Sample Category Title

ECB’s Rehn: May exit restrictive policy as soon as late winter

Speaking at a conference today, Finnish ECB Governing Council member Olli Rehn reiterated that the direction of monetary easing is "clear". However, he emphasized that the "speed and scope " of these cuts will be determined by a trio of factors evaluated at each ECB meeting: the inflation outlook, underlying inflation trends, and the efficacy of monetary policy transmission.

Rehn pointed to the possibility of reducing the ECB’s deposit rate, currently at 3.25%, to a neutral level. Such adjustments could occur by late winter or early spring if the data supports it.

"Current market data and simple maths seem to imply that we would leave restrictive territory sometime in the spring/winter next year 2025," Rehn said. "But that is just an observation from my side, not a commitment."

Has US 100 Index Rally Run Its Course?

- US 100 index trades a tad below its all-time high

- The US election rally appears to have fizzled out

- Momentum indicators remain bullish at this stage

The US 100 cash index is moving sideways again today, as the rally since the US presidential election date appears to have concluded. A new all-time high has been recorded, but the bulls have failed, up to now, to push the US 100 index above the long-term January 6, 2023 trendline. Market participants are probably taking a breather and preparing for this week’s key US data releases. Meanwhile, the bullish trend since the August 5 low remains firmly in place, supported by a series of higher highs and higher lows.

The momentum indicators are comfortably bullish at this juncture. More specifically, the Average Directional Movement Index (ADX) is edging higher and hence signalling a strengthening bullish trend in the US 100 index. Similarly, the RSI is hovering above its midpoint, confirming the recent bullish pressure. More importantly, the stochastic oscillator has jumped back inside its overbought area (OB). It can stay there for a while before signalling its intention for a bearish breakout.

Should the bulls remain confident, they could try to lead the US 100 index above January 6, 2023 trendline, opening the door to another all-time high. The 21,500 appears to be the first target, with the 200% Fibonacci extension level of the November 22, 2021 – October 13, 2022 downtrend positioned just north of 23,000.

If the bears manage to regain the market reins, they could try to keep the US 100 index below the January 6, 2023 trendline and then push it towards the 20,683-20,772 area. This region is populated by the 161.8% Fibonacci extension level, the July 11, 2024 high and it is the point that the August 5, 2024 and October 26, 2023 ascending trendlines currently cross. A move below this busy area will open the door to a test of the support set by the 50- and 100-day simple moving averages (SMAs) at the 19,722-19,978 region.

To sum up, the US 100 index is trading sideways as market participants are potentially preparing for Wednesday’s US CPI release that could result in increased volatility and potentially complement the current bullish trend.

