Sample Category Title

Dollar Retreats as Markets Stabilize Post-Election; Focus Shifts to BoE and FOMC

Dollar saw a modest pullback in Asian session today, easing off its sharp post-election rally as market enthusiasm stabilized. US equities, including DOW, S&P 500, and NASDAQ, all closed at record highs overnight on strong gains, with DOW particularly outperforming. Meanwhile, 10-year Treasury yield surged to a crucial Fibonacci resistance level that could prove pivotal. The focus now shifts to today’s FOMC rate decision, where Chair Jerome Powell’s stance will be closely scrutinized for indications of rate cuts, especially amid market adjustments following the election outcome.

In the currency markets, Kiwi and Aussie are currently the strongest performers of the day, buoyed by improved risk sentiment. This positive mood was further supported by robust trade data from China, which reported a 12.7% yoy increase in exports for October—the fastest pace in 19 months. The surge is attributed "front-loading" shipments ahead of escalating trade tensions when Donald Trump assumes office. Sterling also showed resilience, with market focusing on BoE rate decision. There is speculation that policy easing might proceed at a slower pace than initially anticipated due to the government's new inflationary budget.

Conversely, Euro is trailing behind, following the greenback as the second weakest currency for the day, with Swiss Franc not far behind. Yen sits in the middle of the pack alongside Loonie. Japan's top currency diplomat, Atsushi Mimura, expressed concern over recent sharp rise in USD/JPY, characterizing the movement as "one-sided and drastic". He indicated that the government is closely monitoring currency developments, including speculative activities, and is prepared to take necessary measures if required. However, it is unclear what possible actions Japan could implement to counter the "one-sided" strength of Dollar.

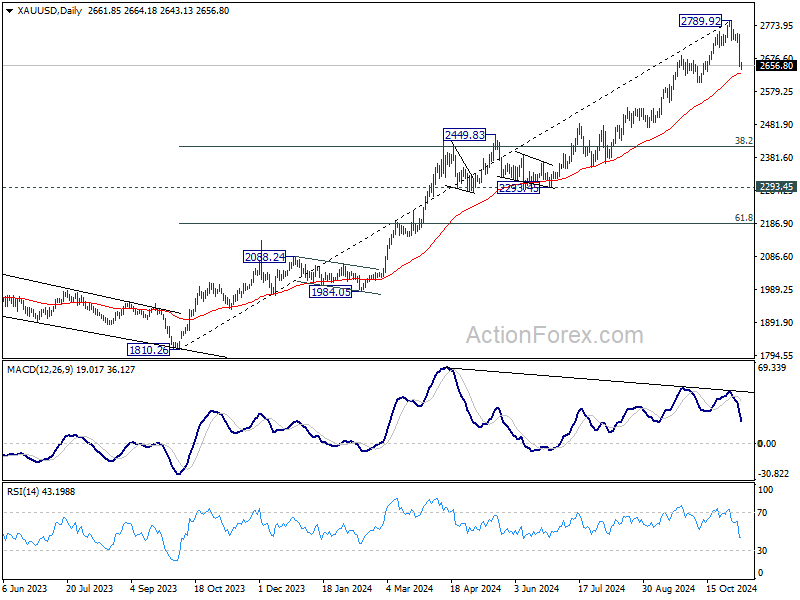

Technically, considering bearish divergence condition in D MACD, Gold might have formed a medium term top at 2789.92 as rise from 1810.26 completed a give wave impulsive move. Firm break of 55 D EMA (now at 2633.42) will strengthen this case, and bring deeper correction to 38.2% retracement of 1810.26 to 2789.92 at 2415.68, which is located inside 2293.45/2449.83 support zone.

In Asia, at the time of writing, Nikkei is down -0.26%. Hong Kong HSI is up 1.43%. China Shanghai SSE is up 1.61%. Singapore Strait Times is up 2.04. Japan 10-year JGB yield is up 0.0314 at 1.012. Overnight, DOW rose 3.57%. S&P 500 rose 2.53%. NASDAQ rose 2.95%. 10-year yield rose 0.137 to 4.426.

Fed rate cut expected with Powell’s tone on inflation in focus

Fed is widely anticipated to announce a 25bps rate cut today, lower the federal funds rate to 4.50%-4.75%. While Fed Chair Jerome Powell is likely to sidestep any definitive remarks about the implications of Donald Trump’s election win, the market will be watching closely for any signs of how Fed might respond to inflationary impacts from new fiscal policies.

Powell's stance on inflation will be particularly scrutinized in light of expected policy shifts under Trump, especially on any indications that Fed is adopting a more vigilant approach toward inflation given that Trump’s policies could drive up spending, which might, in turn, fuel price increases. Any hint of a shift to a more defensive stance against price pressures could influence expectations for the rate path in 2025.

Although fed funds futures still reflect around a 67% probability of another 25 bps cut in December, this is slightly down from over 70% before the election. More importantly, Fed may move more conservatively in 2025, cutting rates only twice to reach a target range of 3.75%-4.00% by mid-year, then pausing for further assessment.

A key development to watch is the 10-year Treasury yield, which has been in a sustained rally since September. After gapping up yesterday, the yield is testing a critical technical level at 61.8% retracement of 4.997 to 3.603 at 4.464. Sustained break there will further solidify the case that correction from 4.997 has completed with three waves down to 3.603. Further rally should then be seen to retest 4.997 high next.

BoE rate cut expected as Reeves’ budget clouds future policy path

BoE is widely anticipated to reduce its benchmark interest rate by 25bps to 4.75% today. While the decision is likely to be unanimous, with known hawk Catherine Mann the only probable dissenting voice. Nevertheless, BoE’s direction for future policy has been complicated by recent domestic and international developments

Governor Andrew Bailey had previously signaled openness to more aggressive policy easing to support the slowing economy. However, after a week spent analyzing Chancellor Rachel Reeves' recent budget—which is considered inflationary—Bailey could revert back to a more measured approach. The budget's emphasis on increased spending could stoke inflationary pressures, limiting the central bank's appetite for rapid rate cuts.

Market expectations have shifted too in response to these developments. Investors are now pricing in between two and three additional 25 basis point cuts by the end of 2025, down from nearly four cuts anticipated before Reeves delivered her budget.

