Sample Category Title

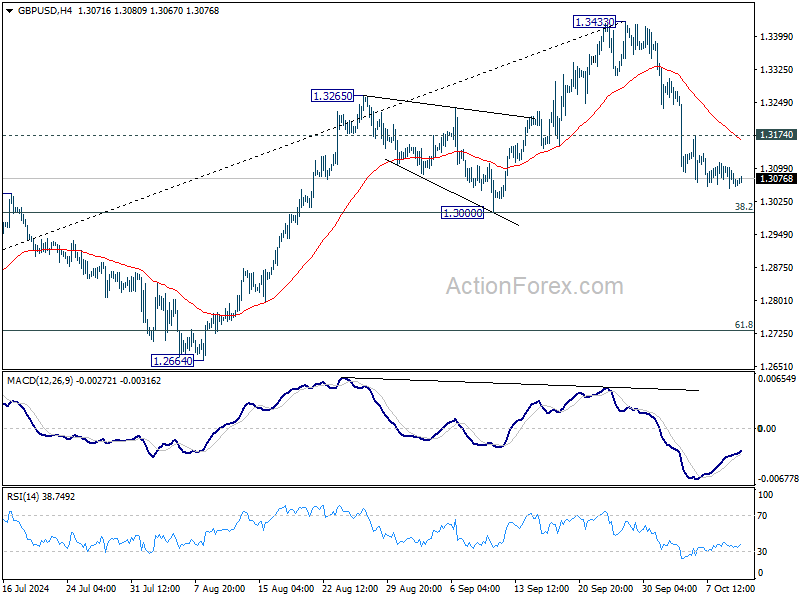

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3049; (P) 1.3081; (R1) 1.3107; More...

Intraday bias GBP/USD stays neutral for the moment. While corrective fall from 1.3433 might extend lower, strong support should be seen from 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) to contained downside. Above 1.3174 minor resistance will turn bias back to the upside for stronger rebound. However, decisive break of 1.3000 will carry larger bearish implications.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

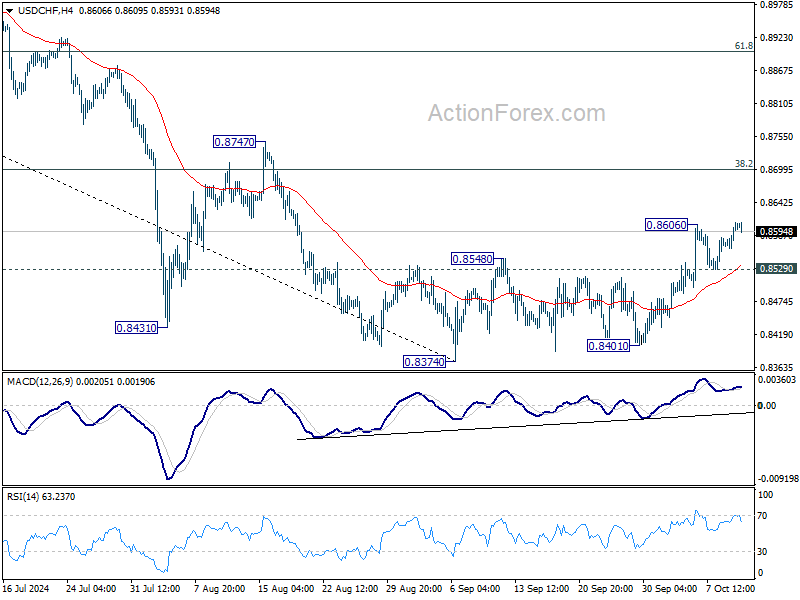

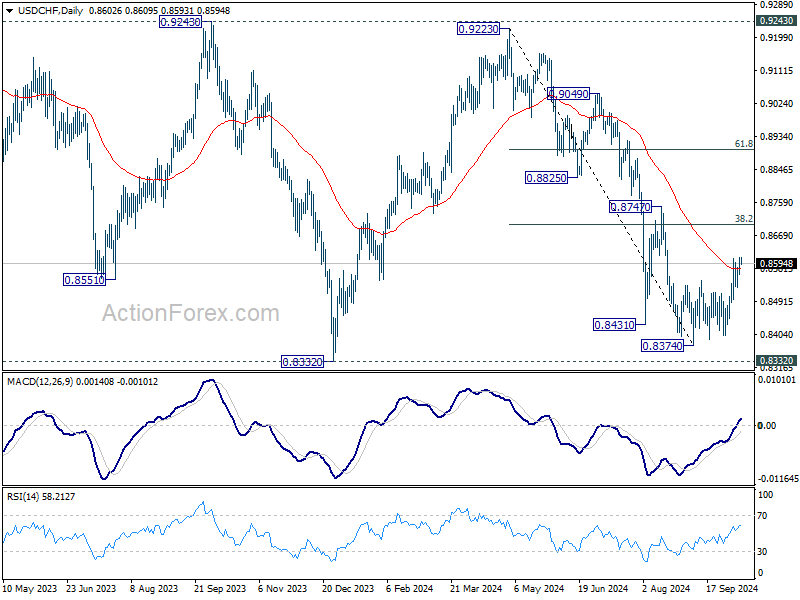

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8579; (P) 0.8594; (R1) 0.8624; More…

