Sample Category Title

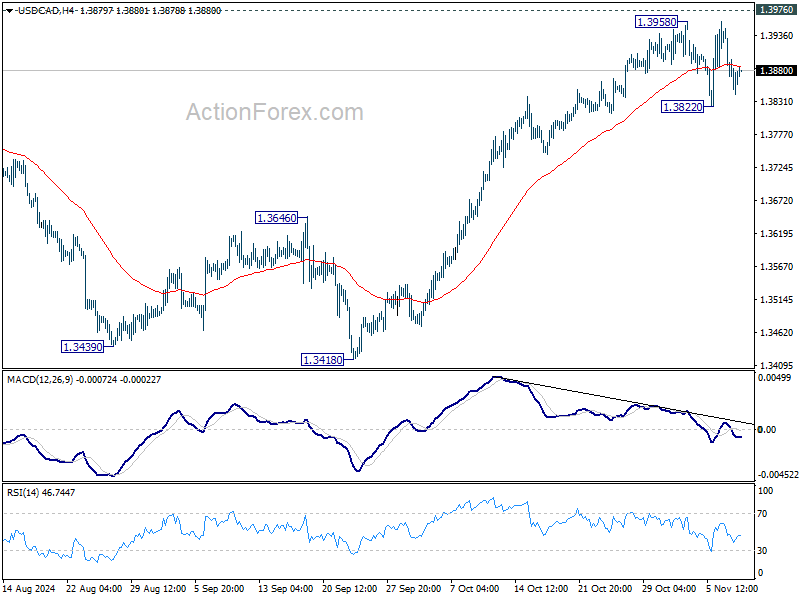

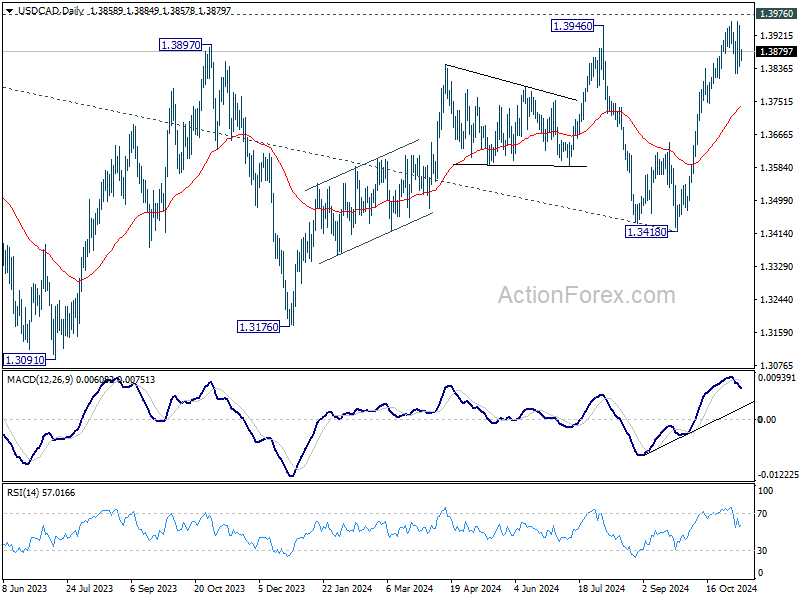

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3819; (P) 1.3884; (R1) 1.3925; More...

Intraday bias in USD/CAD remains neutral as range trading continues below 1..3958. On the downside break of 1.3822 will bring deeper pullback. But downside should be contained by 55 D EMA (now at 1.3740). On the upside, decisive break of 1.3976 will resume larger up trend.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

