Sample Category Title

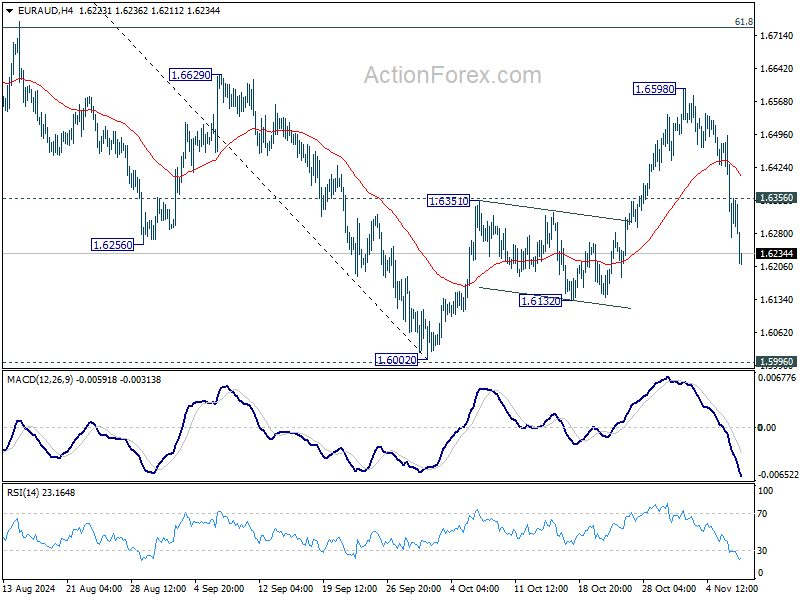

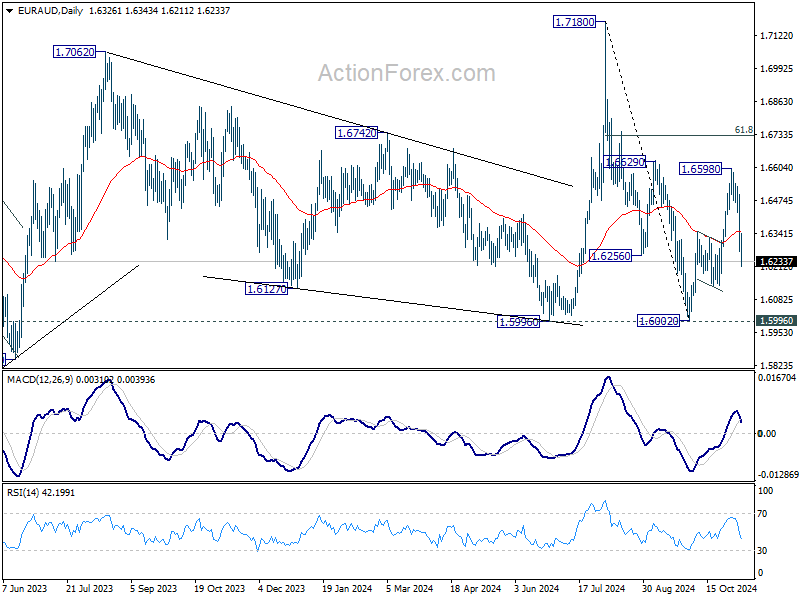

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6233; (P) 1.6366; (R1) 1.6458; More...

Intraday bias in EUR/AUD remains on the downside for 1.6132 support. Break there will extend the fall from 1.6598 to retest 1.5996 key support level. On the upside, above 1.6356 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.6598 resistance holds, in case of recovery.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

