Sample Category Title

Sunset Market Commentary

Markets

The consequences of yesterday evening’s decision by German Chancellor Scholz to sack his finance minister, Lindner, might by far-reaching. Lindner’s hard “no” against modifying the debt brake enshrined in the German constitution to allow for more spending in order to revive the economy mired in recession but also to grant more support to Ukraine for example, was the straw that broke the coalition’s back. Scholz tabled a confidence vote on December 15. Assuming he’ll lose it, snap elections could be set up for March (instead of September). German opposition leader Merz (CDU) today indicated he wants to speed things up with a confidence vote next week allowing for January elections. Lindner’s FDP backed that call. We think that German elections would effectively result in a looser fiscal policy stance, even as the CDU’s (leading in the polls) official view is still one committed to strict borrowing rules and against additional joint EU debt. Last week’s UK budget and this week’s US presidential elections proved that you can’t win an election running on any other platform than the economy/purchasing power (and safety/migration). Markets anticipate what could be coming. German Bunds underperform today more than reversing yesterday’s odd gains. German yields rise by 5.3 bps (2-yr) to 7.9 bps (30-yr). The Bund/swap spread turns positive for the first time on record in a sign of rising German credit risk. The inflationary monetary shift started a reversal from a deeply negative Bund/swap spread and that move accelerated under impulse of recent UK/US/German developments. It’s clear that governments are willing to take the inflationary risk to boost short term growth. This will have consequences for central banks, as evidenced by today’s Bank of England gathering and potentially at tonight’s FOMC meeting although the lack of new growth and inflation forecasts might push the issue to the December meeting.

The BoE cut its policy rate by 25 bps to 4.75% in a 8-1 vote. Catherine Mann preferred to maintain the rate at 5%. In a first estimate, the UK central bank measures the combined effects of the measures announced in Chancellor Reeves’ Autumn Budget as a boost to the level of GDP by around 0.75% at the peak in a year’s time compared to August projections: 1.7%-1.7%-1.1%-1.4% for 2024-2027 (from 2%-0.9%-1.5%; 2027 is a first estimate). The Budget is provisionally expected to boost CPI inflation by just under half of a percentage point at the peak: 2.4%-2.7%-2.2%-1.6% for 2024-2027 (from 2.7%-2.2%-1.6%). There remains significant uncertainty on the impact on the labour market. A gradual, data-dependent approach to removing policy restraint remains appropriate. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target have dissipated further. BoE governor Bailey at the press conference stressed that the UK central bank can’t cut rates too quickly or by too much. Market by and large anticipated today’s hawkish cut. Sterling made an attempt to go for test of the EUR/GBP 0.83 support, but the move never went far.

News & Views

The Swedish Riksbank accelerated its normalization cycle with a flagged 50 bps rate cut from 3.25% to 2.75%. The central bank argues that core CPIF inflation dynamics held close to the target since the start of the year. At the same time, activity remains weak and there are few signs of the hoped-for recovery. They stick with plans of easing policy further in December and H1 2025, but could accelerate the process compared with indications in the September forecast. Markets see the Riksbank policy rate close to 2% at the end of Q3 2025. After touching a short-term low just above EUR/SEK 11.70, the krone yesterday and today rebounded modestly. A return below 11.50 is needed to call off the short term negative alert on the Swedish currency.

Divergence in Scandinavian monetary policy persists. The Norges Bank left its policy rate unchanged at the cycle top of 4.5%. Policy restriction has cooled activity and dampened inflation, but a weak krone and a rapid rise in business costs will slow further disinflation. International policy rate expectations have increased as well. The Norwegian central bank maintained its guidance to gradually reduce the policy rate from Q1 2025 as indicated in September. Money markets discount a first 25 bps rate cut by the end of Q1. After almost touching the EUR/NOK 12 barrier earlier this week, the krone yesterday and even more today rebounded to the EUR/NOK 11.75 area.