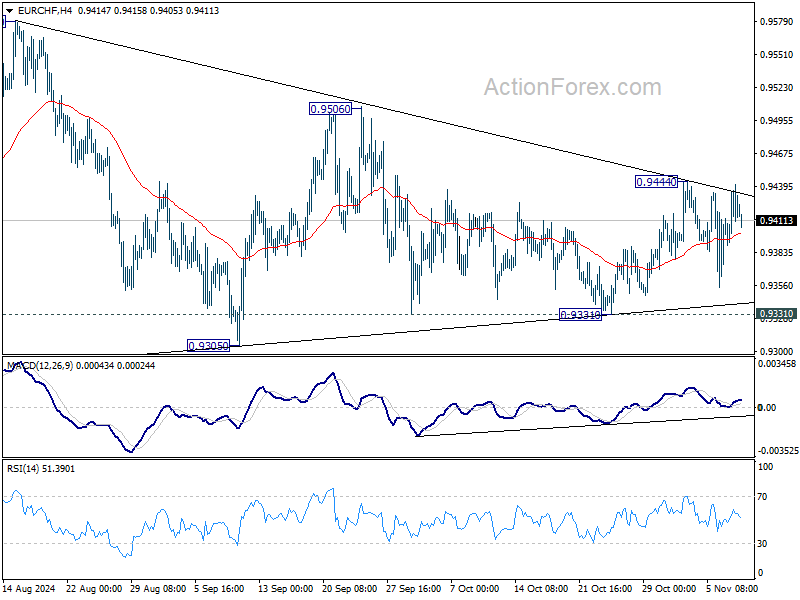

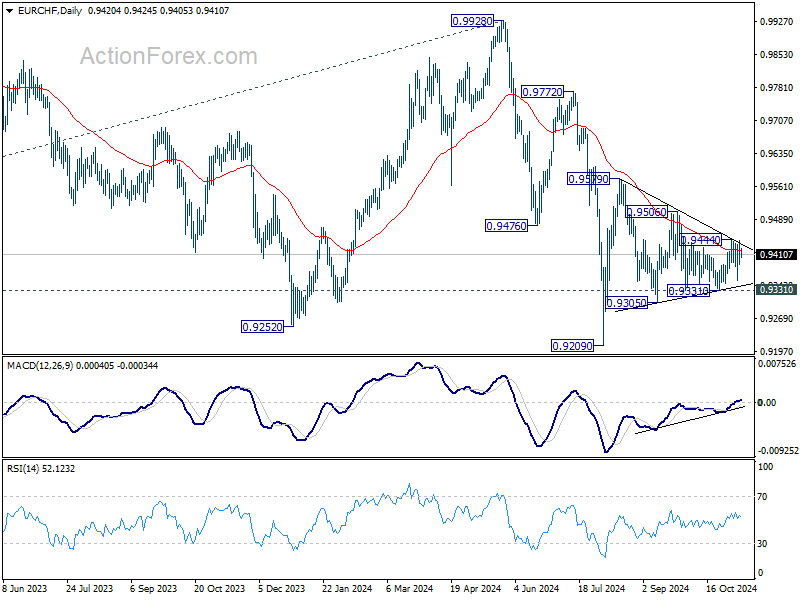

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9390; (P) 0.9417; (R1) 0.9451; More....

EUR/CHF is still bounded in converging triangle and intraday bias remains neutral. On the upside, break of 0.9444 will turn intraday bias to the upside for 0.9506 resistance and above. On the downside, break of 0.9331 will resume the fall from 0.9579 towards 0.9209 low.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9421) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

