Sample Category Title

New Zealand Dollar Shrugs as Inflation Expectations Remains Near 2%

The New Zealand dollar is showing limited movement on Monday. In the European session, NZD/USD is trading at 0.5967, up 0.07% on the day. The New Zealand dollar was trounced on Friday, falling 1%.

New Zealand inflation expectations inch up to 2.1%

New Zealand inflation expectations inched higher to 2.1% in the fourth quarter, up from 2.0% in Q3. Expectations for one-year ahead annual inflation declined to 2.05% from 2.40%. The Reserve Bank of New Zealand keeps a careful eye on inflation expectations are they can translate into real inflation. Inflation has been on a downtrend and fell to 2.2% in the third quarter, the first time in over three years that inflation is back in the target band of 1% to 3%.

The RBNZ has been aggressive in its easing cycle in response to falling inflation. The central bank slashed the cash rate by 50 basis points to 4.75% last week and is expected to reduce rates by another 50 bp at the final meeting of the year on Nov. 27. The RBNZ is likely to continue trimming rates in 2025, with the pace and size of rate cuts largely dependent on inflation, employment and GDP.

China’s CPI ticks lower

China’s consumer prices rose 0.3% y/y in October, below the 0.4% gain in September and the lowest since June. This missed the market estimate of 0.4%. The monthly reading pointed to deflation, coming in at -0.3%, compared to 0% in September and lower than the -0.1% market estimate. China’s central bank announced in September aggressive stimulus to boost the sluggish economy and encourage more consumption, but the measures will take time to filter through the economy.

NZD/USD Technical

- NZD/USD has pushed above resistance at 0.5987 and is testing resistance at 0.6002

- There is support at 0.5957 and 0.5942

XAU/USD Outlook: Gold Holds in Red as Markets Await Fresh Signals from US Inflation Data

Gold remains at the back foot and stays in red for the second day on firmer dollar and also pressured by eased US political uncertainty, which recently fueled safe haven demand, along with geopolitics and expectations for stronger Fed rate cuts.

New circumstances after Trump’s victory point to measures which will boost economic growth and subsequently fuel inflation that requires revision of Fed’s current stance on monetary policy.

The latest remarks from Fed Chair Powell suggest that the US central bank will be likely less aggressive in rate cuts and that policy easing cycle would likely end earlier than initially planned, which may further dent metal’s safe haven appeal.

Pivotal supports at $2646/43 (Fibo 76.4% of $2602/$2790 / Nov 7 higher low) came under pressure, with break here to further weaken near-term structure and risk test of key supports at $2616/02 (top of thick rising daily Ichimoku cloud / Oct 10 trough), violation of which to generate reversal signal and open way for deeper correction.

Such scenario won’t be a surprise as gold was in steep uptrend and without significant correction for one year, however fundamentals, currently metal’s key driver, are expected to define fresh direction.

Technical studies weakened on daily chart as negative momentum continues to strengthen, MA’s (10/20/30-d) turned to bearish configuration and south-heading RSI points to more space for downside extension.

Adding to negative signals was last week’s bearish close with the biggest weekly loss since mid-May.

Markets focus on release of US October inflation data and speeches from several Fed officials (due later this week) which would provide fresh details on direction and the pace of changes in the US monetary policy in the near future.

Res: 2686; 2700; 2749; 2758.

Sup: 2643; 2600; 2560; 2471.

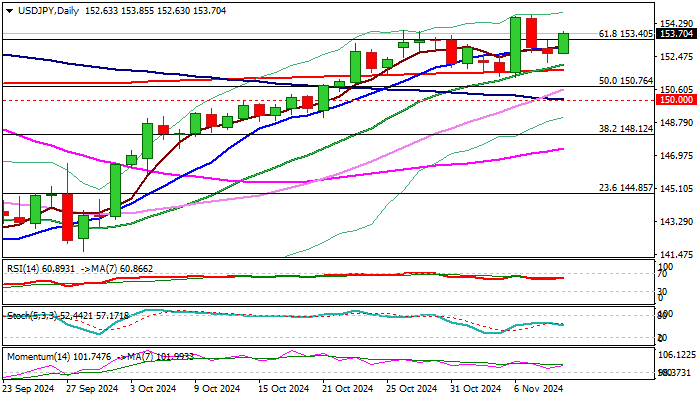

USD/JPY Outlook: Bulls Regain Control After Correction

USDJPY regained traction and bounced from 152.14 (low of two-day pullback from new multi-week tops), offsetting negative signal from bull-trap on weekly chart (failure to register weekly close above 153.40 (Fibo 61.8% of 161.95/139.57).

Fresh strength signals that the dollar is likely to continue benefiting from renewed Fed hawkishness on expectations that Trump’s administration will follow campaign’s promises and focus on boosting economic growth.

Technical studies on daily chart show strong positive momentum, with the latest formation of 20/200DMA golden cross, adding support.

We look for initial bullish signal on close above 153.40 Fibo level but lift and close above 154.70 double top (Nov 6/7 highs) to confirm signal and open way for acceleration towards next target at 156.67 (Fibo 76.4%).