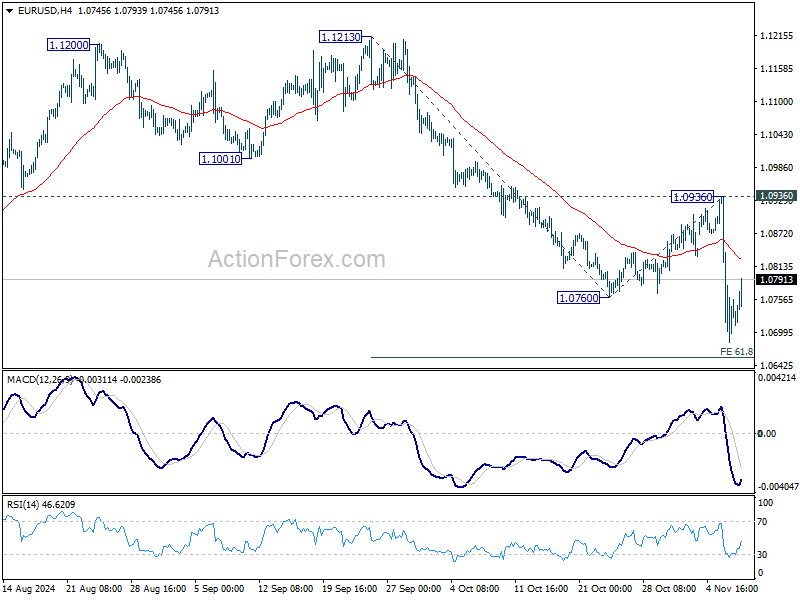

EUR/USD Mid-Day Outlook

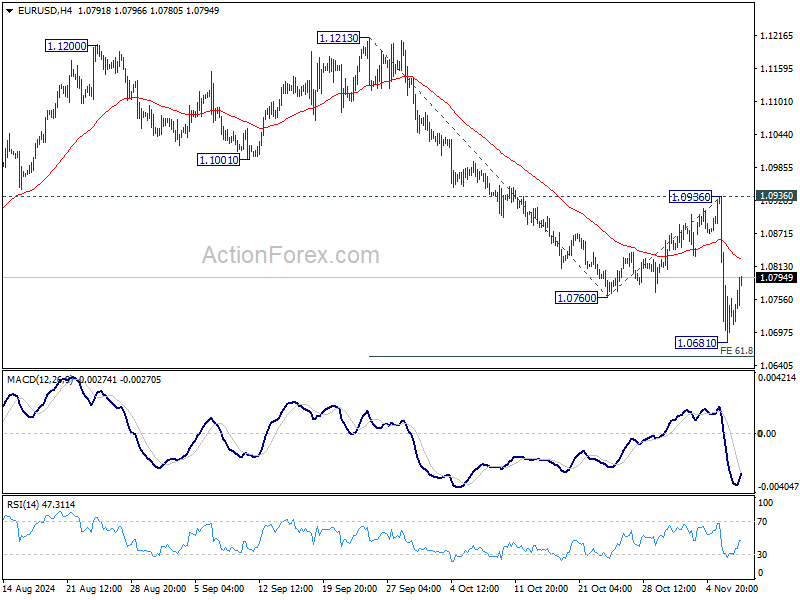

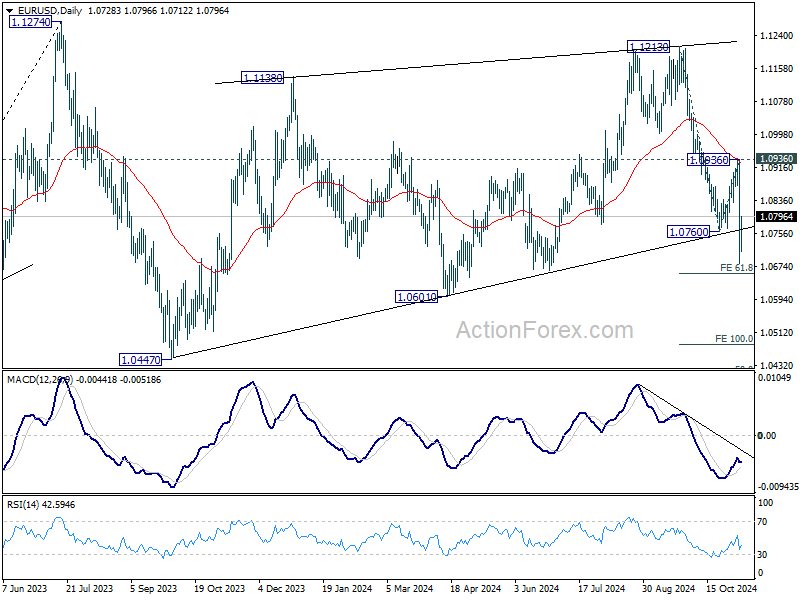

Daily Pivots: (S1) 1.0628; (P) 1.0783; (R1) 1.0885; More...

Intraday bias in EUR/USD Is turned neutral first with current recovery. Some consolidation would be seen but further decline is expected as long as 1.0936 resistance holds. ON the downside, sustained break of 61.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0656 will pave the way to 100% projection at 1.0483.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

GBP/USD Mid-Day Outlook

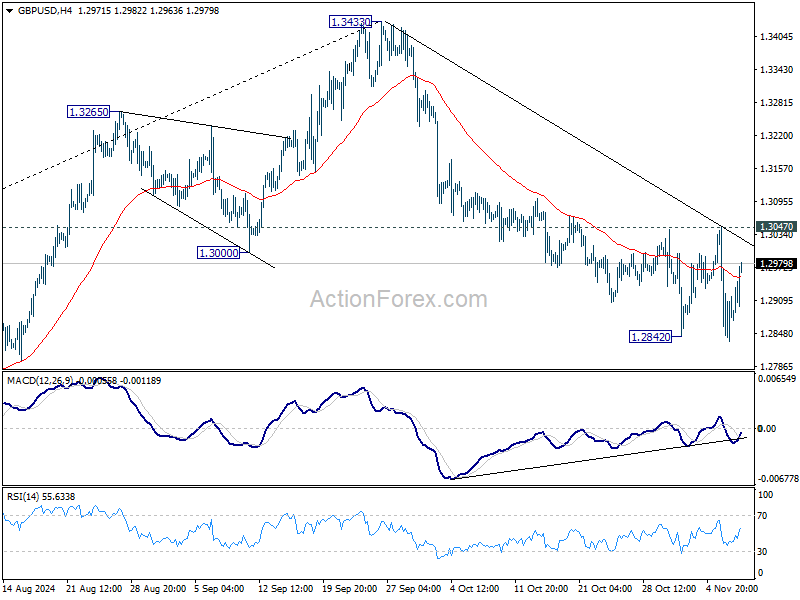

Daily Pivots: (S1) 1.2793; (P) 1.2920; (R1) 1.3007; More...