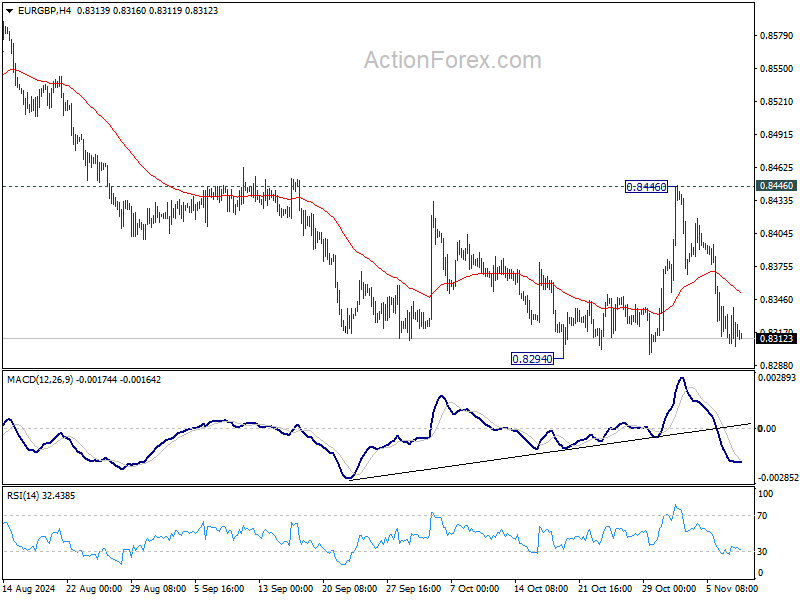

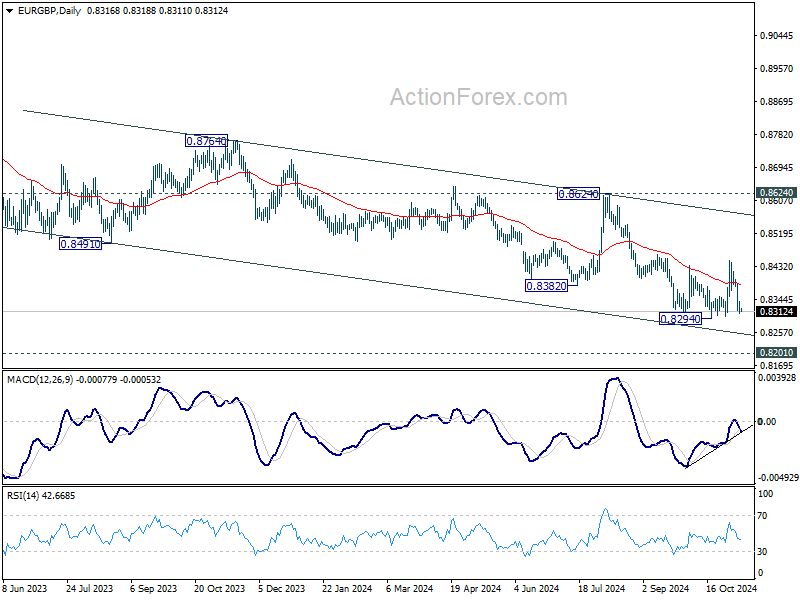

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8303; (P) 0.8322; (R1) 0.8336; More...

Intraday bias in EUR/GBP stays neutral and outlook remains bearish with 0.8446 resistance intact. On the downside, break of 0.8294 low will resume larger down trend to 0.8201 key support next. On the upside, break of 0.8446 will resume the rebound from 0.8294 short term bottom towards 0.8624 resistance instead.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

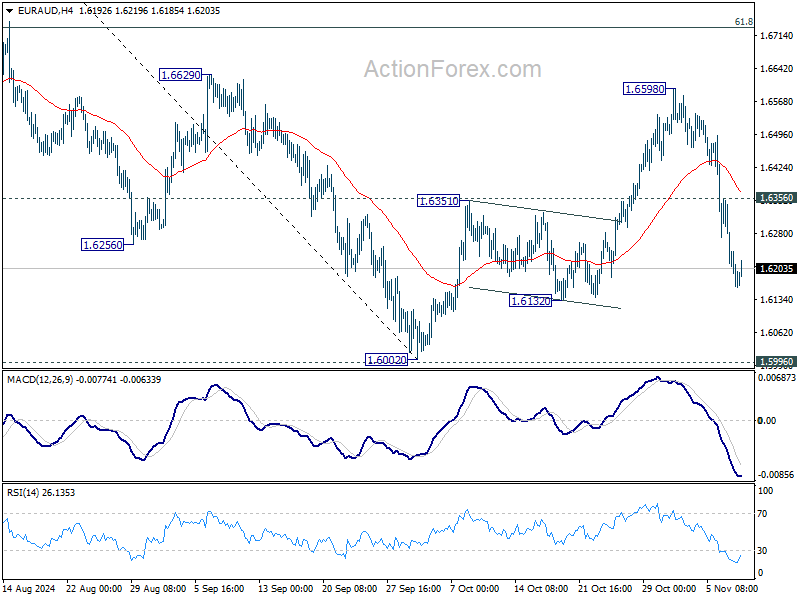

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6107; (P) 1.6227; (R1) 1.6291; More...

EUR/AUD's fall from 1.6598 is in progress and intraday bias stays on the downside. Break of 1.6132 will target 1.5996 key support again. Strong support could be seen there to bring rebound. ON the upside, above 1.6356 minor resistance will turn intraday bias neutral again first.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.08; (P) 198.82; (R1) 199.31; More...