Caution on potential repeated rejection a 154.70 pivot which would keep the price in extended consolidation, with bullish bias above correction low (152.14).

Stronger bearish signal to be expected on firm break of 151.70/30 zone (200DMA / recent range floor).

Res: 153.88; 154.70; 155.22; 156.67.

Sup: 153.40; 153.00; 152.14; 151.69.

GBP/USD Chart Analysis: Bears Apply Pressure to Key Support

According to ICE data, the U.S. Dollar Index futures have reached highs last seen in early July 2024. The dollar’s strength is attributed, in part, to anticipated economic stimulus measures outlined by the newly elected President Donald Trump during his campaign.

This has put pressure on other currencies paired with the dollar. Currently, the British pound is trading near 1.28400, close to a three-month low.

Today’s technical analysis of the 4-hour GBP/USD chart reveals:

→ long-term price fluctuations have shaped an upward channel since May;

→ the pair is near a key support level at the lower boundary of this channel;

→ a downtrend channel (in red) has formed since early October, highlighting recent bearish control; → the ATR indicator is at an annual high, indicating heightened volatility.

Key economic events are on the horizon:

→ UK labour market data on Tuesday at 10:00 (GMT+3),

→ U.S. CPI figures on Wednesday at 16:30 (GMT+3),

→ speeches by the Fed and Bank of England heads on Thursday.

With these events approaching, traders may anticipate continued wide fluctuations around the lower boundary of the upward channel.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