Intraday bias in USD/CHF is back on the upside with breach of 0.8606 temporary top. Rebound from 0.8374 is resuming for 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. Next target will be 61.8% retracement at 0.8899. On the downside, below 0.8529 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

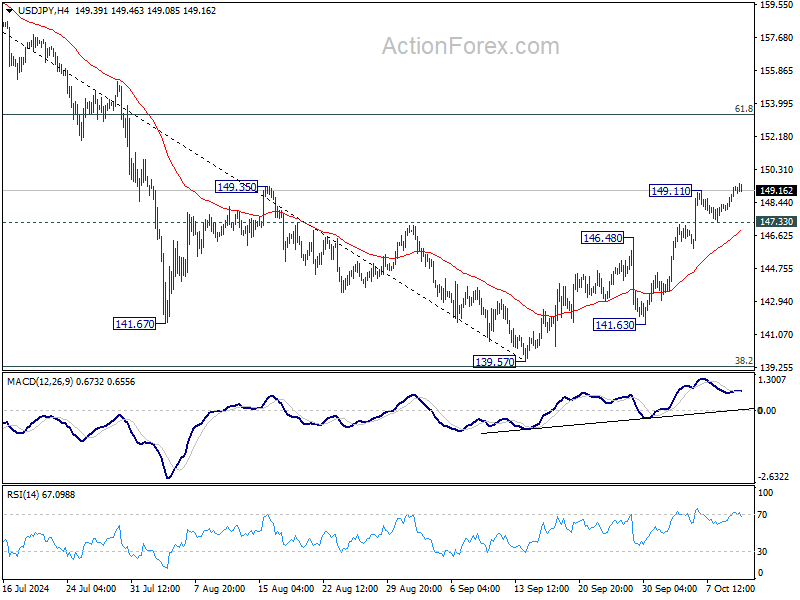

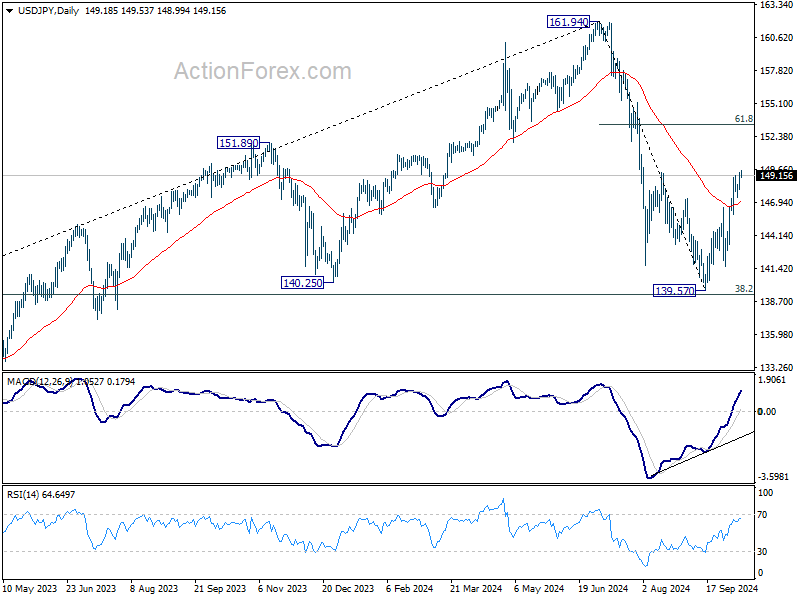

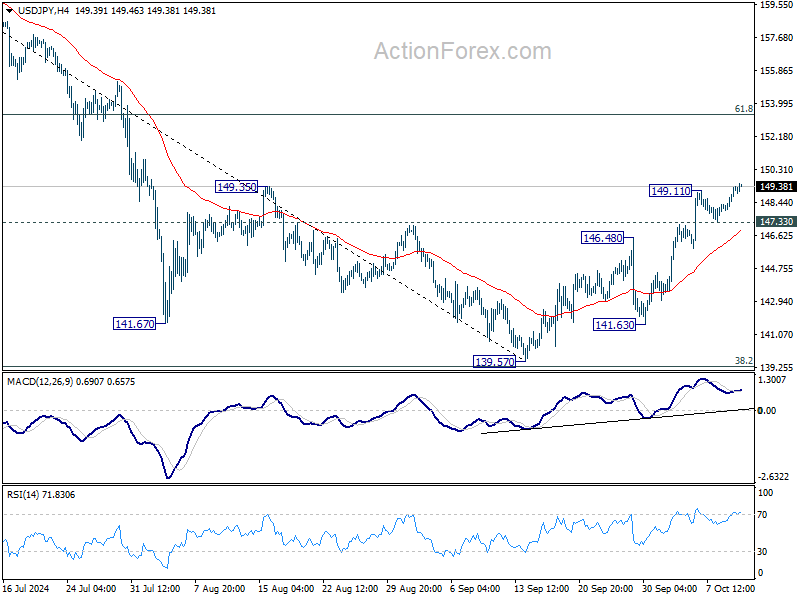

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.43; (P) 148.89; (R1) 149.78; More...