Range trading continues in GBP/USD and intraday bias stays neutral. With 1.3047 resistance intact, further decline is still expected. Firm break of 1.2842 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bullish convergence condition in 4H MACD, firm break of 1.3047 will indicate short term bottoming, and turn bias back to the upside.

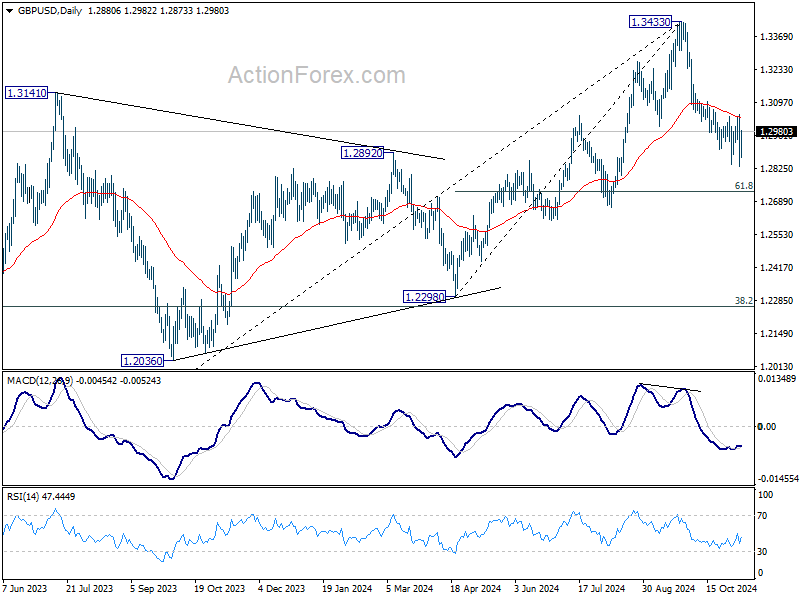

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

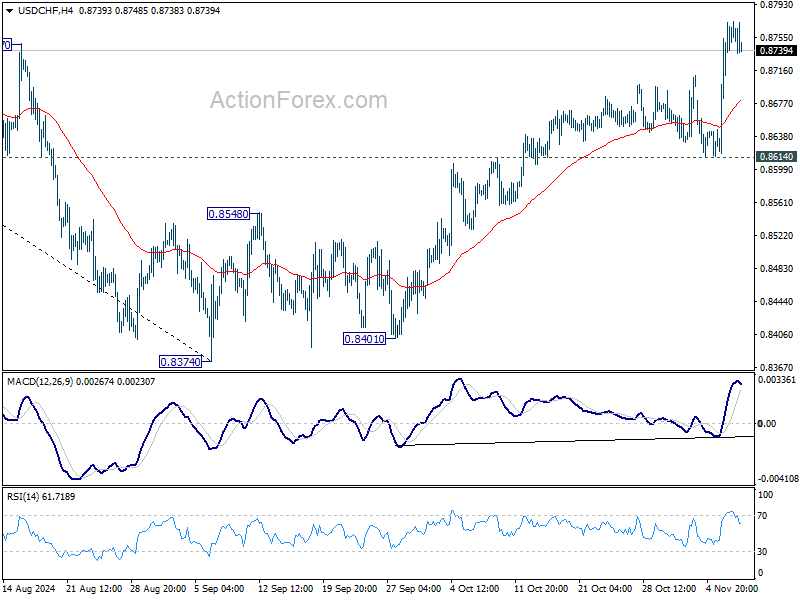

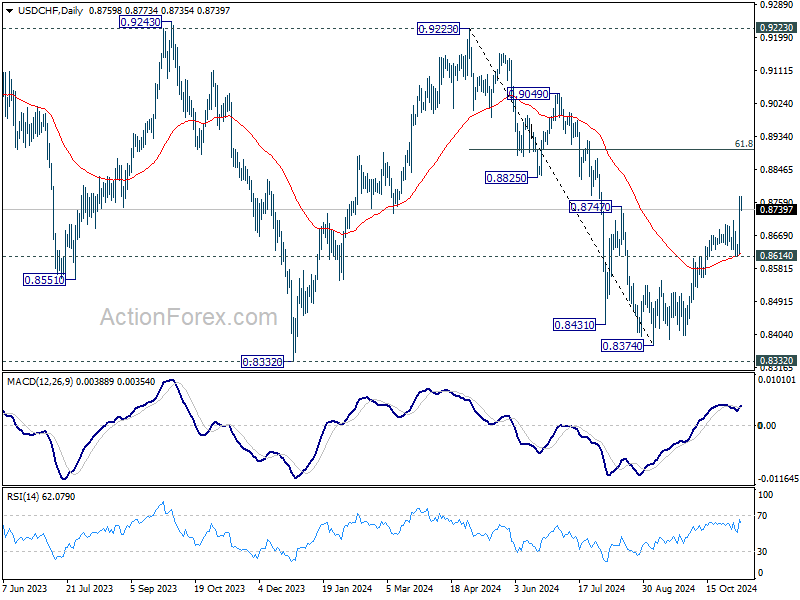

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8666; (P) 0.8720; (R1) 0.8820; More…

