Sample Category Title

Australia’s NAB business confidence improves to -2, inflation pressures still high despite easing costs

Australia’s NAB Business Confidence improved in September, rising from -5 to -2. Business conditions also increased from 4 to 7, with key components such as trading conditions rising from 8 to 12, profitability up from 2 to 5, and employment conditions also climbing from 1 to 5.

A key positive development was the continued easing in input cost pressures. Labour cost growth slowed to 1.7% in quarterly equivalent terms, down from 1.8% in August. Purchase cost growth eased to 1.2%, from 1.6%.

NAB’s Head of Australian Economics, Gareth Spence, noted that while business conditions have been trending lower over the past 24 months due to slower economic growth, capacity utilization remains significantly above its long-run average.

Spence remarked, “This remains an important dynamic for the RBA where, despite slow growth, inflation remains too high, suggesting that the balance of supply and demand in the economy is yet to fully normalize.”

Australian Westpac consumer sentiment hits 2.5-year high as rate hike fears ease

Australia's Westpac Consumer Sentiment surged by 6.2% yoy in October to 89.8, marking the highest reading since RBA began its tightening cycle two and a half years ago.

Westpac noted that consumer sentiment has been buoyed by interest rate cuts overseas and improving inflation conditions domestically. "Consumers are no longer fearful that the RBA could take interest rates higher," Westpac commented.

In particular, the Mortgage Rate Expectations Index, which tracks expectations for variable mortgage rates over the next 12 months, saw a significant drop of -14.1% mom to 106.4. The index has now declined by one-third since July, as households feel less pressure from future rate increases.

Westpac anticipates that RBA's cash rate target will remain unchanged for the rest of the year. While Q3 CPI data, due on October 30, is expected to show inflation tracking lower, it may not be enough for RBA to "shift to an explicit easing bias" at the November meeting. However, Westpac believes the Board could begin easing its "hawkish hold" and adopt a more neutral policy stance as inflation pressures show signs of abating.

Japan’s real wages fall -0.6% yoy in Aug as inflation outpaces wage growth

Japan's real wages declined by -0.6% yoy in August, marking the first drop in three months. Nominal wages rose for the 32nd consecutive month, increasing by 3.0% yoy, slightly missed market expectations of 3.1% .

The wage growth was not enough to offset inflationary pressures. The CPI used to calculate real wages, which includes fresh food prices but excludes owners' equivalent rent, surged by 3.5% yoy in August, the highest increase since October 2023.

On a positive note, base wages (excluding bonuses and overtime) saw a significant 3.0% yoy increase, the largest rise in nearly 32 years. Overtime pay grew by 2.6% yoy. However, these gains were still outpaced by inflation.

In other data, household spending fell -1.9% yoy in August, but the decline was less severe than the market's expected drop of -2.6%.

Fed’s Musalem urges patience as Kashkari flags shifting balance of risks

In a speech overnight, St. Louis Fed President Alberto Musalem noted last week's employment report, despite exceeding expectations, did not prompt him to alter his baseline outlook for the economy. He added that both inflation and the labor market are currently in a "good place," with risks to the Fed's dual mandate—price stability and full employment—"roughly balanced."

Nevertheless, Musalem expressed caution, arguing that the "costs of easing too much too soon" would outweigh the risks of easing too little. He added that should maintain its approach of "gradual reductions" in interest rates over time, highlighting that "patience" has been key to Fed’s progress on inflation. He maintained that this approach "has served the FOMC well" but was careful not to commit to any specifics regarding the size or timing of future rate cuts.

Separately, Minneapolis Fed President Neel Kashkari echoed Musalem’s sentiment regarding the resilience of the labor market, noting, “It looks like it is still a strong labor market.”

Kashkari acknowledged that traditionally, Fed’s aggressive rate hikes would have led to more significant weakness in employment, but so far, that hasn’t materialized. "We have not seen that, so that's a really good fact that the job market has stayed strong while inflation has come down," Kashkari said.