GBP/JPY dips notably today as consolidation from 199.79 extends. Intraday bias remains neutral first. Further rally is expected as long as 55 D EMA (now at 194.79) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

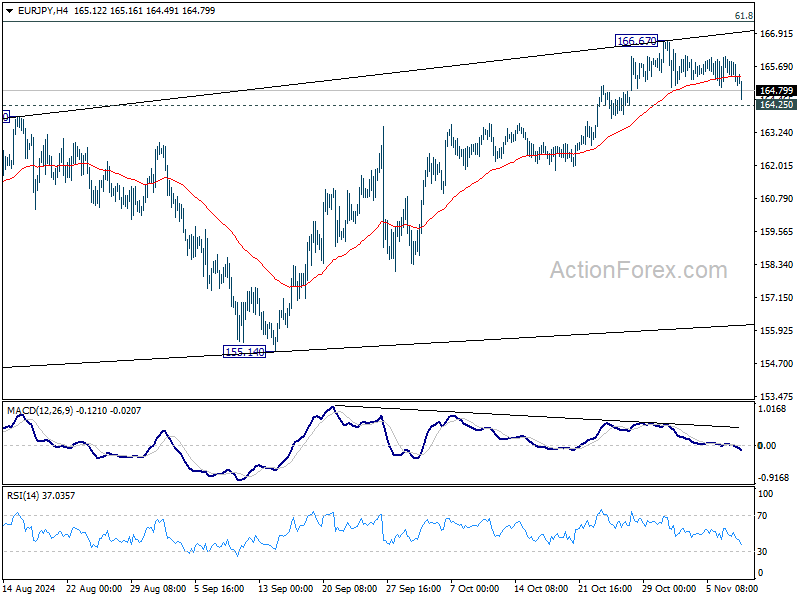

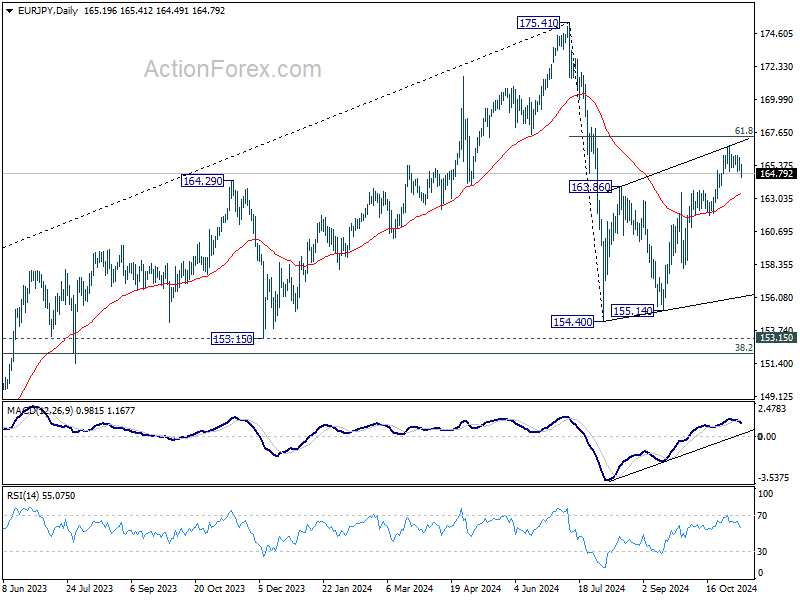

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.80; (P) 165.39; (R1) 165.79; More....

EUR/JPY's retreat from 166.67 extends lower today but stays above 164.25 minor support. Intraday bias remains neutral for the moment, and further rally is in favor. On the upside, Sustained break of 61.8% retracement of 175.41 to 154.40 at 167.38 will pave the way to retest 175.41 high. However, considering bearish divergence condition in 4H MACD, firm break of 164.25 will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 163.36).

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

Yen Rebounds as Japan and South Korea Signal Readiness to the Region’s Currency Markets

Yen jumps broadly in Asian trading today, boosted by heightened government warnings against the recent selloff on the currency. Japanese Finance Minister Katsunobu Kato issued a strong statement addressing the “one-sided and drastic moves” in Yen, confirming that the government is monitoring the situation with the “utmost sense of urgency.” He emphasized Japan’s commitment to take “appropriate actions” to counter what it considers excessive volatility.

Supporting this stance, Japanese Ministry of Finance released quarterly data revealing substantial interventions earlier last quarter. On July 11, Japan spent JPY 3.168T on dollar-selling intervention, followed by an additional JPY 2.367T on July 12. These efforts successfully lifted the Yen from a low of 161.76 to 157.30 within two days, effectively defending the critical 160 psychological level.

