Sample Category Title

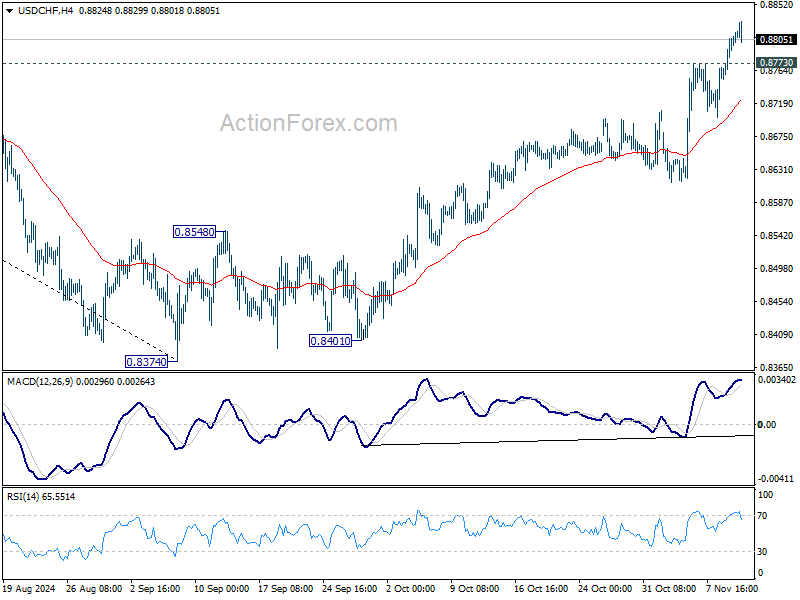

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8770; (P) 0.8790; (R1) 0.8790; More…

USD/CHF's rally is in progress and intraday bias stays on the upside. Current rise from 0.8374 should target 61.8% retracement of 0.9223 to 0.8374 at 0.8899. Sustained trading above there will pave the way towards 0.9223 high. On the downside, below 0.8773 support will turn intraday bias neutral again and bring consolidations first, before staging another rally.

