Sample Category Title

China – Lift to GDP Forecast After Leaders Draw Line in the Sand

- Following the big stimulus and clear growth message from Chinese leaders, we revise up our China growth forecast in 2025 from 4.8% to 5.2%. For 2024 we keep our 4.8% forecast.

- The stimulus is the strongest coordinated push to lift the economy since the global financial crisis in 2008. We expect China to follow up with fiscal stimulus measures on the other side of the National Day holiday.

- The key to turning the Chinese slump is to put a stop to the housing crisis, which we see as the epicentre of current challenges. We now look for a gradual improvement in housing over the next year but not a fast rebound.

- China is set to change from a disinflationary force to a more neutral force. Since we look for the recovery to be gradual we do not expect China to become an inflationary force within the next 6-12 months.

EURUSD & GBPUSD Breakdown

The US Dollar (USD) continued to strengthen against other major currencies on Tuesday, reaching its highest level in nearly two weeks, climbing above 101.00. Investors are keeping an eye on important data, such as the European unemployment rate and US employment numbers from ADP, along with speeches from key Federal Reserve officials.

The USD got a boost on Tuesday after the US reported an increase in job openings for August. However, the manufacturing sector remained weak, as shown by the ISM Manufacturing PMI data, which missed expectations. Concerns over rising geopolitical tensions in the Middle East are also influencing markets. Iran reportedly launched around 200 missiles at Israel, prompting threats of retaliation, which has added uncertainty to the global outlook.

In response, the stock market dipped slightly, while the Euro and British Pound both dropped against the Dollar. Gold prices briefly rose due to the heightened geopolitical risk but are struggling to keep momentum, hovering near $2,650 on Wednesday.

