Sample Category Title

Dollar Holds Strong Against Europeans, Awaits Fed Insights

Dollar strength and European weakness is currently the main theme in the markets this week so far. The greenback shrugs off strong risk-on sentiment, as reflected in another day of record closes in major US indexes, with strong momentum against Euro and Swiss Franc.

A lineup of Fed officials today will provide commentary that could shed light on the central bank’s stance as markets look for cues about its policy easing pace moving forward. However, the most anticipated event remains tomorrow’s US CPI release. While another 25bps cut is widely expected in December to round up the year, the outlook for rate reduction in 2025 remains highly uncertain.

Meanwhile, Sterling is also on the verge of breaking to new low against the greenback. Focuses is now on UK job data today, with attention particular on wages growth. Euro will also look into ZEW economic sentiment, which might reveal some reactions to US elections.

Commodity-linked currencies are among the stronger performers this week, after Dollar, supported by the prevailing risk-on environment. Meanwhile, Yen is mixed in the middle.

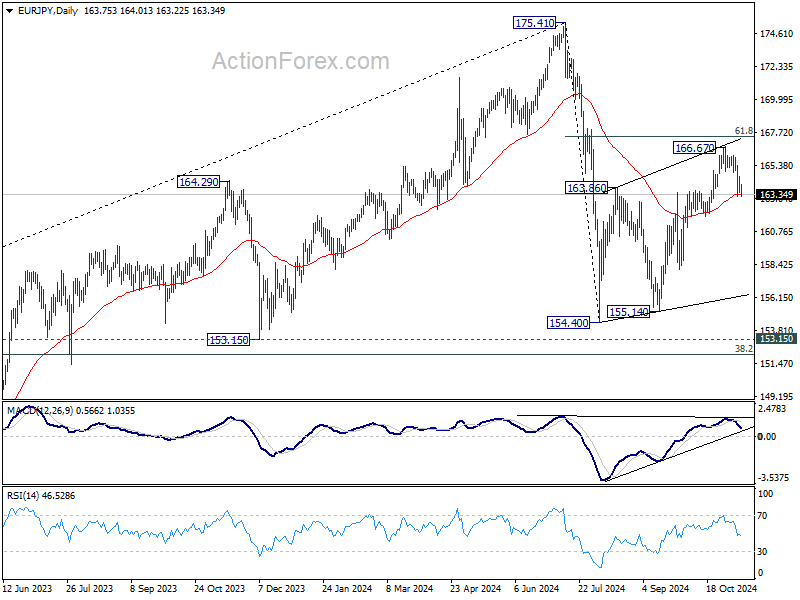

Technically, a focus for rest of the week is whether Euro's decline will persist and if Yen can extend its near term rebound. EUR/JPY is now pressing 55 D EMA (now at 106.33). Sustained trading below there would argue that the corrective rise from 154.40 has completed with three waves up to 166.67. In this case, near term outlook will be turned bearish for 155.14/154.40 support zone.

In Asia, at the time of writing, Nikkei is down -0.98%. Hong Kong HSI is down -2.81%. China Shanghai SSE is down -0.93%. Singapore Strait Times is down -0.95%. Japan 10-year JGB yield is up 0.0022 at 1.004. Overnight, DOW rose 0.69%. S&P 500 rose 0.10%. NASDAQ Rose 0.06%. 10-year yield rose 0.002 to 4.308.

Australian Westpac consumer sentiment jumps 5.3%, but US election casts shadow on outlook

Australian consumer sentiment saw a solid rebound in November, with Westpac Consumer Sentiment Index climbing by 5.3% mom to reach 94.6. This marks a 14.4% rise from its mid-year low, leaving it just 5.4 points shy of the neutral 100 mark.

The improvement was led by increased optimism about the short-term economic outlook. The "economic outlook, next 12 months" sub-index jumped 8.7% to 100.9, the first optimistic reading (above 100) since post-COVID recovery. Confidence around personal finances also strengthened, with the "family finances, next 12 months" sub-index up 4.4% to 104.1. Meanwhile, Unemployment Expectations Index dropped by -7.2% to 120.5, indicating the highest level of labor market confidence since April 2023.

