Sample Category Title

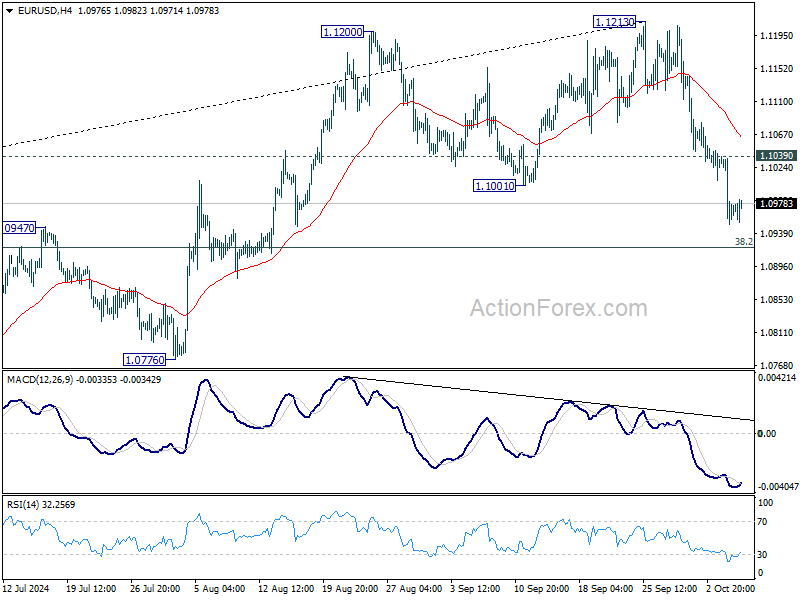

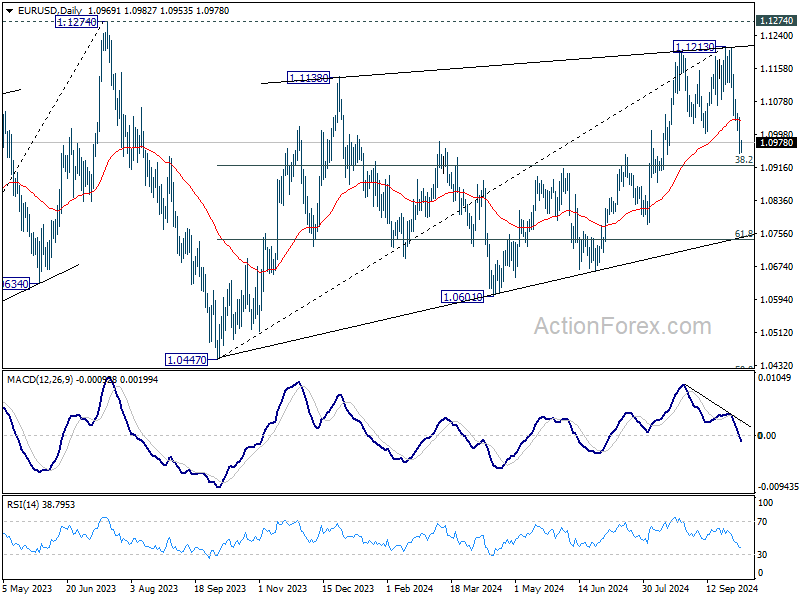

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0937; (P) 1.0989; (R1) 1.1026; More....

EUR/USD's fall from 1.1213 is in progress and intraday bias stays on the downside for 38.2% retracement of 1.0447 to 1.1213 at 1.0920. Sustained break there will argue that fall from 1.1213 is the third leg of the corrective pattern from 1.1274. In this case, deeper decline would be seen to 61.8% retracement at 1.0740 next. On the upside, above 1.1039 minor resistance will turn intraday bias neutral first.

In the bigger picture, rejection by 1.1274 resistance suggests that corrective pattern from 1.1274 (2023 high) is not completed yet. Instead, decline from 1.1213 might be another falling leg. Sustained break of 55 W EMA (now at 1.0877) will validate this case, and bring deeper fall towards 1.0447 support again.