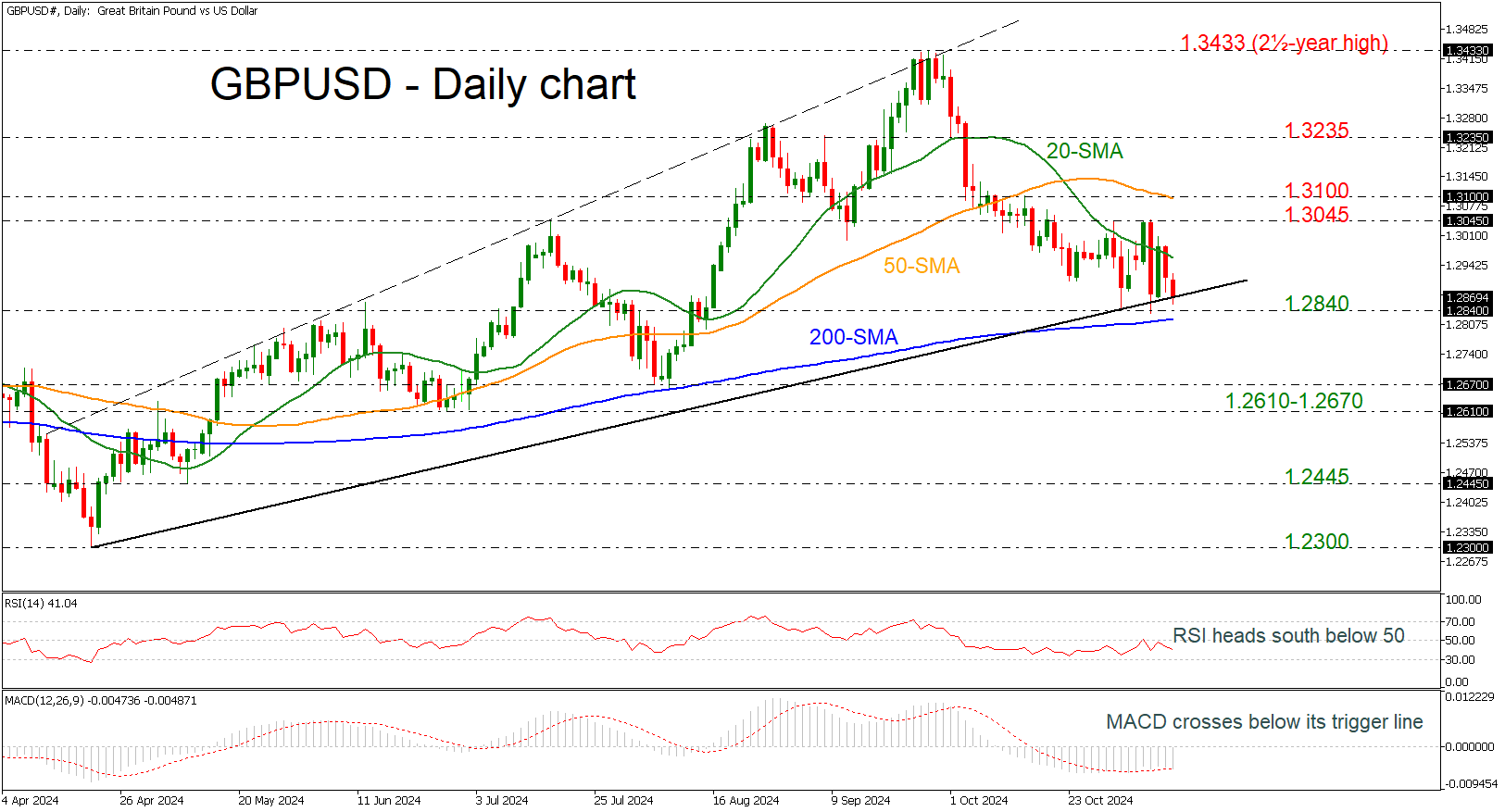

GBPUSD Gives Strong Battle With Uptrend Line

- GBPUSD holds in tight range in near term

- MACD and RSI tick lower

GBPUSD is flirting with the long-term ascending trend line after the downfall of the 1.3045 resistance level. The next crucial point for traders to meet is the 1.2840 support and the 200-day simple moving average (SMA) at 1.2820.

According to technical oscillators, the RSI is pointing south below the 50 territory, while the MACD is crossing its trigger line to the downside below the zero level.

If the market retreats further and breaks the 200-day SMA at 1.2820, then the market could challenge the restrictive supportive region of 1.2610-1.2670.

On the other hand, a potential rebound off the uptrend line may drive the market toward the 20-day SMA at 1.2960. Climbing higher, the pair may touch the 1.3045 barrier and the 1.3100 round number, which overlaps with the 50-day SMA, endorsing the bullish mode in the bigger picture.

All in all, GBPUSD has been in a sideways move over the last month, but a plunge below the 200-day SMA would open the way for steeper bearish actions.

