Sample Category Title

Canada’s retail sales rises 0.4% mom in Aug, vs exp 0.6% mom

Canada's retail sales grew 0.4% mom to CAD 66.6B in August, worse than expectation of 0.6% mom. Sales were up in four of nine subsectors and were led by increases at motor vehicle and parts dealers. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -0.4% mom.

Advance estimate suggests that sales increased 0.4% mom in September.

Will AUDUSD Keep Falling? Key U.S. and Australia Economic Drivers to Watch

Fundamental Analysis

U.S.:

- September CPI: Headline inflation eased to 2.4% y/y, aligning closer to the Fed’s target, though core CPI rose by 3.3% y/y, driven by housing and insurance.

- September Jobs: The U.S. added 254,000 jobs, surpassing expectations, which may prompt the Fed to maintain high rates short-term.

- Treasuries: 10-year yields rose to 4.24% this week, reflecting growth optimism and potential for sustained high rates.

Australia:

- September CPI: Inflation slowed to 5.4% y/y, which could support the RBA's wait-and-see approach.

- September Employment: Only 6,700 jobs were added, indicating a cooling economy and reinforcing expectations that the RBA will hold rates steady.

The AUDUSD has faced downward pressure largely due to divergent fundamentals between the U.S. and Australia. As the Fed considers sustained high rates, driven by core inflation and job growth, the RBA adopts a more cautious approach amidst slowing inflation and weaker job gains. Additionally, rising U.S. Treasury yields have made the dollar more attractive than the AUD, intensifying the pair's bearish trend.

In the short term, should U.S. rates remain elevated with Treasury yields climbing, AUDUSD is likely to stay under pressure. However, any shifts in RBA policy or signs of a U.S. economic slowdown could provide support for the Australian dollar.

Technical Analysis

AUDUSD, H2

- Supply Zones (Sells): 0.6666 and 0.6677

- Demand Zones (Buys): 0.6621

The pair has been trending lower throughout October, forming a one-week accelerated bearish channel. The last validated resistance level at H4 is 0.6695.

In this context, further selling is expected as long as prices stay below the daily open (D1) at 0.6636, with intraday targets at supports 0.6614, 0.66, and the average bearish range at 0.659. A sustained break would allow for a broader downward move toward August 15 support at 0.6557.

However, intraday exhaustion of bears could drive a break above the initial supply zone around 0.6635 and local resistance at 0.6644, potentially extending toward 0.6661 intraday and the high-volume node around 0.6677 next week. This correction would still maintain the bearish structure as long as it remains below the key resistance at 0.6661.

Technical Summary

- Corrective Bearish Scenario: Intraday sells below 0.6635 (upon confirmed PAR* pattern), targeting 0.6614, 0.66, 0.6590, and extension to 0.6557. Use a 1% SL.

- Bullish Continuation Scenario: Buys above 0.6644, targeting 0.6661, 0.6677, or extended to 0.6690. Employ a 1% SL with low lot size to accommodate volatility.

Always await the formation and confirmation of a *Reversal Exhaustion Pattern (PER) on M5 as outlined here before entering key zones.

Naked POC

POC = Point of Control: A zone of highest volume concentration.