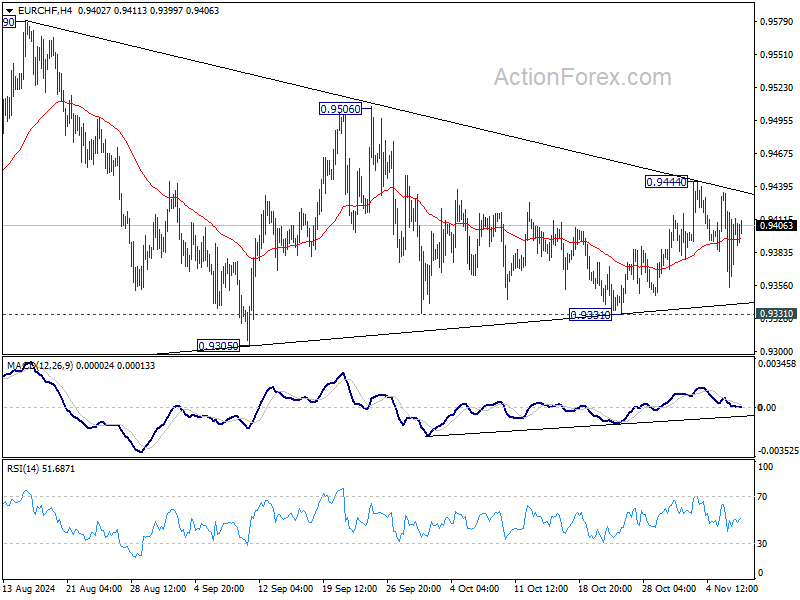

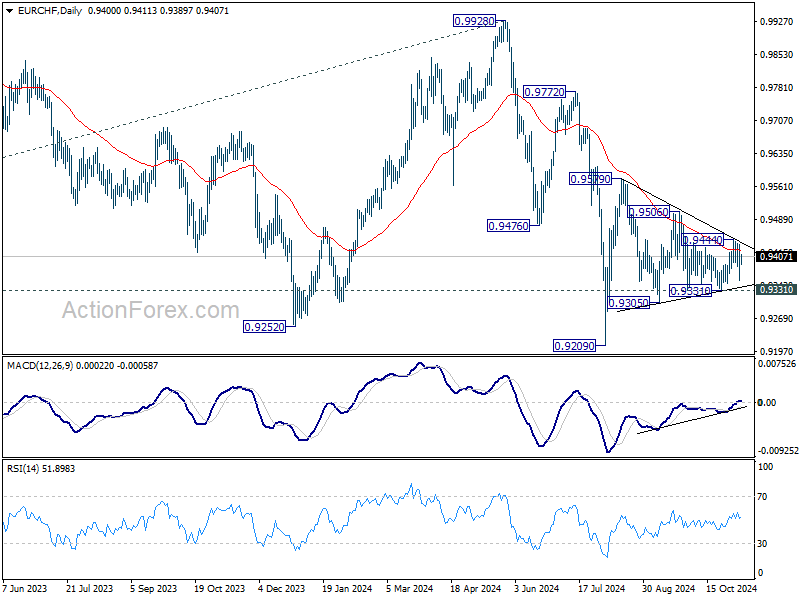

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9363; (P) 0.9400; (R1) 0.9443; More....

EUR/CHF is still bounded in converging triangle for now, and intraday bias remains neutral. On the downside, break of 0.9331 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9444 will turn intraday bias to the upside for 0.9506 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9421) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming at 0.9209 and bring stronger rebound back towards 0.9928 key resistance.

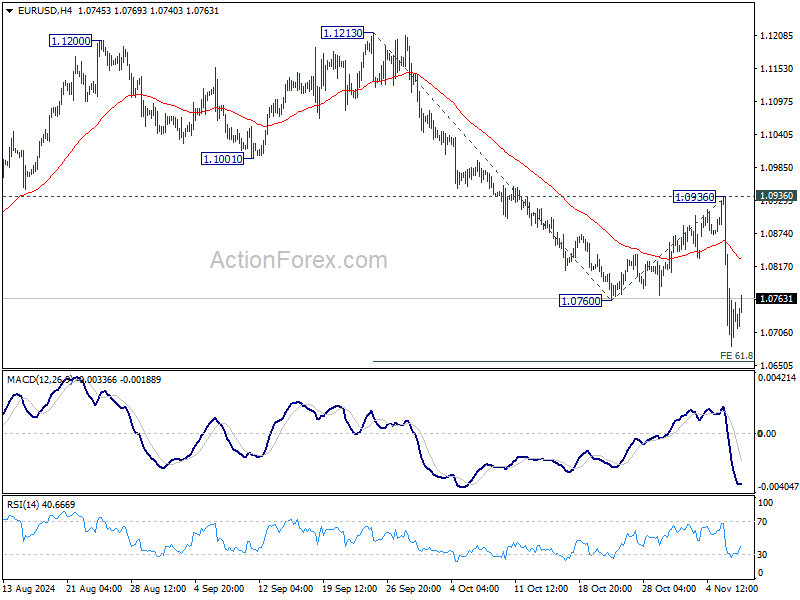

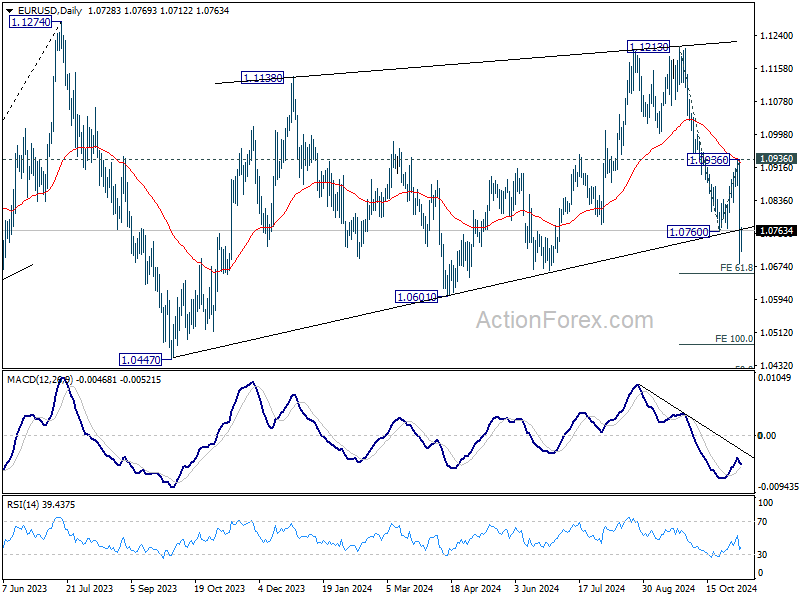

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0628; (P) 1.0783; (R1) 1.0885; More...