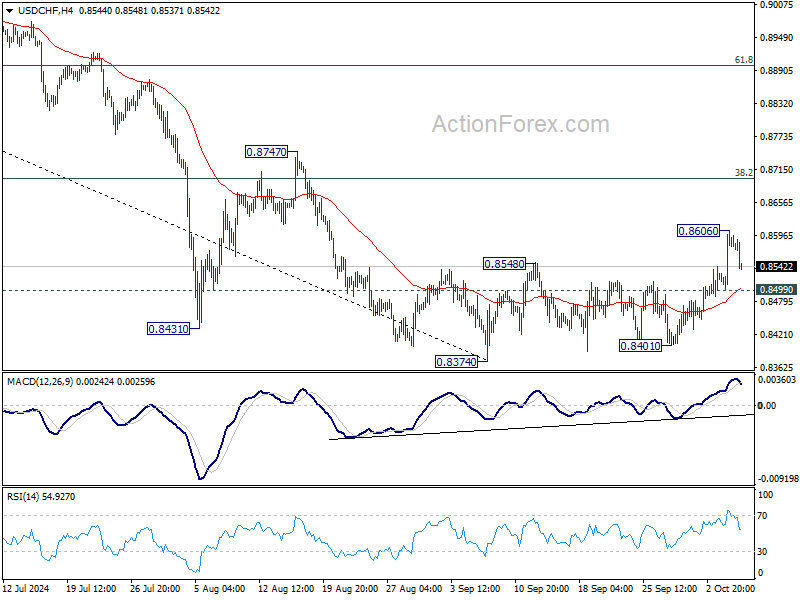

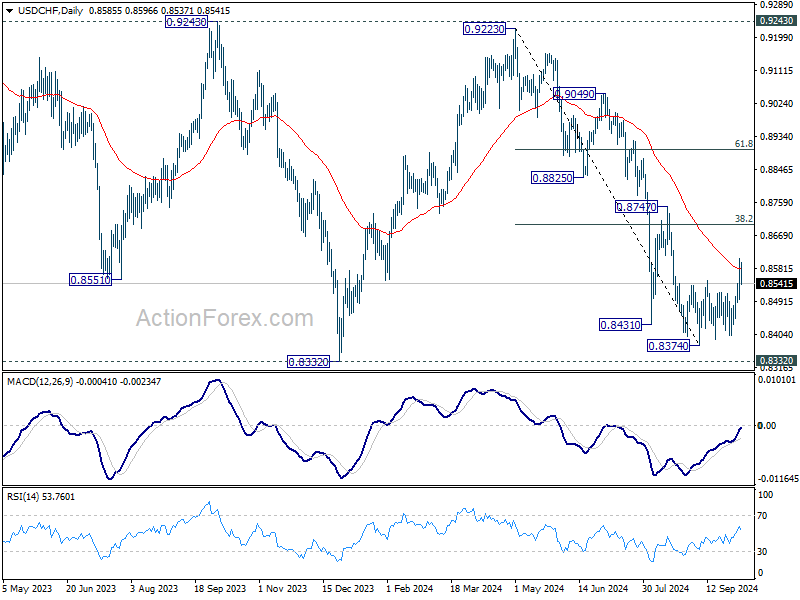

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8518; (P) 0.8563; (R1) 0.8626; More…

Intraday bias in USD/CHF is turned neutral with current retreat and some consolidations would be seen. Further rise is in favor as long as 0.8499 minor support holds. Above 0.8606 will target 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. Next target will be 61.8% retracement at 0.8899. On the downside, break of 0.8499 will turn bias back to the downside for retesting 0.8374 low instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

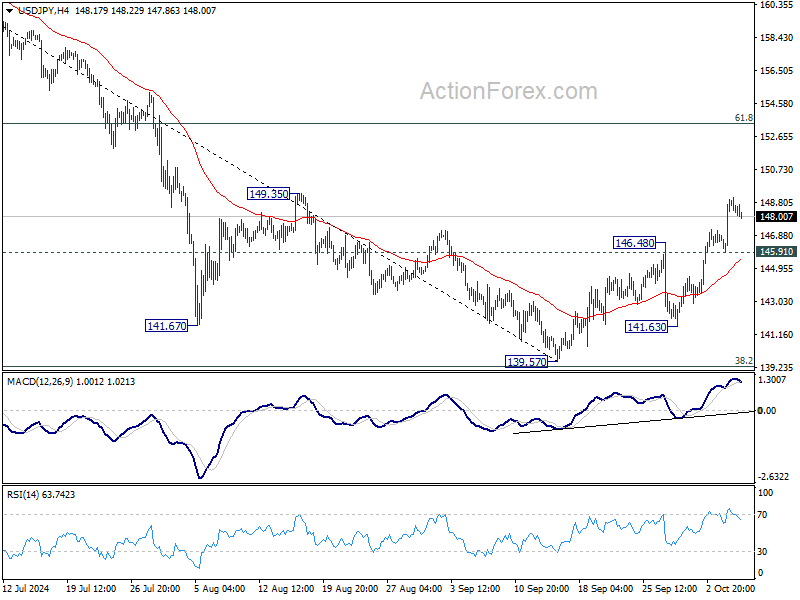

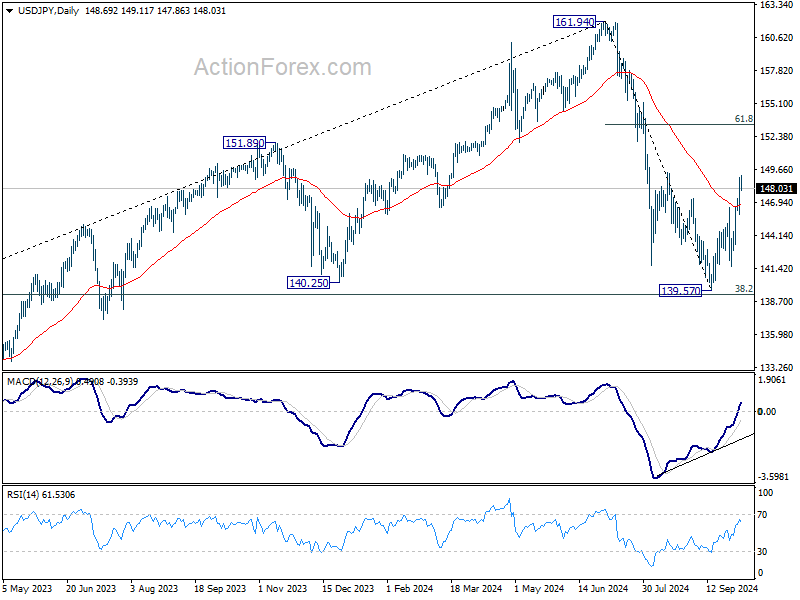

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.78; (P) 147.89; (R1) 149.86; More...

USD/JPY's rebound from 139.57 is still in progress and intraday bias stays on the upside. Rise from 139.57 is seen as the second leg of the corrective pattern from 161.94. Break of 149.35 resistance will target 61.8% retracement of 161.94 to 139.57 at 153.39 next. On the downside, below 145.91 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