Westpac noted three important observations in November's sentiment trends. First, confidence reached 99.7 in the early survey period, prior to RBA’s rate decision, reflecting marked optimism. Secondly, consumer sentiment remained unaffected by RBA's decision to hold rates steady. Lastly, sentiment dropped sharply after US election result, averaging 91.1 in the survey’s latter half. This indicates an unusually wide range of ±5% for November's final read, suggesting a degree of uncertainty not typically seen.

Australian NAB business confidence surges to 5, easing cost pressures but persistent retail inflation

Australia's NABs Business Confidence Index jumped from -2 to 5, marking a notable improvement after a prolonged period of below-average sentiment. Business conditions remained stable at 7, while trading conditions saw a slight increase from 12 to 13. Profitability held steady at 5, and employment conditions edged lower from 5 to 3.

Gareth Spence, NAB’s Head of Australian Economics, highlighted the jump in confidence as an encouraging development, noting that it is “just one month” but shows "tentative improvement" in forward orders, suggesting possible momentum.

Input cost pressures continued to ease, with labor cost growth decelerating from 1.9% to 1.4% on a quarterly basis from 1.9%, and purchase cost growth slowing from 1.3% to 0.9%. Retail price growth, however, saw a rebound, rising from 0.6% to 1.1%.

Spence noted, "The survey, like other price indicators, continues to suggest an ongoing gradual easing in inflation pressure, but also that there is still some way to go in in the inflation moderation when we look at the consumer facing components”.

Bitcoin extends powerful rally amid "Trump Pump" optimism, ready for 100k milestone

Bitcoin's robust rally continues at the start of this week, buoyed by the so-called "Trump Pump" effect. Cryptocurrency investors are optimistic about US President-elect Donald Trump's promises to create a more supportive and friendly regulatory environment for crypto businesses.

The crypto market has long struggled with a lack of regulatory clarity, and these anticipated policy changes are fueling strong positive sentiment. Expectation of a more defined regulatory framework is encouraging both institutional and retail investors to increase their exposure to Bitcoin, driving further price appreciation.

Such optimism is expected to persist through the rest of 2024, with Bitcoin setting its sights on the significant 100k mark.

Technically, Bitcoin is in clear upside acceleration as seen in D MACD. The immediate focus is on 161.8% projection of 58846 to 73608 from 66763 at 90647. Break could push Bitcoin a bit further higher to 200% projection at 96287.

The real test lies in medium term level at 100% projection of 24898 to 73812 from 52703 at 101617, which is slightly above 100k psychological level. Strong resistance could be seen there to bring consolidations on first attempt.

Looking ahead

UK employment and Germany ZEW economic sentiment are the main feature in European session. Later in the day, US will release NFIB small business index, and Canada will puiblish building permits.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2841; (P) 1.2884; (R1) 1.2911; More...