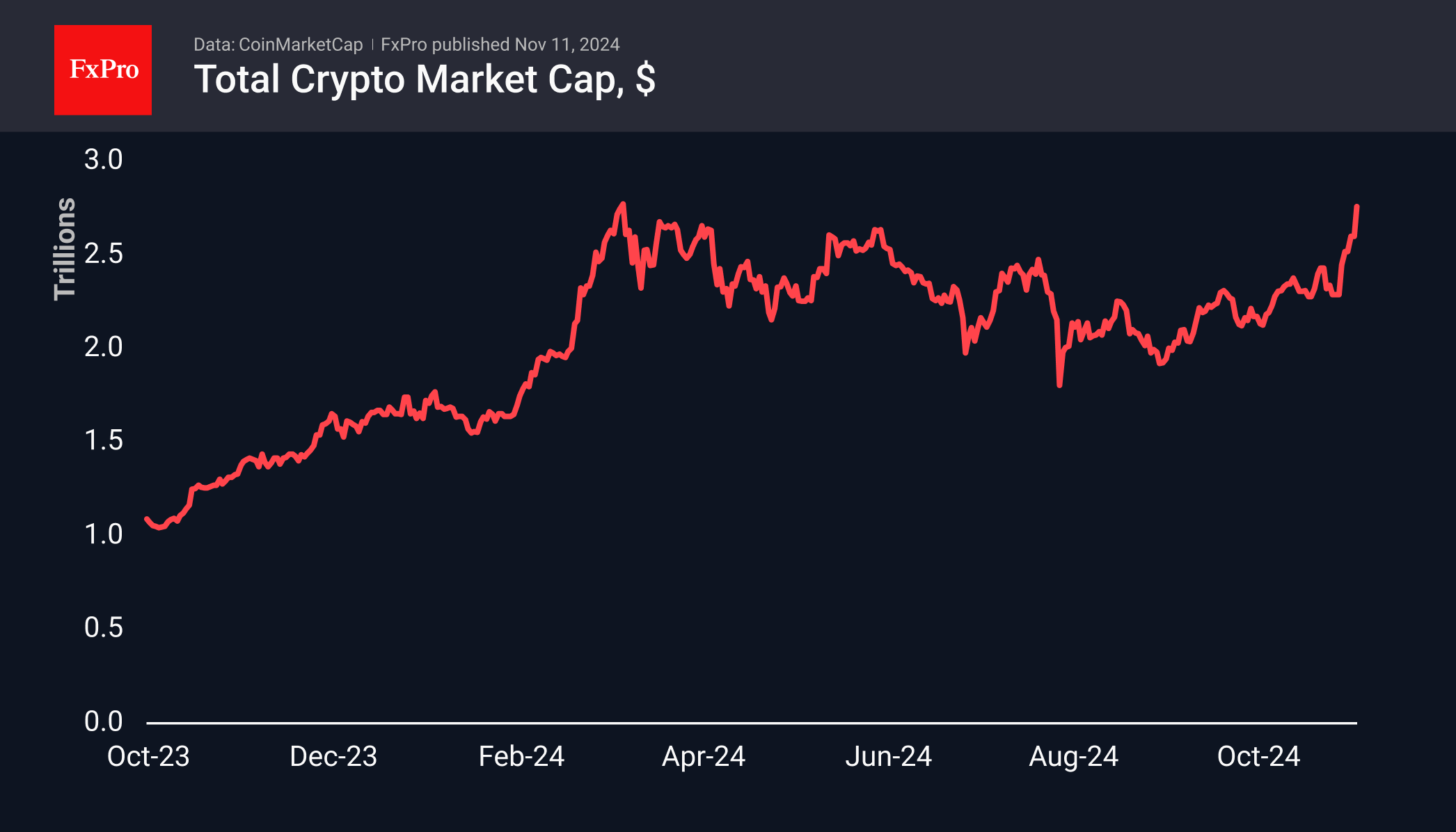

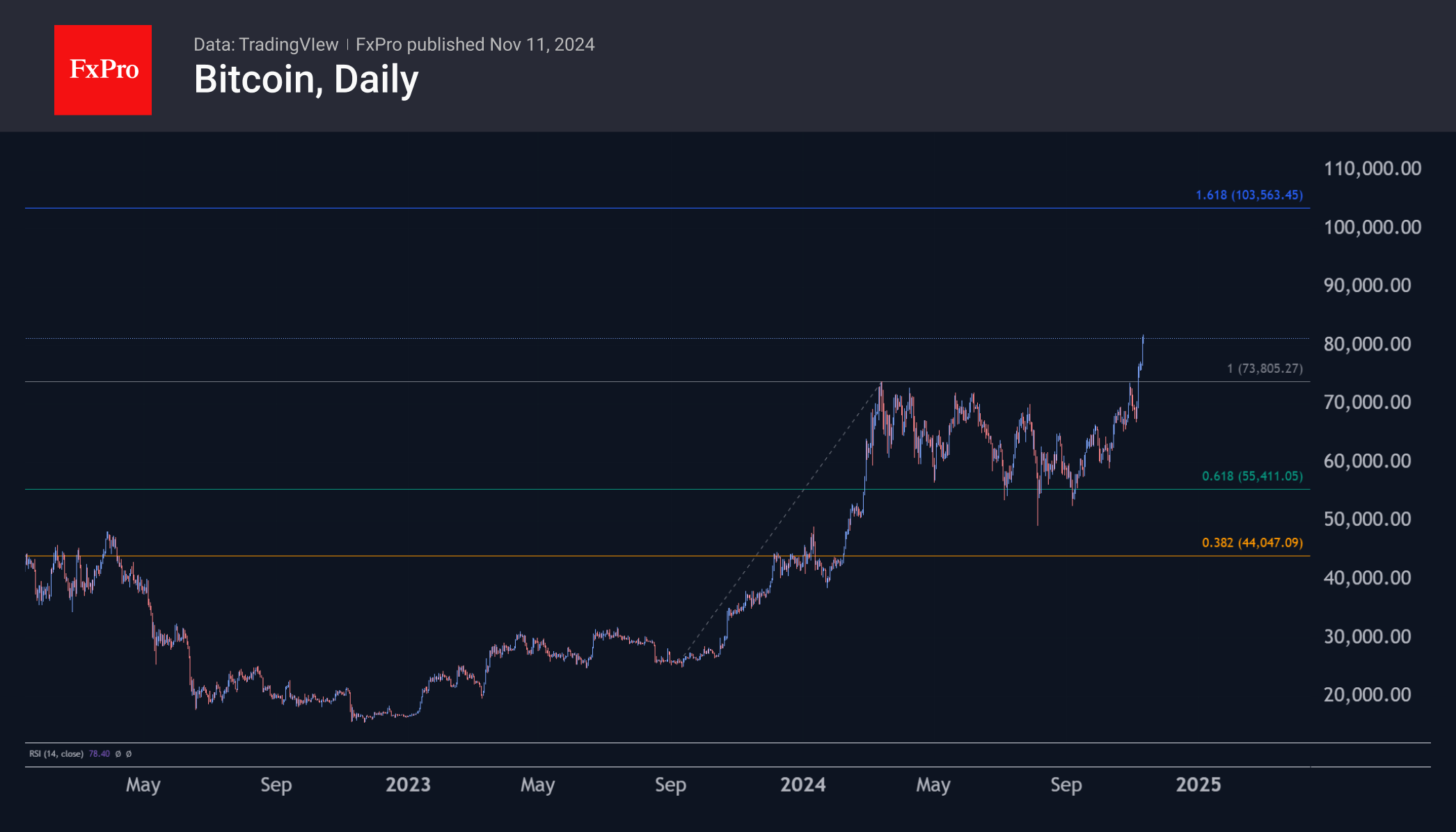

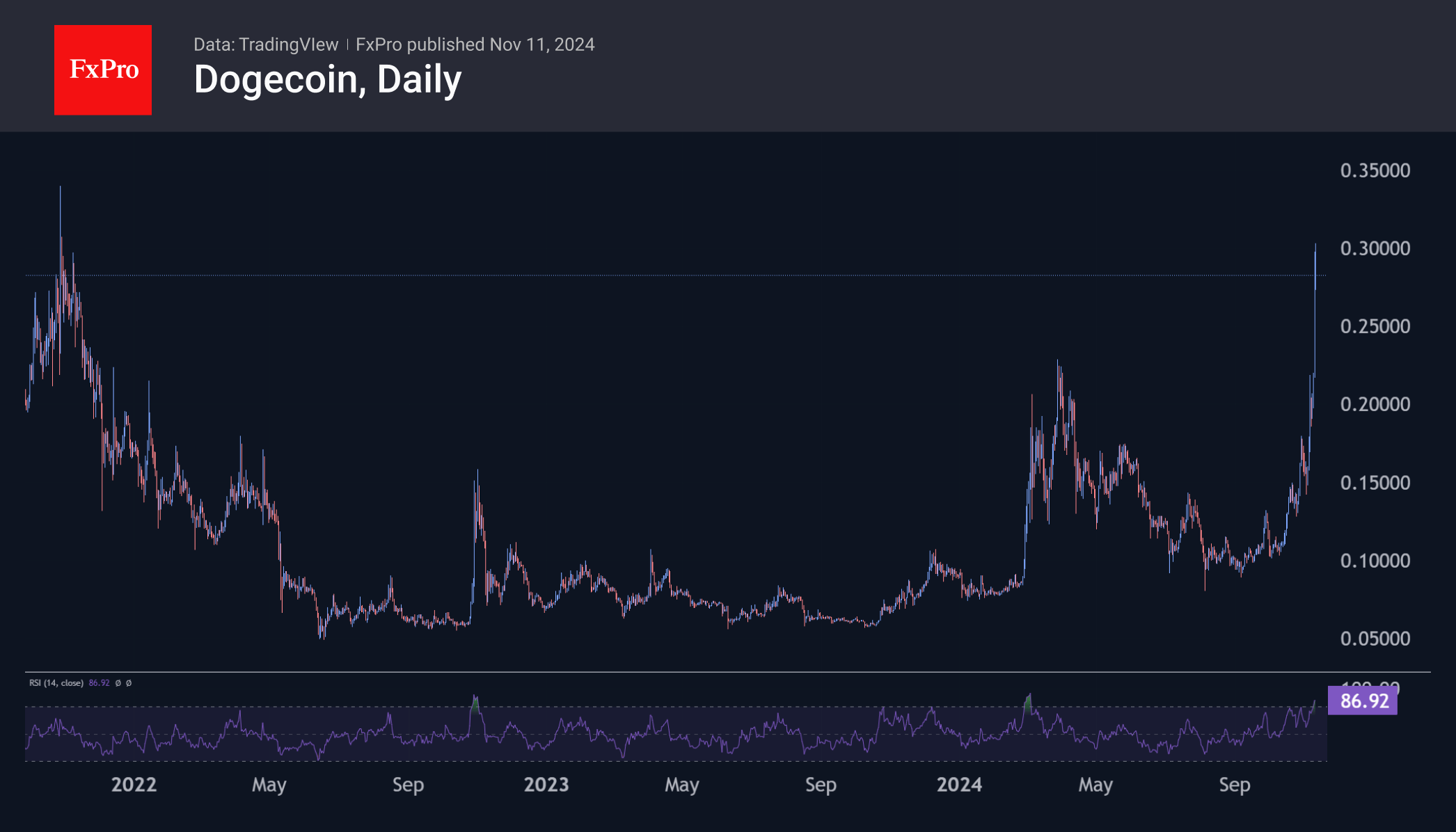

Altcoins Acceleration Amid Bitcoin’s New Heights

Market Picture

The crypto market capitalisation has reached $2.75 trillion, approaching the peak of $2.77 trillion reached in March this year. The next target for the crypto bulls looks to be the historical highs at $2.86 trillion and possibly even the next round level of $3.0 trillion.

Bitcoin has broken the upper boundary of the ascending channel, accelerating the renewal of historical highs. A key technical target and next milestone now appears to be the $100-110K area, as the five-month drift down from $73K to $50K looks like a correction of the bullish momentum from September 2023 to March 2024. The breakout to new highs confirmed the extension of the bullish momentum, making the 161.8% level the next target. Next, the $100-110K area should be ready for a major shakeout as many will be looking to take profits after impressive gains and on reaching key round levels.

.

Bitcoin is attracting attention with its all-time highs and weight in the crypto market. However, altcoins such as Dogecoin and Cardano, although far from their highs, more than doubled in value in the 5 days following Trump’s victory before correcting late on Sunday. Although both coins look overbought on daily timeframes, they are being driven by FOMO and short squeeze, which promises more chaotic moves in the coming days. Perhaps now is the time to pick up altcoins, which have so far shown growth rates averaging between Bitcoin and Dogecoin.

News Background

From a fundamental perspective, Bitcoin shows no signs of overheating. Galaxy Digital notes the lack of a spike in funding costs for perpetual contracts and a moderate increase in open interest (OI) for cryptocurrencies in general.

According to Fundstrat co-founder Tom Lee, Bitcoin prices will rise to “six figures” before the end of the year. He believes the likely reason for the interest in BTC is its potential as a reserve asset. Trump has previously promised to create a national Bitcoin reserve.

Technical analyst Peter Brandt commented on the optimal time to buy Bitcoin. According to him, the asset will rise another 73-100% and form a cycle top in August or September 2025.

The US SEC has postponed a decision on the NYSE’s proposal to list options-based spot Ethereum ETFs. The NYSE requested this from the SEC on August 7th.

Tether’s investment arm has funded a $45 million USDT crude oil deal that is “the first of its kind” and provides new lending opportunities in various areas, the company said.

