Sample Category Title

Dollar Unstoppable for Now

The dollar continues to rise on speculation of policy changes following the US election. The Dollar Index rose above 105.5 on Monday – its highest level since early July – before easing slightly in trading.

The main contributors to the index’s strength are weakness in the single currency and the Japanese yen. In both cases, there is a cocktail of political uncertainty and fears that Trump’s protectionist policies will hurt EU and Japanese exporters.

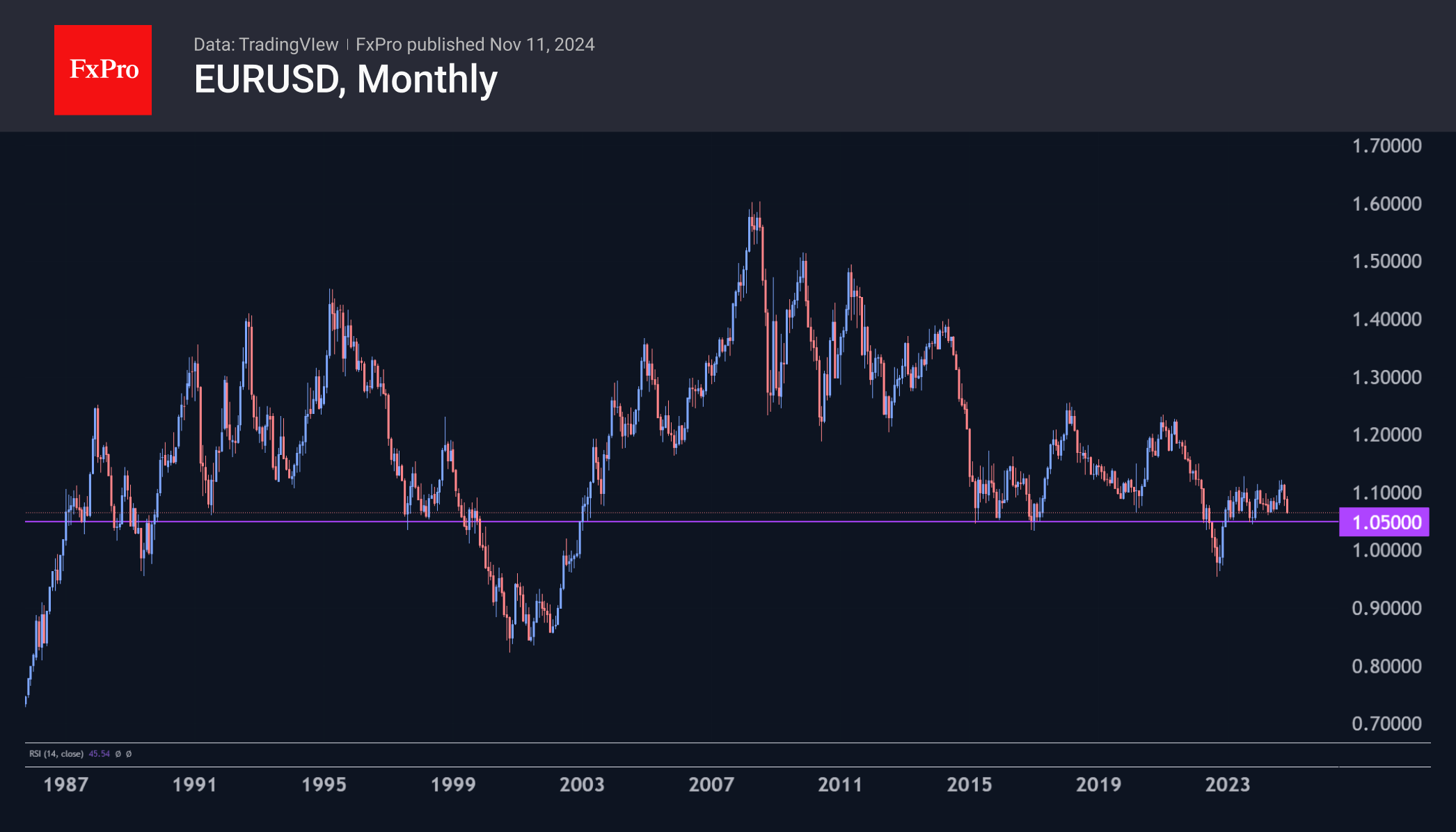

The EURUSD has pulled back to the 1.0650 area. Over the past 12 months, it has only traded below this level for a few days in April. The pair reversed sharply from the 1.20 area after the so-called Trump trade began in early October.

Now that the Republicans have indeed come to power, we should expect further declines in the pair. The next important milestone on the way down is the 1.05 area, where we should expect a global shakeout, as this is historically the most important pivot area for the EURUSD. In 2022 and 2000, a break below 1.05 opened the door to a move well below parity. Conversely, if the EURUSD bulls can defend this level, the rally could be long and high.