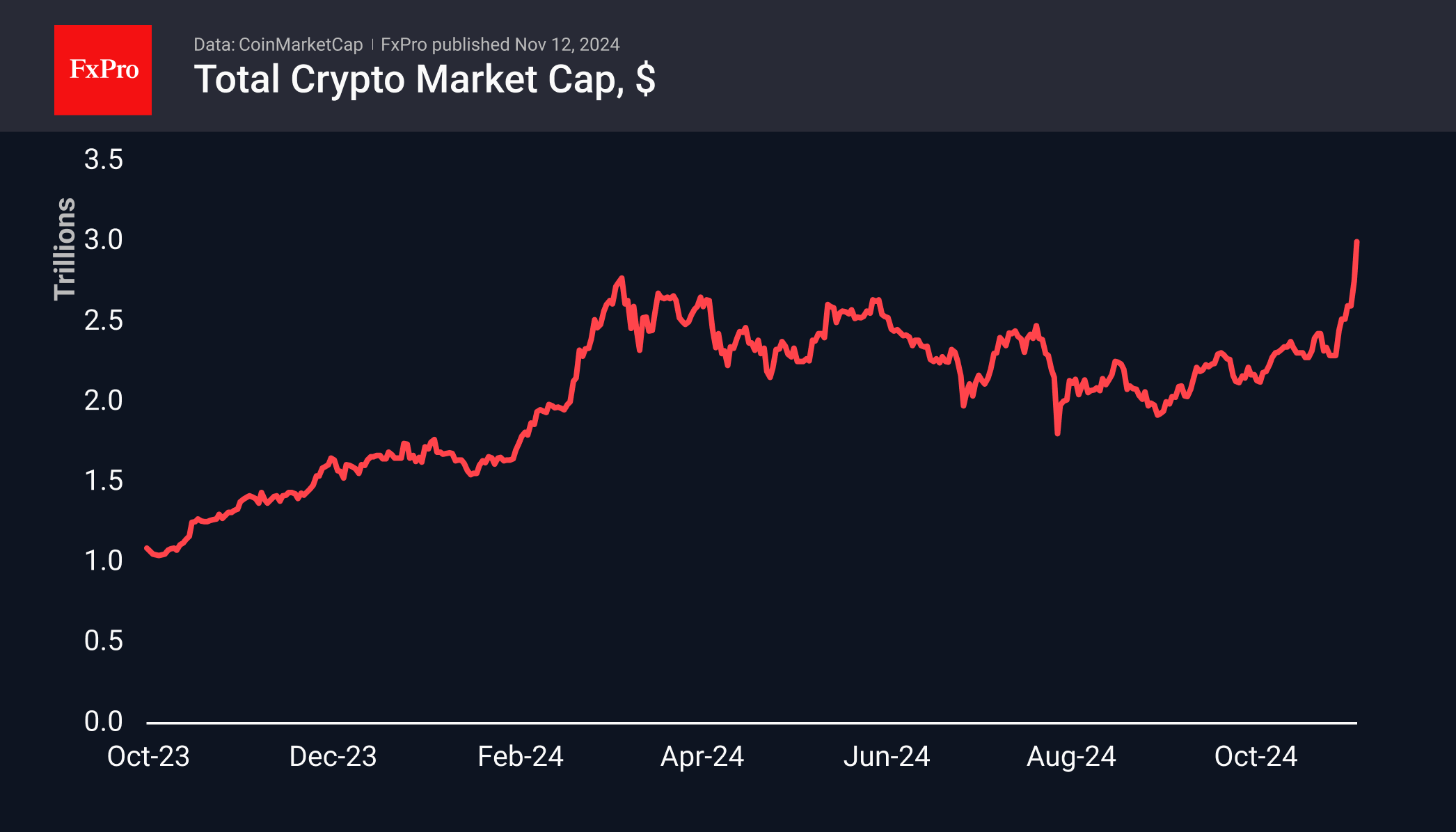

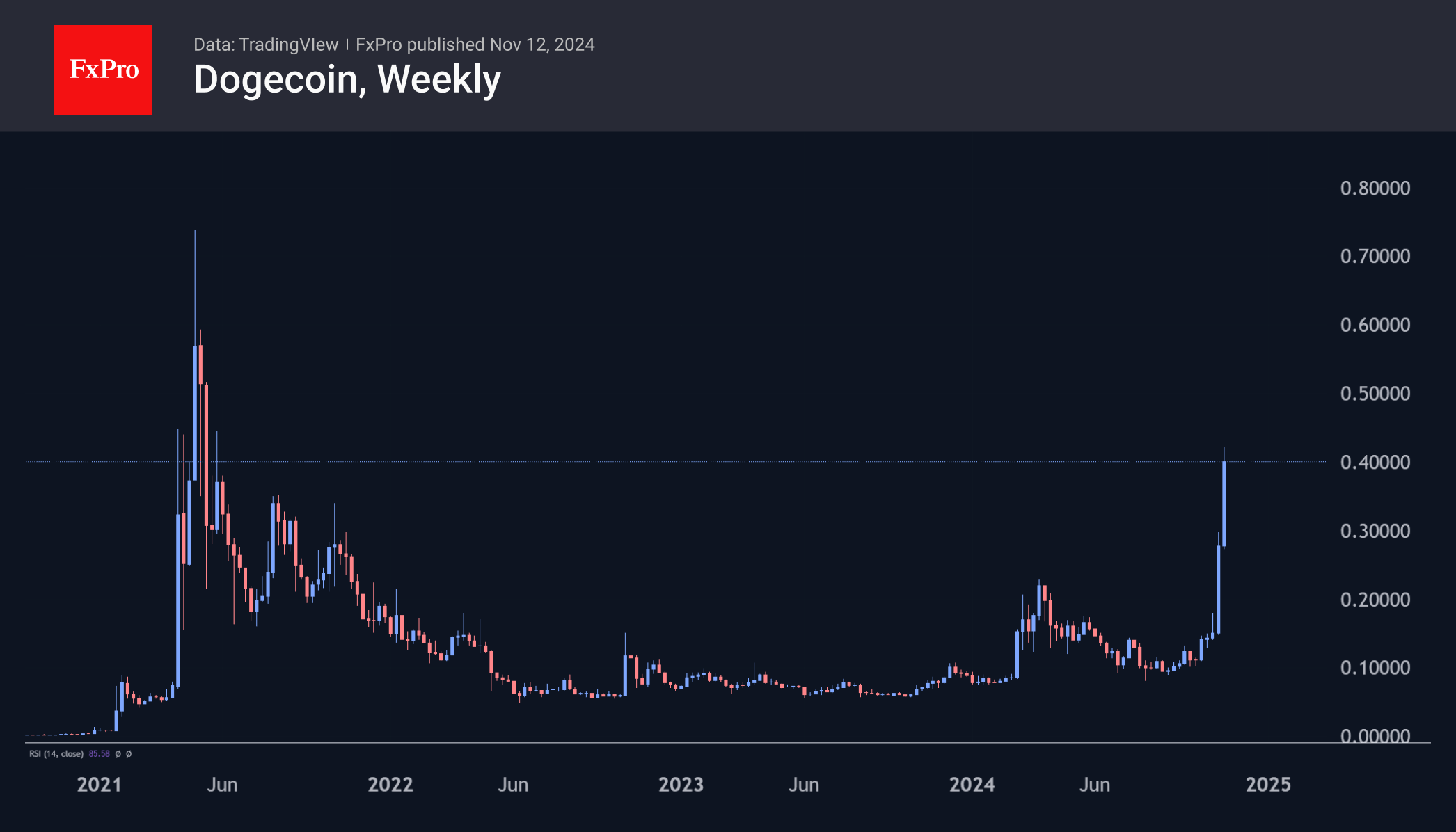

Crypto Punishes Sceptics

Market Picture

The total capitalisation of the cryptocurrency market approached $3 trillion, rewriting the record set almost exactly three years ago. During the day, the indicator grew by more than 8%. The nature of the movement indicates the liquidation of short positions in the largest coins, primarily bitcoin. At the same time, individual altcoins are increasingly shooting up.