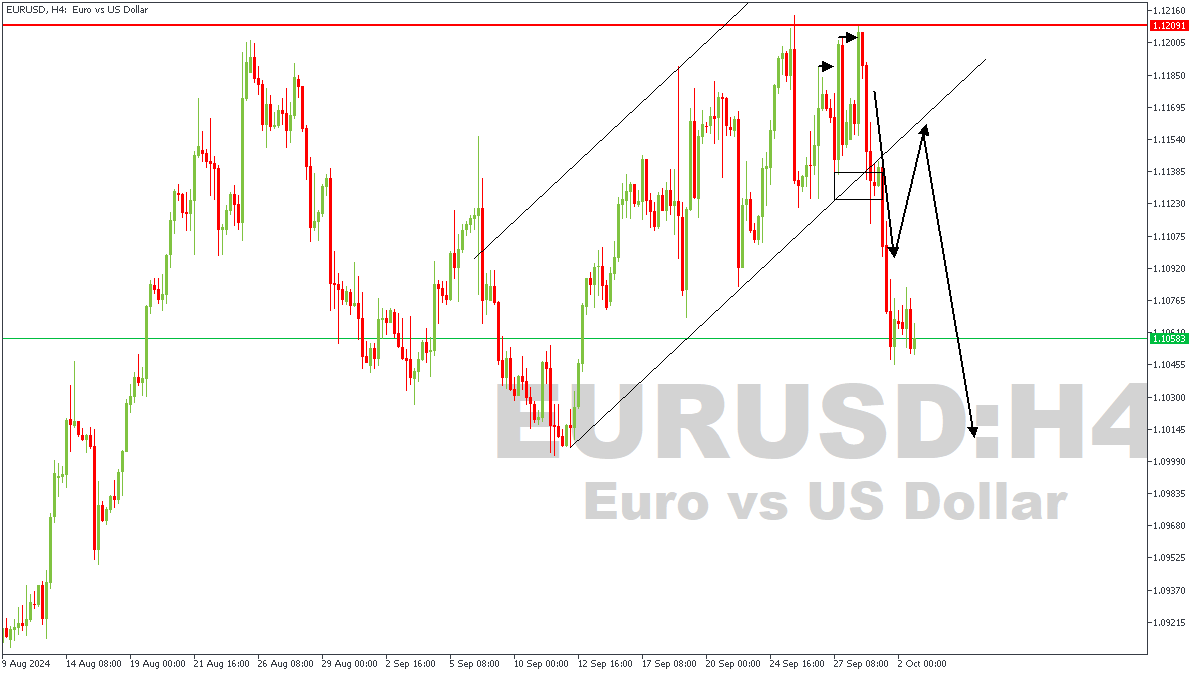

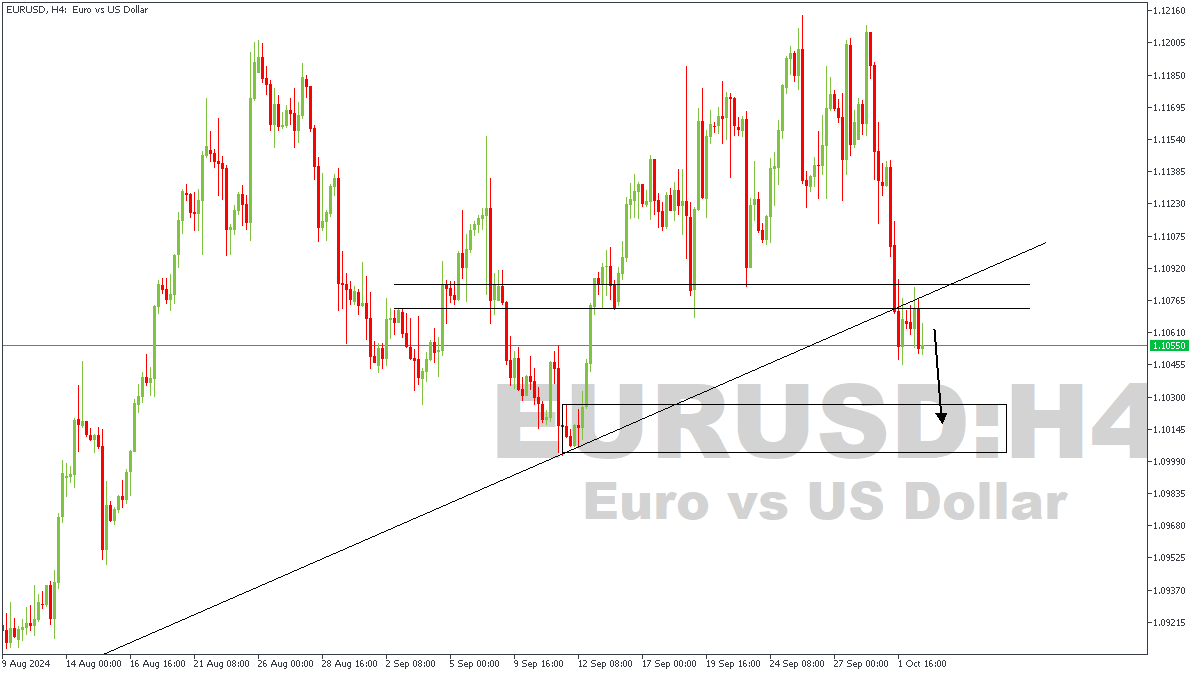

EURUSD – RECAP

On Monday, 30th of September, during the livestream with the VIP community, we took a look at the price action on EURUSD and predicted a drop from the daily timeframe pivot. At this moment, price has completed a 155-pip drop and seems to still have some more to go.

EURUSD – H4 Timeframe

The 4-hour timeframe of EURUSD at the moment indicates price has recently broken below, and retested a pivot region on the 4-hour timeframe. A trendline support was also broken with a retest; the conclusion here, therefore is that price intends to remain bearish.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.10257