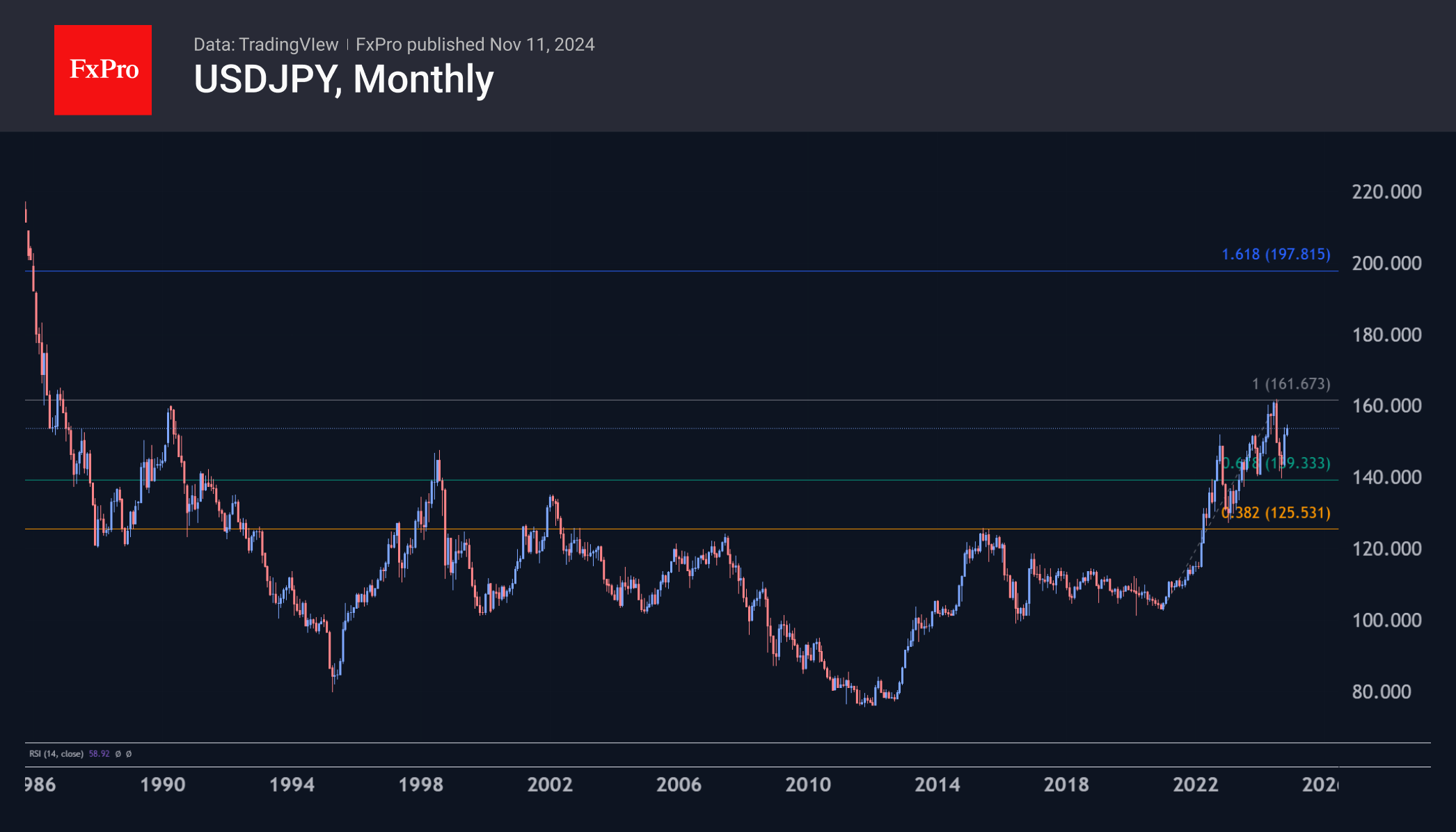

USDJPY jumped 0.8% on Monday, back to last week’s local highs at 154. The pair has risen more than 10% from the mid-September lows and has made intra-week highs for ten consecutive weeks. The drivers were first disappointed with the pace of monetary tightening, then the Trump trade. Political reshuffles following the surprise defeat of the ruling party and uncertainty about further rate hikes have also played a role.

If we consider the 14% drop in USDJPY from 162 to 139 as a correction of the rise since the beginning of 2020, the new upside momentum promises to end closer to 200. However, only the passivity of the Treasury and the BoJ in breaching the 162 level will confirm the end of this monumental scenario.

EURUSD – Steep Downtrend Extends to New Multi-Month Low

EURUSD started the week negatively (down 0.7% until early US trading on Monday, in extension of Friday’s 0.8% drop, with total loss of 2.7% since announcement of Trump’s victory on Wednesday.

The single currency has also registered a weekly loss of 1.8% vs dollar, with near term action weighed by large weekly bearish candlestick and formation of bearish engulfing pattern on weekly chart.

Fresh strength of the US dollar pushed the euro to the lowest in over 6 months on Monday, with steep downtrend (bear-leg from 1.0936, Nov 5 lower top) eyeing key med-term support at 1.0601 (2024 low posted on Apr 16).

Firmly bearish daily technical studies add to euro-negative fundamentals (euphoria over expectations of Trump’s measures to strongly boost economic growth / fears of tariffs on imports from the EU), with partial profit-taking to spark limited correction.

Broken Fibo 76.4% (1.0745) to ideally cap, with extended upticks to stall under broken psychological 1.08 supported, now acting as solid resistance, to keep larger bears in play and provide better selling opportunities.

Res: 1.0682; 1.0745;1.0761; 1.0800

Sup: 1.0601; 1.0516; 1.0495; 1.0448

Gold (XAU/USD) Prices Slide as US Dollar (DXY) Rally Continues

- Gold prices retreat as US Dollar strengthens as hopes of aggressive rate cuts fade.

- China’s economic slowdown concerns and potential sanctions impact iron ore and gold prices.

- Technical analysis indicates gold’s vulnerability to further downside, with key levels identified.

Gold prices have started the week on the back foot as the US Dollar continues to advance. Growing hopes of a ceasefire under a Trump Presidency have also diminished the safe haven’s appeal coupled with expectations of fewer rate cuts in 2025.

The biggest loser from the US election last week appears to be commodity markets which are feeling the strain of a rampant US Dollar. Gold prices retreated last week followed by Silver, Platinum with iron ore facing fresh challenges from concern around China growth as well.

China, who had been a major buyer of Gold this year, has remained on the sidelines for the past few months as Gold prices continued to soar to fresh highs. Concerns around the growth picture in China have also impacted Iron Ore prices as markets anticipate a slowdown in the Chinese economy which could dent demand for raw materials. The threat of sanctions has seen UBS downgrade China growth for 2025 to 4% while warning that 2026 could prove even more challenging. Will we see more downgrades in the coming weeks?

US Dollar Strength Expected to Continue

The problem for Gold prices moving forward is that President Trump will only take office in January. This means that any of the optimism around a Middle East peace deal and the potential for higher rates may not change until then. This could leave Gold in a spot of bother with the recent selloff likely to continue.

There are a few things that could reignite the bullish rally in the precious metal with one of them being a retaliatory attack on Israel by Iran. This could put hopes of a Middle East ceasefire in jeopardy and thus lead to an increase in demand for safe havens once more.

Many had touted a Trump victory as a positive for the Gold rally, however given that markets have some experience from Trump’s first term it appears they are a lot calmer this time around.

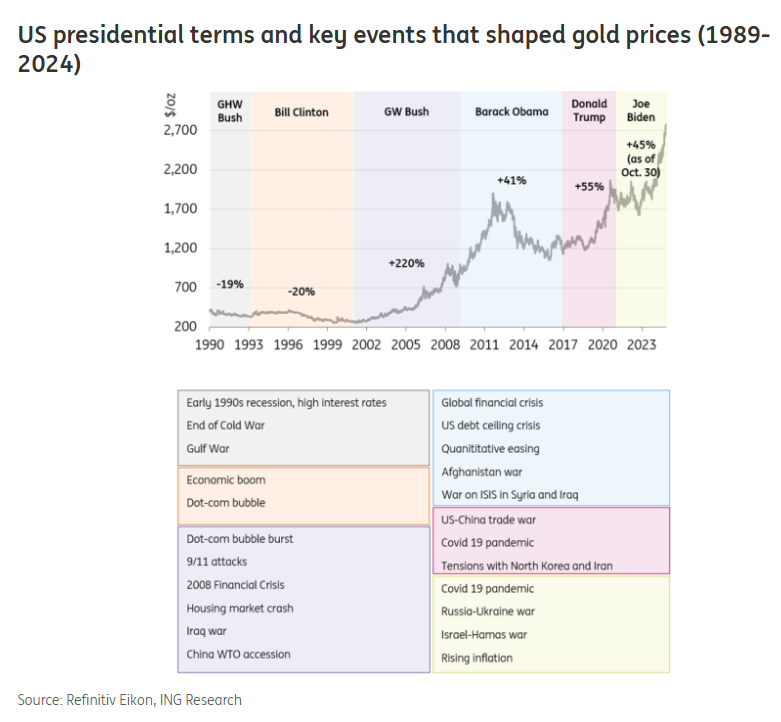

Looking back at the performance of Gold under various Presidents, during Trump’s first term in office the precious metal rose 55%. The picture however may be distorted by the fact that the last year of the Trump Presidency occurred during the pandemic as Gold demand was ramped up due to the uncertainty.