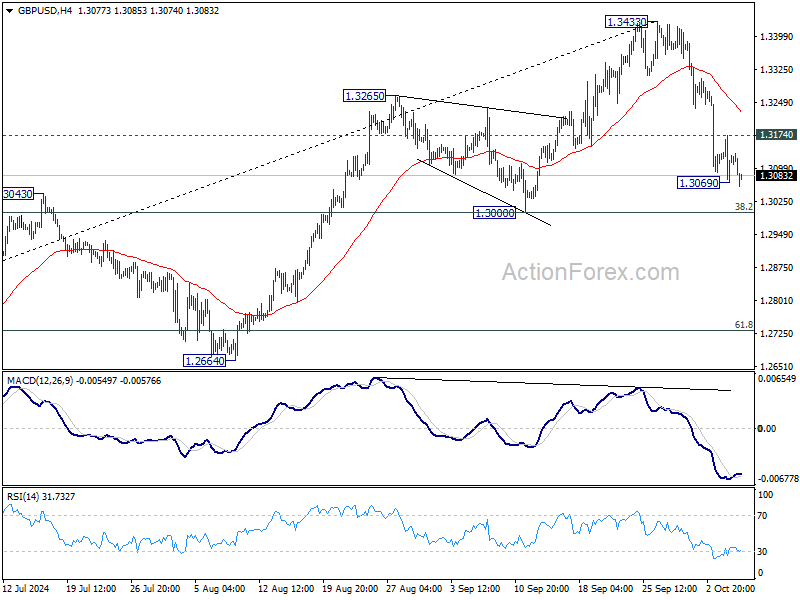

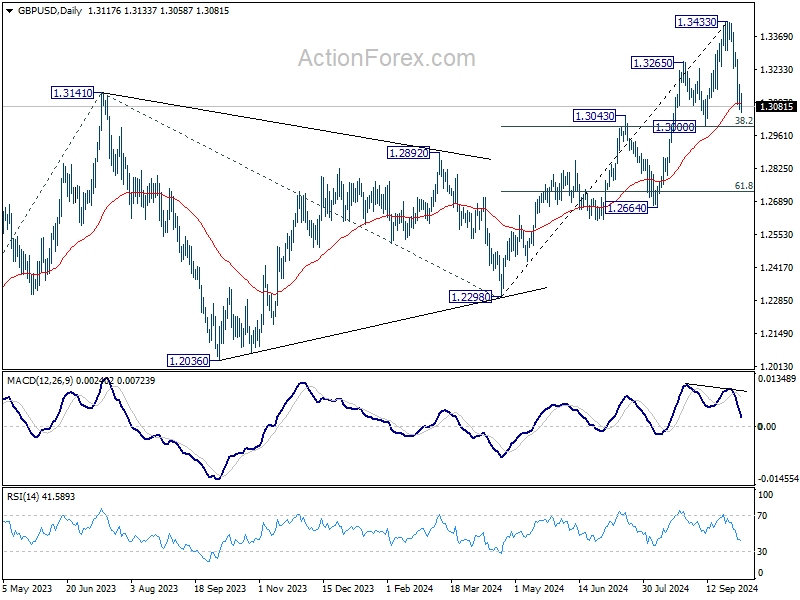

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3072; (P) 1.3123; (R1) 1.3177; More...

Intraday bias in GBP/USD is back on the downside with breach of 1.3069 temporary low. Fall from 1.3433 is in progress for 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999). Strong support should be seen there to bring rebound. On the upside, above 1.3174 minor resistance will turn intraday bias neutral again first.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

Weaker Risk Appetite Drags Sterling Down; Aussie Eyes RBA Minutes and Sentiment Data

Risk sentiment is a little bit subdued as US futures trade in the red ahead of North American session. Yen is recovering broadly, partly supported by Japan’s renewed verbal intervention efforts, with traders closely monitoring the possibility of action if USD/JPY breaches 150 psychological level. Swiss Franc and Dollar are also on the firmer side. On the other hand, Sterling, Kiwi and Loonie are the weaker ones. Meanwhile, Euro and Aussie are mixed in the middle.

Looking ahead, the upcoming Asian session will focus on the release of the RBA minutes, Australia’s Westpac consumer sentiment, and NAB business confidence data. Speculation continues around the timing of the first rate cut by the RBA, with three of the country’s four major banks—Westpac, ANZ, and NAB—forecasting a February cut next year. Commonwealth Bank remains the outlier, predicting a rate cut as early as December. Any sharp deterioration in consumer and business sentiment could prompt a rethink by the RBA. However, the key indicator will still be Q3 CPI data, set to be released on October 30.

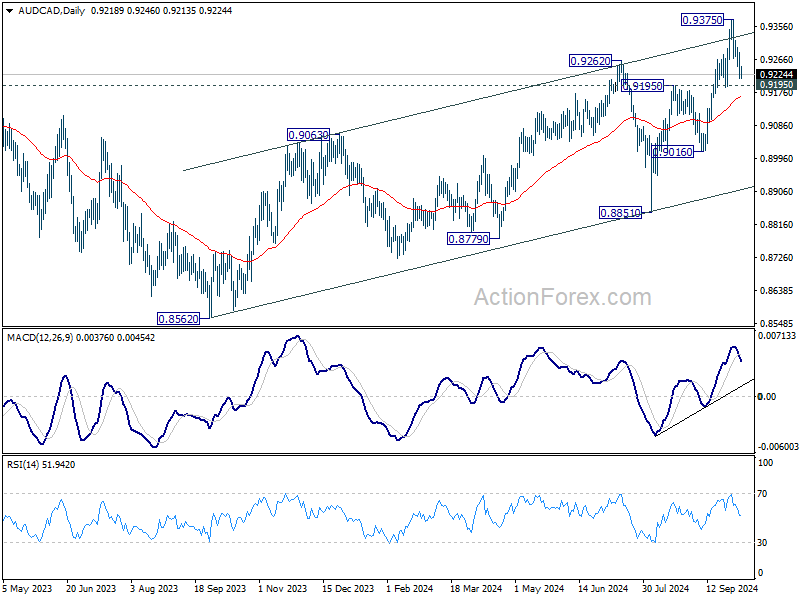

Aussie has been in a mixed path this month, outperforming Kiwi, but lagging behind Loonie. Technically, As long as 0.9195 resistance turned support holds, rise from 0.8562 is still expected to continue through 0.9375 at a later stage. However, firm break of 0.9195 will open up deeper pullback to 0.9016 support, or even further to medium term channel support (now at 0.8912).

In Europe, at the time of writing, FTSE is up 0.48%. DAX is down -0.04%. CAC is up 040%. Germany 10-year yield is up 0.037 at 2.251. UK 10-year yield is up 0.071 at 4.203. Earlier in Asia, Nikkei rose 1.80%. Hong Kong HSI rose 1.60%. China was on the last day of holidays. Singapore Strait Times rose 0.28%. Japan 10-year JGB yield rose 0.040 to 0.926.

Eurozone Sentix rises to -13.8, expectations jump on ECB cut and China stimulus

Eurozone Sentix Confidence Improves Slightly, Expectations Rise Amid Stimulus and Rate Cuts

Eurozone Sentix Investor Confidence edged up in October, rising from -15.4 to -13.8, slightly better than the forecast of -13.9. Current Situation Index saw its fourth consecutive decline, down from -22.5 to -23.3, its lowest level since December 2023. Expectations Index improved notably from -8.0 to -3.8.

Sentix remarked, "The downward economic trend has been halted for the time being," as Eurozone economy attempts to "find its way out of recession/stagnation". Investors are finding renewed optimism, not only due to ECB’s recent rate cuts but also the stimulus measures coming out of China.

