Sample Category Title

Week Ahead – A Decisive Week for USD with NFP and More; BoJ Meets

- A crucial week lies ahead with US jobs report, advance GDP and PCE inflation

- The Bank of Japan is expected to hold rates, but will it flag a year-end hike?

- Flash GDP and CPI data for the euro area are also hotly anticipated

- Australian quarterly CPI and UK budget on the agenda too

All eyes on US data as Fed turns hawkish again

The Federal Reserve’s surprise decision in September to cut rates by a larger-than-expected 50-basis-points seems like a distant memory now, as policymakers are once again sending out hawkish soundbites.

US economic indicators since the September meeting have been on the strong side, including the CPI report, with Fed officials cautioning that another 50-bps cut is unlikely in the near term. The sudden switch in the narrative from ‘hard landing’ to ‘soft landing’, or possibly even a ‘no landing’, has spurred a sharp reversal in Treasury yields, which in turn has pushed the US dollar higher.

With the Fed’s November policy decision fast approaching, next week’s data will serve as a timely update on the strength of the US economy as well as on inflation.

Slowdown, what slowdown?

Kicking things off are the October consumer confidence index and the JOLTS job openings for September on Tuesday. But the top-tier releases do not start until Wednesday when the first estimate of third quarter GDP is due.

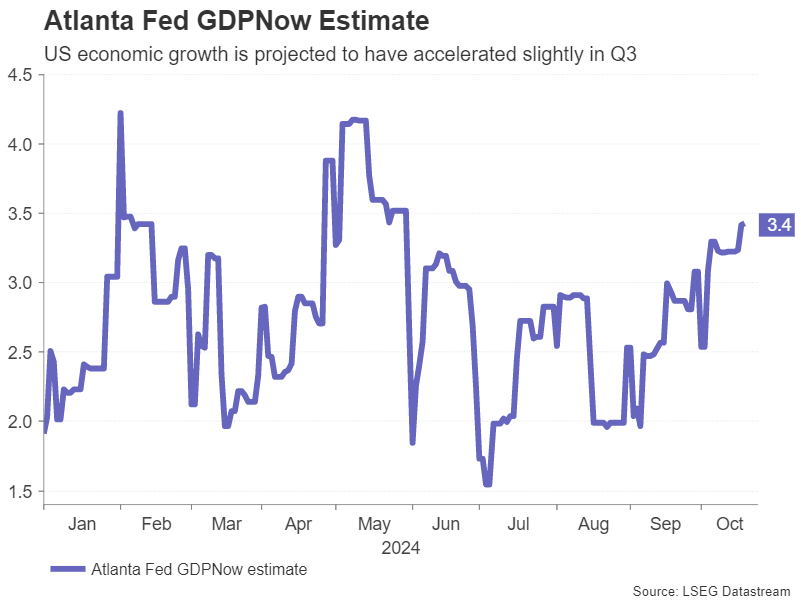

The US economy is expected to have expanded by an annualized rate of 3.0% in Q3, the same pace as in Q2. Not only is this above average growth but an upside surprise is more likely than a downside one as the Atlanta Fed’s GDPNow model puts the estimate at 3.4%.

Other data on Wednesday will include the ADP private employment report, which will provide an early glimpse into the labour market, and pending home sales.

Spotlight on PCE inflation after mixed CPI

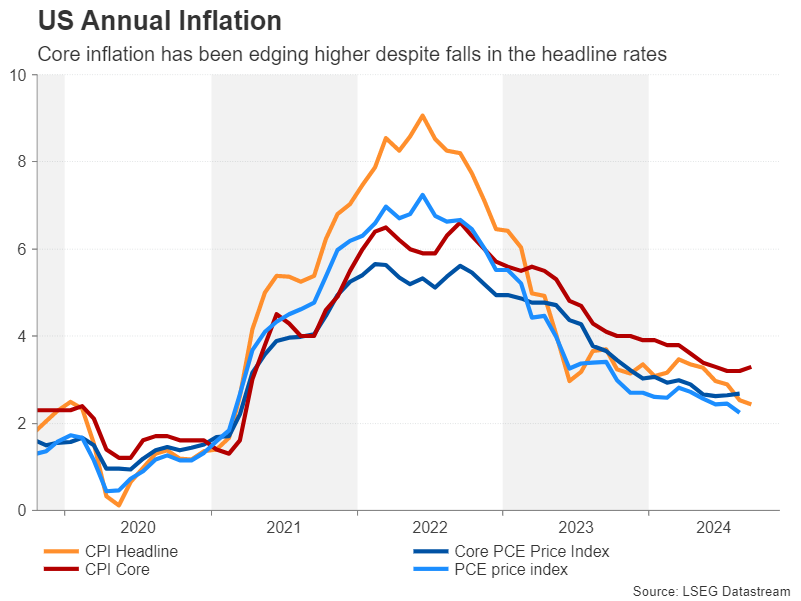

Both the CPI and PCE measures of inflation show a divergence between the headline and core readings. The core PCE price index, which the Fed puts the most weight on in its decision making, ticked up to 2.7% y/y in August even as headline PCE eased to 2.2%. It’s likely that both prints stayed unchanged in September or fell slightly. Hence, the inflation numbers may not be particularly helpful for the Fed or investors.