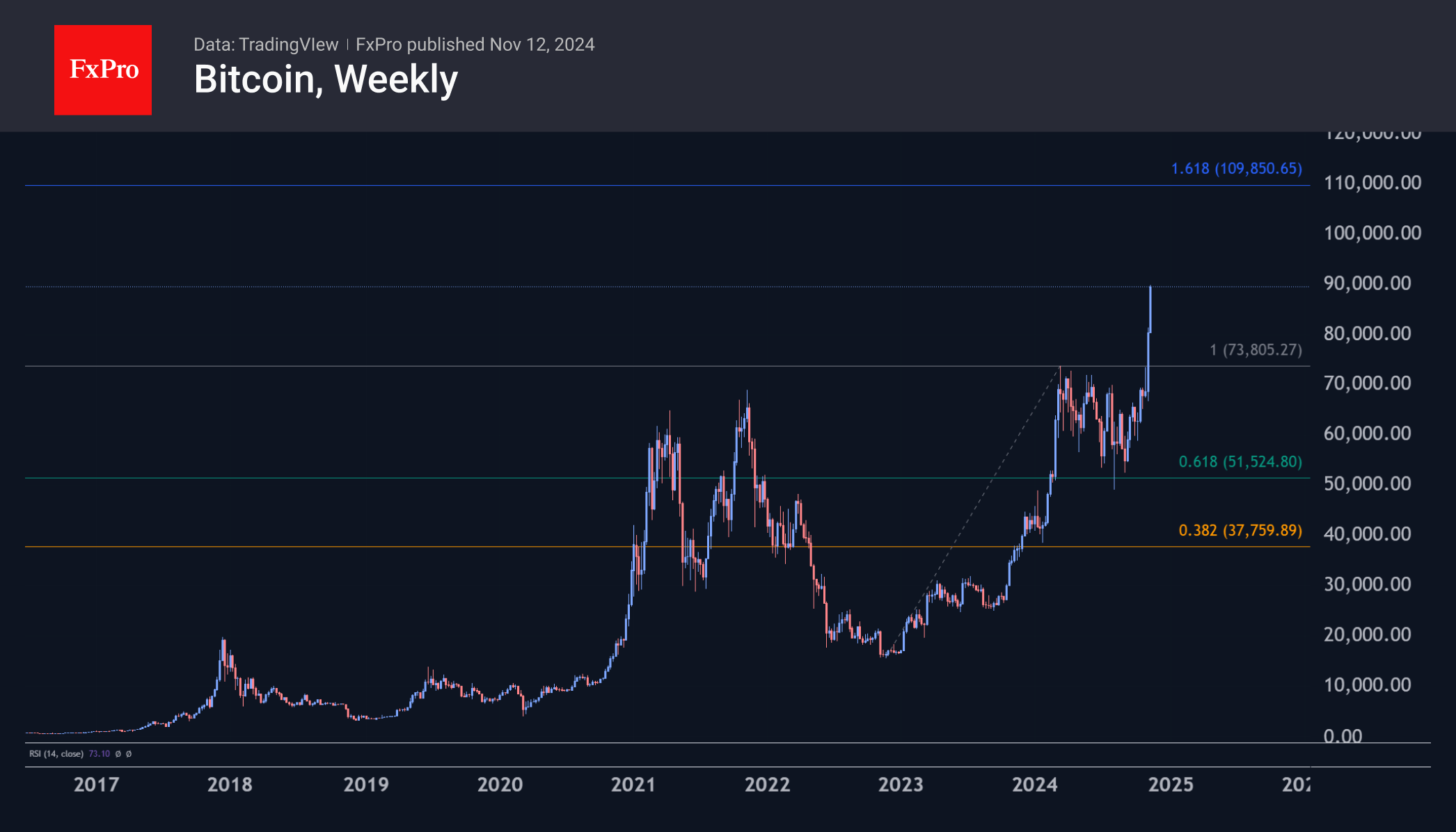

The first cryptocurrency soared almost 10% in 24 hours, coming close to $90K, although only a little over a day ago, it tried to consolidate at $80K. Reaching the $100-110K target area now looks like a matter of a couple of weeks or even days.

Dogecoin is even more actively destroying sceptics with open positions. In 24 hours, it soared 44% to $0.4. It traded sustainably higher for only 15 days in May 2021. This area was pivotal in April and June that year, so it’s worth paying extra attention to it this time around as well.

News Background

According to CoinShares, global crypto fund investments rose by $1.978bn last week after inflows of $2.177bn previously. The positive trend continued for the fifth consecutive week. Investments in Bitcoin increased by $1.796bn, Ethereum by $157m, and Solana by $4m. Investments in funds with multiple crypto assets increased by $23m.

Inflows into crypto-ETFs since the beginning of the year reached $31.3bn. Due to price growth, global assets under management reached a new all-time high of $116bn. Trading volumes rose to their highest level since April. The combination of a favourable macroeconomic environment (Fed rate cuts) and seismic shifts in the US political system (after Trump’s victory) are likely reasons for such favourable investor sentiment, CoinShares suggests.

According to founder Michael Saylor, MicroStrategy bought an additional 27,200 BTC between 31 October and 10 November for $2.03 billion (at ~$74,463 per coin). The firm now holds 279,420 BTC, acquired for $11.9bn at an average exchange rate of $42,692.