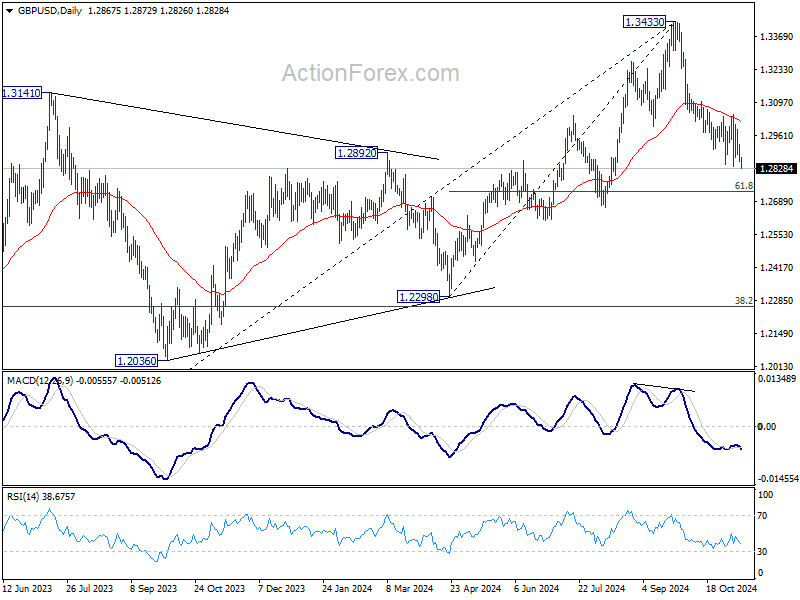

GBP/USD's breach of 1.2833 temporary low suggests that fall from 1.3433 is resuming. Intraday bias is back on the downside for 61.8% retracement of 1.2298 to 1.3433 at 1.2732. Sustained break there will pave the way towards 1.2298 key support. On the upside, above 1.3008 resistance will turn intraday bias neutral again first.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

RBNZ Preview: Maintaining Pace Towards the Neutral Zone

- We expect the RBNZ will cut the OCR by a further 50bps to 4.25% at its November Monetary Policy Statement meeting.

- The RBNZ will likely indicate increased confidence that pricing and wage setting behaviour will quickly normalise now that annual CPI inflation is close to 2%.

- The RBNZ’s projections will likely suggest further OCR cuts in 2025 and a 3.5% OCR by year-end (around 35bps lower than they forecast back in August). The RBNZ’s terminal rate will likely still be in the 3-3.5% zone after 2025.

- Near-term CPI projections should be revised down modestly, reflecting the better starting point.

- We are not expecting major changes to the Bank’s economic growth projections, although recent improvements in commodity prices and a slightly more front-loaded easing cycle might lift near-term growth at the margin.

- The RBNZ will likely acknowledge the elevated geopolitical risks associated with political change in the US, which could impact the NZD and tradable inflation going forward. Few conclusions will be drawn given the significant uncertainties.

RBNZ decision and associated communication – our baseline scenario.

Our baseline scenario sees the RBNZ cutting the OCR by 50bp to 4.25% at its November policy meeting. We also expect that the RBNZ will revise down their OCR forecast profile to be consistent with the OCR reaching around 3.5% by the end of 2025 (compared with 3.85% in the August MPS).

At the end of this note we summarise key data and developments over the past few months. Based on the latest information to hand, we think the RBNZ will:

- express comfort that lower headline inflation (now at 2.2%y/y) gives confidence that price setting behaviour and inflation expectations will be consistent with inflation around 2% on an ongoing basis;

- explain that this confidence has allowed for more front-loading of the easing cycle, resulting in the OCR being cut by 50bps in October and again this month;

- note that recent activity and employment trends remain broadly in line with expectations;

- continue to point to elevated non-tradables inflation, so that restrictive conditions and a negative output gap remain appropriate for a while to squeeze out the last of those inflation pressures;

- acknowledge the riskier geopolitical environment, but draw no strong conclusions at this point aside from noting that NZ’s floating exchange rate will help buffer adverse external shocks that eventuate; and

- provide guidance that if the economic outlook evolves as anticipated, the pace of easing will slow in 2025 as the OCR draws closer to the neutral zone.

Alternative scenarios.

Around that baseline scenario, to which we attach a 50% probability, we see four other potential outcomes at next week’s policy meeting:

- Hawkish scenario (15% probability): 25bp cut. The RBNZ might opt for a smaller cut, noting that the starting point for the economy has not been quite as weak as depicted in the August MPS and that downside risks appear less prominent. As part of that scenario the RBNZ could revise up their neutral OCR to 3-3.25%, reflecting higher long-term interest rates in NZ and abroad. Risks around the exchange rate and the sustainability of weak tradable inflation could be highlighted, as could the more elevated pricing intentions trends in the ANZ’s business survey. Stronger NZ commodity export prices – especially dairy prices – could also be seen as supporting the medium-term outlook.