Intraday bias in USD/CHF stays on the upside at this point. Current rise from 0.8374 should target 61.8% retracement of 0.9223 to 0.8374 at 0.8899 next. For now, near term outlook will stay bullish as long as 0.8614 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

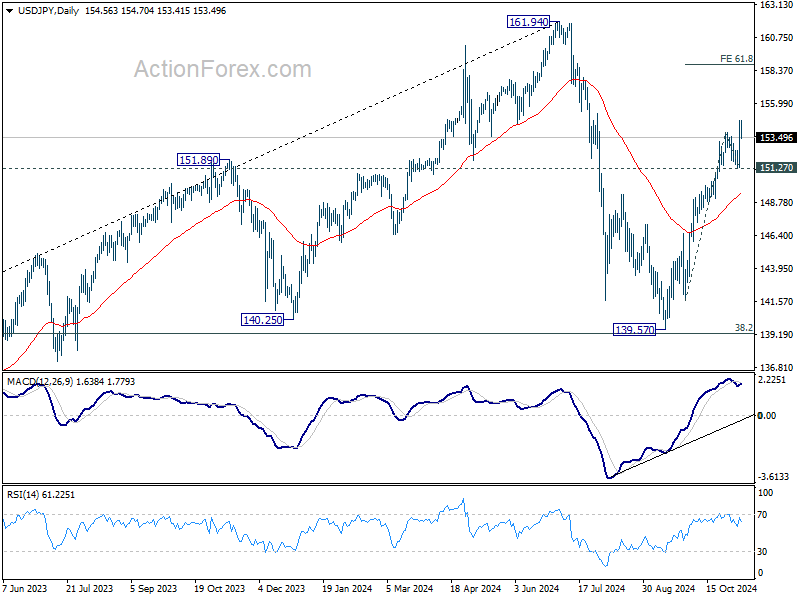

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.37; (P) 153.54; (R1) 155.78; More...

Intraday bias in USD/JPY is turned neutral with current retreat and some more consolidations would be seen first. Further rally is expected as long as 151.27 support holds. On the upside, break of 154.70 will resume the rally from 139.57 to 61.8% projection of 141.63 to 153.87 from 151.27 at 158.83.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Reverses Post-Election Gains as Markets Seek Clarity on Fed’s Rate Path

Dollar continued to weaken in early US session, erasing the strong gains it enjoyed following Donald Trump's election victory. The greenback has turned negative for the week against several major currencies, suggesting that the initial post-election optimism has waned. Investors are now shifting their attention to Fed's upcoming rate decision for guidance on Dollar's next move. However, the pressing issue of Fed's monetary policy path for next year—beyond today's expected 25bps cut and another anticipated in December—is unlikely to be resolved immediately. Market participants may have to wait until the FOMC releases new economic projections in December to gain a clearer understanding of the central bank's plans.

Meanwhile, British Pound holds steady after BoE's widely anticipated 25bps rate cut to 4.75%. The accompanying statement indicates that BoE will proceed with a measured, gradual approach to policy easing moving forward. However, Governor Andrew Bailey noted during the press conference that the pace of rate cuts could accelerate if inflation continues to decline more rapidly than expected.

In the currency markets, Aussie is currently the strongest performer of the week, followed by Kiwi and Loonie, reflecting a typical risk-on environment where investors favor higher-yielding assets. On the other end of the spectrum, Swiss Franc is the weakest currency, with Euro and Yen also underperforming. Dollar and Pound are positioned in the middle of the pack.

Technically, as Dollar's pullback persists, key levels are coming into focus including 1.0936 resistance in EUR/USD, 1.3057 resistance in GBP/USD, 0.8614 support in USD/CHF and 151.27 support in USD/JPY. As long as these levels hold, Dollar's near term rally would remain intact for resumption at a later stage.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 1.44%. CAC is up 0.51%. UK 10-year yield is down -0.0185 at 4.545. Germany 10-year yield is up 0.040 at 2.448. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 2.02%. China Shanghai SSE rose 2.57%. Singapore Strait Times rose 1.96%. Japan 10-year JGB yield rose 0.0258 to 1.007.

US initial jobless claims rises to 221k vs exp 220k

US initial jobless claims rose 3k to 221k in the week ending November 2, slightly above expectation of 220k. Four-week moving average of continuing claims fell -10k to 227k.

Continuing claims rose 39k to 1892k in the week ending October 26, highest since November 13, 2021. Four-week moving average of continuing claims rose 8.5k to 1876k, highest since November 27, 2021.