Source: Refinitiv, ING Think (click to enlarge)

Even then given the recent rally in Gold and the expectation that Trump policies could lead to higher inflation and a stronger USD, another 55% gain seems unlikely.

A look ahead to the rest of the day, Veterans day holiday in the US should see a low liquidity US session which could lead to a lot of choppy price action as the European session comes to a close.

Technical Analysis Gold (XAU/USD)

From a technical analysis standpoint, Gold on a daily timeframe is looking ominous and vulnerable toward further downside.

A break of the long term ascending trendline last week was followed by a brief foray higher before a rejection and selloff which has brought Gold to within touching distance of last week’s low. At the moment though, price appears to be caught between support at 2650 and resistance 2700.

Immediate support rests at 2650 before 2639 and 2624 comes into focus.

Now a recovery from her will need acceptance above the 2700 handle if we are to see a further push to the upside. At this stage the 2800 handle appears far away but could still come into play moving forward.

Gold (XAU/USD) Daily Chart, November 11, 2024

Source: TradingView (click to enlarge)

Support

- 2650

- 2639

- 2624

Resistance

- 2675

- 2700

- 2711

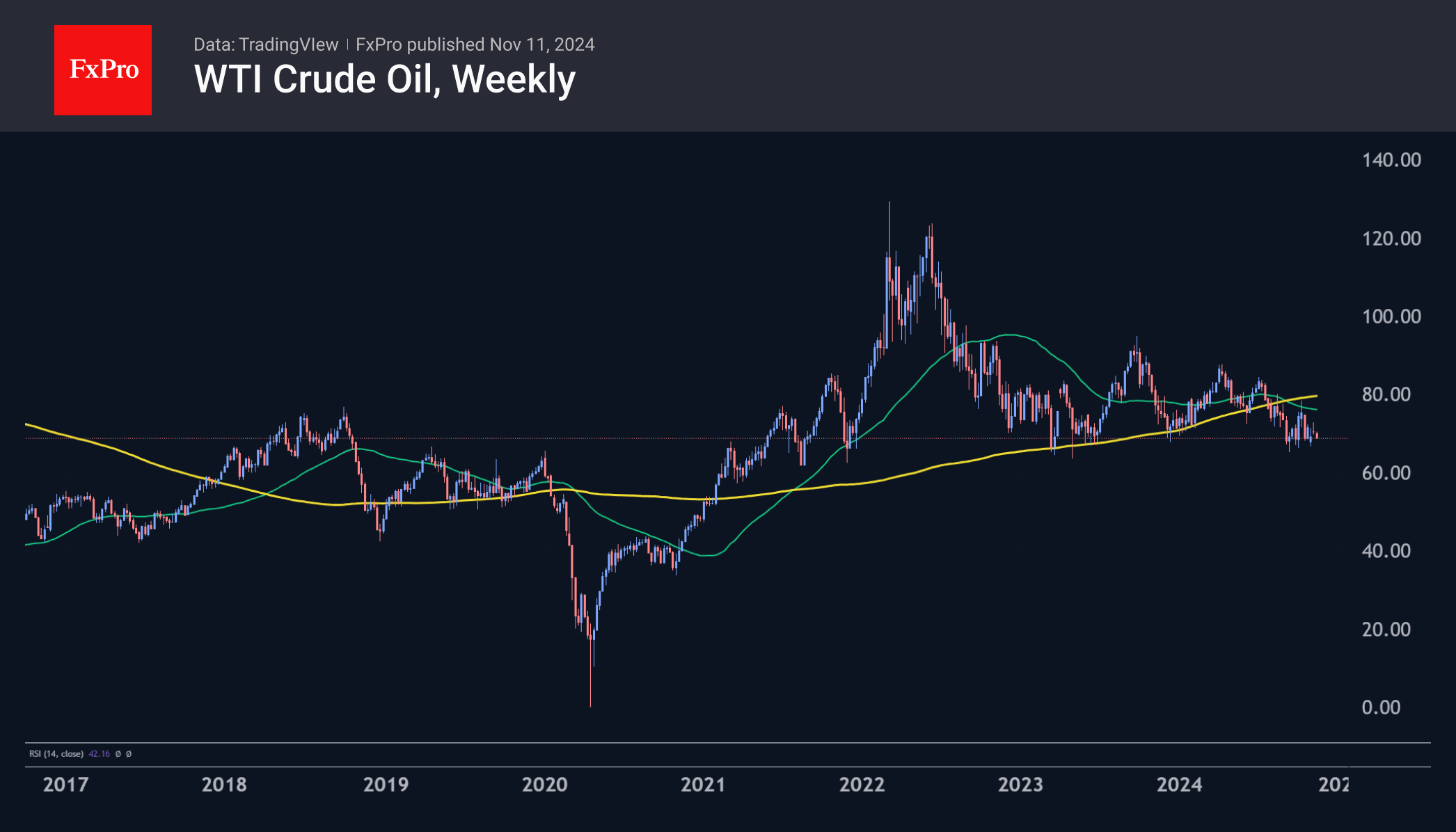

Oil & Gas: Still Mostly Bearish Prospects

Crude Oil

The price of a barrel of crude oil has fallen 1.6% since the start of Monday, bringing the decline over the last two trading sessions to 4%. Pressures on the oil price include signals from the ceasefire talks between Israel and Lebanon (reducing supply risks) and disappointment over the size of China’s stimulus package (revising expected demand).

