Sample Category Title

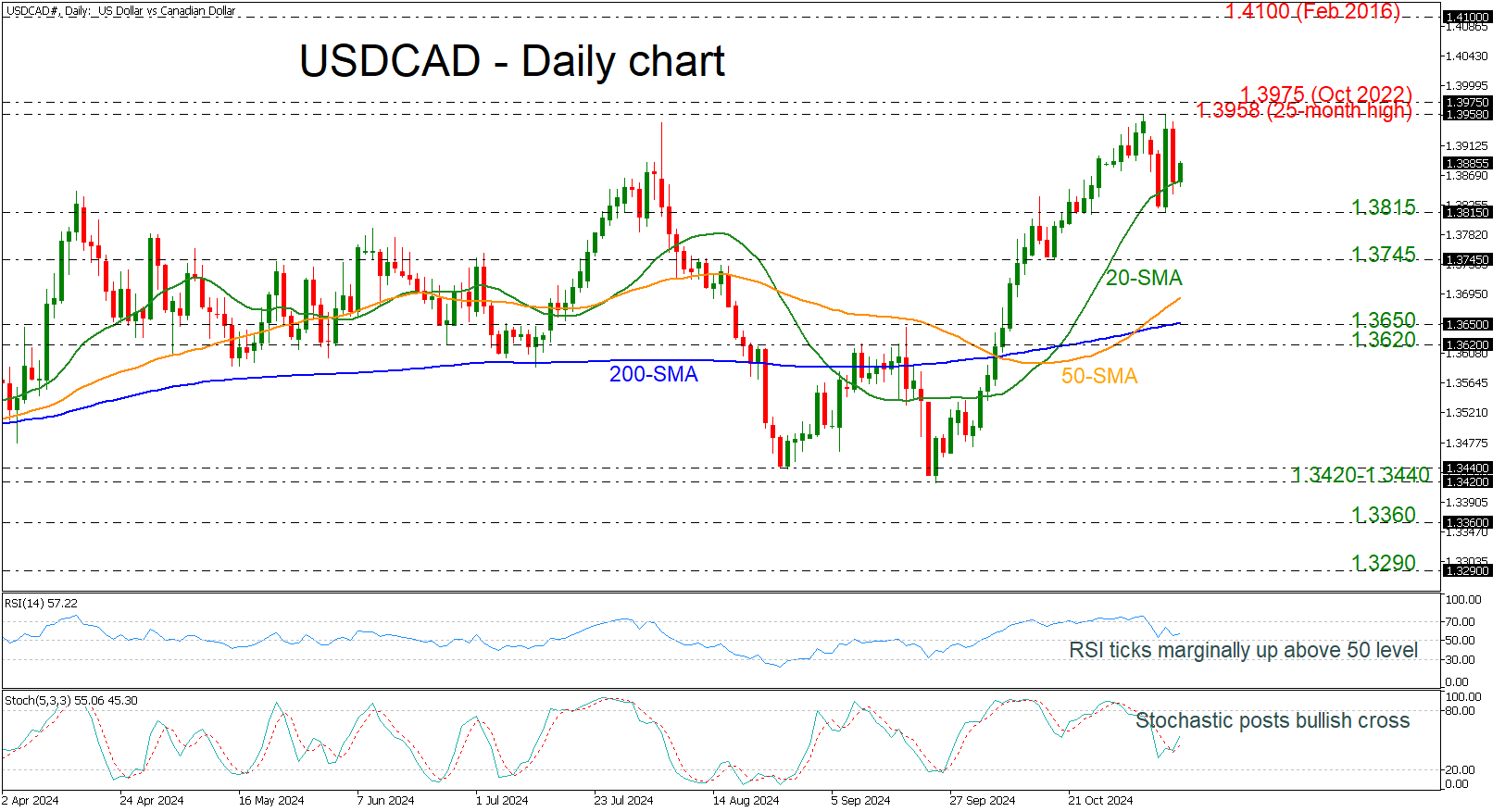

USDCAD Retains Bullish Bias Above 20-day SMA

- USDCAD posts new 25-month high but currently stands beneath it

- Stochastics and RSI show positive signs

USDCAD has been developing above the 20-day simple moving average (SMA) since the bounce off the 1.3815 support level and is trying to regain ground.

Daily oscillators suggest that the upside momentum is still in place, reflecting the pullback in the market. The RSI turned up after it reached the 50 level, while the stochastic posted a bullish crossover within its %K and %D lines.

If buyers maintain control and push the price above the more than two-year high of 1.3958, it could reach the peak of 1.3975 achieved in October 2022. Rising further, the market could rest near the next round number of 1.4100, registered in February 2016.

However, should sellers take charge, the first obstacle to the downside might be the 1.3815 support ahead of the 1.3745 barricade. If this support is violated, the focus would then shift to the 50-day SMA at 1.3690, which is ahead of the 200-day SMA, which is located near the 1.3650 support.

Summarizing, as long as the price remains above the 200-day SMA, the outlook remains bullish in the short term. A decisive break above the October 2022 peak of 1.3975 would switch the broader picture to positive as well.