The Sentix central bank theme barometer remains supportive, although it has pulled back from the higher levels seen last month. This more moderate outlook is tied to expectations that inflation declines will slow.

Eurozone retail sales rise 0.2% mom in Aug, EU up 0.3%...

Eurozone retail sales volume rose 0.2% mom in August, matched expectations. The increase was driven by a 0.2% rise in food, drinks, and tobacco sales, a 0.3% boost in non-food products (excluding automotive fuel), and a 1.1% jump in sales of automotive fuel from specialised stores.

In the wider EU, retail sales grew by 0.3% month-on-month. Luxembourg led the gains with a 5.3% increase in total retail trade volume, followed by Cyprus at 2.2% and Romania at 1.6%. On the downside, Denmark saw the steepest drop at -1.5%, while Slovakia, Bulgaria, and Croatia also posted declines in retail trade volume.

BoJ upgrades economic outlook for two regions, cautions on wage pressures for small firms

In its latest Regional Economic Report, BoC indicated that all nine regions in the country are "recovering moderately, picking up, or picking up moderately". Also, BoJ upgraded its economic assessments for the Hokuriku and Tokai regions, reflecting stronger local conditions.

In a separate release summarizing discussions among branch managers, BoJ noted that many business leaders increasingly believe wages need to continue rising into next year. This reflects growing wage pressure, which has been a key driver of consumption. Younger workers, in particular, have seen "fairly big pay hikes", boosting their spending power and supporting the broader economy.

However, the central bank cautioned that smaller and medium-sized businesses are struggling to generate sufficient profits to sustain wage hikes. BoJ emphasized that this situation "required vigilance."

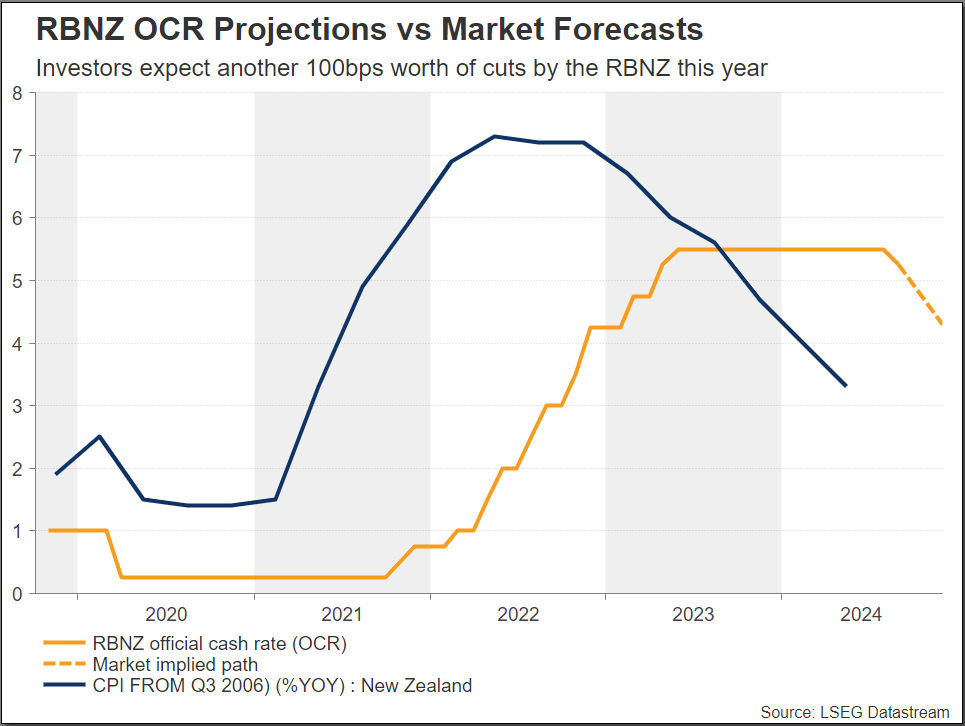

NZIER shadow board evenly split on size of RBNZ rate cut this week

The NZIER Shadow Board is evenly divided on whether RBNZ should lower the OCR by 25 or 50 basis points in its upcoming meeting this week.

Those advocating for a 50bps cut highlighted ongoing economic weakness and rising excess capacity, as well as easing headline inflation and inflation expectations, which they believe justify a larger reduction in rates.

Other members preferred a more cautious 25bps cut, citing persistent risks from non-tradable inflation and recommending a more measured approach.

Looking ahead, the Shadow Board agrees that RBNZ should continue with its easing cycle over the next year, with most members expecting OCR to settle between 3.5% and 4.5%.Some members urged a gradual, data-driven approach, while others argued for more rapid cuts, pointing to weak economic conditions that may require further stimulus.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3072; (P) 1.3123; (R1) 1.3177; More...

Intraday bias in GBP/USD is back on the downside with breach of 1.3069 temporary low. Fall from 1.3433 is in progress for 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999). Strong support should be seen there to bring rebound. On the upside, above 1.3174 minor resistance will turn intraday bias neutral again first.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

RBNZ Policy Meeting: 25 or 50 bps Rate Cut?

- RBNZ decision could shake kiwi/dollar

- As inflation ticks lower, another rate cut is expected

- Policy meeting takes place on Wednesday at 01:00 GMT

RBNZ decision to cut rates

The Reserve Bank of New Zealand is poised to make another rate cut on Wednesday. The RBNZ is expected to follow the Federal Reserve with a half-point cut, as the pressure to reduce real rates at a faster tempo is being exacerbated by a sluggish activity picture and lower inflation. But while a smaller 25-bps reduction cannot be ruled out, markets may continue to favour a dovish pricing approach for an extended period, putting downward pressure on the New Zealand dollar.

Inflation slows down

The inflation rate in New Zealand has been decreasing, and the consumer price index is now approaching the RBNZ's target range of 1-3%. This decline is the result of a decrease in domestic demand pressures and a reduction in imported inflation. It is also anticipated that the inflation of services, which has remained relatively high, will decrease as economic capacity increases.

The New Zealand economy has been showing below-trend expansion in recent quarters, while domestic economic activity has clearly and broadly weakened. The global economic situation affects this slowdown since growth in developed countries stays modest/subdued. However, encouragingly for future price stability, the RBNZ notes that business inflation expectations have fallen to roughly 2% in the medium- and longer-term horizons.