However, Kashkari did caution that the balance of risks is now shifting "away from higher inflation towards maybe higher unemployment"

ECB’s Cipollone sees slower growth and faster inflation deceleration

ECB Executive Board member Piero Cipollone suggested in an interview that growth may come in "a little bit slower" than previously expected. Weak PMI data is also raising concern. The "signals coming from the real side of the economy are a little bit weak", he added.

Cipollone also noted that inflation is "decelerating faster" than anticipated. "So we will get all this information and reassess the situation on the next monetary policy meeting," he said.

Separately, Governing Council member Robert Holzmann emphasized that, while inflation is "on the right track," core inflation remains problematic. He attributed much of the recent inflation drop to lower energy costs but warned that the underlying inflation picture still "doesn't look so good." Holzmann, who backed the September rate cut, cautioned against assuming that further rate cuts are imminent.

JPY Pairs Approach Key Levels Rapidly

The USDJPY pair has pulled back after reaching its highest level since mid-August, dropping to around 148.00 before recovering slightly. The Japanese Yen gained strength due to comments from Japan’s Vice Finance Minister for International Affairs, which raised concerns about potential market intervention. Additionally, global risk sentiment shifted, with rising geopolitical tensions in the Middle East driving investors towards safer assets like the Yen. However, the US Dollar remains strong after a solid US jobs report on Friday, which lowered expectations of a large interest rate cut by the Federal Reserve. Traders are likely cautious ahead of key events this week, including the release of the Fed’s meeting minutes and important US inflation data. These factors will play a major role in guiding the next moves in the USDJPY pair. In the meantime, market participants will keep an eye on any statements from Fed officials for short-term trading opportunities.

