Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0890; (P) 1.0913; (R1) 1.0954; More...

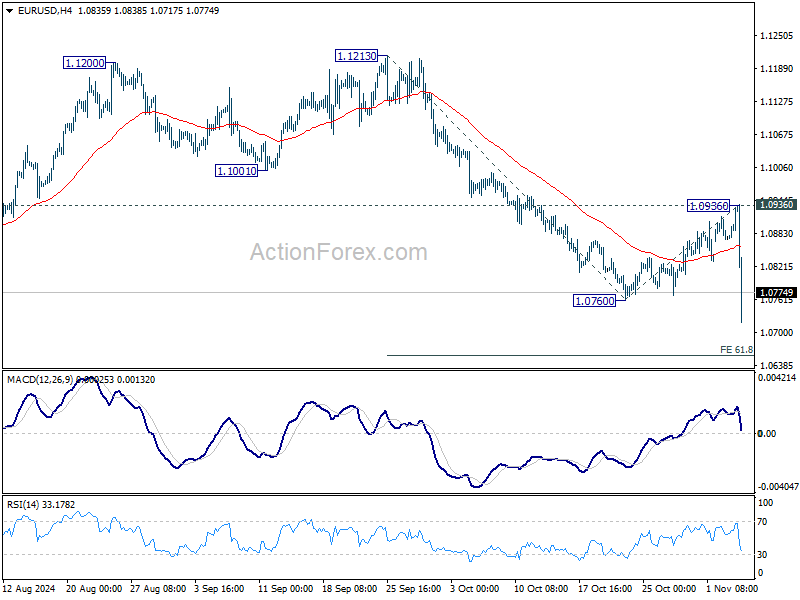

EUR/USD's breach of 1.0760 indicates that corrective recovery from there has completed after rejection by 55 D EMA (now at 1.0939), and fall from 1.1213 is resuming. Intraday bias is back on the downside for 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656. Firm break there will pave the way to 100% projection at 1.0483. For now, near term outlook will stay bearish as long as 1.0936 resistance holds, in case of recovery.

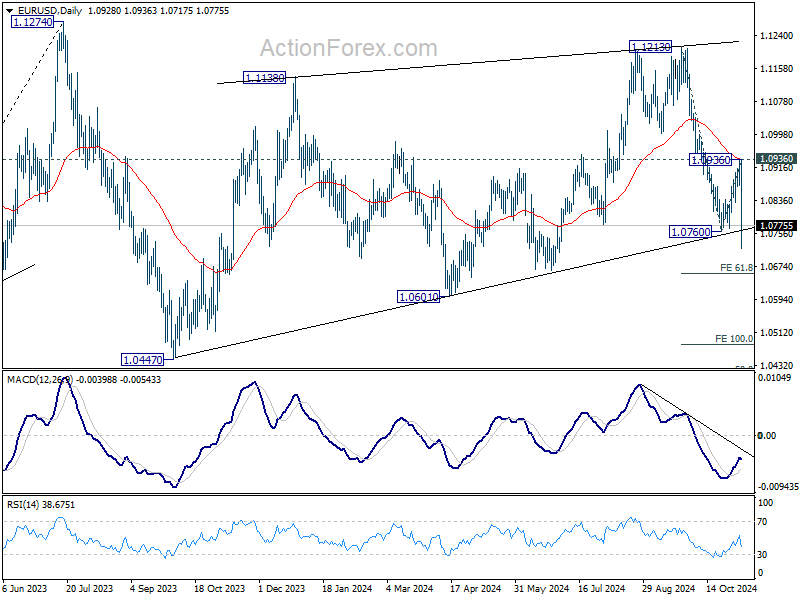

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

Trump’s North Carolina Victory Boosts Dollar and Yields, Bitcoin Hits New High

Dollar rallied sharply today after news broke that Republican candidate Donald Trump defeated Democrat Kamala Harris in North Carolina, a crucial battleground state. This win is considered a pivotal move toward Trump’s return to office, sparking significant moves across financial markets. US stock futures responded with enthusiasm, with DOW futures climbing over 500 points. Meanwhile, 10-year Treasury yield surged above 4.4%, reinforcing the sentiment around Trump’s impact on fiscal policy. Despite this initial surge, traders remain on edge, waiting for further confirmation from key states before taking on new positions.