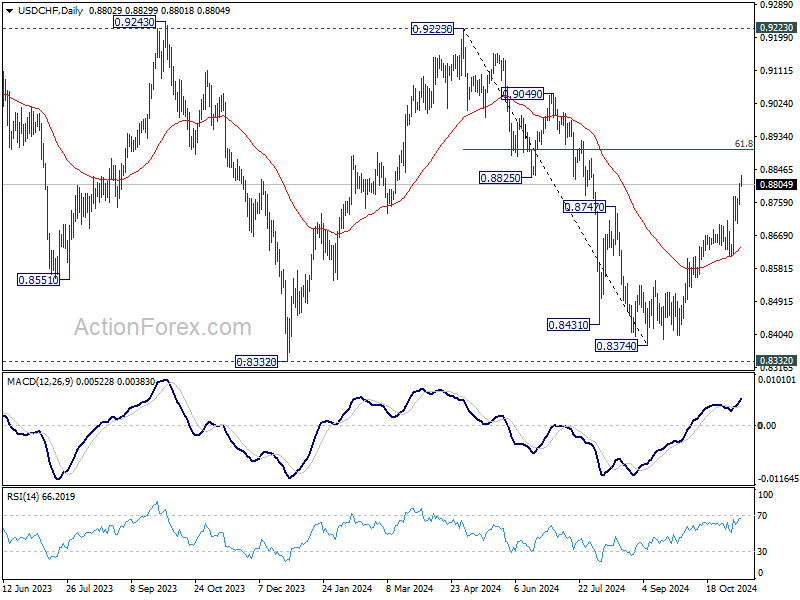

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

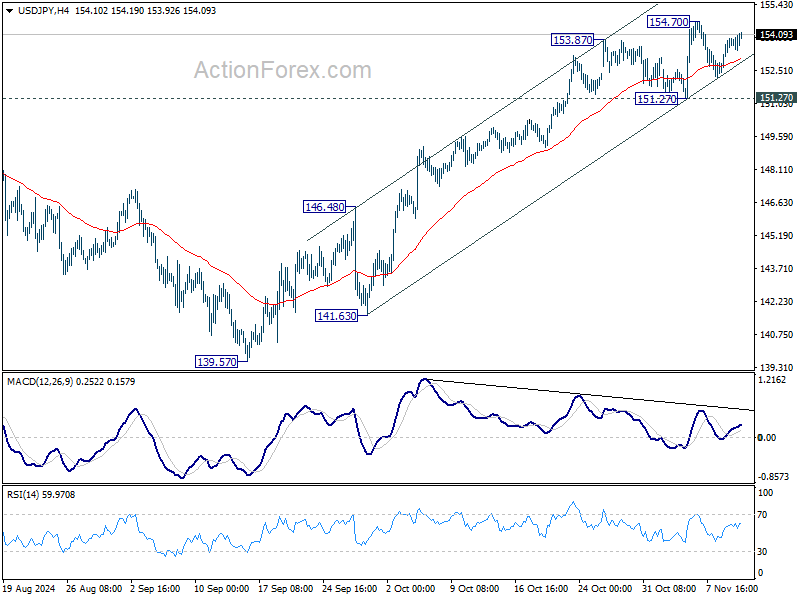

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.93; (P) 153.44; (R1) 154.25; More...

USD/JPY is staying in range below 154.70 and intraday bias remains neutral. Further rise is expected as long as 151.27 support holds. Above 154.70 will resume the rally from 139.57 towards 161.94 high. However, considering bearish divergence condition in 4H MACD, break of 151.27 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 149.89).

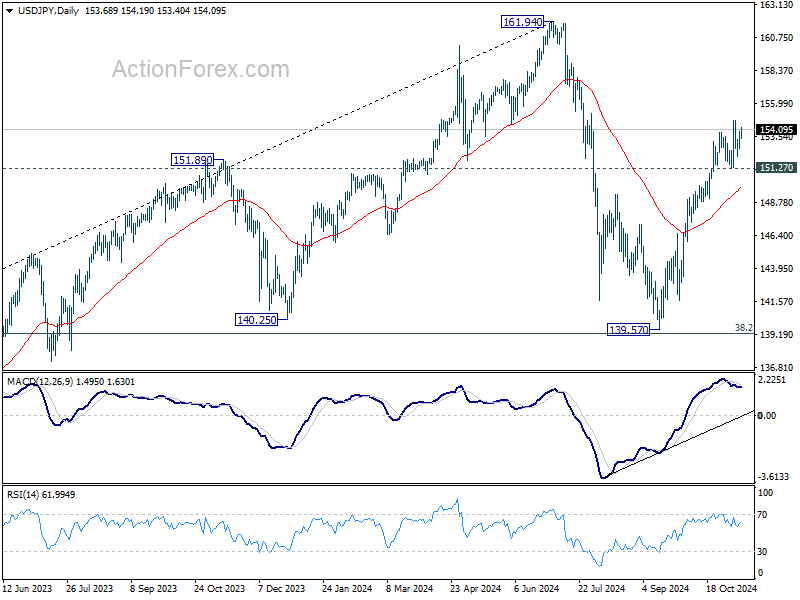

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

BoE’s Pill cites persistent pay growth and underlying inflationary pressures

At a conference today, BoE Chief Economist Huw Pill referred to today's UK labor market data, noted that wage growth remains "quite sticky at elevated levels," which he characterized as "hard to reconcile" with the inflation target, given current productivity growth expectations.

While acknowledging the significant disinflation seen in recent months, which has allowed for a reduction in monetary policy restrictions, Pill cautioned that "does not mean it is job done".

He emphasized that despite some easing in headline inflation, “some underlying inflationary pressures” persist in the UK economy.

German ZEW slumps to 7.4, domestic political uncertainty and US election outcome

German ZEW Economic Sentiment index took a significant hit in November, plunging from 13.1 to a mere 7.4, sharply missing expectations of 13.2. Current Situation Index also declined, falling from -86.9 to -91.4, below the anticipated -86.0.