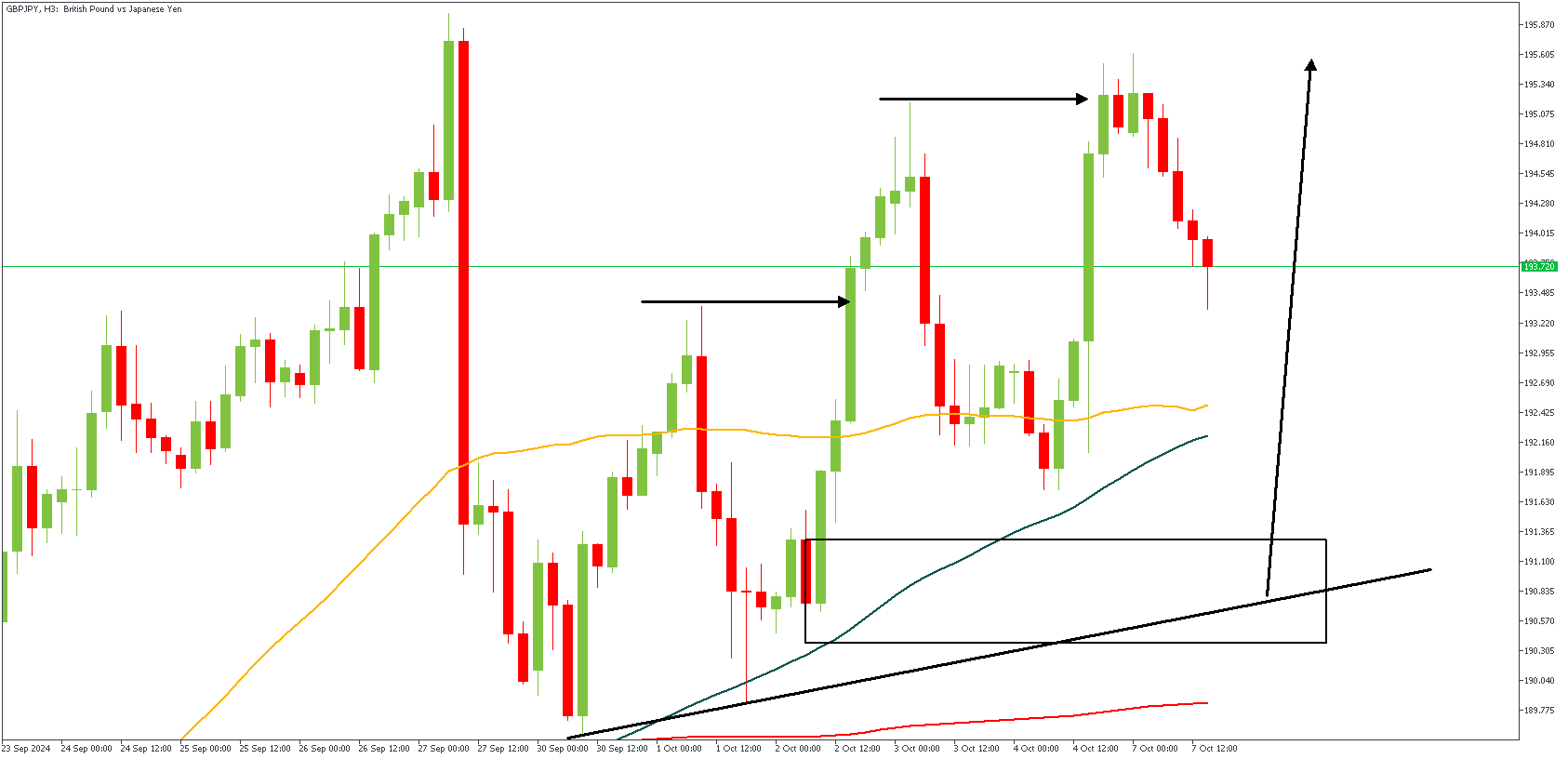

GBPJPY – H3 Timeframe

The 3-hour timeframe of GBPJPY on the currently shows the moving averages arranged in a bullish array. The trendline support is another viable confluence to consider. Additionally, we can see the demand zone, and the break of structure, all these point in favor of a bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 195.623