Elliott Wave View in EURGBP Calling for More Downside

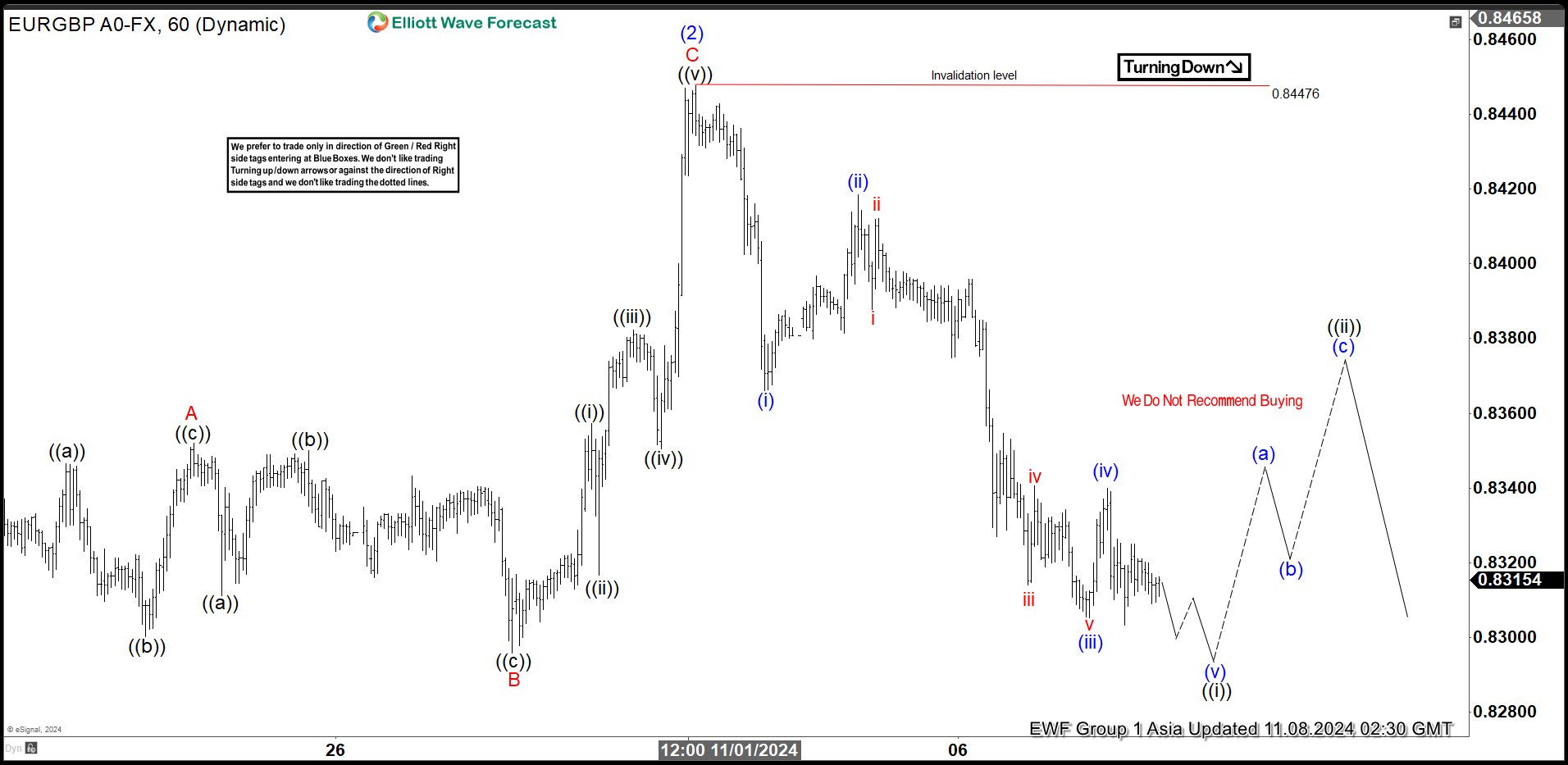

Short Term Elliott Wave View in EURGBP suggests that decline to 0.8295 on October 18, 2024 ended wave (1). Wave (2) corrective bounce is proposed complete at 0.8447 as the 1 hour chart below shows. Internal subdivision of wave (2) unfolded as a Flat Elliott Wave structure. Up from 10.18.2024 low, wave A ended at 0.8352 and wave B pullback ended at 0.8295. Wave C higher ended at 0.8447 which completed wave (2) in higher degree. Pair has turned lower in wave (3) with internal structure of an impulse.

Down from wave (2), wave (i) ended at 0.8366 and wave (ii) ended at 0.8418. Wave (iii) has resumed lower as an impulse. Down from wave (ii), wave i ended at 0.8388 and wave ii ended at 0.8412. Wave iii lower ended at 0.8414 and wave iv rally ended at 0.834. Last leg wave v lower ended at 0.8305 which completed wave (iii) in higher degree. Wave (iv) corrective rally ended at 0.833. Expect pair to extend lower to end wave v of ((i)). Then it should rally in wave ((ii)) to correct cycle from 11.1.2024 high before it resumes lower. Near term, as far as pivot at 0.8447 high stays intact, expect rally to fail in 3, 7, or 11 swing for further downside.

