Sample Category Title

EUR/JPY Weekly Outlook

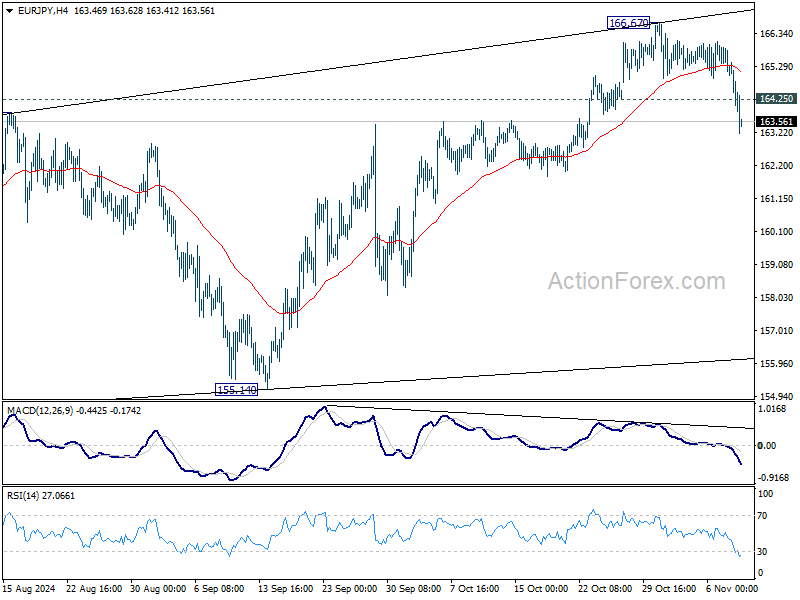

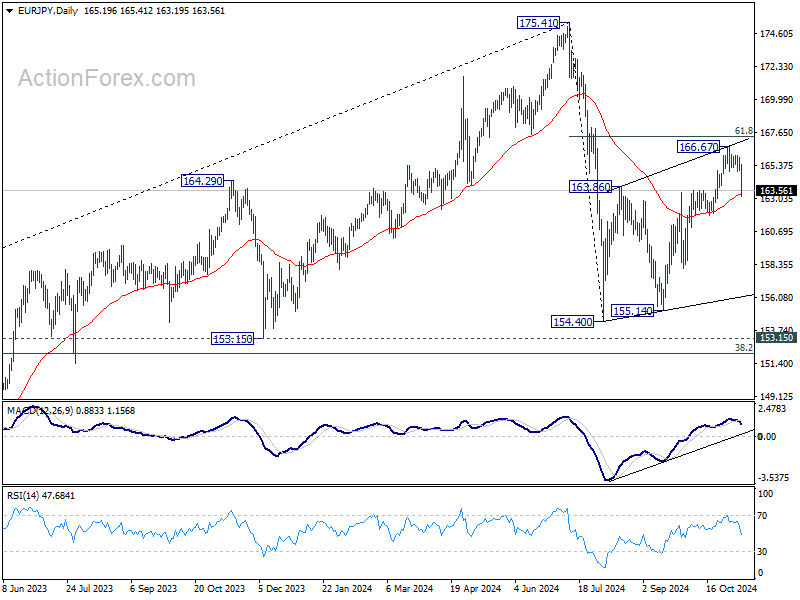

EUR/JPY's fall from 166.67 extended last week and the late selloff suggested that a short term top was already formed. Initial bias is back on the downside this week. Sustained trading below 55 D EMA (now at 163.31) will argue that whole corrective rise from 154.40 has completed with three waves up to 166.67. Deeper decline should then be seen back to 154.40/155.14 support zone. On the upside, break of 166.67 will target 61.8% retracement of 175.41 to 154.40 at 167.38 instead.

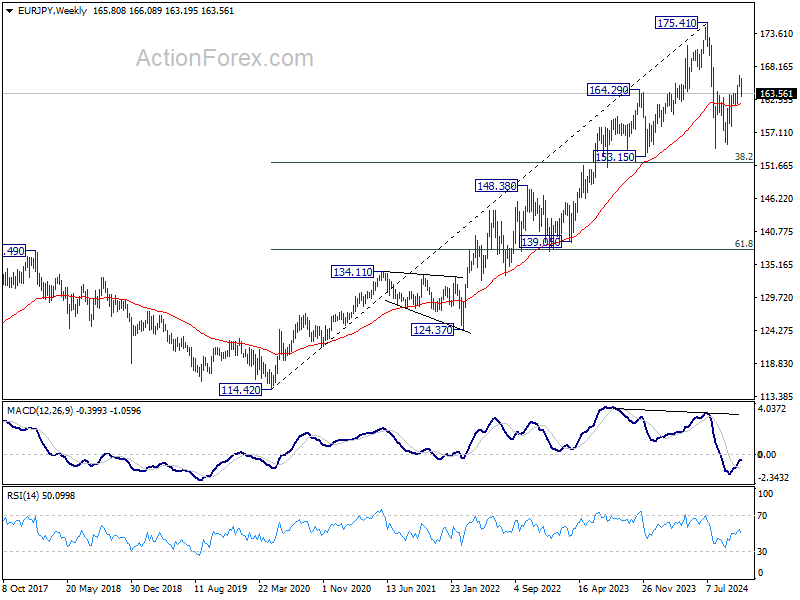

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

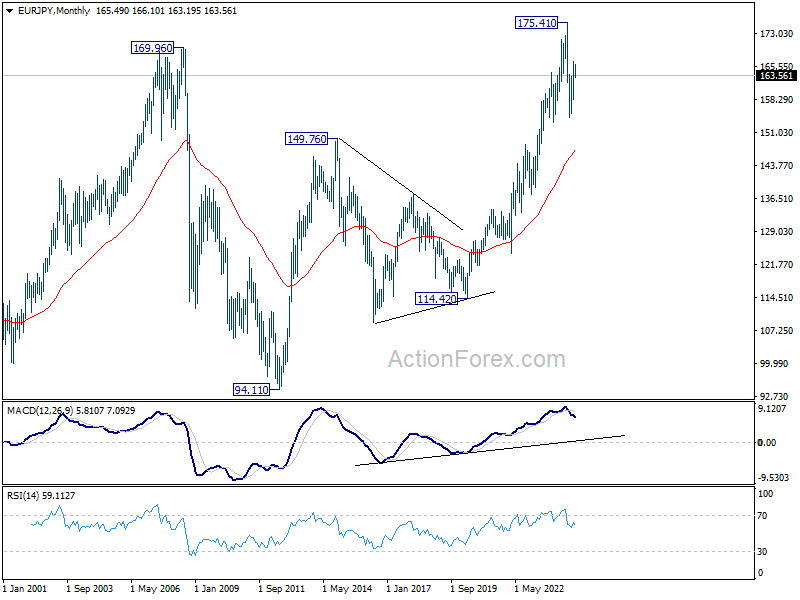

In the long term picture, considering bearish divergence condition in W MACD, 175.41 is at least a medium term top. It's still early to conclude that up trend from 94.11 (2012 low) has completed. But a medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 147.33).

