Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6720; (P) 0.6745; (R1) 0.6773; More...

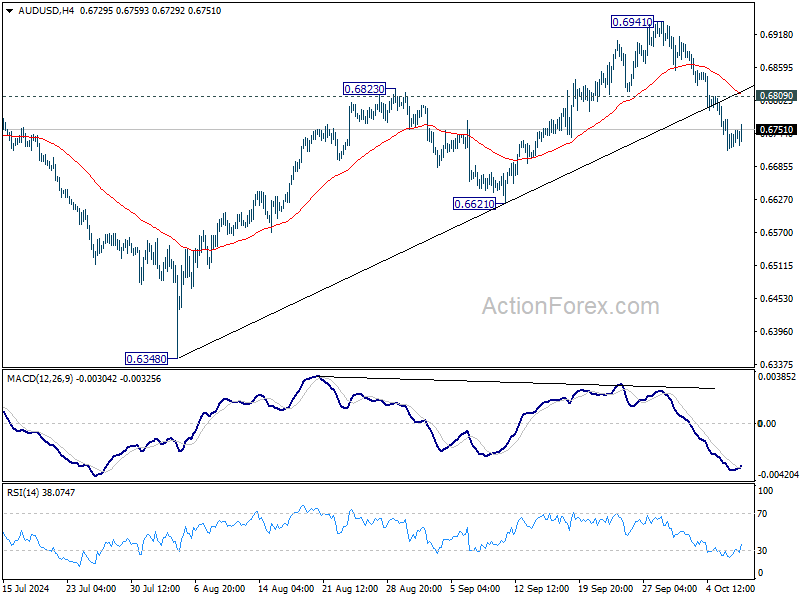

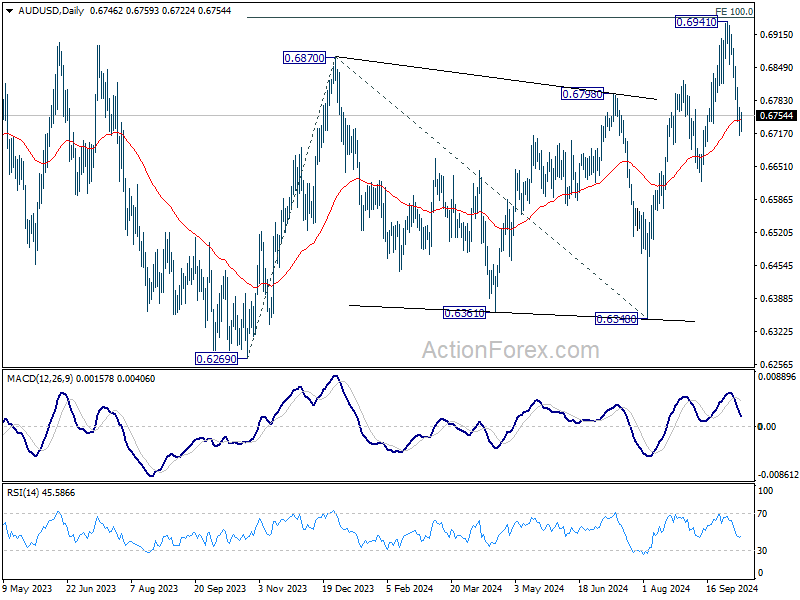

Intraday bias in AUD/USD remains on the downside for the moment. Fall from 0.6941 is in progress. Sustained trading below 55 D EMA (now at 0.6744) should confirm rejection by 0.6941 fibonacci level, and bring deeper decline to 0.6621 support. On the upside, above 0.6809 minor resistance will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.

Kiwi Falls After RBNZ’s 50bps Rate Cut, Risk-Off Sentiment Weighs on AUD

New Zealand Dollar has taken a hit in Asian session after RBNZ delivered a widely expected 50bps rate cut. With excess capacity in the economy, further policy easing is expected, and some economists foresee an additional 50bps rate cut in November. The central bank would continue loosening in the first half of next year, though a return to a more gradual pace of policy changes is likely.