Economists are looking to BoE's new economic projections for clarity on how the central bank plans to navigate these challenges. However, it's uncertain to what extent the forecasts will incorporate the potential inflationary impact of Reeves' fiscal plans. If the projections do not fully account for the new budget measures, market participants may find limited guidance on the BoE's policy outlook, leaving questions about the pace and extent of future rate cuts.

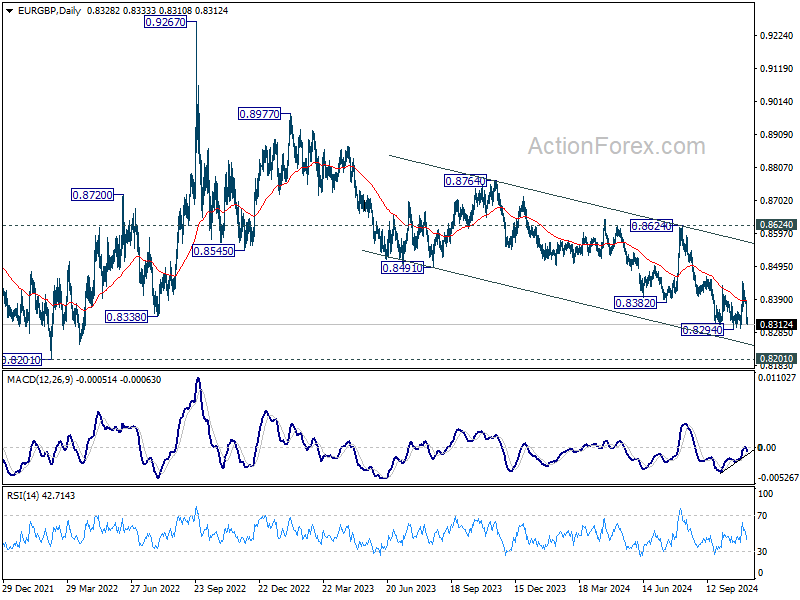

In the currency markets, a key focus today is EUR/GBP's reaction to BoE's decision and communications. The down trend from 0.9267 (2022 high) remains intact. Break of 0.8294 will target 0.8201 support (2022 low). The question is whether this level could provided enough support for EUR/GBP to form a bottom and stage a medium term reversal.

Japan’s real wages dip again in Sep, despite continued nominal wage growth

Japan's real wages declined by -0.1% yoy in September, marking a second consecutive monthly drop as inflation erodes purchasing power. This dip follows a record 26-month downturn that ended in May, with wages briefly turning positive in June and July. However, the fading impact of summer bonuses led to another decline in August.

Nominal wages, reflecting total monthly earnings including base and overtime pay, rose by 2.8% yoy in September, marking the 33rd consecutive month of growth, but missed expectation of 3.0% yoy. When excluding bonuses and unscheduled payments, average wages grew by 2.6% yoy, the highest increase in nearly 32 years. Despite this, overtime pay and allowances declined by -0.4% yoy.

Separately, a Nikkei Research poll indicates optimism among companies for wage increases in the upcoming fiscal year. Approximately 42% of surveyed firms plan to raise wages by 3% to 5% for the fiscal year starting in April 2025, while 9% consider a larger increase of 5% to 7%. However, a significant portion (41%) of companies anticipate more conservative hikes in the range of 1% to 3%, suggesting that while wage pressures may continue, the scope and impact could vary widely across sectors.

RBA's Bullock: Waiting for clear signals before assessing Trump's win

At a Senate session today, RBA Governor Michele Bullock indicated that the central bank has not yet conducted detailed scenario analyses on how Donald Trump's US presidential victory might impact Australia's monetary policy.

Bullock emphasized that the effects could go different directions. She pointed out that while a Trump presidency might be "inflationary in some ways," particularly if it leads to increased global demand or fiscal stimulus, it could also be "deflationary" if China, a key trading partner for Australia, is negatively affected.

Bullock stressed the importance of basing policy decisions on concrete developments rather than speculation. "We cannot be setting policy on the basis of things that could happen or might not happen," she remarked. She added that the central bank intends to "wait and see what actually does happen" before making any adjustments.

As it stands, RBA has not revised its inflation outlook. Bullock reiterated that inflation is expected to return to the target band of 2-3% sustainably by 2026.

ECB’s Villeroy: US election calls for stronger European unity amid rising global risks

French ECB Governing Council member Francois Villeroy de Galhau emphasized the heightened economic risks following the US presidential election results, urging Europe to respond with a united stance.

Speaking at a conference overnight, Villeroy noted, “The result of the American election increases both risks for the global economy and the necessity for Europe to rally together.”

While acknowledging that the specifics of Trump’s policy agenda remain to be seen, Villeroy expressed concerns over the potential for rising deficits and inflation within the US economy, both of which could have broader global consequences.

Villeroy warned that more protectionist measures, such as higher tariffs, could contribute to inflationary pressures domestically in the US while simultaneously straining global economic growth, affecting Europe in particular.

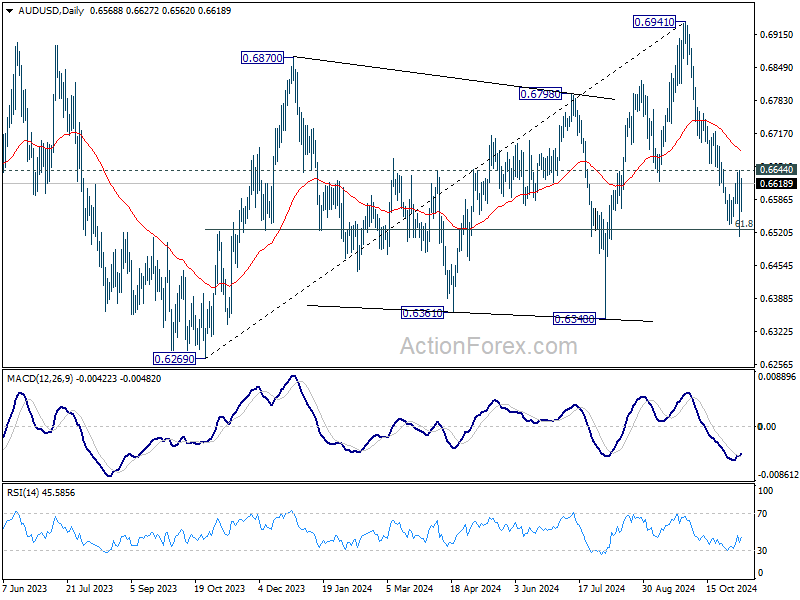

AUD/USD Daily Report

Daily Pivots: (S1) 0.6508; (P) 0.6577; (R1) 0.6640; More...

