Sample Category Title

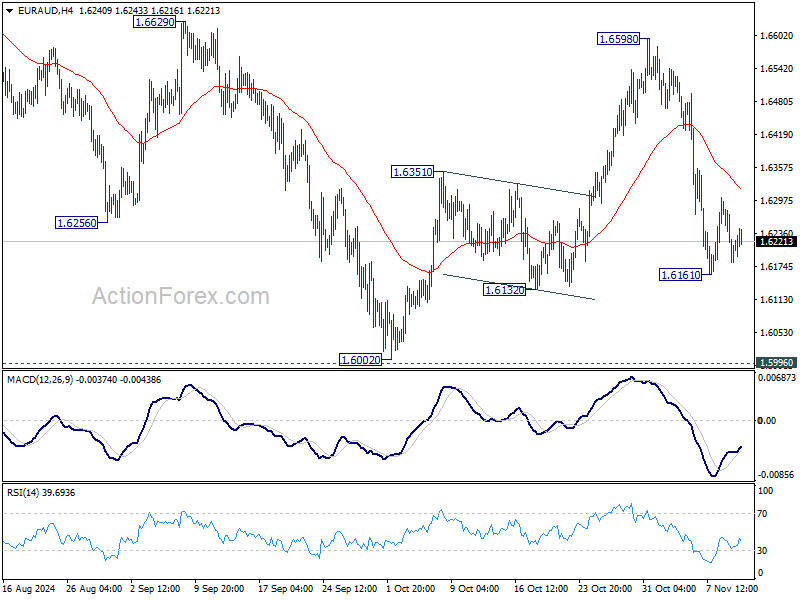

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6165; (P) 1.6226; (R1) 1.6267; More...

Intraday bias in EUR/AUD stays neutral at this point. For now, risk will stay mildly on the downside as long as 1.6598 holds, in case of stronger rebound. On the downside, break of 1.6161 will resume the decline from 1.6590 to target a test on 1.5996/6002 key support zone.

In the bigger picture, as long as 1.5996 cluster support , up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

Mixed UK labor data as unemployment rate and earnings growth climbs

In October, UK employment data indicated slight weakening in the labor market, with payrolled employees decreasing by -5k or -0.0% mom to a total of 30.4m. Comparing to the same month a year ago, payrolled employment rose 95k or 0.3% yoy. However, the claimant count for job-related benefits rose by 26.7k to reach 1.806mn, smaller than expectations of a 30.5k increase.

In the three months to September, unemployment rate climbed from 4.0% to 4.3%, higher than the anticipated 4.1%. On the earnings front, total average earnings, including bonuses, rose by 4.8% yoy, outpacing both the previous 3.9% growth and market forecasts. Excluding bonuses, average earnings grew by 4.8% yoy, marginally down from 4.9% yoy in the prior period but still above the projected 4.7% yoy.

Will ZEW for November Match October’s Improvement?

In focus today

Today will be light on the data front, with the German ZEW indicator for November only. It will be interesting to see if the improvement in expectations recorded in October continued in November.

Economic and market news

What happened overnight

In Sweden, the Public Employment Service (PES) released their latest unemployment statistics at 06:30 CET which showed an increase in the unemployment rate to 6.9%. According to PES's figures, the unemployment rate has been increasing for the past year, but the pace of said increase is less dramatic than what is implied by the often officially quoted figures from LFS. Still, the PES press release note that the labour market is clearly weak.

What happened yesterday

In Denmark, inflation increased to 1.6% y/y in October from 1.3% y/y in September, with higher electricity prices in particular driving the uptick. While inflation increased slightly, underlying price pressure remains modest, with the substantial wage growth not acting as an inflationary force in Denmark.