The RBNZ is expected to take a more accommodative approach considering the present economic climate. The stability of inflation expectations and the degree to which price-setting behaviour adjusts to a reduced inflation environment will determine the rate of future rate reductions.

What analysts are saying

Due to the persistent weakness and rising spare capacity in the New Zealand economy, analysts are divided on the extent of the rate cut. Some analysts advocate for a decrease of 50 basis points, while others advocate for no reduction at all. Others propose a 25-basis-point reduction, which is more cautious and accounts for the potential for upside risks in non-tradable inflation. The decision made by the RBNZ will be keenly monitored for any indications related to the future course of monetary policy.

Will this policy meeting affect the kiwi/dollar?

The anticipation of a 50-bps reduction in the RBNZ will have a detrimental effect on the kiwi. Investors are likely to price in a high probability of an additional 50-bps cut for the 27 November meeting, unless there is substantial wording against further half-point reductions ahead. Markets are not entirely pricing in such a move.

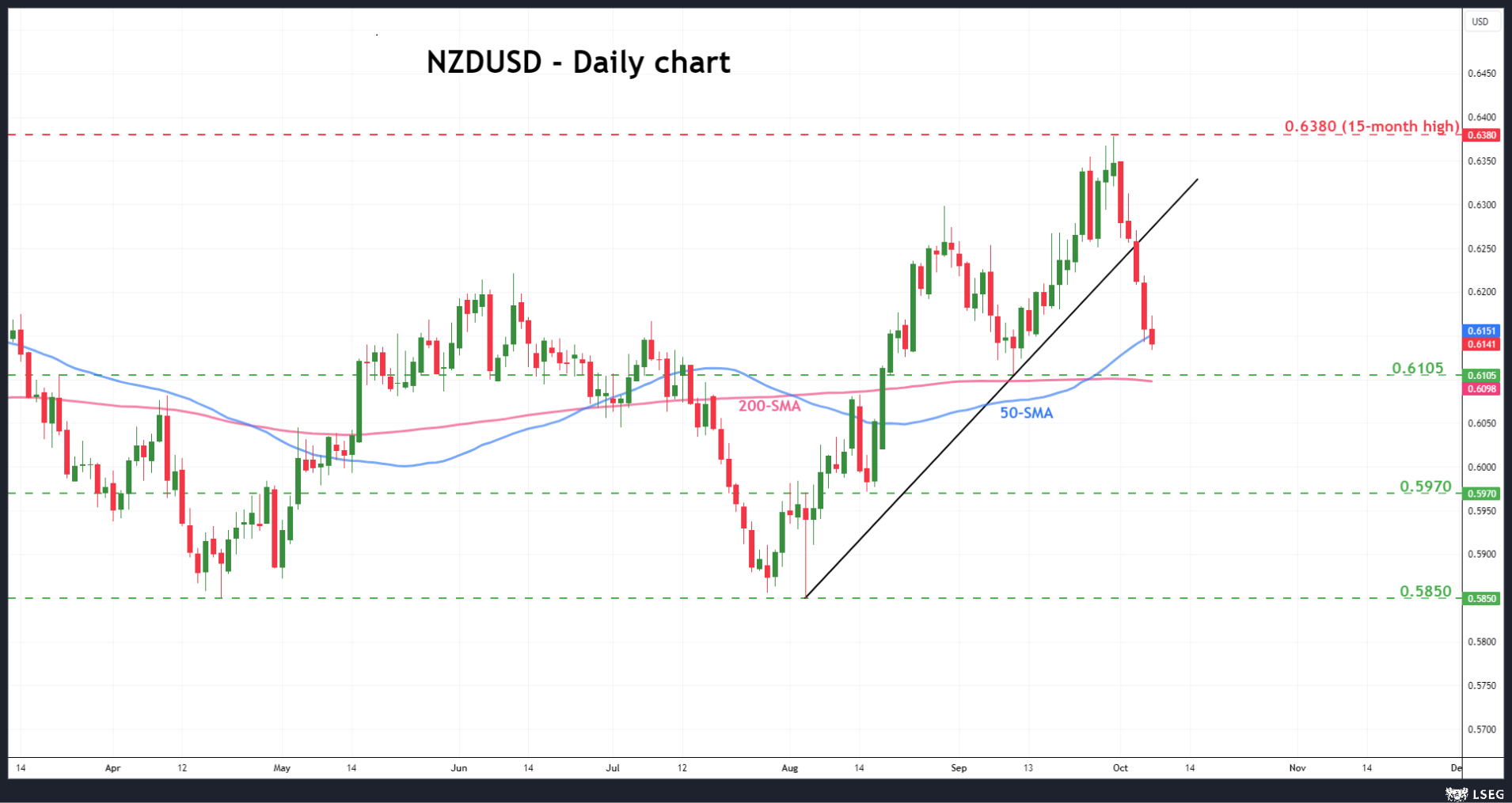

In the end, a non-tradable CPI that is slightly above the consensus when it’s released on October 15 could be beneficial for hawkish repricing and provide some relief to the New Zealand dollar. However, the turbulent risk sentiment situation resulting from Middle East tensions, in addition to potential defensive prepositioning ahead of the US elections, may limit NZD’s rebound attempts. Anything less than 50 bps in the October and November meetings would probably cause a massive move to the currency. Moreover, before the US election, NZD/USD may return to approximately 0.6100.

Currently, kiwi/dollar is experiencing a bearish correction following an aggressive pullback from the 15-month peak of 0.6380 on September 30, which resulted in a loss of more than 3%.