EURGBP 60 Minutes Elliott Wave Chart

EURGBP Elliott Wave Video

https://www.youtube.com/watch?v=r6x2q1AhrH8

Fed Powell Said Too Soon to Say How Trump Administration’s Policies Would Reshape Outlook

Markets

The barrage of central bank meetings in Sweden, Norway, the Czech Republic and the UK ended with a decision in the US. The Fed delivered the expected 25 bps cut to 4.5-4.75%. The new statement featured little changes compared to September and guidance for future decisions, if any, was limited. Chair Powell in the presser said the way to a more neutral stance will be dictated by the health of the US economy and that the data currently do not suggest there’s “any need to be in a hurry to get there.” He added that as rates closed in on neutral, it may be appropriate to slow down the pace. With president-elect Trump on track to loosen the purse materially and add fuel to an already solid economy, the Fed may already be pretty close to that point. Powell said yesterday it was too soon to say how the Trump administration’s policies would reshape the outlook. But things may have gotten clearer by the December 18 meeting. Barring unexpected economic weakness, we wouldn’t be surprised to see the updated economic forecasts and Powell to lay the groundwork for a skip or pause the cycle early 2025. US interest rates dropped on a daily basis but that had little to do with the Fed decision. Yields simply gave back some of the post-election gains, easing between 6.3 (2-yr) and 12.1 (7-yr) bps, the belly of the curve outperforming the wings. Bunds underperformed Treasuries in anticipation of a new, willing-to-spend German government (already in January?) after the current one collapsed yesterday over the liberal democrat’s hard pass for lifting the debt brake. Yields recovered between 3.8 and 5.3 bps. Interest rate differentials favoured EUR/USD, lifting the pair back towards the 1.08 area. Sterling gained modestly to EUR/GBP 0.831. The Bank of England cut rates to 4.75% but governor Bailey was cautious about future cuts given the expansionary Labour budget. After a key four days that covered all corners of the world, the economic calendar shifts into lower gear ahead a long weekend for US (bond) markets. That paves the way for technical trading as markets look for a new balance in the run-up to, amongst others, next week’s US inflation numbers and retail sales. We do keep a close eye at the outcome of an important meeting in China that ends today. More supportive measures are expected to be announced.

News & Views

The Czech National Bank cut its key policy rate by 25 bps yesterday, to 4%, in a split decision. One out of seven members voted for leaving rates unchanged and one voted for a larger 50 bps rate cut. The Czech economy is recovering only slowly and is below its potential. GDP forecasts faced a downward revision compared with August: 1% for this year and 2.4% for 2025, from respectively 1.2% and 2.8%. Inflation is the central bank’s key worry though. The Bank board expects it to rise temporarily over the next few months (food prices) but core inflation remains elevated as well, especially in services. CPI forecasts faced an upward revision, from 2.2% to 2.5% this year and from 2% to 2.2% next year. It is expected to remain withing the 1%-3% tolerance band around the 2% inflation target but thus more elevated. Risks and uncertainties around the outlook are modestly inflationary overall. In this respect, the CNB says that it will approach future monetary policy easing with great caution and may pause or terminate the interest rate reduction process in the month ahead at levels that are still restrictive as rates approach neutral levels (3.5%). The Czech krone won ground after the hawkish cut with EUR/CZK dropping from the 25.40 support area to 25.25.

October’s KPMG and REC, UK report on jobs survey signaled further declines in both permanent and temporary placements during October. Rates of decline were the steepest since March, amid reports of reduced demand and hiring freezes at firms (partly in the run-up to the late October government Budget). Higher staff availability (20th consecutive monthly rise) amid a reduced number of vacancies was also seen. The increase in temps was notable in being the sharpest recorded by the survey since December 2020. “With many of the tax rises announced in last week’s Budget impacting businesses, the expectation from some chief execs is that this could further dampen hiring as companies grapple with absorbing any extra costs.” Whilst firms signaled willingness to pay higher salaries to suitable candidates, permanent salary growth softened in October to its lowest level since early 2021. REC CEO Carberry said that there’s little in the pay data of today’s report that suggests the BoE should step away from further cuts to interest rates, which will also boost business confidence.

Fed Has No Choice But to Dance to Trump’s Tune

The Federal Reserve (Fed) delivered the second rate cut of the year yesterday. Chair Jerome Powell said that the Fed doesn’t rule ‘out or in’ a rate cut in December, that the US economy is expanding solidly, that conditions in the labour market eased but the unemployment rate remains low, that inflation ‘made progress’ but not a ‘further progress’ – just progress – toward the committee’s 2% objective but remains elevated’, that the Trump policies won’t have an immediate impact on the US fundamentals as they don’t know how much time it will take the new Trump administration to implement them, and that he wouldn’t step down if Trump asked him to do so.

But the Fed has no choice but to dance to Trump’s tune, whether it likes it or not. That reality comes with the risk of higher-than-otherwise inflation and deserves careful attention.

For now, the probability of another 25bp cut in December is given 71% in the immediate aftermath of the US election and the Fed cut. The US 2-year yield retreated yesterday, following a Trump-led spike earlier this week. The 10-year yield also eased from an earlier spike to 4.33%. If US inflation doesn’t ease enough, and if the US economy remains robust and labour market remains in a good shape, the bond vigilantes, who think that the Fed is cutting too fast by too much, will send the yields higher. There are rumours of a potential spike in the 10-year yield to 5%. The latter would destroy the impact of rate cuts and weigh on sentiment.