Australian Dollar is also facing pressure, as risk sentiment across the Asian markets has soured, with China at the heart of investor concerns. The Shanghai SSE index has wiped out the post-holiday gains seen yesterday, while Hong Kong equities remain near their lows following Tuesday’s selloff, which was the steepest since the 2008 financial crisis.

Investors were left disappointed by China's National Development and Reform Commission, which offered scant new details on its highly anticipated stimulus package. Instead of fresh fiscal stimulus, the measures appeared to be part of existing plans, further frustrating market participants. China will likely need to intensify efforts to revive market confidence.

In a broader market context, this week has seen a typical "risk-off" environment unfold. Japanese Yen stands as the strongest currency so far, followed by Swiss Franc and Dollar. Meanwhile, New Zealand and Australian Dollars have slumped to the bottom, reflecting weaker risk appetite, with Canadian Dollar joining them as another underperformer. Euro and British Pound are positioned in the middle of the performance table.

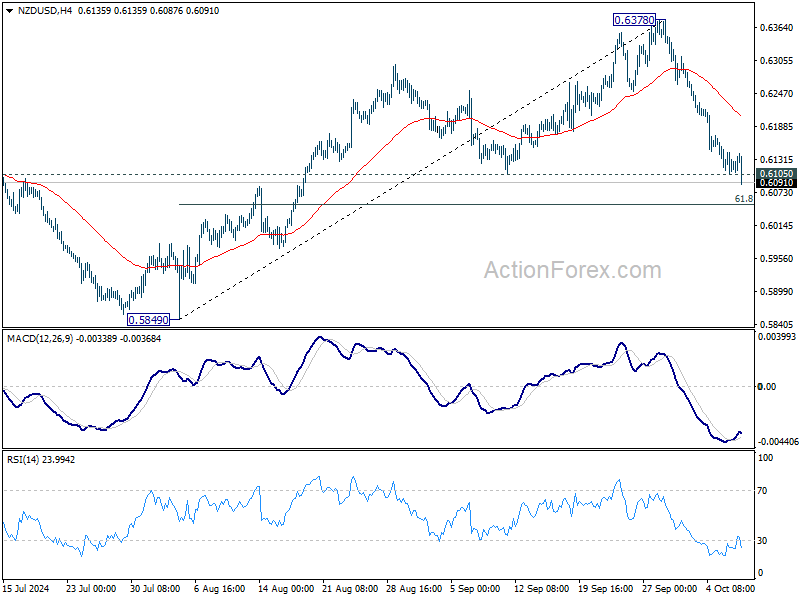

Technically, NZD/USD's break of 0.6105 structural support indicates that rise from 0.5849 has completed at 0.6378 already. Further decline is expected as long as 55 4H EMA (now at 0.6210) holds. Sustained break of 61.8% retracement of 0.5849 to 0.6378 at 0.6051 will pave the way back to 0.5849 support. The question is whether AUD/USD would follow and break through 0.6621 (corresponding support to 0.6105 in NZD/USD) very soon.

In Asia, at the time of writing, Nikkei is up 0.72%. Hong Kong HSI is down -1.39%. China Shanghai SSE is down -5.30%. Singapore Strait Times is up 0.38%. Japan 10-year JGB yield is up 0.0086 at 0.935. Overnight, DOW rose 0.30%. S&P 500 rose 0.97%. NASDAQ Rose 1.45%. 10-year yield rose 0.007 to 4.033.

RBNZ cuts rates by 50bps, citing weak economic conditions and excess capacity

As widely expected, RBNZ cut its Official Cash Rate by 50bps to 4.75%. In its accompanying statement, the central bank emphasized that this move was deemed "appropriate" to achieve and maintain low, stable inflation while minimizing "unnecessary instability" in output, employment, interest rates, and the exchange rate.

