for more concrete evidence of underlying inflationary pressures easing before considering any policy loosening.

She highlighted the significance of monetary policy's immediate effects on the economy, stating, "Part of my activist strategy is when I move, I will move big."

Mann underscored that while the traditional view of long policy lags—the "olden day story," as she referred to it—still holds some relevance, recent research indicates that rate adjustments can have prompt impacts on firms' pricing decisions and inflation expectations.

As BoE's most hawkish member, Mann maintained her cautious perspective on the inflation outlook. She pointed out the persistence of "pretty sticky" services inflation and cautioned about the potential for increased volatility in prices. "For those two reasons I say that inflation has not yet been vanquished," she concluded.

ECB’s Nagel defends rate path, warns of 1% economic hit from Trump tariffs

In an interview with Die Zeit, German ECB Governing Council member Joachim Nagel reinforced ECB’s current rate path as necessary, citing persistent inflationary pressures, particularly within the services sector due to rising wages.

Nagel emphasized, "We are not exaggerating. There is still noticeable price pressure" .

Nagel also voiced concern over economic fallout from US President-elect Donald Trump’s proposed tariffs, estimating they could trim as much as 1% from Germany’s economic output if enacted.

“If the new tariffs actually materialize, we could even slip into negative territory,” he warned, a worrisome prospect as Germany already faces weak growth projections.

The German economy is anticipated to stagnate through 2024, with growth in 2025 expected to remain below 1%.

ECB’s Villeroy sees more rate cuts as US inflation risks resurface under Trump

French ECB Governing Council member Francois Villeroy de Galhau shared his outlook on inflation and global growth risks today with France Inter, suggesting a period of moderate inflation within France alongside more rate cuts from ECB. He also projected that France’s unemployment rate could temporarily increase to around 8% before stabilizing back to 7%.

Villeroy raised concerns over the inflationary impact of US President-elect Donald Trump’s proposed economic policies, specifically warning that Trump’s program “risks bringing back inflation to the United States.” He suggested this could slow global growth, although the full extent of this impact remains uncertain and could vary between the US, China, and Europe.

A particular focus of Villeroy's remarks was on Trump’s proposed tariffs, which aim to eliminate the US trade deficit by imposing a 10% or higher tax on all imported goods.

Villeroy argued that such protectionist policies could ultimately hurt US consumers, noting, “Protectionism almost always means reduced purchasing power for consumers.”

Japan’s PPI rises 3.4% yoy in Oct, highest since mid-2023

Japan’s PPI rose from 3.1% yoy to 3.4% yoy in October, surpassing market expectations of 3.0% and marking the highest annual increase since July 2023. On a monthly basis, PPI advanced by 0.2%, reflecting sustained inflationary pressure within Japan’s production sector.

The data also revealed a less pronounced decline in Yen-based import prices, down -2.2% yoy compared to a -2.5% drop in September, signaling that import costs may be stabilizing. This relative improvement aligns with a 4.3% mom increase in Yen's exchange rate. However, on a monthly scale, import prices saw a notable 3.0% rise after a -2.8% decrease in September.

Australia's wage growth slows as public sector outpaces private for first time since 2020

Australia's wage growth softened in Q3, with the Wage Price Index rising by 0.8% qoq, slightly missing the forecast of 0.9%. On an annual basis, wage growth slowed from 4.1% yoy to 3.5% yoy, falling short of the expected 3.6% yoy and marking the lowest annual increase since Q4 2022. This deceleration follows four consecutive quarters of 4% or higher wage growth, pointing to easing in wage-driven inflation pressures.

For the first time since late 2020, public sector wage growth surpassed that of the private sector. Public sector wages rose by 3.7% yoy, higher than the 3.5% yoy recorded in the same quarter last year but down from the recent high of 4.2% yoy in Q4 2023, lowest since Q3 2022.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0591; (P) 1.0627; (R1) 1.0659; More...

Intraday bias in EUR/USD is turned neutral first with current recovery. But further decline is expected as long as 1.0760 support turned resistance holds. Break of 1.0592 temporary low will resume the fall from 1.1213 to 100% projection of 1.1213 to 1.0760 from 1.0936 at 1.0483.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

US CPI rises to 2.6% yoy in Oct, core CPI unchanged at 3.3% yoy

US CPI rose 0.2% mom in October while core CPI (ex food and energy) rose 0.3% mom, matched expectations. The index for shelter rose 0.4 mom, accounting for over half of the monthly all items increase. Food index increased 0.2% mom. Energy index was unchanged.