In Norway, October core inflation dropped to 2.7% y/y (cons: 2.7%), while the monthly figure fell to 0.2% m/m (cons: 0.3%). Details reveal a broad-based fall with lower price pressure in all main components apart from clothing/shoes - albeit much of it is base effects. Heading into this print it was widely expected that inflation once again would undershoot Norges Bank's projections at 2.9% y/y (September monetary policy report). That said, at this point, markets have widely understood Norges Bank's revealed preferences for waiting until March 2025 before delivering the first rate cut - also reiterated at last week's interim meeting last week. Given their preferences, the bar for a December cut has seemed high for some time, and we would likely have to see the real economy, particularly capacity utilisation, turn over sharply before a cut could come back into play. Hence, yesterday's print changed nothing in that regard.

In China, the credit data came in yesterday, showing a moderate improvement in October, but data remains soft in general. At the same time, money supply growth also rebounded (M1 from -7.4% y/y to -6.1% y/y, M2 from 6.8% y/y to 7.5% y/y), though coming from weak levels. With the stimulus taking hold, we project credit growth to pick up in the coming quarters. The big uncertainty now, however, is when and how much the impact will be of Trump's expected tariffs hikes on Chinese products - and the tit-for-tat trade war that may follow.

In Japan, the Lower House convened on Monday to select a new prime minister. As expected, the LDP retained power, re-electing PM Ishiba despite his scandal-hit coalition losing its parliamentary majority in last month's election. We will keep an eye on what the DPP's (whose support is critical to Ishiba) opposition to rate hikes might mean to the government's stance on monetary policy.

In commodities space, Oil prices were down almost 3% in yesterday's session amid China's stimulus plan disappointing investors hoping for stronger Chinese demand growth, a stronger USD and expectations of increased supply due to Trunp's pro-drilling stance. Later today, OPEC publishes its Monthly Oil Market Report, which includes major issues affecting the oil market and an outlook for oil market developments for the year to come.

In crypto space, Bitcoin continued its journey north. As of this morning, the world's biggest crypto currency is hovering around USD 88,600.

Equities: Global equities were higher yesterday; however, it is worth highlighting the calmness in the markets and the massive drop we have seen in implied volatility measures such as the VIX and Move indices. Yesterday was also devoid of significant fundamental events, with no important key economic figures or monetary policy developments. Therefore, it was a day when investors had the opportunity to reflect thoroughly following the immediate reaction to the US election. The largest disturbance was the US Veterans Day holiday, which meant that there was no trading of treasuries. In terms of sector rotation, we observed precisely what we anticipated, with cyclicals performing exceptionally well, led by financials, consumer discretionary, and industrials. That being said, one should not expect Tesla's post-election frenzy to continue. We even argue that there is a risk of it backfiring if Trump initiates a tariff war against Europe and Europe begins to retaliate. Materials underperformed, which we attribute to the disappointing messages emanating from China. Style-wise, small caps performed excellently yesterday, particularly in the US.

In the US yesterday: Dow +0.7%, S&P 500 +0.1%, Nasdaq +0.1%, Russell 2000 +1.5%.

Markets in Asia are lower this morning. China H-shares, along with Taiwan, are experiencing declines. The two major drivers here are the post-US election effects and the disappointing Chinese stimulus measures. In Taiwan, TSM, accounting for more than one-third of the main index, is leading the index lower after reportedly being ordered by the US to stop shipping chips used for AI to Chinese customers. Futures in Europe and the US are also lower this morning, with the Euro Stoxx 50 down by almost 1%.

FI: Yesterday, European government bond yields declined and extended the rally from Friday. 10Y German government bond yields have declined almost 20bp from the peak last week and are back below levels before the US election. The US bond market was closed yesterday, but we have seen a modest rise in US yields this morning in Asian Trade after a solid decline last week, where 10Y US Treasuries fell some 13bp on Thursday and Friday. Furthermore, after a long period with curve steepening the curves are flattening once again.

FX: Limited activity after the European close due to US holiday (Veteran's Day), but EUR/USD held on to the move below 1.07 from earlier in the session. The EUR was one of yesterday's biggest losers, not only vs USD but also against Scandies. The Brent oil price fell close to 3% but NOK/SEK barely moved, currently trading just above 0.98.

