Sample Category Title

Dollar Index Outlook: Dollar Eases from New Multi-Month High in Likely Positioning for Fed Rate Decision

The Dollar Index eases from new four-month high (105.33) posted on Wednesday’s sharp rally (the biggest daily gain in two years) on news of Trump’s election victory.

Partial profit-taking pushed the price lower, but the dollar keeps firm tone (daily studies remain in full bullish setup) suggesting that current dip is just positioning for fresh push higher.

Fed ends its two-day meeting and will announce its rate decision later today, with new situation on monetary policy outlook developing after Donald Trump won the US 2024 presidential election.

Trump’s campaign promises to focus on economy would boost economic growth and subsequently fuel inflation which will need recalibration of Fed’s current rate view.

Market expectations are shifting towards less rate cuts in the near future and earlier than expected end of Fed policy easing cycle, which would add support to the currency.

Solid supports at 104.50/30 (former top/daily Tenkan-sen) should contain dips and keep larger bulls intact for fresh acceleration higher and possible attack at 105.87 (June 28 peak).

Res: 105.33; 105.87; 106.00; 106.36.

Sup: 104.50; 104.30; 103.79; 103.64.

GBP/USD Outlook: Bears Take a Breather After Post-Election Fall

Cable edges higher following Wednesday’s post-US election 1.1% drop, generating an initial signal of recovery, after bears repeatedly experienced strong downside rejection.

Double failure to register clear break of Fibo support at 1.2846 (76.4% of 1.2664/1.3434) points to formation of a double-bottom pattern (1.2843/34) as nearby 200DMA (1.2813) also produced headwinds to bears.

However, more work at the upside is still required to verify recovery signals, with primary target at 1.2940 (dally Tenkan-sen) and more significant psychological 1.30 barrier and the base of thick daily cloud (1.2949) where extended upticks would be capped.

Bearishly aligned daily technical studies (negative momentum/price action weighed by thick daily cloud) favor scenario of limited correction /prolonged consolidation, before larger bears resume.

On the other hand, fundamentals are likely to play a key role today as Bank of England will deliver its rate decision.

A 25 basis points cut to 4.75% is widely expected, with focus BoE’s narrative being a key. Hawkish cut to probably inflate Pound, although stronger rally is still seen as limited, as pressure from stronger dollar on new US political outlook is likely to persist.

Firm break of 1.2843/34 double-bottom (reinforced by 200WMA) and 1.2813 (200DMA) to generate signal of bearish continuation.

Res: 1.2940; 1.2979; 1.3000; 1.3049.

Sup: 1.2872; 1.2834; 1.2813; 1.2765.

Japanese Yen Stabilizes After Post-Election Slide

The Japanese yen has steadied on Thursday after plunging 2% a day earlier. In the European session, USD/JPY is trading at 154.00, down 0.40% on the day.

The dust hasn’t settled from the US election, as a red Republican wave swept across the country. Republican Donald Trump retook the presidency in convincing fashion, easily defeating Democrat Kamala Harris. The Republicans have gained control of the Senate and the House of Representatives race is too close to call.

The US presidential race was a dead heat going into the election and the financial markets were bracing for an unclear outcome and a period of political instability. Trump’s resounding victory sent the US dollar and US equity markets soaring on Wednesday.

Will Trump make good on his tariff threats?

Trump has threatened to slap trade tariffs on China and Europe, which could boost inflation and slow the pace of the Federal Reserve’s interest rate cuts, which would be positive factors for the US dollar. There is understandable concern in China and Europe that Trump’s policies could lead to confrontation with the US, but trade wars would also hurt the US economy and it remains to be seen if Trump’s bark is worse than his bite.

Japan reported that wage growth jumped 2.6% y/y in September, up from 2.4% in August. This was the highest level in over 31 years and supports the case for the Bank of Japan to raise interest rates in the coming months. The BoJ wants to see higher wages which will boost spending and demand and push inflation higher. As wages move higher, expectations are rising that the BoJ will hike rates, possibly in January 2025.

The BoJ won’t be happy about the yen’s 2% slide after Trump’s election win and if the yen continues to fall it would raise pressure on the BoJ to raise rates at the December meeting or intervene in the currency markets to provide some relief for the yen.