The Ethereum Foundation (EF) reported $970 million in cash reserves, which includes liquid and vesting allocations. In 2022-2023, startups in the Ethereum ecosystem received $497 million in funding, according to the EF report.

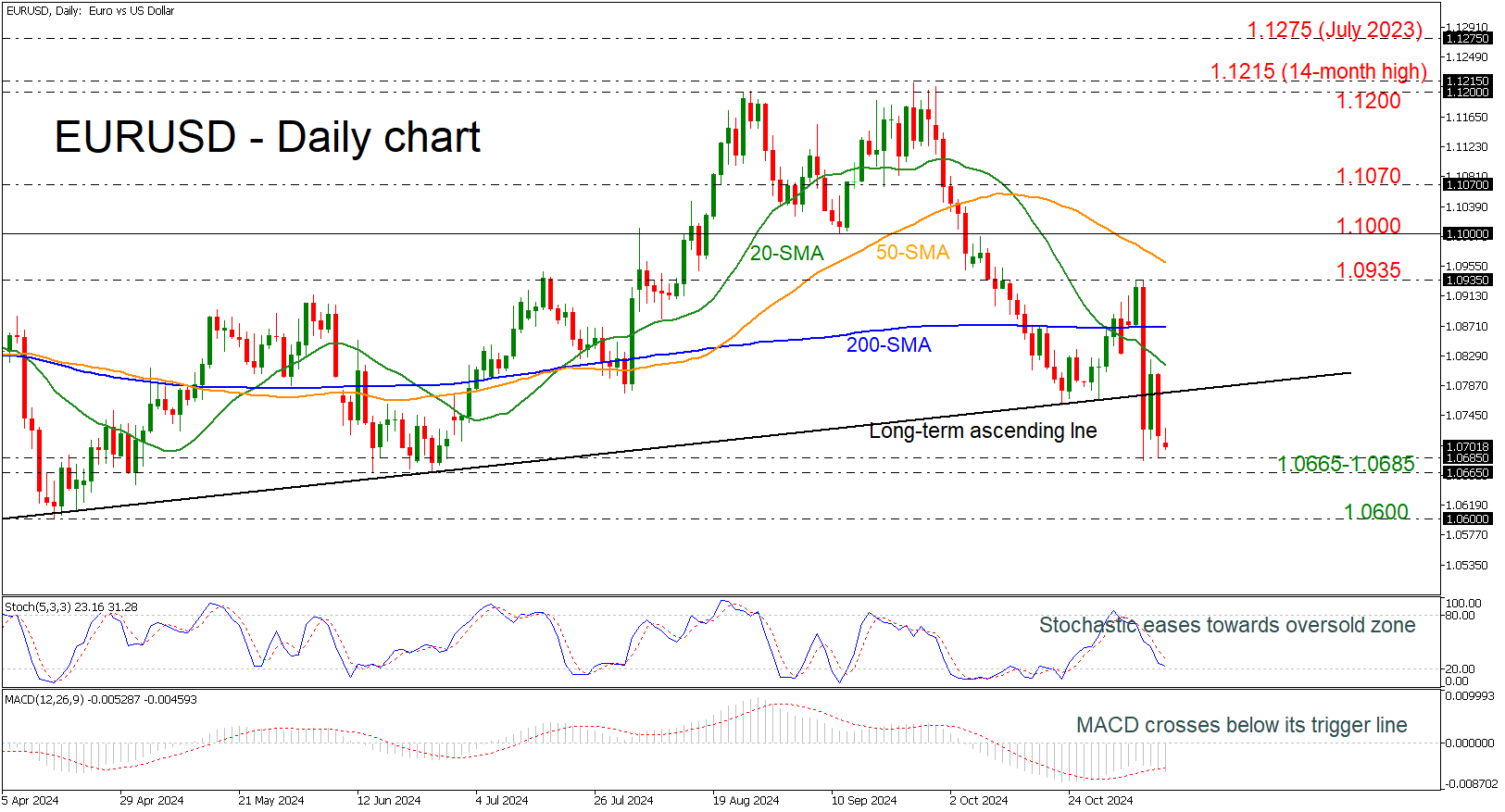

EURUSD Creates Negative Gap Near 1.0700

- EURUSD remains under selling pressure

- Next pause at 1.0665-1.0685

- Stochastics and MACD confirm bearish structure

EURUSD recently took a considerable dive, falling beneath the 1.0700 round number and developing below the long-term ascending trend line. The pair began the day with a negative gap, with the technical oscillator suggesting further declines. The stochastic is moving toward the oversold region, while the MACD is extending its bearish momentum beneath its trigger and zero lines.

If the market retreats further, it could test the restrictive supportive region of 1.0665-1.0685 before resting near the 1.0600 handle, creating a lower low.

On the flip side, a successful attempt above the ascending trend line could find significant obstacles at the 20- and 200-day simple moving averages (SMAs) at 1.0815 and 1.0870, respectively. Further up, the peak at 1.0935 could potentially halt the upward trend.

Overall, EURUSD has been shifting from a broader bullish outlook to a bearish one, particularly after the drop below the uptrend line.