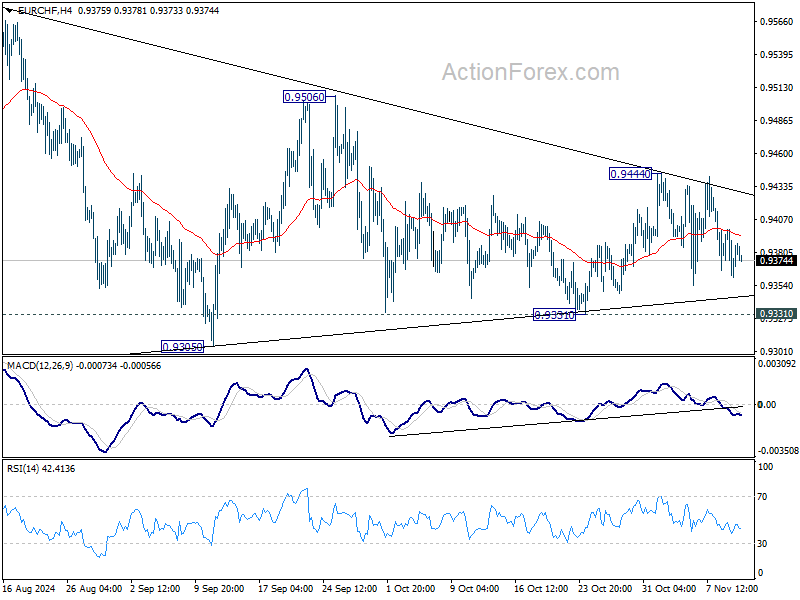

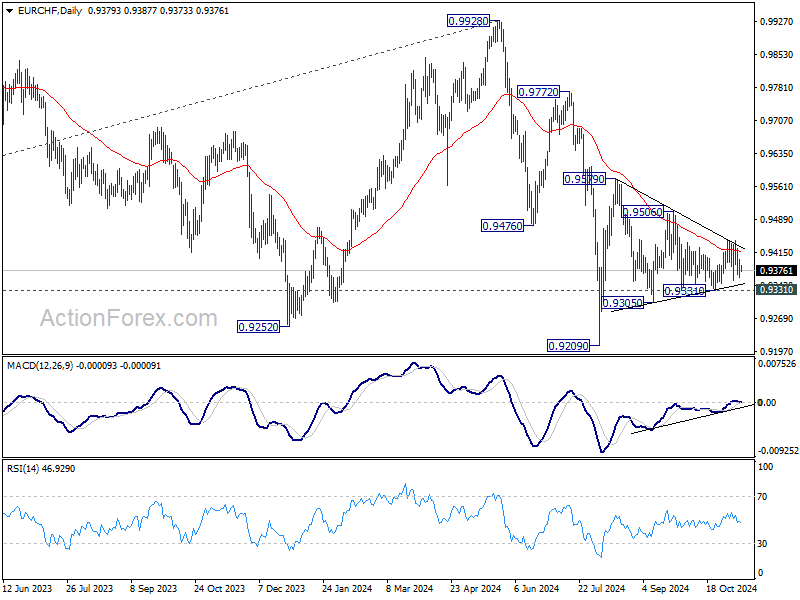

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9367; (P) 0.9383; (R1) 0.9405; More....

EUR/CHF continues to trade inside converging triangle and intraday bias remains neutral. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9419) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