Asian stock markets offered a mixed picture in response to the news. Japan's Nikkei soared over 2%, driven by positive sentiment linked to a possible Trump victory, as markets see his economic policies as supportive of growth and deregulation. On the other hand, Hong Kong stocks suffered, dropping by more than -2.5% amid concerns over Trump's stance on China, which could bring intensified tensions. In contrast, markets in China and Singapore traded in a narrow range, reflecting uncertainty and caution.

In currency markets, the Australian Dollar is currently the weakest performer, followed by Euro and Yen, pressured by Dollar’s strength. Meanwhile, Canadian Dollar joins Dollar as one of the stronger performers, with Swiss Franc also displaying resilience. New Zealand’s Kiwi is holding steady, seemingly unaffected by recent Q3 employment data, trading alongside the British Pound in mid-range.

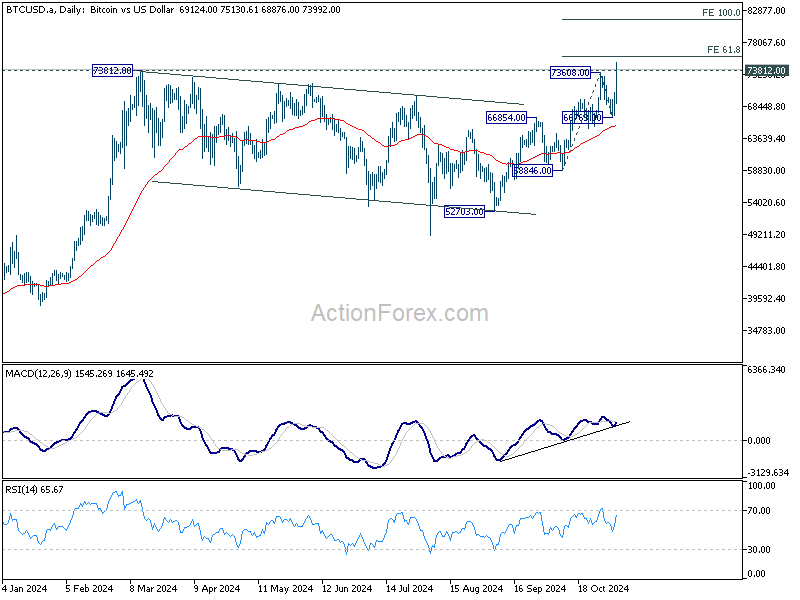

Technically, Bitcoin hits new record high by breaking through 73812 resistance today. Immediate focus is now on 61.8% projection of 58846 to 73608 from 66763 at 75885. Decisive break there could prompt upside acceleration to 100% projection at 81525 rather quickly.

In Asia, at the time of writing, Nikkei is up 2.24%. Hong Kong HSI is down -2.61%. China Shanghai SSE is up 0.16%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield is up 0.0421 at 0.971. Overnight, DOW rose 1.02%. S&P 500 rose 1.23% .NASDAQ rose 1.43%. 10-year yield fell -0.020 to 4.289.

BoC minutes reveals strong consensus for aggressive rate cut

Summary of BoC Governing Council’s October 23 meeting highlights a decisive stance among members to prioritize growth through an aggressive 50bps rate cut. While members initially discussed the possibility of a modest 25bps cut, a "strong consensus" emerged in favor of a larger reduction to counter economic headwinds.

The Governing Council members expressed "increasingly confident" that inflationary pressures are expected to ease, reducing the need for a restrictive policy stance. Some members voiced concern that an unusual 50bps cut might be perceived as a signal of “economic trouble.” Despite this, they agreed that a more substantial cut was justified, given the "ongoing softness" in the labor market and the need to bolster growth to "absorb excess supply" in the economy.

BoJ minutes: Yen stabilization gives time to monitor global economic risks

Minutes from BoJ's September meeting reveal a careful stance on monetary policy amid global economic uncertainties. At the meeting, BoJ kept its interest rate steady at 0.25%.

Regarding future direction of monetary policy, members broadly agreed that if Japan's economic and inflation outlook aligns with their projections, the Bank would "continue to raise the policy interest rate" and gradually adjust its level of monetary accommodation.

The minutes also underscore the need for "high vigilance" given uncertainties in overseas economies, particularly in the US, and ongoing volatility in global financial markets.