Intraday bias in EUR/USD remains on the downside as fall from 1.1213 is in progress. Next target is 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656. Firm break there will pave the way to 100% projection at 1.0483. For now, near term outlook will stay bearish as long as 1.0936 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

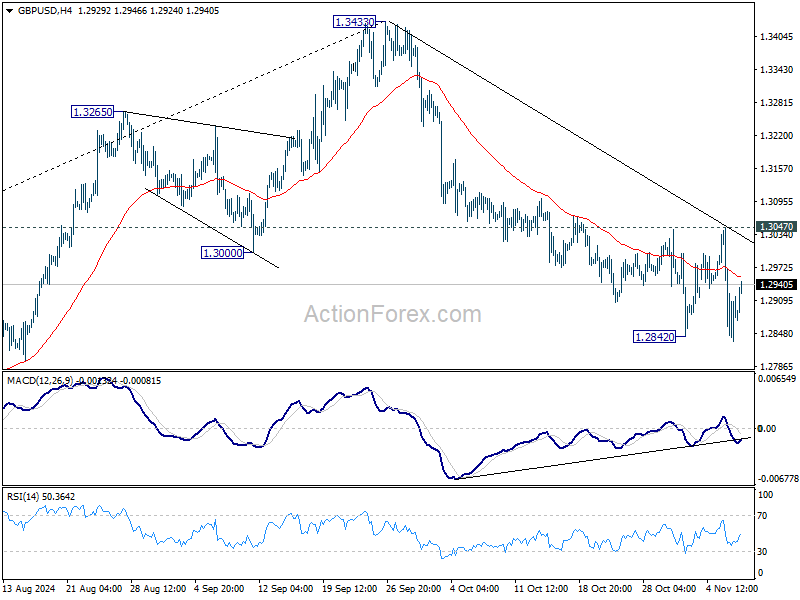

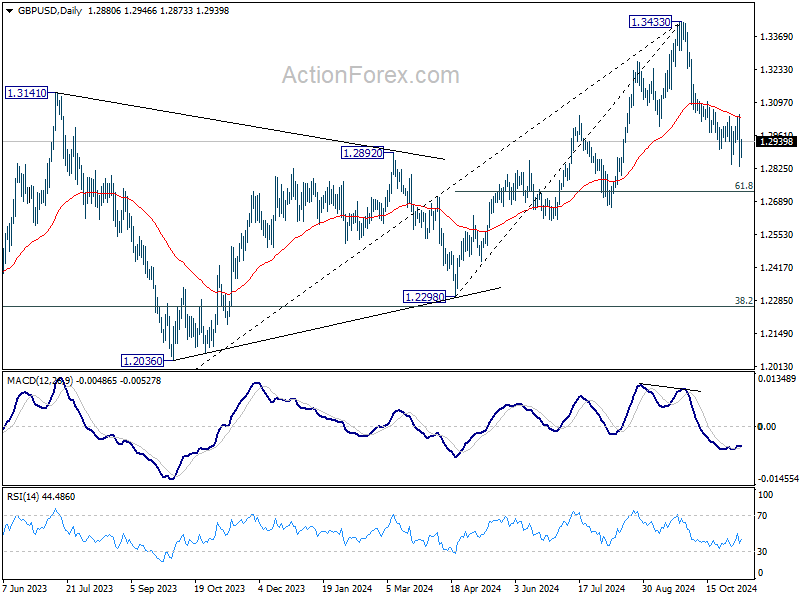

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2793; (P) 1.2920; (R1) 1.3007; More...

Intraday bias in GBP/USD remains neutral and more consolidations would be seen. Further decline is expected as long as 1.3047 resistance holds. Below 1.2842 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bullish convergence condition in 4H MACD, firm break of 1.3047 will indicate short term bottoming, and turn bias back to the upside.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