The broader Eurozone felt the impact as well, with its ZEW Economic Sentiment index dropping from 20.1 to 12.5, and the Current Situation Index slipping by 3.0 points to 43.8.

ZEW President Achim Wambach highlighted that the drop in German economic expectations was heavily influenced by two recent developments: Donald Trump’s election victory and the collapse of Germany’s government coalition.

According to Wambach, “Economic sentiment has declined – and the outcome of the US presidential election is likely to be the main reason for this.” The survey data reflect rising optimism toward the US, while sentiment for China and Eurozone continues to deteriorate, reinforcing concerns of broader instability.

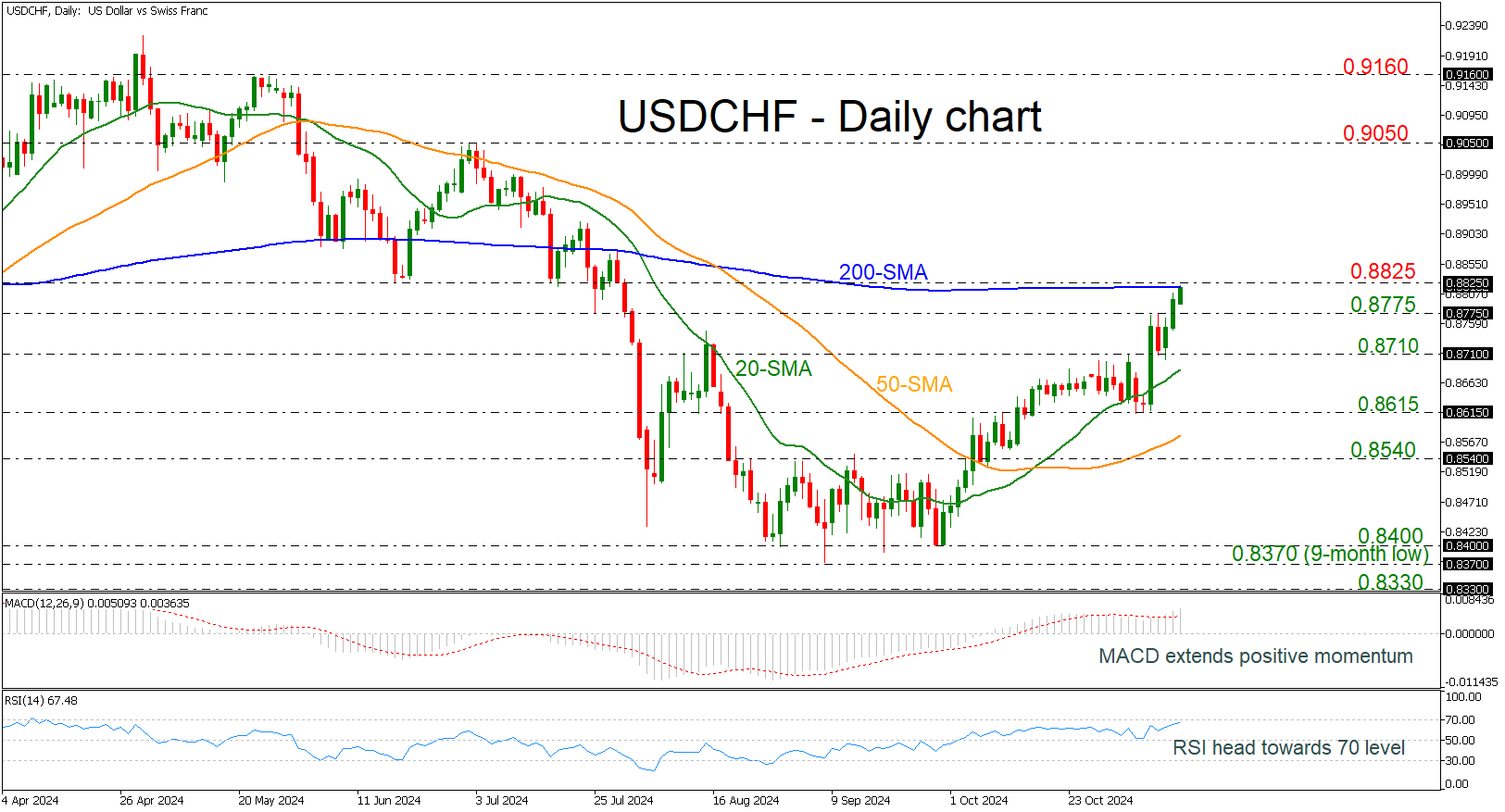

USDCHF Struggles at 200-day SMA

- USDCHF has been rallying since end of September

- MACD and RSI seem to be strongly positive

USDCHF is finding immediate strong resistance at the 200-day simple moving average (SMA) at 0.8816, recording a new three-and-a-half-month high. The momentum oscillators are confirming aggressive buying interest in the market, as the MACD is strengthening its movements above its trigger and zero lines, while the RSI is approaching the 70 level.

If the market successfully overcomes the 0.8825 restrictive region, then it may rally until the 0.9050 barricade.

Alternatively, a slip below the previous high of 0.8775 could send traders toward the 0.8710 support and the 20-day SMA at 0.8680. Even lower, the market could switch to neutral, touching the lows of 0.8615 and the 50-day SMA at 0.8580.

In a nutshell, USDCHF has been creating a strong bullish run since the end of September, and a rise beyond the 200-day SMA would endorse the positive scenario.