Some members pointed out that recent retracements in Yen’s depreciation have moderated upside risk to inflation from import prices. Given this development, they noted that the Bank has "enough time" to evaluate the effects of global economic shifts and recent policy rate hikes before deciding on further moves.

Japan's PMI services finalized at 49.7, first contraction since Jun

Japan's services sector slipped into contraction in October, with PMI Services index finalized at 49.7, down from September’s 53.1 and marking its first contraction since June. PMI Composite also declined to 49.6 from 52.0, signaling a contraction in private sector activity for the first time in four months and the lowest reading since November 2023.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the services sector’s performance “came to an abrupt halt” at the start of Q4. While the decline was modest, it was driven by a notable slowdown in new business inflows, particularly in export orders. Despite the dip, businesses maintained a positive outlook, though optimism weakened to its lowest in over two-and-a-half years, with companies citing concerns over labor shortages as a key factor.

The services sector slowdown, combined with a continuing contraction in manufacturing, contributed to the steepest private sector contraction in nearly a year. New order inflows stagnated, particularly impacted by weakened demand in manufacturing order books. Business sentiment, overall, has also softened, with optimism now at its lowest since January 2021.

NZ employment falls -0.5% in Q3, unemployment rate rises to 4.8%

New Zealand’s labor market showed signs of cooling in Q3, with employment falling by -0.5% qoq, in line with expectations. Unemployment rate rose from 4.6 to 4.8%, slightly better than the anticipated 5.0%, but still indicative of softening labor conditions.

Labor force participation rate also declined, dropping from 71.7% to 71.2%, while the employment rate slipped from 68.4% to 67.8%, reflecting fewer people actively engaged in the workforce.

On the wage front, growth showed deceleration. The labor cost index, which includes salary and wage rates with overtime, rose by 3.8% yoy, down from the previous quarter’s 4.3% yoy increase.

The slowdown in wage growth suggests some relief in wage-driven inflation pressures, which could factor into RBNZ's upcoming rate cut.

Looking ahead

Germany factory orders, Eurozone PMI services final and PPI, UK PMI construction will be released in European session. Later in the day, Canada will release Ivey PMI.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0890; (P) 1.0913; (R1) 1.0954; More...

EUR/USD's breach of 1.0760 indicates that corrective recovery from there has completed after rejection by 55 D EMA (now at 1.0939), and fall from 1.1213 is resuming. Intraday bias is back on the downside for 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656. Firm break there will pave the way to 100% projection at 1.0483. For now, near term outlook will stay bearish as long as 1.0936 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

GBP/USD Recovery Potential: Can The Pound Rebound?