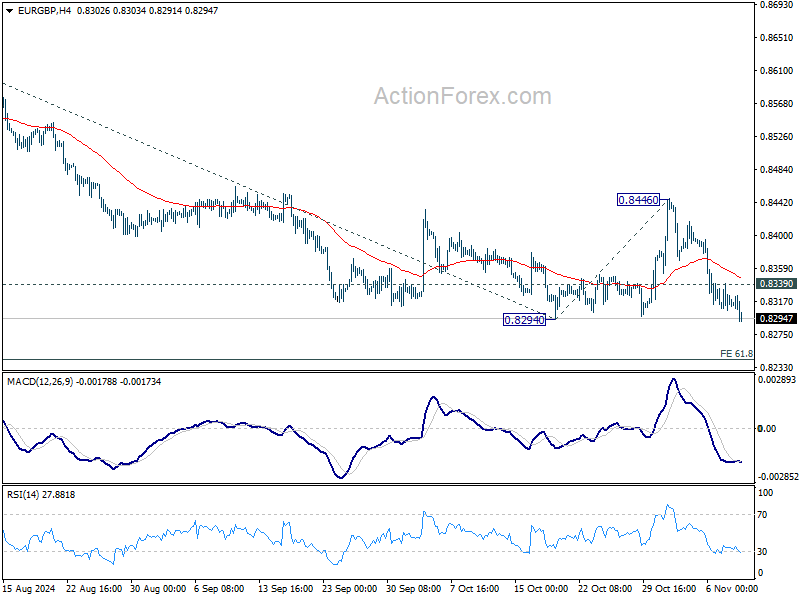

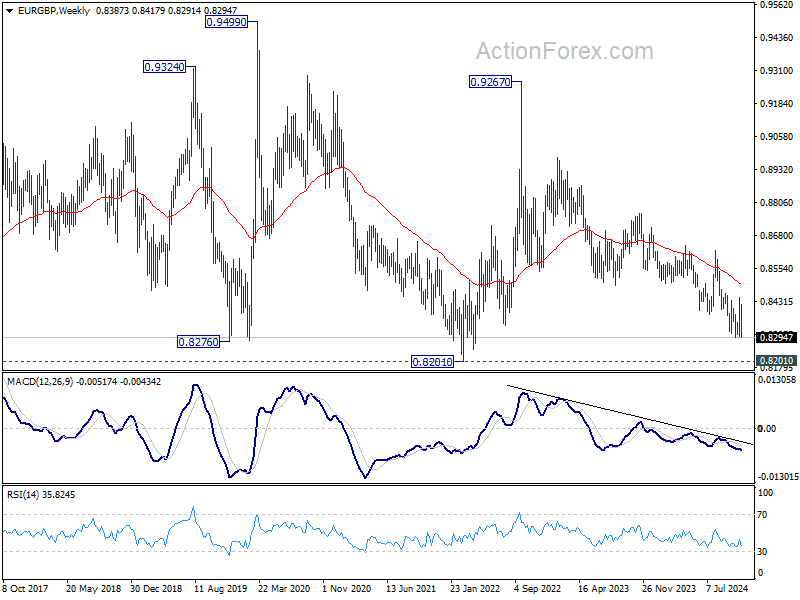

EUR/GBP Weekly Outlook

EUR/GBP's late breach of 0.8294 suggests that larger down trend is resuming. Initial bias stays on the downside this week for 61.8% projection of 0.8624 to 0.8294 from 0.8446 at 0.8242. Break there will target 0.8201 key support. On the upside, above 0.8339 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 0.8446 resistance holds, in case of rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