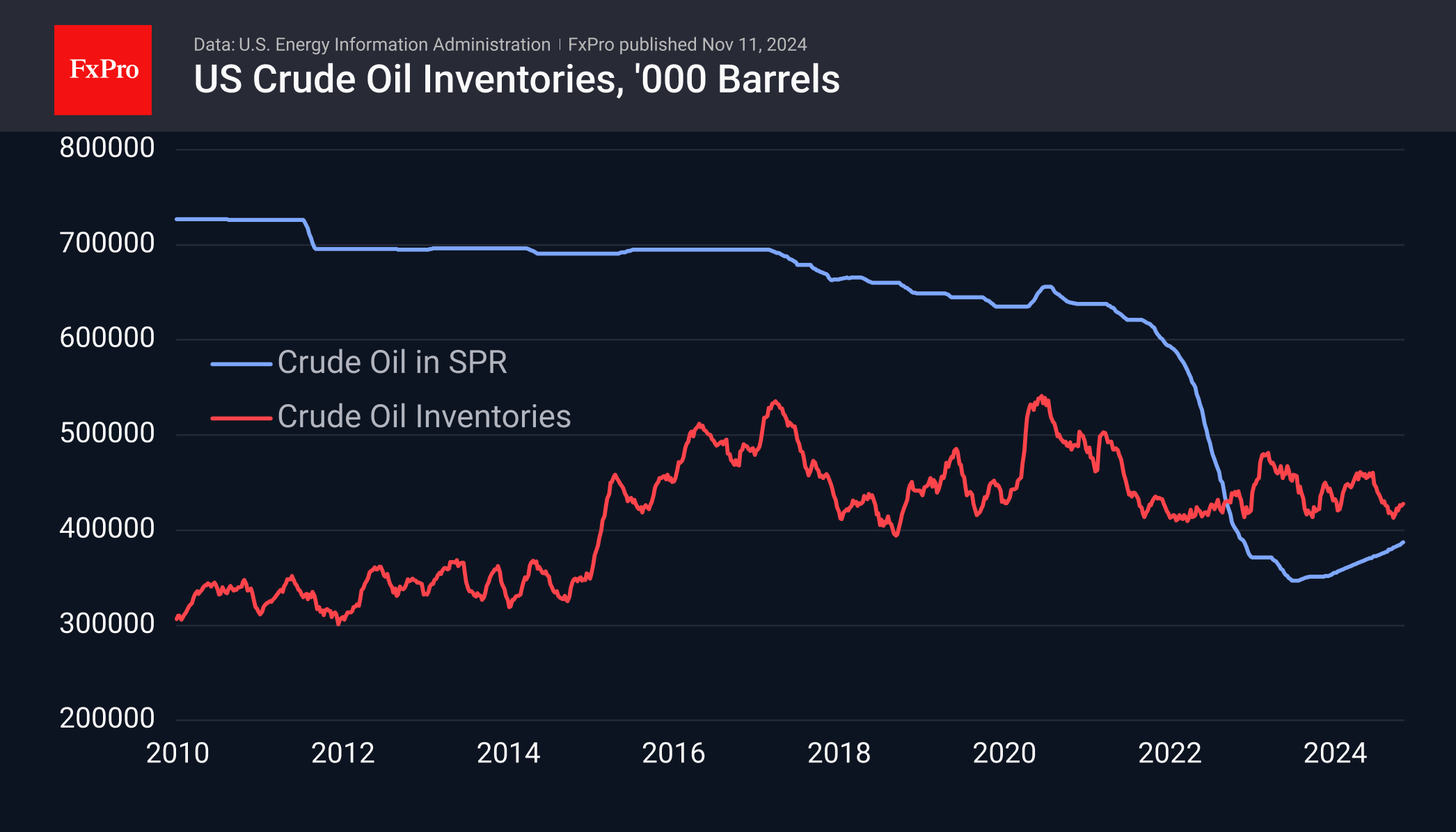

Among the longer-term factors, the upward trend in US oil inventories has continued. The strategic reserve has increased by 1.4 million barrels, maintaining the pace in recent weeks and accelerating from the average rate of 750k barrels per week since the beginning of the year. The acceleration appears to be driven by lower prices, which also help to provide soft support.

Commercial inventories have been on an upward trend since the end of September, with oil producers adding at a record pace of 13.5 mb/d over the past four weeks. However, the current level of commercial inventories (427.7 mb/d) is at the lower end of the range of the past 5 years, and this factor is unlikely to seriously worry the markets as long as inventories remain below 500 mb/d.

The markets expect the Republican party’s political dominance to favour oil producers. However, we doubt this will lead to an increase in production. Instead, the focus will be on optimising profits (with equal emphasis on price and volume) and reducing subsidies for alternative energy sources.

A Republican administration may step up purchases of oil reserves after January, but that’s still more than two months away.

Technically, oil continues to be dominated by the bears, with a sharp reversal below the 50-week moving average in early October and trading near the lower end of its range over the past three years. The price also closed below its 50-day moving average last week and is now actively declining after falling below $69/bbl WTI. We will be watching the price dynamics and OPEC+ comments with interest in the event of a pullback to $65-66, as this would take Brent back to $70-71, which looks like an informal floor for the major cartel members.