Key Highlights

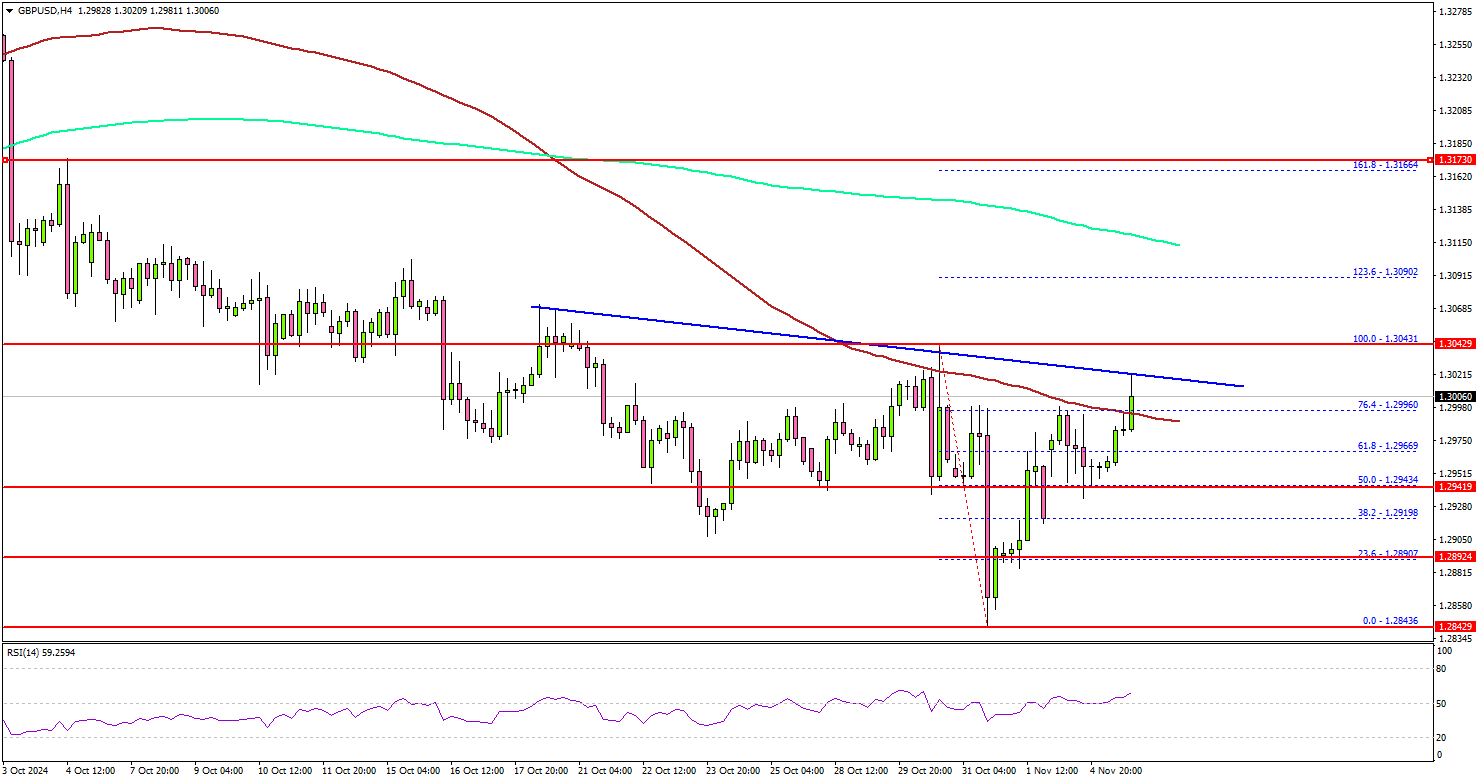

- GBP/USD is attempting to recover from the 1.2840 support zone.

- A connecting bearish trend line is forming with resistance at 1.3020 on the 4-hour chart.

- EUR/USD could gain bullish pace if it clears the 1.0920 resistance.

- Bitcoin bulls aim for a fresh move above the $70,000 resistance.

GBP/USD Technical Analysis

The British Pound started an upside correction from the 1.2840 zone against the US Dollar. GBP/USD climbed above the 1.2880 and 1.2950 resistance levels.

Looking at the 4-hour chart, the pair traded above the 50% Fib retracement level of the downward move from the 1.3043 swing high to the 1.2843 low. However, the pair struggled to settle above the 100 simple moving average (red, 4-hour) and remained well below the 200 simple moving average (green, 4-hour).

On the downside, immediate support sits near the 1.2940 level. The next key support sits near the 1.2890 level. Any more losses could send the pair toward the 1.2840 level.

On the upside, the pair could face resistance near the 1.3020 level. There is also a connecting bearish trend line forming with resistance at 1.3020 on the same chart. The first key resistance is near the 1.3050 level.

A close above the 1.3050 level could set the tone for another increase. The next major resistance could be 1.3120, above which the price could accelerate higher toward the 1.3200 resistance.

Looking at EUR/USD, the pair started a recovery wave and the bulls now aim for a move above the 1.0920 resistance.

Upcoming Economic Events:

- Euro Zone Services PMI for Oct 2024 – Forecast 51.2, versus 51.2 previous.

- UK Services PMI for Oct 2024 – Forecast 56.0, versus 57.2 previous.

BoJ minutes: Yen stabilization gives time to monitor global economic risks

Minutes from BoJ's September meeting reveal a careful stance on monetary policy amid global economic uncertainties. At the meeting, BoJ kept its interest rate steady at 0.25%.

Regarding future direction of monetary policy, members broadly agreed that if Japan's economic and inflation outlook aligns with their projections, the Bank would "continue to raise the policy interest rate" and gradually adjust its level of monetary accommodation.

The minutes also underscore the need for "high vigilance" given uncertainties in overseas economies, particularly in the US, and ongoing volatility in global financial markets.