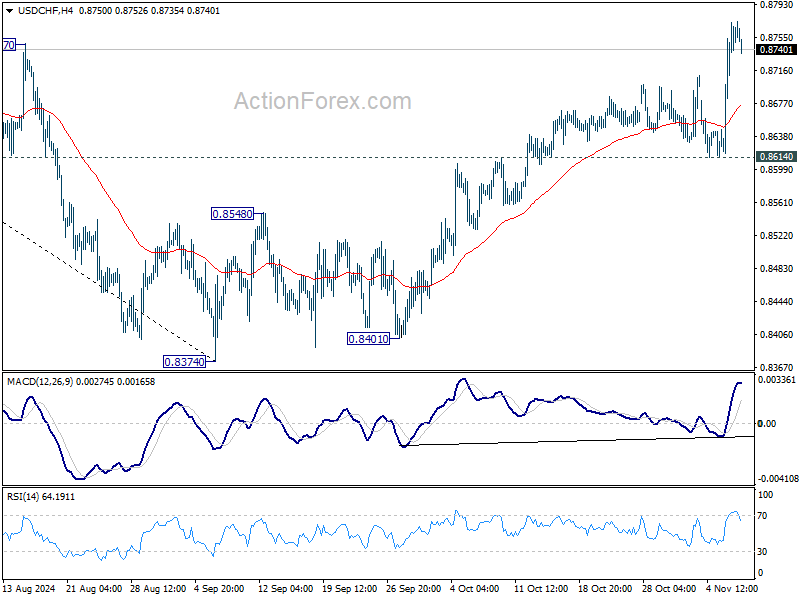

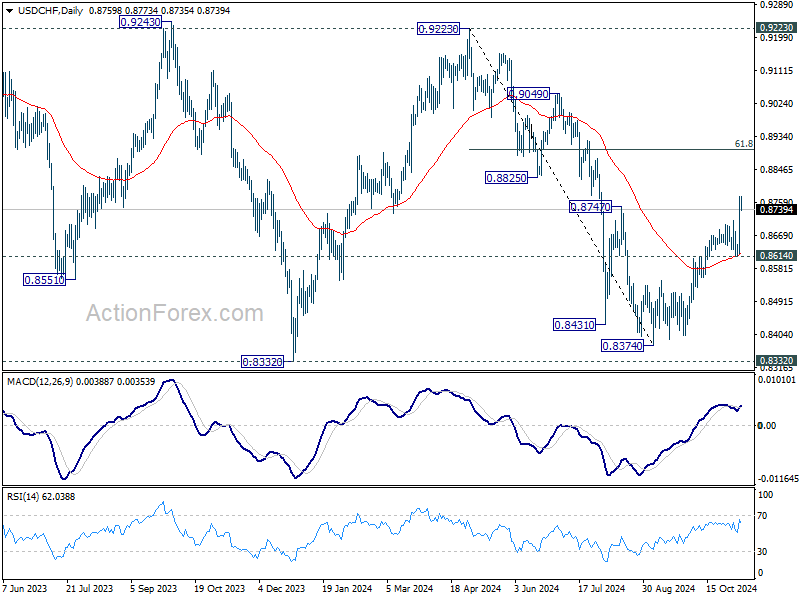

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8666; (P) 0.8720; (R1) 0.8820; More…

USD/CHF's rally is still in progress and intraday bias stays on the upside. Current rise from 0.8374 should target 61.8% retracement of 0.9223 to 0.8374 at 0.8899 next. For now, near term outlook will stay bullish as long as 0.8614 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