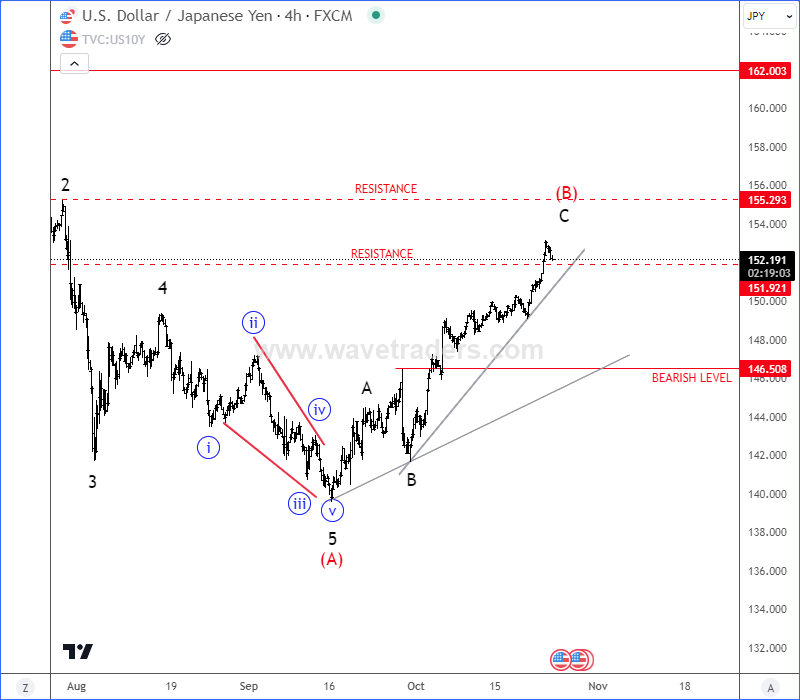

USD/JPY May Face Resistance, At Least Temporary One

USDJPY made big, sharp and impulsive sell-off through summer. That was wave (A) that caused a bounce in last two months, for a rally in (B) which is now at important 153-155 resistance, but there’s no evidence of a reversal yet, unless we see a bearish intraday impulse, below 146.50, where overlap will likely confirm end of subwave C on 4h time frame.

However, due to strong rise, keep in mind that current rally could also be a five-wave impulse into first leg A of a bigger and larger A-B-C corrective rally in wave (B) according to the secondary count, especially if we respect what yields/notes are doing, but even in this case, we can expect a reversal down within wave B soon.

Canadian Dollar Eyes Retail Sales

The Canadian dollar is showing little movement on Friday. In the European session, USD/CAD is trading at 1.3845 at the time of writing, down 0.07%.

It has been a relatively quiet week for the Canadian dollar, and even an oversized 50-basis point rate cut from the Bank of Canada failed to shake up the Canadian currency. The jumbo cut was priced in by the markets, as inflation has fallen below the BoC’s 2% target and the economy remains week despite the central bank’s gradual rate cuts. This week’s cut was the fourth in as many meetings and the BoC is hoping that the large rate cut will boost economic activity.

BoC Governor Tiff said after the rate meeting that “monetary policy has worked” and that both headline and core inflation have come down. Does Tiff’s pat on the back mean that the BoC will revert back to modest cuts of 25-bp increments? Not necessarily – Tiff said that the rate move should “contribute to a pickup in demand”, and if the economy remains sluggish and consumer spending doesn’t improve, the BoC could repeat a 50-bps move in December.

The US will release durable goods orders and UoM consumer sentiment later today. The manufacturing sector has contracted for four straight months and core durable goods orders are expected to fall 1% in September, after no change in August. The UoM consumer sentiment index is expected to fall to 68.9 in October, compared to 70.1 in September. Consumers are unhappy about high inflation and there is uncertainty over the US election, which is a dead heat with just 10 days to the election.

USD/CAD Technical

- USD/CAD is testing support at 1.3846. Below, there is support at 1.3823

- There is resistance at 1.3879 and 1.3902

USD/JPY Technical: 4-Week of JPY Persistent Weakness Led by Political Factors

- The recent movement of the USD/JPY has been influenced primarily by political factors.

- The JPY has weakened significantly due to the growing risk that the current LDP-led coalition may lose its majority seats after this Sunday, 27 October snap election.

- Watch the 151.10 key short-term support on the USD/JPY.

Since our last publication, the bears have continued to gain a foothold in the Japanese yen as it weakened further against the US dollar and burst above the 151.95 key long-term pivotal resistance of the USD/JPY and its 200-day moving average.

Growing internal political risk is inflicting damage on the JPY outlook in the near term

There is now a growing risk that Japan may end up with a minority coalition government after this Sunday, 27 October snap general election for the lower house.

Recent polls have indicated the possibility of the ruling Liberal Democratic Party (LDP)-Komeito coalition losing its majority in parliament and may also cause the newly appointed Prime Minister Ishiba to lose his premiership or force the LDP to look for additional coalition partner to stay in power.