Some members pointed out that recent retracements in Yen’s depreciation have moderated upside risk to inflation from import prices. Given this development, they noted that the Bank has "enough time" to evaluate the effects of global economic shifts and recent policy rate hikes before deciding on further moves.

Japan’s PMI services finalized at 49.7, first contraction since Jun

Japan's services sector slipped into contraction in October, with PMI Services index finalized at 49.7, down from September’s 53.1 and marking its first contraction since June. PMI Composite also declined to 49.6 from 52.0, signaling a contraction in private sector activity for the first time in four months and the lowest reading since November 2023.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the services sector’s performance “came to an abrupt halt” at the start of Q4. While the decline was modest, it was driven by a notable slowdown in new business inflows, particularly in export orders. Despite the dip, businesses maintained a positive outlook, though optimism weakened to its lowest in over two-and-a-half years, with companies citing concerns over labor shortages as a key factor.

The services sector slowdown, combined with a continuing contraction in manufacturing, contributed to the steepest private sector contraction in nearly a year. New order inflows stagnated, particularly impacted by weakened demand in manufacturing order books. Business sentiment, overall, has also softened, with optimism now at its lowest since January 2021.

NZ employment falls -0.5% in Q3, unemployment rate rises to 4.8%

New Zealand’s labor market showed signs of cooling in Q3, with employment falling by -0.5% qoq, in line with expectations. Unemployment rate rose from 4.6 to 4.8%, slightly better than the anticipated 5.0%, but still indicative of softening labor conditions.

Labor force participation rate also declined, dropping from 71.7% to 71.2%, while the employment rate slipped from 68.4% to 67.8%, reflecting fewer people actively engaged in the workforce.

On the wage front, growth showed deceleration. The labor cost index, which includes salary and wage rates with overtime, rose by 3.8% yoy, down from the previous quarter’s 4.3% yoy increase.

The slowdown in wage growth suggests some relief in wage-driven inflation pressures, which could factor into RBNZ's upcoming rate cut.

BoC minutes reveals strong consensus for aggressive rate cut

Summary of BoC Governing Council’s October 23 meeting highlights a decisive stance among members to prioritize growth through an aggressive 50bps rate cut. While members initially discussed the possibility of a modest 25bps cut, a "strong consensus" emerged in favor of a larger reduction to counter economic headwinds.

The Governing Council members expressed "increasingly confident" that inflationary pressures are expected to ease, reducing the need for a restrictive policy stance. Some members voiced concern that an unusual 50bps cut might be perceived as a signal of “economic trouble.” Despite this, they agreed that a more substantial cut was justified, given the "ongoing softness" in the labor market and the need to bolster growth to "absorb excess supply" in the economy.

NZ First Impressions: Labour Market Data, September Quarter 2024

The unemployment rate rose to 4.8% in the September quarter, a smaller than expected rise due to more young people exiting the labour force. Wage growth is moderating broadly as expected.

- Unemployment rate: 4.8% (prev: 4.6%, Westpac f/c: 5.0%, RBNZ f/c 5.0%)

- Employment change (quarterly): -0.5% (prev: +0.2%, Westpac f/c: -0.6%, RBNZ f/c -0.4%)

- Labour costs (private sector, quarterly): +0.6% (prev: +0.9%, Westpac f/c: +0.7%, RBNZ f/c +0.7%)

- Average hourly earnings (private sector, ordinary time quarterly): +1.1% (prev: +1.4%)

New Zealand’s labour market continues to soften, in line with the shallow drawn-out recession we have been experiencing over the last couple of years. The unemployment rate rose from 4.6% to 4.8% in the September quarter, the highest level since December 2020.

This was a smaller rise than we and the Reserve Bank had been expecting, with the miss being entirely due to a sharper than expected fall in the labour force participation rate. This reflects an ongoing unwind of the pressures that had built up in the labour market in previous years.

The number of people employed fell by 0.5%, roughly in line with what the Monthly Employment Indicator (MEI) had signalled. In fact, the various employment measures were unusually in agreement this time, with the Quarterly Employment Survey (QES) also showing a 0.3% fall in filled jobs and full-time equivalent employees.