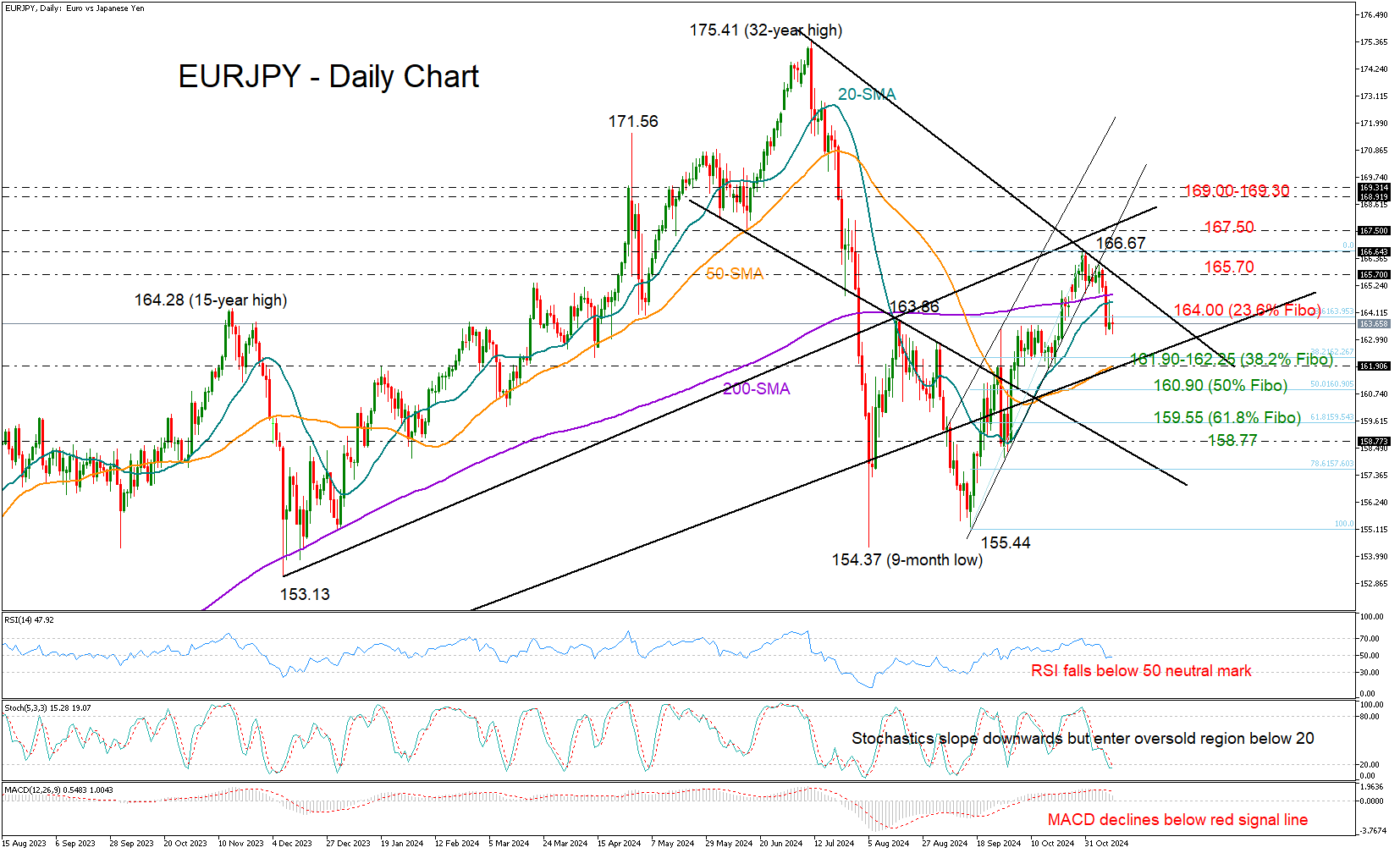

EURJPY Takes a Bearish Turn

- EURJPY moves sideways, but technical signals point to more downside

- Support could come near 162.25; bulls need a break above 165.70

EURJPY continued to trade quietly within the 163.00 range for the second consecutive day, but despite the lack of momentum in the price, the technical signals suggest that further downside could be on the horizon.

The pair broke below a key short-term support trendline last week and slipped beneath both its 20-day and 200-day simple moving averages (SMAs), signaling that the bears are regaining control.

The RSI and the MACD are reinforcing the bearish shift in sentiment as the former is pointing down below its 50 neutral mark and the latter is decelerating beneath its red signal line. Likewise, the stochastic oscillator is trending southward, though it has already entered the oversold area below 20, suggesting the market may be ripe for a rebound.

The 162.25 region, which coincides with the 38.2% Fibonacci retracement of the latest upleg, could be the nearest pivot point. Additionally, the 50-day SMA is in the vicinity at 161.90, making this level a key battleground for the bulls and the bears. If the bears stay in charge, selling pressure could intensify toward the 50% Fibonacci mark of 160.90. Then, the focus may turn to the 61.8% Fibonacci of 159.55 and the downward-sloping trendline around 158.77.