All in all, such political risk is likely to hamper the Bank of Japan (BoJ) current monetary policy normalisation plan to hike interest rates gradually after it ended its decades-long of negative interest rate in March and increased the overnight short-term interest rate to 0.25% in July.

At this juncture, the main opposition party, the Constitutional Democratic Party of Japan has ruled out the prospect of forming a coalition with the LDP.

Thus, smaller opposition parties, Japan Innovation Party and Democratic Party for the People are the only choices that LDP has as potential coalition partners to secure its power base.

Both opposition parties favour expansionary fiscal and monetary policies to achieve sustained economic and wage growth. Hence, BoJ is likely to face a hurdle in enacting additional interest rate hikes next year if such economic proposals are taken into consideration by a newly formed LDP-led coalition.

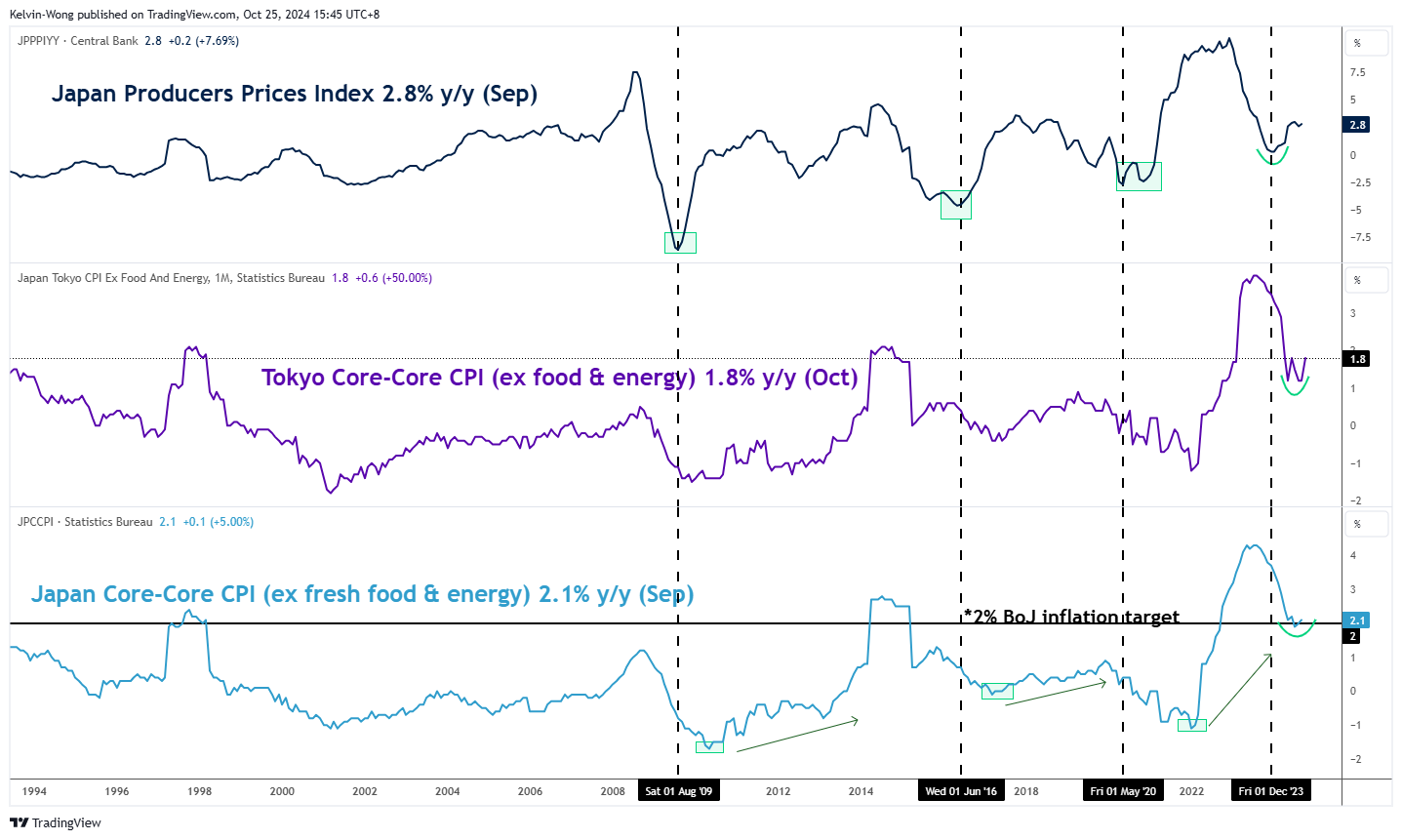

Fundamentals are still supporting further interest rate hikes in Japan

Fig 1: Monthly Japan PPI, CPI & Tokyo CPI trends (y/y) as of Sep & Oct 2024 (Source: TradingView, click to enlarge chart)

Even though the latest headline inflation in Tokyo slowed to 1.8% y/y in October, down from 2.2% a month earlier, the Tokyo core-core inflation rate (excluding food and energy) came in strong-than-expected as it rose to 1.8% y/y from 1.2% printed in September (see Fig 1).

The Tokyo inflation data are considered a leading inflationary trend for the nationwide Japan CPI which BoJ will take into consideration at next week’s monetary policy meeting on 31 October when it also releases its latest quarterly growth and inflation trend forecasts.

The market consensus is looking for BoJ to keep its short-term interest rate unchanged at 0.25% due to uncertainties surrounding the upcoming US presidential election on 5 November.

Watch the 151.10 key short-term support on USD/JPY

Fig 2: USD/JPY minor trend as of 25 Oct 2024 (Source: TradingView, click to enlarge chart)

