Sample Category Title

Australian Dollar Eyes Employment Data

The Australian dollar is steady on Wednesday. In the European session, AUD/USD is trading at 0.6525, down 0.12% on the day.

Australia’s wage inflation within expectations

Wage inflation in Australia eased to 3.5% y/y in the third quarter, down from 4.1% in Q2 and just shy of the market estimate of 3.6%. This was the weakest wage price growth since Q4 2022. Quarterly, wage growth remained at 0.8% in the third quarter, below the market estimate of 0.9%.

The data is in line with the Reserve Bank of Australia’s projection that wage growth has peaked. The central bank expects wages to continue to easing in the fourth quarter and next year, which supports the case for a rate cut. The RBA has insisted that a rate hike remains on the table as underlying inflation is too high. The decline in wage growth is an encouraging sign as high wages have driven services inflation, which remains much higher than the 2% inflation target.

The RBA’s hawkish stance has put it out of sync with other major central banks are lowering rates in response to falling inflation. The markets have priced in another hold in rates at the December meeting, with an initial rate cut likely in the first half of 2025.

Australia releases the October employment report on Thursday. The economy is expected to have added 25 thousand jobs, after a sparkling 64.1 thousand gain in September, most of which was full-time employment. The unemployment rate is expected to remain unchanged at 4.1%.

In the US, Minneapolis Fed President Neel Kashkari said on Wednesday that the US economy is in a “good place” and that monetary policy is currently “modestly restrictive”. Kashkari added that economic data would be the guide as to the Fed’s rate path.

AUD/USD Technical

- There is support at 0.6505 and 0.6475

- 0.6543 and 0.6573 and the next resistance lines

XAU/USD Analysis: Gold Price Drops to $2,600 per Ounce

On November 4, when gold was trading around $2,750, we observed bearish signals on the XAU/USD chart.

Since then, the price has declined to the $2,600 level, briefly dipping below it — the lowest price since mid-September.

According to Trading Economics, investors may be losing interest in gold for several reasons:

→ Strong U.S. Dollar: A robust dollar reduces gold's appeal as a safe-haven asset.

→ Optimism Following Trump’s Election: Market participants are reacting to Trump’s fiscal and monetary policy pledges, shifting toward riskier assets.

→ Upcoming Key U.S. Inflation Data: The CPI data, expected today at 16:30 GMT+3, may reveal no unexpected negative trends.

Today’s XAU/USD technical analysis shows that:

→ Gold’s price is at the lower boundary of the blue channel, which has been extended to reflect recent trading data.

→ The channel’s median line has shifted from support to resistance (shown with arrows).

It is possible that today’s inflation news may catalyse one of two scenarios on the XAU/USD chart:

→ Bullish Rebound: Buyers may attempt to resume an uptrend from the lower boundary of the blue channel, facing resistance around $2,655.

→ Bearish Control: Sellers may continue to dominate, potentially making the blue channel less relevant as price stabilises below $2,600.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