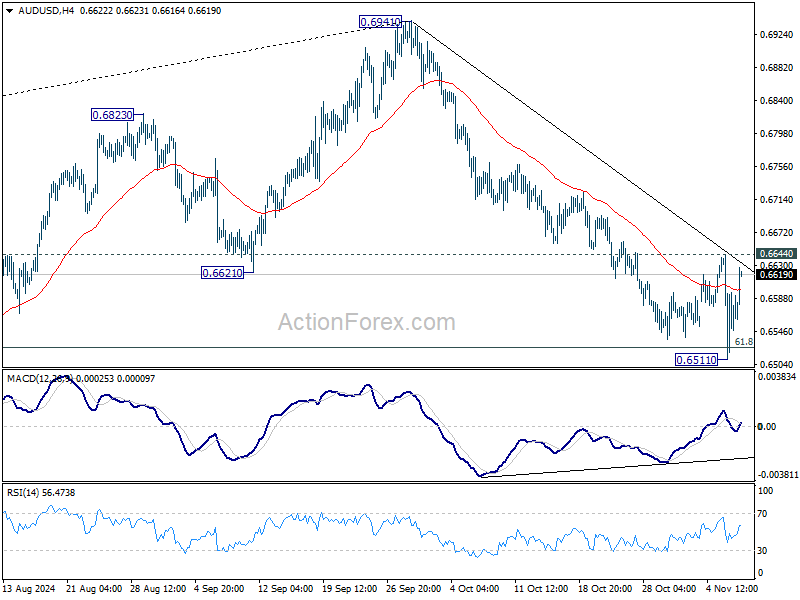

AUD/USD failed to sustain below 61.8% retracement of 0.6269 to 0.6941 at 0.6526 will target 0.6348, and recovered after dipping to 0.6511. Intraday bias is turned neutral again first. Further fall is still expected as long as 0.6644 resistance holds. Firm break of 0.6526 will pave the way to 0.6348 support next. However, considering bullish convergence condition in 4H MACD, break of 0.6644 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 0.6682).

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

Fed rate cut expected with Powell’s tone on inflation in focus

Fed is widely anticipated to announce a 25bps rate cut today, lower the federal funds rate to 4.50%-4.75%. While Fed Chair Jerome Powell is likely to sidestep any definitive remarks about the implications of Donald Trump’s election win, the market will be watching closely for any signs of how Fed might respond to inflationary impacts from new fiscal policies.

Powell's stance on inflation will be particularly scrutinized in light of expected policy shifts under Trump, especially on any indications that Fed is adopting a more vigilant approach toward inflation given that Trump’s policies could drive up spending, which might, in turn, fuel price increases. Any hint of a shift to a more defensive stance against price pressures could influence expectations for the rate path in 2025.

Although fed funds futures still reflect around a 67% probability of another 25 bps cut in December, this is slightly down from over 70% before the election. More importantly, Fed may move more conservatively in 2025, cutting rates only twice to reach a target range of 3.75%-4.00% by mid-year, then pausing for further assessment.

A key development to watch is the 10-year Treasury yield, which has been in a sustained rally since September. After gapping up yesterday, the yield is testing a critical technical level at 61.8% retracement of 4.997 to 3.603 at 4.464. Sustained break there will further solidify the case that correction from 4.997 has completed with three waves down to 3.603. Further rally should then be seen to retest 4.997 high next.

BoE rate cut expected as Reeves’ budget clouds future policy path

BoE is widely anticipated to reduce its benchmark interest rate by 25bps to 4.75% today. While the decision is likely to be unanimous, with known hawk Catherine Mann the only probable dissenting voice. Nevertheless, BoE’s direction for future policy has been complicated by recent domestic and international developments

Governor Andrew Bailey had previously signaled openness to more aggressive policy easing to support the slowing economy. However, after a week spent analyzing Chancellor Rachel Reeves' recent budget—which is considered inflationary—Bailey could revert back to a more measured approach. The budget's emphasis on increased spending could stoke inflationary pressures, limiting the central bank's appetite for rapid rate cuts.

Market expectations have shifted too in response to these developments. Investors are now pricing in between two and three additional 25 basis point cuts by the end of 2025, down from nearly four cuts anticipated before Reeves delivered her budget.

Economists are looking to BoE's new economic projections for clarity on how the central bank plans to navigate these challenges. However, it's uncertain to what extent the forecasts will incorporate the potential inflationary impact of Reeves' fiscal plans. If the projections do not fully account for the new budget measures, market participants may find limited guidance on the BoE's policy outlook, leaving questions about the pace and extent of future rate cuts.

In the currency markets, a key focus today is EUR/GBP's reaction to BoE's decision and communications. The down trend from 0.9267 (2022 high) remains intact. Break of 0.8294 will target 0.8201 support (2022 low). The question is whether this level could provided enough support for EUR/GBP to form a bottom and stage a medium term reversal.