USD/JPY Technical

- USD/JPY faces resistance at 155.78 and 156.95

- 153.54 and 152.37 are the next support levels

Eurozone retail sales rises 0.5% mom, mixed sectoral performance

Eurozone retail sales rose by 0.5% mom in September, slightly above the expected 0.4% mom increase. Breaking down the numbers, the volume of retail trade showed a mixed sectoral performance. Sales for non-food products, excluding automotive fuel, saw a notable rise of 1.1% mom, while sales for food, drinks, and tobacco slipped by -0.4% mom. Automotive fuel sales in specialized stores edged up by 0.2% mom.

Across the broader EU, retail sales rose by 0.3% mom. Among member states with available data, Belgium, Denmark, and Croatia recorded the highest increases, each posting a robust 2.1% mom rise in retail trade volume. Germany followed with a 1.2% mom gain. In contrast, Slovenia experienced the sharpest drop at -2.6% mom, followed by Poland at -2.0% mom and Finland at -1.6% mom.

USDJPY Hits 14-Week High Amid US Election Dynamics

The USDJPY pair has surged to a 14-week peak, touching 153.83 as demand for the US dollar strengthens with the unfolding US presidential election. This rally aligns with increasing support for Donald Trump, whose lead in critical states has fuelled investor optimism.

This week, US political developments are poised to dominate market attention, with the outcome still pending in several swing states.

In Japan, the recent Bank of Japan (BoJ) meeting minutes indicate a consensus among board members to persist with interest rate hikes, aligning with their inflation and economic objectives. Despite this, there is no immediate expectation for a rate increase until at least January 2025, reflecting the prevailing global economic uncertainties and market volatility.

Currently, the Japanese yen is not favoured as a safe-haven asset, with the market focus sharply pivoting towards the US dollar.

Technical analysis of USDJPY

The USDJPY pair has completed a corrective phase to 151.28 and initiated the fifth wave of growth towards 155.38. A consolidation phase around 153.33 suggests the potential for an upward breakout, continuing the ascent towards 155.38. This bullish scenario is supported by the MACD indicator, which shows a solid upward momentum from below the zero level.

Following a full correction to 151.28, the pair found strong support and advanced to 153.33. The market is now consolidating at this level, and a continuation of the upward trend to 155.38 is anticipated. This view is corroborated by the Stochastic oscillator, positioned near 80, indicating sustained upward pressure.

Gold Price Takes Hit While WTI Crude Oil Eyes Upsides

Gold price is declining below the $2,700 support zone. Crude oil price is rising and it could climb further higher toward the $75.00 resistance.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price failed to clear the $2,800 resistance and corrected lower against the US Dollar.

- There is a key bearish trend line forming with resistance at $2,725 on the hourly chart of gold at FXOpen.

- WTI Crude oil prices are moving higher above the $70.00 resistance zone.

- There is a key bullish trend line forming with support near $70.90 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price was able to climb above the $2,750 resistance. The price even broke the $2,765 level before the bears appeared.

The price traded toward $2,785 before there was a fresh decline. There was a move below the $2,760 pivot zone. The price settled below the 50-hour simple moving average and RSI dipped below 30. Finally, it tested the $2,645 zone.

The price is now consolidating losses near the $2,660 level. Immediate resistance on the upside is near the $2,668 level or the 23.6% Fib retracement level of the downward move from the $2,749 swing high to the $2,643 low.

The next major resistance is near the 50-hour simple moving average and the 61.8% Fib retracement level of the downward move from the $2,749 swing high to the $2,643 low at $2,708.

There is also a key bearish trend line forming with resistance at $2,725. An upside break above the $2,725 resistance could send Gold price toward $2,760. Any more gains may perhaps set the pace for an increase toward the $2,780 level.

If there is no recovery wave, the price could continue to move down. Initial support on the downside is near the $2,645 level. The first major support is $2,635. If there is a downside break below the $2,635 support, the price might decline further. In the stated case, the price might drop toward the $2,620 support.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a decent increase against the US Dollar. The price gained bullish momentum after it broke the $69.40 resistance.

There was a sustained upward move above the $70.00 and $70.90 levels. The bulls pushed the price above the 50-hour simple moving average and the RSI climbed toward 70. A high was formed near $72.31 before there was a downside correction.