Adding a broader regional perspective, South Korea’s Finance Minister, Choi Sang-mok, also announced an expanded 24-hour monitoring framework that will now include financial markets and foreign exchange alongside ongoing concerns related to the Middle East. Minister Choi assured markets that South Korean authorities are prepared to act swiftly if volatility spikes in the currency or financial markets.

The coordinated messages from both Japan and South Korea suggest the possibility of regional intervention should depreciation pressures on Yen and South Korean Won intensify, highlighting a collective commitment to maintaining currency stability in the face of global economic uncertainties.

Overall in the currency markets, Aussie is currently as the strongest performer of the week, followed by Kiwi and Loonie. Aussie is bolstered by robust risk-on sentiment emanating from the US, RBA's vigilance on inflation, and the notable rebound in copper prices. Conversely, Euro is currently the weakest, followed by Swiss Franc and Dollar. Sterling and Yen are positioned in the middle of the performance spectrum.

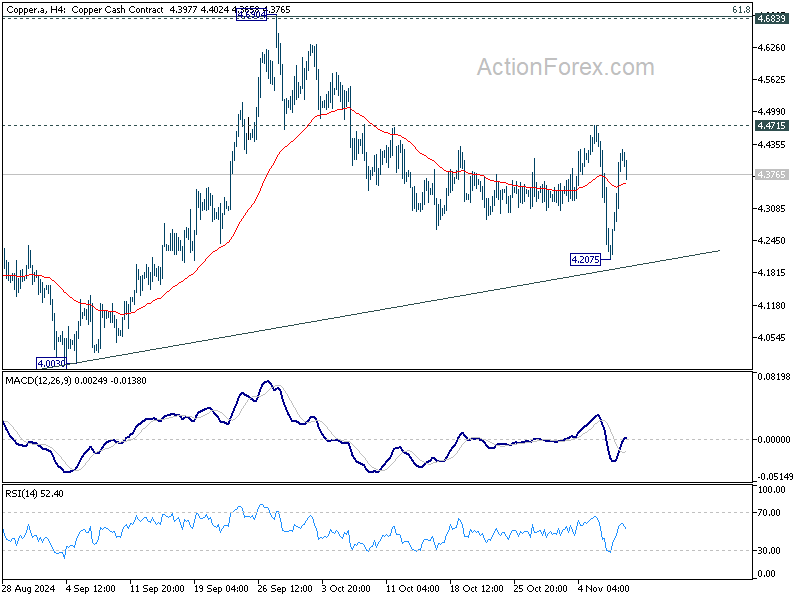

Technically, focus is now back on 4.4715 resistance in Copper after the strong rebound from 4.2075. Firm break there will argue that corrective fall from 4.6904 has completed as a three-wave corrective move. In this case, stronger rise would be seen back to 4.6904. If realized, this would provide extra lift to AUD/USD towards 0.6941 high.

In Asia, at the time of writing, Nikkei is up 0.22%. Hong Kong HSI is down -0.58%. China Shanghai SSE is down -0.33%. Singapore Strait Times is up 1.55%. Japan 10-year JGB yield is down -0.0056 at 1.001. Overnight, DOW fell -0.00%. S&P 500 rose 0.74%. NASDAQ rose 1.51%. 10-year yield fell -0.085 to 4.341.

US 10-yr yield retreats after Fed holds rates steady; Powell highlights fiscal risks

US 10-year Treasury yield eased back notably overnight following Fed's decision to keep interest rates steady. Chair Jerome Powell's balanced commentary offered a calm counterpoint to the election-fueled rally in yields seen earlier this week.

During the press conference, Powell downplayed the immediate impact of the election on monetary policy, stating that it "will have no effect on our policy decisions" in the near term. He emphasized that Fed's current policy stance is "well positioned" to manage risks and uncertainties, and that the central bank can adjust its policy restraints "more slowly" or "more quickly" depending on how economic developments unfold.

Addressing recent inflation data, Powell noted that it "wasn't terrible," but was "a little higher than expected." He highlighted that by December, the FOMC will have additional data to consider, including one more employment report and two more inflation reports. "We’ll make a decision as we get to December," Powell said.