- Invalidation: 189.899

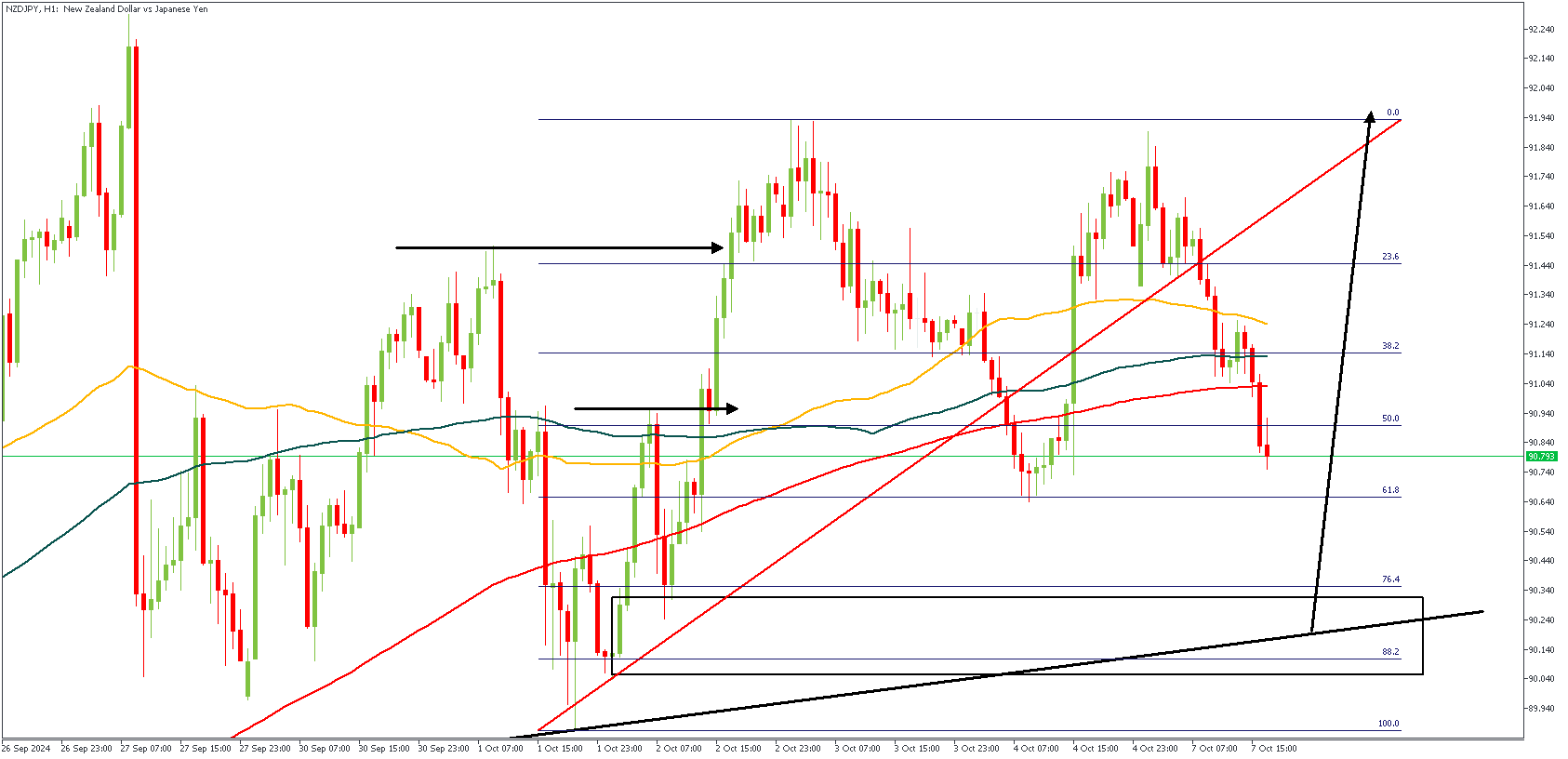

NZDJPY – H1 Timeframe

On the 1-hour timeframe of NZDJPY, we can see the recent break above the previous high. The break of structure is the initial basis of my bullish sentiment. The next confluence is the 76% of the Fibonacci retracement; since it overlaps a drop-base-rally demand zone. The trendline support lends the final clue in favor of the bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 91.970

- Invalidation: 89.838

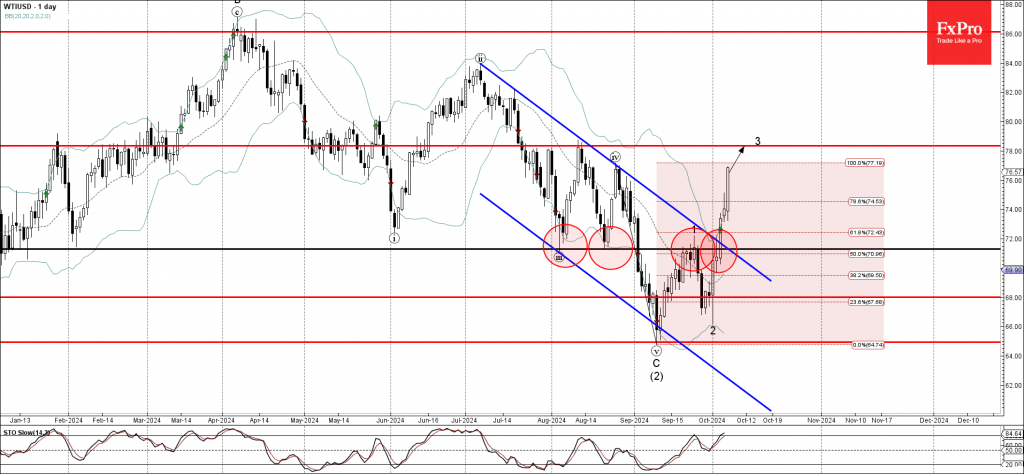

WTI Wave Analysis

- WTI under strong bullish pressure

- Likely to rise to resistance level 78.3

WTI crude oil under the strong bullish pressure after the price broke the resistance level 71.30 (former strong support from August) intersecting with the resistance trendline of the daily down channel from July.