Investors on a rosy cloud

The week saw the nest possible combination for US equity bulls. Trump has just won the presidential election and the Fed lowered the interest rates. The S&P500 hit another record high, as did Nasdaq 100, as did the Dow Jones. The rally in the small caps slowed on rising worries about the small companies’ ability to carry the burden of higher yields on their shoulders, but the mid caps could be an alternative for those who think that the prospects of higher yields on Trump makes the big caps look expensive at the current valuations.

Elsewhere

The US dollar bounced lower yesterday, as the Fed’s rate cut gave a good reason to the market to correct and consolidate the latest gains. The EURUSD rebounded but the upside remained capped near the 1.08 resistance, and Cable strengthened to flirt with the 1.30 on the back of a hawkish rate cut from the Bank of England (BoE), but gains were challenged by strong offers near the 1.30 psychological resistance.

This being said, the BoE is right to adopt a less dovish outlook given that the UK’s new budget – with extra spending to boost growth – will also boost inflation by half a percentage point according to the BoE. As such, Bailey – who had turned aggressive on rate cuts – didn’t remain long at that party. The BoE is now expected to keep lowering rates ‘gradually’. And that shift from ‘aggressive’ to ‘gradually’ easing outlook is supportive of the pound if of course the growth outlook doesn’t deteriorate significantly. Mid-1.30s look a reasonable target for the sterling bulls if the Fed insists on staying where it stands today.

But as Baily emphasized, the world has become a place with ‘very big geopolitical shocks’ and there are ‘very big uncertainties in the world economy and the world at large’. The latter should continue to help gold to defend its place in portfolios. The yellow metal saw support at the 50-DMA yesterday and should continue to be supported by haven flows and sustained central bank buying as a response, or preparation, to the new Trump era.

Over in China, the wait is long for investors who just want to see the Chinese authorities put a number on the amount of fiscal stimulus it will deploy to counter the Trump shock.

In energy, US crude was better bid this week, as news that OPEC would delay the production restrictions by at least a month and rumours that tensions in the Middle East could revive anytime were topped by the ‘hope’ that Trump would abandon the alternative energy plans altogether and put all of his weight behind the traditional energy sources. Presently, the barrel of US crude is testing the major 38.2% Fibonacci resistance on the summer selloff, near $72.85pb. A sustainable rise above this level requires encouraging fiscal boost from China. If not, the price rallies will remain interesting opportunities to sell the tops and keep the price of barrel close to the $70pb level.

China to Unveil Fiscal Stimulus Package

In focus today

Today, we should finally get actual numbers on China's fiscal stimulus as the meeting in the Standing Committee of the National People's Congress ends. In the US, the University of Michigan's flash consumer sentiment survey is due for release.

Economic and market news

What happened yesterday

In the US, the Fed unanimously cut rates by 25bp to 4.75%. This was widely expected and with the FOMC meeting giving little guidance for 2025, the market reaction was very muted. The Fed is still in a cutting cycle, economic data has generally been somewhat stronger than expected and downside risks have eased. However, how that translates to the rates outlook remains uncertain. Markets price in around 65-70% probability of the Fed delivering another 25bp cut at the December meeting. We make no changes to our call and still expect cuts to continue at every meeting towards H1 2025.

In the euro area, the euro climbed 0.64% regaining lost ground on the 1.8% fall on Wednesday, as investors digest the political events in Germany. Depending on the upcoming developments in Germany, a stable German government and a more pro-active fiscal stance could foster renewed confidence in the euro. The retail sales data surprised to the upside with retail sales m/m at 0.5% (cons: 0.4%, prior: 0.2%) and retail sales y/y at 2.9% (cons: 1.3%, prior: 0.8%). Read about our outlook for the euro area in: Research euro area - Fiscal policy to slow growth in 2025 - but mind the RFF, 7 November.

In Germany, following the turbulent political events of Wednesday, industrial production declined 2.5% m/m (cons: -1.0 % m/m, prior: 2.9% m/m) in September, thereby extending the downward trend seen over the past one and a half year, leaving German industrial production in Q3 2.3% lower than in the second quarter. We expect activity in the industry to continue to fall in the coming quarter, before gaining some support next year as financial conditions ease, global manufacturing improves, and energy prices have come down. However, we are not looking for a strong rebound next year but merely a stabilisation.

In the UK, the BoE cut rates by 25bp to 4.75% as expected. Importantly the committee shifted to a more hawkish stance in terms of a gradual approach. Last meeting the gradual approach would be warranted for "most members" now it is included in the bullet regarding the entire MPC. Overall, we saw a very muted reaction in the market, which we think the MPC aimed for following the jitters from the budget. Sending a signal of a gradual cutting cycle with a marginal hawkish bias given the inflationary budget, but not spooking markets following the significant market reactions we saw last week. We expect the BoE to remain on hold at the December meeting and maintain its "gradual approach". In 2025, we expect cuts at every meeting starting in February and until H2 2025, where we expect a step down to a quarterly pace. This leaves the Bank rate at 3.25% by YE 2025.