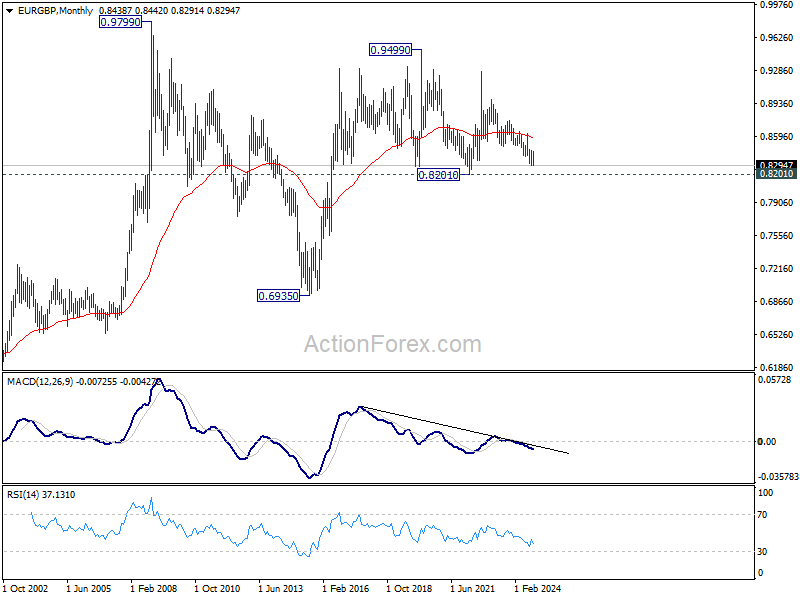

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

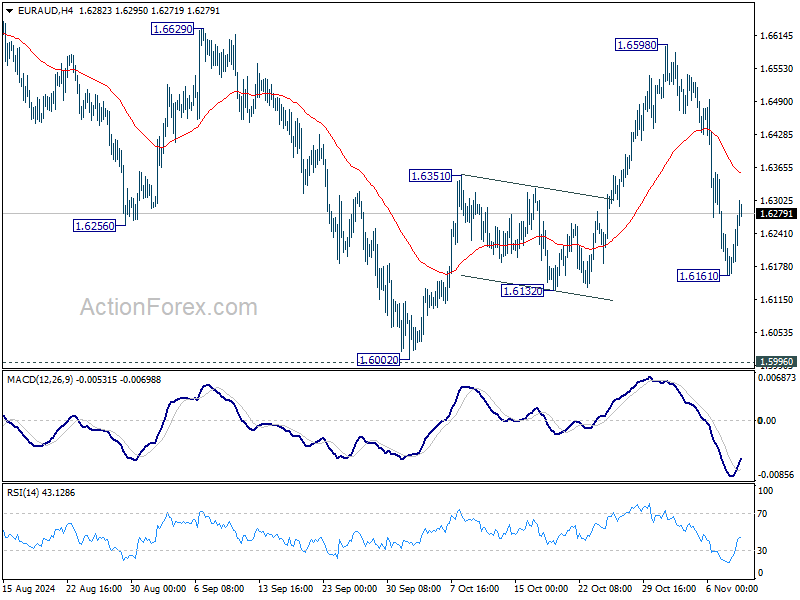

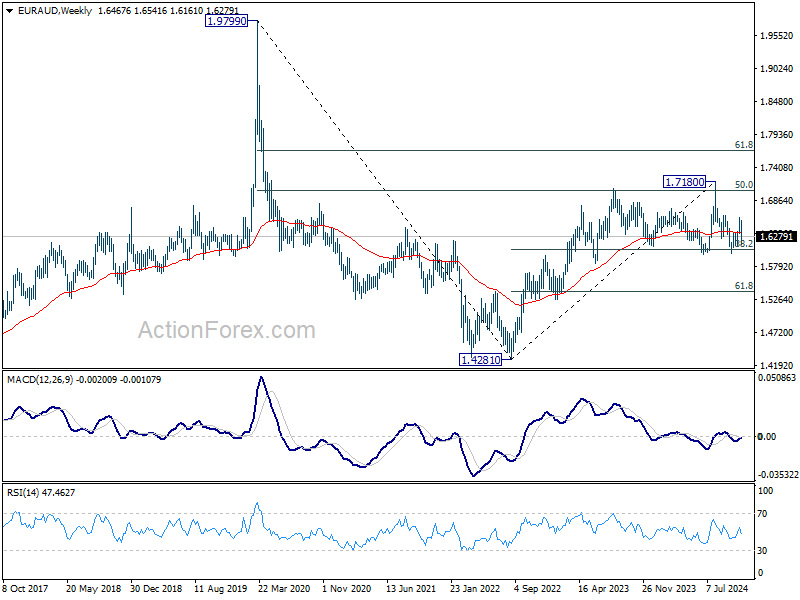

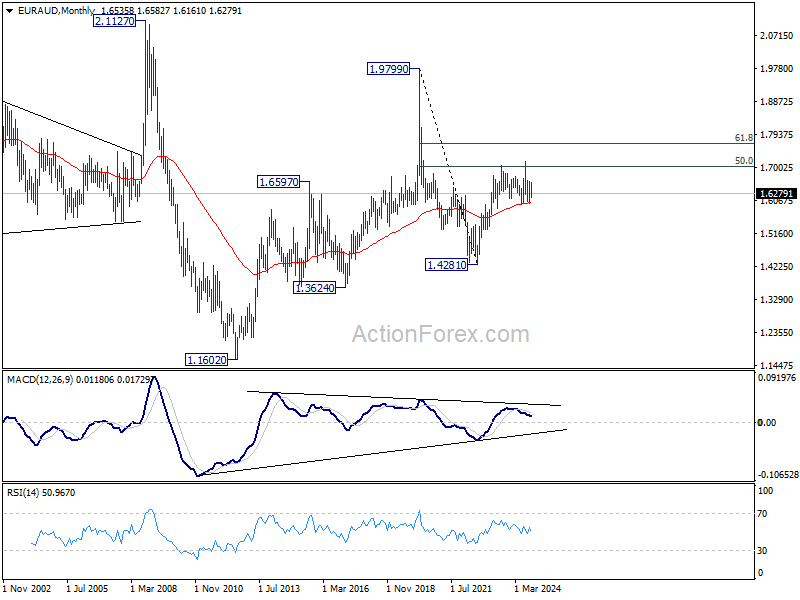

EUR/AUD Weekly Outlook

EUR/AUD's steep decline last week suggests that rebound from 1.6002 has completed with three waves up to 1.6598. But as a temporary low was then formed at 1.6161, initial bias is neutral this week first. On the downside, below 1.6161 will target a test on 1.5996/6002 key support zone. For now, risk will stay mildly on the downside as long as 1.6598 holds, in case of stronger rebound.

In the bigger picture, as long as 1.5996 cluster support , up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6031) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

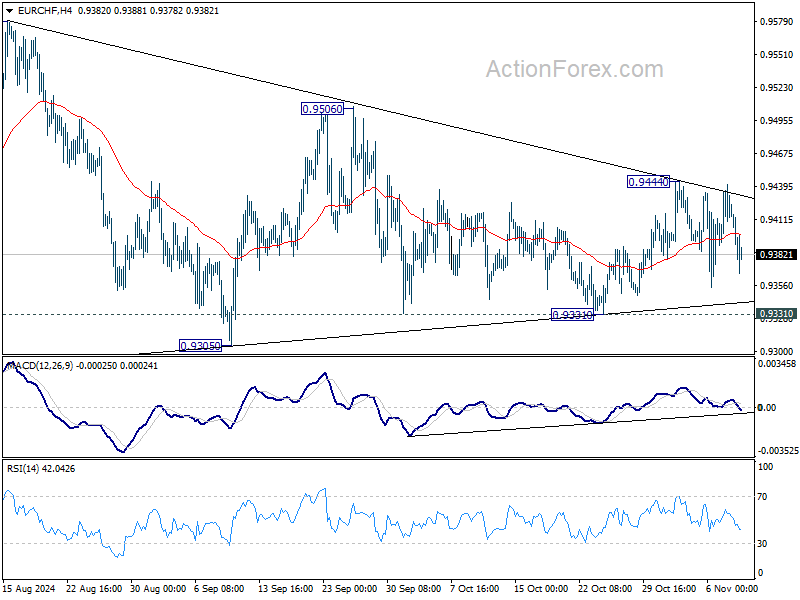

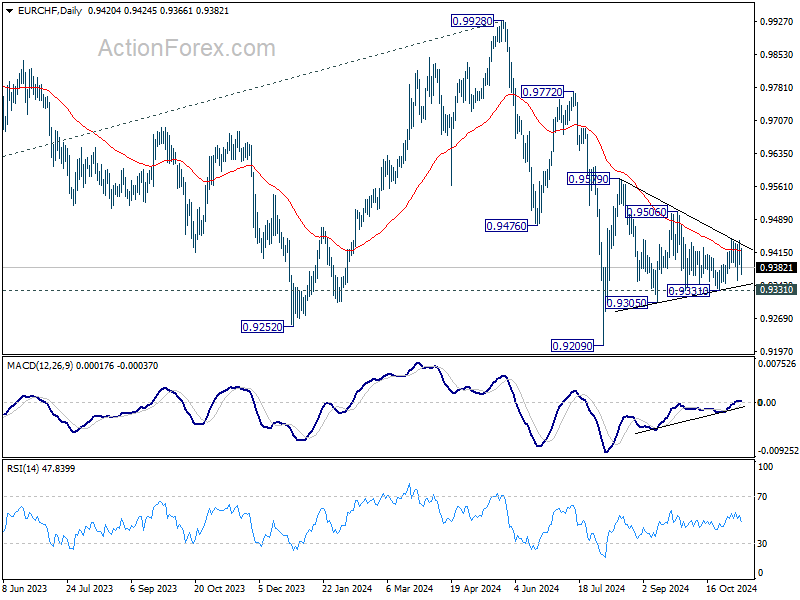

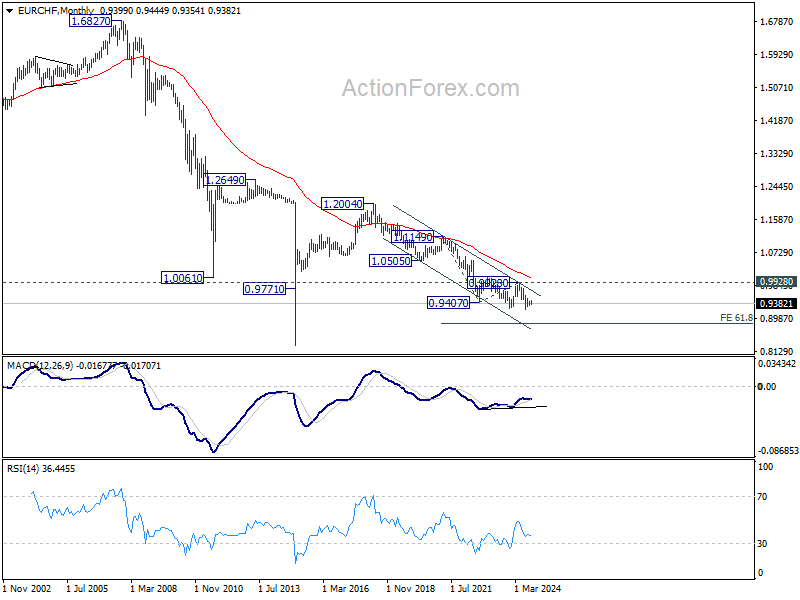

EUR/CHF Weekly Outlook

EUR/CHF continued to stay in converging triangle last week and outlook is unchanged. Initial bias stays neutral this week first. On the downside, break of 0.9331 will target 0.9305 support first. Firm break there will bring retest of 0.9209 low. On the upside, break of 0.9444 will bring stronger rally to 0.9506 resistance next.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9419) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