The breakout pf the resistance level 71.30 accelerated the active short-term impulse wave 3.

Given the fact that the price is currently rising inside two impulse waves 3 and (3), WTI crude oil can be expected to fall rise further to the next resistance level 78.3, target for the completion of wave 3.

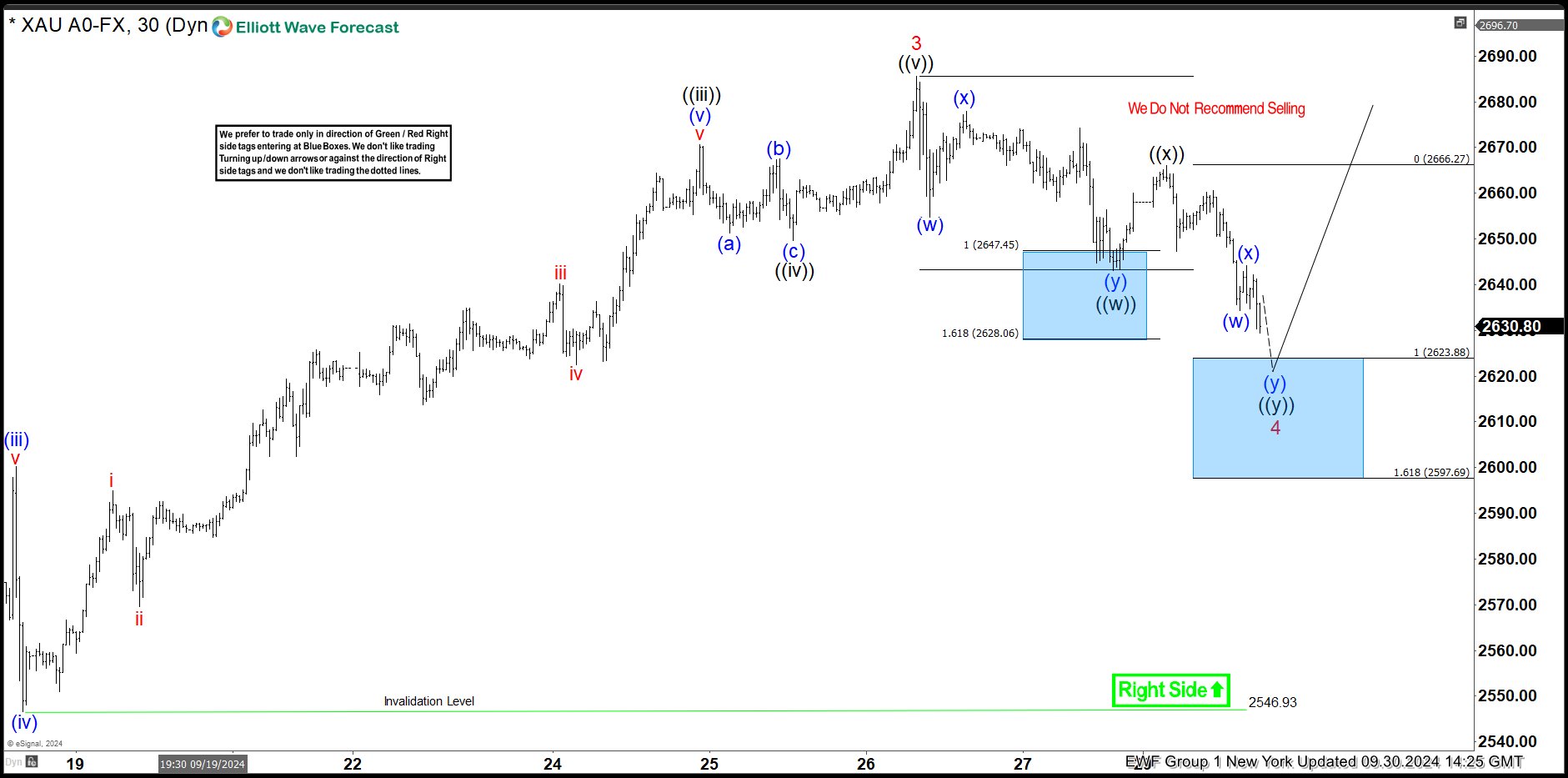

Gold Found Buyers Once Again At The Blue Box Area

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of the Gold. The rally from the 25 July 2024 low showed a higher high sequence & provided a short-term extreme trading opportunity. In this case, the pullback managed to reach the equal legs area & provided a perfect reaction higher. So, we advised members not to sell Gold but to buy the blue box area for a minimum reaction higher to happen. We will explain the structure & forecast below:

Gold 1-Hour Elliott Wave Chart From 9.30.2024

Here’s the 1-hour Elliott wave Chart from the 09/30/2024 NY update. In which, the rally to $2685.58 high ended wave 3 & made a pullback in wave 4. The internals of that pullback unfolded as Elliott wave double three structure where wave ((w)) ended at $2643.02 low. Then a short-term bounce to $2665.99 high-ended wave ((x)) & started the next leg lower in wave ((y)) towards $2623.88- $2597.89 equal legs area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

Gold Latest 1-Hour Elliott Wave Chart From 10.07.2024

Above is the Latest 1-hour Elliott Wave Chart from the 10.07.2024 London update. In which the metal is showing a perfect reaction higher taking place from the equal legs area. Right after ending the correction. Allowed members to create a risk-free position shortly after taking a long position. But a break above $2685.58 high would still be needed to confirm the next leg higher minimum towards the $2699.74- $2723.00 area & avoid double correction lower.

USD/JPY Soars as Rate Hike Hopes Chilled

The yen has stabilized after massive losses last week. In the North American session, the USD/JPY is trading at 148.03 at the time of writing, up 0.45%.