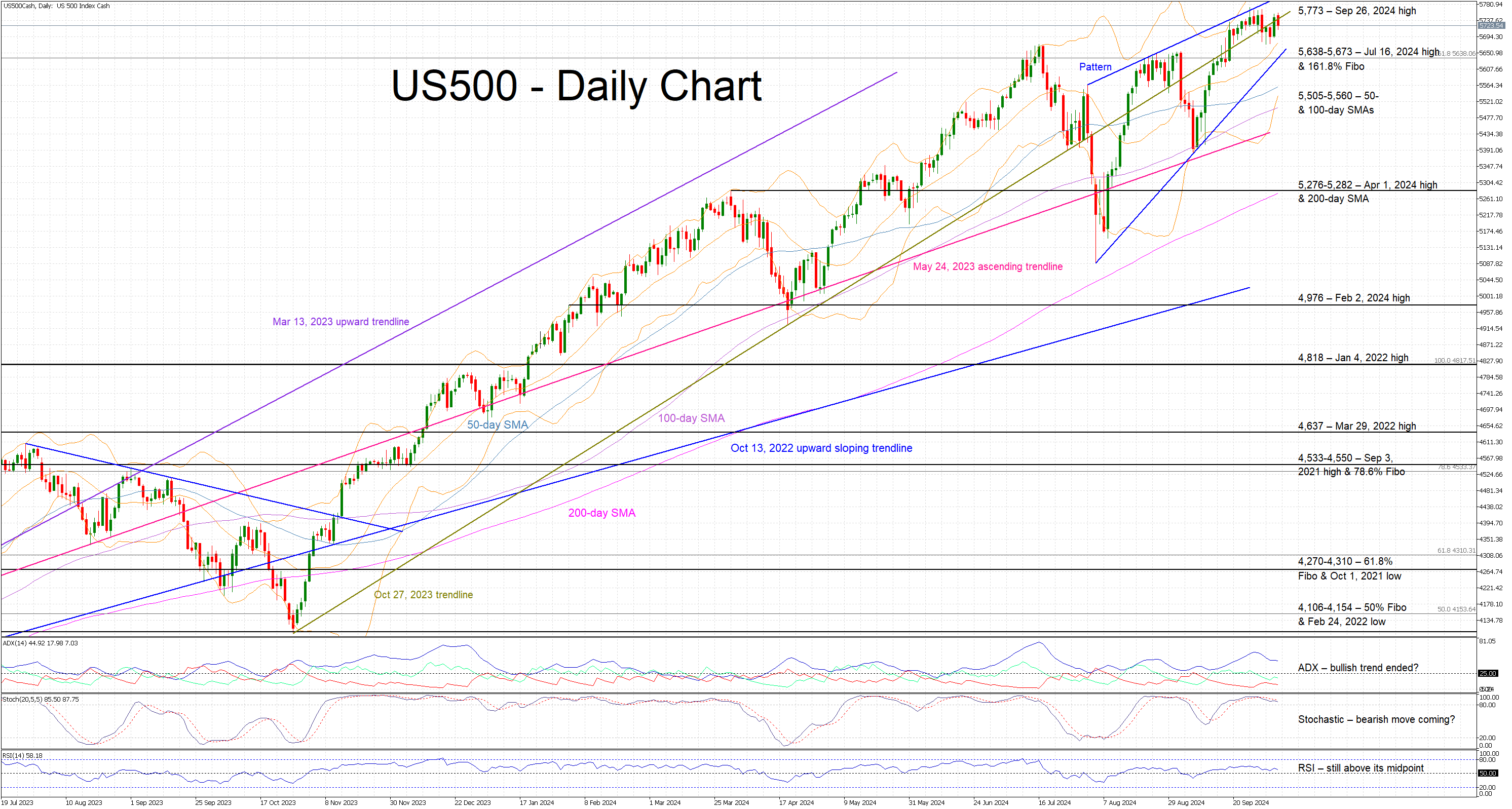

US 500 Pares Post-NFP Gains

- US 500 index is edging lower, erasing part of Friday’s rally

- It remains a tad below its all-time high, inside a pattern

- Momentum indicators could turn bearish soon

The US 500 cash index is edging lower today but remains very close to its recent all-time high. Friday’s strong US jobs report caused a significant repricing of Fed rate cut expectations and resulted in an unexpectedly positive reaction in US equities. However, this move is proving short-lived as today’s price action is erasing a good part of Friday’s rally. With the market’s attention gradually shifting to Thursday’s US CPI report, the US 500 index continues to trade inside a rising wedge, potentially opening the door to a bearish reaction.

In the meantime, the momentum indicators remain hesitantly bullish. The Average Directional Movement Index (ADX) is trading sideways, potentially signalling the end of the recent bullish move. Similarly, the RSI is hovering a tad above its midpoint area, and it appears unable to record a higher high at this stage. Interestingly, the stochastic oscillator is still trading inside its overbought territory (OB), but it could be preparing for a downward breakout. Should this move take place, it would be seen as a strong bearish signal.

Should the bulls remain confident, they can try to overcome the October 27, 2023 upward sloping trendline and then record a new all-time high. The next plausible target is the 5,800 level, with the upper boundary of the developing pattern standing in the bulls' way next.

On the other hand, the bears are trying to retake market control and push the US 500 index lower towards the busier 5,638-5,673 area, which is populated by the July 16, 2024 high and the 161.8% Fibonacci extension of the January 4, 2022 – October 12, 2022 downtrend. A break below the rising wedge pattern could help the bears tackle the expectedly strong support to be met at the 5,505-5,560 region.

To conclude, the US 500 index’s failure to record a high higher coupled with the mixed momentum indicators and the developing pattern, could open the door to a bearish move soon.

Pound Falls to 3-Week Low, Markets Expect BoE Cut in November

The British pound continues to lose ground on Monday after a dismal week. In the European session, GBP/USD is trading at 1.3063, down 0.48% on the day and its lowest level since October 12. The pound can’t find its footing against the rejuvenated US dollar and fell 1.9% last week.

Much of the pound’s slide was driven by comments from Bank of England Governor Bailey. On Thursday, Bailey said that the BoE could cut rates more aggressively if inflation continues to fall. The pound reacted with a slide of 1% after the comments as the markets took Bailey’s remarks as a signal that the central bank is ready to ratchet up the pace of rate cuts. The BoE trimmed rates in August for the first time in four years but paused in September. Another rate cut is widely expected at the November meeting.

A day after Bailey’s remarks, the BoE’s Chief Economist Huw Pill sought to dampen the excitement over potential rate cuts. Pill urged caution and called for a gradual easing of policy. Pill added that service inflation and wage growth were “a continued source of concern”.

US nonfarm payrolls blow past estimate

The US labor market remains resilient, as September nonfarm payrolls soared by 254 thousand, up from a revised 159 thousand in August and crushing the market estimate of 140 thousand. This was the strongest job report in six months. The unemployment rate dipped lower to 4.1%, compared to 4.2% in August and below the market estimate of 4.2%. The markets have raised the odds of a 25-basis point cut at the Fed November meeting to 87%, compared to 65% one week ago.