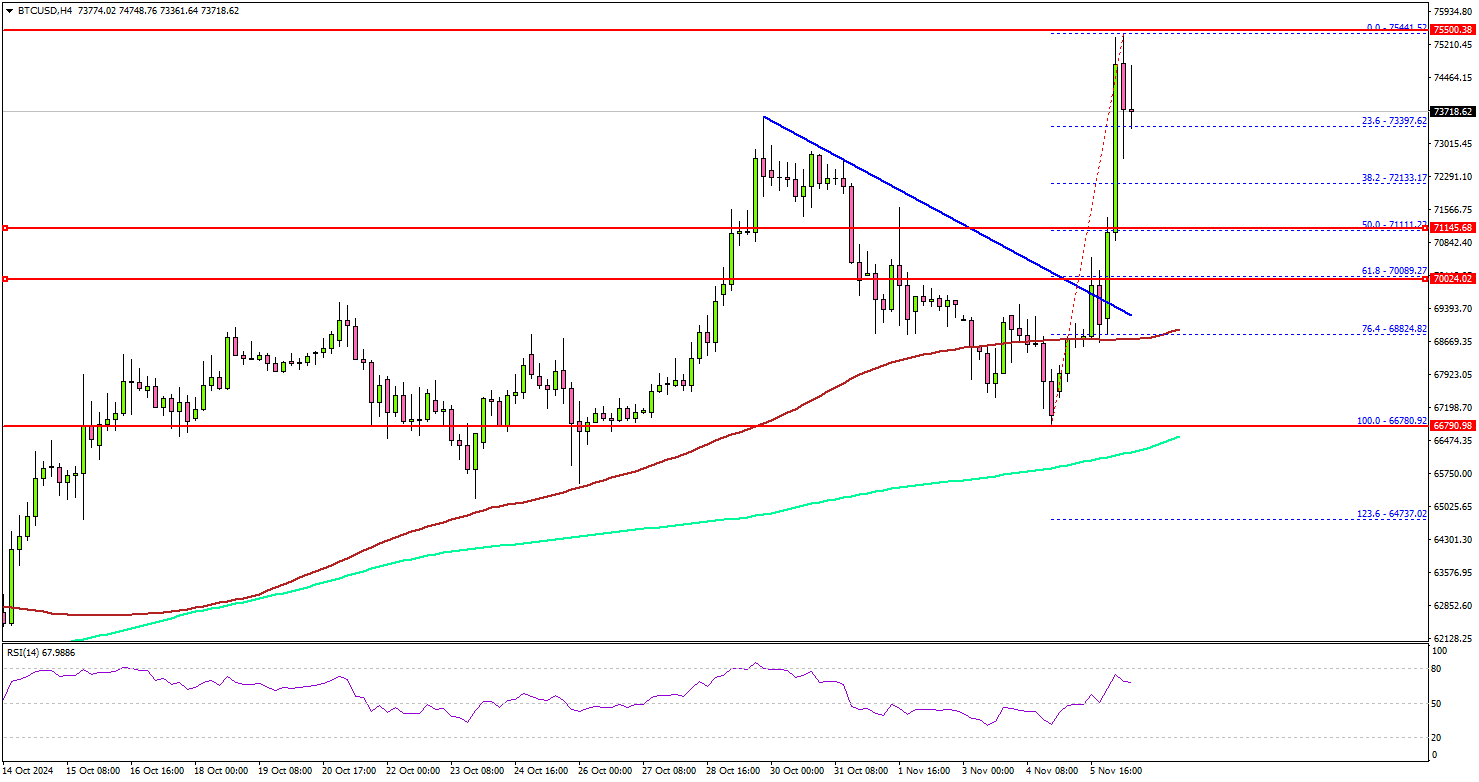

Bitcoin Price Soars To Record Levels Amid Trump’s Presidential Win

Key Highlights

- Bitcoin price started a fresh increase and traded to a new all-time high above $75,000.

- BTC surpassed a major bearish trend line with resistance at $69,200 on the 4-hour chart.

- Gold prices dipped sharply below the $2,720 support zone.

- EUR/USD took a U-turn and traded below the 1.0760 support after Trump’s win.

Bitcoin Price Technical Analysis

Bitcoin price started a fresh increase above the $68,500 resistance zone. BTC/USD cleared the $70,000 and $70,500 levels to move into a positive zone.

Looking at the 4-hour chart, the price surpassed a major bearish trend line with resistance at $69,100. There was a sharp increase during the election result as Donald Trump was elected the 47th president of the United States.

The price even broke the $73,500 barrier and traded to a new record high above $75,000 before it started a consolidation phase. It settled above the $72,000 level, the 200 simple moving average (green, 4 hours), and the 100 simple moving average (red, 4 hours).

On the upside, the price could face resistance near the $75,000 level. The next key resistance is $75,500. A successful close above $75,500 might start another steady increase. In the stated case, the price may perhaps rise toward the $76,800 level or even $78,000.

If not, there might be another downside correction. Immediate support is near the $73,200 level. The next key support sits at $72,500. A downside break below $72,500 might send Bitcoin toward the $71,120 support. Any more losses might send the price toward the $70,000 support zone.

Looking at EUR/USD, the pair saw a lot of bearish moves and the bears push it below the 1.0760 support.

Today’s Economic Releases

- BoE Interest Rate Decision - Forecast 4.75%, versus 5.0% previous.

- US Initial Jobless Claims - Forecast 221K, versus 216K previous.

Japan’s real wages dip again in Sep, despite continued nominal wage growth

Japan's real wages declined by -0.1% yoy in September, marking a second consecutive monthly drop as inflation erodes purchasing power. This dip follows a record 26-month downturn that ended in May, with wages briefly turning positive in June and July. However, the fading impact of summer bonuses led to another decline in August.

Nominal wages, reflecting total monthly earnings including base and overtime pay, rose by 2.8% yoy in September, marking the 33rd consecutive month of growth, but missed expectation of 3.0% yoy. When excluding bonuses and unscheduled payments, average wages grew by 2.6% yoy, the highest increase in nearly 32 years. Despite this, overtime pay and allowances declined by -0.4% yoy.

Separately, a Nikkei Research poll indicates optimism among companies for wage increases in the upcoming fiscal year. Approximately 42% of surveyed firms plan to raise wages by 3% to 5% for the fiscal year starting in April 2025, while 9% consider a larger increase of 5% to 7%. However, a significant portion (41%) of companies anticipate more conservative hikes in the range of 1% to 3%, suggesting that while wage pressures may continue, the scope and impact could vary widely across sectors.

ECB’s Villeroy: US election calls for stronger European unity amid rising global risks

French ECB Governing Council member Francois Villeroy de Galhau emphasized the heightened economic risks following the US presidential election results, urging Europe to respond with a united stance.

Speaking at a conference overnight, Villeroy noted, “The result of the American election increases both risks for the global economy and the necessity for Europe to rally together.”

While acknowledging that the specifics of Trump’s policy agenda remain to be seen, Villeroy expressed concerns over the potential for rising deficits and inflation within the US economy, both of which could have broader global consequences.

Villeroy warned that more protectionist measures, such as higher tariffs, could contribute to inflationary pressures domestically in the US while simultaneously straining global economic growth, affecting Europe in particular.