The pull-back of the USD/JPY that took form on Thursday, 24 October from a three-month high of 153.19 printed on Wednesday, 23 October has managed to stall at its 200-day moving average and slightly above the lower boundary of its minor ascending channel from 30 September 2024 low of 141.65 (see Fig 2).

Watch the 151.10 key short-term pivotal support to maintain its current streak of impulsive upmove sequence for the next intermediate resistances to come in at 153.80 and 154.70/80 next.

However, failure to hold at 151.10 invalidates the bullish tone to kickstart a potential mean reversion decline to expose the intermediate supports of 150.30 and 148.95 (also the 20-day moving average).

Tokyo Core CPI Complicates BoJ’s Rate Plans

The Japanese yen is showing limited movement on Friday. In the European session, USD/JPY is trading at 151.94, up 0.09%.

Tokyo Core CPI falls below BoJ’s target

Tokyo Core CPI, a leading indicator of inflation trends in Japan, fell to 1.8% y/y in October, down from 2% in September and just above the market estimate of 1.7%. This marked a second straight deceleration and was the lowest level since April. A key service inflation indicator also slowed in October, dropping from 2.7% to 2.6%, a four-month low.

The decline in inflation is a disappointment for the Bank of Japan, which wants to see inflation remain sustainable around its 2% target before its raises interest rates on the path towards normalization. The BoJ meets next week and is expected to maintain rates. The central bank will release growth and inflation forecasts which could provide insights into future monetary policy. The cautious BoJ is unlikely to raise rates until early next unless inflation reverses its current downtrend and pushes higher.

The US wraps up the week with core durable goods orders and UoM consumer sentiment. The manufacturing sector has contracted for four straight months and core durable goods orders are expected to fall 1% in September, after no change in August. The UoM consumer sentiment index is expected to fall to 68.9 in October, compared to 70.1 a month earlier. Consumers are unhappy about high inflation and there is uncertainty over the US election, with an extremely tight race between Donald Trump and Kamala Harris.