MN Consultancy head Michael van de Poppe said that the much-anticipated altcoin season has begun in the background of Bitcoin’s new all-time highs. He described Ethereum’s rise in recent days as impressive. The altcoin bull cycle could last until 2026 or 2027 and transform into a full-blown Supercycle.

In the past few days, the bankrupt FTX has filed 23 lawsuits against various companies and individuals to recover funds from creditors. In the lawsuit against Binance, FTX’s lawyers are demanding the return of $1.8bn paid as part of a share buyback in 2021.

EUR/USD Dips Further While USD/CHF Turns Green

EUR/USD extended losses and traded below the 1.0775 support. USD/CHF is rising and might aim a move toward the 0.8850 resistance.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro struggled to clear the 1.0935 resistance and declined against the US Dollar.

- There is a key bearish trend line forming with resistance at 1.0680 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF is showing positive signs above the 0.8745 pivot zone.

- There was a break above a short-term bullish continuation pattern with resistance at 0.8770 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair failed to clear the 1.0935 resistance. The Euro started a fresh decline below the 1.0825 support against the US Dollar, as mentioned in the previous analysis.

The pair declined below the 1.0775 support and the 50-hour simple moving average. Finally, the pair tested the 1.0630 level. A low was formed at 1.0628 and the pair is now consolidating losses. The pair is showing bearish signs, and the upsides might remain capped.

Immediate resistance on the upside is near the 23.6% Fib retracement level of the downward move from the 1.0825 swing high to the 1.0628 low at 1.0680.

There is also a key bearish trend line forming with resistance at 1.0680 and the 50-hour simple moving average. The next major resistance is near the 1.0725 zone. The main resistance sits near the 76.4% Fib retracement level of the downward move from the 1.0825 swing high to the 1.0628 low at 1.0775.

An upside break above the 1.0775 level might send the pair toward the 1.0825 resistance. Any more gains might open the doors for a move toward the 1.0935 level.

On the downside, immediate support on the EUR/USD chart is seen near 1.0630. The next major support is near the 1.0600 level. A downside break below the 1.0600 support could send the pair toward the 1.0565 level.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a decent increase from the 0.8615 support. The US Dollar climbed above the 0.8700 resistance zone against the Swiss Franc.

There was a break above a short-term bullish continuation pattern with resistance at 0.8770. The bulls were able to pump the pair above the 50-hour simple moving average and 0.8770. Finally, the pair tested the 0.8815 zone.

A high was formed near 0.8817 and the pair is still showing signs of more upsides. On the upside, the pair is now facing resistance near 0.8820.

The main resistance is now near 0.8840. If there is a clear break above the 0.8840 resistance zone and the RSI remains above 50, the pair could start another increase. In the stated case, it could test 0.8920.

If there is a downside correction, the pair might test the 0.8790 level or the 23.6% Fib retracement level of the upward move from the 0.8701 swing low to the 0.8817 high.

The first major support on the USD/CHF chart is near the 0.8770 level. The next key support is near the 61.8% Fib retracement level of the upward move from the 0.8701 swing low to the 0.8817 high at 0.8745.

A downside break below 0.8745 might spark bearish moves. The next major support is near the 0.8700 pivot level. Any more losses may possibly open the doors for a move toward the 0.8615 level in the near term.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Dollar Sets the Pace in FX Markets

Markets

US markets were closed yesterday in observance of Veteran’s Day, thinning trading conditions at the start of the week. For now, the by default trading mechanisms are the ones put in place after US Republicans secured their hattrick last week. The dollar sets the pace in FX markets with the trade-weighted greenback (DXY) closing in on 106.13 June top (currently 105.70). It’s the first of a set of mediocre resistance levels on the way to the upper band of the sideways trading channel in place since the start of 2023. Via 106.52 (2024 top) and 107.11 (Nov 23 high), we arrive at the 2023 top of 107.35 which is still our preferred scenario. EUR/USD sets a new short-term low at 1.0630 this morning and is equally looking at 1.0601 (2024 low) as final support ahead of the range bottom of the past two years (1.0448). The People Bank of China fixed the yuan at its weakest since September (USD/CNY now 7.2350), suggesting that a weaker currency will become part of the policy mix. Regulators are also planning to cut taxed for home purchases as the government drives up its fiscal spending efforts to revive the economy.

The underlying trend in (long-term) bond yields is still up as markets gear up for more fiscal stimulus on a global level. These short term growth and inflationary boosting measures come with a higher credit premium as well. Last week’s first ever positive Bund/swap spread is a point in case with the German government heading to early elections as the coalition collapsed over breaking up the debt brake. Such fiscal strategies have implications for monetary policy as well with BoE governor Bailey’s call for activism making way for “not too many and not too much” after calculating the impact of Chancellor Reeves’ 2025 budget. A higher growth and inflation peak in 2025 call for a careful monetary approach given that inflation remains stick above the 2% targets.