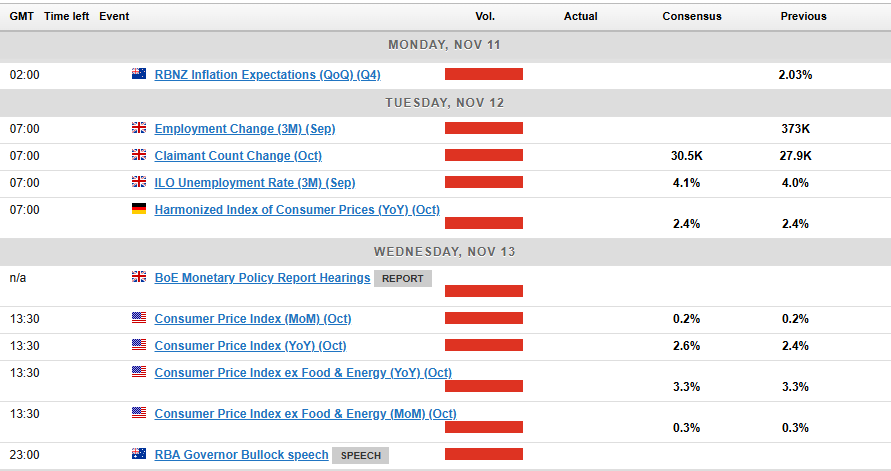

Summary 11/11 – 11/15

Monday, Nov 11, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Oct | 2.70% | 2.70% |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Current Account (JPY) Sep | 2.99T | 3.02T |

| 02:00 | NZD | RBNZ Inflation Expectations Q4 | 2.03% | |

| 05:00 | JPY | Eco Watchers Survey: Current Oct | 47.2 | 47.8 |

| 23:30 | AUD | Westpac Consumer Confidence Nov | 6.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Oct | |

| Forecast: 2.70% | Previous: 2.70% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Current Account (JPY) Sep | |

| Forecast: 2.99T | Previous: 3.02T | ||

| 02:00 | NZD | RBNZ Inflation Expectations Q4 | |

| Forecast: | Previous: 2.03% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Oct | |

| Forecast: 47.2 | Previous: 47.8 | ||

| 23:30 | AUD | Westpac Consumer Confidence Nov | |

| Forecast: | Previous: 6.20% | ||

Tuesday, Nov 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 1.50% | 1.30% |

| 00:30 | AUD | NAB Business Confidence Oct | -2 | |

| 00:30 | AUD | NAB Business Conditions Oct | 7 | |

| 07:00 | EUR | Germany CPI M/M Oct F | 0.40% | 0.40% |

| 07:00 | EUR | Germany CPI Y/Y Oct F | 2.00% | 2.00% |

| 07:00 | GBP | Claimant Count Change Oct | 30.5K | 27.9K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.10% | 4.00% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 3.90% | 3.80% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 4.90% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | 13.2 | 13.1 |

| 10:00 | EUR | Germany ZEW Current Situation Nov | -86 | -86.9 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 20.5 | 20.1 |

| 11:00 | USD | NFIB Business Optimism Index Oct | 91.9 | 91.5 |

| 13:30 | CAD | Building Permits M/M Sep | -1.10% | -7.00% |

| 23:50 | JPY | PPI Y/Y Oct | 3.00% | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | |

| Forecast: 1.50% | Previous: 1.30% | ||

| 00:30 | AUD | NAB Business Confidence Oct | |

| Forecast: | Previous: -2 | ||

| 00:30 | AUD | NAB Business Conditions Oct | |

| Forecast: | Previous: 7 | ||

| 07:00 | EUR | Germany CPI M/M Oct F | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 07:00 | EUR | Germany CPI Y/Y Oct F | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 07:00 | GBP | Claimant Count Change Oct | |

| Forecast: 30.5K | Previous: 27.9K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | |

| Forecast: 4.10% | Previous: 4.00% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | |

| Forecast: 3.90% | Previous: 3.80% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | |

| Forecast: | Previous: 4.90% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | |

| Forecast: 13.2 | Previous: 13.1 | ||

| 10:00 | EUR | Germany ZEW Current Situation Nov | |

| Forecast: -86 | Previous: -86.9 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | |

| Forecast: 20.5 | Previous: 20.1 | ||

| 11:00 | USD | NFIB Business Optimism Index Oct | |

| Forecast: 91.9 | Previous: 91.5 | ||

| 13:30 | CAD | Building Permits M/M Sep | |

| Forecast: -1.10% | Previous: -7.00% | ||

| 23:50 | JPY | PPI Y/Y Oct | |

| Forecast: 3.00% | Previous: 2.80% | ||

Wednesday, Nov 13 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 0.90% | 0.80% |

| 13:30 | USD | CPI M/M Oct | 0.20% | 0.20% |

| 13:30 | USD | CPI Y/Y Oct | 2.40% | 2.40% |

| 13:30 | USD | CPI Core M/M Oct | 0.30% | 0.30% |

| 13:30 | USD | CPI Core Y/Y Oct | 3.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q3 | |

| Forecast: 0.90% | Previous: 0.80% | ||

| 13:30 | USD | CPI M/M Oct | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | CPI Y/Y Oct | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 13:30 | USD | CPI Core M/M Oct | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Oct | |

| Forecast: | Previous: 3.30% | ||

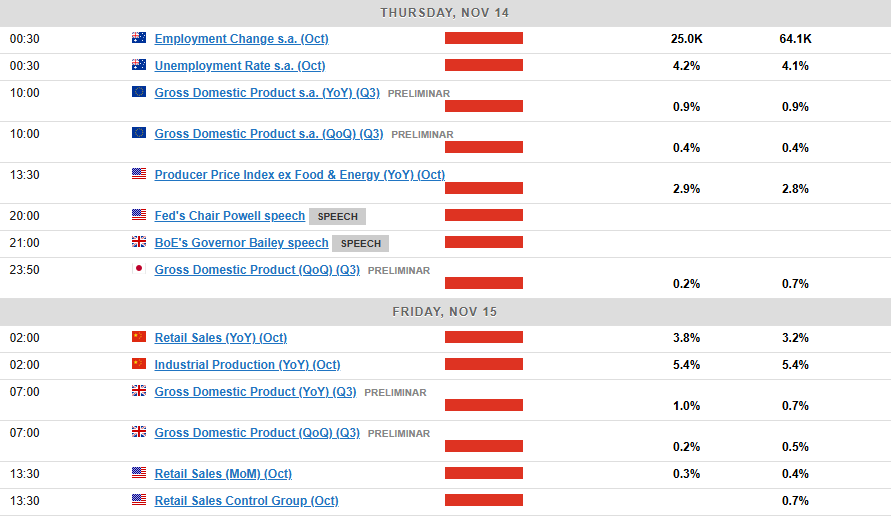

Thursday, Nov 14, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Nov | 4.00% | |

| 00:01 | GBP | RICS Housing Price Balance Oct | 12% | 11% |

| 00:30 | AUD | Employment Change Oct | 25.0K | 64.1K |

| 00:30 | AUD | Unemployment Rate Oct | 4.10% | 4.10% |

| 10:00 | EUR | Eurozone GDP Y/Y Q3 P | 0.90% | 0.90% |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.40% | 0.40% |

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -1.20% | 1.80% |

| 12:30 | EUR | ECB Meeting Accounts | ||

| 13:30 | USD | PPI M/M Oct | 0.20% | 0.00% |

| 13:30 | USD | PPI Y/Y Oct | 1.80% | |

| 13:30 | USD | PPI Core M/M Oct | 0.30% | 0.20% |

| 13:30 | USD | PPI Core Y/Y Oct | 2.80% | |

| 13:30 | USD | Initial Jobless Claims (Nov 8) | 221K | |

| 15:30 | USD | Natural Gas Storage | 69B | |

| 16:00 | USD | Crude Oil Inventories | 2.1M | |

| 21:30 | NZD | Business NZ PMI Oct | 46.9 | |

| 23:50 | JPY | GDP Q/Q Q3 P | 0.20% | 0.70% |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | 2.90% | 3.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Nov | |

| Forecast: | Previous: 4.00% | ||

| 00:01 | GBP | RICS Housing Price Balance Oct | |

| Forecast: 12% | Previous: 11% | ||

| 00:30 | AUD | Employment Change Oct | |

| Forecast: 25.0K | Previous: 64.1K | ||

| 00:30 | AUD | Unemployment Rate Oct | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 10:00 | EUR | Eurozone GDP Y/Y Q3 P | |

| Forecast: 0.90% | Previous: 0.90% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | |

| Forecast: -1.20% | Previous: 1.80% | ||

| 12:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 13:30 | USD | PPI M/M Oct | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 13:30 | USD | PPI Y/Y Oct | |

| Forecast: | Previous: 1.80% | ||

| 13:30 | USD | PPI Core M/M Oct | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 13:30 | USD | PPI Core Y/Y Oct | |

| Forecast: | Previous: 2.80% | ||

| 13:30 | USD | Initial Jobless Claims (Nov 8) | |

| Forecast: | Previous: 221K | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 69B | ||

| 16:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 2.1M | ||

| 21:30 | NZD | Business NZ PMI Oct | |

| Forecast: | Previous: 46.9 | ||

| 23:50 | JPY | GDP Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | |

| Forecast: 2.90% | Previous: 3.20% | ||

Friday, Nov 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | CNY | Industrial Production Y/Y Oct | 5.40% | 5.40% |

| 02:00 | CNY | Retail Sales Y/Y Oct | 3.80% | 3.20% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 3.50% | 3.40% |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | 0.20% | -1.10% |

| 04:30 | JPY | Industrial Production M/M Sep F | 1.40% | 1.40% |

| 07:00 | GBP | GDP M/M Sep | 0.20% | 0.20% |

| 07:00 | GBP | GDP Q/Q Q3 P | 0.20% | 0.50% |

| 07:00 | GBP | Industrial Production M/M Sep | 0.20% | 0.50% |

| 07:00 | GBP | Industrial Production Y/Y Sep | -1.60% | |

| 07:00 | GBP | Manufacturing Production M/M Sep | 0.00% | 1.10% |

| 07:00 | GBP | Manufacturing Production Y/Y Sep | -0.30% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -16.5B | -15.1B |

| 07:30 | CHF | PPI M/M Oct | 0.10% | -0.10% |

| 07:30 | CHF | PPI Y/Y Oct | -1.30% | |

| 13:30 | CAD | Manufacturing Sales M/M Sep | -0.70% | -1.30% |

| 13:30 | CAD | Wholesale Sales M/M Sep | 0.20% | -0.60% |

| 13:30 | USD | Empire State Manufacturing Index Nov | 3.6 | -11.9 |

| 13:30 | USD | Retail Sales M/M Oct | 0.30% | 0.40% |

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 0.20% | 0.50% |

| 13:30 | USD | Import Price Index M/M Oct | -0.10% | -0.40% |

| 14:15 | USD | Industrial Production M/M Oct | -0.20% | -0.30% |

| 14:15 | USD | Capacity Utilization Oct | 77.10% | 77.50% |

| 15:00 | USD | Business Inventories Sep | 0.20% | 0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | CNY | Industrial Production Y/Y Oct | |

| Forecast: 5.40% | Previous: 5.40% | ||

| 02:00 | CNY | Retail Sales Y/Y Oct | |

| Forecast: 3.80% | Previous: 3.20% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Sep | |

| Forecast: 0.20% | Previous: -1.10% | ||

| 04:30 | JPY | Industrial Production M/M Sep F | |

| Forecast: 1.40% | Previous: 1.40% | ||

| 07:00 | GBP | GDP M/M Sep | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 07:00 | GBP | GDP Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 07:00 | GBP | Industrial Production M/M Sep | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 07:00 | GBP | Industrial Production Y/Y Sep | |

| Forecast: | Previous: -1.60% | ||

| 07:00 | GBP | Manufacturing Production M/M Sep | |

| Forecast: 0.00% | Previous: 1.10% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Sep | |

| Forecast: | Previous: -0.30% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | |

| Forecast: -16.5B | Previous: -15.1B | ||

| 07:30 | CHF | PPI M/M Oct | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 07:30 | CHF | PPI Y/Y Oct | |

| Forecast: | Previous: -1.30% | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | |

| Forecast: -0.70% | Previous: -1.30% | ||

| 13:30 | CAD | Wholesale Sales M/M Sep | |

| Forecast: 0.20% | Previous: -0.60% | ||

| 13:30 | USD | Empire State Manufacturing Index Nov | |

| Forecast: 3.6 | Previous: -11.9 | ||

| 13:30 | USD | Retail Sales M/M Oct | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Oct | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 13:30 | USD | Import Price Index M/M Oct | |

| Forecast: -0.10% | Previous: -0.40% | ||

| 14:15 | USD | Industrial Production M/M Oct | |

| Forecast: -0.20% | Previous: -0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | |

| Forecast: 77.10% | Previous: 77.50% | ||

| 15:00 | USD | Business Inventories Sep | |

| Forecast: 0.20% | Previous: 0.30% | ||

Markets Weekly Outlook – Attention Shifts Back to Data, US CPI in Focus

- Trump’s clean sweep saw a significant rise in the US Dollar and Yields. Can it continue?

- Data in focus next week, US CPI data is due with potential implications for Federal Reserve policy and interest rate decisions.

- US Dollar Index (DXY) breaks above key level of 105.00. Where to next for the Greenback?

Week in Review: Trump Trade in Spotlight as US Dollar and Yields Rise

A blockbuster week comes to a close with a slow Friday as markets still digest the news and potential developments after Donald Trump swept to victory in the US elections. Not a surprise, at least from my side, however there were a few moves in markets that took me by surprise.

Looking back at the week, the US Dollar and Wall Street indexes rose sharply following Trump’s victory. This should not have come as a surprise given the much discussed Trump trade in the lead up to the election or the growing narrative that Trump will be a positive for economic growth.

The 47th President of the United States will only assume office on January 20, 2025. Despite this, markets are already beginning to anticipate the effect of some of Trump’s policies which are likely to be implemented. The biggest one being tariffs which if implemented could potentially lead to an uptick in inflation and potentially slower rate cuts. We are already seeing the effect in the lead up to and since the election as US yields rose on heightened inflation expectations. However, a December rate cut remains firmly on the cards with January likely to be an interesting meeting for the Fed as incoming President Trump would have just assumed office.

The US Dollar Index (DXY) has hit levels last seen in July, which together with the rising US Yields dragged Gold prices down to a weekly low around 2642. However, Thursday saw a significant recovery for the precious metal but it looks set to end the week below the $2700 handle. US Yields did however give back most of the gains made this week trading flat at the time of writing.

Source: TradingView

Oil prices had a surprisingly muted week given the moves across global markets. Brent was trading around 1% down for the week at the time of writing.

On the FX front, the rise of the USD index has dragged Cable and EUR/USD lower with emerging markets. One of the biggest winners of the week is undoubtedly Bitcoin which printed two fresh highs, first at 75000 and then on Friday a fresh high at 77000. A lot of the move is down a Trump presidency with the incoming President a proponent of the Cryptocurrency industry.

The Week Ahead: China’s Standing Committee Meeting

Asia Pacific Markets

The week ahead in the Asia Pacific region will see a slowdown with the exception of data from China.

In China, CPI data will be released on Saturday morning, and it is expected to stay around 0.4% compared to last year. More data will be released next Friday, and it is anticipated that the numbers will be a bit stronger for October, following the monetary easing from September. Housing prices will be watched closely for signs that they are starting to stabilize, and even a smaller drop than usual would be seen as positive news.

Japan will release its third-quarter GDP data next week. Growth is expected to slow to 0.3% from 0.8% in the second quarter because of typhoon and earthquake warnings affecting economic activities. Private consumption is expected to increase a little, but construction and facility investment might decrease. Growth is anticipated to pick up again in the fourth quarter due to a rebound.

Australia’s labor market is expected to slowly weaken in the fourth quarter, with unemployment increasing to 4.3%. This is because while there are still many people available for work, the number of new jobs being created is slowing down.

Europe + UK + US

In developed markets, the Euro Area will have a break from high impact data. There are some data releases from smaller countries which are likely to have a minimal impact on the under pressure Euro.