USD/JPY Technical

- USD/JPY is testing resistance at 1.5207. The next resistance line is 152.58

- 151.30 and 150.79 are providing support

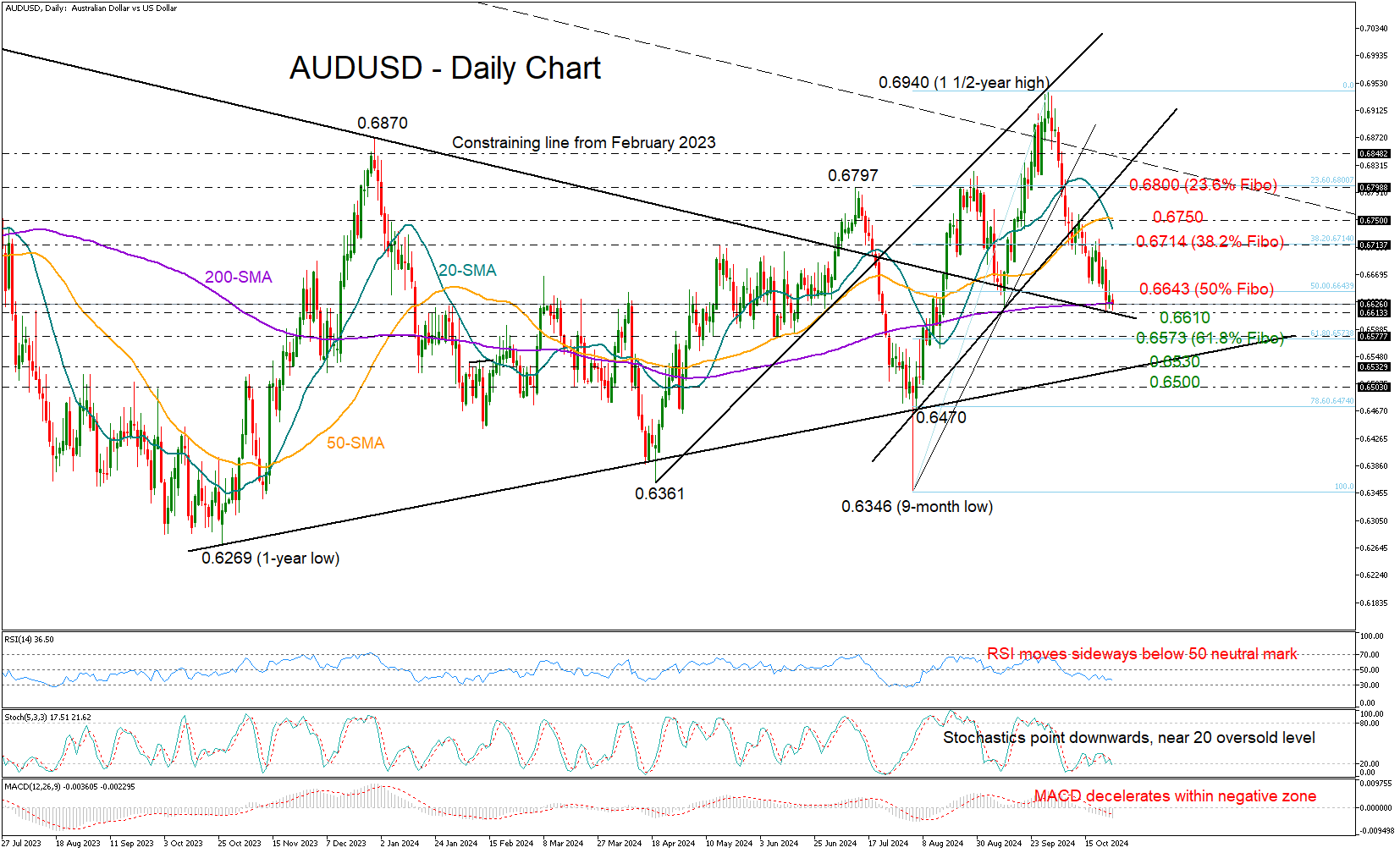

AUDUSD: Will September’s Bullish Vibes Return?

- AUDUSD tests support area near 200-day SMA

- Short-term bias remains on the negative side

AUDUSD has been on a downward slide again, marking its fourth consecutive week in the red. It recently dipped to a two-month low of 0.6612 but held above the 200-day simple moving average (SMA) and the constraining falling line from February 2023, which increases speculation as to whether the sell-off is finally hitting a bottom.