However, he issued a stark warning about the US fiscal situation, asserting that fiscal policy is "on an unsustainable path." Powell elaborated: “The federal government’s fiscal path, fiscal policy, is on an unsustainable path. The level of our debt relative to the economy is not unsustainable, the path is unsustainable." He added, “We see that in a very large deficit, you’re at full employment that’s expected to continue, so it’s important that be dealt with. It is ultimately a threat to the economy.”

More on FOMC:

- Fed Review: In a Good Place After All

- Fed Continues To Dial Back Policy Restraint via 25 bps Rate Cut

- FOMC Focused on Health of Labour Market and Success with Inflation

Technically, 10-year yield has encountered notable resistance from medium term falling trend line and 61.8% retracement of 4.997 to 3.603 at 4.464. Some consolidations would be seen first, but such consolidations should be relatively brief as long as 4.223 support holds. Rise from 3.603 is expected to resume sooner rather than later. Sustained trading above 4.464 will pave the way to retest 4.997 high. Nevertheless, break of 4.223 will argue that deeper correction is underway back to 55 D EMA (now at 4.075).

Looking ahead

France trade balance, Swiss SECO consumer climate will be featured in European session. Later in the day, Canada employment and US U of Michigan consumer sentiment will be released.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.80; (P) 165.39; (R1) 165.79; More....

EUR/JPY's retreat from 166.67 extends lower today but stays above 164.25 minor support. Intraday bias remains neutral for the moment, and further rally is in favor. On the upside, Sustained break of 61.8% retracement of 175.41 to 154.40 at 167.38 will pave the way to retest 175.41 high. However, considering bearish divergence condition in 4H MACD, firm break of 164.25 will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 163.36).

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

Cliff Notes: An Event-Filled Week

Key insights from the week that was.

Domestically, the main event was the RBA’s November policy meeting, where the Board decided once again to leave the cash rate unchanged at 4.35%. Communications on the day – via the decision statement, press conference, and Statement on Monetary Policy – provided more colour around changes to the RBA’s forecasts. Most notable were a near-term downgrade to consumer spending and the edging down of underlying inflation in 2026, while the outlook for employment growth was revised up.

On balance, developments since the last policy meeting have not materially altered the RBA’s perspective, a mixed picture on the domestic economy reinforcing the Board’s patient approach of “not ruling anything in or out” for the time being. Echoing this point, the Board’s policy discussion in November considered the balance of risks around the central case of remaining on hold versus actively considering a rate hike or cut – similar to September.

In a video update midweek, Chief Economist Luci Ellis explained the key takeaways from the RBA’s decision in more detail. In our view, the RBA’s interpretation of the recent data flow is slightly more hawkish than our own, offering greater certainty the RBA Board will not change their stance this year. However, we remain of the view that the first rate cut will be delivered in February 2025 and easing will continue at a measured pace of 25bps per quarter from there until 3.35% in Q4 2025, a rate we consider to be broadly neutral for the economy.

Offshore, the medium-term settings and consequences of fiscal policy are becoming less certain, but the immediate path for monetary policy is clear.

Throughout the week, markets were squarely focussed on the US Presidential and Congressional elections. Donald Trump comfortably surpassed the 270 Electoral College votes needed to serve a second term as President. While some Congressional contests are still to be confirmed, the Republican party looks to be on track to hold a majority in both the Senate and House of Representatives. These results should give President-elect Trump considerable scope to enact mooted policy reform across tax, regulation, spending and trade. While specific policy detail won’t be known until after inauguration on 20 January, the net result for the deficit is expected to be expansionary, steepening the uptrend in Federal Government debt on issue over the coming decade. Market participants are likely to continue to front-run fiscal decision making, holding Treasury yields around their current level, almost 75bps above September’s low.

The immediate outlook for monetary policy is certainly not behind the lift in yields. This week the FOMC followed up September’s 50bp cut with a 25bp reduction, taking the mid-point of the fed funds range to 4.625%. Chair Powell was clear in the press conference that the Committee expect inflation to continue to abate to target, with non-housing services and goods inflation already consistent with headline inflation of 2.0%yr, and strength in housing inflation a consequence of past agreements not current market dynamics. While positive on the outlook for activity and employment, it is clear the FOMC are now more concerned with downside risks for the labour market than upside price risks. Any further deterioration in the labour market would be unwanted.