Over the last 12 months, CPI accelerated from 2.4% yoy to 2.6% yoy, matched expectations. Core CPI was unchanged at 3.3% yoy. Energy index decreased -4.9 yoy. Food index increased 2.1% yoy.

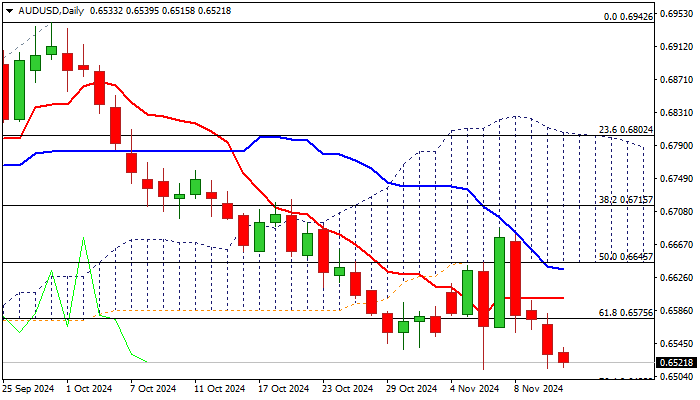

AUD/USD Outlook: US CPI Data in Focus

AUDUSD remains in red for the fourth straight day, but bears slowed on Wednesday and action holding within a narrow range just above three-month low.

Technical studies remain bearish on daily chart and favor further downside, though oversold conditions suggest that consolidation is likely to precede.

Broken daily Tenkan-sen (0.6600) should cap upticks to marks positioning for fresh push lower and attack at 0.6488 Fibo support (76.4% of 0.6348/0.6942).

Only firm break of daily Kijun-sen / cloud base (0.6637/45 respectively) would sideline bears.

Fundamentals, however, are likely to be pair’s key driver today, with Australia’s wage growth slowing in Q3 to the lowest in almost two years, though the data are unlikely to have significant impact on RBA’s stance on interest rates.

Focus is on release of US CPI (Oct y/y 2.6% f/c vs Sep 2.4%; core Oct 3.3% f/c, unchanged from Sep), which will be key driver today and Australia’s Oct labor report (due early Thursday).

Res: 0.6537; 0.6575; 0.6600; 0.6637.

Sup: 0.6512; 0.6488; 0.6400; 0.6348.

Euro Under Pressure, US Inflation Next

The euro is lower for a fourth straight trading day and has deUS clined 0.10% on the day, trading at 1.0612 at the time of writing. Earlier today, the euro dropped below the 1.06 line for the first time since November 2023.

US CPI expected to rise to 2.6%

The US releases the October inflation report later today. Headline CPI is expected to rise to 2.6% y/y, up from 2.4% in September. The monthly rate is projected to remain at 0.2%. The core rate is also expected to stay unchanged from September, at 3.3% y/y and 0.3% m/m.

If headline inflation moves higher as expected, the markets could respond by trimming the probability of a rate cut at the Dec. 18 meeting. The current market pricing for a 25-basis point cut is 58%, down from 68% a day ago. This means that investors are not sold on a rate cut at the final meeting of the year. The US economy is in good shape but underlying inflation remains above the 2% target and the labor market has been cooling. Today’s inflation report could be a key factor in the rate decision at the December meeting.

Will ECB lower rates in December?

The European Central Bank meets on Dec. 12 and there are differing opinions among Governing Council members as to the timing of another rate cut. Inflation has been falling, but it the pace fast enough to warrant a rate cut at the December meeting? Some voices have been calling for a jumbo 50-basis point cut in December, while more dovish members want to wait until early next year.

The most recent development which the ECB must contend with is the Trump election win, which could mean US tariffs on European goods. Governing Council member Robert Holzmann said on Tuesday that if Trump enacted tariffs, the US dollar would rise against the euro and that would put upward inflation on eurozone inflation and make it more difficult for the ECB to achieve its 2% target.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0627. Above, there is resistance at 1.0659

- 1.0591 is the next line of support, which has held since November 2023. Below, there is support at 1.0559

BoE’s Mann advocates ‘activist’ approach as inflation not yet been vanquished

BoE MPC member Catherine Mann reiterated her hawkish stance on inflation during a panel discussion today, emphasizing the need for an "activist" approach to monetary policy. Mann expressed that she prefers to wait for more concrete evidence of underlying inflationary pressures easing before considering any policy loosening.

She highlighted the significance of monetary policy's immediate effects on the economy, stating, "Part of my activist strategy is when I move, I will move big."

Mann underscored that while the traditional view of long policy lags—the "olden day story," as she referred to it—still holds some relevance, recent research indicates that rate adjustments can have prompt impacts on firms' pricing decisions and inflation expectations.