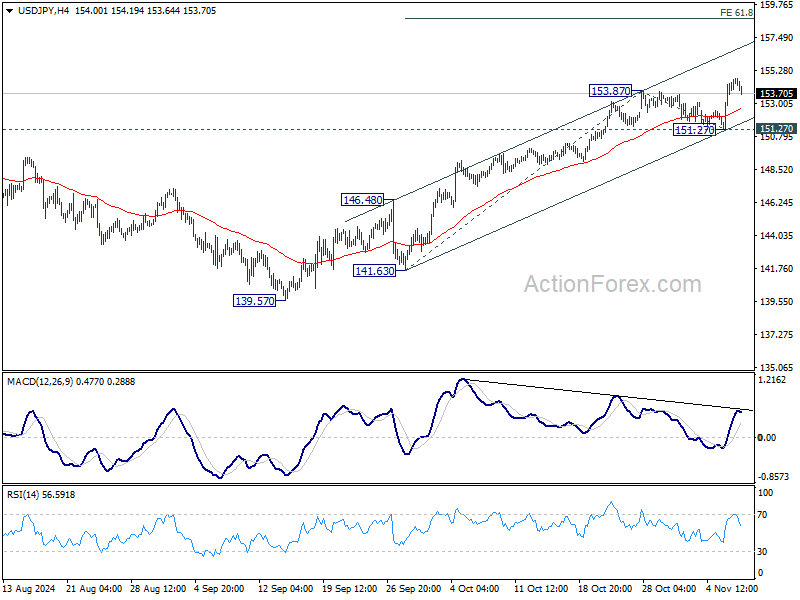

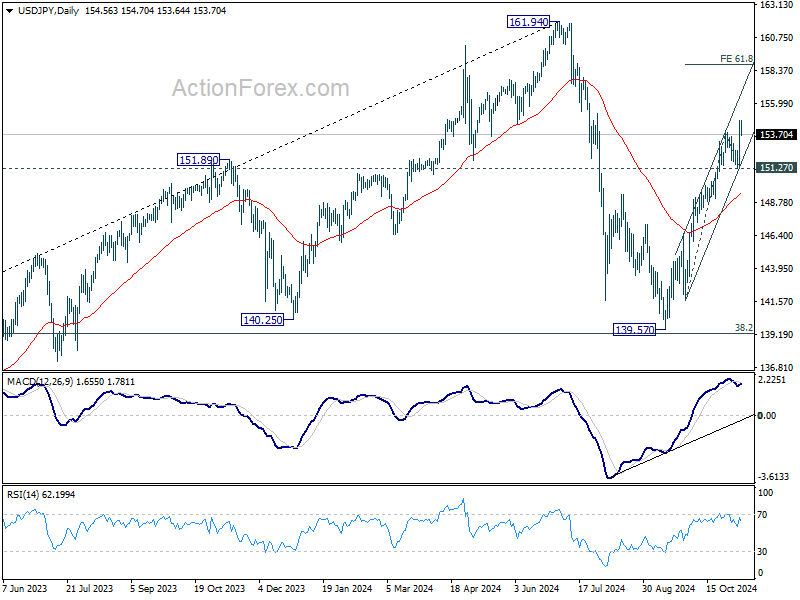

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.37; (P) 153.54; (R1) 155.78; More...

USD/JPY's rally is still in progress and intraday bias stays on the upside. Rise from 139.57 should target 61.8% projection of 141.63 to 153.87 from 151.27 at 158.83. For now, outlook will remain bullish as long as 151.27 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

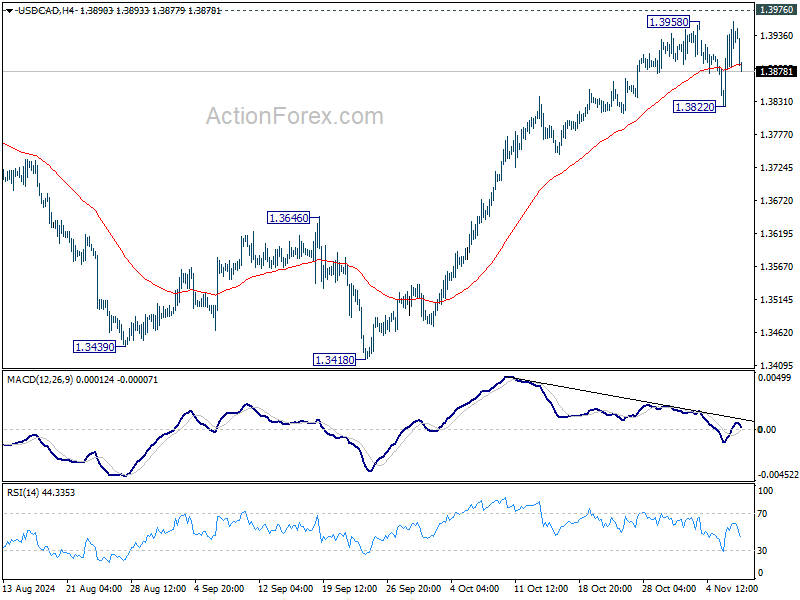

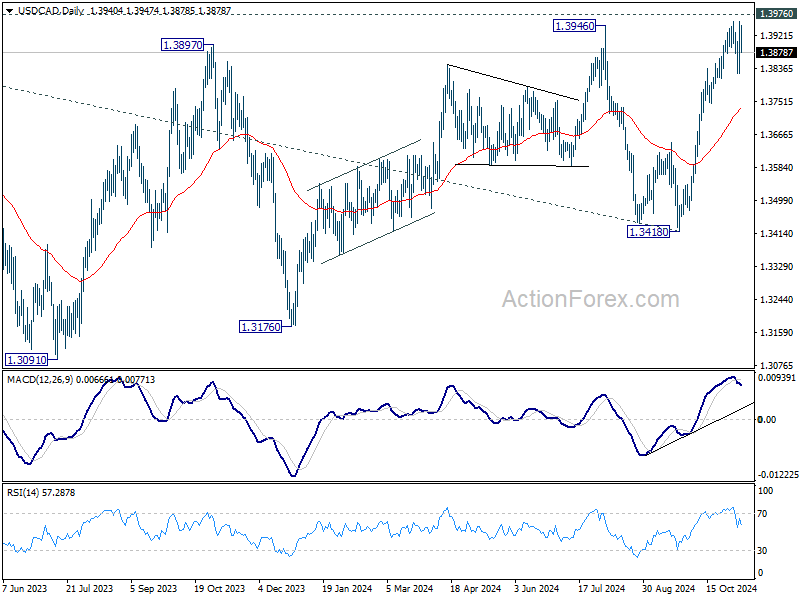

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3850; (P) 1.3905; (R1) 1.3992; More...