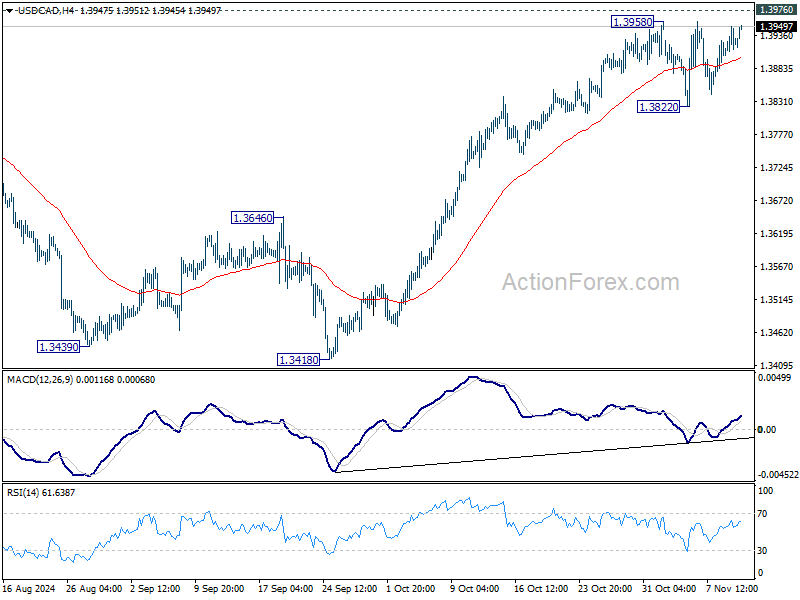

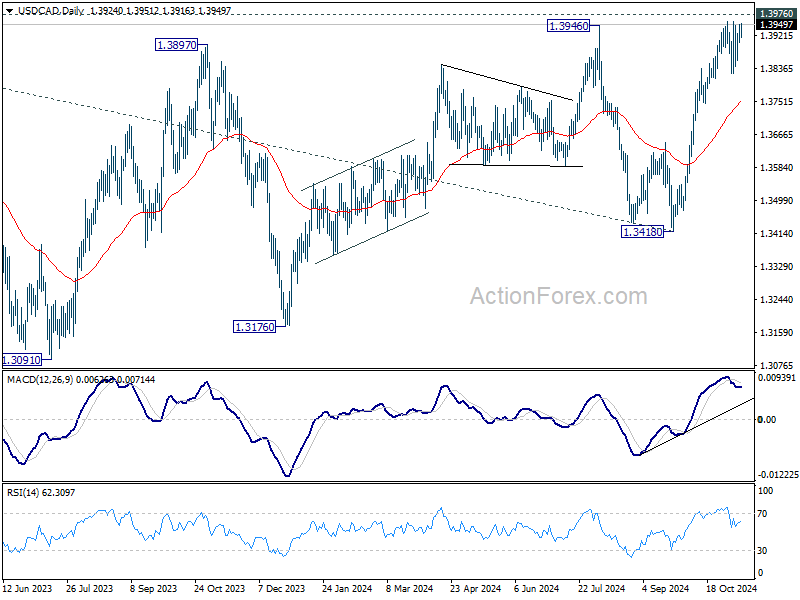

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3903; (P) 1.3927; (R1) 1.3949; More...

Sideway trading continues in USD/CAD below 1.3958. Intraday bias stays neutral, but further rise is is expected as long as 1.3822 support holds. On the upside, decisive break of 1.3976 key resistance will confirm larger up trend resumption. On the downside break of 1.3822 support will bring deeper pullback towards 55 D EMA (now at 1.3755).