The price declined below the 23.6% Fib retracement level of the upward move from the $69.43 swing low to the $72.31 high. However, the bulls are active above the 50-hour simple moving average.

There is also a key bullish trend line forming with support near $70.90. Immediate resistance is near the $72.30 level. If the price climbs further higher, it could face resistance near $73.50. The next major resistance is near the $74.20 level. Any more gains might send the price toward the $75.00 level.

Conversely, the price might correct gains and retest the 50-hour simple moving average or the 50% Fib retracement level of the upward move from the $69.43 swing low to the $72.31 high at $70.90.

The next major support on the WTI crude oil chart is near $70.10. If there is a downside break, the price might decline toward $68.75. Any more losses may perhaps open the doors for a move toward the $66.85 support zone.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

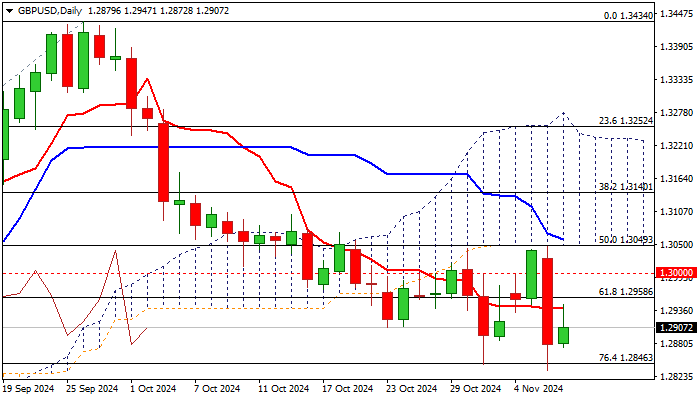

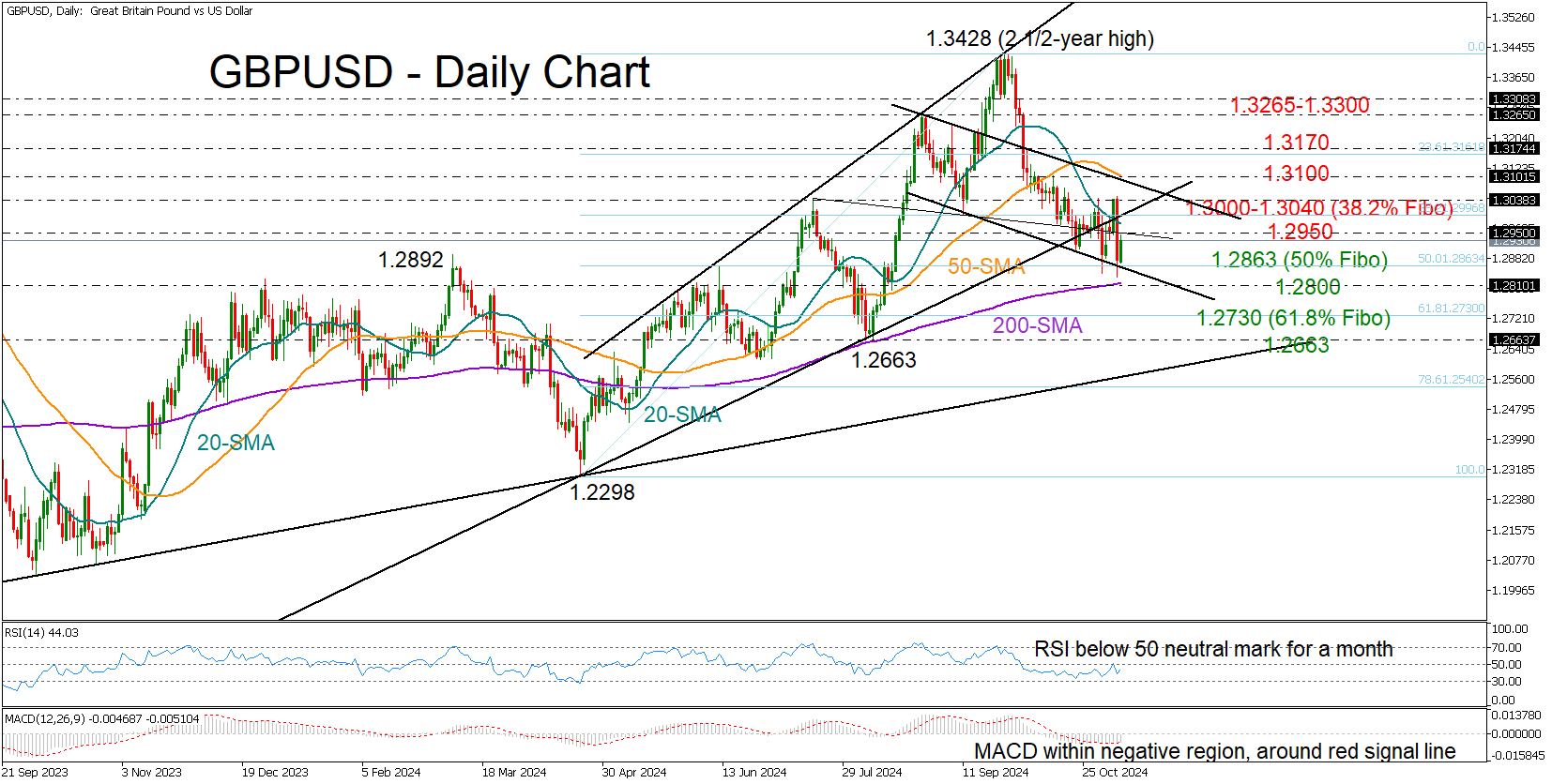

GBPUSD in the Red for Six Weeks

- GBPUSD hits a new two-month low as Trump wins White House

- Short-term outlook remains bearish; focus on 200-SMA for potential support

- Bank of England, Fed announce their rate decisions today

GBPUSD took a sharp dive to a two-month low of 1.2833 on Tuesday as the return of Trumponomics gave fresh impetus to the greenback.

On Wednesday, the 50% Fibonacci retracement level of the April-September rally came to support the market ahead of the BoE and Fed rate decisions, but with the price failing to hold above the ascending trendline from September 2022 and struggling to push past 1.3000 in recent days, downside risks remain in play.

That said, the 200-day simple moving average (SMA), which triggered the rally to a 2½-year high of 1.3428 in August, is at a short distance near 1.2800. This could act as a potential rebound point if the bulls can manage a reversal. Plus, with the RSI and MACD staying in bearish territory for over a month, some traders might feel that the recent downfall has been overdone.

For the bulls to gain some power, they will initially need to clear the 1.2950 zone and then take out the 1.3000-1.3040 range. If that happens, the 50-day SMA near 1.3100 could be the next hurdle. Breaking above 1.3100 would violate the current bearish trend and set up a move toward 1.3265, unless resistance around 1.3170 holds things back.