USD/CAD is still bounded in range below 1.3958 and intraday bias stays neutral. On the downside break of 1.3822 will bring deeper pullback. But downside should be contained by 55 D EMA (now at 1.3736). On the upside, decisive break of 1.3976 will resume larger up trend.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

Rate Decisions and German Politics Join US Election as Key Market Focus Areas

In focus today

Today, focus will remain on investors digesting the US election result. In addition, German political uncertainty has resurfaced (see below) and we are in for several important monetary policy decisions. We expect Fed to cut rates by 25bp to 4.75%, the BoE to cut by 25bp to 2.75%, the Riksbank to cut by 50bp to 2.75% and Norges Bank to stay on hold at 4.5%. This is in line with market expectations. That said, recent budget uncertainty in the UK leaves the Bank of England communication with the potential to move markets irrespective of the rate decision.

We also get quite a few datapoints around the globe: September retail sales data in the euro area, industrial production data for September in Germany, flash inflation data and budget balance for October in Sweden, wage data for September in Japan overnight and trade data for October in China.

Economic and market news

What happened overnight

In China, total exports surprised significantly to the topside at 12.7% Y/Y (cons: 5.2% Y/Y, prior: 2.4% Y/Y). Leading up to the election, Chinese factories rushed production as a Trump win became more likely, increasing the threat of a tariffs and ultimately a trade war. At the same time, imports turned negative at -2.3% Y/Y (cons: -1.5% Y/Y, prior: 0.3% Y/Y). Trumps election could, in the short run boost Chinese exports as seen this month, as importers increase their purchases ahead of potential US and EU tariffs.

What happened yesterday

In the US, Republicans eyed a red sweep as President Donald Trump was re-elected, the Republicans gained control of the Senate, while the battle for the House remained undecided - albeit leaning in favour of the Republicans. Following the outcome of the US election, the dollar index had its biggest gain since September 2022, US yields surged, and US stocks hit record-highs.

If the Democrats take the House - at this point only priced as a 5% likelihood in prediction markets, some market reactions might reverse, particularly in fixed income markets. A Republican majority would likely entail a fiscal priority of increasing the budget deficit and public debt, potentially heightening inflation pressures. In response to these developments, US yields rose, with the 10-year U.S. breakeven inflation rate reaching around 2.40%. This rate is within the Federal Reserve's tolerance level, although further increases might prompt a more hawkish stance.

Looking ahead, market focus is expected to return to economic fundamentals, starting with the FOMC meeting today and the US CPI report due next week. The election outcomes reinforce a bearish outlook for EUR/USD through 2025, driven by stronger U.S. growth dynamics.

In the euro area, the final PMIs for October came in: Composite at 50.0 (cons: 49.7, prior: 49.7), Services at 51.6 (cons: 51.2, prior: 51.2) and Manufacturing at 46.0 (cons: 45.9, prior: 45.9). Additionally in Germany, we receive data on factory orders in September, providing a hint of what the industrial production data will show on Thursday. The final PMIs surprised slightly to the upside, largely due to the growth in services in Italy, France and Germany. The activity in services continues to support growth in the euro area, despite the decline in manufacturing.

The Trump win increases uncertainty of the economic outlook in the euro area, but short-term we do not expect an impact on the economy, while the medium-term effect is negative. The increased uncertainty of the medium-term growth outlook supports our expectations for back-to-back rate cuts by the ECB due to concerns of below-potential growth.

In Germany, the chancellor Olaf Scholz, fired his finance minister, Christian Lindner and called for snap elections in March, throwing the country into political disarray. The firing of Lindner from the liberal party comes after many months of disagreements over the 2025 budget and a longer-term plan to revive the German business model. Increased political uncertainty will not be positive for the already fragile German economy and curt hurt growth through lower investments.

In Sweden, the monthly inflation expectations survey revealed that that lower inflation and lower rates have not yet had a positive impact on consumers and that the hard-beaten construction sector is still deteriorating. While headline PMIs firmed, the services employment index collapsed. Inflation is a tad higher than the Riksbank's forecast, however given the bleaker-than-anticipated recovery the probability of a rate cut today has in our view tilted in favour of 50bp. The rate decision will be published at CET 09:30.

Equities: Global equities were up 1.7% yesterday, driven by the outcome of the US election. Looking at this morning's moves in open cash trades and futures, markets appear to be fluctuating in a normalized fashion. While the outcome of the House cannot yet be definitively called, it seems most likely that we will see a red sweep. On a global scale, the election itself did not have an overwhelming effect on equity returns, considering the huge focus. Beneath the surface, we observed a massive outperformance of US equities and a stronger dollar. As expected, cyclicals outperformed defensives by a substantial margin, with banks performing particularly strongly in the US. The US KBW regional bank index ended 10.7% higher yesterday. European banks underperformed compared to their US counterparts, mainly due to differences in cross-Atlantic yields and changes in the relative monetary policy outlook. Spanish and Portuguese markets were the primary losers, driven by their banking sectors. It is important to note the "Mexican effect", with some of these banks deriving up to 50% of their profits from Mexico.