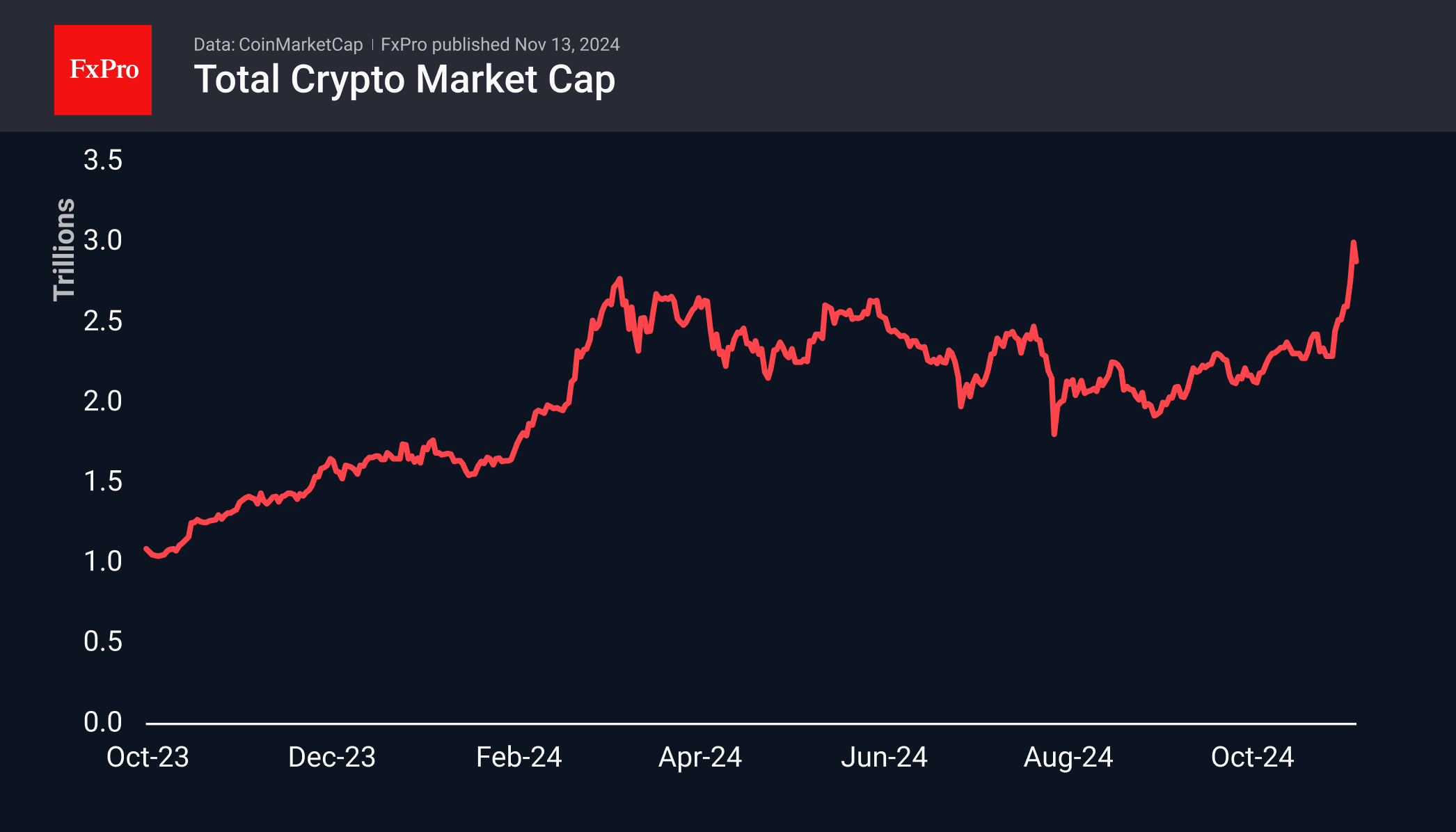

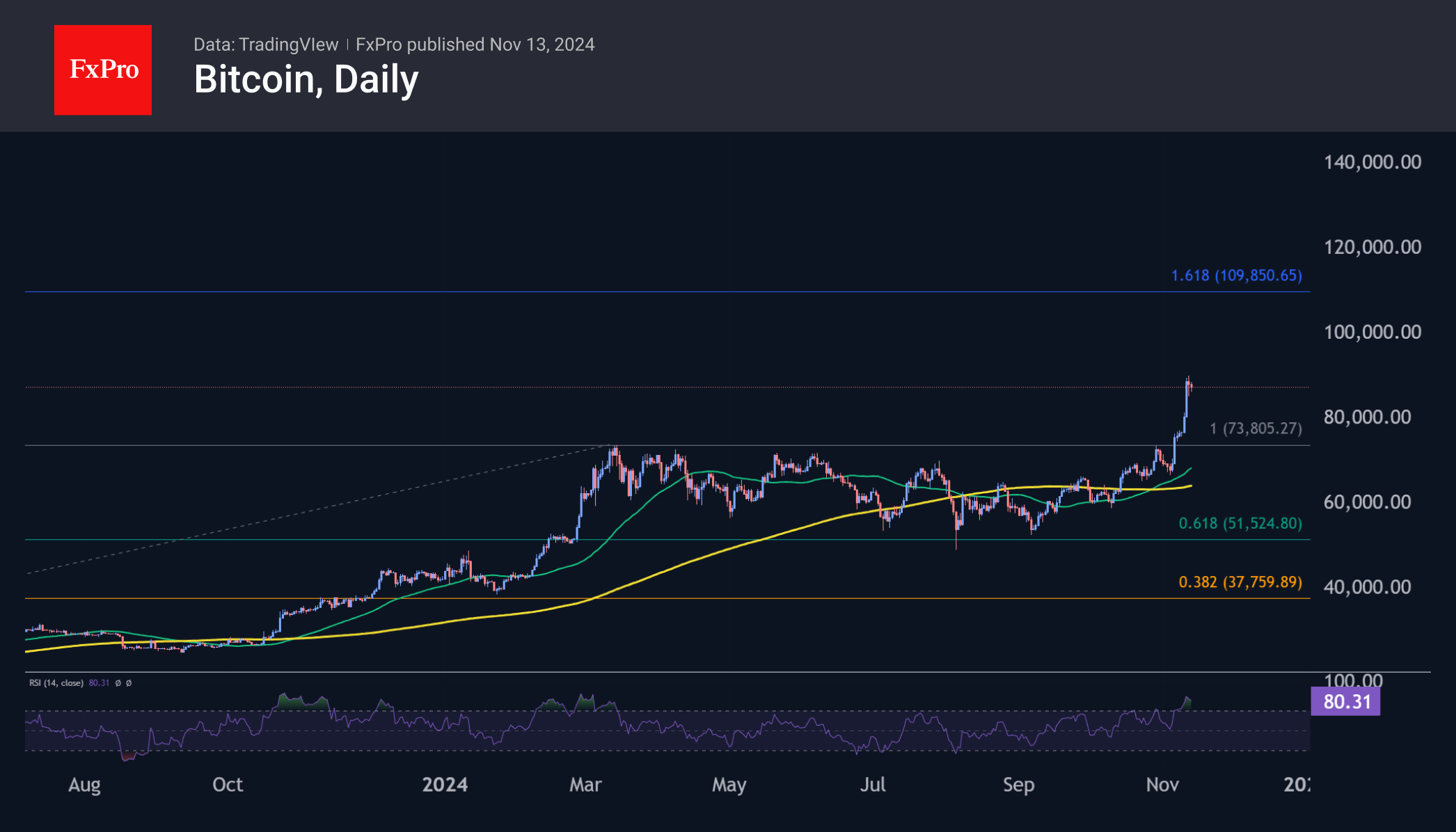

Crypto Market Locks in Weekly Rally

Market Picture

The crypto market cap fell to $2.88 trillion, down 5% over the day. It appears that the market has started to take profits after a week of rallying. The first target for such a pullback appears to be the March-June resistance area around $2.70 trillion. However, we are optimistic that the market may well pick up cryptocurrencies at higher levels and trigger FOMO.

Bitcoin kept things interesting on Tuesday, starting the day by testing the $90K level, then dropping to $85K before testing $90K again. On Wednesday morning, the price pulled back to $87K, the first significant daily decline in eight days. Technically, a pullback to $84K or even $81K would fit within the correction pattern of the last impulse. In that case, a broader correction could begin. For now, however, we believe the market has stumbled and could quickly return to growth.

News Background

Amid the rapid rise of cryptocurrencies, tech analyst Ali Martinez noted an ‘explosion of institutional FOMO’, citing Bernstein’s recent positive report. ‘We are literally starting the dot-com cycle for cryptocurrencies,’ said Michael van de Poppe, founder of MN Trading.

On 11 November, MicroStrategy shares hit a new all-time high of $351.7, taking its YTD growth rate to 438%. Coinbase shares have been at their highest since November 2021. The exchange’s shares have jumped 75% in the last five days.

Arkham Intelligence notes that 2,500 BTC ($222m) were sent to two unknown addresses from the wallets of the former Mt.Gox. This is the fifth Bitcoin transaction in the last two weeks, totalling more than $2 billion.

Polymarket users are betting that bitcoin will reach $100K by the end of November. The proportion of such bets has reached 57%.