On this week’s election specifically, Chair Powell made clear that the outcome will have no effect on monetary policy in the near term. It is only over time, as policy is committed to and implemented, that the economic implications become clear and any monetary policy response can be decided upon. The December FOMC meeting will be the first opportunity for Committee members to update their forecasts; however, this will be more than a month before the new administration takes office, let alone when the President-elect and new Congress begin to debate policy. By late-2026 however, we believe the FOMC will see a need to tighten policy to counteract the cumulative inflationary consequences of more expansionary fiscal policy, which is likely to focus on supporting demand versus supply. With much of the expected fiscal policy effects already priced in, term interest rates are likely to hold near current levels over the coming year, then edge higher from late-2025, pre-empting monetary policy tightening.

Across the pond, the Bank of England also cut rates by 25bp to 4.75% this week. The Committee provided its assessment of the new government budget, nudging the GDP profile higher by ¾% at its peak in Q4 2025. A rise in employment costs from an increase in the National Living Wage and changes in the employers' National Insurance contribution will also influence wages and profits margins, and ultimately inflation. The inflation outlook was nudged up from Q3 2025, with headline inflation not expected to be sustainably at target until Q2 2027, a year later than in the prior set of forecasts. The BoE's central case is that further economic slack is needed to normalise inflation and wage dynamics, warranting a 'gradual approach' to removing restrictive policy. The exact pace of rate cuts from here will depend on the data flow, meeting by meeting. The closer Bank Rate gets to its neutral level, the greater the justification for prudence.

USD/JPY Rebounds With New Traction: Can It Sustain Rise?