RBA’s Bullock: Waiting for clear signals before assessing Trump’s win

At a Senate session today, RBA Governor Michele Bullock indicated that the central bank has not yet conducted detailed scenario analyses on how Donald Trump's US presidential victory might impact Australia's monetary policy.

Bullock emphasized that the effects could go different directions. She pointed out that while a Trump presidency might be "inflationary in some ways," particularly if it leads to increased global demand or fiscal stimulus, it could also be "deflationary" if China, a key trading partner for Australia, is negatively affected.

Bullock stressed the importance of basing policy decisions on concrete developments rather than speculation. "We cannot be setting policy on the basis of things that could happen or might not happen," she remarked. She added that the central bank intends to "wait and see what actually does happen" before making any adjustments.

As it stands, RBA has not revised its inflation outlook. Bullock reiterated that inflation is expected to return to the target band of 2-3% sustainably by 2026.

Global Takeaways of the U.S. Election

Summary

In this report, we examine some thematic and global takeaways from the U.S. election. We view a second Trump administration—and more specifically his proposed tariff policies—as a catalyst for further deglobalization and global economic fragmentation. Tariffs could also act as an inflection point for China to approach stimulus efforts differently, while the nature of U.S. involvement in foreign affairs also has scope to take a new path relative to the Biden administration Lastly, we maintain our view for a stronger dollar over the medium term, and believe any attempts from Trump to manufacture dollar weakness will prove to be futile.

Global Takeaways of the U.S. Election

Deglobalization and fragmentation are likely to gather momentum in a Trump 2.0 administration. In our view, Trump winning the White House and having a largely unilateral ability to implement tariffs and shift U.S. trade policy in a more protectionist direction is yet another deglobalization force. During his first administration and over the course of his latest campaign, Trump has been unwavering in his commitment to tariffs. Time will tell how tariff policy ultimately evolves, but as our U.S. economists note in a post-election report, Trump's tariff threats should be taken seriously. Global trade cohesion has suffered since the Global Financial Crisis and deteriorated further as a result of COVID. Erecting new barriers to trade will place additional pressure on the interconnectedness of the global economy, which can have longer-term negative implications for global economic growth, especially if retaliatory tariffs are imposed on the United States. Fragmentation (i.e. countries choosing to strategically align with either the U.S. or China) is a product of deglobalization, and as U.S. trade and broader economic policy becomes more uncertain, strategic alignments could shift back toward China. We observed a noticeable shift in alignment patterns toward China during Trump's first term, driven by countries opting for stronger trade relations with China, participating in China's foreign investment programs and voting in unison with China on geopolitical issues at the United Nations General Assembly. With U.S. trade policy likely to turn more contentious and inward-looking, countries around the world could look to strengthen economic and geopolitical ties with China.

Trump's tariff threats could be China's stimulus inflection point. China's National People’s Congress Standing Committee will meet this week, which was of interest pre-election, but has become more meaningful post-election. Authorities announced fiscal stimulus in September and October, and while details are scarce and likely to be at least partially revealed this week, the old playbook of directing support toward the real estate sector and manufacturing capabilities could now be abandoned. With Trump set to significantly raise new tariffs on China, authorities may take the stance that directing stimulus toward manufacturing could be counterproductive. Trump's proposed global tariff would also diminish China's ability to circumvent U.S. tariffs through proxy nations such as Mexico. Meaning China’s export sector—which has been the primary bright spot of China's economy this year—could face heightened vulnerability under the next Trump administration. Ultimately, the U.S. election could become the tipping point for when authorities' direct fiscal stimulus toward stimulating domestic demand and having household consumption play a larger role in the economy. Authorities have warned against China moving toward “welfarism” and not wanting to offer “Western style” fiscal stimulus, especially when the public sector balance sheet is already over leveraged. While we do not believe Chinese authorities will deliver fiscal stimulus to spark domestic consumption this week or in the immediate-term, authorities could look at the U.S. election as the catalyst for adjusting how China approaches stimulus efforts over the longer term. Without a shift in stimulus thinking—away from real estate and manufacturing—China's economy could slow more rapidly than we currently expect, placing risks to global and developing economy growth squarely to the downside.

U.S. approach to foreign policy is likely to become more transactional. With hot wars on two continents, and cold wars taking shape globally—with most indirectly or directly involving the U.S.—we expect Trump to maintain the United States' posture of having a role in foreign affairs; however, the nature of the U.S. role may change relative to the Biden administration. Trump has signaled a willingness to negotiate with both President Putin and President Zelensky to end the conflict. Could Trump use Ukraine's military vulnerabilities and Russia's sanctioned economy as means toward a peace deal? In the Middle East, Trump has pointed to the Abraham Accords—finalized during his first administration—as evidence of his ability to maintain security in the region and normalize relations between Israel and select Arab nations. At the same time, Trump has stated his unwavering support for Israel and an intention to revert to maximum pressure policy on Iran. Can Trump reset geopolitical relations in the Middle East again with another “deal”? Trump has also questioned the United States' commitment to NATO as well as defending Taiwan from any potential invasion attempt by China unless European Nations and Taiwan pay a larger financial cost for defense arrangements. Would Trump abandon NATO allies and Taiwan if financial benefits do not present themselves? Point being, U.S. involvement in foreign affairs will likely become transactional and negotiable going forward. We fully believe Trump's overall aim is worldwide peace, but how peace is potentially achieved seems likely to change.

Trump will not be able to manufacture dollar depreciation. In our October International Economic Outlook, we noted how a Trump White House would lead us to become more positive on the U.S. dollar. Now that Trump has indeed won the election, we reinforce our view for a strong dollar over the course of 2025 and into 2026, and will become more positive on the dollar outlook in our next forecast update. As far as the dynamics surrounding a more constructive dollar view, in their post-election report, our U.S. economics colleagues noted the extension and possible expansion of the expiring provision of the Tax Cuts and Jobs Act (TCJA) in addition to the likelihood of higher tariffs. Over the next few years, tariffs and looser fiscal policy could lead to higher U.S. inflation, and through reduced purchasing power of U.S. consumers and businesses, could also contribute to slower U.S. growth. With the Federal Reserve potentially cautious about the overall inflationary implications of the new administration's policies, the U.S. central bank may lower interest rates more gradually than we currently expect. While there may also be some influence on foreign central bank monetary policy, we think the impact would be far more limited. Slower U.S. growth and tariffs would likely spillover to foreign economies, placing both growth and interest rate differentials in favor of the U.S. dollar over the longer-term. Sporadic bouts of markets volatility could also provide the dollar with safe haven tail-winds over the next 18 months. Also, despite any rhetoric aimed at weakening the dollar, Trump will be unable to influence the long-term direction of the dollar. In our view, Trump's preference for a weaker dollar would have to be accommodated by and in coordination with the Federal Reserve, which we view as unlikely. We view the Fed as a monetary authority that is unlikely to pursue a weaker dollar at the direction of the President nor have its independence questioned by global financial markets.