Small caps benefited yesterday, outperforming large caps by more than 1% on a global level, again led by the US with the Russell 2000 index ending 5.8% higher. The strong performance in small caps may be surprising to many, as small caps generally suffer from higher yields. However, considering the developments leading up to the election, this should not be as surprising. Despite suffering from higher yields, small caps are benefiting from de-regulation and US-first policies. One of the interesting aspects to follow will be the M&A activity across the board, from small to mega-cap deals under the new administration.

The main loser has been utility companies, as they are both related to the green transition and negatively exposed to higher yields. In the US yesterday, the Dow was up by 3.6%, the S&P 500 by 2.5%, Nasdaq by 3.0%, and the Russell 2000 by 5.8%. Asian markets are mixed this morning, reversing some of the differences from yesterday. While the effect of Chinese policy announcements can be hard to separate from the US election effect, we can at least partly conclude that the US election result has not led to investors fleeing away from China. US and European markets are calm this morning with small gains in both markets.

FI: Markets are extending the "Trump trade" with higher yields, higher BEI-rates and a steeper US yield curve driven from the long end. However, the impact on the European yield curves has been somewhat different as short-dated yields declined and the curve steepened from the short end as the market are factoring in more rate cuts in Europe and less rate cuts in the US. However, we still expect that the Federal Reserve will cut rates tonight with 25bp.

FX: EUR/USD dropped by around two full figures, trading in the mid 1.07-1.08 range, as a significant divergence emerged between USD and EUR rates following Trump's win. The USD broadly gained, not only within the G10 space but also against tariff-exposed currencies such as CNH and MXN. USD/JPY rose above the 154-mark. EUR/GBP tracked lower during yesterday's session and ahead of today's expected 25bp rate cut from the BoE. Despite the extended dollar rally, EUR/Scandies kept stable, even closed lower on the day. There could be an initial negative impact on the SEK if the Riksbank opts for a 50bp rate cut today, but upside in EUR/SEK should be limited given that it is broadly anticipated and that our short-term model suggests that the cross is stretched overbought.

Chapter Two

The 2024 US election delivered a decisive victory for Donald Trump, with Republicans positioned to gain control of both houses of Congress.

The S&P500 jumped 2.5% to a fresh record and recorded its best post-election gain. The energy stocks surged nearly 4%. Nasdaq 100 advanced 2.74%, to a fresh record high, as well. Tesla soared almost 15% as Technoking Elon Musk’s heavy campaigning for Donald Trump now leaves him with super-close connections to the White House. Then, the Dow Jones surged more than 3.5% to a fresh record as well, as bank stocks rallied hard on Trump’s promise of deregulation. Invesco’s KBW Bank ETF, for example, jumped more than 10%. Bitcoin, of course, rallied to a fresh record high, and the small caps gained nearly 6% on hope that Trump’s protectionist stance will help their business.

In the FX, the US dollar soared to the highest levels since summer. Gold dived to its 50-DMA on relief that the election result was clear. And the USDCHF received a greenlight to step into the medium-term bullish consolidation zone.

As such, the Trump trade went according to the plan. US equities rallied, banks and small caps led gains, the US dollar gained, as the US yields rose on anticipation of further ballooning of the national debt. Everything that has to do with green, alternative, clean energy lost.

Beyond the borders

I was writing yesterday, before the market open, that the DAX and Eurostoxx futures were in the negative on fear that Trump would hit the European companies with new tariffs. Well, they turned positive at the open on hope that Trump presidency would call for a swift dovish response from the European Central Bank (ECB) to counter the shock. But gains remained short-lived and the European indices closed the session in the negative.

On top, Olaf Scholz called for a snap election in Germany as his three-way coalition collapsed under the weight of economic difficulties European carmakers faced a tough day, pressured by fears of higher tariffs.

Among the European indices, the Swiss SMI and FTSE 100 ended with relatively small losses – the SMI because it’s defensive by nature, and the FTSE 100 because the US dollar’s surge gave a boost to the FTSE 100 companies that get a clear majority of their revenues from abroad. But Trump policies are pro-US growth and anti-global growth. Therefore, the SMI is a good option for investors seeking defensive names. But Trump’s medium-term impact on mining companies’ revenues will not necessarily be positive. Copper futures – a gauge of global growth - dived more than 5% as a reaction to Trump win.

Trumpflation

For the US, it’s clear: pro-growth policies, tax cuts, tariffs point at higher inflation in the US. The Federal Reserve (Fed) is expected to announce a 25bp cut today, but the policy beyond today’s decision must be readjusted accordingly. The expectation, so far, was that the Fed would cut today by 25bp, and deliver another 25bp cut in December, and a full point cut next year. Now, the December cut is on a slippery ground and the Fed should not consider more than 2-3 rate cuts next year. That’s – at least – the policy response that you would reasonably expect from a central bank as an economist.