On the flip side, if the price falls below the 1.2800 area, support could come in around the 61.8% Fibonacci level of 1.2730, or near the August low at 1.2663. A deeper decline could stabilize around 1.2565.

To sum up, GBPUSD remains in a bearish trend in the short-term picture, with the 200-day SMA at 1.2800 marking a key level to watch. For a potential shift to the upside, the pair needs to push past 1.3100 and hold above it. Otherwise, further downside could be in the cards.

After Outsized Politically-Driven Repositioning, Markets Return to Normal Dynamics

Markets

The Republican hattrick trigged the most pure version of the America First trade. US equities, yields and the dollar all jumped sharply higher, betting on a strong, domestic-driven outperformance of the US economy. The Dow (+3.57%), S&P 500 (+2.53%) and the Nasdaq (2.95%) all touched record highs. The outperformance of the Russel 2000 (domestic-oriented small caps +5.84%) was telling. The US yield curve staged an impressive bear steepening move, with yields rising between 8.5 bps (2-y) and 17.6 bps (30-y). A highly stimulative fiscal policy will not only support growth, but also inflation and fiscal deficits. In such a scenario, there is little reason for the Fed to take aggressive action to prevent an unwarranted slowdown in growth and/or the labour market. Markets eased expectations for Fed easing toward the end of next year to 1%, including the expected 25 bps rate cut today. The rise in LT yields also suggests higher fiscal and inflation risk premia , but that’s not what investors currently are focused on. Similar story for the dollar. The greenback jumped sharply against all majors. DXY closed above the 105 handle for the first time since July. USD/JPY jumped to close at 154.6. Japan’s chief currency official Atsushi Mimura this morning already warned that he will closely monitor what he sees as a one-sided move. EUR/USD nosedived from the 1.0930 area to close at 1.0729 as USD strength met euro weakness as markets ponder the potential negative impact from trade tariffs on the EMU economy. Striking in this respect, the euro/German yield curves also steepened, but in a bull fashion. The Germany 2-y yield dropped 12.7 bps. The 30-y added 4.1 bps. Markets apparently concluded that the ECB will have to provide additional support to keep the EMU economy afloat. Given the uncertain outlook on inflation, potentially higher risk premia globally and a weak euro, we consider it too early to draw any conclusions on this topic. In this respect, a new German government also might take a more pragmatic approach on fiscal orthodoxy (cf infra).