USD/JPY's rally from 139.57 short term bottom resumed after brief consolidations, and intraday bias is back on the upside. Current rally is seen as the second leg of the corrective pattern from 161.94. Next target is 61.8% retracement of 161.94 to 139.57 at 153.39. On the downside, below 147.33 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

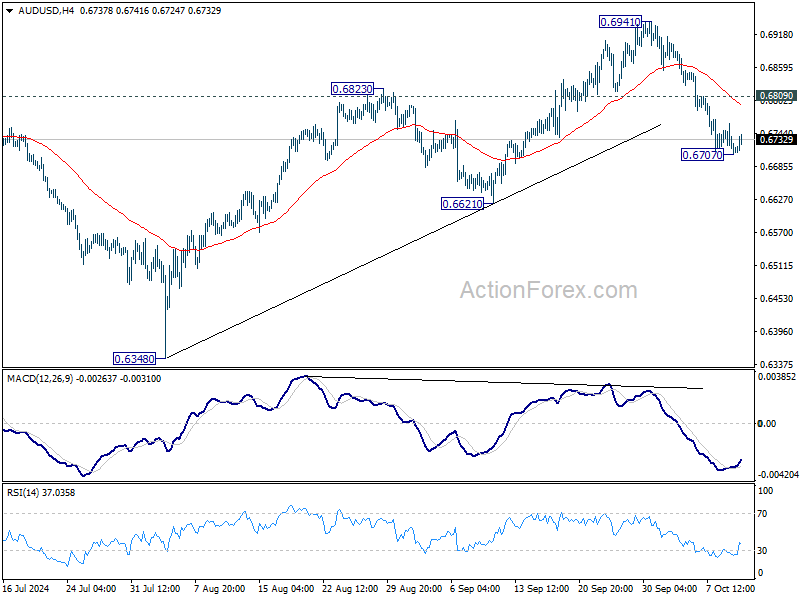

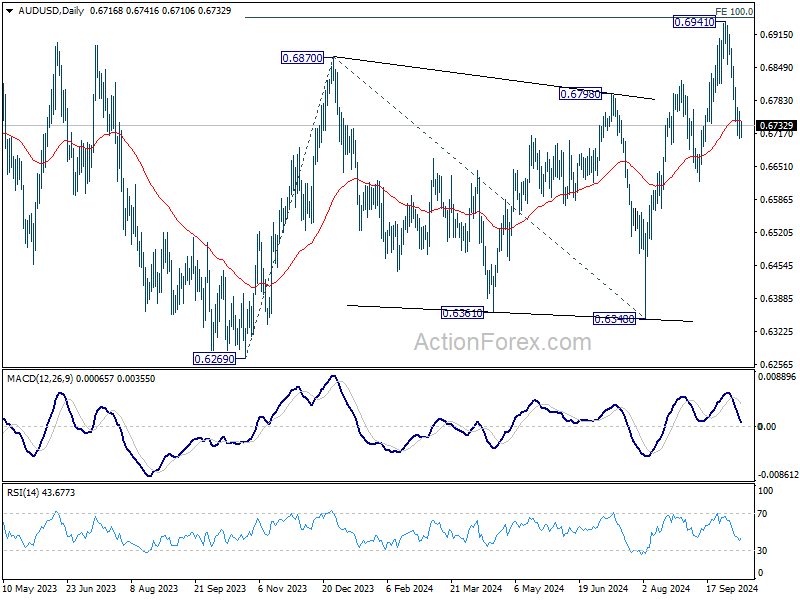

AUD/USD Daily Report

Daily Pivots: (S1) 0.6697; (P) 0.6729; (R1) 0.6751; More...