Still, the personal income and consumption figures due the same day will offer additional clues for policymakers, while October Challenger Layoffs and the quarterly employment cost will be watched too.

NFP report may hold the cards

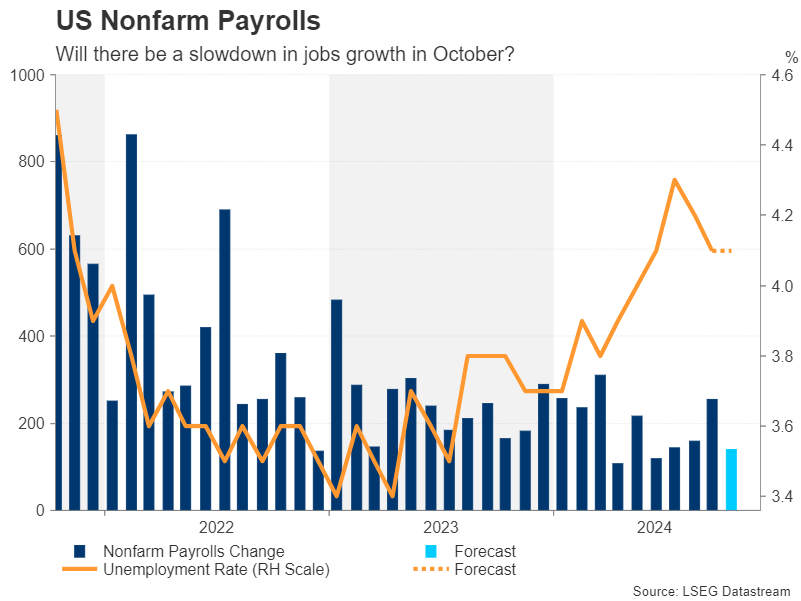

Finally on Friday, the week’s highlight – the October nonfarm payrolls report – will come to the fore. After a solid 254k rise in September, it’s projected that the US labour market created 140k new jobs in October, signalling a marked slowdown. Nevertheless, the unemployment rate is expected to have held at 4.1%, while average hourly earnings are forecast to have moderated slightly from 0.4% to 0.3% m/m.

Also important will be the ISM manufacturing PMI, which is expected to improve from 47.2 to 47.6 in October. With the Fed now more worried about the jobs market than inflation, soft payrolls could set the tone back to a more dovish one.

Can the US dollar extend its rebound?

Moreover, any signs that the American economy is cooling is likely to push up market bets of back-to-back rate cuts for the next few meetings. However, if growth remains robust and more significantly, PCE inflation points to some stickiness, rate cut bets will probably suffer a further blow.

At the moment, only one additional 25-bps reduction is fully priced in for 2024. If a rate cut in November starts to come into doubt, the US dollar could climb to fresh highs but stocks on Wall Street would probably come under selling pressure.

For the latter, however, a busy earnings week might keep the positive momentum going if results from Microsoft, Apple and Amazon.com don’t disappoint.

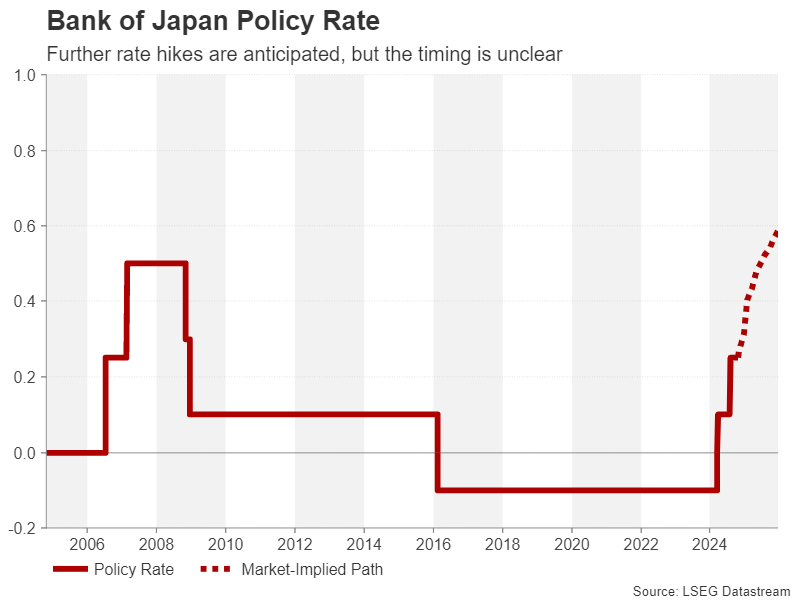

Bank of Japan expected to stand pat

Twenty twenty-four was a turning point for the Bank of Japan’s decades-long fight against deflation. The BoJ abandoned its yield-curve control policy, halved its bond purchases, and raised borrowing costs twice, ending its policy of negative interest rates.