Tesla’s Bitcoin value has exceeded $1 billion. The company holds 11,509 BTC. According to Arkham data, El Salvador’s Bitcoin assets exceeded $500 million. The country holds 5,932 BTC.

ECB’s Villeroy sees more rate cuts as US inflation risks resurface under Trump

French ECB Governing Council member Francois Villeroy de Galhau shared his outlook on inflation and global growth risks today with France Inter, suggesting a period of moderate inflation within France alongside more rate cuts from ECB. He also projected that France’s unemployment rate could temporarily increase to around 8% before stabilizing back to 7%.

Villeroy raised concerns over the inflationary impact of US President-elect Donald Trump’s proposed economic policies, specifically warning that Trump’s program “risks bringing back inflation to the United States.” He suggested this could slow global growth, although the full extent of this impact remains uncertain and could vary between the US, China, and Europe.

A particular focus of Villeroy's remarks was on Trump’s proposed tariffs, which aim to eliminate the US trade deficit by imposing a 10% or higher tax on all imported goods.

Villeroy argued that such protectionist policies could ultimately hurt US consumers, noting, “Protectionism almost always means reduced purchasing power for consumers.”

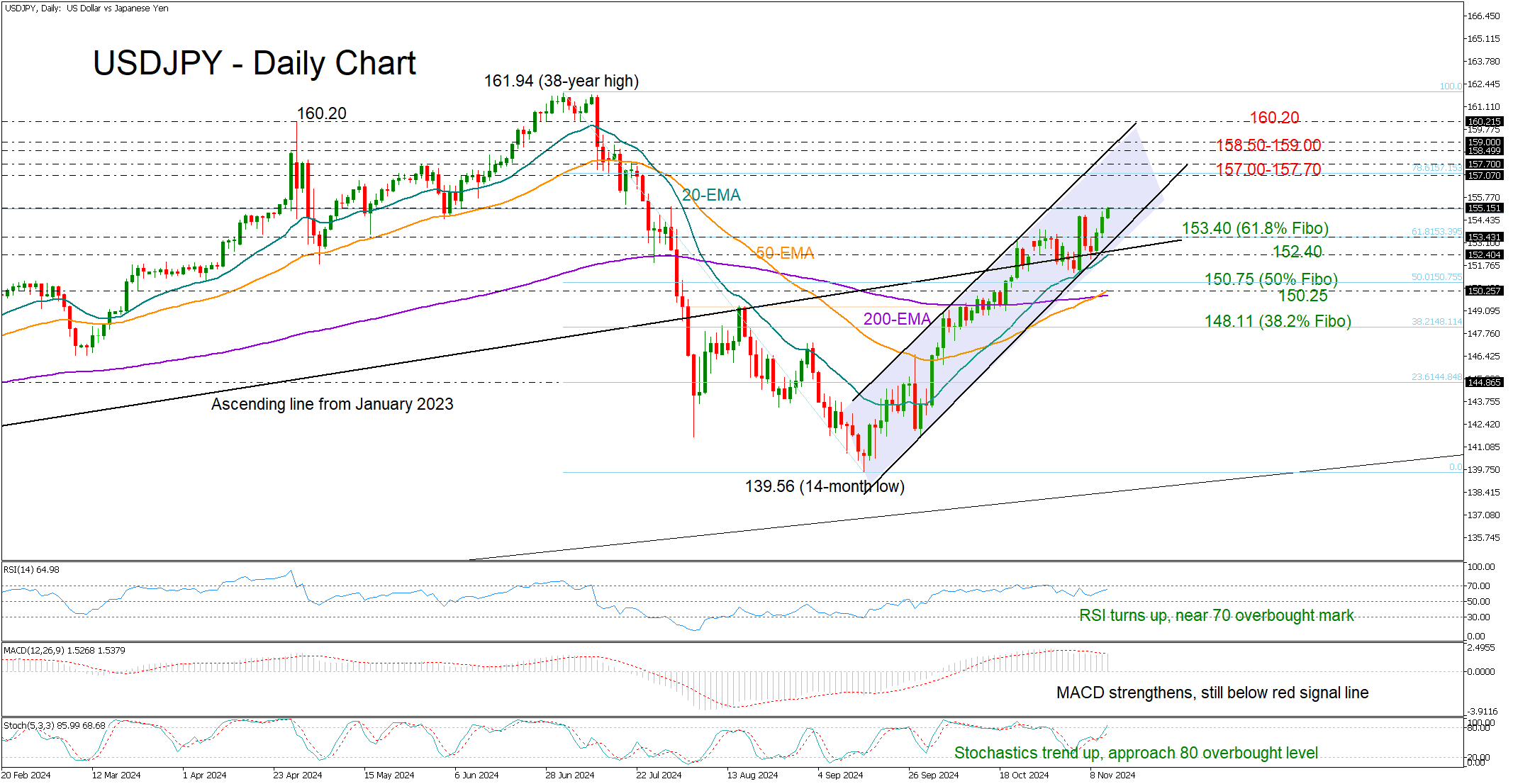

USDJPY Stretches Uptrend into 155 Area

- USDJPY resumes uptrend, unlocks 3½-month high

- Short-term bias is positive; July’s barrier could pose a test

USDJPY broke into the 155.00 territory for the first time since July, reigniting optimism that the upleg which started in mid-September has more room to run.

That said, the pair seems to be facing an obstacle near the 155.20 level – the same zone that sparked a sharp downfall at the end of July. With the RSI and stochastic oscillator edging toward overbought territory, a potential slowdown or consolidation could be on the cards.