Intraday bias in AUD/USD is turned neutral first with 4H MACD crossed above signal line. Some consolidations could be seen, but further decline is expected as long as 0.6809 minor resistance holds. Below 0.6707 will resume the fall from 0.6941 short term top. Sustained trading below 55 D EMA (now at 0.6744) should confirm rejection by 0.6941 fibonacci level, and bring deeper decline to 0.6621 support.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.

After Some Hesitation, Dollar Gradually Regaining Traction

Markets

Yesterday’s risk-on sentiment, Fed comments and the release of the Minutes of the Fed September meeting all contributed to a gradual, but protracted intraday uptrend in US yields. They closed higher between 7.1 bps (5-y) and 4.7 bps (30-y). Fed comments (Daly, Logan) suggest most governors see inflationary pressures receding while risks to employment are growing, despite Friday’s US payrolls report. The minutes of the September 17-18 meeting also showed some internal debate on the need for a 50 bps inaugural step. Some participants would have preferred a 25 bps reduction and few other embers indicated that they could have supported such a decision. In this respect, the also indicated that a 25 bps ‘reduction would be in line with a gradual path of policy normalization that would allow policymakers time to assess the degree of policy restrictiveness as the economy evolved.’ Markets now pricing in slightly less than 50 bps of cumulative cuts for the two remaining meetings of this year can be considered as more or less in line with the aim of gradualism. Of course, the Fed works in a status of data-dependency. German yields added 3.2 bps (2-y) to 0.4 bps even as ECB governors show a ‘near-consensus’ on a 25 bps step next week, with ECB Kazimir one of the exceptions the rule. Especially US equities still feel supported by the combo of decent growth and the prospect of (gradual) policy easing. The S&P 500 (+0.71%) closed at a new record (5792.04). After some hesitation earlier this week, the dollar is gradually regaining traction, moving further beyond the resistance levels broken in the wake of last week’s strong US eco data. EUR/USD closed at 1.094. DXY at 102.93.

Asian markets mostly remain in risk-on mode this morning. Mainland China investors are looking forward to a press conference by the China’s Finance Minister on Saturday that should bring some clarity on the amount of (fiscal) stimulus. Later today, attention shifts to the US September CPI release. Consensus expects headline inflation to ease to 0.1% M/M and 2.3% Y/Y (was 0.2% M/M and 2.5% Y/Y) and core inflation at 0.2% M/M and 3.2% (was 0.3%, 3.2%). The market and Fed focus recently turned from inflation to growth. We assume that a big upward surprise is needed for markets to again reconsider this shift. With markets not fully discounting two additional 25 bps steps for the two remaining Fed meetings this year, the room for a further rise in short-term US yields might become limited. LT yields maybe still have some further upside in case of solid data or as the focus turns to fiscal policy in the run-up the US election. In theory, this also should be a rather neutral set-up for the dollar. However, the technical picture in most USD cross rates is improving. EUR/USD 1.0881/82 (76% retr. since early August/correction low) is the next intermediate target on the charts.

News & Views

The People’s Bank of China announced details of the swap facility which was part of the broader support package launched on September 24. Eligible brokers and insurers can now pledge assets with the Chinese central bank such as bonds, stock ETF’s and shares of companies listed on the CSI 300 in return for liquid assets. The size is CNY 500bn but may be expanded in the future. The announcement helps Chinese stock markets 3% to 5% higher this morning, extending their volatile ride. USD/CNY tries to break with the post-payrolls USD-strength that pulled the pair away from 7-area (lowest since May 2023) to currently 7.07. Focus now turns to a press conference by Finance Minister Lan Fo’an on Saturday with more (details on) fiscal stimulus expected.

The New Zealand Department of Treasury published financial government statements for the year ended 30 June 2024. The deficit was NZD 12.85bn, compared to NZD 11.07bn projected in the May budget. That’s an increase from the NZD 9.45bn deficit in the 2022/2023 financial year. Finance Minister Willis warned that the books are not in great shape and wants to tidy them up. She targets a return to budget surplus in 2028 and wants to reduce debt to less than 40% of GDP (42.5% of GDP end June). According to the budget forecasts, the deficit will widen further to NZD 13.37 bn in the year through June 2025 before starting to narrow.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) still is a source of concern, but very weak PMI’s and soft comments of Lagarde (and other MPC members) suggest the ECB is likely to step up the pace of easing with an October cut. Spill-overs from strong US data prevented a test of the 2.0% barrier. 2.00-2.35% might serve as a ST consolidation range.