News & Views

An article in the Financial Times suggests that the European Union is preparing a change in its spending policies that can potentially redirect tens of billions of euro to defense and security. According to the reporting, the policy shift could apply to about a third of the EU’s common budget mentioning an amount of about €392bn over the 2021 to 2027 budget period as only about 5% of these cohesion funds have been spend. For now, the funds can’t be used to fund the military, but according to the FT referring to EU officials, more flexibility will be allowed to support the defense industry and to support military mobility projects. The FT quotes a spokesman of the European Commission saying that cohesion funds could be used for the defense industry as they contribute to the overall mission to enhance regional development, including military mobility. According to the FT analysis, this shift in spending might also be supported by net payers of the EU budget who see it as preferable to issuing joined debt or providing additional EU funding.

Czech inflation accelerated further to 0.3% M/M and 2.8% Y/Y in October. The outcome was in line with expectations but shows a further rise from September (-0.4% M/M and 2.6% Y/Y). The monthly increase was mainly due to of housing, water, electricity, gas another solid fuels (0.4%). Food and non-alcoholic beverages rose 0.3% M/M. Price of goods in total increased by 0.2% M/M and 1.3% Y/Y. Prices of services were 0.5% higher in a monthly perspective and 5.3% compared to the same period last year. Core inflation at 2.4% Y/Y was in line with the forecast of the Czech national Bank (CNB). While still within the CNB tolerance band, the gradual rise in inflation comes as the CNB and its governor Michl recently indicated that they were considering a halt to its rate cutting cycle after the policy rate was reduced to 4% at last week’s policy meeting. In this respect, Michl indicated that he prefers core inflation to decline slightly below the 2% target. After a temporary rebounding last week, the Czech koruna currently again trades slightly weaker near EURCZK 25.34.

Trumpforia

Bitcoin added another 10% yesterday and came just shy of the $90K per coin, while Ethereum flirted with the $3400 mark. The crypto-friendly Donald Trump – who says that the US should become the center of the digital assets – will probably remove the crypto-sceptics of the government institutions from their position and replace them by crypto-friendly regulators who will let the crypto industry ‘thrive’ in the US. And when there is a comprehensive and solid policy ground, the banks could more comfortably integrate cryptocurrencies on their platforms and attract more institutional money on board. More demand should push the price of Bitcoin – which has a limited supply – higher. Eyes are on the $100K mark and above. High volatility will be on the menu for Xmas.

Elsewhere, the S&P 500 consolidated gains near ATH level, while small caps extended rally by 1.5% despite the rising US yields – which should become a challenge for the US small caps as the post-election euphoria settles.

In the traditional currencies, the US dollar index is pushing higher along with the US yields on expectation that Trump’s pro-growth policies and tariffs would lead to higher inflation and softer-than-otherwise policy easing from the Federal Reserve. That’s in contrast with the worsening economic and political outlook for the Eurozone, with Germany preparing for a snap election on government’s inability to tackle the financial difficulties and revive growth. The euro tanked to 1.0628 against the US dollar, and to 0.8260 against the pound yesterday. The German and the Eurozone economic sentiment indicators are due this morning and are somehow expected to print a slight improvement in November, but a slight improvement per se won’t be enough to lift mood in Europe while Trump’s tariff threat is taking a toll. The Stoxx 600 rebounded yesterday, probably on the expectation that a softer European Central Bank (ECB) policy could boost valuations, but the ECB will probably remain more cautious than many expect when it comes to easing policy because a rapid appreciation of the US dollar will have a boosting effect on global (and euro area) inflation and could eventually limit the ECB’s ability to cut wholeheartedly.

In Japan, the likelihood of further policy normalization is melting by the day. There is still hope – for the yen bulls – that the Bank of Japan (BoJ) will deliver another rate hike in December or January, but to me, the December meeting is probably off the table, and January is on a very slippery ground. One of the new PM Ishiba’s closest allies, Economic Revitalization Minister Akazawa, attended the BoJ meeting for the first time and he said that it’s important for the BoJ to continue monetary easing to ensure a complete end of deflation. Of course, this man is responsible for Economic Revitalization, and of course he has appetite for favourable monetary policy, but the BoJ has more doves on board than hawks, and the rising global uncertainties look increasingly supportive of the yen bears until a new FX intervention is triggered. Soft yen, combined with the government’s pledge to support growth – especially in tech space – remain supportive of the Nikkei.

In energy, the barrel of US crude kicked off the week on a negative note. Gloomy outlook for China both due to the sluggish fundamentals and Trump threat, the Chinese authorities’ inability to meet the market’s demand in terms of fiscal stimulus and the idea that the Trump administration will ‘drill baby drill’ sent the barrel of US crude below the $68pb this morning. Trend and momentum indicators have turned negative and the RSI suggests that there is room for further selloff before the market hits the oversold conditions. Next natural target for the bears stands at $65pb. As such, it’s probably just a matter of time for the USDCAD to reach the 1.40 psychological mark.

Elsewhere, the AUDUSD is bearing the brunt of falling iron ore prices on sluggish Chinese growth outlook and the energy and mining heavy FTSE 100 was better bid yesterday and should benefit from a broad-based USD strength, but a softer pound alone won’t enough to keep the FTSE 100 in the actual bullish trend. The sluggish China and the prospects of higher-than-otherwise global yields – as the US is expected to exports its Trumpflation – look unpromising. The major support to the past year’s rebound stands a few points above the 8000p psychological mark.