On the flip side, if the bulls manage to lift the price back above the 200-day SMA at 164.85, there is a chance for a short-term recovery. However, another significant hurdle may emerge near the tentative resistance line seen near 165.70. A step above this border might be necessary for an advance toward the October high of 166.67 or higher to 167.50. Further up, the rally could take a breather within the 169.00-169.30 zone.

In summary, EURJPY is currently in a bearish posture, with technical indicators and price action favoring further downside in the near term.

Hang Seng Index: Medium-Term Bullish Trend in Jeopardy After China Stimulus Disappoints

- Lack of concrete fiscal stimulus measures ex-post China NPC Standing Committee meeting.

- Deflationary and liquidity trap risks are now back in the forefront that may trigger a medium-term negative feedback loop into the Hong Kong & China stocks.

- Watch the 19,700 key support on the Hang Seng Index.

Since hitting a 52-week high of 23,242 on 7 October, the Hang Seng Index has failed to revive its prior bullish momentum that took shape in September on the backdrop of anticipated “more forceful” fiscal stimulus measures to accompany an expansionary monetary policy as China’s central bank, PBoC has cut its policy interest rates and injected more liquidity in the past two months.

After a month of lacklustre performance in October where the Hang Seng Index recorded a monthly loss of 3.9%, the slide failed to reverse and started to gain downside momentum on Monday as it gapped down and shed 1.45% on Monday, 11 November.