US 10-y yield

The Fed kicked off its easing cycle with a 50 bps move. Powell and Co turning the focus from inflation to a potential slowdown in growth/employment made markets consider more 50 bps steps. Strong US September payrolls suggest the economy doesn’t need aggressive Fed support for now, but the debate might resurface as the economic cycle develops. For the US 10-y, 3.60% serves as strong support. The steepening trend is taking a breather.

EUR/USD

EUR/USD twice tested the 1.12 big figure as the dollar lost interest rate support at stealth pace. Bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) partially offset some of the general USD weakness. After solid early October US data, the dollar regained traction, with EUR/USD breaking the 1.1002 neckline. Targets of this pattern are near 1.08.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness was indicated to be further unwound gradually. The economic picture between the UK and Europe also (temporarily?) diverged to the benefit of sterling, pulling EUR/GBP below 0.84 support. Dovish comments by BoE Bailey ended by default GBP-strength. Uncertainty on the UK budget to be released end this month is becoming an additional headwind for the UK currency.

All Eyes on US CPI

The S&P 500 hit its 44th record this year on Wednesday, Nasdaq 100 closed above the 20’000 mark. The Dow Jones index advanced 1% to an almost ATH, while investors were less enthusiastic regarding the small stocks, the Russell 2000 gained 0.26%. Over in Europe, the Stoxx 600 was better bid, the FTSE 100 recovered a part of the previous day’s China related losses. In China, the bleeding in the CSI 300 stopped and the index jumped close to 3% in the Asian session on hope that the new government briefing on fiscal policy due Saturday will bring the kind of stimulus measures that investors are happy with. Xi’s government probably understood this week that anything less than absolutely-mind-blowing wouldn’t do as we are celebrating the fourth year of the crackdown on the country’s big technology companies. Alibaba was trading near $300 a share in October 2020, and now hardly above $100. China has a long ways to go to bring investors back on board and it must deliver to restore appetite. Confidence is another story...

But anyway, market sentiment isn’t bad; copper, iron ore and US crude are better bid today. The barrel of US crude tipped a toe below the 50-DMA and below a major Fibonacci support yesterday but rapidly rebounded on the back of ongoing geopolitical tensions and despite a 5.8-mio barrel build in US oil inventories last week. The geopolitical risks remain tilted to the upside, and the excitement that China could announce a nice fiscal stimulus package this weekend, will likely throw a floor under any weakness in oil prices into the weekend.

Elsewhere, European futures are up and US futures are flat at the time of writing. The Federal Reserve (Fed) minutes released yesterday showed that there has been some pushback to the Fed’s 50bp cut last month, as some members thought it would be more reasonable and cautious to start with a 25bp cut. But most preferred to rush to the exit – a possibly premature decision that could justify a month of pause from the Fed to rectify the overly dovish move in November? We will see that. The probability of a no cut is gently creeping in. That probability now stands at 15% ahead of the upcoming US CPI data, and has further room to mature if the economic data continues to defy the slowdown expectations in the US.

All eyes on US CPI

Even though the Fed members’ shifted their attention from inflation to jobs, inflation is still important. As some Fed members say, the risks are probably roughly ‘in balance’ right now. That means that any uptick in US inflation could reshuffle the Fed expectations, and the market pricing attached to them. Headline US inflation is expected to have eased from 2.5% to 2.3% in September, but the core inflation likely remained sticky above 3% - and wages grew at 4% last month, meaning that the Fed is getting closer to its destination, but it is not there just yet. And the last mile could – and would in theory – require an undesired weakness in the jobs market to stabilize inflation near the 2% level. That’s what the good, old Philips curve suggests.

But anyway, the reasoning goes as usual.

A CPI data in line with expectations, or ideally softer-than-expected, will keep the expectation of another rate cut from the Fed in November alive.

We will unlikely see a data soft enough to boost the expectation of a 50bp cut – that expectation is rather boosted by the weakness of jobs data and the latest jobs data was too strong to hold on to it. Atlanta Fed’s GDP Now is now pointing at a growth of more than 3% in the US in the Q3 and that’s not the kind of number that would back another 50bp from the Fed. a sufficiently soft inflation figure will keep the expectation of another rate cut on the table for November.

A stronger-than-expected CPI read could further revive the worries that the Fed may have declared victory over inflation prematurely and boost the bets that it should wait in November to rectify its jumbo cut decision.

What’s easier with inflation – unlike with jobs data – is that a stronger-than-expected inflation is no good news for no one. Therefore, if today’s data isn’t soft enough, we could see the US yields and the dollar extend gains, and the major US indices refuse to renew record. Otherwise, the US dollar’s nascent bullish trend will be questioned and the major US indices will have reason to opt for another fresh high.