- Invalidation: 1.10828

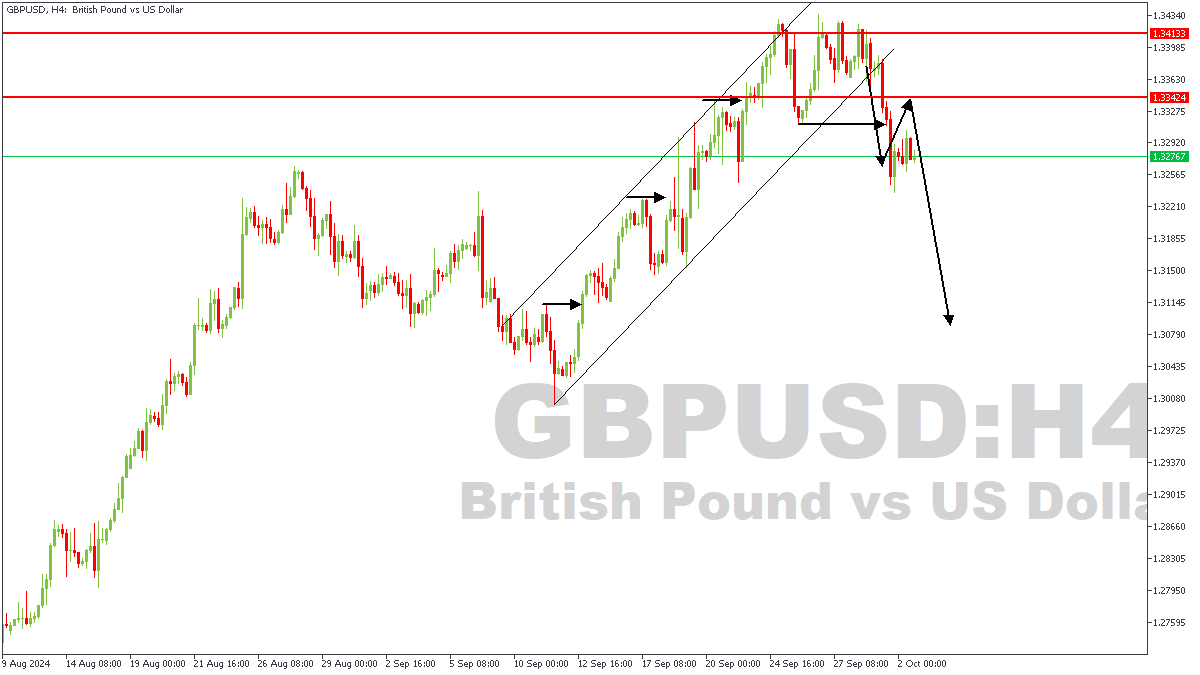

GBPUSD – RECAP

GBPUSD was not left out of the analysis during the Monday Market Review in the VIP community – with Gold going on to drop over 180pips afterwards.