- Moderately hawkish scenario (20% probability): 50bp cut but only slightly reduced end-2025 OCR forecast. The RBNZ would signal ongoing cuts at the MPS meetings in the first half of 2025 but to an end 2025 level of around 3.75%, perhaps due to concerns that ongoing disinflation in tradables might be less sustainable given downside risks to the exchange rate. Signs of a rebound in activity in the housing market and business surveys might also cause the RBNZ to project a more cautious approach in 2025 as the neutral zone for the OCR approaches.

- Moderately dovish scenario (10% probability): 50bp cut and end 2025 forecast OCR revised down to market pricing levels of around 3.25%. The RBNZ could largely endorse market pricing, with a move towards a 3% terminal OCR projected to be largely completed by the end of 2025. The RBNZ would need to be willing to signal high confidence that wage and price setting behaviours have normalised, and that upside inflation risks seem modest.

- Dovish scenario (5% probability): 75bp cut. The RBNZ would be signalling high confidence that inflation will remain no higher than 2% and perhaps concern that the recovery in economic activity might be more sluggish than hoped. Thereafter, 50bp cuts would seem most likely at the February 2025 MPS and April MPR meetings as the OCR is pushed to 3% by mid- 2025. We don’t think the RBNZ would signal a move in the OCR below 3% in 2025 but the risks that this might ultimately be required could be noted. This could especially be the case if the RBNZ sees predominantly downside risks coming from recent geopolitical trends (e.g., China deflation, or an unjustified rise in global long-term interest rates).

Key developments since the August Monetary Policy Statement.

Key economic developments since the RBNZ’s last policy statement in August are noted below. We suspect that the RBNZ will conclude that activity and pricing indicators released since the August projections provide a basis for increased confidence that inflation will track close to the midpoint of the 1-3% target range on a sustained basis.

- Inflation: September quarter inflation was a touch softer than the RBNZ forecast (+2.2%yr vs August MPS forecast +2.3%). Lower tradables and especially energy prices explain much off the move lower in headline inflation. In contrast, non-tradables inflation has been easing more gradually, albeit with some clear progress lower once government charges are excluded. Lower tradables inflation means some chance the RBNZ will project headline inflation a little below 2% for a brief period.

- Inflation expectations/pricing indicators: On balance, most gauges of cost and pricing pressures are looking increasingly consistent with the RBNZ’s medium term target (the ANZ business survey’s pricing intentions index being in the notable exception). Similarly, surveys of inflation expectations are now back at levels consistent with the RBNZ’s inflation target or at least at around the levels normally seen when inflation is running close to the target midpoint.

- Activity: The 0.2% fall in June quarter GDP was not as weak as we or the RBNZ expected. More recently, business activity indicators have improved but remain subdued and so suggest another modest decline in GDP in Q3. However, we are seeing signs that the downturn in domestic activity is flattening off. For instance, retail spending has started to push higher since August and residential consent numbers appear to have found a base following sharp declines over the past couple of years. Forward sentiment indicators in the QSBO and ANZ business survey have continued to improve in recent months as respondents have factored more neutral policy settings into their forecasts.

- Labour market: The labour market is tracking no weaker than expected. The unemployment rate didn’t rise as much as the RBNZ feared (4.8% vs 5%) but employment growth and labour costs were a touch weaker than expected – the latter consistent with the slowdown in inflation seen in private sector services prices. Recent trends in filled jobs appear consistent with the RBNZ’s August forecast that employment will fall only modestly further in the current quarter. Any RBNZ concerns of a larger shakeout in the labour market have probably been assuaged by recent data (including more positive hiring intentions surveys, albeit advertised job vacancies are yet to improve).

- Housing market/population growth: House sales are yet to show much improvement from subdued levels, while house prices have continued to track sideways at best with prospective buyers able to select from a significant level of inventory. However, mortgage applications have picked up and both anecdotal evidence and housing surveys point to a prospective increase in activity over coming months. So, on balance we would not expect much change in the RBNZ’s forecasts for the housing market. That said, it is possible that the RBNZ might slightly lower its forecasts for net migrant inflows.