However, despite policymakers’ clear intention to continue the normalization of monetary policy and raise rates even higher, inflation appears to be settling around the BoJ’s 2.0% target, lessening the need for further tightening. The most recent commentary from Governor Ueda and other board members suggests a rate hike is not forthcoming on Thursday when the Bank announces its October decision.

But the updated outlook report with a fresh set of projections on inflation and growth should be quite insightful on the likelihood of a rate hike in December or during the first few months of 2025.

In the absence of any hints about a rate hike anytime soon, the yen will probably continue to struggle against the US dollar. Yet, a renewed weakness in the yen will only incentivize policymakers to hike sooner rather than later and this is a risk investors may be overlooking.

Also on the Japanese schedule are preliminary industrial output figures and retail sales figures for September, both due on Thursday.

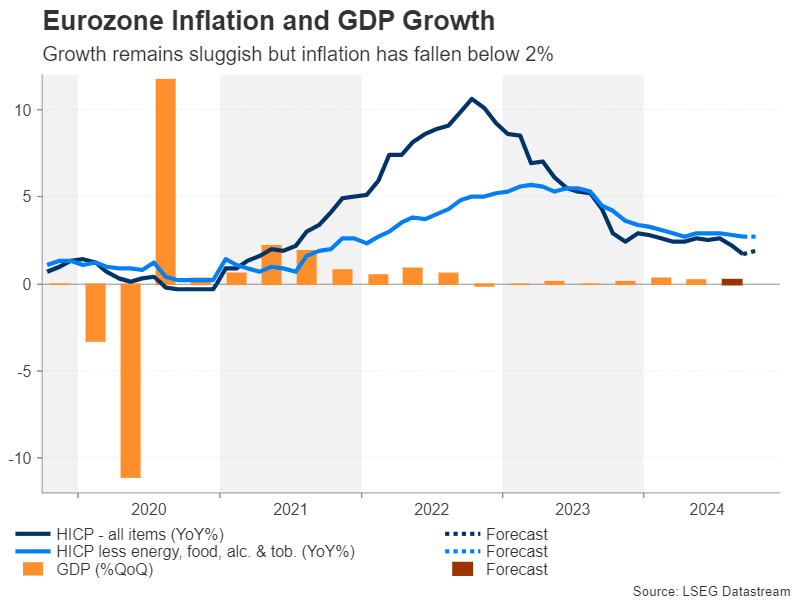

Euro awaits flash GDP and CPI

The euro’s double top pattern against the greenback did not let down technical analysis enthusiasts and the pair recently brushed 16-week lows, falling below $1.08. Next week’s releases are unlikely to be of much help to the bulls.

The flash estimate of GDP out on Wednesday is expected to show that the Eurozone economy eked out growth of just 0.2% q/q in the third quarter. On Thursday, attention will turn to the flash CPI readings. The headline rate probably edged up from 1.7% to 1.9% y/y in October, but the ECB is already forecasting a pickup in the coming months.

Nevertheless, stronger-than-expected data could provide the euro with some short-term relief following four consecutive weeks of losses. Alternatively, if the numbers disappoint, investors are sure to ramp up their bets of a 50-bps cut by the ECB in December.

Pound looking shaky ahead of UK budget

It hasn’t been the best of times for sterling either lately, despite the Bank of England being one of the more hawkish central banks at the moment. The pound has lost grip of the $1.30 handle, and there could be more downside on Wednesday when the UK Chancellor of the Exchequer Rachel Reeves announces the new Labour government’s first budget.

The UK press has gone into overdrive with its coverage of the budget and all indications are that Reeves will unveil tax increases of £40 billion, raising the tax burden to the highest since 1948. Whilst this may not be good news for taxpayers, BoE policymakers might welcome it, as tighter fiscal policy will dampen demand in the economy, paving the way for faster rate reductions.

The pound is at risk of slipping further from a deficit-reducing budget. Even if there are some growth boosting policies included, they are likely to be longer-term measures and not get in the way of the BoE cutting rates. Yet, there might be some support for sterling if investors take note of the fact that the UK government is focusing on long term investments and keeping the deficit in check rather than on short-term sweeteners for voters that push up borrowing.