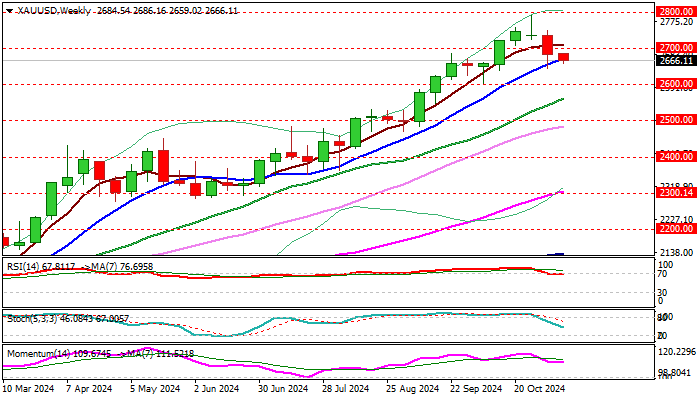

Gold Price Takes Hit While WTI Crude Oil Eyes Upsides

Gold price is declining below the $2,700 support zone. Crude oil price is rising and it could climb further higher toward the $75.00 resistance.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price failed to clear the $2,800 resistance and corrected lower against the US Dollar.

- There is a key bearish trend line forming with resistance at $2,725 on the hourly chart of gold at FXOpen.

- WTI Crude oil prices are moving higher above the $70.00 resistance zone.

- There is a key bullish trend line forming with support near $70.90 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price was able to climb above the $2,750 resistance. The price even broke the $2,765 level before the bears appeared.

The price traded toward $2,785 before there was a fresh decline. There was a move below the $2,760 pivot zone. The price settled below the 50-hour simple moving average and RSI dipped below 30. Finally, it tested the $2,645 zone.

The price is now consolidating losses near the $2,660 level. Immediate resistance on the upside is near the $2,668 level or the 23.6% Fib retracement level of the downward move from the $2,749 swing high to the $2,643 low.

The next major resistance is near the 50-hour simple moving average and the 61.8% Fib retracement level of the downward move from the $2,749 swing high to the $2,643 low at $2,708.

There is also a key bearish trend line forming with resistance at $2,725. An upside break above the $2,725 resistance could send Gold price toward $2,760. Any more gains may perhaps set the pace for an increase toward the $2,780 level.

If there is no recovery wave, the price could continue to move down. Initial support on the downside is near the $2,645 level. The first major support is $2,635. If there is a downside break below the $2,635 support, the price might decline further. In the stated case, the price might drop toward the $2,620 support.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a decent increase against the US Dollar. The price gained bullish momentum after it broke the $69.40 resistance.

There was a sustained upward move above the $70.00 and $70.90 levels. The bulls pushed the price above the 50-hour simple moving average and the RSI climbed toward 70. A high was formed near $72.31 before there was a downside correction.

The price declined below the 23.6% Fib retracement level of the upward move from the $69.43 swing low to the $72.31 high. However, the bulls are active above the 50-hour simple moving average.

There is also a key bullish trend line forming with support near $70.90. Immediate resistance is near the $72.30 level. If the price climbs further higher, it could face resistance near $73.50. The next major resistance is near the $74.20 level. Any more gains might send the price toward the $75.00 level.

Conversely, the price might correct gains and retest the 50-hour simple moving average or the 50% Fib retracement level of the upward move from the $69.43 swing low to the $72.31 high at $70.90.

The next major support on the WTI crude oil chart is near $70.10. If there is a downside break, the price might decline toward $68.75. Any more losses may perhaps open the doors for a move toward the $66.85 support zone.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Divergence

Last week ended on a very positive note for the US equity markets. All major indices rallied, the S&P500 notched its best week in more than a year and toped the 6000 level for the first time in history. The Dow Jones traded past the 44’000 level for the first time as well, while Nasdaq 100 closed above 21’100, and small caps approached at ATH, despite some investors pessimism that the Trump-fuelled US yields could backfire on small caps as they have smaller margin to shoulder higher-than-otherwise borrowing costs. And indeed, the Minneapolis Federal Reserve (Fed) President Neel Kashkari said that the bank could lower the rates less than previously anticipated, but he rather pointed at the strength of the US economy rather than Trump policies. He said that it’s too early to determine the impact of what’s to come in terms of Trump policies. If the new President favours tax cuts over tariffs, the US equities could continue to surf on a wave of optimism, while focusing on tariffs before tax cuts would brush off a part of the present optimism.

For now, optimism prevails. During the weekend, the Trump optimism continued to show in Bitcoin prices. The price of a coin spiked past the $81’000 level, and the next natural target on the grill is the $100’000 psychological level.

That’s the American leg of the story: the picture remains bullish for the US equities. Elsewhere, worries mount: FTSE 100 and the European Stoxx 600 index both closed last week below the 200-DMA on worries about a heated international trade environment and the Chinese leg of the story is much less dreamy, too. China announced that it will deploy 10 trillion yuan to refinance local government debt, as expected by investors. Alas, the announcement failed to revive optimism as many were hoping to see bigger measures deployed in response to Trump presidency – who is now expected to increase tariffs on Chinese goods to 60%. As such, the big banks are back to cutting their growth forecasts for China. Standard Chartered and Macquarie expect the increased US tariffs to shave 2 percentage points off annual growth. While UBS trimmed its growth forecast from 4.5% to 4%.