- Commodity prices/exchange rate: Overall, commodity prices are on the rise. That includes dairy prices, which have been bid up at the recent global dairy trade auctions (as reflected in Fonterra’s decision this week to raise its forecast milk payout for the current season). Prices for meat, New Zealand’s other major export category, have also lifted off the back of increasingly favourable demand and supply fundamentals. As noted below, there are some downside risks to the NZ dollar, although at present the trade-weighted exchange rate index (TWI) is trading slightly firmer than the 69.5 assumption made in the August MPS.

- Geopolitical developments: War in the Middle East has intensified but to date oil prices haven’t been impacted and risk sentiment remains strong. The key development is Trump’s resounding win in the US presidential election and Republican control of the Senate and (likely) the House. Global markets have moved to price in the expected impact of Trump’s relatively unimpeded policy program. The implications are higher US growth, inflation, interest rates and the US dollar, although the exact magnitude is uncertain. For New Zealand, developments on the global stage signal potentially significant risks to export incomes over the medium-term. We may see short-term downside risks to energy and import prices should Russian oil be better able to reach global markets through eased sanctions after a brokered ceasefire in Ukraine, and if Chinese manufactured goods need to find an alternate destination due to US tariffs. However, short-term inflation benefits could be at least partially offset by a weaker NZD. On balance these developments confer more risk to the outlook which could make the RBNZ more cautious on the medium-term inflation outlook.

Bitcoin extends powerful rally amid “Trump Pump” optimism, ready for 100k milestone

Bitcoin's robust rally continues at the start of this week, buoyed by the so-called "Trump Pump" effect. Cryptocurrency investors are optimistic about US President-elect Donald Trump's promises to create a more supportive and friendly regulatory environment for crypto businesses.

The crypto market has long struggled with a lack of regulatory clarity, and these anticipated policy changes are fueling strong positive sentiment. Expectation of a more defined regulatory framework is encouraging both institutional and retail investors to increase their exposure to Bitcoin, driving further price appreciation.

Such optimism is expected to persist through the rest of 2024, with Bitcoin setting its sights on the significant 100k mark.

Technically, Bitcoin is in clear upside acceleration as seen in D MACD. The immediate focus is on 161.8% projection of 58846 to 73608 from 66763 at 90647. Break could push Bitcoin a bit further higher to 200% projection at 96287.

The real test lies in medium term level at 100% projection of 24898 to 73812 from 52703 at 101617, which is slightly above 100k psychological level. Strong resistance could be seen there to bring consolidations on first attempt.

Australian NAB business confidence surges to 5, easing cost pressures but persistent retail inflation

Australia's NABs Business Confidence Index jumped from -2 to 5, marking a notable improvement after a prolonged period of below-average sentiment. Business conditions remained stable at 7, while trading conditions saw a slight increase from 12 to 13. Profitability held steady at 5, and employment conditions edged lower from 5 to 3.

Gareth Spence, NAB’s Head of Australian Economics, highlighted the jump in confidence as an encouraging development, noting that it is “just one month” but shows "tentative improvement" in forward orders, suggesting possible momentum.

Input cost pressures continued to ease, with labor cost growth decelerating from 1.9% to 1.4% on a quarterly basis from 1.9%, and purchase cost growth slowing from 1.3% to 0.9%. Retail price growth, however, saw a rebound, rising from 0.6% to 1.1%.

Spence noted, "The survey, like other price indicators, continues to suggest an ongoing gradual easing in inflation pressure, but also that there is still some way to go in in the inflation moderation when we look at the consumer facing components”.

Australian Westpac consumer sentiment jumps 5.3%, but US election casts shadow on outlook

Australian consumer sentiment saw a solid rebound in November, with Westpac Consumer Sentiment Index climbing by 5.3% mom to reach 94.6. This marks a 14.4% rise from its mid-year low, leaving it just 5.4 points shy of the neutral 100 mark.

The improvement was led by increased optimism about the short-term economic outlook. The "economic outlook, next 12 months" sub-index jumped 8.7% to 100.9, the first optimistic reading (above 100) since post-COVID recovery. Confidence around personal finances also strengthened, with the "family finances, next 12 months" sub-index up 4.4% to 104.1. Meanwhile, Unemployment Expectations Index dropped by -7.2% to 120.5, indicating the highest level of labor market confidence since April 2023.