In the UK, the unemployment rate is expected to go up slightly, but these numbers are seen as unreliable because of sampling problems. Other payroll data shows that hiring outside the government has dropped a lot this year. Wage growth is likely to slow down as well, partly because of comparisons to previous high numbers.

UK GDP data is also due, monthly data indicates that growth in the third quarter was much slower compared to the first half of the year, partly because of earlier data fluctuations. Surveys show that the pace has slowed a bit, but the new budget is expected to help increase growth next year.

In the US next week attention shifts firmly back to data. Although market attention has shifted to the jobs market I expect inflation to still hold weight moving forward especially after the election.

Used and new car prices are expected to rise for October’s CPI, keeping the overall rate at 0.2% and core CPI at 0.3%. This is above the 0.17% monthly rate needed for the 2% inflation target, which might lead to doubts about the Fed cutting rates in December. However, with a cooling job market and tight monetary policy, a rate cut is still anticipated. There might be a pause in January due to possible stronger growth with Donald Trump as President, a business-friendly environment, and higher inflation from trade tariffs.

Chart of the Week

This week’s focus is back to the US Dollar Index (DXY), which has finally broken higher after a brief period of consolidation. Looking at the Trump trade, the question will be whether it continues until Trump’s election.

Looking at the DXY chart there is a key area of support marked off with the red box on the chart around 104.50. Below that we have support at 104.028 with the 200-day MA resting at 103.850 which makes this area a key area of confluence.

Conversely, a move to the upside may find resistance at 105.40 and 105.63 before the 106.00 handle comes into focus.

As I mentioned above, the biggest factor to pay attention to will be whether the ‘Trump trade’ continues, if it dies the DXY may continue higher.

US Dollar Index Daily Chart – November 8, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 104.50

- 104.00

- 103.65

Resistance

- 105.40

- 105.63

- 106.00

The Weekly Bottom Line: Trump Victory Likely to Bring Big Policy Changes

Canadian Highlights

- Donald Trump’s election victory means heightened macroeconomic uncertainty north of the border.

- Canada’s labour market put in a decent showing in October as the unemployment rate steadied, while job creation continues.

- A hefty increase in preliminary housing sales data for October may be proof that interest rate cuts are beginning to boost housing market activity.

U.S. Highlights

- President-elect Donald Trump will serve as the 47th president of the United States, securing 295 of the 538 Electoral College votes.

- Republicans also gained control of the Senate, while the House of Representatives is still up for grabs. Odds favor the Republicans maintaining control of the House, though 25 seats have yet to be called.

- The Federal Reserve delivered on a quarter-point rate cut this week, and kept the door open to further cuts in the months ahead.

Canada – With Certainty Comes Uncertainty

In case you missed it, there was a U.S. election this week! Former President Trump will return to the White House come January. With that, the degree to which his policies will impact Canada’s economy will be a lingering question for months to come. We have gathered our initial thoughts on the economic impacts here. In the aftermath of the results, Canada’s 10-year yield spiked nearly 20 basis points (bps) to over 3.40% but has fully retraced at the time of writing. The CAD finished flat on the week (0.719 cents) despite heightened volatility, while Canadian stocks caught a bid, rising 2.5%.

A big near-term question is how Trump’s tariff policy will jolt U.S.–Canadian trade relations. Our recent research details our expectations related to the future state of trade. In short, the existing USMCA trade agreement with the U.S. (and Mexico) could keep Canada insulated from tariffs, so long as we make a handful of concessions come the pact’s review in 2026. That said, we do not discount the very real risk that Trump could move forward with tariffs on Canada, which would have immediate negative impacts on GDP, inflation, and trade.

Trump’s presidency also puts the Canadian dollar on a different path. Our forecast for higher U.S. inflation will result in a slower pace of U.S. rate cuts in 2025, widening the spread between the Bank of Canada and the Fed, and pressuring the loonie lower (Chart 1). The Canadian dollar has already depreciated around 3% against the Dollar since early-September, and we expect the CAD will bottom in Q1-2025 before modestly appreciating thereafter. It would not surprise us to see the CAD temporarily break below 70 cents in the near-term.

The election overshadowed some important domestic developments. For one, Canada’s job market looks to be on solid footing. Canada’s economy has added a respectable 270k jobs so far this year, 15k of which came in October. Against this backdrop, we are seeing the unemployment topping out around current levels (Chart 2), as the federal government’s plan to aggressively slow population growth should limit the buildup of further labour market slack. Meanwhile, wages continue to show signs of stickiness and a jump in hours worked suggests October GDP growth could print a solid number.

Elsewhere in the Canadian economy, housing markets may finally be responding to rate cuts. Preliminary sales data for October are consistent with a hefty 8% increase in home sales based on double digit surges in Toronto and Vancouver sales activity. With additional interest rate cuts on the way and new federal borrowing measures, more momentum is likely to build.

For now, the Bank of Canada’s (BoC) best approach would be to look through the near-term uncertainties when setting the policy rate. It is still too early to have a high-conviction call for the December 11th meeting given the deluge of data between now and then, but we do think that the Bank will revert back to a 25 bps cut after opting for a 50 bps jumbo move last month.

U.S. – Trump Victory Likely to Bring Big Policy Changes

U.S. equities surged higher this week following Donald Trump’s decisive victory in the presidential election. Longer-term Treasury yields also shot higher, but later retraced all of Wednesday’s Trump trade as the Federal Reserve helped to calm the bond market by delivering on a quarter-point rate cut. The S&P 500 ended the week 4% higher and is now up an impressive 25% year-to-date. Meanwhile, the 10-year Treasury yield is looking to the end week slightly lower at 4.32% but is up nearly 60 basis points (bps) over the past month. (Chart 1).

Beyond winning the White House, the Republicans also took control of Senate, securing 53 of the 100 seats as of writing. Two races are still too close to call, so there’s potential for the GOP’s majority to widen a bit more once all the ballots are counted. Meanwhile, control for the House of Representatives remains up in the air, with 25 seats still to be called. At this point, odds heavily favor the Republicans maintaining control of the House, but it’s unclear whether the GOP will be able to make further inroads relative to their current slim majority of four. If the GOP retains only a slim majority in the House, President Trump will need near-unanimous GOP support to pass legislation, which could present some challenge to his agenda.

One thing is for certain under Trump 2.0: tariffs are coming. Once sworn in on January 20th, we expect Trump to use executive powers to act quickly and levy sweeping tariffs on many of the U.S.’s trading partners. China is at the top of the list, but history has shown that Trump isn’t afraid to raise tariffs on allies. While it is possible that Canada and Mexico receive some carve-outs, it would likely be conditional on them following the U.S.’s lead and leveraging similar tariffs on China. Others may also negotiate concessions, but that isn’t likely to happen until after the tariffs are in play.

No matter which way you slice it, the more protectionist trade measures will be inflationary and work against the Federal Reserve’s objective of restoring 2% inflation. At the press conference, Chair Powell acknowledged this point, but also noted that the Fed doesn’t adjust its policy rate to potential changes in fiscal or other government policies. For now, the FOMC remains highly data dependent. This puts next week’s inflation report in focus, particularly after the September reading came in hotter than expected. With the economic data still strong, any further signs of stickiness on the inflation front will likely push Fed officials away from continued quarter-point cuts and towards a slower rate cut trajectory.

At this point, we still feel that a December rate cut is still likely. However, we’ve revised our forecast for next year, reflecting the fact that tariffs (and the potential for tax cuts) will result in more persistent inflationary pressures. We now assume the Fed takes a more gradual approach in reducing the policy rate in 2025, cutting at every-other meeting, resulting in a total of 100 bps of easing by year-end (Chart 2).