Remember back in September when those support lines gave the price a nice boost? Well, as long as they stay in play there is hope for a bullish reversal. However, the mood is still a bit cautious, with the RSI and the MACD reflecting persistent selling appetite. If the price dips below 0.6610, support could come from the 61.8% Fibonacci retracement level around 0.6573. If that doesn’t hold, the pair could next head for the ascending trendline at 0.6530, and if that breaks as well, watch out for the protective zone between 0.6470 and 0.6500.

On the brighter side, if AUDUSD can bounce back above the 50% Fibonacci level at 0.6643, it could see some momentum building up to the 38.2% Fibonacci level at 0.6714. And if it climbs above the 0.6750 resistance, where the 50-day SMA hangs out, that could really get things moving towards the 23.6% Fibonacci level at 0.6800.

In summary, while AUDUSD has not overcome downside risks, a recovery attempt could be possible as the pair is currently testing a familiar pivot area.

NZD/USD Hits Four-Week Low Amid US Dollar Strength

The NZD/USD pair dropped to 0.5988 this Friday, marking a potential close lower for the fourth consecutive week. The strength of the US dollar continues to dominate the currency pair, fuelled by expectations of a moderate interest rate cut by the Federal Reserve and persistent demand for the USD amid geopolitical tensions in the Middle East and the lead-up to the US presidential election.

Reserve Bank of New Zealand Governor Adrian Orr recently reaffirmed the central bank’s capability to maintain low and stable inflation, noting that the bank is vigilant and ready to act should market conditions necessitate intervention. These comments have solidified market expectations of a potential RBNZ rate cut in November, with a 50-basis-point reduction widely anticipated. Some speculate that a more aggressive cut of 75 basis points could be on the table if conditions worsen.

Recent data indicating a drop in consumer confidence in New Zealand after three months of gains has added to the bearish sentiment surrounding the NZD.

NZD/USD technical analysis

The NZD/USD pair is extending its downward trajectory towards 0.5983. Following the achievement of this level, a corrective move towards 0.6182 could be in the offing, with an intermediate target at 0.6119. This potential rebound is supported by the MACD indicator, whose signal line remains below zero but is trending upwards, suggesting a possible easing of downward pressure.

On the hourly chart, NZD/USD has established a consolidation pattern around the 0.6000 level and has since dipped to a local low of 0.5987. A brief recovery to 0.6000 may occur as a test from below before another possible descent to 0.5983. Should this level be reached, it would likely mark the exhaustion of the current downward wave. The Stochastic oscillator reinforces this outlook, with its signal line positioned below 20 but curving upwards, indicating the potential for a short-term upward correction.