The current weakness seen in the Hong Kong stock market has been attributed to the lack of details of the promised fiscal stimulus measures from China to negate the ongoing deflationary spiral that is at high risk of being entrenched in the behaviours of Chinese consumers and businesses.

After a week-long economic-related meeting helmed by the National People’s Congress Standing Committee, China’s policymakers have announced the expected and approved 10 trillion yuan of debt swaps to allow local governments to reduce off-balance sheet hidden debt on late Friday afternoon, 8 November.

However, it stopped short of unleashing new fiscal stimulus to counter a potential increase in trade tariffs towards China goods and services from incoming US President-elect Trump’s White House administration.

Hence, financial market participants have started to lose confidence and patience in the timing and willingness of China’s top policymakers to enact “whatever it takes” bazooka-liked fiscal stimulus measures to jumpstart consumer confidence and spending, which in turn, relay negative feedback loops back into the Hong Kong and China stock markets.

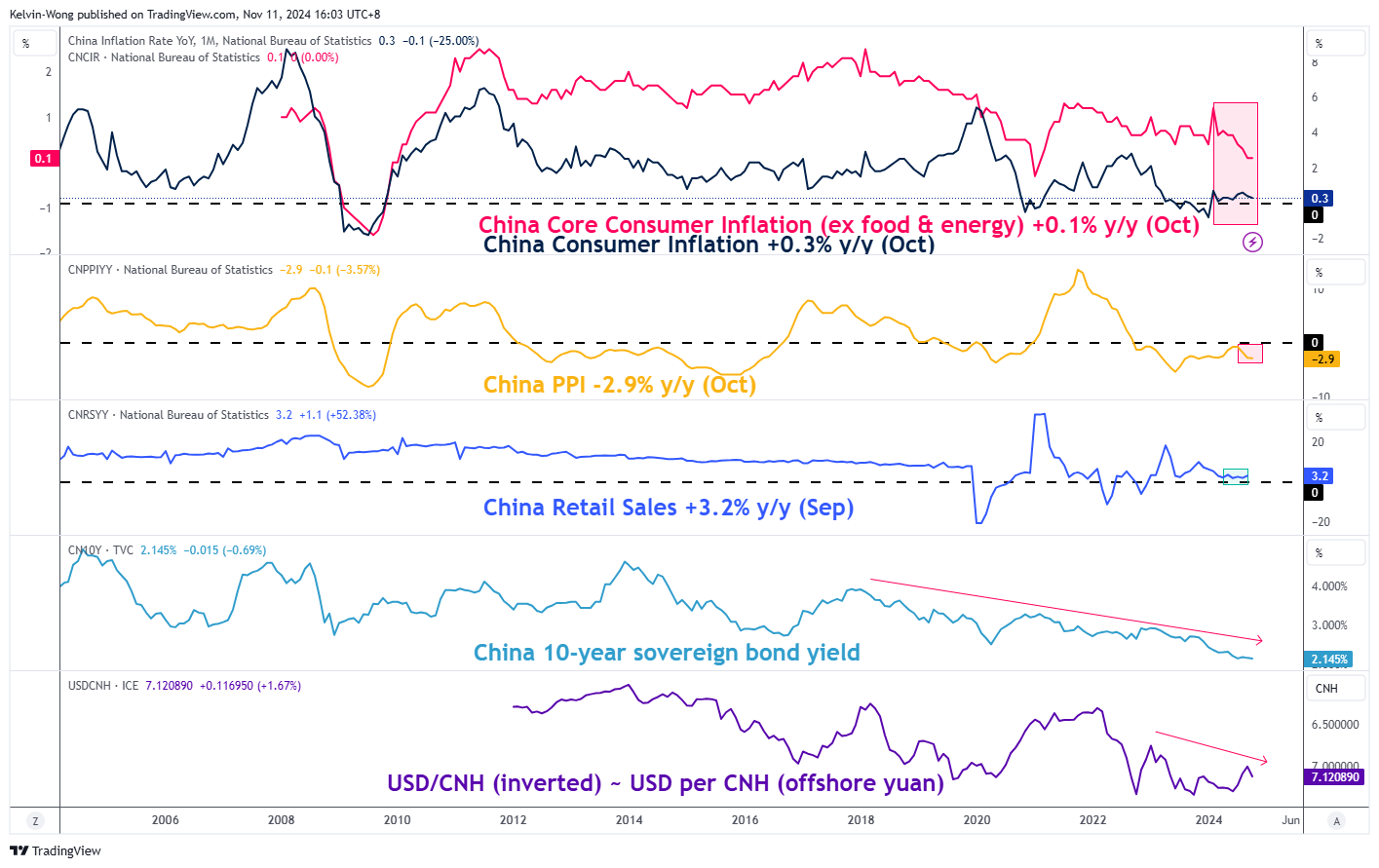

Heightened deflationary spiral and liquidity trap risks

Fig 1: China’s inflation data, 10-year sovereign bond yield & CNH/USD trends as of 31October 2024 (Source: TradingView, click to enlarge chart)

Despite China’s central bank, PBoC’s slew of interest rate cuts and liquidity injections in the past two months, there is still a lack of confidence to trigger a boost in internal demand, and it can be seen apparently in the data of core consumer inflation and producers’ inflation (factory gate prices) that continued to decelerate in October and came in below expectations.

The deceleration of factory gate prices continued to be the main culprit of the ongoing heightened risk of a deflationary spiral unfolding in China. It continued to decline since July, and it fell further to -2.9% y/y in October from -2.8% in September (see Fig 1).

The resultant effect is a continuation of a major impulsive downtrend sequence of the China 10-year sovereign bond yield that led to a total wipeout of the gains seen in the offshore yuan against the US dollar in September, induced by the first US Federal Reserve’s interest rate cut.