Westpac noted three important observations in November's sentiment trends. First, confidence reached 99.7 in the early survey period, prior to RBA’s rate decision, reflecting marked optimism. Secondly, consumer sentiment remained unaffected by RBA's decision to hold rates steady. Lastly, sentiment dropped sharply after US election result, averaging 91.1 in the survey’s latter half. This indicates an unusually wide range of ±5% for November's final read, suggesting a degree of uncertainty not typically seen.

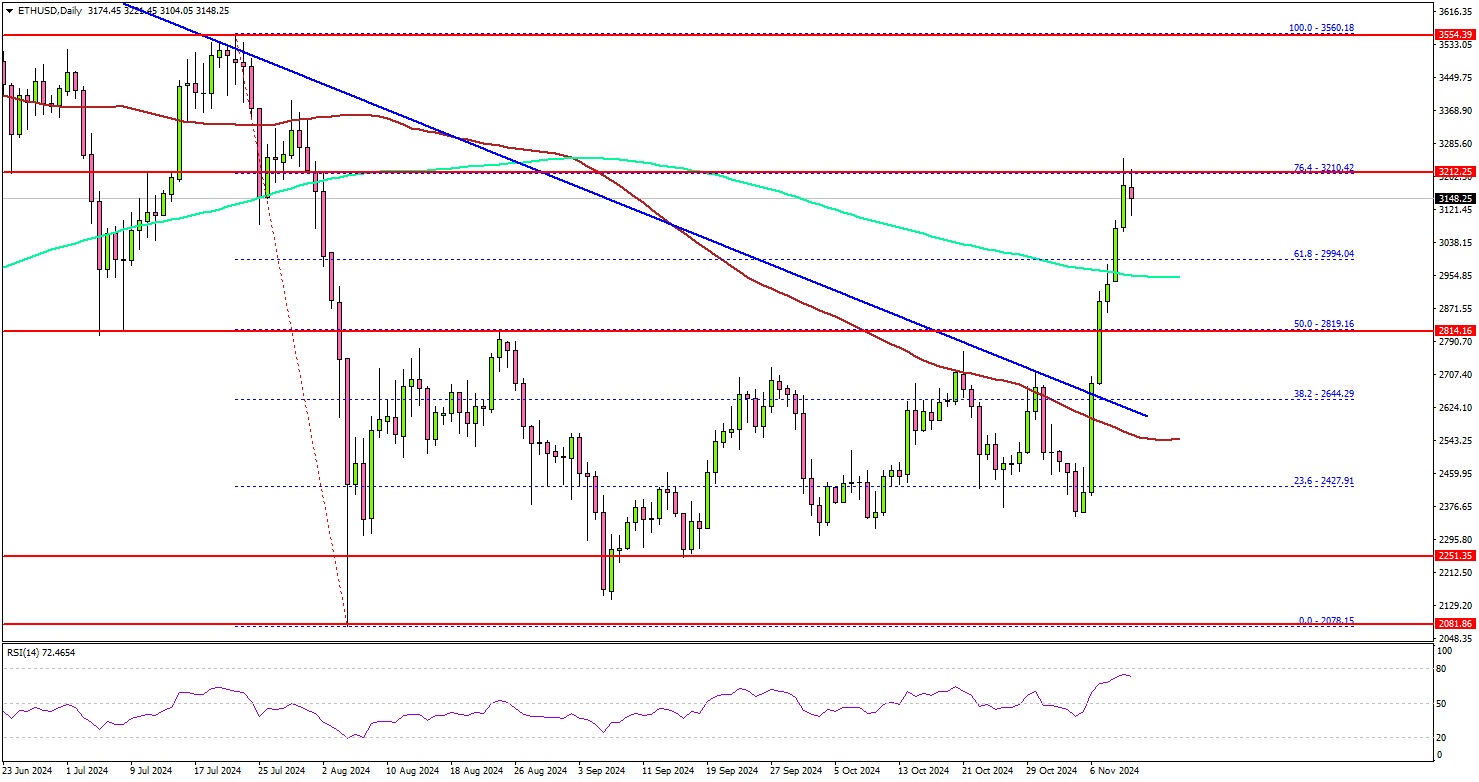

Ethereum Hints at Breakout: Can ETH Match Bitcoin’s Surge?