In Sweden, the Riksbank cut rate by 50bp to 2.75% as expected as focus turns to support growth and the expected recovery for next year. The Riksbank highlighted uncertainty around the economic recovery, international developments on economic policies (i.e. US election), geopolitics and the SEK. We continue to expect 25bp cuts over the next three meetings and finally reaching an end point of 1.75% by June, but also admit that the uncertainty looking into next year is high.

October flash CPIs came out above both market expectations and Riksbank expectations, with CPI at 0.2% m/m and 1.6% y/y, CPIF at 0.4% m/m and 1.5% y/y and CPIF ex energy at 0.2% m/m and 2.1% y/y.

In Norway, Norges Bank stayed on hold at 4.5% in line with our view and market expectations. As has been the case historically for Norges Bank interim meetings, the central bank gave very little news for markets to trade on. Norges Bank instead reiterated the message from September that rates will most likely be kept unchanged in December and that the first cut most likely looks set for March 2025; in line with our call.

In Japan, September wage data was released with annual earnings growth remaining solid and unchanged at 2.8%. While this still implies a 0.1% drop in annual real earnings, deflated with CPI excl. rent, but developments in recent months look promising. Currently we do not see wage data as a strong argument for hiking nor waiting. The Trump win added further to the yen slide giving some tailwind to our call for the next hike in December. Down the line, we will look out for the vote on PM in the Lower House on Monday and whether a new coalition will be opposed to higher rates.

In Denmark, Statistics Denmark reported a 4.9% decrease in total industrial production for September, with a more modest 2.2% decline when pharmaceuticals are excluded. Despite these figures, Denmark's industrial sector continues to perform well compared to other European regions, bolstered by a 1.3% upward revision in production in previous months. Globally, industrial performance is weak, particularly due to prolonged dip in demand for physical goods, high interest rates and economic slowdowns. However, Danish machinery industries have shown resilience and growth. Looking ahead, Danish industrial sales have promising prospects with potential growth initiatives in China and anticipated international rate cuts. However, forthcoming US trade policies under Donald Trump may introduce risks to Danish exports, although his proposed tax cuts might temporarily boost American consumption and, consequently, Danish exports.

Equities: Global equities were higher again yesterday, on the second trading day after the news about the next US president. One of the most intriguing aspects of yesterday's trade was that investors did not send down Emerging Markets, indicating how much was already priced in, along with the usual beta to growth. Moreover, one thing is Trump's comments during the election; another is how they translate into actual politics.

Calmness was the second significant takeaway from yesterday. There were few outsized moves, with the VIX and the move index dropping significantly. The VIX is already down at 15, matching the level we argued for a week ago if the election uncertainty had not been affecting markets. Thirdly, we observed some reversal of moves and rotations yesterday. Some of the biggest winners, including small caps and banks, underperformed. While some of this can be related to the uncertainty about the composition of the House of Representatives, we place greater weight on the belief that Trump and the new administration will not reverse the economic outlook.

To the equation of yesterday's moves, we must also add the fact that three major Western central banks made cuts. However, all of these were as expected and priced in before yesterday. In the US yesterday: Dow 0.0%, S&P 500 +0.7%, Nasdaq +1.5%, and Russell 2000 -0.4%. This morning, Asian markets are mostly lower, while European futures are marginally higher. US futures are very close to unchanged, feeding into the narrative of calmness returning to financial markets very quickly following this US presidential election.

FI: 10Y US Treasury yields fell some 10-12bp through yesterday's session as markets revisited the political premium added on Wednesday. Last night's FOMC meeting did not fuel any noticeable reaction in markets as Powell abstained from providing specific clues on the December meeting. In Europe, the German ASW-spread tightening continued through yesterday's session as the political turmoil in Germany added renewed pressure on bonds. The Bund spread is now trading at negative levels (-1.8bp) - the lowest levels seen since 2004. In EGB space, peripherals such as Italy saw some outperformance yesterday with the 10Y BTP-Bund spread narrowing 4bp.

FX: EUR/USD rose to around the 1.08 mark as broad USD appreciation following the Trump election outcome paused yesterday, with anticipated 25bp rate cut from the Fed. GBP/USD rose and temporarily breached 1.30 after Bank of England cut the policy by 25bp to 4.75%. We have argued for some time that EUR/SEK had reached overbought territory and was prone for a correction. Hence, we approve of the SEK gains after the US election even though it was a Trump win and after the Riksbank even though it was a 50bp rate cut. EUR/SEK now at 11.55 after peak just above 11.70 earlier this week. EUR/NOK dropped to below 11.80 after Norges Bank left rates unchanged. NOK/SEK rose to a 0.9880 intraday peak, though some gains was erased in the US session.