Hence, for the bulls to maintain momentum, they'll need to decisively pierce through the 155.20 wall. Such a move could pave the way for the next target range around 158.50-159.00, where the upper boundary of the upward-sloping channel lies. From there, the 160.20 mark could be the next major hurdle.

Otherwise, a pullback could initially take a halt somewhere between the 61.8% Fibonacci retracement of the previous downleg at 153.40 and the 20-day exponential moving average (EMA) at 152.40. If the bears breach that floor, confirming a negative shift in market sentiment, the spotlight may immediately fall on the 50% Fibonacci mark of 150.75 and the 50- and 200-day EMAs. Further downside could see the pair test the 38.2% Fibonacci level at 148.11.

In summary, USDJPY is back in an uptrend, though for a continuous rally, the bulls must successfully close above the 155.20 barrier.

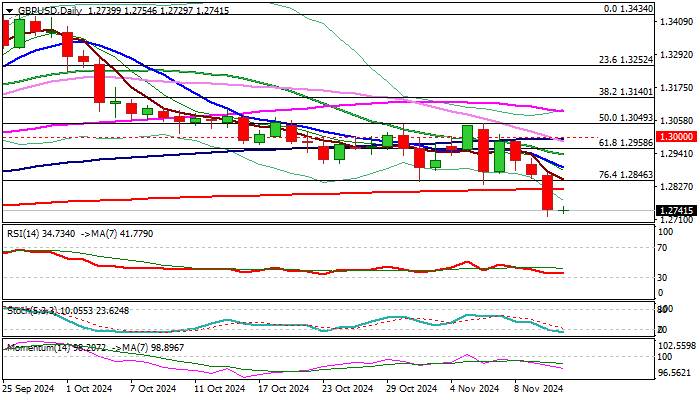

GBP/USD Outlook: Bears Take a Breather After Sharp Three-Day Fall

Cable is holding within a narrow consolidation in early Wednesday’s trading as bears started to run out of steam after steep fall (down 1.85%) in past three days.

Tuesday’s break and close well below pivotal supports at 1.2846 (Fibo 76.4% of 1.2664/1.3434 / former base) and 1.2817 (200DMA) generated strong bearish signal.

Markets await release of US inflation data for October (due later today) for fresh signals that keeps the pair in a quiet mode this morning.

Broken 200DMA / Fibo reverted to resistances which should ideally cap upticks to keep larger bears intact and guard falling 10DMA (1.2894) and 20DMA (1.2938) violation of which would question bears and risk test of upper breakpoint at 1.3000 (psychological / 100DMA).

Res: 1.2776; 1.2817; 1.2846; 1.2894.

Sup: 1.2719; 1.2664; 1.2612; 1.2599.