BoE cuts 25bps, emphasizes gradual easing amid upgraded inflation projections

BoE reduced the Bank Rate by 25bps to 4.75%, in line with expectations. The Monetary Policy Committee made the decision by an 8-1 vote, with Catherine Mann dissenting, preferring to keep rates steady. In its statement, BoE highlighted that a “gradual approach” to reducing policy restraint remains “appropriate,” stressing that restrictive monetary policy will need to persist “for sufficiently long” until risks to sustainable 2% inflation are more fully mitigated.

BoE’s revised economic projections reflect a significant adjustment in inflation expectations. The forecast for CPI in Q4 2025 was raised from 2.2% to 2.7%, while the Q4 2026 estimate increased from 1.6% to 2.2%. Longer-term, inflation is expected to ease to 1.8% by Q4 2027, suggesting a slower return to the target rate.

GDP growth estimates were also adjusted, with the Q4 2025 growth forecast increased from 0.9% to 1.7%, though growth for Q4 2026 was revised down to 1.1%, followed by a modest recovery to 1.4% in Q4 2027.

BoE also provided an initial assessment of the government's Autumn Budget 2024, forecasting that the fiscal measures could boost GDP by approximately 0.75% at their peak, compared to the August projections.

The budget’s influence on CPI inflation is anticipated to peak at just under 0.5%, due to both the narrowing excess supply margin and direct inflationary impacts from the budget measures.

Eurozone retail sales rises 0.5% mom, mixed sectoral performance

Eurozone retail sales rose by 0.5% mom in September, slightly above the expected 0.4% mom increase. Breaking down the numbers, the volume of retail trade showed a mixed sectoral performance. Sales for non-food products, excluding automotive fuel, saw a notable rise of 1.1% mom, while sales for food, drinks, and tobacco slipped by -0.4% mom. Automotive fuel sales in specialized stores edged up by 0.2% mom.

Across the broader EU, retail sales rose by 0.3% mom. Among member states with available data, Belgium, Denmark, and Croatia recorded the highest increases, each posting a robust 2.1% mom rise in retail trade volume. Germany followed with a 1.2% mom gain. In contrast, Slovenia experienced the sharpest drop at -2.6% mom, followed by Poland at -2.0% mom and Finland at -1.6% mom.

Japan’s real wages dip again in Sep, despite continued nominal wage growth

Japan's real wages declined by -0.1% yoy in September, marking a second consecutive monthly drop as inflation erodes purchasing power. This dip follows a record 26-month downturn that ended in May, with wages briefly turning positive in June and July. However, the fading impact of summer bonuses led to another decline in August.

Nominal wages, reflecting total monthly earnings including base and overtime pay, rose by 2.8% yoy in September, marking the 33rd consecutive month of growth, but missed expectation of 3.0% yoy. When excluding bonuses and unscheduled payments, average wages grew by 2.6% yoy, the highest increase in nearly 32 years. Despite this, overtime pay and allowances declined by -0.4% yoy.

Separately, a Nikkei Research poll indicates optimism among companies for wage increases in the upcoming fiscal year. Approximately 42% of surveyed firms plan to raise wages by 3% to 5% for the fiscal year starting in April 2025, while 9% consider a larger increase of 5% to 7%. However, a significant portion (41%) of companies anticipate more conservative hikes in the range of 1% to 3%, suggesting that while wage pressures may continue, the scope and impact could vary widely across sectors.

RBA's Bullock: Waiting for clear signals before assessing Trump's win

At a Senate session today, RBA Governor Michele Bullock indicated that the central bank has not yet conducted detailed scenario analyses on how Donald Trump's US presidential victory might impact Australia's monetary policy.

Bullock emphasized that the effects could go different directions. She pointed out that while a Trump presidency might be "inflationary in some ways," particularly if it leads to increased global demand or fiscal stimulus, it could also be "deflationary" if China, a key trading partner for Australia, is negatively affected.

Bullock stressed the importance of basing policy decisions on concrete developments rather than speculation. "We cannot be setting policy on the basis of things that could happen or might not happen," she remarked. She added that the central bank intends to "wait and see what actually does happen" before making any adjustments.

As it stands, RBA has not revised its inflation outlook. Bullock reiterated that inflation is expected to return to the target band of 2-3% sustainably by 2026.