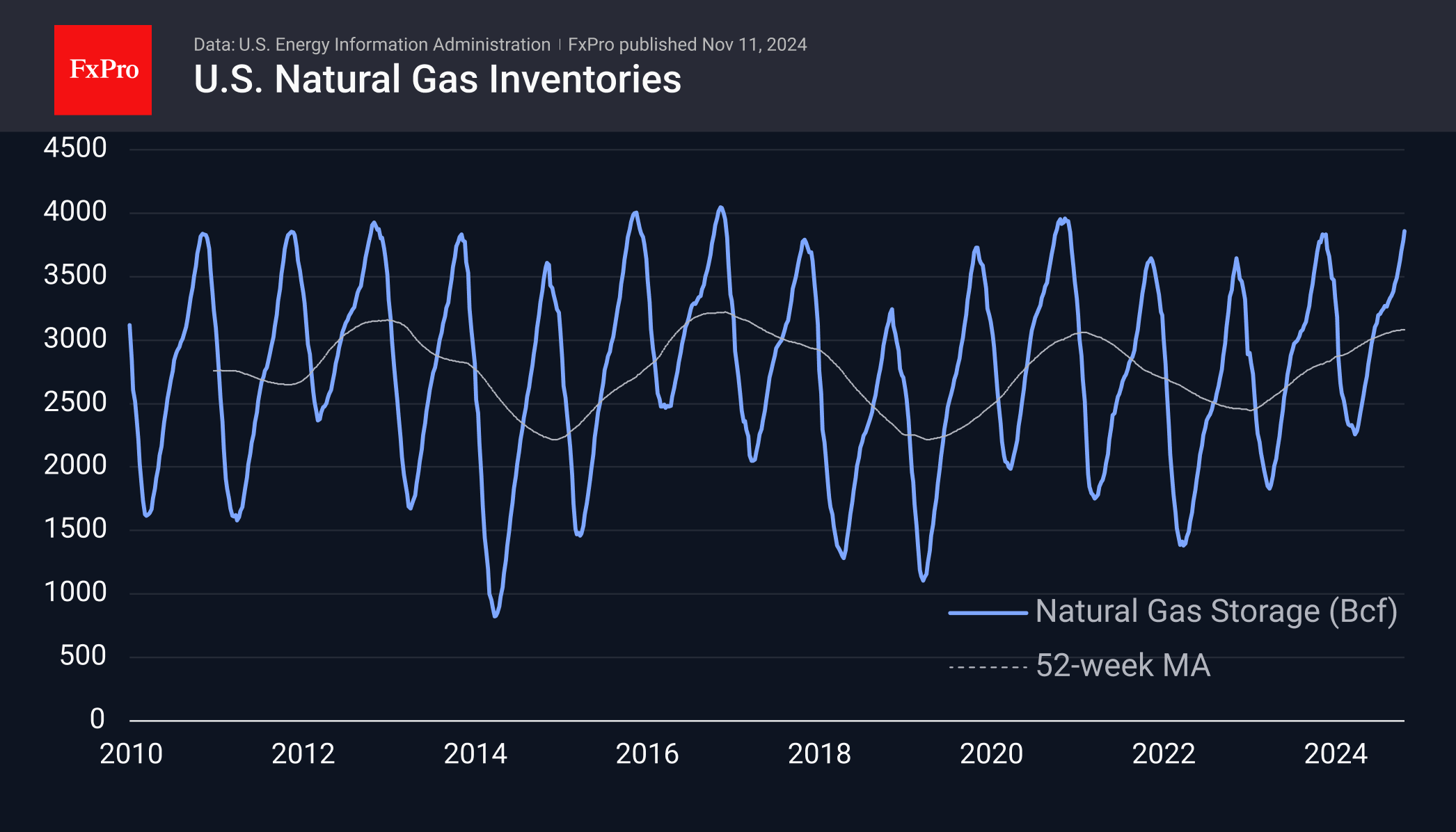

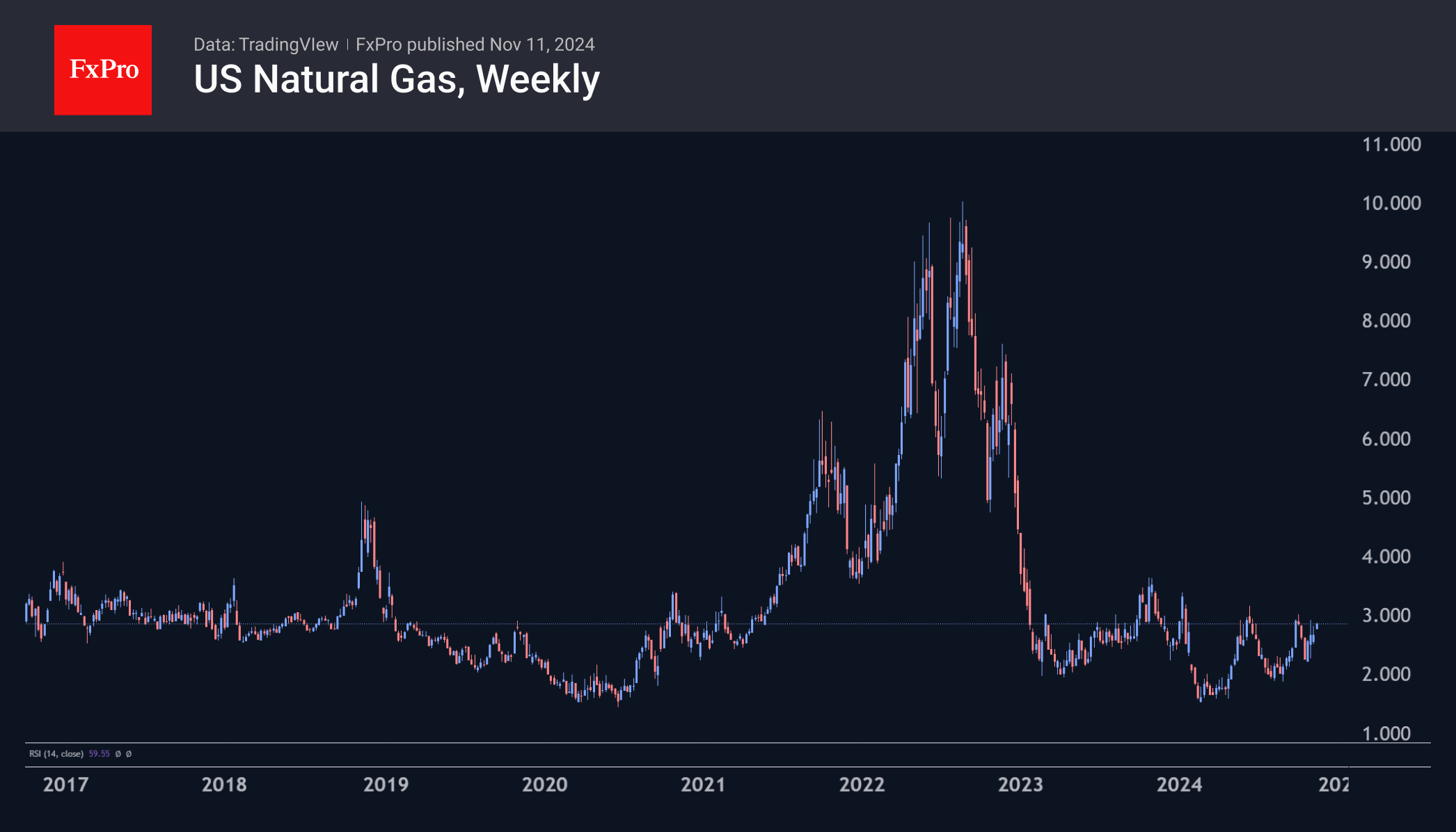

Natural Gas

On Monday, the US Natural Gas price rose more than 5% since the start of the day due to the temporary shutdown of 16% of gas production capacity in the Gulf of Mexico.

This doesn’t seem to be a problem for the US now, with the latest data showing the highest gas inventories in 4 years and close to historical highs for the index.

The price has returned to the $3.0 area – highs in just under two weeks. The $3.0-$3.20 area has acted as pivot resistance more than once this year, and it will be interesting to see if this pattern continues. Given the inventory levels and dynamics of oil, a new downtrend is more likely for now. In the case of gas, however, a break of resistance could trigger a dramatic rise.