RBNZ highlighted that economic activity in New Zealand remains "subdued," with both business investment and consumer spending showing signs of weakness. Employment conditions are also softening, and low productivity growth is acting as a further constraint on activity.

The central bank pointed out that the economy is now in a state of "excess capacity," which is encouraging adjustments in price- and wage-setting behavior, aligning with a low-inflation environment. Falling import prices are aiding the disinflation process.

Additionally, RBNZ noted that despite the rate cut, OCR of 4.75% is still "restrictive" and leaves monetary policy well-positioned to handle any near-term surprises.

Fed's Jefferson: Inflation risks diminished, employment risks rising

Fed Vice Chair Philip Jefferson highlighted the shift in the balance of risks between the central bank's two mandates: inflation and employment.

Jefferson noted at an event overnight that "risks to inflation have diminished," while "risks to employment have risen," bringing these factors into closer balance.

He emphasized that the robust performance of the labor market provided Fed with "headroom" to keep policy in restrictive territory for an extended period.

However, with unemployment drifting upward, now at 4.1%, and inflation closer to the 2% target, Jefferson acknowledged it was appropriate to consider "recalibrating" monetary policy.

Fed's Bostic stays "laser-focused" on inflation

Atlanta Fed President Raphael Bostic reiterated his firm stance on inflation during remarks overnight, emphasizing that inflation remains "too high”. He added, “I want people to understand that I'm still laser-focused on the inflation target.”

Regarding the labor market, Bostic acknowledged that while it has slowed, it is not weak by any means. He said, adding that monthly job creation is still "pretty robust." He also noted that the current unemployment rate, though slightly higher than recent lows, aligns with pre-pandemic levels of full employment.

Fed's Collins: Further rate cuts likely, remain carefully data dependent

Boston Fed President Susan Collins highlighted yesterday that further rate cuts will "likely be needed" to support the economy. However, she emphasized that Fed's policy decisions are not on a "pre-set path" and will remain "remain carefully data dependent".

Collins noted that while core inflation pressures are still elevated, she is gaining confidence that inflation is gradually returning to the 2% target. She also addressed the labor market, noting that the September jobs report, which exceeded expectations, confirms her view that the job market is "in a good place" — neither too hot nor too cold. She stressed that preserving the healthy labor market conditions is crucial and will require economic activity to grow near trend, which remains her baseline outlook for the coming months.

Looking ahead

The economic calendar is rather light today, with German trade balance as the only notable feature in European session. Later in the day FOMC minutes would be the main focus while a number of Fed officials are scheduled to speak.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6720; (P) 0.6745; (R1) 0.6773; More...

Intraday bias in AUD/USD remains on the downside for the moment. Fall from 0.6941 is in progress. Sustained trading below 55 D EMA (now at 0.6744) should confirm rejection by 0.6941 fibonacci level, and bring deeper decline to 0.6621 support. On the upside, above 0.6809 minor resistance will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.