GBP/USD Technical

- GBP/USD is testing support at 1.3072. Below, there is support at 1.3018

1.3123 and 1.3177 are the next resistance lines

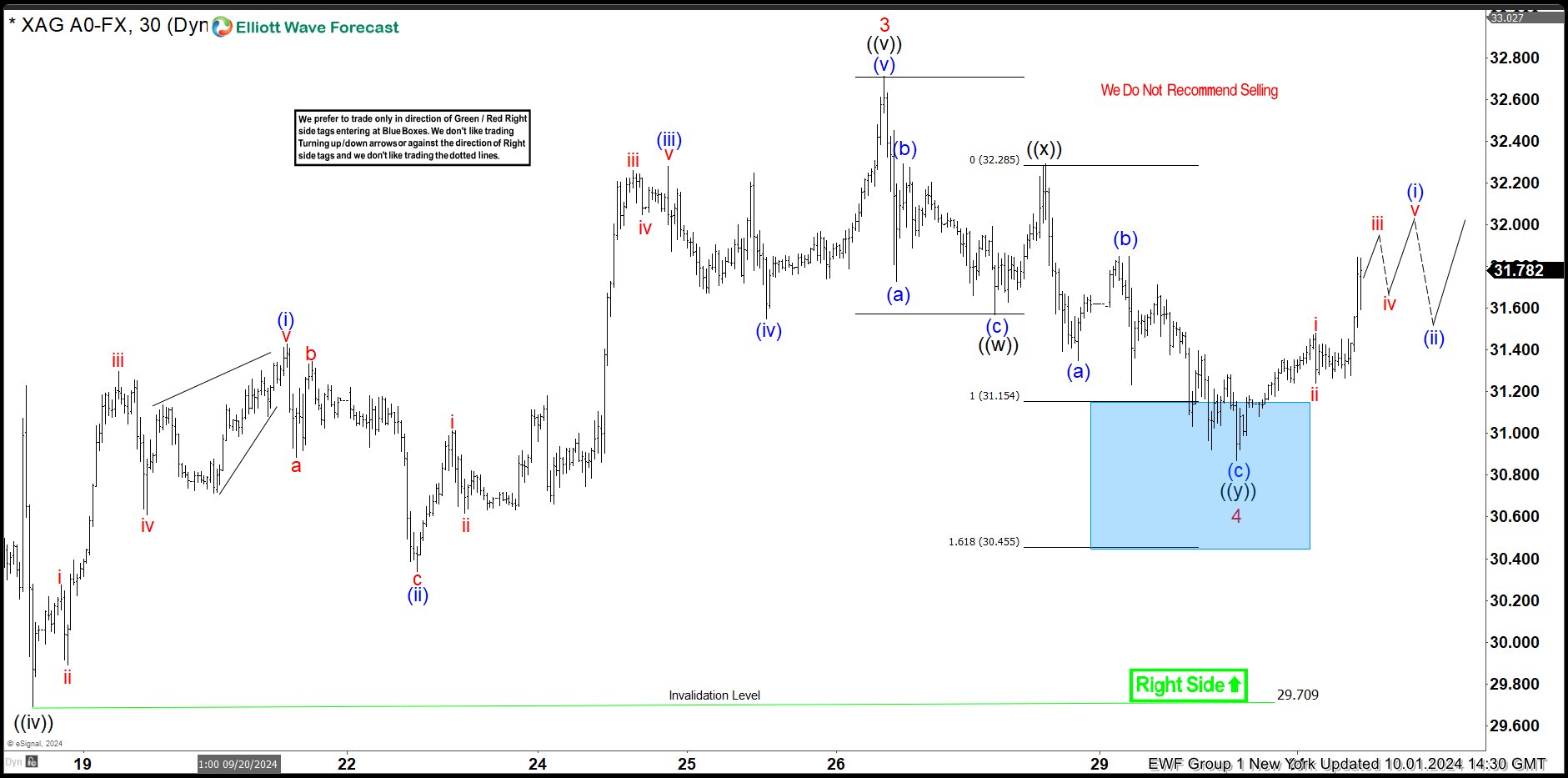

Silver (XAGUSD) Buying the Dips at the Blue Box Area

In this technical article we’re going to take a quick look at the Elliott Wave charts of Silver (XAGUSD ) commodity , published in members area of the website. As our members know, Silver has recently given us correction against the September 6th low. The commodity reached our target zone and completed correction right at the Equal Legs ( Blue Box Area) . In further text we’re going to explain the Elliott Wave pattern and trading setup.

SILVER H1 Update 09.30.2024

The commodity is giving us wave (iv) blue correction. The pull back has incomplete structure at the moment. Consequently, we are looking for another short term low toward the extreme zone ( Blue Box ). However, we don’t recommend selling it. We expect it to attract buyers at the Blue Box zone. The commodity could make either rally towards new highs or a larger corrective bounce in three waves at least. Once the bounce reaches the 50% Fibonacci retracement level against the connector high – x red, we’ll secure our position by moving the stop-loss to breakeven. Break below the marked invalidation level : 30.44 would invalidate the trade.

A quick reminder:

Our charts are designed for simplicity and ease of trading:

Red bearish stamp + blue box = Selling Setup

Green bullish stamp + blue box = Buying Setup

Charts with Black stamps are deemed non-tradable. 🚫

SILVER H1 Update 10.01.2024

SILVER H1 Update 10.01.2024

The commodity made another leg down and found buyers within the Blue Box area as expected. We got a nice rally from our buying zone, consequently counting 4 red pull back completed at 30.86 low. The bounce has exceeded the 50% Fibonacci retracement level against the connector peak – currently marked as ((x)) black. As a result, traders who entered long positions are now enjoying risk-free profits. With the price holding above the 30.86 low, we believe the next leg up can be in progress. For confirmation on the next leg up, we’re looking for a break above the 3 red peak.

SILVER H1 Update 10.05.2024

Eventually the commodity made break of 3 red peak as we expected. We expect Silver to keep trading higher ideally as far as pivot at 30.86 low holds.