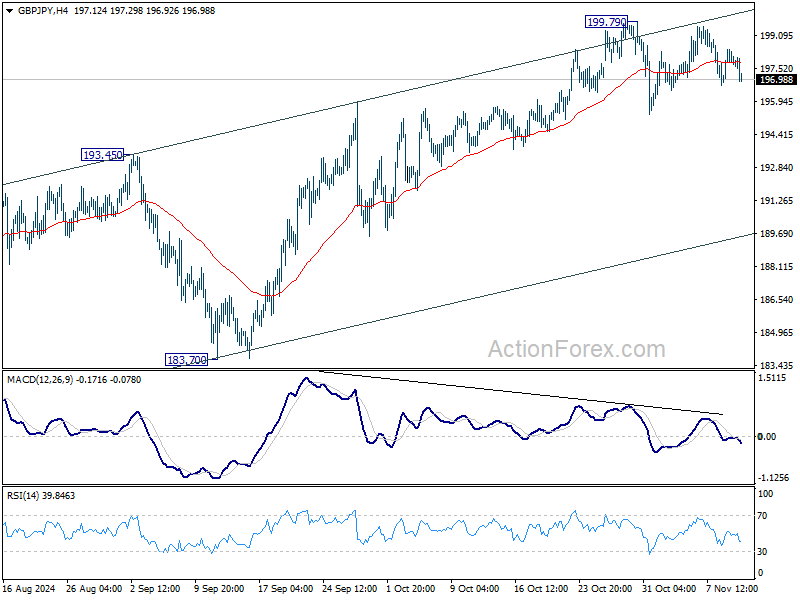

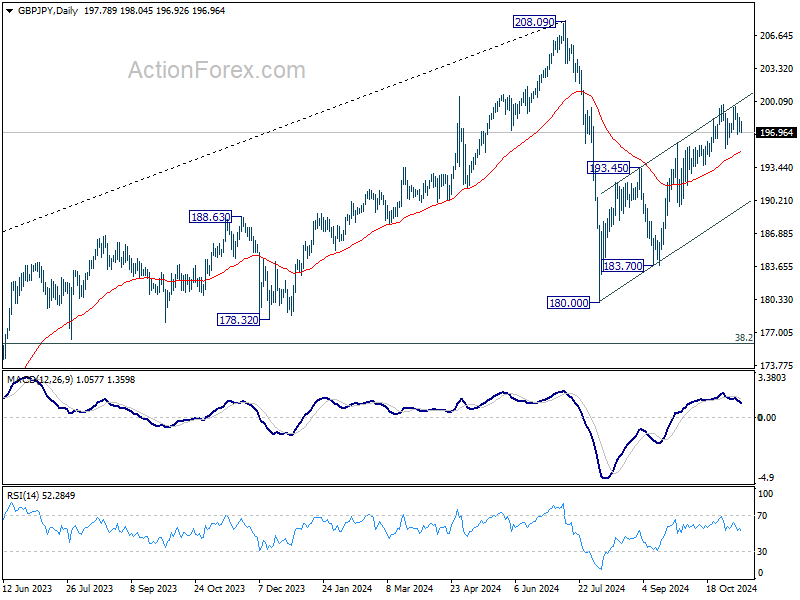

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.03; (P) 197.75; (R1) 198.57; More...

Range trading continues in GBP/JPY and intraday bias stays neutral for the moment. Further rally is expected as long as 55 D EMA (now at 194.99) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