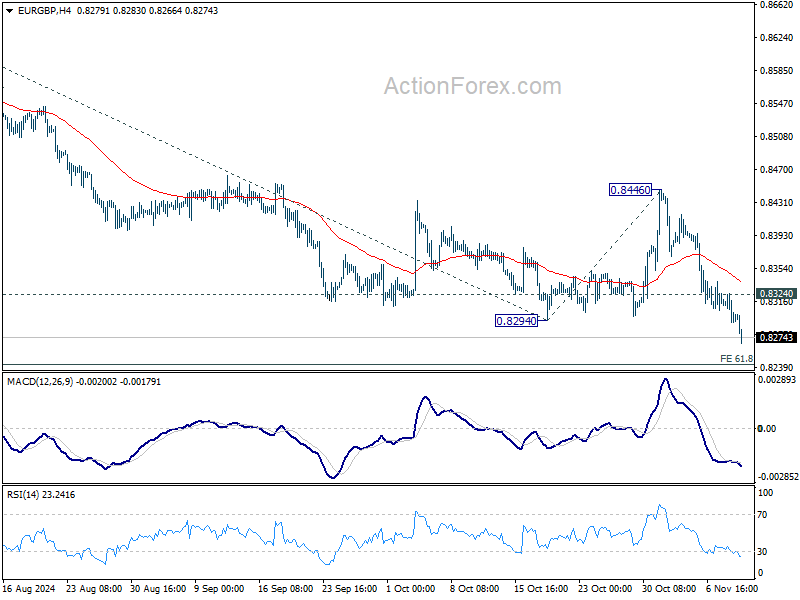

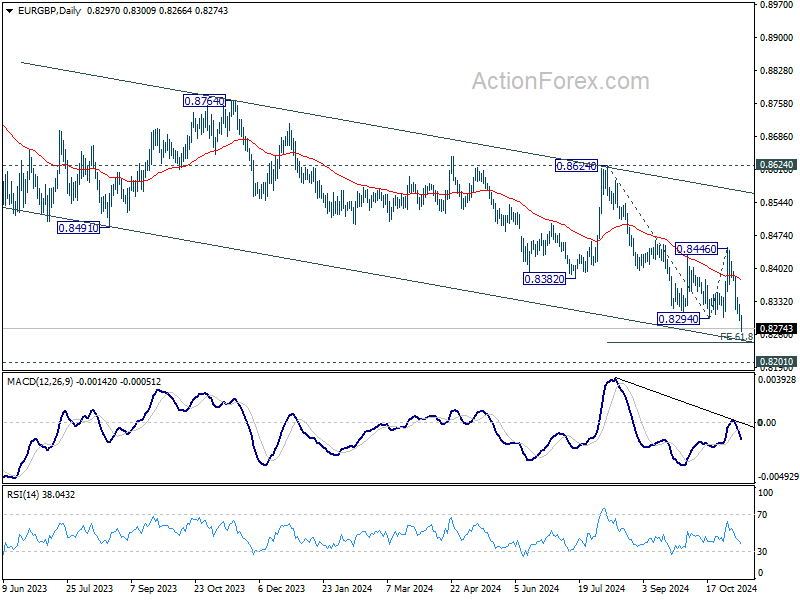

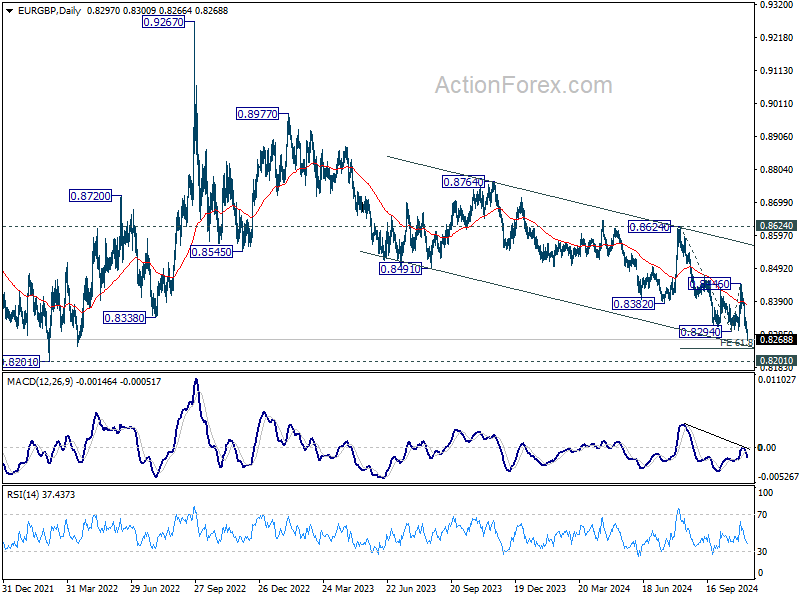

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8283; (P) 0.8305; (R1) 0.8317; More...

EUR/GBP's decline accelerates lower today and intraday bias stays on the downside for 61.8% projection of 0.8624 to 0.8294 from 0.8446 at 0.8242. Break there will target 0.8201 key support. On the upside, above 0.8324 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 0.8446 resistance holds, in case of rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

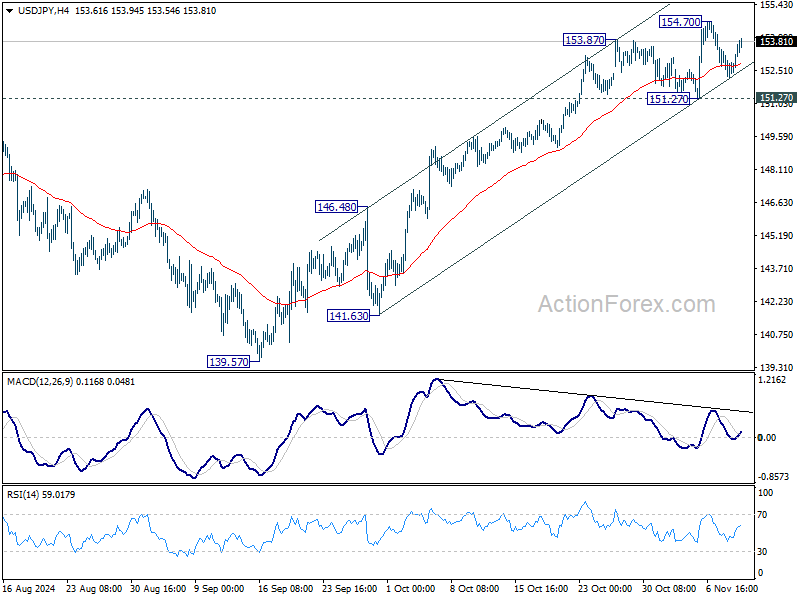

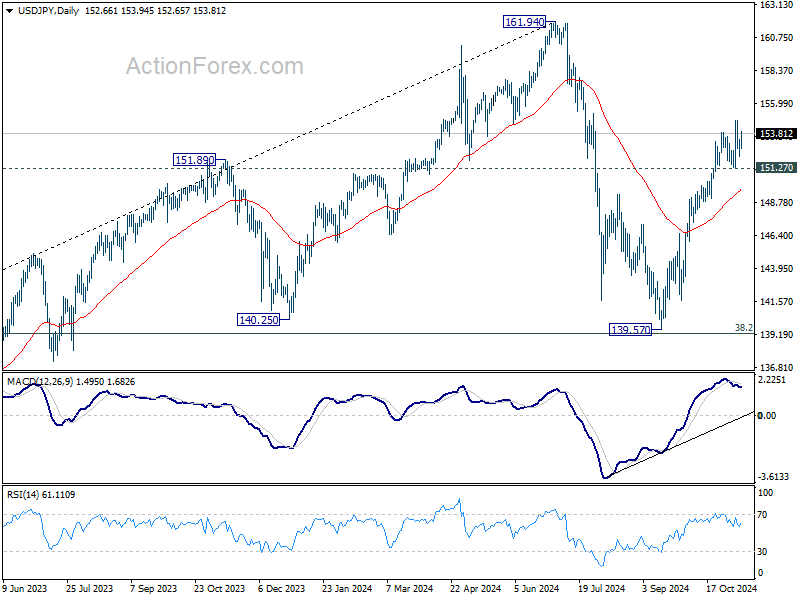

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.07; (P) 152.72; (R1) 153.30; More...

Range trading continues in USD/JPY and intraday bias stays neutral for the moment. Further rise is expected as long as 151.27 support holds. Above 154.70 will resume the rally from 139.57 towards 161.94 high. However, considering bearish divergence condition in 4H MACD, break of 151.27 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 149.74).