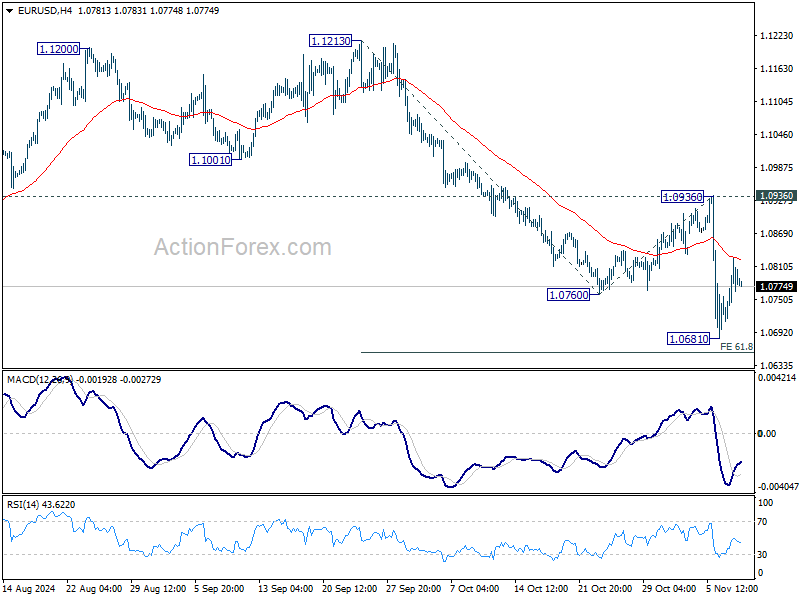

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0628; (P) 1.0783; (R1) 1.0885; More...

Intraday bias in EUR/USD remains neutral for consolidations above 1.0681 temporary low. Further decline is expected as long as 1.0936 resistance holds. On the downside, sustained break of 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656 will pave the way to 100% projection at 1.0483.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

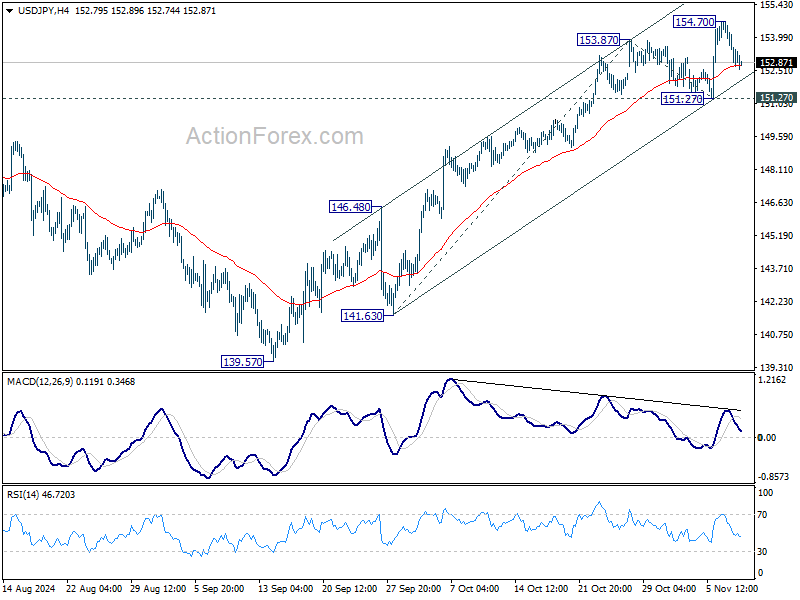

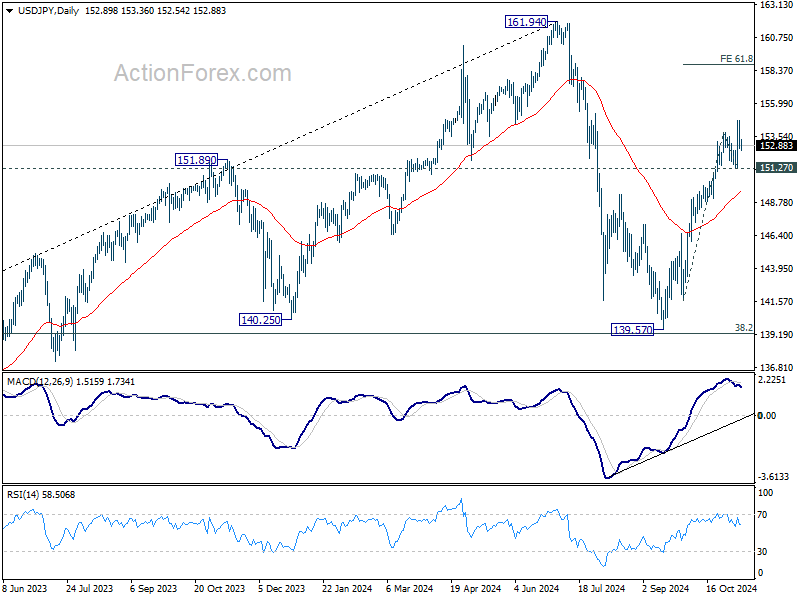

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.16; (P) 153.44; (R1) 154.17; More...