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

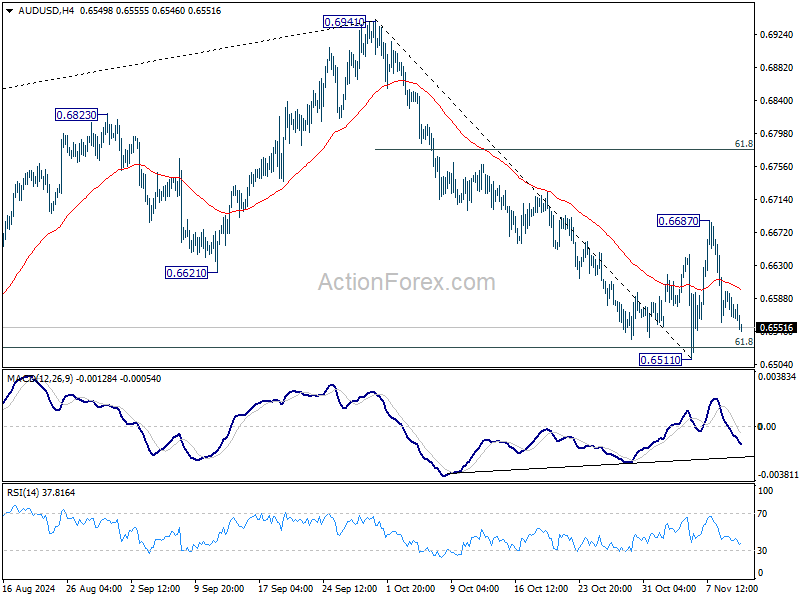

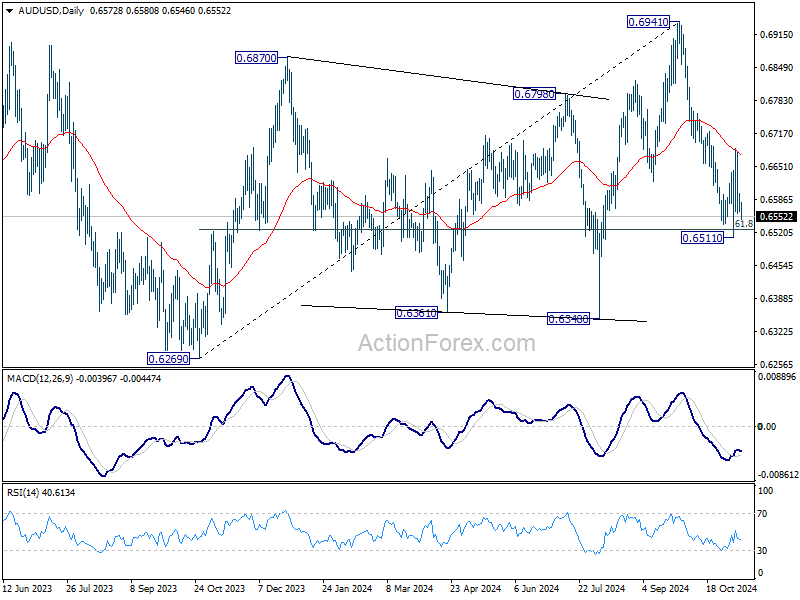

AUD/USD Daily Report

Daily Pivots: (S1) 0.6559; (P) 0.6579; (R1) 0.6594; More...

Intraday bias in AUD/USD stays neutral at this point. Further rise is mildly in favor as long as 0.6551 short term bottom holds. Above 0.6687 will target 61.8% retracement of 0.6941 to 0.6511 at 0.6777. On the downside, break of 0.6511 will resume the fall from 0.6941 instead.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