USD/JPY at a Three-Month Peak: No One Opposes the US Dollar

The USD/JPY currency pair has climbed to a three-month high of 154.87, driven by the strengthening US dollar following Donald Trump’s election victory. Markets anticipate that Trump’s protectionist policies, which are expected to bolster the US economy, might also fuel inflation, prompting the Federal Reserve to maintain higher interest rates than previously anticipated.

In Japan, producer prices rose at their fastest pace in 14 months in October, signalling persistent inflation pressures. Attention is shifting towards Japan’s GDP data for Q3 2024, set to be released on Friday, which will provide further insight into the economic trends affecting the yen.

The Bank of Japan is under scrutiny as it contemplates an interest rate increase to 1% per annum during the first half of fiscal 2025. However, Japanese monetary authorities remain cautious, considering the external economic factors and the challenges posed by persistent inflation.

Technical analysis of USD/JPY

On the H4 USD/JPY chart, the market continues developing the third wave of growth to the level of 156.15. After reaching this level, we will consider the probability of the start of correction to the level of 154.15. Further, we expect the beginning of a new wave of growth to the level of 157.00. Technically, this scenario is confirmed by the MACD indicator. Its signal line is above the zero level and is directed upwards.

On the H1 USD/JPY chart, the market has formed a consolidation range around the 154.15 level and continues developing the wave to 156.15 with an upward exit. After reaching this level, we expect a correction towards 154.15, initially targeting 155.20. Technically, this scenario is confirmed by the Stochastic oscillator. Its signal line is above the level of 50 and is directed upwards.

Euro Hits Yearly Lows, Pound Dips Below 1.2800

Looking at recent moves in major currency pairs, it’s clear that market participants have come to terms with Donald Trump's victory in the U.S. presidential election and are starting to prepare for changes to the global economic landscape. Among the new president’s campaign promises was the introduction of additional tariffs on imports to the U.S. For instance, Trump has proposed around a 25% tariff on Mexican imports and a range of 10% to 20% for goods from European nations. Unsurprisingly, the prospect of potential trade wars is impacting the pricing of pairs such as EUR/USD and GBP/USD.

EUR/USD

The Euro has been in decline for the second consecutive week. Yesterday, it hit a new yearly low near 1.0600 but found support at 1.0590, bouncing slightly. If the 1.0600-1.0580 range turns into resistance, the pair may test the lows seen in 2023, around 1.0520-1.0460. A sustained upward move is likely only if the pair firmly clears 1.0730-1.0680.

The following news could significantly influence EUR/USD pricing:

- Today at 11:00 (GMT +3), a European Central Bank meeting on non-monetary policy

- Today at 13:30 (GMT +3), Germany's 10-year treasury bond auction

- Today at 16:30 (GMT +3), release of the U.S. core consumer price index (CPI)

GBP/USD

Yesterday, GBP/USD sellers broke through a critical support range at 1.2830-1.2800, with the price declining to 1.2720 before correcting to 1.2760. The price’s behavior around the 1.2800-1.2760 range will be key for identifying the next trend. A rejection at this level may lead to further declines towards 1.2720-1.2700, while a break above 1.2800 could signal the start of an upward correction.

Key events that could affect GBP/USD today:

- 12:45 (GMT +3) – Speech by Bank of England Monetary Policy Committee member Catherine Mann

- 13:00 (GMT +3) – Release of data on the sale of 4-year treasury securities in the UK

- 21:30 (GMT +3) – Speech by Federal Reserve official Jeffrey Schmid

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Elliott Wave View on DAX Looking for Larger Degree Correction

Short Term Elliott Wave View in DAX suggests rally to 19670 ended wave ((3)). Wave ((4)) pullback is currently in progress as a double three Elliott Wave structure. Down from wave ((3)), wave (i) ended at 19451.7 and rally in wave (ii) ended at 19591.5. Wave (iii) lower ended at 19368.69 and wave (iv) rally ended at 19468.6. Final wave (v) lower ended at 19330.1 which completed wave ((a)). Rally in wave ((b)) ended at 19643.12 with internal subdivision as a zigzag. Up from wave ((a)), wave (a) ended at 19555.45 and wave (b) ended at 19399.16. Wave (c) higher ended at 19643.12 which completed wave ((b)) in higher degree.