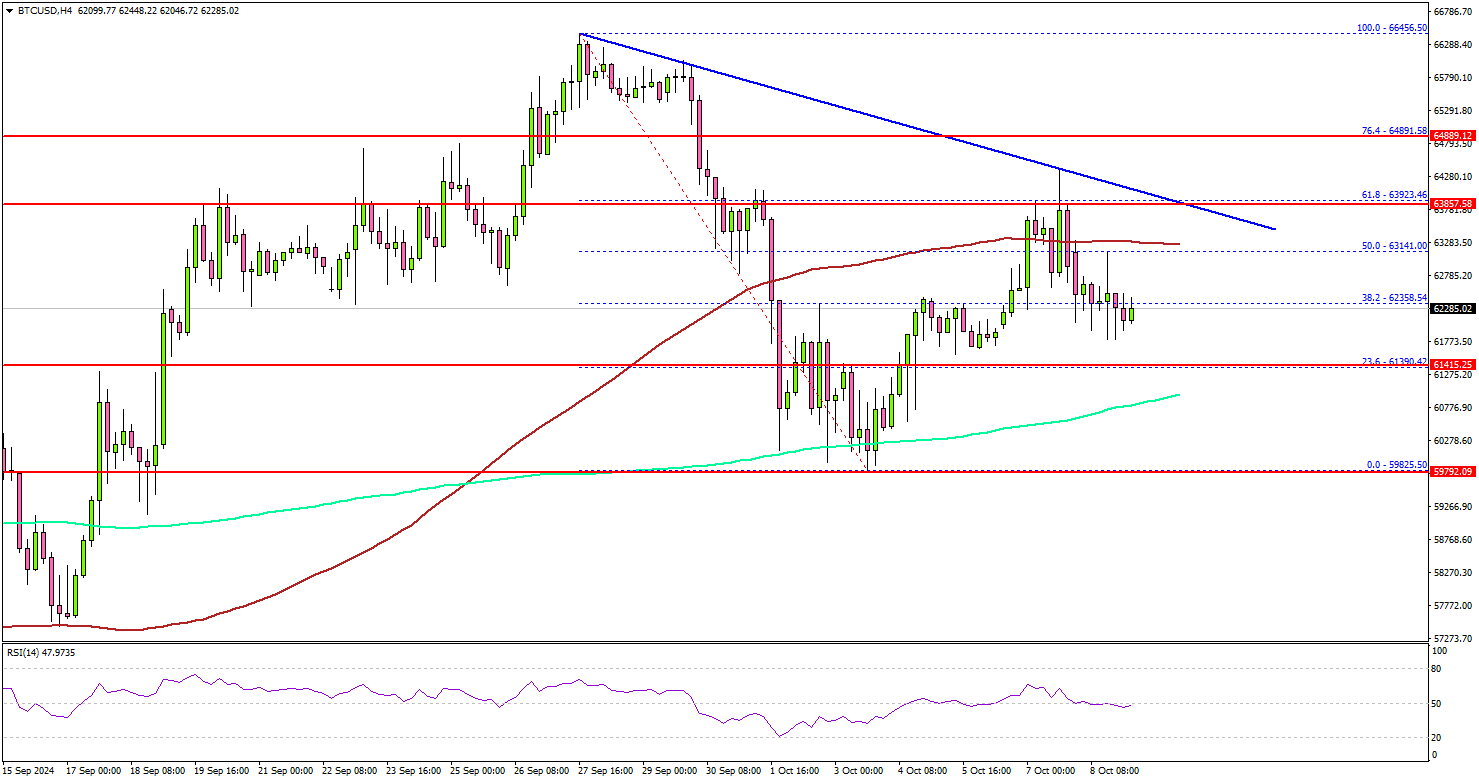

Bitcoin Price Facing Obstacles: Can Bulls Push Through?

Key Highlights

- Bitcoin price struggled to clear the $64,000 resistance zone.

- BTC faced hurdles near a key bearish trend line at $64,200 on the 4-hour chart.

- Oil prices rallied toward $78.80 before the bears appeared.

- EUR/USD is consolidating losses above the 1.0950 zone.

Bitcoin Price Technical Analysis

Bitcoin price started a decent upward move above the $62,000 resistance zone. BTC/USD climbed above the $63,500 resistance before it faced hurdles.

Looking at the 4-hour chart, the price settled above the 200 simple moving average (green, 4 hours) and traded toward the $64,500 resistance zone. It faced resistance near the 61.8% Fib retracement level of the downward move from the $66,456 swing high to the $59,825 low.

The price faced hurdles near a key bearish trend line at $64,200 on the same chart. There was no convincing close above the 100 simple moving average (red, 4 hours).

The price corrected gains and declined below the $63,500 level. Immediate support is near the $62,200 level. The next key support sits at $61,400. A downside break below $61,400 might send Bitcoin toward the $60,500 support. Any more losses might send the price toward the $60,000 support zone.