Intraday bias in USD/JPY remains neutral at this point, and some more consolidations would be seen below 154.70 temporary top. Further rally is expected as long as 151.27 support holds. On the upside, break of 154.70 will resume the rally from 139.57 to 61.8% projection of 141.63 to 153.87 from 151.27 at 158.83.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

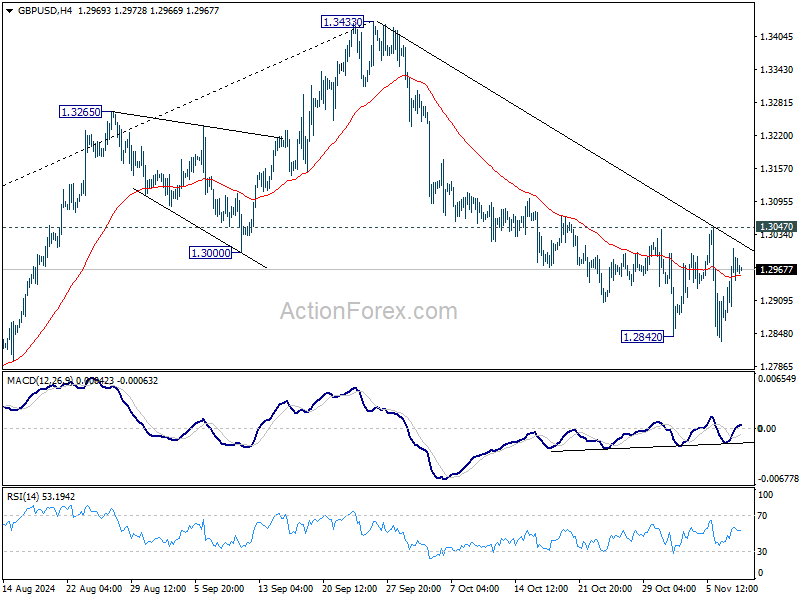

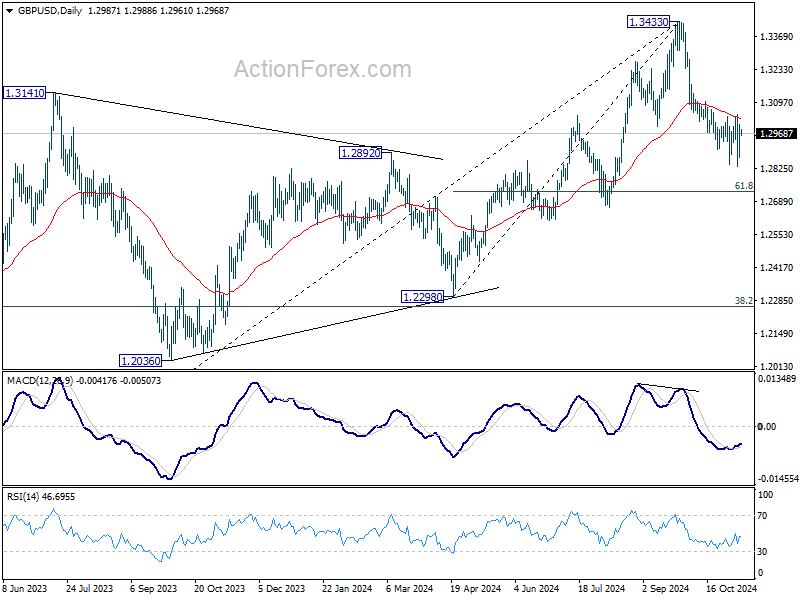

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2903; (P) 1.2956; (R1) 1.3040; More...

Intraday bias in GBP/USD stays neutral as sideway trading continues. With 1.3047 resistance intact, further decline is still expected. Firm break of 1.2842 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bullish convergence condition in 4H MACD, firm break of 1.3047 will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