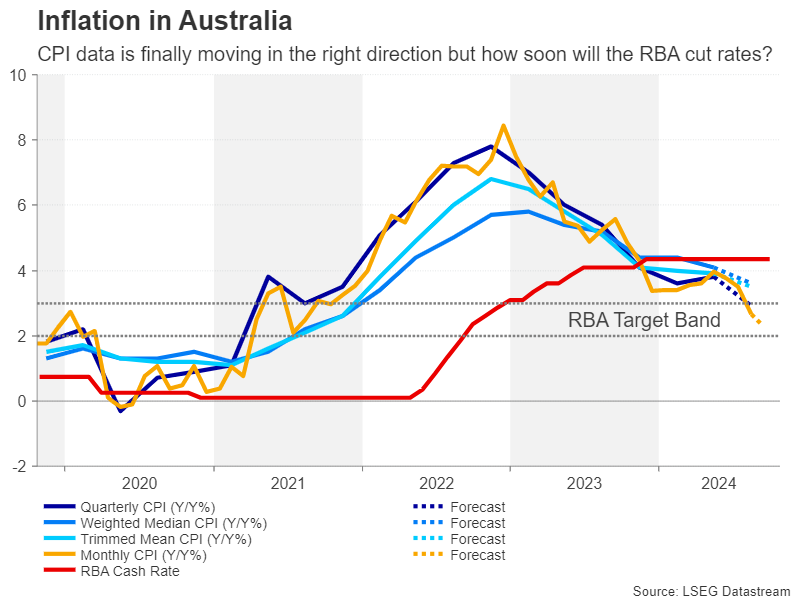

Australian CPI eyed as RBA decision looms

Finally, traders will be watching CPI stats out of Australia on Wednesday as the Reserve Bank of Australia maintains a neutral stance on rates. After edging up earlier in the year, inflation in Australia finally started moving in the right direction over the summer. The monthly print fell to 2.6% y/y in August, hitting the RBA’s 2-3% target band for the first time since 2021.

The quarterly data, which is deemed more accurate, is bound to form the basis of discussion for the November 5 meeting. However, even if there is more good progress in bringing inflation down, particularly in the trimmed and weighted mean measures, the RBA is likely to remain cautious for now and at best, begin the debate of when to start cutting rates.

But for the Australian dollar, a hawkish RBA may only go so far in coming to the aussie’s aid if broader market risk sentiment remains fragile and the US dollar stays strong. In addition to domestic data, aussie traders will also be monitoring China’s October PMIs out on Thursday and Friday.

Weekly Focus – Stagnant Euro Area Economy Supports Gradual Easing

The dollar continued its October rally, and yields edged higher this week. The moves reversed somewhat by the end of the week, as investors maybe questioning the sustainability of the recent sharp rise in US rates. Oil prices retraced some of the decline from recent weeks which weighs on energy-importing currencies such as euro and yen. The latter has been the big loser in October in general amid the moderation in the Fed pricing as US recession fears have been placed on the back burner.

The modest growth trajectory in the euro area continues with the October composite PMI at 49.7 on the back of a weaker-than-expected service sector and a stronger-than-expected manufacturing sector. Interestingly, German and French employment indices are now below 50 in the service sector for the first time in four years. That said, the two dominating economies are also the weak links in the euro area. The French service sector in particular pulled activity lower, but since we compare to a September with Paralympics in Paris, the world's third largest sporting event, we think markets should have been less surprised by the weak service print. German data was better than expected with a reaccelerating service sector and manufacturing increasing from very low levels. Ifo data also confirmed the encouraging German signs with both the current assessment and expectations moving higher, although from very low levels.

Largely the data aims with gradual ECB easing as we see it. That said, it does not keep investors from pricing in a growing probability of a jumbo cut in December and even a hawk such as Dutch governing council member Klaas Knot would not rule it out when speaking this week.

The coming week will be eventful. In the euro area, we will look out for inflation and Q3 GDP. In the former, gauging service price momentum will be key following a marked slowdown in September. We suspect it was mainly a blip and expect service price momentum to pick up again. We expect 0.2% Q3 GDP-growth supported by Southern Europe and the Olympic Games in France.

We also get a fan of key data releases from the US. On the labour market, we will look out for the number of job openings in the JOLTS report, which is an important measure of labour demand for the Fed. We think nonfarm payrolls growth slowed down to 130k (Sep: 254k) both due to weather-related distortions and less favourable seasonal adjustment. We expect Q3 GDP-growth of 2.5% on annualized Q/Q basis (Q2: 3.0%).

In Japan, we will keep an eye on the general election on Sunday. Polls have indicated the ruling coalition is in danger of losing its Lower House majority. This could compromise the backing for further rate hikes from the Bank of Japan (BoJ). That said, the largest opposition party, which has refused to enter the coalition, has a more hawkish stance on monetary policies, so the consequences for potential rate hikes down the line are not clear. We still look for another rate hike in December or January, but we expect the BoJ to stay on hold on Thursday.