In numbers

The US dollar index pushed above its major 38.2% Fibonacci resistance on summer decline, near 102.50, yesterday, and is awaiting the inflation print having stepped into the medium-term bullish consolidation zone. The EURUSD sank below its own major 38.2% retracement on summer rebound and is now consolidating in the medium-term bullish consolidation zone. The USDJPY also traded past its own major 38.2% Fibonacci resistance, near 148.10 level, last Friday and is preparing to test the 150 offers. If the US inflation data is not soft enough, the USD bulls are already in a mood to push the dollar rally further.

CPI from US, Norway and Denmark

In focus today

In the US we get the September CPI figures, which is the most important data release this week. We forecast headline inflation slowing down to 0.1% m/m SA and 2.4% y/y (from 0.2% and 2.6%) mostly driven by lower energy prices, and core inflation to 0.2% m/m SA and 3.2% y/y (from +0.3% and 3.3%). Signs of stickier price pressures especially in the services sector would add to expectations that the Fed opts for only smaller 25bp rate cuts at the coming meetings.

This morning at 10.00 CET, Danske Research hosts a US election webinar, covering fiscal and trade policy outlooks and implications for financial markets.

In Norway, we receive September CPI. We believe that the disinflationary tendency continued, but still expect core inflation to rise to 3.4% y/y, because of unusually low inflation in September last year. If we are right, this will be 0.1 percentage points higher than Norges Bank assumed in the MPR in September and in isolation confirm that there will be no rate cut this year, like we continue to expect.

We expect Swedish August GDP, production and consumption indicators (08.00 CET) all to show some improvement judging from previously released data such as employment, hours worked and retail sales. At 08.30 CET, Riksbank head Thedeén will be discussing the economic policy frameworks together with the head of the Swedish Fiscal Policy Council, Lars Heikensten (previously also head of the Riksbank).

In Denmark September CPI is due for release. Energy prices will drag inflation lower, and we expect a decline to 1.2% from 1.4% in August. The underlying price pressure has remained muted in Denmark despite solid wage growth.

Economic and market news

What happened yesterday

In the US, FOMC minutes suggest that the September rate decision was indeed a close call. The minutes describe that FOMC participants had somewhat differing views on how the easing cycle should be started. 'Some' participants would have preferred a 25bp cut and 'a few others' could have supported such decision. Ultimately, only Bowman dissented from the 50bp cut in the vote. Some emphasized that communicating the outlook for more cuts was more important than the size of the initial cut. So indeed, it was a close call between a 25bp and 50bp moves, as market pricing implied ahead of the meeting. Going forward, we stick to our call for a 25bp rate cut at the next meeting.

In the euro area several ECB members spoke about monetary policy. Villeroy said that a cut is very likely, and that it will not be the last one in this rhythm, but the pace is still dependent on how inflation evolves. In his support to cuts at the two remaining meetings this year, Stournaras argued that monetary policy will still be restrictive after cutting in both October and December. This adds to other members who have spoken for rate cuts over the last couple of weeks, even the traditional hawks Nagel and Kazaks. However, the hawkish tones still exist, for example Wunsch who is undecided as he still sees domestic inflation pressures as too high, and fears that geopolitical tensions could push energy prices higher.

China's Finance Ministry will hold a briefing on Saturday on strengthening fiscal policy. Fiscal measures are typically announced by the Finance Ministry, which is why we did not get any details from the National Development and Reform Commission on Tuesday. The briefing on Saturday is thus the place to look for China's fiscal stimulus plans. We do expect a clear fiscal stimulus plan, but markets will likely be nervous until we see the plans as there is some risk that they underwhelm expectations that have become very high. Still, calm has been restored in Chinese stock markets for now with offshore shares up 4% this morning.

In the Middle East, US president Biden and Israeli prime minister Netanyahu discussed Israel's planned response to Iran's missile attack last week. They also spoke about the Israeli offensive in Lebanon, where President Biden apparently urged Israel to find a diplomatic solution to avoid civilian casualties.

Equities: Global equities were higher yesterday, except for China and Latin America. The uplift in equities was relatively broad-based, although the defensive sectors lagged, particularly utilities which underperformed yet again. Utilities have been one of the best-performing sectors over the summer as yields have been coming lower and equity markets have been choppy. With the latest reassuring job data from the US and a lift in yields it is not so surprising to see the utility sector underperforming. In the US yesterday, the Dow closed up by +0.9%, the S&P 500 by +0.5%, Nasdaq by +0.4%, and the Russell 2000 by +0.4%. The positive sentiment continues in Asia this morning, including sizable lifts in both Chinese A-shares and H-shares. Futures in Europe and the US are also higher this morning.