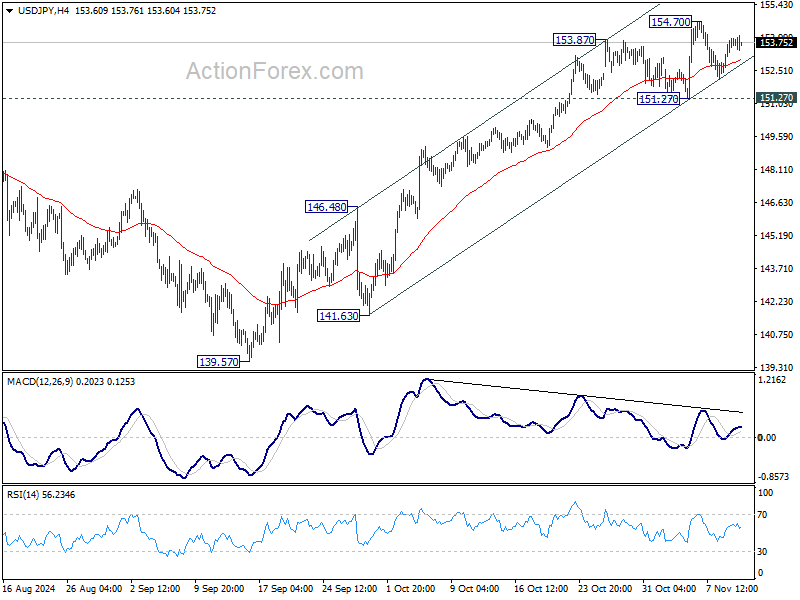

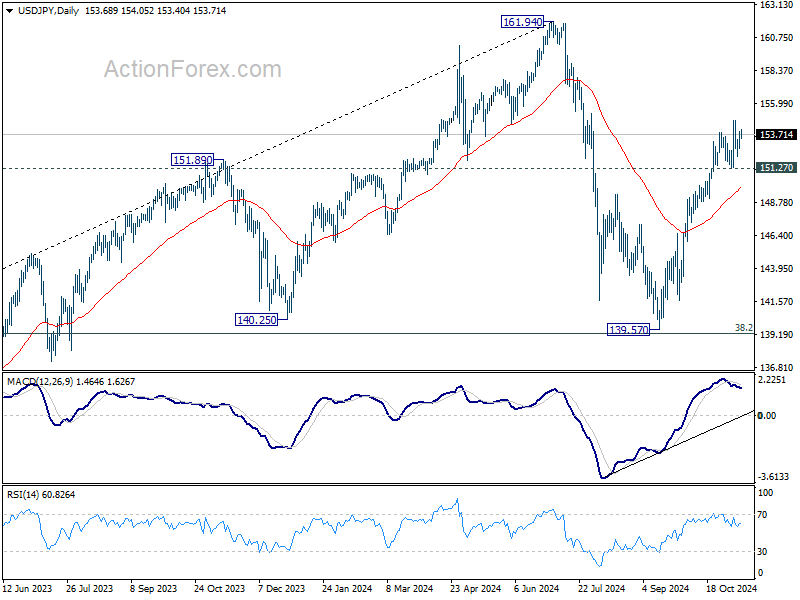

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.93; (P) 153.44; (R1) 154.25; More...

Intraday bias in USD/JPY remains neutral as sideway trading continues below 154.70. Further rise is expected as long as 151.27 support holds. Above 154.70 will resume the rally from 139.57 towards 161.94 high. However, considering bearish divergence condition in 4H MACD, break of 151.27 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 149.89).