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

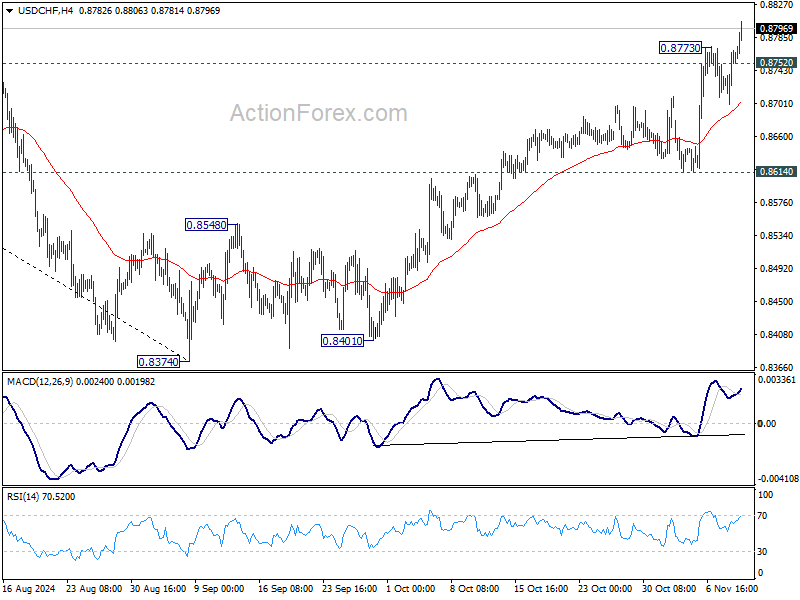

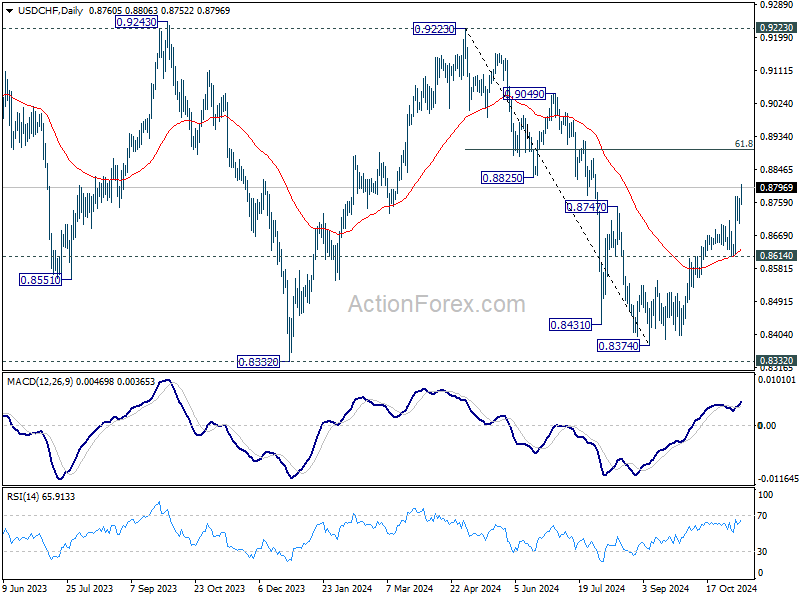

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8716; (P) 0.8742; (R1) 0.8784; More…

USD/CHF's rally resumed by breaking through 0.8733 temporary top and intraday bias is back on the upside. Current rise from 0.8374 should target 61.8% retracement of 0.9223 to 0.8374 at 0.8899 next. On the upside, below 0.8752 minor support will turn intraday bias neutral again. But outlook will stay bullish as long as 0.8614 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

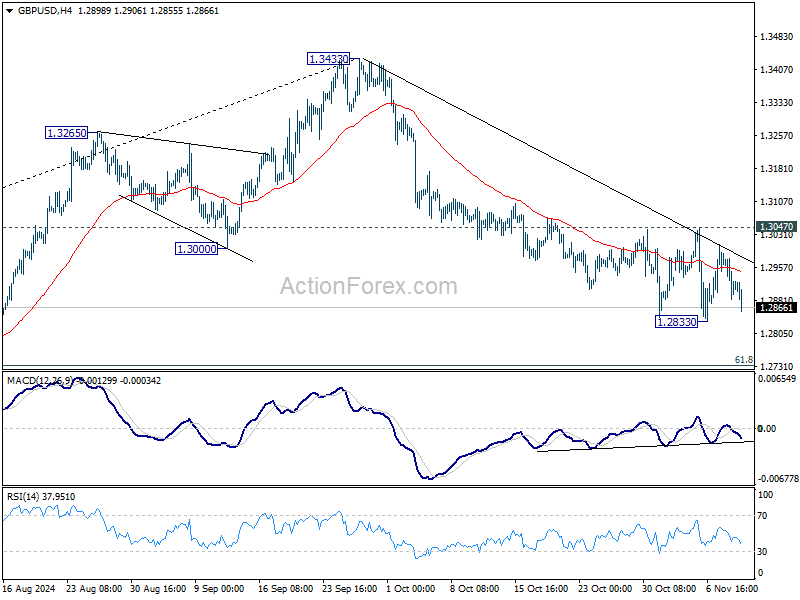

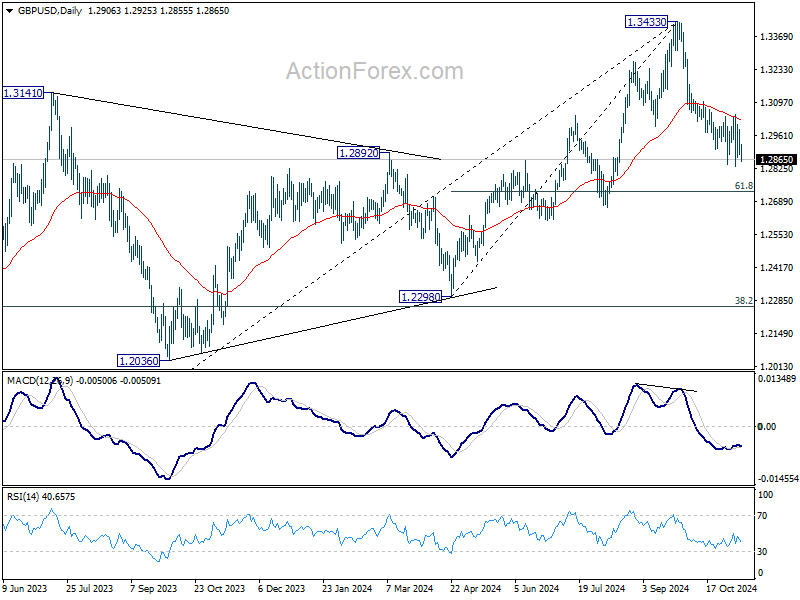

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2870; (P) 1.2933; (R1) 1.2981; More...