Markets Brace For Higher Inflation and Interest Rates Under President Trump

Summary of Election Results & Financial Market Reaction

As of 11 AM ET, Donald Trump has secured 277 of the 538 Electoral College votes, becoming the 47th president. While ballots are still being counted, President Trump also looks to have won the popular vote, which has not happened for a Republican president since George W. Bush in 2004.

The Republicans have also taken control of the Senate, securing 52 of the 100 seats. Six seats are still up for grabs, so there’s potential for the Republicans to gain a bit more ground in the Senate once the final votes are counted. Either way, a GOP controlled upper chamber will make it much easier for President Trump to make key appointments requiring Senate approval.

Meanwhile, control of the House of Representatives remains up in the air, with 57 seats still to be called. As of the time of writing, the Associated Press is showing that the Republicans have secured 198 of the required 218 votes. However, it is possible that the final outcome of the House isn’t known for a few days, leaving some ambiguity on how much of Trump’s agenda will be implemented, since Congressional approval is required for tax or spending changes.

Financial markets responded swiftly, extending the moves seen right before the election. The S&P 500 is up by nearly 2% today. Bond yields are also rising, with the U.S. 10-year Treasury up 17 bps this morning. Fed funds futures for the remainder of 2024 are relatively unchanged, still pointing to a 25 bp cut tomorrow and a near 70% chance of another 25-bps cut in December. Further out, pricing has shifted higher by nearly 20 bps, implying that markets are expecting the combination of tax cuts and tariffs raising the Fed’s neutral rate. Importantly, we aren’t seeing much in the way of rising U.S. debt risk premia, which was feared to rise with potentially wider fiscal deficits. The U.S. dollar has continued to gain ground against most of its peers, with the trade-weighted measure up nearly 2% this morning (Chart 1). Most of the gains are coming against the Mexican peso and euro (both down around 2%).

We are changing our forecast for the Fed, as higher inflation results in a slower pace of rate cuts in 2025. We now have the Fed cutting by 25 bps tomorrow, in December, and in January, but then pausing in March. The Fed will continue with a cut-pause-cut pace through 2025, resulting in a higher fed funds rate at the end of 2025 of 3.5%, up from 3.0%. In H1 2026, we have the Fed cutting to 3.0%, implying that we don’t see any change to the neutral rate, just that the Fed gets there later.

In the Event Republicans Also Win the House…

We expect Congressional Republicans to provide some degree of fiscal check on President Trump, limiting passage of the full $10 trillion worth of tax cuts he floated in the campaign.

Chart 1 shows a second Trump presidency has extended Trump trade

- It is likely Trump can extend much, if not all, of the 2017 Tax Cuts and Jobs Act (TCJA) measures set to expire at the end of 2025. The cost of this is around $4.5 trillion. Should the Republicans end up with a narrow majority in the Senate, the GOP will likely need to use reconciliation, setting up another expiry showdown at a future date. Lastly, extending TCJA avoids fiscal tightening rather than expanding fiscal accommodation. Because our forecast assumes status quo on current policy, even a full extension of TCJA is unlikely to add further upside to the outlook.

- Expensive promises like repealing the cap on the state and local tax (SALT) deduction, eliminating tax on social security benefits and overtime pay as well as reducing the corporate tax rate for domestic manufacturers are less likely to be passed, but cannot be completely ruled out.

Trump has also said he would eliminate many of the clean energy tax credits built into the 2022 Inflation Reduction Act (IRA). There is less clarity on whether these efforts will meet success given that 75% of the investments from the IRA have flowed to Republican-held states and repealing the IRA would require approval from Congress.

However, when it comes to tariffs, the President can act more independently. Some version of this promise will be kept. Trump has proposed a universal 10% tariff on all countries exporting to the U.S., and a 60% tariff on China to help pay for the tax cuts proposed above. However, even with the potential added revenue, the federal deficit would still grow by another $7 trillion over the next decade (assuming Trump’s full suite of tax promises are implemented). If only TCJA were extended, but the full suite of tariffs was still imposed, the deficit trajectory would worsen relative to the CBO’s current baseline, but by far less than the alternative scenario (Chart 2).

From a legal standpoint, it appears that President Trump has the authority to implement tariffs as he sees fit. In 2018, Trump used Section 232 of the Trade Expansion Act of 1962 to implement broad steel and aluminum tariffs, only to reduce/eliminate the tariffs through negotiations with some countries. Similarly, Trump used section 301 of the Trade Act of 1974 to leverage tariffs on China and the European Union.

- In his second term, Trump will likely invoke the International Emergency Economic Powers Act (IIEPA), which will allow for faster and more expansive power to leverage tariffs. We suspect Trump is likely to move quickly on implementing the tariffs.

- The big question is whether some countries get specific carve-outs. An obvious example would be Canada and Mexico, who are technically both covered under an existing trade agreement (US-Mexico-Canda Trade Agreement) that was signed into law under the prior Trump administration. One possibility is that Canada/Mexico would remain insulated from tariffs, so long as they follow the U.S.’s lead and leverage similar tariffs on China.

- For China, Trump is likely to repeal the Permanent Normal Trade Relations (PNTR), which was passed after China joined the WTO in 2001, leading to a vast reduction in tariffs. Repealing PNTR would result in current Chinese tariffs increase from 19% to 61%. This will require approval from Congress.

- Assuming full implementation of the Trump tariffs in early-2025, our estimates suggest that the twelve-month change on core PCE inflation could be higher by 50-100 bps by the end of next year relative to our current baseline where inflation is assumed to have returned to 2%.