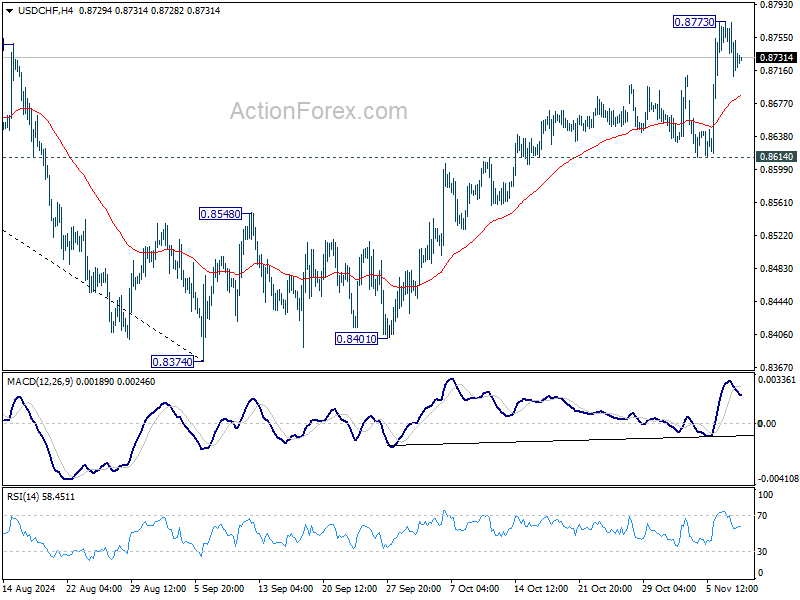

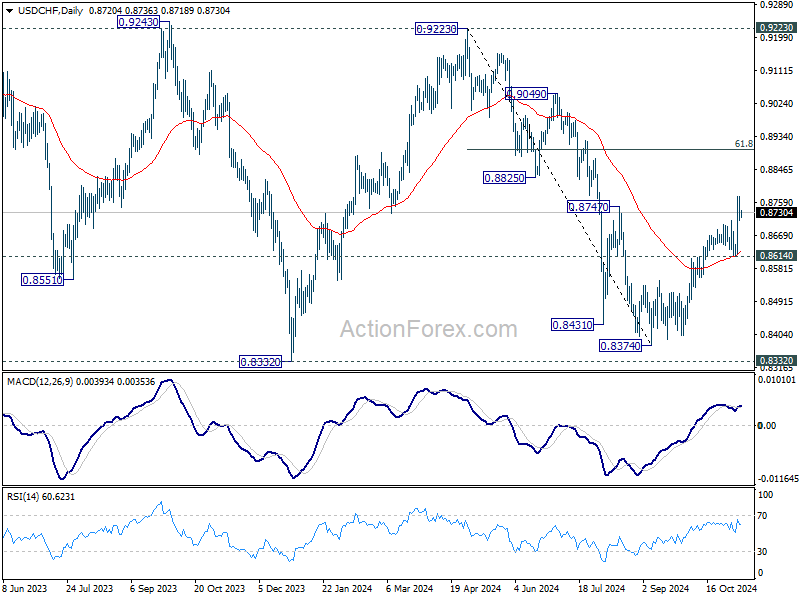

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8698; (P) 0.8736; (R1) 0.8762; More…

Intraday bias in USD/CHF is turned neutral with current retreat, and some consolidations would be seen below 0.8773 temporary top first. Further rally is still expected as long as 0.8614 support holds. Above 0.8773 will resume the rise from 0.8374 for 61.8% retracement of 0.9223 to 0.8374 at 0.8899 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

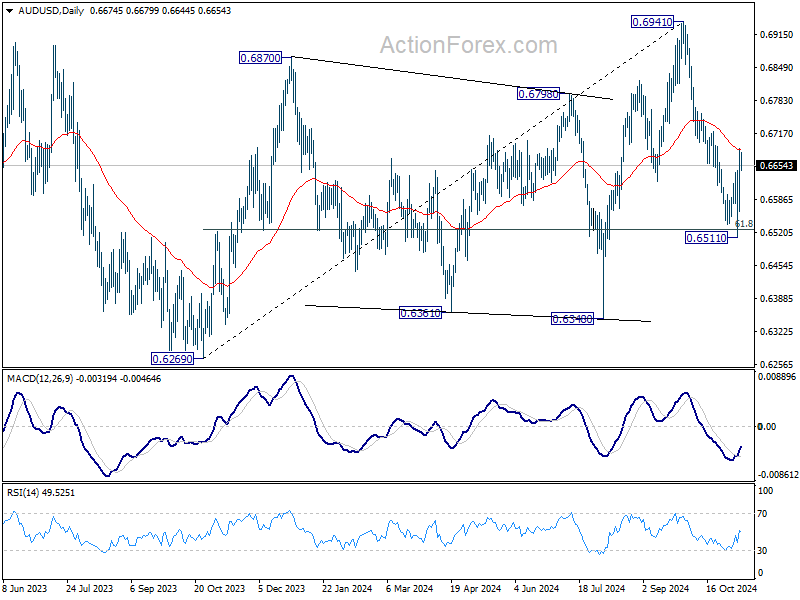

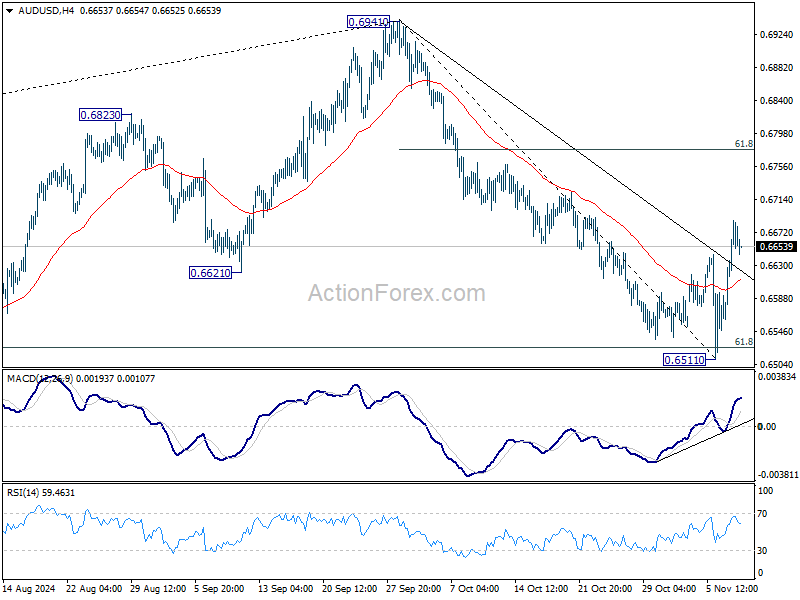

AUD/USD Daily Report

Daily Pivots: (S1) 0.6600; (P) 0.6644; (R1) 0.6724; More...

Intraday bias in AUD/USD remains on the upside as rebound from 0.6511 short term bottom is in progress. Sustained break of 55 D EMA (now at 0.6682) will bring stronger rebound back 61.8% retracement of 0.6941 to 0.6511 at 0.6777. On the downside, break of 0.6511 will resume the fall from 0.6941 instead.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.