Elsewhere, opinions diverge. Some believe that the US will export its Trumpflation – if nothing by a stronger US dollar, but others argue that cheap Chinese goods – heavily taxed in the US - will spill over into the rest of the world, potentially keeping price pressures contained elsewhere.

In this new context (as says Emmanuel Macron), the Bank of England (BoE) has the hard task to deliver its first policy decision post-Trump. The BoE is expected to cut rates by 25bp today. The markets price in two more rate cuts by the end of next year and gives a 35% chance for a third one. Of course, the BoE must also deal with the higher government spending that Rachel Reeves promised a few days ago – that alerted the BoE hawks that the easing must be carefully measured to counter the fiscal expansion, as well. But since then, the gilt yields soared so sharply that they wiped out all the UK’s fiscal headroom. And now, the bank analysts are lowering their post-Trump growth expectations for the UK – which is, in return, dovish for the BoE bets.

In summary, no one knows quite which foot to dance on. All eyes are on Powell and Bailey to help chart a roadmap.

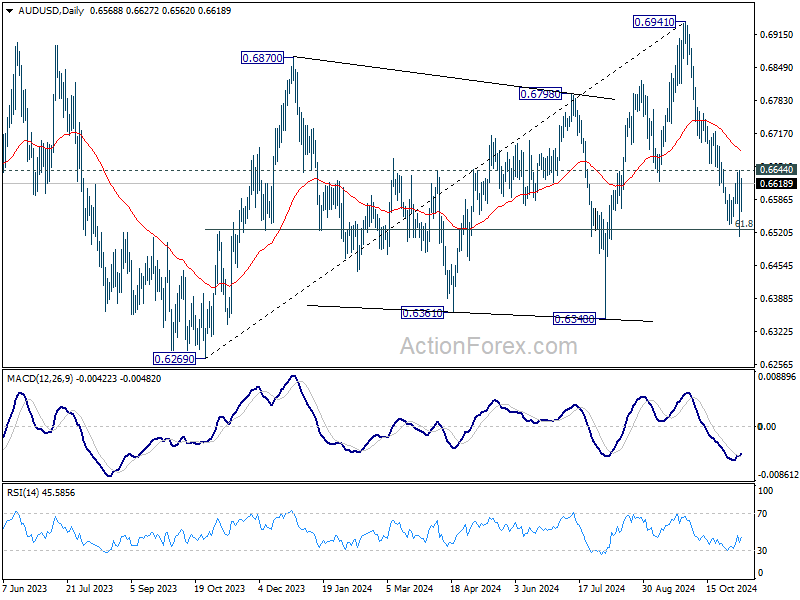

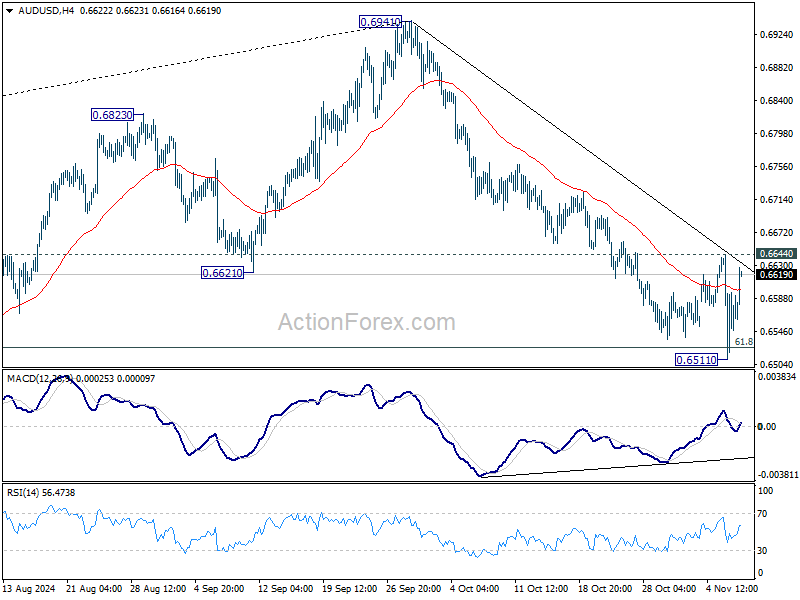

AUD/USD Daily Report

Daily Pivots: (S1) 0.6508; (P) 0.6577; (R1) 0.6640; More...

AUD/USD failed to sustain below 61.8% retracement of 0.6269 to 0.6941 at 0.6526 will target 0.6348, and recovered after dipping to 0.6511. Intraday bias is turned neutral again first. Further fall is still expected as long as 0.6644 resistance holds. Firm break of 0.6526 will pave the way to 0.6348 support next. However, considering bullish convergence condition in 4H MACD, break of 0.6644 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 0.6682).

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.