Sunset Market Commentary

Markets

German Bunds underperformed US Treasuries today. Yields added between up to 2.2 bps, the front end of the curve taking the lead. Yesterday’s PMI’s didn’t deliver a similar September-shocker and even offered a glimpse of hope for the battered German economy. That led some of the more hawkish ECB policymakers to come out of the shadows and push back against building market expectations for a 50 bps cut in December. Kazaks (“markets shouldn’t run ahead of themselves”), Muller (“best policy choice is measured rate cuts”), Wunsch (“don’t need a discussion on 50 bps at this stage”) and Simkus (“don’t see case for 50 bps cut”) all hit the wires. US yields ease a few basis points but remain on track for weekly gains from 6 (30-yr) to 12 bps (3, 5-yr). The euro ekes out a tiny gain on improving interest rate differentials in technically insignificant trading (EUR/USD 1.084). The trade-weighted dollar index eases few ticks and is testing the 104 big figure. EUR/GBP steadies around 0.834. The eco calendar contained US September durable goods data. The headline figure eased -0.8%, less than the expected -1% but came after the August number was revised down from flat to -0.8%. Core gauges beat estimates but a key one, shipments, missed the bar by unexpectedly dropping 0.3% m/m. The latter is a proxy for investments in GDP and is probably the reason why we’ve seen some intraday (yield) jitters: markets are headed towards an important eco calendar next week with the US, amongst others, publishing the first estimate of third-quarter GDP growth on Wednesday. Estimates are for a solid 3% q/q (annualized), matching the previous quarter’s pace. Other critical US data include PCE inflation (Thursday), October payrolls (for which the bar is pretty low because of an expected hurricane impact) and the manufacturing ISM (both on Friday). Next week are heydays for European number crunchers too. GDP growth on Wednesday may be better than the dire Q3 PMI readings suggest (0.2% vs flat) as hard data lately often deviated from soft indicators. European inflation numbers for October are scheduled on Thursday. Base effects should make clear that the current 2% undershoot is temporary at least through the end of the year. Investors are also keeping a close eye on the UK Chancellor presenting the Budget on Wednesday. Reeves already disclosed she’s altering the fiscal rules in order to create additional budgetary headroom of as much as £50bn over the coming years. Markets are on high alert. The Bank of Japan meets on Thursday. It won’t hike rates from the current 0.25% but it may hint at one in December. The Japanese yen sure won’t complain, having lost more than 10 big figures in just one month. The earnings season meanwhile also gains traction: Apple, Amazon, Intel, Microsoft, Meta Platforms, Alphabet and many others report.

News & Views

The ECB consumer expectations survey of September, inflation perceptions over the previous 12 months, for the next 12 months and for three years ahead all declined to respectively 3.4% (from 3.9% in August), 2.4% (from 2.7% and now the lowest since September 2021) and 2.1% (from 2.3%, the lowest since the Russia invaded Ukraine in February 2022). Expectations for nominal income growth rose slightly from 1.2% to 1.3% while those for spending growth over the next year remained unchanged at 3.2%. Stable expectations for spending and at the same time a lower inflation trajectory suggests a positive turning point for real spending, according to the comment in the survey. Consumers still see economic growth unchanged at -0.9% in the next 12 months with the unemployment rate rising to 10.6% from 10.4%.

The business survey of the National Bank of Belgium showed a small recovery in October. After successive declines since June the indicator rose slightly to -12.8 from -13.3. Business confidence improved in the building industry, trade and business-related service, but confidence in the manufacturing industry worsened. The improvement in the building industry was mainly due to an improvement in demand expectations and increased order books. The trade sector also expressed greater optimism on expected demand and intends to place more orders with suppliers. In business-related services respondents assess the current activity much more negatively but expect it to improve in the next three months. They also believe that general market demand will rise. The slight fall in manufacturing is mainly due to a more unfavourable assessment of total order books. The sector anticipates a slight drop in demand but is more optimistic about stock levels and expectations for employment.

Canada: Retail Sales Grow for the Second Consecutive Month, Supported by Auto Sales.

Retail sales rose by 0.4% month-on-month (m/m) in August, coming in worse than Statistics Canada's advance estimate for a 0.5% m/m increase. July's print was unchanged at 0.9% m/m reported in the advance estimate.

Adjusting for inflation, the volume of retail sales was 0.4% higher on the month.

Sales at motor vehicle and parts dealers rose by 3.5% m/m – the second consecutive month of growth. Ex-autos, sales were down 0.7% m/m, below the consensus expectation for growth of 0.4% m/m.

Receipts at gas stations and fuel vendors fell 2.7% m/m in nominal terms, as gas prices declined thanks to lower oil prices. Still, in volume terms, receipts were down 2.2% m/m in August.

Excluding auto sales and receipts at gas stations, core retail sales were down by 0.4% m/m in August.

- The loss in core sales was led by food and beverage stores (-1.5% m/m) and furniture & electronics stores (-2.6% m/m).

- A few categories reported gains, but they weren’t strong enough to offset the contraction reported by biggest category declines.

E-commerce sales declined by 2.5% m/m, erasing gains of the previous month.

Statistics Canada's advanced estimate for September points to an increase of 0.4% m/m.

Key Implications

Strong auto sales continued to drive retail growth in August. However, ex-autos, sales were the weakest in three months. Our internal credit and debit card spending data, which primarily reflects non-durable and durable goods, indicates a softening trend through September. Together, these signals align with our forecast, where a rebound in durable goods is expected to be the largest contributor to Q3 growth in total personal consumption expenditures - projected to rise at a below-trend rate of 1.0-1.5% quarter-on-quarter (annualized).

Alongside the weakness in core sales, the downward trend in retail spending per capita remains intact, marking a major area of concern for the Bank of Canada, which moved to cut rates by 50 basis points this week. By accelerating its easing cycle, the Bank wants to see consumption growth strengthen, but it risks sparking more demand for housing instead. Financial markets are currently pricing in a coin-flip chance of another jumbo cut in December.