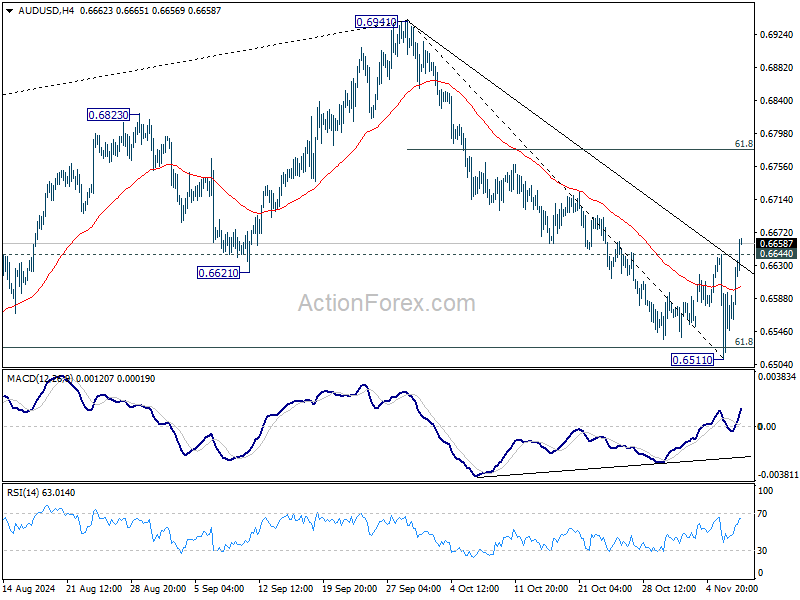

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6508; (P) 0.6577; (R1) 0.6640; More...

AUD/USD's break of 0.6644 resistance indicates short term bottoming at 0.6511, on bullish convergence condition in 4H MACD, after drawing support from 61.8% retracement of 0.6269 to 0.6941 at 0.6526. Intraday bias is back on the upside for 55 D EMA (now at 0.6682). Sustained break there will bring stronger rebound back 61.8% retracement of 0.6941 to 0.6511 at 0.6777.

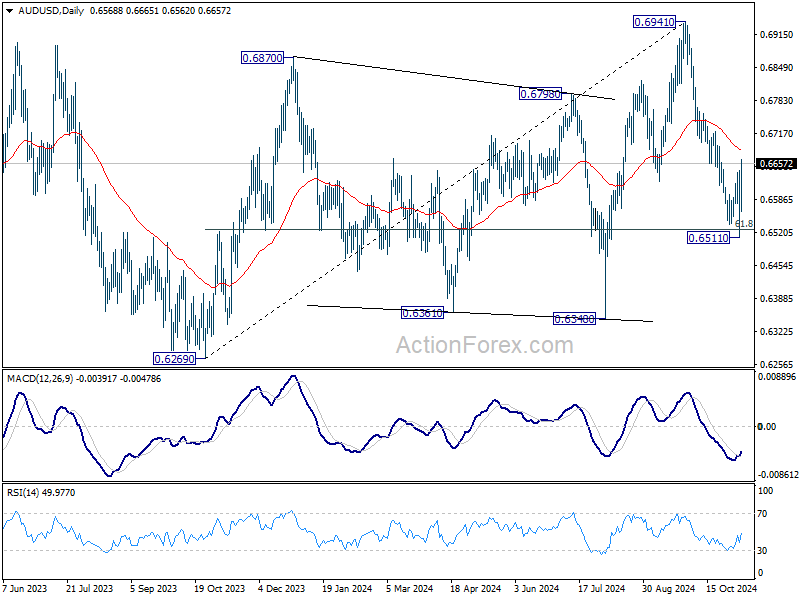

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6508; (P) 0.6577; (R1) 0.6640; More...

AUD/USD's break of 0.6644 resistance indicates short term bottoming at 0.6511, on bullish convergence condition in 4H MACD, after drawing support from 61.8% retracement of 0.6269 to 0.6941 at 0.6526. Intraday bias is back on the upside for 55 D EMA (now at 0.6682). Sustained break there will bring stronger rebound back 61.8% retracement of 0.6941 to 0.6511 at 0.6777.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

US initial jobless claims rises to 221k vs exp 220k

US initial jobless claims rose 3k to 221k in the week ending November 2, slightly above expectation of 220k. Four-week moving average of continuing claims fell -10k to 227k.

Continuing claims rose 39k to 1892k in the week ending October 26, highest since November 13, 2021. Four-week moving average of continuing claims rose 8.5k to 1876k, highest since November 27, 2021.

BoE cuts 25bps, emphasizes gradual easing amid upgraded inflation projections

BoE reduced the Bank Rate by 25bps to 4.75%, in line with expectations. The Monetary Policy Committee made the decision by an 8-1 vote, with Catherine Mann dissenting, preferring to keep rates steady. In its statement, BoE highlighted that a “gradual approach” to reducing policy restraint remains “appropriate,” stressing that restrictive monetary policy will need to persist “for sufficiently long” until risks to sustainable 2% inflation are more fully mitigated.

BoE’s revised economic projections reflect a significant adjustment in inflation expectations. The forecast for CPI in Q4 2025 was raised from 2.2% to 2.7%, while the Q4 2026 estimate increased from 1.6% to 2.2%. Longer-term, inflation is expected to ease to 1.8% by Q4 2027, suggesting a slower return to the target rate.

GDP growth estimates were also adjusted, with the Q4 2025 growth forecast increased from 0.9% to 1.7%, though growth for Q4 2026 was revised down to 1.1%, followed by a modest recovery to 1.4% in Q4 2027.

BoE also provided an initial assessment of the government's Autumn Budget 2024, forecasting that the fiscal measures could boost GDP by approximately 0.75% at their peak, compared to the August projections.

The budget’s influence on CPI inflation is anticipated to peak at just under 0.5%, due to both the narrowing excess supply margin and direct inflationary impacts from the budget measures.