The data released during the weekend wasn’t encouraging, either. Consumer inflation in China came in line with expectations, but deflation in producer prices unexpectedly accelerated last month to -2.9% on a yearly basis, and came as a mixed signal on the impact of the stimulus measures on the Chinese economy. As such, the CSI 300 bounced lower on Friday and erased a part of last week’s gains that were built on optimism that the Chinese stimulus measures would – this time – please.

And crude oil is under a renewed pressure since Friday, on China’s failure to wet investors’ appetite with fiscal stimulus measures. The barrel of US crude is back testing the $70pb support to the downside, having erased past week gains that were supported by geopolitical worries and hints that OPEC would delay the end of its production restrictions by at least a month. Iron ore is also under pressure, the spot price slipped below the 100-DMA and the latter weighs on the Aussie.

Elsewhere, in the FX, the US dollar index remains bid on rising uncertainties regarding the Fed’s easing path. For now, the markets still expect the Fed to deliver another 25bp cut before the year ends, but that probability fell from above 70% to below 65%. The data – especially the inflation data – will gain importance moving forward as Trump policies – the tax cuts and tariffs – are inflationary and will certainly limit the Fed’s capacity to ease wholeheartedly. This week, investors will focus on the next US CPI update, due Wednesday. The headline inflation is seen steady at 2.4% and core inflation unchanged at 3.3%. Higher-than-expected figures could further awaken the Fed hawks and support the dollar bulls against major peers.

Speaking of major peers, the EURUSD is testing the 1.07 support to the downside. The Trump’s tariff threat on European imports has become one of the major drivers here as well, combined with the troubled French finances and the chatter of early election in Germany. A further retreat is on the cards, unless we see a surprise easing in US inflation. Across the Channel, Cable consolidates below the 1.30 level. The Bank of England’s (BoE) less dovish stance after the UK budget is countered by a broad-based dollar strength, yet sentiment in EURGBP reflects well the divergence between more dovish ECB expectations and less dovish BoE expectations. And the latter points at a possible and a sustainable advance in EURGBP to 0.80/0.82 area.

Light Macro Weak Ahead

In focus today

In Denmark, October inflation data is due, with energy and food prices expected to drive up inflation to 1.7% y/y from 1.3% y/y in September.

Similarly, Norway's October inflation figures are released today. We forecast core inflation to have eased to 2.6% y/y, with a slight risk to the upside. We do not expect a reading below Norges Bank's estimate to trigger a rate cut in December.

While last week saw many significant market events, this week's schedule is lighter. On Tuesday, the German ZEW for November will be released, and the key event - U.S. October inflation data - is set for Wednesday. On Friday, the European Commission is set to publish its new economic forecasts, while US retail sales and industrial production data is also due for release. During the week, we receive Chinese credit data, but no specific date has been set. The figures could give an early indication of the effect of the stimulus.

Economic and market news

What happened since Friday

In the US, the University of Michigan's flash consumer sentiment survey for November hit a seven-month peak, rising to 73.0 from 70.5, with the expectations index reaching a 3.5-year high, up nearly 6% to 78.5. Consumers are now less concerned about near-term inflation, with 1y expectations dropping to 2.6% from 2.7%, while 5y expectations edged up to 3.1% from 3.0%.

Turning to politics, Republicans are close to securing control of the House with 214 seats confirmed, needing four more seats to keep a majority, and underscoring that the Republican party is close to sweeping the Congress. A Republican sweep would pave the way for Trump's political agenda, likely implying fiscal policies that could increase the budget deficit, public debt and ultimately inflationary pressures. With Arizona also counted, President-elect Trump won all swing states.

In China, the fiscal policy announcement on Friday fell short of expectations, offering no specific stimulus figures beyond a pledge to be "forceful." That said, there was an announcement of a CNY 6tn local government debt swap program which should ease the situation for local governments and make them able to support the economy more. All in all, it remains unclear to what extent policies will be able to turn the situation around for Chinese growth. Moreover, Chinese October inflation data came in lower than expected at 0.3% y/y and -0.3% m/m (cons: 0.4% y/y, -0.1% m/m).

In Germany, incumbent Chancellor Scholz stated on Sunday he is willing to call a vote of confidence before Christmas, moving up his initial proposal of January 15 amid rising political and public pressure.

In crypto space, Bitcoin surpassed USD 80,000 for the first time on Sunday following Trump's sweep of all swing states and expectations of a more pro-crypto administration. At the time of writing, Bitcoin is hovering around USD 81,600.

Equities: Global equities ended higher on Friday and concluded the week on a positive note, with considerable attention focused on the US election, alongside some notable sector and regional differences. However, observing the sector performance on Friday and regional performance this morning, one can discern a China-effect on the markets. Post-cash close on Friday, Beijing released details on both the local government debt swap programme and additional stimulus measures. However, especially the stimulus part surprised on the downside, resulting in the underperformance of the materials sector and Chinese equities this morning.