Ishiba’s U-turn sends yen reeling

The yen is coming off a spectacularly bad week with a 4.5% decline. This marked the yen’s worst week since 2020, during the covid pandemic. The sharp decline was driven by the political drama in Japan, which included the election of Shigeru Ishiba as the new prime minister. Ishiba has supported the Bank of Japan tightening policy in the past, but he has taken a U-turn on monetary policy since being elected prime minister.

Ishiba may have shifted his stance in order to avoid any divisive issues, such as raising interest rates, ahead of the snap election on October 27. The election will be followed by the next BoJ meeting on October 31, with the BoJ expected to maintain its policy settings.

On Wednesday, Ishiba met with BoJ Governor Ueda and said that Japan did not need to raise rates further. In a speech to parliament on Friday, Ishiba pledged to defeat deflation, a message which signaled a continuation of “Abenomics”, which advocates an accommodative policy. The yen slid 1.1% on Friday as expectations for a rate hike have evaporated.

Ishiba’s dovish stance and comments by BoJ officials that it the Bank will be extremely cautious before raising rates has dashed expectations for a near-term rate hike and made the Japanese currency less attractive to investors.

US nonfarm payrolls blow past estimate

The US labor market surprised to the upside, as September nonfarm payrolls surged by 254 thousand, up from a revised 159 thousand in August and blowing past the market estimate of 140 thousand. This was the strongest job report in six months. The unemployment rate dipped lower to 4.1%, compared to 4.2% in August and below the market estimate of 4.2%. The markets have raised the odds of a 25-basis point cut at the Fed November meeting to 87%, compared to 65% one week ago.

USD/JPY Technical

- USD/JPY tested support at 147.89 earlier. Below, there is support at 146.78

There is resistance at 149.86 and 150.97