After yesterday’s outsized politically-driven repositioning, markets gradually have to return to more normal dynamics, admittedly in a new context. It’s probably too early for eco data (US productivity data, jobless claims) to already pick-up their role, but a Fed-policy decision and press conference from Fed chair Powel deserves attention as a new era emerges. Fed gradualism will most likely result in scaling back the pace of rate cuts from 50 bps to 25 bps. Powell will stick to a data-dependent approach with the Fed taking into consideration all new info. The December forecast/dots will be an important next reference. For now, we don’t fight the rise in US yields, especially not at the long end of the curve. In the 10-y yield, the YTD top (4.735) is the next key reference on the charts. For EUR/USD, a sell-on -upticks approach is favoured for return action to the 1.0601 YTD low. Also keep a close eye at the BOE meeting (25 bps cut expected) with new forecasts. These (better growth, more fiscal stimulus) probably won’t really support governor Bailey’s call for a more activist approach. Yesterday’s Gilts’ underperformance against Bunds was telling. A break of EUR/GBP below 0.83 opens the way to the 0.8250/0.8202 2022 low.

News & Views

The Brazilian central bank accelerated the pace of rate hikes after restarting a hiking cycle in September. They raised their key rate by 50 bps to 11.25%. The monetary policy committee judges that inflation risks are tilted to the upside, coming from a more prolonged period of deanchoring of inflation expectations, stronger-than-expected resilience of services inflation due to a tighter output gap and a weaker than expected FX rate (amongst others via loose fiscal policy stance and higher risk premia). In the meantime, the domestic economy and labor market continue to exhibit strength. Internationally, uncertainty remains on the pace of US economic deceleration, disinflation and consequently the Fed’s policy stance. The pace of future adjustments of the interest rate and the total magnitude of the tightening cycle will be determined by the firm commitment of reaching the 3% inflation target. The Brazilian real overcame USD strength with USD/BRL falling from near all-time highs above 5.80 to currently 5.67.

Germany is heading for snap elections in March of next year after Chancellor Scholz dismissed his finance minister Lindner and called for a January 15 confidence vote in his government which he’ll likely lose. The ruling coalition partners (SPD, Greens and FDP) couldn’t agree on how to plug a €9bn funding hole. Liberal FDP FM Lindner wouldn’t touch on the country’s debt brake to allow a looser fiscal policy stance both to help the ailing domestic economy and to provide more aid to Ukraine. Polls currently put the opposition CDU in the lead.

Elliott Wave View: S&P 500 Futures ($ES) Wave 5 In Progress

Short Term Elliott Wave View in S&P 500 Futures (ES) suggests rally from 8.6.2024 low is in progress as an impulse. Up from 8.6.2024 low, wave 1 ended at 5669.75 and pullback in wave 2 ended at 5394. Wave 3 higher ended at 5927.25. Dips in wave 4 unfolded as a double three Elliott Wave structure. Down from wave 3, wave (a) ended at 5861.25 and wave (b) ended at 5904.25. Wave (c) lower ended at 5801 which completed wave ((w)) in higher degree. Rally in wave ((x)) unfolded as a zigzag structure. Up from wave ((w)), wave (a) ended at 5870 and wave (b) ended at 5822.5. Wave (c) higher ended at 900.75 which completed wave ((x)) in higher degree.