FI: Global yields continued rising through yesterday's session, as the market-implied number of rate cuts in 2024-25 continues to fade. The repricing of 10Y US Treasury yields over the past week (+30bp) seems hard to justify based on a single strong jobs report, and the move looks much more like an unwinding of excessive positioning towards a 'very dovish Fed' narrative. The Bund curve rose gradually 3bp across tenors yesterday, while the Bund-ASW spread saw marginal widening (now 27bp). Implied vol remains elevated with the MOVE index trading at the highest levels since April. As the US election approaches, implied rates volatility will likely remain elevated.

FX: EUR/USD has firmly consolidated below 1.10 during what has been a relatively uneventful week so far with focus turning to the release of September CPI print this afternoon. NOK continues to trade heavy amid not least oil coming lower and the sell-off in NOK FI losing steam. This morning, we could see some support to NOK though as we expect the monthly CPI release to reveal a print slightly above both markets' and Norges Bank's projections. Akin to EUR/NOK, EUR/SEK edged slightly higher during yesterday's session but remains below the 11.40 mark.

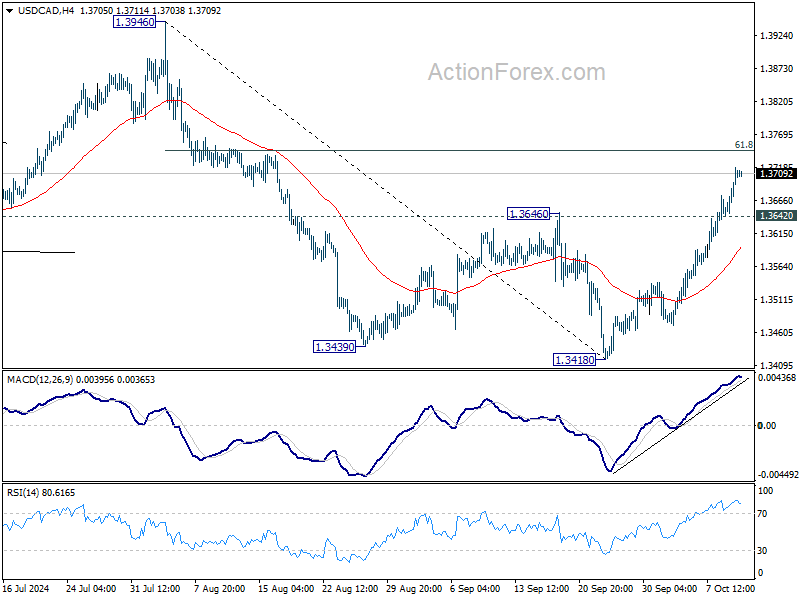

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3663; (P) 1.3691; (R1) 1.3739; More...

USD/CAD's rally from 1.3418 continues today and intraday bias stays on the upside. Pullback from 1.3946 should have completed at 1.3418 already. Rise from there would target 61.8% retracement of 1.3946 to 1.3418 at 1.3559. Decisive break there will target 1.3946 again. On the downside, below 1.3642 minor support will turn intraday bias neutral first.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

Risk Appetite Returns as Focus Shifts to US CPI

Risk-on sentiment is back in the global markets, with DOW and S&P 500 surging to new record highs in the latest session. Notably, this rally isn’t limited to just the big tech giants. ETFs tracking both industrials and financials sectors also closed at record highs, signaling that the strength is broad-based, extending across multiple sectors of the economy.

Today’s spotlight is on the US CPI report, which is expected to show further easing in headline inflation. However, core inflation may continue to show signs of stickiness. This CPI data is unlikely to alter market expectations of a 25bps rate cut by Fed in both November and December, which fed funds futures indicate have over 80% probability. However, the CPI numbers could significantly influence Fed's upcoming economic projections in December, shaping expectations for the first quarter of 2025 and beyond.

In Asia, markets are also staging a strong comeback, with both Hong Kong and China seeing robust rebounds following a bout of extreme volatility. The People’s Bank of China has launched a CNY 500B initiative to inject liquidity into the financial system by allowing institutional investors to swap their bond and stock holdings for government securities. This move, alongside expectations for a fiscal stimulus announcement during Finance Minister Lan Foan’s press conference on Saturday, is bolstering market sentiment in the region.

Currency markets, meanwhile, show a familiar theme of strength in Dollar, which remains the strongest performer of the week so far, followed by Euro and Swiss Franc. Commodity-linked currencies, including New Zealand Dollar, Canadian Dollar, and Australian Dollar, continue to underperform despite today's recovery. Yen and Pound are holding in mid-range positions.