On the upside, the price could face resistance near the $63,250 level. The next key resistance is at $64,500. A successful close above $64,500 might start another steady increase. In the stated case, the price may perhaps rise toward the $65,500 level.

Looking at EUR/USD, the pair saw a lot of bearish moves, and recently started a consolidation phase above the 1.0950 support.

Today’s Economic Releases

- FOMC Meeting Minutes.

RBNZ cuts rates by 50bps, citing weak economic conditions and excess capacity

As widely expected, RBNZ cut its Official Cash Rate by 50bps to 4.75%. In its accompanying statement, the central bank emphasized that this move was deemed "appropriate" to achieve and maintain low, stable inflation while minimizing "unnecessary instability" in output, employment, interest rates, and the exchange rate.

RBNZ highlighted that economic activity in New Zealand remains "subdued," with both business investment and consumer spending showing signs of weakness. Employment conditions are also softening, and low productivity growth is acting as a further constraint on activity.

The central bank pointed out that the economy is now in a state of "excess capacity," which is encouraging adjustments in price- and wage-setting behavior, aligning with a low-inflation environment. Falling import prices are aiding the disinflation process.

Additionally, RBNZ noted that despite the rate cut, OCR of 4.75% is still "restrictive" and leaves monetary policy well-positioned to handle any near-term surprises.

RBNZ October 2024 Monetary Policy Review: The Wait is Over

- Today the RBNZ cut the OCR by 50bps to 4.75%, meeting Westpac and market expectations.

- According to the RBNZ the economy is now in a position of excess capacity, encouraging price- and wage-setting to adjust to a lowinflation economy.

- Economic activity was described as “subdued”, with business and consumer spending “weak” and employment conditions continuing to “soften”. That weakness was partly ascribed to restrictive monetary policy.

- The MPC agreed that a 50bp easing was most consistent with meeting the inflation target and avoiding unnecessary instability in output, employment, interest rates, and the exchange rate.

- We continue to forecast a further 50bps cut in the OCR on 27 November, and that the OCR will fall to a low of 3.75% in the first half of next year.

OCR cut 50bps as expected as inflation risks move into better balance.

Going into today’s RBNZ policy review, the only question was the size of the OCR cut that the Bank would choose to deliver. As it turns out, the RBNZ chose to cut the OCR by 50bps to 4.75%, as was expected by Westpac, most economists and as largely priced by markets. And looking ahead, the brief policy statement and the record of meeting indicate that a further cut in the OCR of 50bps can reasonably be expected at the next meeting on 27 November, provided that the dataflow over coming weeks prints broadly in line with our expectations (see further below).

In the accompanying brief policy statement, the RBNZ described economic activity as “subdued”, in part due to restrictive monetary policy. Business investment and consumer spending were described as “weak”. The RBNZ also noted that employment conditions were continuing to “soften”. On a more positive note, it was recognised that some exporters have benefited from improved export prices. However, this was balanced by the observation that global economic growth remains “below trend”. The RBNZ stated that “The outlook for the United States and China is for growth to slow, while geopolitical tensions remain a significant headwind for world economic activity.” Importantly, the RBNZ estimates that the New Zealand economy is now in a position of excess capacity, “…encouraging price- and wage-setting to adjust to a low-inflation economy”, with disinflation assisted by lower import prices.

Further nuance on the key factors considered by the Bank’s Monetary Policy Committee (MPC) in arriving at today’s decision can be found in the unusually brief “record of meeting”. The MPC discussed the respective benefits of a 25bps versus a 50bps cut in the OCR. They agreed that a 50bps cut “…at this time is most consistent with the Committee’s mandate of maintaining low and stable inflation, while seeking to avoid unnecessary instability in output, employment, interest rates, and the exchange rate. The Committee noted that current shortterm market pricing is consistent with this decision.”