(BOE) Bank Rate reduced to 4.75%

Monetary Policy Summary, November 2024

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 6 November 2024, the MPC voted by a majority of 8–1 to reduce Bank Rate by 0.25 percentage points, to 4.75%. One member preferred to maintain Bank Rate at 5%.

There has been continued progress in disinflation, particularly as previous external shocks have abated, although remaining domestic inflationary pressures are resolving more slowly.

CPI inflation fell to 1.7% in September but is expected to increase to around 2½% by the end of the year as weakness in energy prices falls out of the annual comparison. Services consumer price inflation has declined to 4.9%. Annual private sector regular average weekly earnings growth has continued to fall but remained elevated at 4.8% in the three months to August. Headline GDP growth is expected to fall back to its recent underlying pace of around ¼% per quarter over the second half of this year. The MPC judges that the labour market continues to loosen, although it appears relatively tight by historical standards.

Monetary policy has been guided by the need to squeeze remaining inflationary pressures out of the economy to achieve the 2% target both in a timely manner and on a lasting basis. The Committee’s deliberations have been supported by the consideration of a range of cases that could impact the evolution of inflation persistence. These three cases are set out further in the accompanying November Monetary Policy Report.

In the first case, most of the remaining persistence in inflation may dissipate quickly as pay and price-setting dynamics continue to normalise following the unwinding of the global shocks that drove up inflation. In the second case, a period of economic slack may be required to normalise these dynamics fully. In the third case, some inflationary persistence may also reflect structural shifts in wage and price-setting behaviour. Each case would have different implications for how quickly the restrictiveness of monetary policy could be withdrawn.

The MPC’s latest projections for activity and inflation are also set out in the accompanying November Report. This forecast is based on the second case. CPI inflation is projected to fall back to around the 2% target in the medium term, conditioned on the usual 15 day average of forward interest rates, as a margin of slack emerges later in the forecast period that acts against second-round effects in domestic prices and wages.

The combined effects of the measures announced in Autumn Budget 2024 are provisionally expected to boost the level of GDP by around ¾% at their peak in a year’s time, relative to the August projections. The Budget is provisionally expected to boost CPI inflation by just under ½ of a percentage point at the peak, reflecting both the indirect effects of the smaller margin of excess supply and direct impacts from the Budget measures.

There remains significant uncertainty around the outlook for the labour market. Data are difficult to interpret and wage growth has been more elevated than usual relationships would predict. The impact of the Budget announcements on inflation will depend on the degree to and speed with which these higher costs pass through into prices, profit margins, wages and employment.

At this meeting, the Committee voted to reduce Bank Rate to 4.75%, reflecting the continued progress in disinflation.

Based on the evolving evidence, a gradual approach to removing policy restraint remains appropriate. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee continues to monitor closely the risks of inflation persistence and will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 6 November 2024

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying November 2024 Monetary Policy Report.

2: The Committee discussed the near-term global risks and their potential impact on the inflation outlook in the United Kingdom. The balance of risks to global activity, particularly stemming from China and Germany, remained to the downside in the near term. Alongside that, there were upside risks to goods and commodity prices from greater trade fragmentation and adverse geopolitical developments, including from events in the Middle East.

3: Since the MPC’s previous meeting, the market-implied path for Bank Rate in the United Kingdom had shifted up materially. For the period prior to Autumn Budget 2024, market intelligence had attributed the modest upward moves in the market-implied path largely to international factors such as stronger-than-expected economic data in the United States. For the period around the time of the Budget, the upward shift had been more material. However, market pricing had continued to remain consistent with a 25 basis point reduction in Bank Rate at this MPC meeting.

4: Bank staff continued to judge that the economy was growing at around ¼% per quarter on an underlying basis. According to the official data, GDP had grown by 0.5% in 2024 Q2, 0.2 percentage points weaker than had been expected in the August Report, and 0.1 percentage points weaker than the earlier outturn had indicated at the time of the MPC’s previous meeting. Through the second half of 2024, GDP was projected to grow at a somewhat slower rate than in Q2.

5: The Committee discussed the implications of the latest activity data for the evolution of slack in the economy. There was limited evidence that aggregate demand was falling short of aggregate supply. Surveys of capacity utilisation had remained close to their historical averages, and indicators of labour market tightness, while easing of late, continued to appear relatively tight by historical standards. These developments reinforced the view that the drag on activity from the lagged transmission of past monetary tightening was unlikely to intensify over the coming year.

6: There had been material news to the economic outlook in Autumn Budget 2024. Taken together, the fiscal policy announcements were provisionally expected to boost the level of GDP by around ¾% at their peak in a year’s time, relative to the August projections. The Committee also discussed the increase in the overall cost of employment that was likely to follow from the changes to employers’ National Insurance contributions (NICs) and the increase in the National Living Wage (NLW), and the degree to and speed with which that increase might be transmitted into prices, profit margins, wages and employment.