Russell 2000: Soft to No-Landing Supporting Another Bullish Upleg

- Better than expected US non-farm payrolls & unemployment rate for September have revived the soft to non-landing narrative.

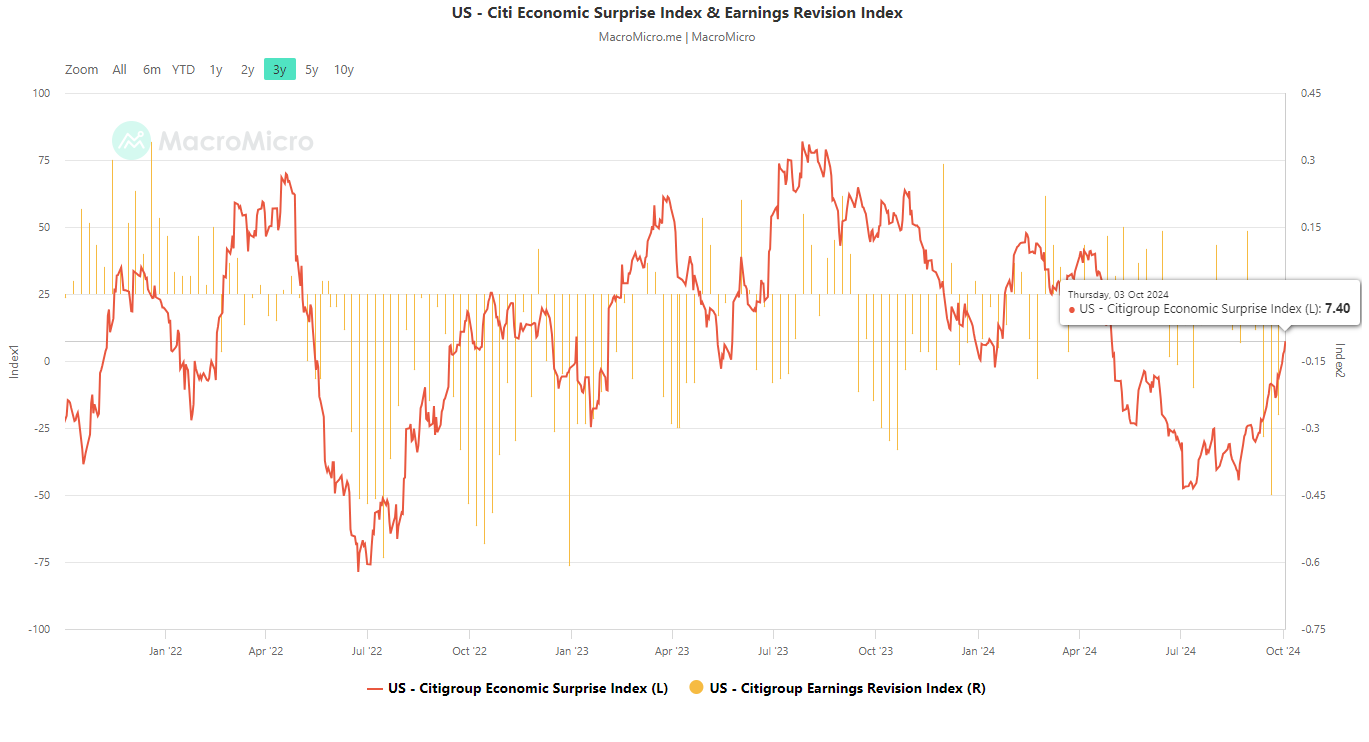

- The Citigroup US Economic Surprise Index has improved significantly since August.

- The improvement in US economic growth prospects is likely to benefit the Russell 2000 at least in the medium-term.

Since our last publication, the performance of Russell 2000 was still down by 2.20% as of last Friday, 4 October close but managed to recover from a synchronized risk-off episode that took shape from late July to early August; since its 5 August low, it has rebounded by 11%.

The latest US non-farm payroll print for September has increased significantly from the prior month and surpassed expectations by a wide margin; +254K jobs added versus +140K consensus estimates and above +159K added for August.

In addition, the unemployment rate for September ticked lower to 4.1% from 4.2% in August which thrust the “soft-landing to no-landing” US economic growth narrative back into the limelight.

Last Friday, the Russell 2000 outperformed among the major US stock indices with a daily gain of 1.50% due to its higher sensitivity towards an improvement in economic growth prospects in the US as it comprises small-cap listed companies that derived most of the revenue streams (close to 80% on the aggregate) domestically in the US.

US economic growth prospects have improved

Fig 1: Citigroup US Economic Surprise Index as of 3 Oct 2024 (Source: MacroMicro, click to enlarge chart)

On an accumulated net basis, more key US economic data came in better than expected in the past month where the Citigroup US Economic Surprise Index has improved significantly from a negative print of -44.50 on 22 August to 7.40 as of 3 October; after it hovered below the negative territory since May (see Fig 1).

Hence, the latest positive trend change seen in the Citigroup US Economic Surprise Index is likely to benefit the laggard Russell 2000 as it is still the only major US stock index among the S&P 500, Nasdaq 100, and Dow Jones Industrial Average that has not scaled new fresh all-time high in past three years; it is still 11% below from its current all-time high of 2,458 printed on 8 November 2021 based on last Friday, 4 October closing price.

2,080 key medium-term support to watch on Russell 2000

Fig 2: US Russell 2000 CFD Index major and medium-term trends 7 Oct 2024 (Source: MacroMicro, click to enlarge chart)

In the lens of technical analysis, the two prior corrective decline sequences of 11% and 14% have managed to find support at the 200-day moving average of the US Russell 2000 CFD Index (a proxy of the E-mini Russell 2000 futures) on 19 April and 5 August which suggests that the major uptrend phase since its 27 October 2023 swing low remains intact (see Fig 2).

Secondly, the daily RSI momentum indicator has continued to print a series of “higher lows” since 7 August which suggests that medium-term bullish momentum has resurfaced.

If the 2,080 key medium-term pivotal support holds, the US Russell 2000 CFD Index may resume its impulsive upmove sequence within its major uptrend phase for the next medium-term resistance to come in at 2,350/390.

However, failure to hold at 2,080 with a daily close below it invalidates the bullish tone for a corrective decline to expose the next medium-term support at 1,990, and even the major support of 1,920/1,890 next.