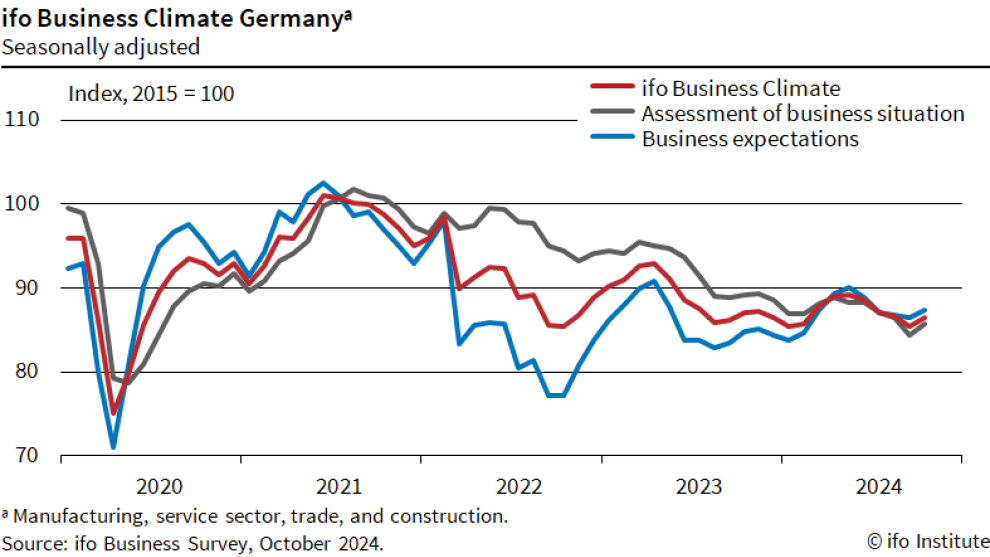

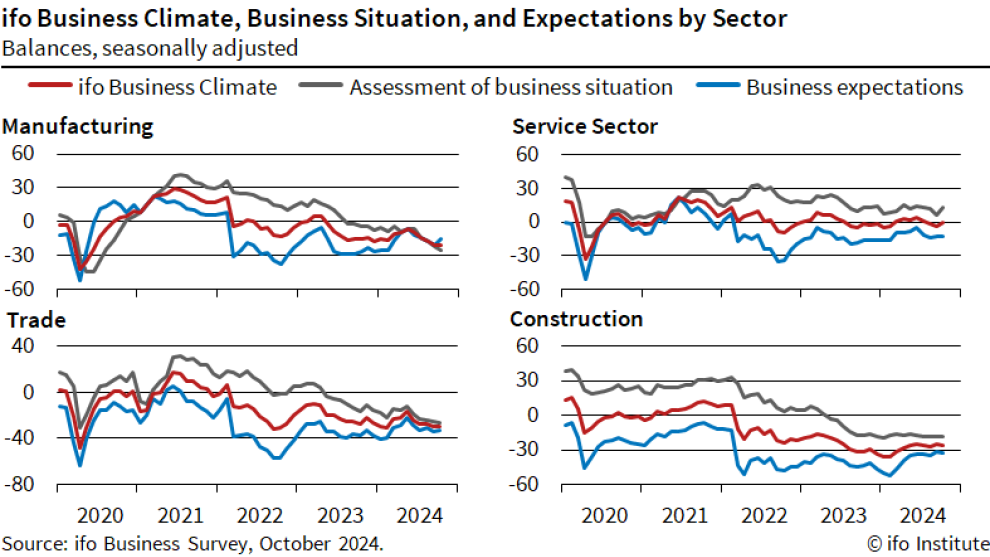

German Ifo rises to 86.5, stops declining for the time being

Germany's Ifo Business Climate index improved in October, rising from 85.4 to 86.5 and exceeding expectations of 85.4. Current Assessment index also showed an uptick from 84.4 to 85.7, surpassing the forecasted 84.1, while Expectations index rose from 86.4 to 87.3, above the anticipated 86.6.

Sectoral data further underscores this cautious optimism, with manufacturing inching up from -21.4 to -20.6, services edging into positive territory from -3.5 to 0.1, and trade posting an improvement from -29.8 to -29.3. Construction sector, however, slipped from -25.3 to -25.7.

This data signals a stabilization in Germany's economic outlook, with Ifo commenting, "The German economy stopped the decline for the time being."