Overall, a resurgence of a major weakening trend of the offshore yuan is likely to trigger a negative double whammy for Hong Kong and China stocks.

Watch the 19,700 support on the Hang Seng Index

Fig 2: Hang Seng Index medium-term & major trends as of 12 Nov 2024 (Source: TradingView, click to enlarge chart)

The Hang Seng Index ended Tuesday, 12 November session on a weak footing as it declined by 2.8% and hit a six-month low despite a positive news flow that reported that China authorities are likely to cut home buying taxes soon to as low as 1% from the current level of 3%.

The daily RSI momentum has just staged a bearish breakdown below a parallel ascending trendline support and inched below the 50 level which suggests a potential resurgence of medium-term bearish momentum.

A break with a daily close below 19,700 key medium-term pivotal support (also the 50-day moving average) may see further weakness to expose the next medium-term supports at 17,900 (also the 200-day moving average) and 16,610 (see Fig 2).

Clearance above the 21,420 intermediate resistance may dissipate the bearish tone for the medium-term resistance to come in at 22,690 in the first step.

Brent Crude Stumbles as Market Sentiments Turn Cautious

Brent crude oil prices have continued to slip, touching 71.74 USD a barrel on Tuesday. This marks a downturn influenced by China's underwhelming stimulus measures. The market's lack of confidence in China's rejuvenation efforts, coupled with persistently weak inflation and subdued energy demand within the country, has led to this downturn.

Compounding the downward pressure on oil prices, the US dollar's strength makes commodity investments less attractive, as a robust USD typically dampens demand for dollar-priced assets like oil. However, the geopolitical landscape, which often serves as a driver for oil price volatility, appears stable for now. With reduced tensions in the Middle East, some risk premiums previously embedded in Brent prices have been alleviated.

Investors eagerly anticipate the monthly OPEC report expected later today, which is set to provide deeper insights into the supply-demand dynamics. This report has the potential to influence market sentiments significantly and is a key focus for investors as they consider global oil demand forecasts for 2025.