While these job losses did lead to a rise in unemployment, there was also a large number of people who exited the labour force altogether. The participation rate fell from 71.7% to 71.2% in the September quarter, its lowest level in over two years – we had assumed a fall to 71.4% in our forecast.

The fall in participation appears to have been strongly concentrated among young people (15-24 years old). In the initial post-Covid period, the economy was running hot and the border closure meant that migrant workers weren’t available. In this time, many young people were drawn into the labour force to fill the gap – often at the expense of study. As the economy has slowed and migration has rebounded, this group has been at the forefront of job losses. While this has led to a rise in the number of unemployed, we’re also increasingly seeing young people return to or remain in study, ending their job search altogether. Indeed, the NEET ratio (young people not in employment, education or training) has actually fallen over the last few quarters.

Turning to wages, the Labour Cost Index (LCI) rose by 0.6% for the quarter, slightly lower than the 0.7% that we and the RBNZ expected. Public sector wages were up by 0.9%, boosted by a pay increase for police, but this didn’t have an impact on the overall results. The unadjusted analytical LCI (which doesn’t exclude pay increases that are related to productivity) rose by 0.9%, the smallest quarterly increase since March 2021.

So what does this mean for the RBNZ? We think not much – it simply highlights the degree of flex that there is in the labour force as economic conditions change. The bottom line is still that employers are shedding workers, and wage pressures are easing accordingly. That’s consistent with the view that inflation pressures are being reined in and that monetary policy no longer needs to be as restrictive. But we don’t think that there’s anything in today’s figures that would shift the RBNZ’s thinking for its next policy decision at the end of this month.

A BoE Rate Cut Expected But Overall Rhetoric Matters

- The BoE meeting concludes on Thursday

- Market expects a 25bps rate cut

- Rhetoric and voting pattern matter

- Pound could suffer from a dovish rate cut

BoE meets on Thursday

The Bank of England will hold its penultimate meeting for 2024 on Thursday, a few hours ahead of the Fed's gathering. With the market anxiously awaiting the outcome of the US presidential election, Governor Bailey et al will examine the progress made since the September meeting.

Mixed signals from the economy

Since the September meeting, economic data releases have been mixed. The headline inflation rate dropped below the 2% level, mostly due to favourable base effects, but core inflation remains north of 3%. Similarly, services inflation eased to 4.9% in September, the lowest rate since May 2022, but remains very elevated.

Meanwhile, unemployment is near record low levels and retail sales continue to strengthen. The retail sales indicator that excludes fuel spending rose by 4% in September, partly reflecting the strong average earnings growth during 2024, although the latter has shown signs of weakness lately.

The most alarming signal comes from the PMI surveys. Both the Manufacturing and Services surveys have been weakening, raising concerns about the short-term outlook of the UK economy.

Autumn budget impact

The Autumn Budget 2024, announced on October 30, was dominated by tax increases. The new government is planning to raise £40bn in extra tax revenue, and spend most of these funds on updating public services. While the independent Office for Budget Responsibility (OBR) published fabourable GDP forecasts, the actual impact on the UK economy remains uncertain, particularly due to the national insurance changes.

Interestingly, the quarterly projections will be released on Thursday. The BoE has already announced that any changes in fiscal policy resulting from the Budget will be incorporated in the November projections. Therefore, it will be interesting to see how the BoE evaluates the impact of these tax increases.

Bailey et al face a true challenge

Putting everything together, the MPC will need to balance domestic developments and a volatile external environment. The economy is probably losing steam as portrayed by the PMI surveys, with the UK budget announcement potentially muddling the economic outlook rather than proving beneficial.

The market is confident that a 25bps rate cut will be announced on Thursday. Despite repeated comments from certain BoE hawks for a gradual approach, it seems that Governor Bailey will achieve the necessary majority to get the rate cut approved.

Apart from the decision, the market’s focus will also be on the overall rhetoric of the meeting, including the press conference. At this stage, it makes sense for the BoE to remain balanced and avoid adopting a more dovish tone. Such a strategy could secure broader support for the rate cut and avoid a repeat of the 5-4 split vote at the July 31 gathering.