In the event of a full and simultaneous implementation of Trump’s policy proposals, our analysis suggests that the drag on economic growth, when combined with tighter border security and the potential deportation of a million immigrants, would more than offset the growth-impulse from the tax cuts.

- This would leave the American economy on a weaker growth trajectory, with structurally higher deficits, inflation, and interest rates.

- This is not a combination any new administration wants, which is why many analysts believe there will be a broader tactical approach on tariffs to create some space for negotiation that pressures parties to the table in a swift and effective manner.

- Estimates vary, but most suggest that for each percentage point increase in the deficit (measured as a share of GDP), it can add anywhere from 15-30 bps to longer-term yields. Some of that increase has already been priced into Treasury yields in recent weeks, but there’s probably a bit more room for yields to climb.

We will be closely watching how markets respond over the coming days. From past experience, Trump’s rhetoric and policies are likely to inject uncertainty into financial markets, but a lot depends on whether polices threaten the current soft-landing of the economy.

In the Event Democrats Win the House …

A divided Congress entirely rules out many of Trump’s promised tax cuts, with an extension of TCJA likely being the one exception:

- However, Democrats will likely require some concessions from Republicans, which could come in the form of bringing back the expanded child tax credit and/or further extending the Affordable Care Act premium tax credits that are set to expire at the end of 2025.

- Both of these would add to the deficit. The Committee for a Responsible Federal Budget estimates that reverting the CTC to $3,600 would cost north of $1 trillion over the next decade, while extending the ACA premium tax credits would cost $400 billion.

Trump would also have executive power to tighten border security, largely through reinstating his 2019 “remain in Mexico program” and Title 42 policy, which allowed U.S. border authorities to quickly deport migrants crossing the Mexico border before being able to claim asylum. These measures would result in lower immigration numbers over the coming years, with net immigration likely falling closer to 2019 levels of ~500,000 per-year or roughly a quarter of this year’s expected gain.

- However, it is highly unlikely that Trump would be able to implement “mass deportations” as it would require significant government funding which would ultimately require approval from Congress.

On tariffs, Trump is likely to take a more measured approach. We suspect that he’ll remain “tough on China” but soften his stance on allies and close trading partners. This would be closer to what played out under the prior Trump administration, where allies such as Canada, Mexico, United Kingdom and the European Union were all able to make concessions.

Lastly, the suspended debt ceiling – negotiated as part the 2023 Fiscal Responsibility Act – is set to expire on January 1st, 2025. Under a divided Congress, this is likely to bring some fireworks as it’s highly unlikely that a resolution will be reached before the deadline, particularly given that any increase in the debt ceiling is likely to be tied to TCJA negotiations. This means the Treasury will again have to resort to “extraordinary measures” to keep the government financed through early-2025. Estimates suggests that the Treasury can likely buy Congress several more months to negotiate a deal, though the closer the U.S. gets to the “X-date” the more volatility this is likely to inject across global financial markets.

Implications for Canada

The nail biting is over, and now the concern is real. Since the USMCA trade agreement came into effect in 2020, trade between Canada, the U.S. and Mexico has flourished. Canada enjoys a healthy goods trade surplus with the U.S. at over 7% of GDP, mainly led by energy exports. The small surplus in exports outside of energy has also been on the rise since the implementation of the USMCA.

Our research shows that a full-scale implementation of Trump’s 10% tariff plan could lead to a near-5% reduction in Canadian export volumes to the U.S. by early-2027, relative to our current baseline forecast. Retaliation by Canada would increase costs for domestic producers, and push import volumes lower in the process.

Slowing import activity mitigates some of the negative net trade impact on total GDP that helps avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026.

The hit to growth could force the Bank of Canada to cut interest rates by about 50–75 basis points more than we currently forecast, widening the spread to U.S. rates and putting additional downward pressure on the Canadian dollar. It would not surprise us to see the loonie break below 70 cents. The CAD is currently down around 1% this morning, to 71 U.S. cents, while BoC pricing is lower by just a few bps. Given that the Canada 10-year is up over 10 bps this morning, it implies that investors are baking in a risk premia to Canadian debt.

Tariffs create a negative income hit to Canadians as they pay more for imports, which would feed into a temporary and modest re-acceleration of inflation to the 2.5–3.0% y/y range before reverting back to the Bank of Canada’s (BoC) 2% target by 2026.

The auto sector would face the deepest negative impacts. The automotive supply chain is one of the most integrated and hardest to diversify away from, evidenced by the almost 20% of intermediary goods inputs that are sourced from the U.S. alone. Outside of autos, the energy sector, chemical/plastic/rubbers manufacturing, forestry products, and machinery have outsized exposure to the U.S. market. The metal ores and non-metallic minerals industries and agriculture sector are a little more insulated as only 25% and 50% of the industries’ exports, respectively, end up in the U.S.

Could Markets Relive 2016 Post-Election Day Performance?

- Euro/dollar could suffer if 2016 repeats itself

- US stocks could further benefit from Trump’s win

- Gold and bitcoin might move in opposite direction

- Euro/dollar volatility could rise further

Trump wins a second term

Former President Trump has won the 2024 presidential election, achieving a noticeable comeback following the 2020 defeat. The market reaction has been mostly within expectations, with the dollar gaining across the board, gold suffering and bitcoin enjoying strong gains.

While market participants are gradually turning their focus to the Fed meeting for any hints on the rate outlook after Thursday’s gathering, it is worth examining the performance of key market assets from election day until year-end in election years since 2000.

Euro/dollar could drop further towards year-end

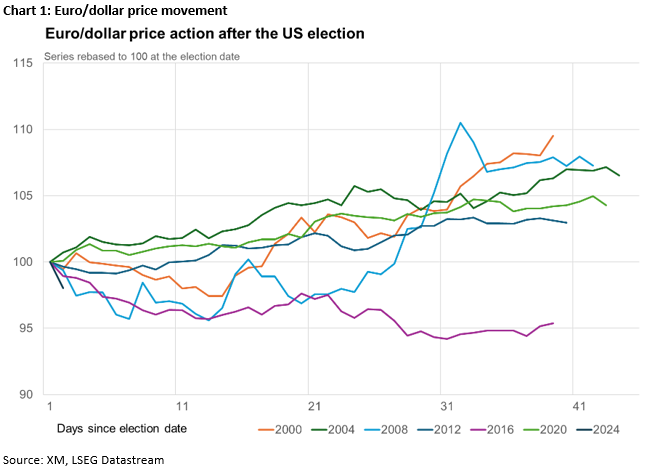

Chart 1 below depicts euro/dollar’s past performance. This pair finished the year in positive territory in every post-election period examined since 2000, with one exception. In 2016, euro/dollar sold off aggressively, finishing the year around 4.5% lower compared to the election date, as Trump’s pro-America agenda boosted the dollar.