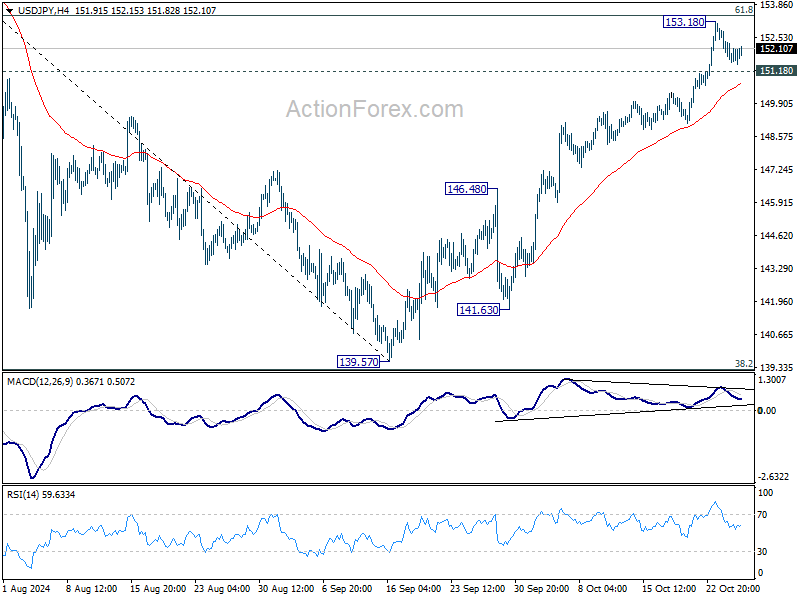

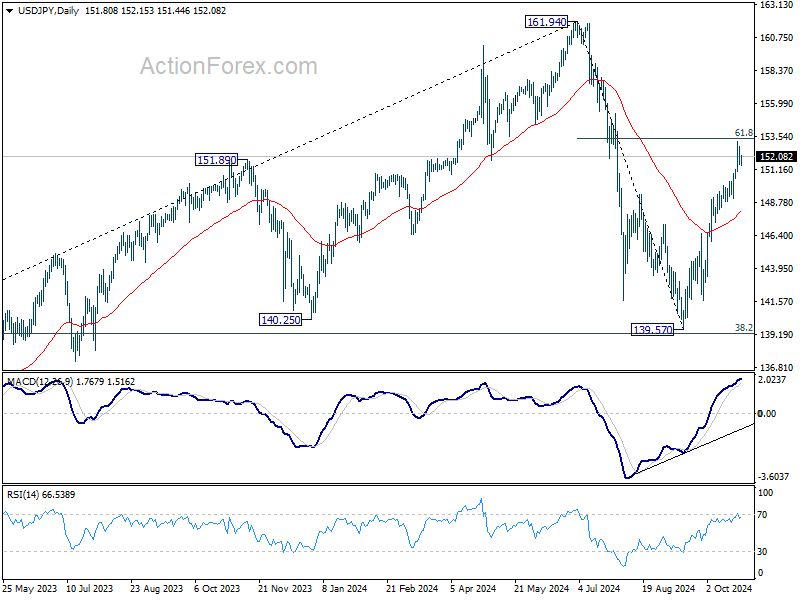

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.30; (P) 152.07; (R1) 152.58; More...

Intraday bias in USD/JPY remains neutral for consolidations below 153.18 temporary top. Further rise is in favor as long as 151.18 minor support holds. Decisive break of 61.8% retracement of 161.94 to 139.57 at 153.39 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, break of 151.18 will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 148.01).