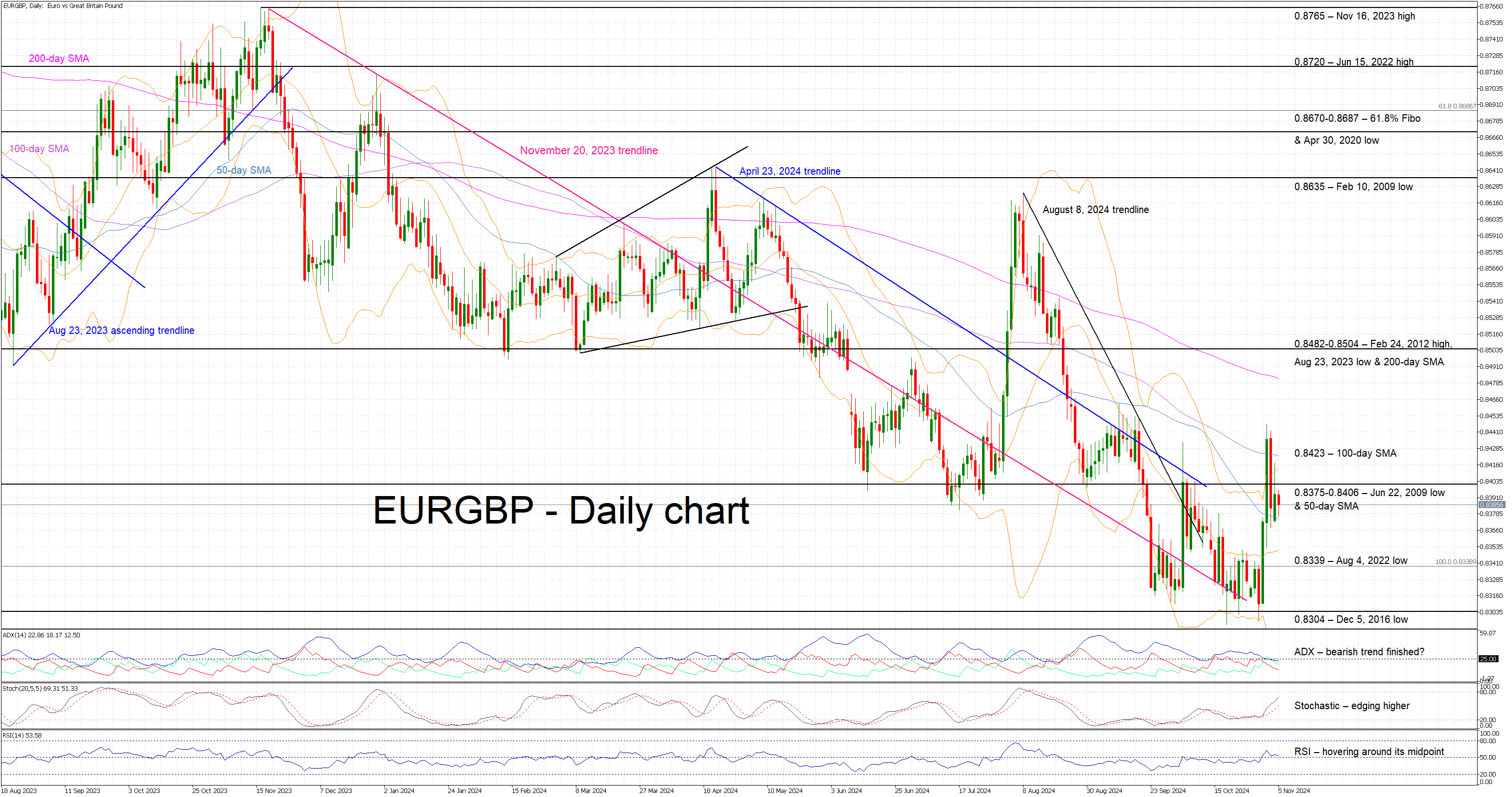

Pound could suffer against the euro

October was a relatively tough month for the pound, as the October 30 budget shocked pound bulls, leading to a sizeable underperformance against both the euro and the dollar.

While the euro is enjoying a brief spell of positive data prints, Thursday’s BoE meeting could reverse the recent euro/pound trend upleg. A rate cut accompanied by balanced rhetoric and a 5-4 split vote could further reduce the chances of back-to-back rate cuts in December, potentially boosting the pound.

On the flip side, a dovish rate cut with strong support could open the door to another rate cut in December. In this scenario, the pound could suffer, with euro/pound potentially climbing decisively above the 100-day simple moving average at 0.8423.