Aside from the China effect, defensives were seen outperforming cyclicals on Friday. We do not believe this marks the beginning of a trend where defensives will consistently outperform following the election, but rather it should be viewed in the context of the substantial outperformance of cyclicals over the last three months. Cyclicals have risen by 15%, while defensives have increased by 1.3% in the last three months. In the US on Friday, the Dow closed up by 0.6%, the S&P 500 by 0.4%, Nasdaq by 0.1%, and the Russell 2000 by 0.7%.

Asian markets are lower this morning, led by Chinese H-shares. Futures in Europe and the US are higher.

FI: Friday was another action-packed trading session in fixed income markets. Long-end EUR rates reversed the bulk of the increases seen on Thursday as the Chinese fiscal announcement on Friday was disappointingly unclear. The Bund ASW-spread turned positive, closing at 1.6bp, as Chancellor Scholz said he is open for discussing a timing of early elections already in January. New polling suggests that 2/3 of German voters want the election as early as possible. 10Y US Treasury yields fell a couple of basis points throughout an uneventful US session. But as the majority will likely be razor-thin, markets should continue to trade the 'Republican light sweep' narrative.

FX: The eventful past week ended with broad USD strength across the G10 space. EUR/USD declined to the lower end of the 1.07-1.08 range. The JPY gained momentum in the latter half of last week, pushing USD/JPY below 153 as the likelihood of a December BoJ hike gained traction, with 11bp now priced in, up from 8bp a week ago. EUR/GBP drifted below 0.83. The Scandies traded heavily on Friday, with EUR/NOK around 11.80 and EUR/SEK at 11.60.

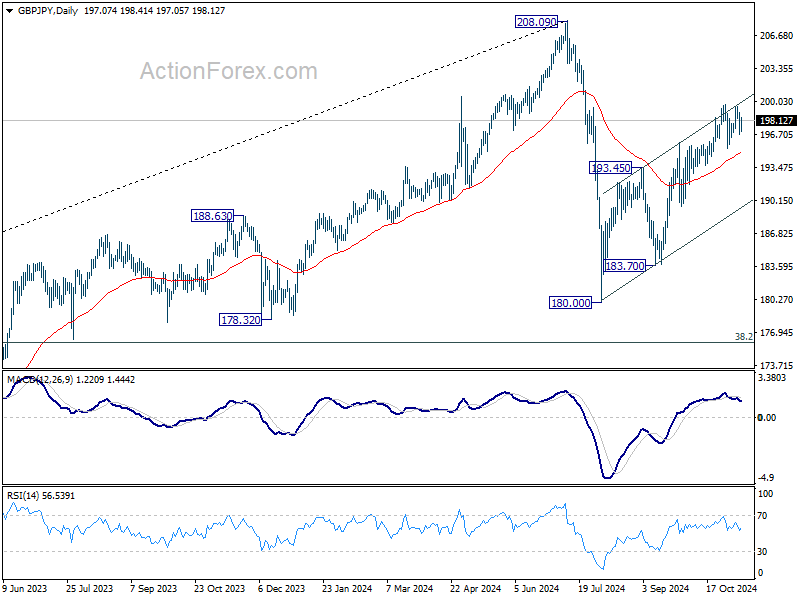

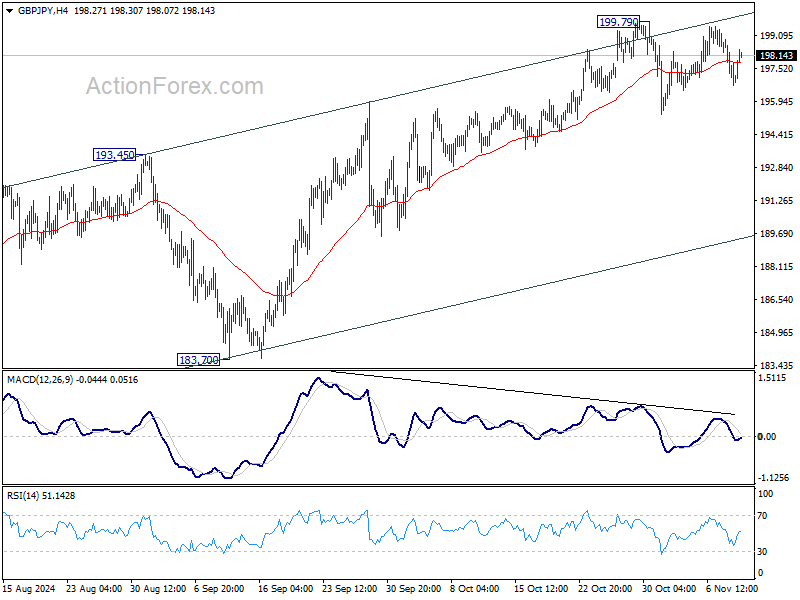

GBP/JPY Daily Outlook

Daily Pivots: (S1) 196.32; (P) 197.62; (R1) 198.50; More...

Intraday bias in GBP/JPY remains neutral and more consolidations could be seen below 199.79. Further rally is expected as long as 55 D EMA (now at 194.99) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.