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

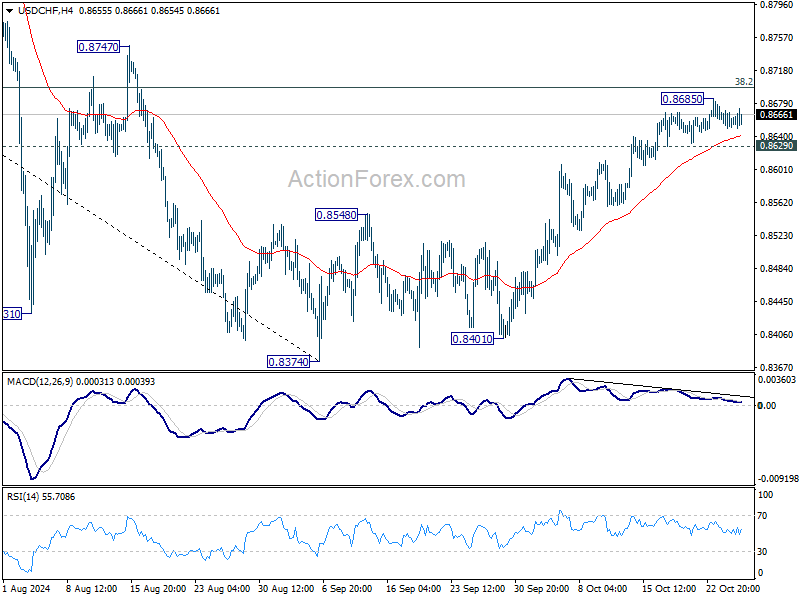

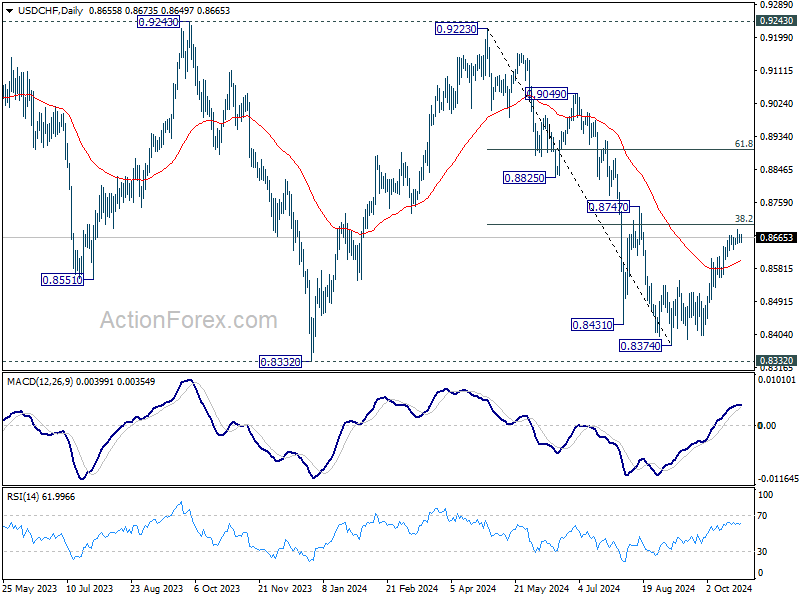

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8646; (P) 0.8662; (R1) 0.8674; More…

Intraday bias in USD/CHF remains neutral for consolidation below 0.8685 temporary low. Further rally is still in favor as long as 0.8629 minor support holds. Sustained break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed at 0.8374, after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.8629 support will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 0.8601).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

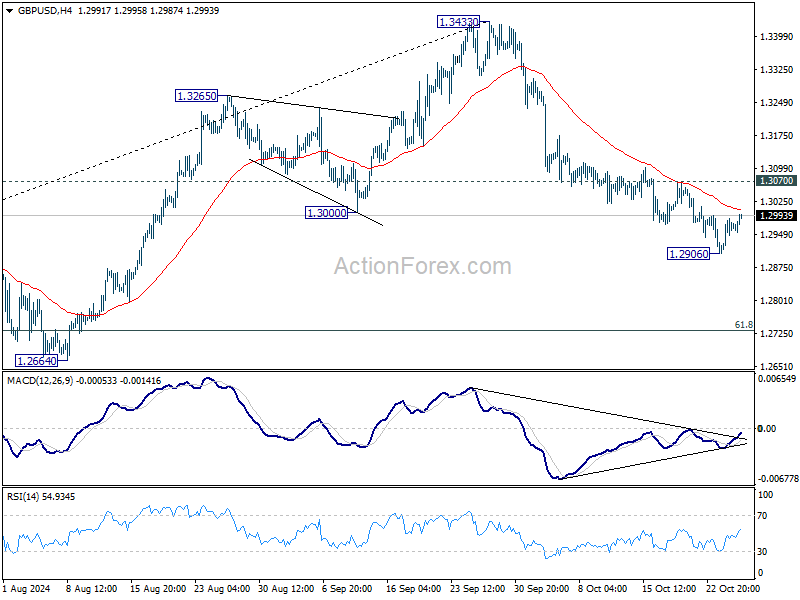

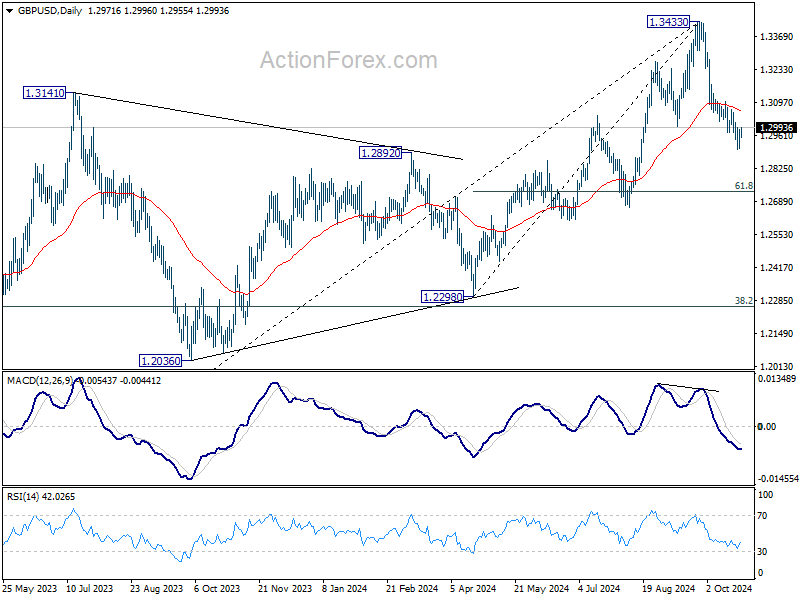

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2928; (P) 1.2958; (R1) 1.3007; More...