The market has reacted to the RBNZ’s decision and message with a modest decline in wholesale interest rates and the NZ dollar. Thirty minutes post the announcement, the 2Y swap has fallen 7bps to 3.64% with the RBNZ’s 27 November meeting now closely to fully priced for a further 50bps rate cut. The NZD/USD has declined by around 25pips.

Our assessment: a further 50bps cut likely at the 27 November MPS meeting.

The RBNZ has delivered as expected. The RBNZ’s assessment is that there isn’t a benefit to maintaining a slow 25bp per meeting pace given that output and employment remain weak, and inflation looks set to print close to 2% very soon. The RBNZ continues to consider the OCR at 4.75% as restrictive.

We saw no pushback on our expectation (and market pricing) for another 50 bp easing at the November Monetary Policy Statement. Hence this remains the modal expected outcome.

The RBNZ rightly notes that their future policy decisions will be influenced by the data to come. The CPI (16 October) and the Labour market reports (6 November) are most prominent to watch out for. We don’t see outcomes in those reports that will push the RBNZ from a further 50bp easing in the November 27 meeting.

Key data and events ahead.

Ahead of the RBNZ’s next policy review several key data releases and events are scheduled. The following seem most important:

- Q3 CPI (16 October): Ahead of the September Selected Prices Indexes (released this Friday), we currently think that the CPI will print close to the 2.3%y/y forecast made by the RBNZ in the August MPS. The October Selected Price Indexes will also be released ahead of the RBNZ’s next policy meeting.

- RBNZ speech on the transmission of policy (16 October): RBNZ Assistant Governor Karen Silk will give an on the record speech on the transmission of monetary policy to financial conditions, which may provide some insights as to how the RBNZ is viewing financial conditions in the wake of recent rate cuts.

- Q3 labour market data (6 November): We presently forecast a rise in the unemployment rate to 5.0%, matching the RBNZ’s August MPS forecast. News on developments in labour costs will also be of interest, to confirm that growth is slowing in response to looser labour market conditions.

- Q4 RBNZ expectations survey (11 November): A large decline in inflation expectations over the past two surveys has contributed to the RBNZ’s dovish change in stance, so the updated survey will also be of interest.

- Global events: The US election on 5 November and Federal Reserve policy meeting on 7 November will have implications for the economic outlook and financial markets. Any further stimulus measures announced by China could also be important.

In addition to the above, we expect the RBNZ will pay very close attention to high frequency measures of business activity (such as the Business NZ PMIs, ANZ business survey) and of behaviour in the consumer sector (electronic card spending and housing market activity and prices). Developments in key export and import commodity prices and broader financial conditions (including the exchange rate) will also be relevant.

(RBNZ) OCR 4.75% – Monetary restraint reduced as inflation converges to target

Media release

The Monetary Policy Committee today agreed to cut the Official Cash Rate (OCR) to 4.75 percent. The Committee assesses that annual consumer price inflation is within its 1 to 3 percent inflation target range and converging on the 2 percent midpoint.

Economic activity in New Zealand is subdued, in part due to restrictive monetary policy. Business investment and consumer spending have been weak, and employment conditions continue to soften. Low productivity growth is also constraining activity.

Some exporters have benefited from improved export prices. However, global economic growth remains below trend. The outlook for the United States and China is for growth to slow, while geopolitical tensions remain a significant headwind for world economic activity.

The New Zealand economy is now in a position of excess capacity, encouraging price- and wage-setting to adjust to a low-inflation economy. Lower import prices have assisted the disinflation.

The Committee agreed that it is appropriate to cut the OCR by 50 basis points to achieve and maintain low and stable inflation, while seeking to avoid unnecessary instability in output, employment, interest rates, and the exchange rate.