S&P 500 historical performance is mixed

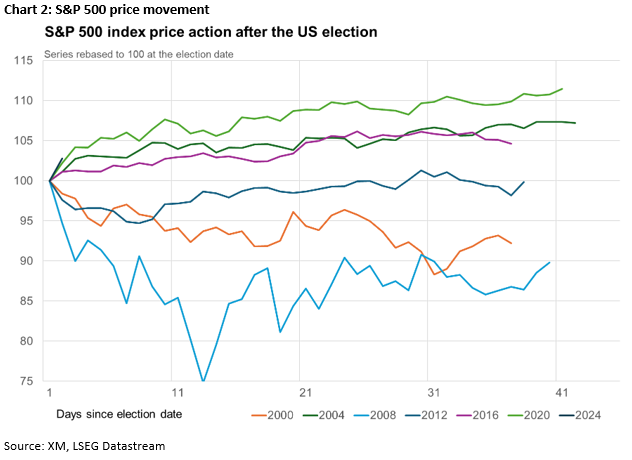

As seen in chart 2 below, the performance of the S&P 500 index after election day has been mixed. However, focusing on 2016, the world’s largest stock index finished the election year around 4.5% higher, partly supported by the customary Santa Rally.

Russell 2000 index could benefit the most

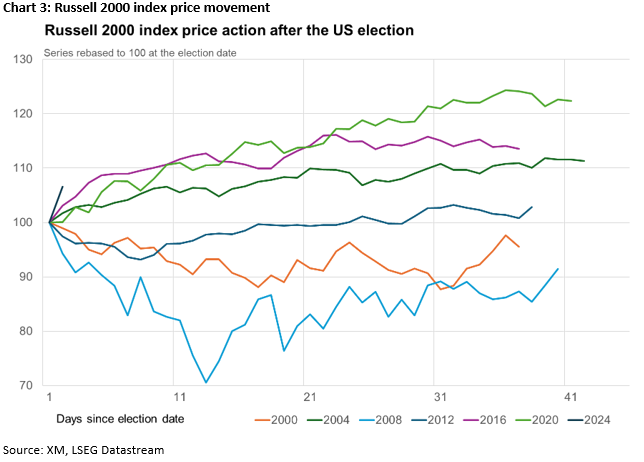

Trump’s “America first” agenda is expected to benefit small- and medium-sized US-based corporates. In 2016, this positive sentiment persisted in the post-election day period, with the index finishing the year around 13% higher compared to the election day close. In this context, the Russell 2000 index, which encapsulated small-cap stocks, is expected to perform well today.

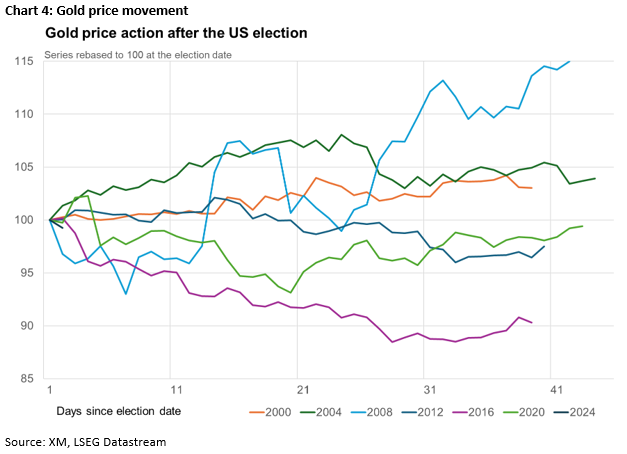

Gold could suffer further into year-end

Similarly to the S&P 500 index, gold’s performance after election day since 2000 has been mixed, with the precious metal rallying significantly in 2008 but suffering in 2016. Since Trump was first elected in 2016, a possible repeat of that performance could mean that gold could drop towards the $2,500 area.

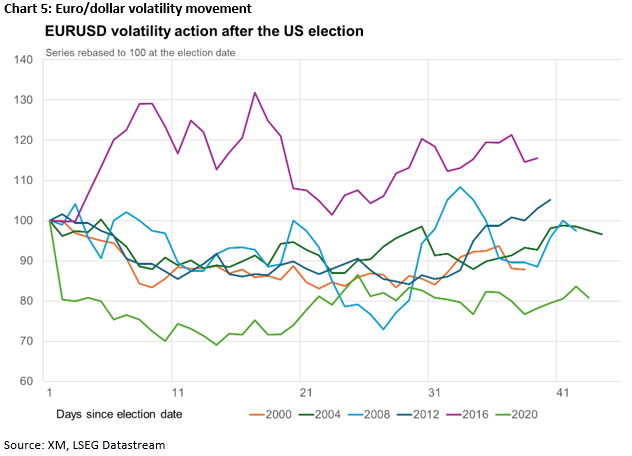

Stocks’ volatility could ease while euro/dollar volatility could rise further

The pre-US election day period is traditionally characterized by increased market volatility. Based on historical analysis, the VIX index tends to drop aggressively after election day, with 2008 being the exception as the 2007-2008 financial crisis was unfolding. In 2016, VIX dropped aggressively, ending the year around 25% lower compared to election day.

On the flip side, as seen in Chart 5 below, euro/dollar volatility has historically eased in the post-election day period. The only time that volatility remained high and experienced a strong rally was in 2016, when Trump was first elected.

Putting everything together, the performance by key market assets after the 2016 election could serve as a guide to what the future might hold. We could indeed see euro/dollar drop, US stocks rally and gold suffer, but past performance does not guarantee future results. Particularly in a period with two active conflicts, in Ukraine and the Middle East, and China struggling to fix its housing sector issues.