Brent technical analysis

On the H4 chart of Brent, the market continues to develop a broad consolidation range around the level of 73.66, extending to the level of 71.33. Today, we expect a growth link to the level of 73.66. After reaching this level, developing another downside structure to 71.22 is possible. Further, we will consider the probability of the beginning of the growth wave development to 76.00, with the prospect of the trend's continuation to 80.80, the local target. Technically, this scenario is confirmed by the MACD indicator. Its signal line is under the zero level and is directed downwards.

On the H1 Brent chart, the market has formed a consolidation range around 73.66 and worked out a downward wave to 71.33, the local target. Today, a correction link for this downward wave is likely with a target at 73.66, followed by another wave of decline to 71.22. At this point, the potential of the downward wave can be considered exhausted. Technically, this scenario is confirmed by the Stochastic oscillator. Its signal line is under 50 and is directed strictly downwards to 20.

Aussie Extends Losses, Wage Inflation Next

The Australian dollar has posted sharp losses on Tuesday. In the European session, AUD/USD is trading at 0.6544, down 0.44% on the day.

Australian consumer, business sentiment accelerates

Australian businesses and consumers are showing improved confidence. The National Bank Business Confidence index for October rose to 55, up from -2 in September and its highest level since January 2023. The Westpac consumer confidence index climbed 5.3% to 94.6 in November, up from 89.8 in October. This was the highest level in over two years.

The positive confidence numbers indicate that businesses and consumers are more confident about the economic outlook, as expectations grow for a rate cut from the Reserve Bank of Australia, which meets on Dec. 10. Australia releases the October employment report on Thursday and the release could be a significant factor as to whether the central bank continues to hold rates or delivers an initial rate cut. Australian inflation has fallen to 2.8%, within the RBA’s target of 1% to 3%.

Australia releases wage inflation on Wednesday. Wages are expected to ease to 3.6% y/y in the second quarter, down from 4.1% in Q1. Wage inflation has been a driver of services inflation which rose to 4.5% in the second quarter, up from 4.3% in Q1. RBA policymakers are hesitant to start lowering rates until services inflation loses some steam and heads lower.

In the US, there are no major events on the calendar but investors will be listening closely as a number of FOMC members make public remarks. The Federal Reserve is expected to continue to trim rates, with a 25-basis point cut the most likely scenario at the December meeting.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6559 and is testing support at 0.6544. Below, there is support at 0.6524

- There is resistance at 0.6579 and 0.6594

GBP/USD Slips to 3-Month Low as Unemployment Rate Jumps

The British pound is down for a third straight trading day on Tuesday. In the European session, GBP/USD is trading at 1.2822, down 0.36% on the day. Earlier today, the pound fell below the 1.28 line for the first time since Aug. 15.

UK employment rate climbs to 4.3%

The UK employment report for the three months to September disappointed, as the unemployment rate shot up to 4.3%, up from 4% in the previous reading and above the market estimate of 4.1%. This was the highest level since the three months to May. Unemployment rolls climbed to 26.7 thousand, up from a revised 10.1 thousand but below the market estimate of 30.5 thousand. The BoE meets next on Dec. 19 and the jump in the unemployment rate could raise expectations for a rate cut. The next employment report will be critical, coming just two days before the BoE meeting.

There was some good news as job growth climbed 220 thousand, lower than the previous reading of 373 thousand, which was a record high. This was the fifth straight three-month period of job growth, pointing to a stable labor market.

Annual earnings, excluding bonuses inched down to 4.8%, down from 4.9% in the three months to August and higher than the market estimate of 4.7%. Wage growth is feeding services inflation, which remains much higher than the BoE’s 2% target.

A host of Federal Reserve members will deliver public remarks today and investors will be looking for clues about future rate moves. The markets have priced in a 25-basis point cut at the Dec. 18 meeting at 69% according to CME’s FedWatch. We can expect market expectations to shift if the US posts unexpected inflation or employment data ahead of the meeting.

GBP/USD Technical

- GBP/USD pushed below support at 1.2841 earlier and is testing support at 1.2814. Below, there is support at 1.2771

- There is resistance at 1.2884 and 1.2911