Summary Record of Meeting – October 2024

Members of the Monetary Policy Committee agreed that the stance of monetary policy has been consistent with ensuring low and stable inflation. Since the August Monetary Policy Statement, the New Zealand economy has evolved largely as expected. The Committee agreed that excess capacity has dampened inflation expectations, and price and wage changes are now more consistent with a low-inflation environment. New Zealand’s annual consumer price inflation is assessed to currently be within the Committee’s 1 to 3 percent target band and is expected to converge to the target midpoint.

Members observed that global economic activity remains below trend

Global economic growth remains below its long-run trend and is expected to remain so for the year ahead. Economic growth in the United States and China is expected to slow. The disinflationary process in advanced economies has led to further reductions in official policy interest rates.

The Committee agreed that domestic activity is weak

Members agreed that increasing excess capacity is leading to lower inflationary pressure in the New Zealand economy. Economic growth is weak, in part because of low productivity growth, but mostly due to weak consumer spending and business investment. High-frequency indicators point to continued subdued growth in the near term. Some exporting businesses have been supported by higher export prices, particularly in the dairy industry.

Labour market conditions are expected to ease further, with filled jobs and advertised vacancy rates continuing to decline. More generally, weak house price growth, lower levels of net immigration, and ongoing fiscal consolidation from spending restraint, are expected to constrain aggregate demand growth.

The Committee noted that while wholesale and bank interest rates have declined, financial conditions remain restrictive, and credit demand remains subdued. The current preference for shorter-term mortgage rates by borrowers will increase the speed with which changes in the OCR influence household cashflows over coming months.

Members are confident that inflation is converging to target

The Committee agreed that monthly price indices signal a continued decline in consumer price inflation in New Zealand. Recent business visits suggest that weak demand is restricting the pass-through of increased input costs to prices faced by consumers. This is consistent with business surveys, which show a declining share of businesses intending to increase prices. Business price-setting behaviour is now more consistent with the Committee’s inflation remit.

The Committee assesses headline consumer price inflation to be within its 1 to 3 percent target band in the September 2024 quarter and to remain around the midpoint in the medium-term.

The Committee considered global and domestic risks

Members discussed how recent events in the Middle East could pose significant risks to both global economic activity and energy prices. Should conflict escalate, oil prices and shipping costs could rise, and adverse investor sentiment could trigger asset price corrections and tighter financial conditions. Members noted that the current market pricing of risk was especially sensitive to downside economic surprises.

Uncertainty about the effectiveness of recent policy actions in China also posed downside risks to New Zealand’s export growth, as well as export and import prices. Heightened uncertainty around the US elections, and the implications for US trade and fiscal policies, could also be significant for international financial markets and global economic activity.

Members noted that while domestic price-setting behaviour is now more in line with its mandate, there are still risks that further adjustments might be faster or slower than currently expected.

Members agreed to ease monetary restraint

The Committee agreed that the economic environment provided scope to further ease the level of monetary policy restrictiveness, consistent with its mandate of low and stable inflation.

The Committee discussed the respective benefits of a 25-basis point versus a 50-basis point cut in the OCR. They agreed that a 50-basis point cut at this time is most consistent with the Committee’s mandate of maintaining low and stable inflation, while seeking to avoid unnecessary instability in output, employment, interest rates, and the exchange rate. The Committee noted that current short-term market pricing is consistent with this decision.

The Committee acknowledged that the outlook is broadly consistent with the August Monetary Policy Statement. Members agreed that an OCR of 4.75 percent is still restrictive and leaves monetary policy well-placed to deal with any near-term surprises. The Committee confirmed that future changes to the OCR would depend on its evolving assessment of the economy.

On Wednesday 9 October 2024, the Committee reached a consensus to reduce the Official Cash Rate by 50 basis points, from 5.25 percent to 4.75 percent.

Attendees

MPC members: Adrian Orr (Chair), Bob Buckle, Carl Hansen, Christian Hawkesby, Karen Silk, Paul Conway, Prasanna Gai

Treasury Observer: James Beard

MPC Secretary: Marea Sing

Fed’s Jefferson: Inflation risks diminished, employment risks rising

Fed Vice Chair Philip Jefferson highlighted the shift in the balance of risks between the central bank's two mandates: inflation and employment.