Wave ((c)) lower ended at 19004.97 which completed wave W in higher degree. Up from wave W, wave ((a)) rally ended at 19297.6 and wave ((b)) ended at 19104.59. Wave ((c)) higher ended at 19563.97 which completed wave X in higher degree. Index has turned lower in wave Y with internal subdivision as a zigzag structure. Down from wave X, wave ((a)) ended at 19007.88. Wave ((b)) rally ended at 19456.9 and Index has turned lower. Near term, as far as pivot at 19669.9 high stays intact, expect Index to extend lower.

DAX 60 Minutes Elliott Wave Chart

DAX Elliott Wave Video

https://www.youtube.com/watch?v=rclDuhY9QCs

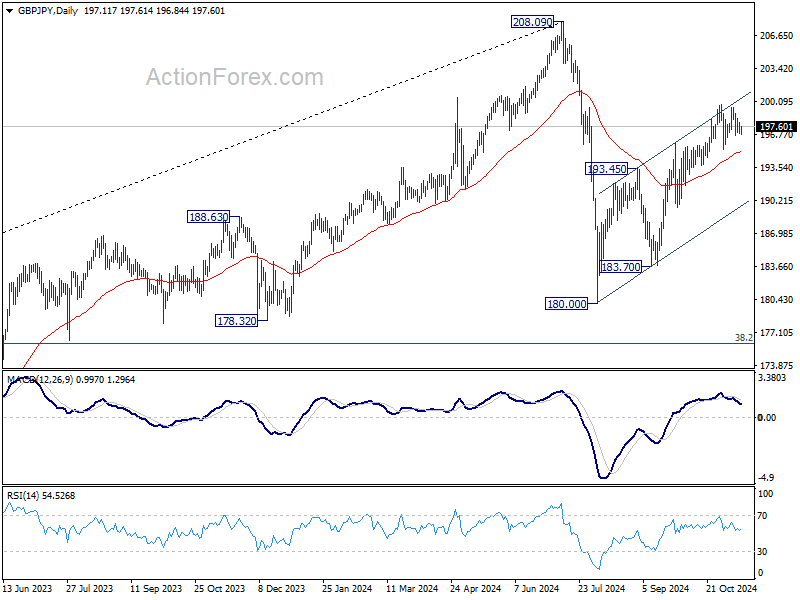

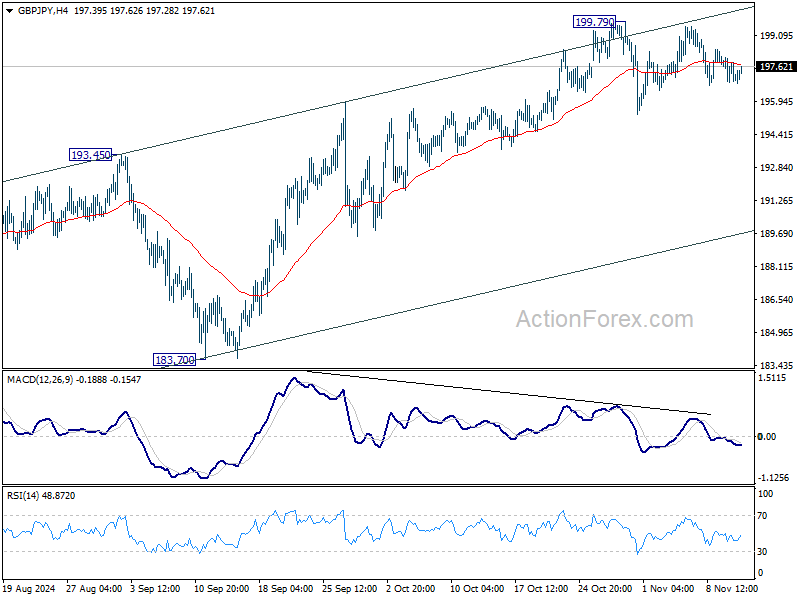

GBP/JPY Daily Outlook

Daily Pivots: (S1) 196.64; (P) 197.36; (R1) 197.82; More...

GBP/JPY continues to trade sideway and intraday bias remains neutral. Further rally is expected as long as 55 D EMA (now at 195.05) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.