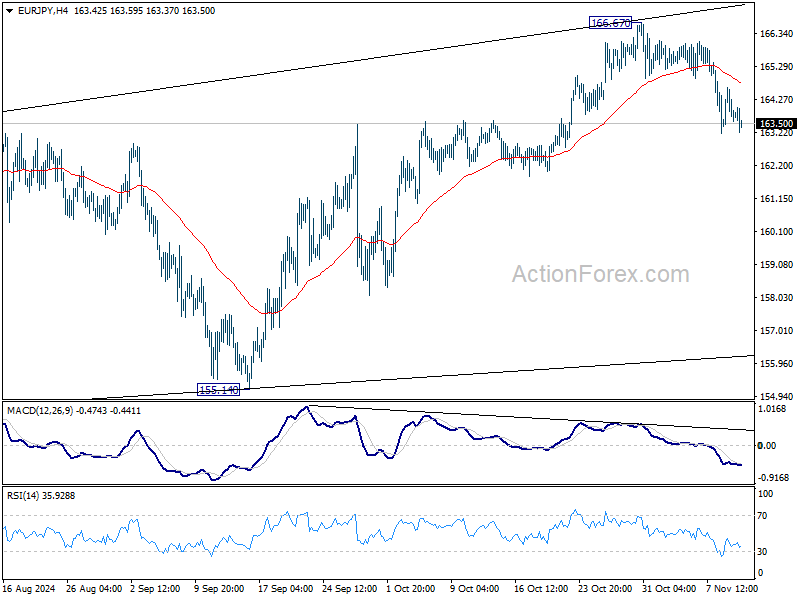

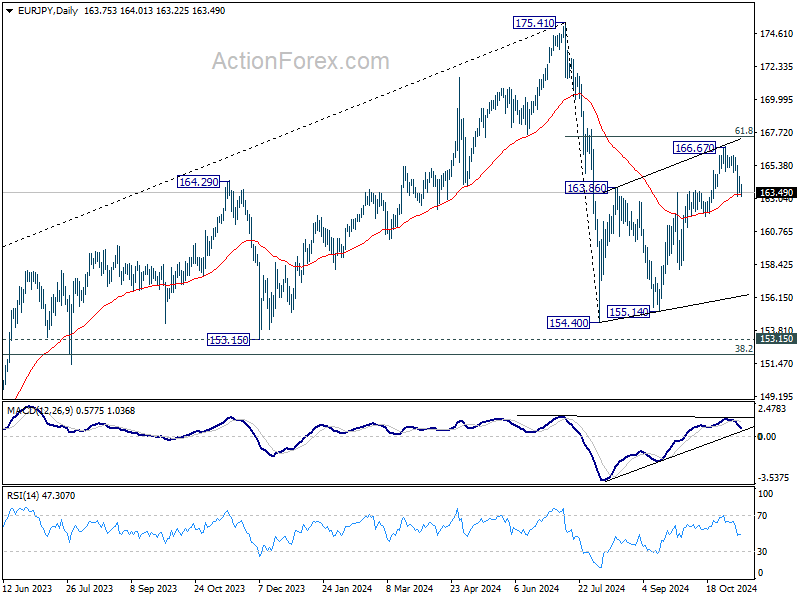

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.33; (P) 163.99; (R1) 164.50; More....

Intraday bias in EUR/JPY remains on the downside. Sustained trading below 55 D EMA (now at 163.34) will argue that whole corrective rise from 154.40 has completed with three waves up to 166.67. Deeper decline should then be seen back to 154.40/155.14 support zone. On the upside, break of 166.67 will target 61.8% retracement of 175.41 to 154.40 at 167.38 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

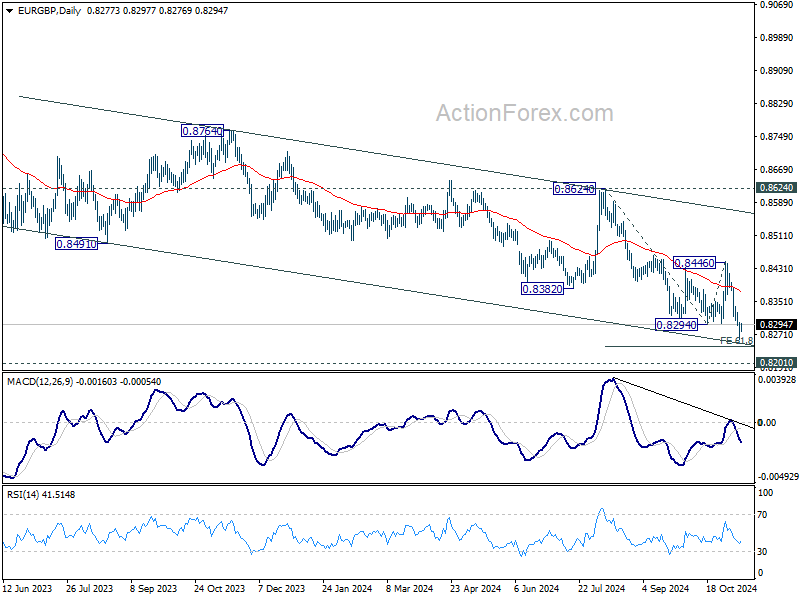

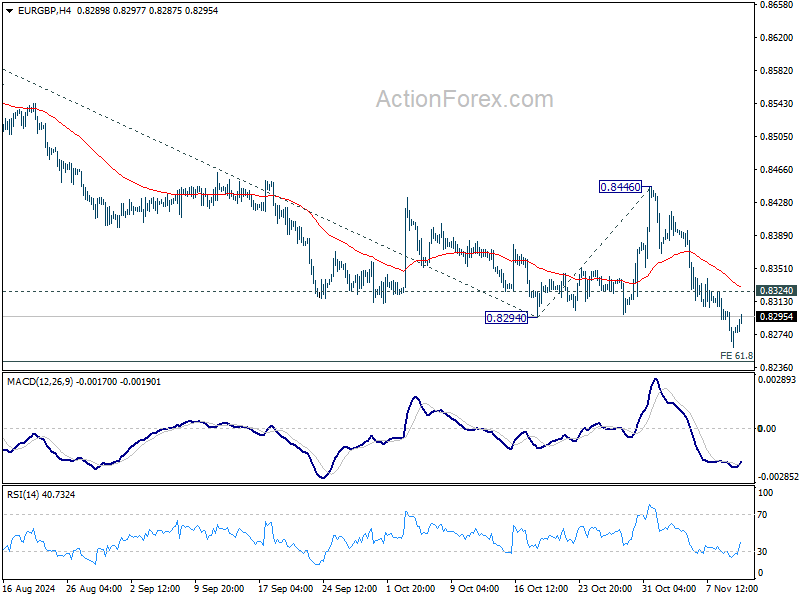

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8259; (P) 0.8281; (R1) 0.8301; More...

Intraday bias in EUR/GBP remains on the downside for 61.8% projection of 0.8624 to 0.8294 from 0.8446 at 0.8242. Break there will target 0.8201 key support. On the upside, above 0.8324 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 0.8446 resistance holds, in case of rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.