Key Highlights

- Ethereum started a fresh surge above the $2,500 resistance zone.

- ETH price cleared a major bearish trend line with resistance near $2,680 on the daily chart.

- Bitcoin price extended gains and traded to a new record high above $88,000.

- Gold prices extended losses and traded below the $2,665 support.

Ethereum Technical Analysis

Ethereum started a fresh increase above $2,500 alongside Bitcoin. The bulls were able to pump ETH above the $2,550 and $2,650 resistance levels.

Looking at the daily chart, the price cleared a major bearish trend line with resistance near $2,680. It settled above the $2,800 level, the 100-day simple moving average (red), and the 200-day simple moving average (green).

It even surpassed the 50% Fib retracement level of the downward move from the $3,560 swing high to the $2,078 low. The bears are now protecting the $3,220 resistance.

The 76.4% Fib retracement level of the downward move from the $3,560 swing high to the $2,078 low is acting as a resistance. The next major resistance is near the $3,350 level. A daily close above the $3,350 resistance zone could start another steady increase.

In the stated case, the price may perhaps rise toward the $3,500 level. The next stop for the bulls may perhaps be near the $3,650 level.

On the downside, Ethereum might find support near the $3,000 level. The next major support is $2,950 and the 200-day simple moving average (green), below which the price could slide toward $2,800. Any more losses might call for a move toward the $2,650 level.

Looking at Bitcoin, there was a steady increase above the $80,000 level, and the price traded to a new all-time high above $88,000.

Economic Releases

- Fed's Waller speech.

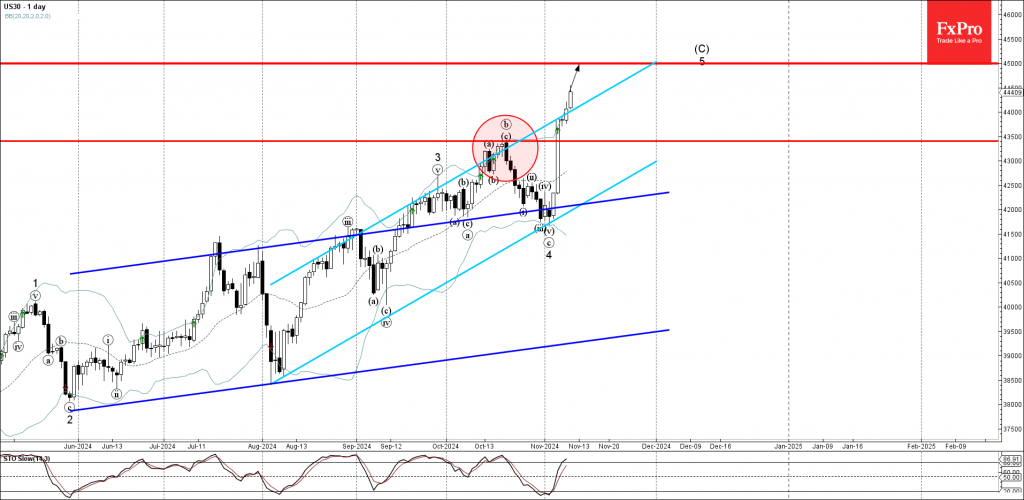

Dow Jones Wave Analysis

- Dow Jones rising inside impulse wave 5

- Likely to reach resistance level 45000.00

Dow Jones index continues to rise inside the minor impulse wave 5, which previously broke the key resistance level 43500.00 and the resistance trendline of the daily up channel from August.

The active impulse wave 5 belongs to the weekly upward impulse sequence (C) from April of this year.