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

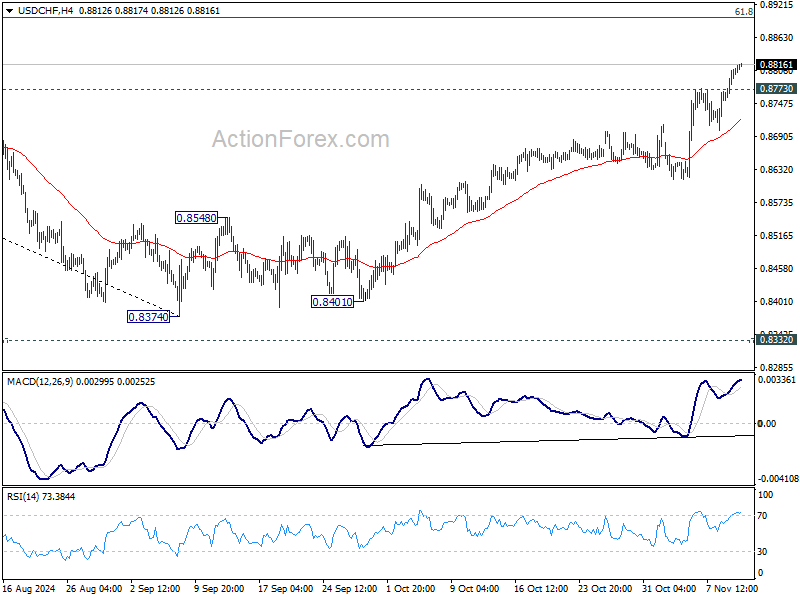

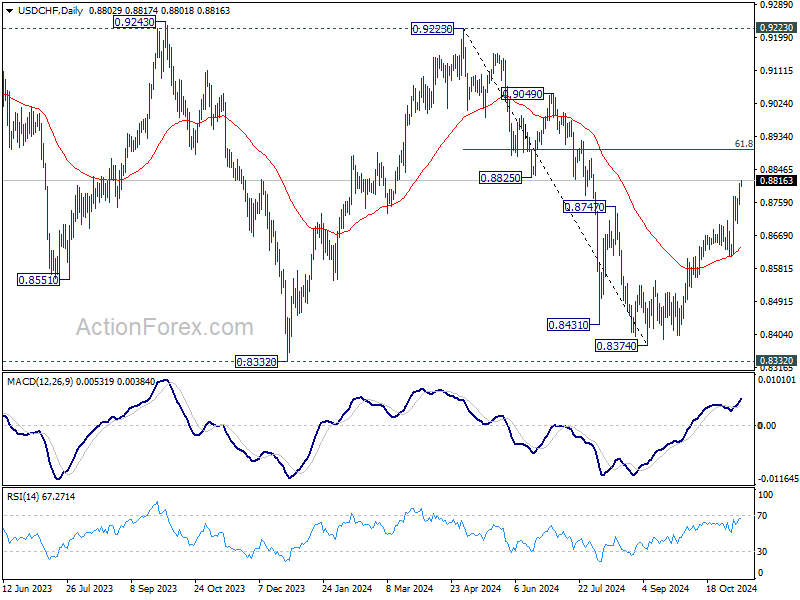

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8770; (P) 0.8790; (R1) 0.8790; More…

Intraday bias in USD/CHF remains on the upside for the moment. Current rally from 0.8374 is in progress for 61.8% retracement of 0.9223 to 0.8374 at 0.8899. Sustained trading above there will pave the way towards 0.9223 high. On the downside, below 0.8773 support will turn intraday bias neutral again and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0614; (P) 1.0671; (R1) 1.0713; More...

Intraday bias in EUR/USD stays on the downside at this point. Sustained trading below 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656 will extend the fall from 1.1213 to 100% projection at 1.0483. On the upside, above 1.0727 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0760 support turned resistance holds.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

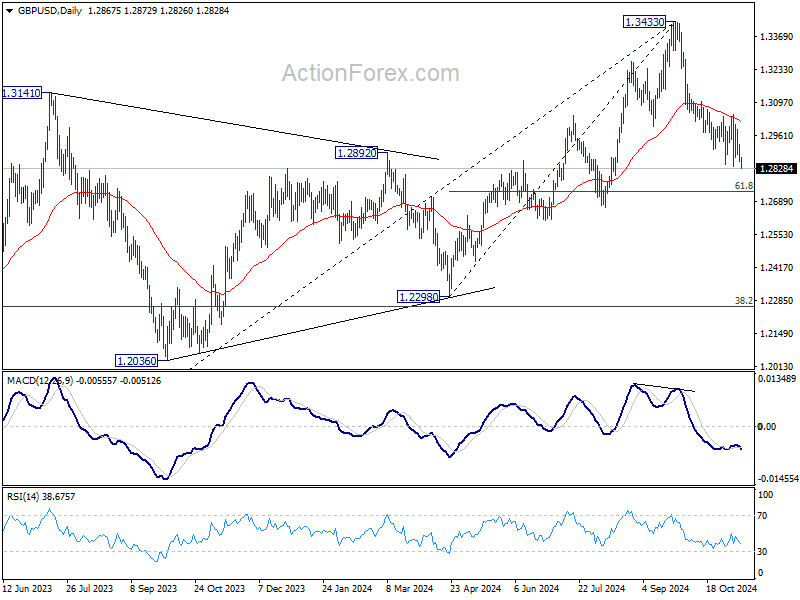

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2841; (P) 1.2884; (R1) 1.2911; More...

GBP/USD's breach of 1.2833 temporary low suggests that fall from 1.3433 is resuming. Intraday bias is back on the downside for 61.8% retracement of 1.2298 to 1.3433 at 1.2732. Sustained break there will pave the way towards 1.2298 key support. On the upside, above 1.3008 resistance will turn intraday bias neutral again first.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.