Index then turned lower in wave ((y)) with internal subdivision as a zigzag. Down from wave ((x)), wave (a) ended at 5835 and wave (b) ended at 5893. Wave (c) lower ended at 5724.5. This completed wave ((y)) of 4 in higher degree. The Index has resumed the rally higher and made a new high. Up from wave 4, wave (i) ended at 5758.75 and wave (ii) ended at 5735. Wave (iii) higher ended at 5954 and wave (iv) ended at 5900.75. Expect the Index to end wave (v) of ((i)) soon, then it should pullback in wave ((ii)) to correct cycle from 11.5.2024 low before it resumes higher. Near term, while pivot at 5724.5 low is intact, expect pullback to find buyers in 3, 7, 11 swing for further upside.

S&P 500 Futures (ES) 60 Minutes Elliott Wave Chart

ES_F Elliott Wave Video

https://www.youtube.com/watch?v=zzIrvVNkGAU

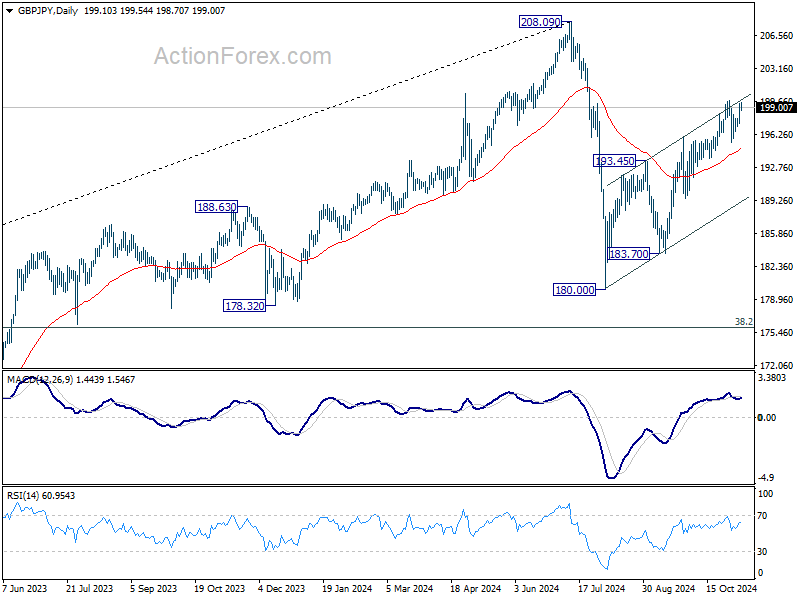

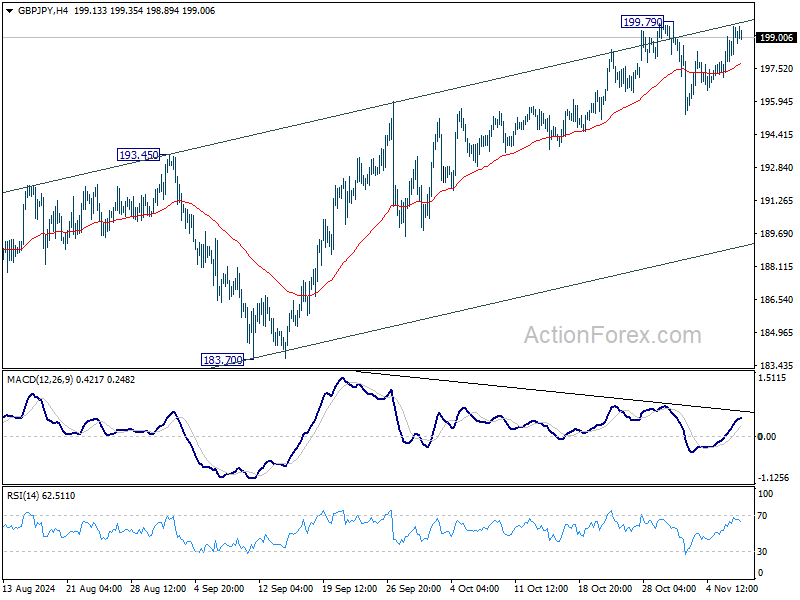

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.79; (P) 198.66; (R1) 200.02; More...

Intraday bias in GBP/JPY remains neutral as consolidation from 199.79 could extend. Further rally is expected as long as 55 D EMA (now at 194.80) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.