GBP/USD is still bounded in range above 1.2833 temporary low and intraday bias stays neutral for the moment. Further decline is expected 1.3047 resistance holds. Break of 1.382 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bullish convergence condition in 4H MACD, firm break of 1.3047 will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

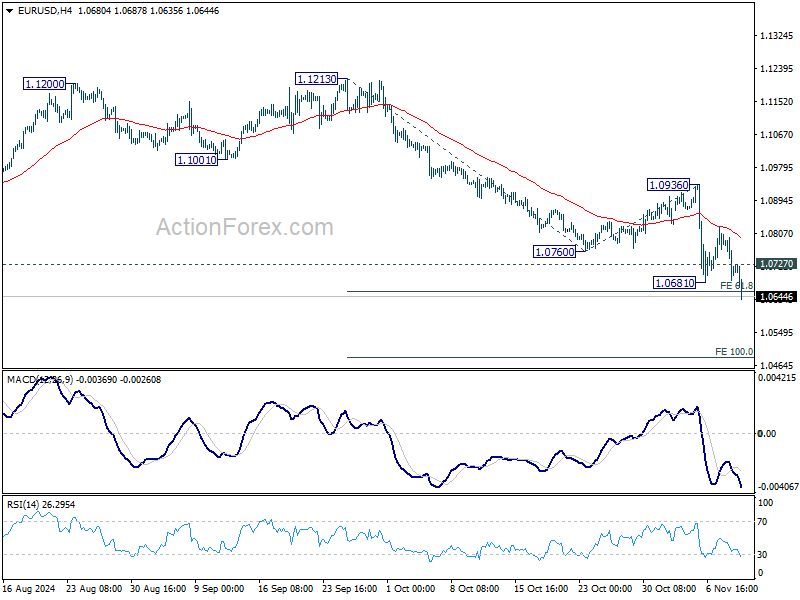

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0667; (P) 1.0738; (R1) 1.0788; More...

EUR/USD's decline resumed by breaking through 1.0681 temporary low and intraday bias is back on the downside. Sustained trading below 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656 will extend the fall from 1.1213 to 100% projection at 1.0483. On the upside, above 1.0727 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0936 resistance holds.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

Renewed US Tariff Concerns and German Instability Hammer Euro

Euro is facing immense selling pressure today as US session commences, driven by both external trade concerns and internal political challenges in Germany. The market is wary of escalation in trade tensions with the US following Donald Trump’s election victory, with reports suggesting that Robert Lighthizer—a trade hawk known for his aggressive stance—could make a return as the US Trade Representative. Such a move signals a push for increased tariffs, raising fears of a "second round" of the trade war, which could place substantial pressure on Europe’s already sluggish economy.

Compounding these external risks, Germany is facing its own internal political crisis. Chancellor Olaf Scholz has indicated willingness to move up national elections after the collapse of his ruling coalition last week. This came following his dismissal of former Finance Minister Christian Lindner, triggering turmoil within the government. The prospect of a snap election adds a layer of uncertainty for Euro, as markets turn anxious about Germany’s future fiscal direction, given its role as the economic engine of the Eurozone.

Despite the Euro's struggles, Yen remains the weakest currency today. Prime Minister Shigeru Ishiba managed to retain his position in a parliamentary vote but received only 221 votes, well below the required majority in the 465-seat legislature. Ishiba’s position is now precarious, heading a minority government that faces escalating trade threats from the US, along with heightened geopolitical challenges involving China and North Korea. This political instability could hinder BoJ’s ability to execute its planned policy tightening as the central bank deals with heightened uncertainty both at home and abroad.

Meanwhile, Dollar is so far the day’s strongest performer, though it remains below last week's peak against all major currencies except the Euro and Swiss Franc, indicating restrained momentum. Australian and New Zealand Dollars follow the greenback as next strongest. British Pound and Canadian Dollar sit in the middle of the pack.

Technically, EUR/GBP's down trend also picks up momentum today. Further fall should be seen to 61.8% projection of 0.8624 to 0.8294 from 0.8446 at 0.8242 and possibly below. The question remains on whether 0.8201 key support (2023 low) is strong enough to contain downside.

In Europe, at the time of writing, FTSE is up 0.68%. DAX Is up 1.45%. CAC is up 1.31%. UK 10-year yield is up 0.033 at 4.478. Germany 10-year yield is down -0.007 at 2.364. Earlier in Asia, Nikkei rose 0.08%. Hong Kong HSI fell -1.45%. China Shanghai SSE rose 0.51%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield fell -0.0045 to 1.001.

SNB's Martin: Swiss Franc appreciation expected due to inflation differentials

SNB Vice President Antoine Martin conveyed a cautious stance on future monetary policy in an interview with Le Temps.

While SNB indicated at its September meeting the readiness to cut interest rates further, Martin stressed that "it's not useful for central banks to lock themselves into forward-looking communications."

He highlighted that "between now and the next decision, there may be changes in conditions that render current communications invalid," This approach means SNB has made "absolutely no commitment" to a specific policy path.

Addressing the performance of Swiss Franc, Martin noted that its development this year has been "neither particularly surprising nor exceptionally problematic."

He explained that due to the inflation differential between Switzerland and other countries, SNB expects Swiss Franc to "appreciate structurally over time in nominal terms."

However, he pointed out that "in real terms, excluding the inflation effect, the appreciation has been limited."

BoJ affirms core stance: Rate hikes to proceed gradually if economic outlook holds

BoJ's Summary of Opinions from its October 30-31 reiterated its "basic thinking" that it will adjust the degree of monetary accommodation if the outlook for economic activity and prices unfolds as expected. Emphasizing the importance of "communicating effectively" this core message, BoJ aims to manage market expectations carefully.

One member indicated that if economic conditions progress as anticipated, BoJ could "raise the policy interest rate gradually," reaching 1.0% in the second half of fiscal 2025 at the earliest.

Conversely, another member expressed caution, noting the difficulty in confidently conveying a medium-term policy rate path due to "high uncertainties" surrounding the neutral interest rate and the transmission mechanism of monetary policy.

RBNZ 1-yr inflation expectation down, 2-yr's up

RBNZ's latest Survey reveals that expectations for one-year-ahead annual inflation dropped significantly by -35 basis points from 2.40% to 2.05%, extending a steady downward trend in inflation expectations since Q2 2023. On the other hand, two-year inflation expectations inched up to from 2.03% 2.12% .

For wage inflation, one-year-ahead expectations decreased modestly by -7 basis points to 2.81%, while two-year projections rose from 2.86% to 3.16%.

Growth expectations improved. The mean one-year-ahead GDP growth expectation jumped by 61 basis points to 1.60%, with a smaller increase of 7 basis points for two-year growth expectations to 2.17%.

On the interest rate front, the survey points to further monetary easing ahead. OCR is expected to be 4.20% by the end of Q4 2024, with a sharper decline to 3.33% anticipated by Q3 2025. OCR is currently at 4.75% following a recent 50bps cut in October.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0667; (P) 1.0738; (R1) 1.0788; More...

EUR/USD's decline resumed by breaking through 1.0681 temporary low and intraday bias is back on the downside. Sustained trading below 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656 will extend the fall from 1.1213 to 100% projection at 1.0483. On the upside, above 1.0727 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0936 resistance holds.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.