Key Highlights

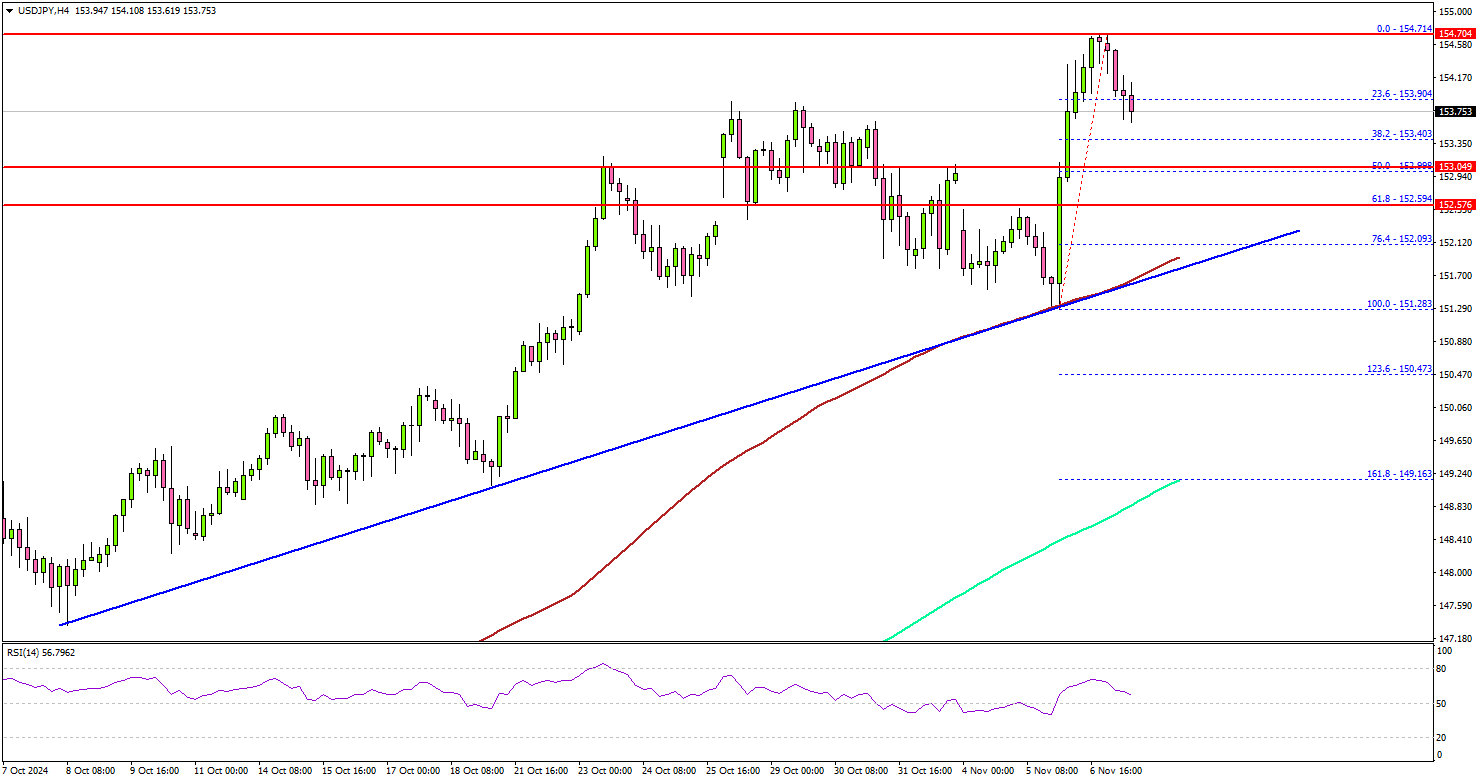

- USD/JPY started a fresh increase above the 153.50 resistance zone.

- A connecting bullish trend line is forming with support at 152.20 on the 4-hour chart.

- EUR/USD is attempting a recovery wave from the 1.0700 zone.

- Bitcoin rallied to a new record high above $76,000 before it saw a consolidation phase.

USD/JPY Technical Analysis

The US Dollar started a fresh increase above the 152.50 resistance zone against the Japanese Yen. USD/JPY cleared the 153.50 level to move into a positive zone.

Looking at the 4-hour chart, the pair settled well above the 153.00 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A high was formed at 154.71 before there was a downside correction.

The pair dipped below the 154.00 level. It broke the 23.6% Fib retracement level of the upward move from the 151.28 swing low to the 154.71 high.

On the downside, immediate support sits near the 152.60 level. The next key support sits near the 152.20 level. There is also a connecting bullish trend line forming with support at 152.20 on the same chart.

Any more losses could send the pair toward the 151.50 level. On the upside, the pair could face resistance near the 154.50 level. The first key resistance is near the 155.00 level.

A close above the 155.00 level could set the tone for another increase. The next major resistance could be 151.20, above which the price could accelerate higher toward the 152.00 resistance.

Looking at EUR/USD, the pair started a recovery wave and the bulls now aim for a move above the 1.0820 resistance.

Upcoming Economic Events:

- Canada’s employment Change payrolls for Oct 2024 – Forecast 25K, versus 46.7K previous.

- Canada’s Unemployment Rate for Oct 2024 - Forecast 6.6%, versus 6.5% previous.

US 10-yr yield retreats after Fed holds rates steady; Powell highlights fiscal risks

US 10-year Treasury yield eased back notably overnight following Fed's decision to keep interest rates steady. Chair Jerome Powell's balanced commentary offered a calm counterpoint to the election-fueled rally in yields seen earlier this week.

During the press conference, Powell downplayed the immediate impact of the election on monetary policy, stating that it "will have no effect on our policy decisions" in the near term. He emphasized that Fed's current policy stance is "well positioned" to manage risks and uncertainties, and that the central bank can adjust its policy restraints "more slowly" or "more quickly" depending on how economic developments unfold.

Addressing recent inflation data, Powell noted that it "wasn't terrible," but was "a little higher than expected." He highlighted that by December, the FOMC will have additional data to consider, including one more employment report and two more inflation reports. "We’ll make a decision as we get to December," Powell said.

However, he issued a stark warning about the US fiscal situation, asserting that fiscal policy is "on an unsustainable path." Powell elaborated: “The federal government’s fiscal path, fiscal policy, is on an unsustainable path. The level of our debt relative to the economy is not unsustainable, the path is unsustainable." He added, “We see that in a very large deficit, you’re at full employment that’s expected to continue, so it’s important that be dealt with. It is ultimately a threat to the economy.”

More on FOMC:

- Fed Review: In a Good Place After All

- Fed Continues To Dial Back Policy Restraint via 25 bps Rate Cut

- FOMC Focused on Health of Labour Market and Success with Inflation

Technically, 10-year yield has encountered notable resistance from medium term falling trend line and 61.8% retracement of 4.997 to 3.603 at 4.464. Some consolidations would be seen first, but such consolidations should be relatively brief as long as 4.223 support holds. Rise from 3.603 is expected to resume sooner rather than later. Sustained trading above 4.464 will pave the way to retest 4.997 high. Nevertheless, break of 4.223 will argue that deeper correction is underway back to 55 D EMA (now at 4.075).