Technically, USD/JPY's rally from 139.57 resumed after brief consolidations. Further rise is expected as long as 147.33 support holds, towards 61.8% retracement of 161.94 to 139.57 at 153.39. The question is, however, whether Japan would step up verbal intervention as USD/JPY rises through 150 psychological level, and the impacts on the markets.

In Asia, at the time of writing, Nikkei is up 0.29%. Hong Kong HSI is up 3.82%. China Shanghai SSE is up 2.72%. Singapore Strait Times is down -0.02%. Japan 10-year JGB yield is up 0.0156 at 0.949. Overnight, DOW rose 1.03% S&P 500 rose 0.71%. NASDAQ rose 0.60%. 10-year yield rose 0.034 to 4.067.

Fed's 50bps rate cut backed by majority, but divisions emerge on future easing pace

Fed's decision to cut interest rates by 50 basis points last month was backed by a "substantial majority," but the minutes of the meeting revealed a more intense debate among policymakers. Only Governor Michelle Bowman dissented, while others showed mixed views on the appropriate pace of easing.

Some participants expressed that a 25bps cut would have been more suitable given inflation remains elevated, economic growth is stable, and unemployment is low. These participants argued that a smaller reduction could support a "more gradual path" for policy normalization, allowing time to assess the economy's response. A few also noted that a 25bps move would signal a "more predictable path" to the markets.

Looking ahead, the split in views deepens. Nearly all participants agreed that the upside risks to inflation had diminished, while most observed increasing downside risks to employment. However, the timing and extent of further rate cuts remain debated.

Some participants stressed that waiting too long to ease policy could "unduly weaken" economic activity and employment, with significant costs if such a weakening were "fully under way". In contrast, others warned that easing "too soon or too much" could risk "stalling or a reversal of the progress on inflation". Given the uncertainty regarding the "longer-term neutral rate" and its implications, some said it's "appropriate to reduce policy restraint gradually".

Fed's Daly: One or two more cuts likely this year

San Francisco Fed President Mary Daly expressed a cautious stance on monetary policy in a discussion last night, indicating that "two more cuts this year, or one more cut this year, really spans the range" of likely outcomes.

With inflation cooling, she noted that inflation-adjusted rates have been rising, which could overburden an economy nearing Fed’s employment and inflation targets. Daly warned that such conditions could "break the economy," stating her desire to prevent further slowing in the labor market.

In a separate speech, Boston Fed President Susan Collins reinforced this measured approach, stating that she supported Fed’s initial 50bps cut and sees further adjustments as likely.

Collins emphasized the importance of a "careful, data-based approach" as rates are lowered to support the economy while ensuring policy remains adaptable to incoming data.

Japan's PPI rises 2.8% yoy in Sep, import prices tumble

Japan’s PPI rose by 2.8% yoy in September, a notable increase from the previous month’s 2.6% yoy and well above the market's expectation of 2.3% yoy.

A significant development was the shift in import prices. Yen-based import price index dropped sharply by -2.6% yoy, turning negative for the first time in eight months. This is a stark reversal from the 10.7% yoy rise recorded as recently as July. Export prices also followed a similar downward trend, falling by -1.0% yoy after previously rising by 2.5% yoy.

On a month-over-month basis, PPI remained flat at 0.0% mom, while yen-based import price index decreased by -2.9% mom, and the export price index fell by -1.7% mom. The decline in both import and export prices reflects a combination of softer global demand and a stronger Yen.

Looking ahead

ECB meeting accounts will be the main focus in European session. Later in the day, US CPI will take center stage while weekly jobless claims will also be published.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3663; (P) 1.3691; (R1) 1.3739; More...

USD/CAD's rally from 1.3418 continues today and intraday bias stays on the upside. Pullback from 1.3946 should have completed at 1.3418 already. Rise from there would target 61.8% retracement of 1.3946 to 1.3418 at 1.3559. Decisive break there will target 1.3946 again. On the downside, below 1.3642 minor support will turn intraday bias neutral first.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

Japan’s PPI rises 2.8% yoy in Sep, import prices tumble

Japan’s PPI rose by 2.8% yoy in September, a notable increase from the previous month’s 2.6% yoy and well above the market's expectation of 2.3% yoy.

A significant development was the shift in import prices. Yen-based import price index dropped sharply by -2.6% yoy, turning negative for the first time in eight months. This is a stark reversal from the 10.7% yoy rise recorded as recently as July. Export prices also followed a similar downward trend, falling by -1.0% yoy after previously rising by 2.5% yoy.

On a month-over-month basis, PPI remained flat at 0.0% mom, while yen-based import price index decreased by -2.9% mom, and the export price index fell by -1.7% mom. The decline in both import and export prices reflects a combination of softer global demand and a stronger Yen.