Trump or Harris? Why Nasdaq 100, S&P 500 Might Not Care Who Wins

- Wall Street Indexes rebounds on strong ISM Services PMI as election uncertainty lingers.

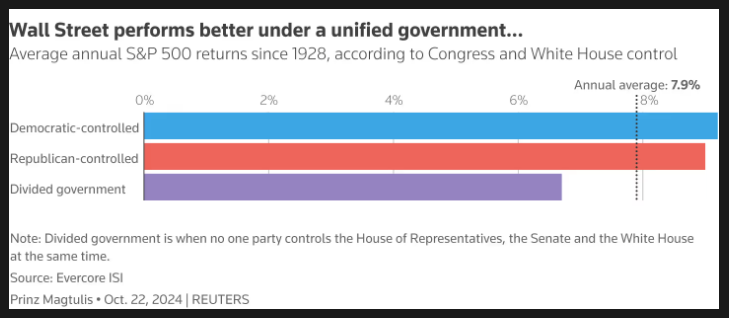

- Investors closely watch Congressional election results, as a unified government is seen as beneficial for stock market performance.

- Market volatility remains low as investors await election results and upcoming Federal Reserve and BoE decisions.

Wall Street Indexes rose in the early hours of the US session helped by a surprise US services activity print. Market participants continue to wait with bated breath on the outcome of the US Presidential election.

The ISM Services PMI in the US unexpectedly jumped to 56 in October 2024, the highest since August 2022, from 54.9 in September and beating forecasts of 53.8. The strong gain was mostly driven by a rebound in employment.

Concerns about political uncertainty grew compared to the previous month. Issues from hurricanes and labor problems at ports were often mentioned, but the impact of the longshoremen’s strike was less severe than expected because it was short-lived, according to Steve Miller, Chair of the ISM Services Business Survey Committee.

The ISM data gave Wall Street Indexes a boost with the S&P 500 seeing all 11 sectors in the green with Industrials .SPLRCI, Consumer Discretionary .SPLRCD and Information Technology .SPLRCT adding more than 1.3%.

On the earnings front, Palantir’s (PLTR.N) stock jumped 23% to a new high after the company increased its yearly revenue prediction for the third time. As the election has drawn closer Trump media continues its rally, with the group surging 14.4%. Big tech stocks also gained on the day, with Tesla increasing by 4% and Nvidia rising by 3.1%.

Trump or Harris: Congressional Elections Results also Key

As the election race heats up the latest polls are showing a tight race. There is growing attention to the congressional elections as well and this may be more important for market participants. The data suggests that US stocks perform better under a unified government as that would allow the President to make significant policy changes. A divided congress can at times be a hurdle for the incoming President especially with the opposing view on the economy and at times foreign policy.

Source: LSEG

Volatility has thus far been low this week as market participants weigh the various risks still ahead this week. After the elections we also have the Federal Reserve decision, the BoE and the University of Michigan sentiment preliminary numbers will be released on Friday.

Technical Analysis

Nasdaq 100

The Nasdaq 100 broke below the ascending channel but failed to push lower ahead of the election. Given the caution on display by market participants it is no surprise that US indexes have failed to push lower after last week’s selloff.

The Nasdaq has broken back above the lows of the ascending channel, however there is a chance that the US election could still be a shot in the arm for a deeper pullback.

Given the excellent US stock market performance this year, I think markets may be oblivious to whoever wins the election. Rather we could just get a spike in volatility and liquidity before markets continue their trend.

In the lead up to the election, many US voters were of the opinion that former President Trump is more pro free markets and better for the economy, however given the performance under the Biden administration markets might remain optimistic with a Harris victory. This makes the potential reaction by markets even more intriguing.

Either way, immediate resistance rests at 20484 and 20675 before the all-time highs around 20790 come into focus.

Conversely, a break below last week’s low at 19918 brings the possibility of a retest of the 100-day MA which rests at 19671. A break below this level will lead to a third touch of the ascending trendline which rests just below the 100-day MA.

Nasdaq 100 Daily Chart, November 5, 2024

Source: TradingView (click to enlarge)

Support

- 19918

- 19750

- 19536

Resistance

- 20484

- 20675 (all-time highs)

- 20790