Weekly Economic & Financial Commentary: Higher Rates Likely Under Trump Administration

Summary

United States: Election Results Don't Clarify the Outlook

- Even as the 2024 presidential election has come and gone, there is still a tremendous amount of uncertainty regarding the trajectory of the economy and Fed policy. Tariffs and a tax policy look to be on the docket in the next administration, which could come with higher inflation and thereby higher rates.

- Next week: NFIB Small Business Optimism Index (Tue.), CPI (Wed.), Retail Sales (Fri.)

International: Global and Thematic Implications of the U.S. Election

- In our view, Trump winning the White House and having a largely unilateral ability to implement tariffs and shift U.S. trade policy in a more protectionist direction is yet another deglobalization force. New trade barriers would have the potential to weigh on the interconnectedness of the global economy, which could have longer-term negative implications for global economic growth. We also view the election results as supportive of further U.S. dollar strength in the medium term.

- Next week: India CPI (Tue.), Central Bank of Mexico (Thu.), China Retail Sales & Industrial Production (Fri.)

Interest Rate Watch: Higher Rates Likely Under Trump Administration

- President-elect Trump’s victory sparked upward movements in equities and bond yields across the curve. This week’s Fed meeting was less eventful. As was widely expected, the FOMC reduced the federal funds target range by 25 bps to 4.50%-4.75%. Although Chair Powell declined to comment on the election, our expectation for the path of Fed easing has evolved. As we see it today, the potential for higher inflation next year raises the likelihood that the federal funds rate bottoms out closer to 4% than 3%.

Topic of the Week: The 2024 U.S. Elections: Economic Implications

- Election Day has come and gone. Donald Trump was elected the 47th president of the United States, becoming the second person to serve two non-consecutive terms as president. We walk through our preliminary thoughts on the recent election results and their implications for the U.S. economy.

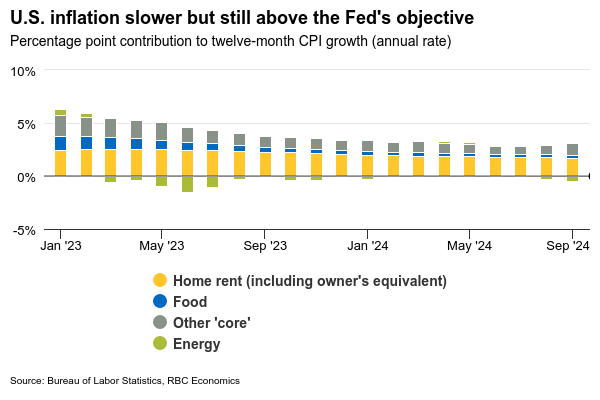

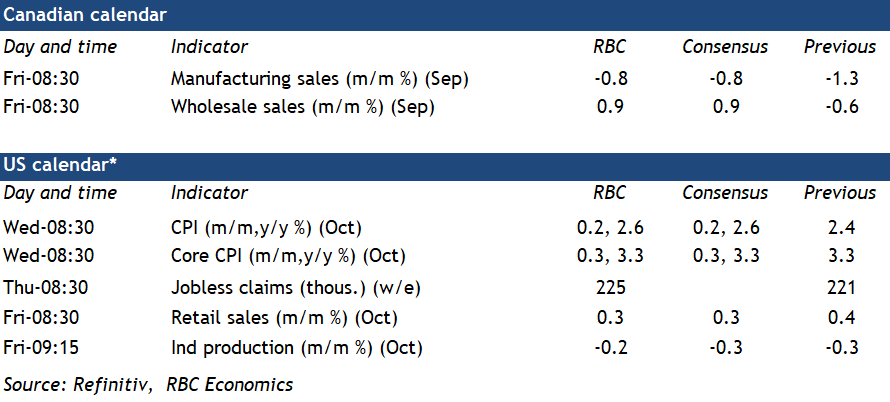

U.S. Inflation Still Running Above Fed’s Target in October

U.S. inflation numbers will be closely watched by policymakers on Wednesday for any further signs that resilient growth domestic product and consumer spending is putting a floor under price growth.

U.S. GDP growth in Q3 was strong and a jump in auto sales in October means Friday's retail sales report should show another increase early in Q4. But that strength has also come alongside firmer-than-expected inflation prints in recent months, and has markets questioning how quickly (and how much) the U.S. Federal Reserve will cut interest rates in the year ahead.

In October, we expect that U.S. headline consumer price index growth ticked up to 2.6% year-over-year from 2.4% in September. Average gasoline prices fell in October and food prices continue to grow at a pace closer to the Fed's 2% target. But, sticky core inflation—which we expect held steady at 3.3% annually—continues to drive the bulk of price growth. Up until September, home rents were responsible for the lack of downward movement in the core measure. But last month, the share of CPI basket items (excluding shelter) reporting price growth above 3% moved higher from September.

The Fed takes a longer-term view of inflation data, with Chair Powell reiterating after a 25 basis point cut this week that price growth has still slowed substantially from where it was despite recent upside surprises. We continue to expect that gradual softening in labour markets will ease underlying inflation pressures enough to justify another Fed interest rate cut in December. But we also expect that interest rates will need to remain higher in 2025 than policymakers have been expecting to offset the inflationary impact of a large government budget deficit and keep price growth on a (sustainable) path back towards the Fed’s 2% objective.

Week ahead data watch

U.S. retail sales likely edged up again in October, given auto sales were strong. However, (a price-led) sales decline at gas stations would partially offset higher auto sales.

We expect the U.S. industrial production on Friday to inch lower in October, following the 0.3% decline in September. The weakness was mainly driven by lower output in the manufacturing sector as the impact of the Boeing strike and hurricanes dragged into October.

Week Ahead – US CPI to Shift Market Focus Back to Data After Trump Shock

- After Trump comeback, normality to return to markets with US CPI

- GDP data from UK and Japan to also be important

- But volatility to likely persist as markets assess impact of Trump 2.0

US CPI eyed as rate cut bets fade after Trump win

Donald Trump’s historic return to the White House was met with a euphoric response by the markets. Wall Street and Bitcoin rallied to record highs, while the US dollar skyrocketed to 4-month highs. Perhaps the most significant move, however, is the surge in Treasury yields.

Yields had already been on the rise since late September as investors pared back their bets of how many times the Federal Reserve would cut interest rates over the course of the next 2-3 years. But Trump’s victory has dealt a further blow to hopes of low interest rates.

If Trump enacts his campaign pledges of lower taxes and higher tariffs, the expected effect on the economy is that this would push up prices by boosting domestic demand and raising import costs. The Fed would have little choice but to maintain restrictive monetary policy for longer than is currently anticipated.

The October CPI report due on Wednesday will be the first post-election test for rate cut bets following the repricing from the ‘Trump trade’. In September, the headline CPI rate fell to 2.4% y/y. However, it is expected to have edged up to 2.5 y/y in October. The month-on-month rate is projected at 0.2%, unchanged from the prior month. Core CPI is also forecast to have ticked up, rising from 3.3% to 3.4% y/y in October.

On Thursday, producer prices for the same month will also be watched, while on Friday, attention will turn to the retail sales report. Other releases will include the Empire State Manufacturing index and industrial production, both due on Friday.

Should the CPI numbers come in below expectations, yields and the dollar will be at risk of correcting lower following the recent sharp gains. However, if the data continue to surprise to the upside, the greenback’s bullish run might have further to go. This could prove problematic for Wall Street, though, as sooner or later, higher yields would begin to bite for Wall Street traders.

Can UK data halt the pound’s slide?