As BoE's most hawkish member, Mann maintained her cautious perspective on the inflation outlook. She pointed out the persistence of "pretty sticky" services inflation and cautioned about the potential for increased volatility in prices. "For those two reasons I say that inflation has not yet been vanquished," she concluded.

ECB’s Nagel defends rate path, warns of 1% economic hit from Trump tariffs

In an interview with Die Zeit, German ECB Governing Council member Joachim Nagel reinforced ECB’s current rate path as necessary, citing persistent inflationary pressures, particularly within the services sector due to rising wages.

Nagel emphasized, "We are not exaggerating. There is still noticeable price pressure" .

Nagel also voiced concern over economic fallout from US President-elect Donald Trump’s proposed tariffs, estimating they could trim as much as 1% from Germany’s economic output if enacted.

“If the new tariffs actually materialize, we could even slip into negative territory,” he warned, a worrisome prospect as Germany already faces weak growth projections.

The German economy is anticipated to stagnate through 2024, with growth in 2025 expected to remain below 1%.

Is Trump’s Election the End of Gold’s Bull Run?

- Trump’s election invites gold bears into the game

- Bets of slower rate cuts by the Fed may be the main driver

- PBoC pauses purchases, but strategy likely not changed

- Speculation around geopolitics may also be weighing

Trump wins but gold loses

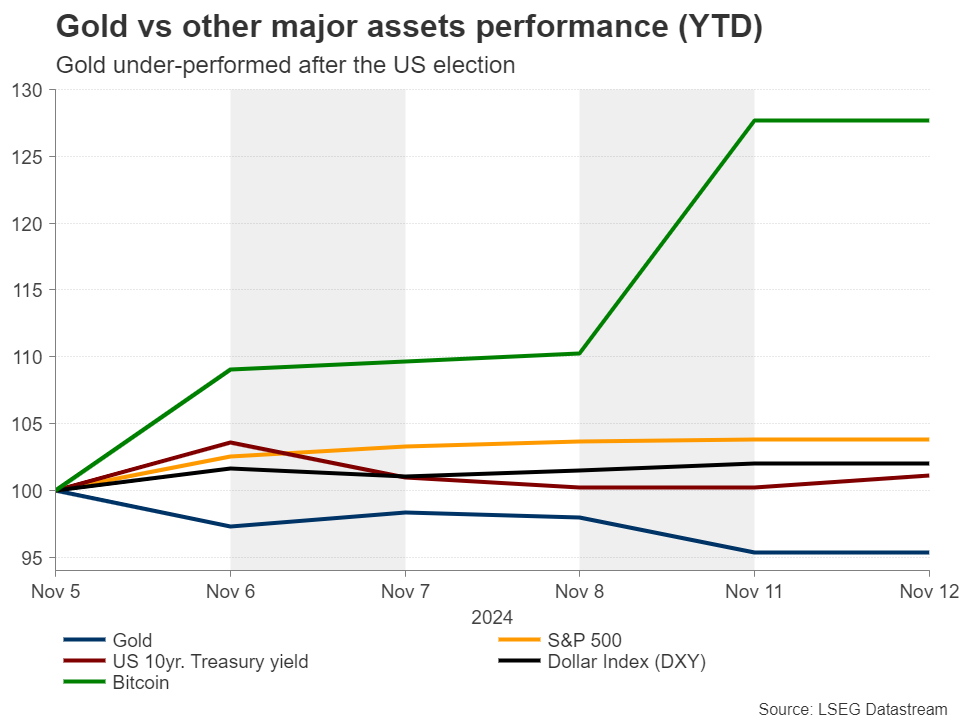

After hitting a record high of around $2,790 on October 30, gold entered a corrective phase due to US data suggesting that the Fed may need to slow down the pace of its future interest rate reductions.

The correction of the precious metal accelerated on the first signs that Donald Trump will be the 47th president of the US, with the bears staying in charge as the financial world continued to pile into the so-called ‘Trump Trade.’

But is the pullback in gold actually part of the ‘Trump trade’? Because ahead of the election, the precious metal was benefiting whenever the chances of Trump returning to the White House were increasing, perhaps due to the uncertainty surrounding a Trump presidency.

Yet, currently, gold seems to be surrendering to the stronger dollar, which is likely benefiting from speculation that Trump’s tax cut and tariff policies will fuel inflation and thereby prompt the Fed to proceed with even slower rate reductions.