Given the clear weekly uptrend, Dow Jones index can be expected to rise to the next resistance level 45000.00 (target price for the completion of the active impulse wave 5).

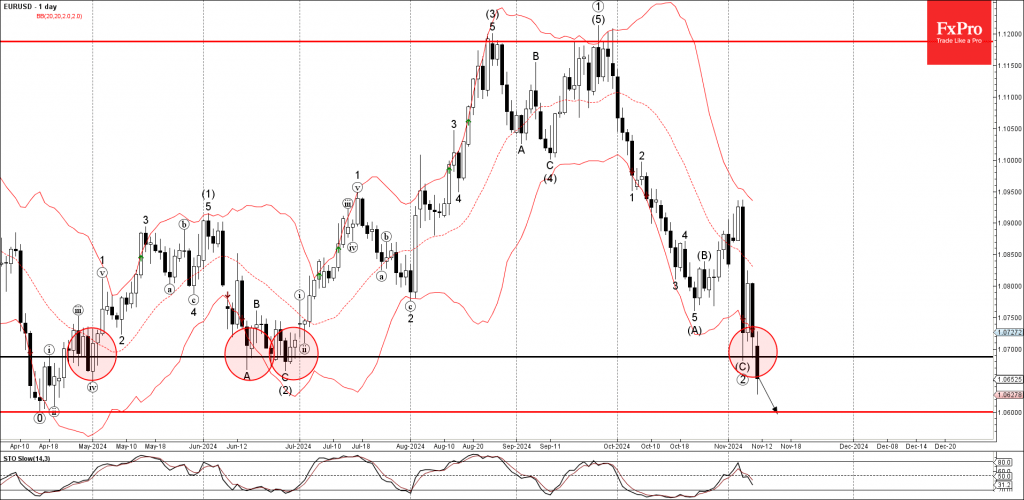

EURUSD Wave Analysis

- EURUSD under bearish pressure

- Likely to fall to support level 1.0600

EURUSD currency pair is under bearish pressure after the earlier breakout of the key support level 1.0685, which has been reversing the price from the middle of June.

The breakout of the support level 1.0685 should strengthen the bearish pressure on this currency pair.

Given the simultaneously bullish USD sentiment and the bearish Euro sentiment seen across the FX markets today, EURUSD currency pair can be expected to fall to the next support level 1.0600 (former strong support from April).

AUD/USD Stabilises as Traders Await Economic Signals

The AUD/USD pair is navigating the week starting with a steady tone, trading around 0.6590. After a significant drop last Friday, triggered by disappointment over China's economic stimulus measures, the pair finds a momentary respite as it consolidates recent movements.

China's announcement of a significant debt reduction and support for local governments and economic growth fell short of full transparency, leaving investors wanting more details. Given China's crucial role as Australia's top trading partner, any economic shifts there have a pronounced impact on the AUD's performance.

The ongoing uncertainties surrounding the implications of Donald Trump's U.S. presidential win also continue to influence market sentiment, particularly regarding U.S.-China relations.

This week is pivotal for Australian data with the release of Q3 payroll statistics and overall employment data, which are essential for assessing the Reserve Bank of Australia's (RBA) future monetary policy decisions. Additionally, RBA Governor Michele Bullock's participation in a regulatory panel might offer fresh insights into the central bank's views on inflation and economic demand.

AUD/USD Technical Analysis

Currently, AUD/USD is hovering around 0.6589 within a tight consolidation range. Anticipations lean towards a downward breakout towards 0.6544, potentially extending to 0.6494 before reversing. Upon reaching these levels, a reversal towards 0.6715 may be considered, with an interim target at 0.6600. The MACD indicator supports a bearish outlook in the short term, as it points downwards from above the zero line.

On the hourly chart, after completing a decline to 0.6557 and a subsequent correction to 0.6600, expectations are for a further dip to 0.6544. Success in reaching this level may prompt a rebound to 0.6600, testing from below before possibly resuming the downward trend towards 0.6494. The stochastic oscillator, currently below the 50 mark, underscores the potential for further declines.