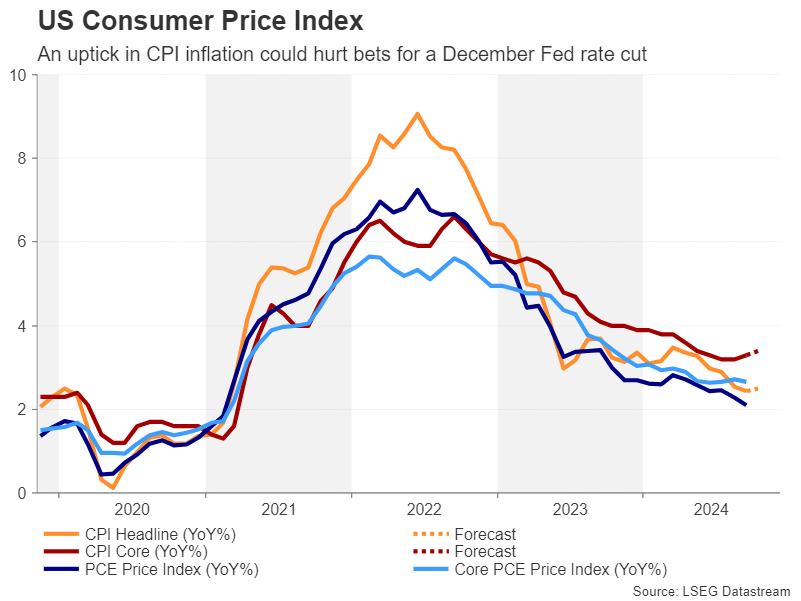

US yields are not the only ones soaring lately. The 10-year yield on UK government gilts has risen by more than 20 basis points since the country’s new Labour government presented its tax and spend budget on October 30. Despite tax hikes amounting to £40 billion, the budget is seen as increasing the government’s borrowing requirements, as spending looks set to rise faster than the tax intake. Moreover, much of the spending increases will be frontloaded in the first two years of the parliamentary term, potentially lifting GDP growth in the current fiscal year and next.

The Bank of England has already incorporated the Budget impact into its economic projections and has signalled it will have to maintain caution on the pace of easing. Wage growth remains a concern despite falling substantially this year. The latest figures on average weekly earnings are out on Tuesday, as well as the employment change for the three months to September.

GDP stats will follow on Friday with the first estimate for the third quarter. The UK economy is forecast to have grown by 0.2% q/q during the quarter, slowing from the prior quarter’s 0.5% pace.

Faster-than-expected growth in Q3 would further dash hopes of the BoE speeding up rate cuts over the coming months, and this may help the pound recoup some of its recent losses versus the greenback.

However, disappointing data could add to sterling’s woes, potentially pushing it below $1.29.

Euro could take to the sidelines

The euro has also been under strain lately amid a gloomier Eurozone outlook compared to other major economies. Nevertheless, Q3 growth surprised to the upside and the preliminary reading of 0.4% q/q will likely be confirmed in the second estimate on Thursday. Quarterly employment growth numbers are also on the agenda on Thursday, as well as September industrial production.

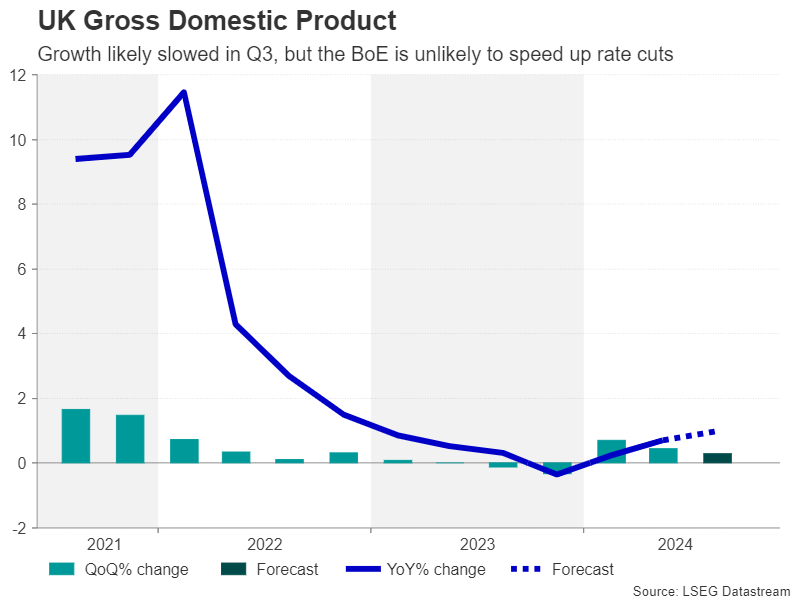

Ahead of those releases, Germany’s ZEW economic sentiment survey might attract some attention on Tuesday. However, investors might be more interested in the political happenings in Germany following the collapse of the coalition government. Snap elections are looming, which may take place as early as January. A change in government in Berlin might pave the way for a reform of the country’s debt brake rule, which limits new borrowing to 0.35% of GDP.

However, any reaction in the euro is likely to be muted for now and the single currency will likely have a calmer time following the volatility of the past week.

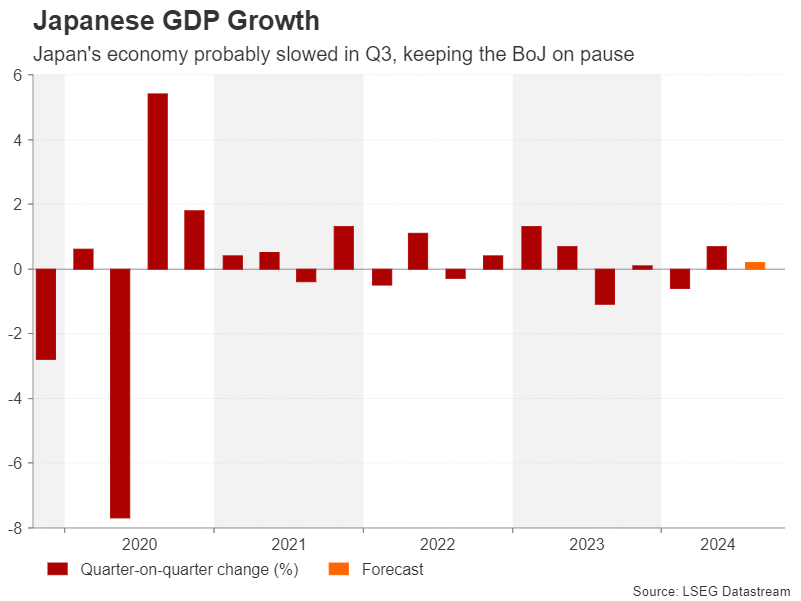

Can Japanese GDP revive the yen?

The yen’s losses since mid-September deepened after the US elections as the dollar jumped to a three-month high of 154.71 yen. But the primary reason for the yen’s negative reversal is the uncertainty around the timing of the Bank of Japan’s next rate hike.

Investors are currently assigning around a 40% probability for a 25-basis-point rate rise in December. But the BoJ may decide to wait until after next year’s annual spring wage negotiations before making up its mind.

For expectations for an earlier rate cut to strengthen, there would have to be a significant improvement in both the growth and inflation data. Hence, better-than-forecast GDP numbers for Q3 on Friday could lift the yen slightly.

Waiting for China’s stimulus to kick in

Elsewhere, the Australian dollar will be keeping an eye on domestic wage growth and employment indicators on Wednesday and Thursday, respectively. Meanwhile the RBZN’s quarterly survey on inflation expectations on Monday could be vital for the New Zealand dollar, as a further decline could bolster bets of a 75-bps rate cut in November.

The aussie and kiwi will additionally be watching the latest data out of China. CPI and PPI figures for October are out on Saturday and the monthly prints on industrial output and retail sales will follow on Friday. Although Chinese authorities have stepped up their stimulus policies over the past year, there’s yet to be a notable acceleration in growth. However, any pickup in activity in October, particularly in retail sales, could raise hopes of a quickening economic recovery, boosting the antipodean currencies and risk assets more broadly.