Jefferson noted at an event overnight that "risks to inflation have diminished," while "risks to employment have risen," bringing these factors into closer balance.

He emphasized that the robust performance of the labor market provided Fed with "headroom" to keep policy in restrictive territory for an extended period.

However, with unemployment drifting upward, now at 4.1%, and inflation closer to the 2% target, Jefferson acknowledged it was appropriate to consider "recalibrating" monetary policy.

Fed’s Collins: Further rate cuts likely, remain carefully data dependent

Boston Fed President Susan Collins highlighted yesterday that further rate cuts will "likely be needed" to support the economy. However, she emphasized that Fed's policy decisions are not on a "pre-set path" and will remain "remain carefully data dependent".

Collins noted that while core inflation pressures are still elevated, she is gaining confidence that inflation is gradually returning to the 2% target. She also addressed the labor market, noting that the September jobs report, which exceeded expectations, confirms her view that the job market is "in a good place" — neither too hot nor too cold. She stressed that preserving the healthy labor market conditions is crucial and will require economic activity to grow near trend, which remains her baseline outlook for the coming months.

Fed’s Bostic stays “laser-focused” on inflation

Atlanta Fed President Raphael Bostic reiterated his firm stance on inflation during remarks overnight, emphasizing that inflation remains "too high”. He added, “I want people to understand that I'm still laser-focused on the inflation target.”

Regarding the labor market, Bostic acknowledged that while it has slowed, it is not weak by any means. He said, adding that monthly job creation is still "pretty robust." He also noted that the current unemployment rate, though slightly higher than recent lows, aligns with pre-pandemic levels of full employment.

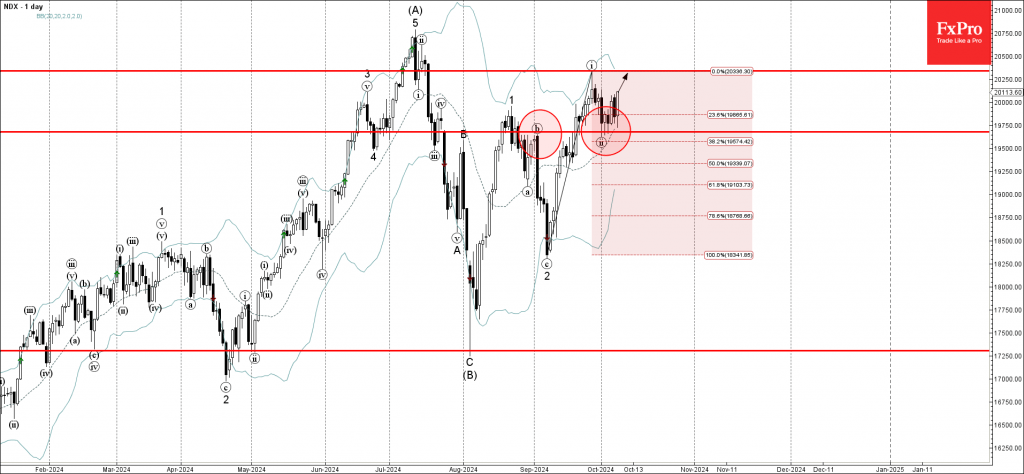

Nasdaq-100 Wave Analysis

- Nasdaq-100 reversed from support zone

- Likely to rise to resistance level 20340.00

Nasdaq-100 index today reversed up from the support zone located between the pivotal support level 19680.00 (former top of wave b from the start of September) intersecting with the 20-day moving average.

The upward reversal from this support zone stopped the previous short-term correction ii.

Given the clear daily uptrend, Nasdaq-100 index can be expected to rise further to the next resistance level 20340.00, high of the previous impulse wave i.