7: Twelve-month CPI inflation had fallen to 1.7% in September. The decline in CPI inflation since the start of this year had primarily reflected lower goods price inflation, with disinflation in underlying services prices having been less pronounced. Services price inflation had, however, decreased quite sharply to 4.9% in September. Most of this downside news had been concentrated in more volatile categories, and some of this was expected to unwind. Services price inflation was expected to remain broadly unchanged over the next six months. Annual growth in private-sector regular average weekly earnings had fallen back significantly since mid-2023, but it had remained relatively strong at 4.8% in the three months to August.

The immediate policy decision

8: The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

9: Since the MPC’s previous meeting, there had been continued disinflation. Twelve-month CPI inflation had fallen to 1.7% in September. The decline in CPI inflation since the start of the year had primarily reflected lower goods price inflation, with disinflation in underlying services prices less pronounced.

10: Annual growth in private sector regular average weekly earnings had fallen back significantly since mid-2023 but had remained relatively strong at 4.8% in the three months to August. Year-ahead expectations for wage growth in the DMP Survey had been flat at around 4% since May, while initial Agents’ intelligence had reported an expected range of pay awards between 2% and 4% next year.

11: GDP had grown by 0.5% in 2024 Q2, slightly weaker than had been expected in the August Report. GDP growth was expected to fall back to its recent underlying pace of around ¼% per quarter over the second half of the year.

12: The combined effects of the measures announced in Autumn Budget 2024 were provisionally expected to boost the level of GDP by around ¾% at their peak in a year’s time, relative to the August projections. The Budget was provisionally expected to boost CPI inflation by just under ½ of a percentage point at its peak, reflecting both the indirect effects of the smaller margin of excess supply and direct impacts from the Budget measures.

13: Based on the collective steer from a wide range of indicators, the MPC judged that the labour market continued to ease but that it appeared relatively tight by historical standards. However, there was significant uncertainty around the labour market outlook and its impact on inflationary persistence. The combined effect of some policies announced in the Budget, particularly the increase in employer NICs and the NLW, was likely to increase the overall costs of employment. The net effect of this news on aggregate inflation would depend on the degree to and speed with which those costs would be transmitted into prices, wages, employment, or otherwise absorbed in profit margins or productivity growth. On the one hand, higher labour costs could constrain firms’ cash-flows if there was limited pass-through to pricing. This in turn could moderate wage growth and further loosen the labour market through reduced labour demand. On the other hand, the increase in labour costs could prove more inflationary if upward pressure on prices were passed on to consumers.

14: The Committee continued to monitor the accumulation of evidence from a broad range of indicators of inflation persistence, including evidence that could point to the three cases set out in the November Monetary Policy Report having begun to materialise. In the first case, most of the remaining persistence in inflation might dissipate quickly as pay and price-setting dynamics continued to normalise following the unwinding of the global shocks that drove up inflation. In the second case, a period of economic slack might be required to normalise these dynamics fully. In the third case, some inflationary persistence might reflect structural shifts in wage and price-setting behaviour.

15: In the November forecast, which was based on the second case, second-round effects in domestic prices and wages were expected to take somewhat longer to unwind than they did to emerge. The margin of slack that emerged later in the forecast period would act against those second-round effects, leading CPI inflation to fall back to around the 2% target in the medium term.

16: If, for example, the economy were to grow broadly as expected, but material downside news to wages and services inflation were nonetheless to emerge, this could increase the weight that the MPC would place on the first case materialising. Signs of a slowing in the disinflation process, particularly in the absence of a pickup in activity growth, could instead increase the likelihood that the MPC would place on the third case materialising.

17: At this meeting, eight members preferred to reduce Bank Rate to 4.75%. There had been continued progress in disinflation, particularly as previous external shocks had abated, although remaining domestic inflationary pressures were resolving more slowly. These members put different probabilities on and risks around the three cases, but they believed that a cut in Bank Rate was appropriate at this meeting. They would continue to assess the range of evidence over time.

18: One member preferred to maintain Bank Rate at 5%. For this member, structural factors in wage and price-setting dynamics continued to draw out the underlying disinflation process, and CPI inflation was projected to remain above the 2% target until the end of the forecast period. Wage developments might continue to be more robust than projected as firms and workers incorporated past and upcoming adjustments in the National Living Wage and National Insurance contributions. This, along with prospects for more robust demand associated with the Budget, was likely to support pricing opportunities for firms. In the face of these uncertainties, maintaining the current level of Bank Rate would allow time to evaluate whether these upside pressures would materialise.

19: Based on the evolving evidence, a gradual approach to removing policy restraint remained appropriate. Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee would continue to monitor closely the risks of inflation persistence and would decide the appropriate degree of monetary policy restrictiveness at each meeting.

20: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be reduced by 0.25 percentage points, to 4.75%.

21: Eight members (Andrew Bailey, Sarah Breeden, Swati Dhingra, Megan Greene, Clare Lombardelli, Huw Pill, Dave Ramsden and Alan Taylor) voted in favour of the proposition. Catherine L Mann voted against the proposition, preferring to maintain Bank Rate at 5%.

Operational considerations

22: On 6 November 2024, the stock of UK government bonds held for monetary policy purposes was £655 billion.

23: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

David Roberts was also present on 28 October, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.