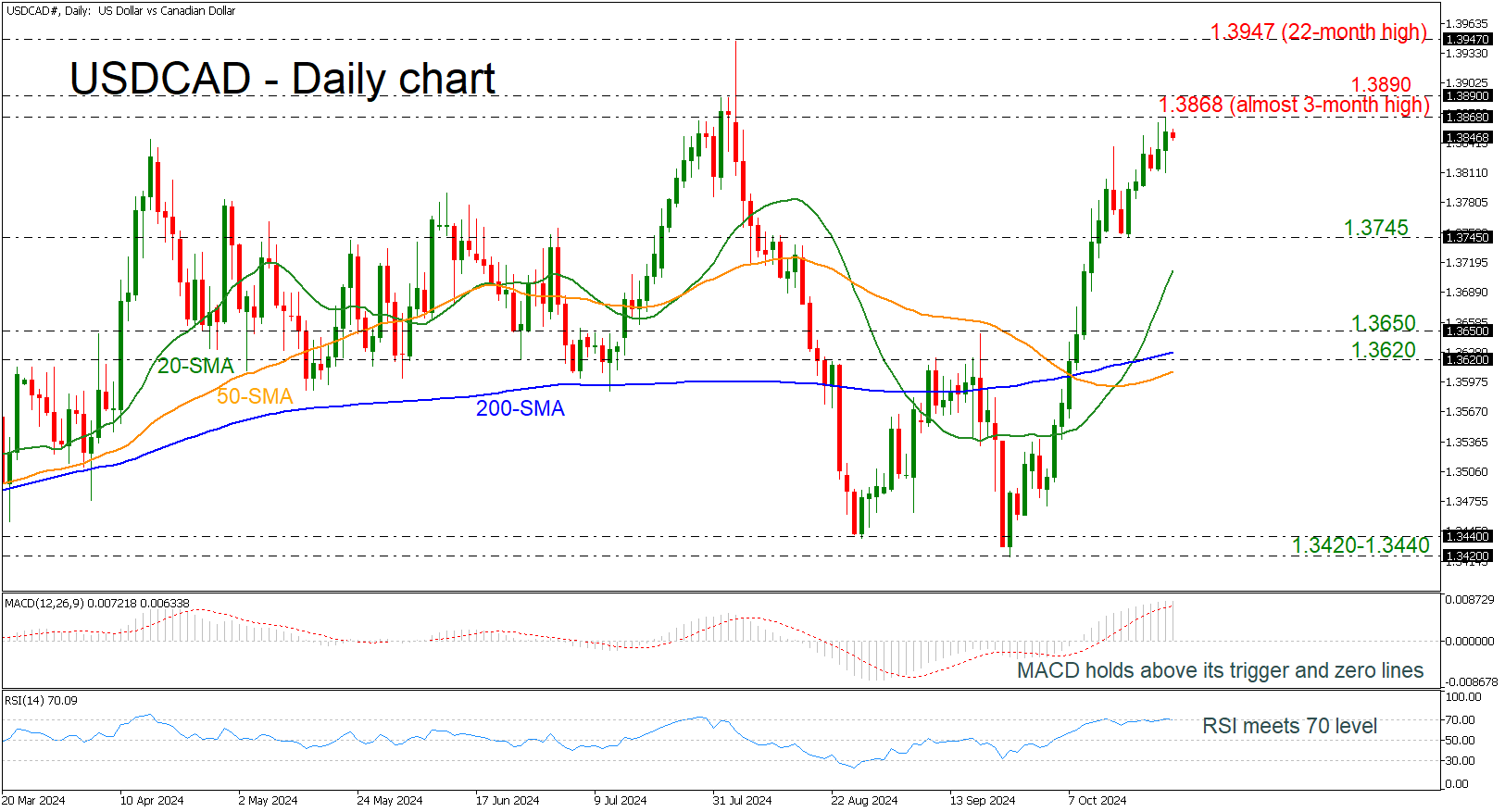

USDCAD Still Near the Almost 3-Month High

- USDCAD adds 3.4% from 1.3420

- Remains well above the SMAs

- MACD and RSI indicate overbought levels

USDCAD has been creating a notable bullish rally since the bounce off the 1.3420 support level, taking the price to an almost three-month high of 1.3868. The pair added 3.4% on this rally, trying to switch the medium-term outlook to positive.

Technically, the RSI is moving horizontally near the 70 level, while the MACD oscillator is losing some momentum above its trigger and zero lines. Both suggest that the market is overstretched, and a potential bearish correction may be on the cards.

Steeper upside movements may drive the market until the 1.3890 barrier ahead of the 22-month peak of 1.3947.

On the other hand, a downside retracement could first find support at the 1.3475 level before testing the 20-day simple moving average (SMA) at 1.3710. Even lower, the inside swing high of 1.3650, taken from the peak on September 19, may pause the bearish move.

All in all, USDCAD is experiencing aggressive buying interest, and only a dive beneath the 200-day SMA, which lies near the 1.3620 bar, may change the bias to neutral.