Intraday bias in GBP/USD remains neutral for consolidations above 1.2906 temporary low. Below 1.2906 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bearish divergence condition in 4H MACD, firm break 1.3070 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0789; (P) 1.0810; (R1) 1.0848; More...

Intraday bias in EUR/USD stays neutral for consolidation above 1.0760 temporary low. Further decline is expected as long as 1.0871 resistance holds. Below 1.0760 will resume the fall from 1.1213 to 1.0601 support next. However, considering bullish convergence condition in 4H MACD, break of 1.0871 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.0963).

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

Dollar Pulls Back with Market Caution Rising Before Critical US Events

The forex markets have shifted into consolidation mode today, with Dollar’s rally slowing as profit-taking sets in. Traders are showing caution ahead of two critical events that could reshape the near-term outlook: the upcoming non-farm payroll report next Friday, and the US presidential election the following week. NFP data is expected to set the stage for November and December FOMC rate decisions. Meanwhile, the presidential election carries broad economic implications, as shifts in administration priorities could impact both US and global markets.

Despite some pullback, Dollar remains the strongest performer this week. Swiss Franc and Euro follow behind. Japanese Yen remains the weakest currency this week. Both New Zealand Dollar and Australian Dollar also lag. Pound and Canadian Dollar are holding in middle ground.

In Europe, at the time of writing, FTSE is down -0.03%. DAX is up 0.07%. CAC is down -0.19%. UK 10-year yield is down -0.0324 at 4.213. Germany 10-year yield is up 0.007 at 2.279. Earlier in Asia, Nikkei fell -0.60%. Hong Kong HSI rose 0.49%. China Shanghai SSE rose 0.59%. Singapore Strait Times fell -0.32%. Japan 10-year JGB yield fell -0.006 to 0.952.

US durable goods orders down -0.8% mom in Sep, ex-transport orders up 0.4% mom

US durable goods orders fell -0.8% mom to USD 284.8B in September, better than expectation of -0.9% mom. Transportation equipment, drove the decrease, -3.1% mom to USD 95.4B Both were down three of the last four months.

Ex-transport orders rose 0.4% mom to USD 189.3B, much better than expectation of -0.1% mom decline. Ex-defense orders fell -1.1% mom to USD 264.9B.

Canada's retail sales rises 0.4% mom in Aug, vs exp 0.6% mom

Canada's retail sales grew 0.4% mom to CAD 66.6B in August, worse than expectation of 0.6% mom. Sales were up in four of nine subsectors and were led by increases at motor vehicle and parts dealers. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -0.4% mom.

Advance estimate suggests that sales increased 0.4% mom in September.

German Ifo rises to 86.5, stops declining for the time being

Germany's Ifo Business Climate index improved in October, rising from 85.4 to 86.5 and exceeding expectations of 85.4. Current Assessment index also showed an uptick from 84.4 to 85.7, surpassing the forecasted 84.1, while Expectations index rose from 86.4 to 87.3, above the anticipated 86.6.

Sectoral data further underscores this cautious optimism, with manufacturing inching up from -21.4 to -20.6, services edging into positive territory from -3.5 to 0.1, and trade posting an improvement from -29.8 to -29.3. Construction sector, however, slipped from -25.3 to -25.7.

This data signals a stabilization in Germany's economic outlook, with Ifo commenting, "The German economy stopped the decline for the time being."

Tokyo CPI core dips to 1.8% in Oct on lower energy prices

Japan's Tokyo CPI core (excluding food) dropped from 2.0% yoy to 1.8% yoy in October, slightly above market expectations of 1.7%. This marks the first time in five months that inflation has dipped below BoJ's 2% target. Headline CPI also slowed from 2.1% yoy to 1.8% yoy.

The deceleration was largely driven by a slowdown in energy prices, with government subsidies for energy costs contributing to a 0.51 percentage point reduction in the overall index.

Despite this, underlying inflationary momentum ticked up, as core-core CPI (excluding food and energy) rose from 1.6% yoy to 1.8% yoy. Services prices also saw an uptick, increasing by 0.8% yoy compared to 0.6% yoy in the prior month.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0789; (P) 1.0810; (R1) 1.0848; More...

Intraday bias in EUR/USD stays neutral for consolidation above 1.0760 temporary low. Further decline is expected as long as 1.0871 resistance holds. Below 1.0760 will resume the fall from 1.1213 to 1.0601 support next. However, considering bullish convergence condition in 4H MACD, break of 1.0871 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.0963).

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

US durable goods orders down -0.8% mom in Sep, ex-transport orders up 0.4% mom

US durable goods orders fell -0.8% mom to USD 284.8B in September, better than expectation of -0.9% mom. Transportation equipment, drove the decrease, -3.1% mom to USD 95.4B Both were down three of the last four months.

Ex-transport orders rose 0.4% mom to USD 189.3B, much better than expectation of -0.1% mom decline. Ex-defense orders fell -1.1% mom to USD 264.9B.