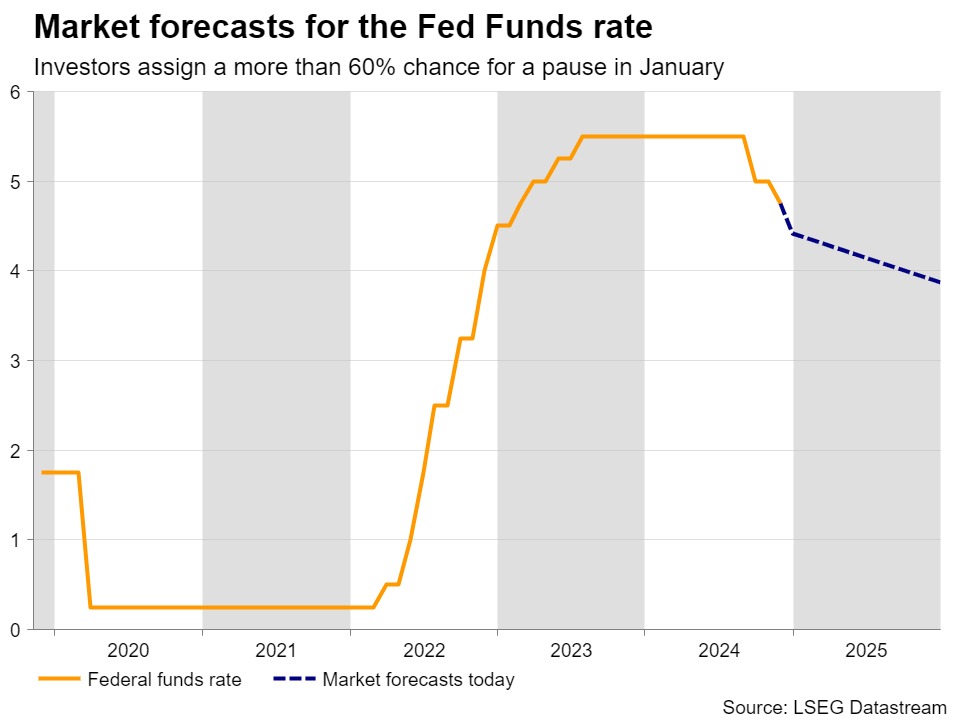

Just after the election, the probability for policymakers stepping to the sidelines in December rose to slightly above 30%. Now, it rests at around 15%, with the probability of taking a pause in January rising to around 63%.

Besides Fed, China and geopolitics are also eyed

Before the US election even started being a theme for financial markets, gold’s main drivers were elevated purchases by major central banks, especially the People’s Bank of China, safe-haven inflows due to geopolitical tensions in the Middle East, as well as speculation of aggressive rate cuts by the Fed.

It is worth mentioning that just after September’s 50bps reduction, investors were assigning a strong chance for a back-to-back double cut in November, although this changed later due to the better-than-expected US data and the increasing chances of Trump winning the election.

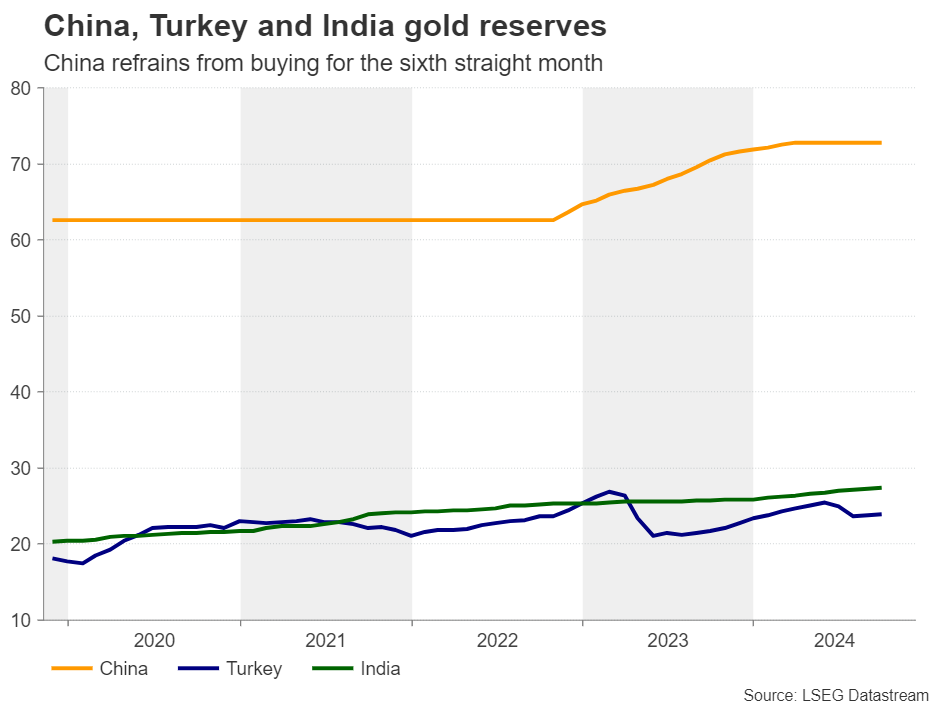

China refrains from buying for the sixth straight month

According to the World Gold Council, central bank purchases of the precious metal may be set to slow further due to a six-month abstain by the Chinese central bank. Its holdings held steady at 72.8mn troy ounces, although the Bank’s value of gold reserves rose to $199bn from $191bn.

But Trump’s return to the White House is likely adding to the chances of China resuming its purchases. After all, the central bank of the world’s second-largest economy has been piling up gold so that it loosens its dependence on the US dollar in case tensions between the US and China escalate. And with Trump pledging to impose massive tariffs on Chinese goods, a Trade War 2.0 seems increasingly likely.

So, China is unlikely to have changed its strategy. They may prefer to wait and buy more gold at more favorable prices.

Can Trump restore peace in Europe and the Middle East?

In terms of geopolitics, some investors may have started unwinding their safe-haven holdings in hopes that as the new US president, Donald Trump will try to resolve the conflicts in the Middle East and Ukraine. However, anything suggesting that a truce may not be so easily achievable, could very well refuel the yellow metal’s prevailing uptrend.

Broader uptrend remains intact

From a technical standpoint, gold corrected sharply lower this month, but it is still holding above the uptrend line drawn from the low of October 6, 2023. This corroborates the view that the current retreat may be destined to stay limited and short lived.

The bulls may decide to jump back into the action from near the crossroads of the uptrend line and the $2,545 zone and perhaps aim for the high of September 26 at $2,685. Should they not stop there, they could aim once again, and even exceed, the record high of $2,790.

For the outlook to shift to bearish, the metal may need to slide below the crossroads of the $2,545 barrier and the aforementioned uptrend line. Such a technical dip may pave the way for the key pivot zone of $2,390, the break of which could carry extensions towards the $2,285 territory, which acted as a floor between April and June.

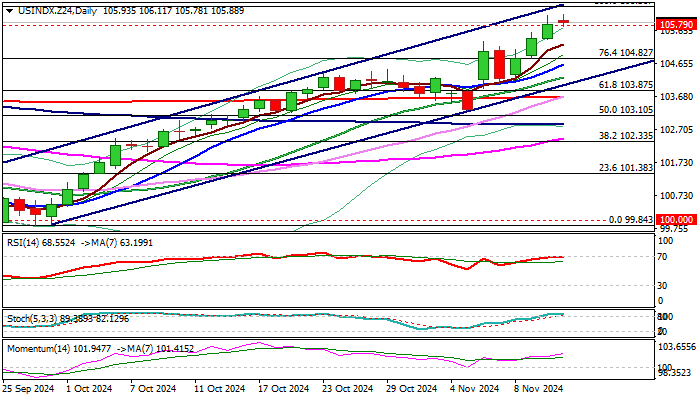

Dollar Index Outlook: Bulls Reduce Speed Ahead of US Inflation Data

The Dollar index keeps firm tone and holding above former top 105.79 but near term action turned to the quiet mode in early Wednesday, ahead of key economic event today – US inflation data.

Recent strong bullish acceleration after the dollar was lifted by US election results (so-called Trump trades) has slowed, as markets look for fresh signals from CPI numbers which will subsequently affect Fed’s stance on interest rates.

However, the new reality after Trump’s election victory and anticipated impact of policies he plans to implement, implies that Fed is unlikely to go for initially planned strong policy easing, but will likely look to adjust its action to expected stronger economic growth and elevated inflation.

This sets stage for further Dollar’s advance with initial target at 106.36 (May 1 peak) and more significant barriers at 107.00 zone (Oct 2023 lower platform /ceiling of a larger range / 50% retracement of 114.72/99.20 downtrend)., violation of which to signal an end of broader range and open way for stronger gains.

Technical picture is firmly bullish on daily chart positive momentum is strong and MA’s in bullish setup and formed a number of bull-crosses, with price action holding near the upper borderline of a bull-channel (106.41).

However overbought conditions may keep bulls on hold for consolidation, with likely shallow dips to offer better levels to re-enter bullish market.

Former top (105.79) marks immediate support, followed by 5DMA (105.22) and broken Fibo 76.4% level (104.82).

Res: 106.41; 106.96; 107.03; 107.88.

Sup: 105.79; 105.22; 104.82; 104.62.