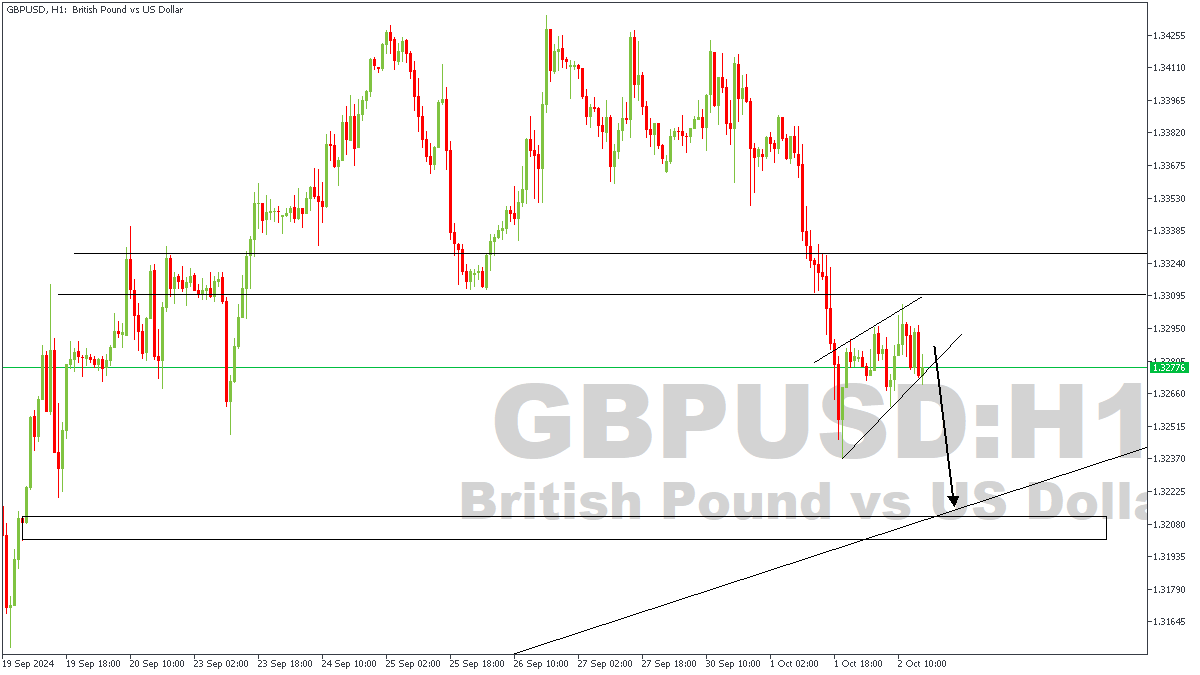

GBPUSD – H1 Timeframe

At the moment on the 1-hour timeframe chart of GBPUSD, price has formed a rising wedge as it approached the recently broken 4-hour timeframe pivot zone. In line with this, I expect to see the bearish momentum continue until it reaches the highlighted area of demand on the chart.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.32127

- Invalidation: 1.32975

BoE’s Bailey signals potential for “activist” rate cuts as inflation pressures fade

In an interview with The Guardian, BoE Governor Andrew Bailey highlighted that cost of living pressures have not been as persistent as the Bank previously feared, which could open the door for more proactive rate cuts.

He noted that if positive inflation data continues, the BoE may adopt a "more activist" stance on reducing interest rates, which currently stand at 5%.

However, Bailey also pointed to geopolitical risks, particularly in the Middle East, as a threat. "Geopolitical concerns are very serious," he said, acknowledging that ongoing conflicts could add strain to already "stretched markets."

Swiss CPI slows to 0.8% yoy in Sep, import product prices plunge -2.7% yoy

Swiss CPI dropped by -0.3% mom in September, falling short of the expected -0.1% mom decline. Core CPI, which excludes fresh and seasonal products as well as energy and fuel, also declined by -0.2% mom. Prices for domestic products fell by -0.2% mom, while prices for imported goods saw a steeper decline of -0.5% mom.

On an annual basis, Swiss CPI growth slowed to 0.8% yoy, down from 1.1% and below expectations of 1.1% yoy. Core inflation eased to 1.0% from 1.1%. Notably, prices for imported goods dropped by -2.7% yoy, down from -1.9% yoy. Domestic product prices remained steady at 2.0% yoy.

The sharper-than-expected slowdown in inflation adds pressure on SNB to consider additional rate cuts. With core inflation and imported goods prices continuing to decline, SNB may need to act to prevent deflationary risks from taking hold in the coming months.

Sterling Loses Ground Following BoE Bailey’s Interview by Guardian

Markets

Core bonds reversed the safe-haven triggered gains of Tuesday. US yields rose by 3.7 bps (2-yr) to 5.8 bps (30-yr) while German yields rose by 1.9 bps (2-yr) to 5.5 bps (30-yr). The US underperformance at the front end of the curve was linked to a decent ADP employment report (143k from 103k vs 125k expected) which tilted the odds again somewhat more in favour of a 25 bps Fed November rate cut. EUR/USD slid from the 1.1075 area to currently 1.1025. Comments by ECB Schnabel – “we cannot ignore the headwinds to growth” – further bolster the case of a 25 bps rate cut by the ECB in October. US weekly jobless claims and services ISM are today’s sources of volatility. JPY remains in the defensive following political calls (new PM Ishiba) at the address of the BoJ to keep policy rates stable. The jury is out whether this will have any impact (independent central bank?!) or whether this is more of a window-dressing operation to polish his market-friendly image. USD/JPY moved from 143.50 yesterday morning to currently 146.50. The BoJ meets next on October 31.

Sterling loses ground this morning following the release of an interview by Bank of England governor Bailey with the Guardian. He said that the UK economy proved more resilient than feared over the past two years, so there’s a base there to develop. The BoE governor is also encouraged by the fact that cost of living pressures had not been as persistent as thought. If news on inflation (2.2% Y/Y in August) continues to be good, he argues in favour of becoming a bit more activist in the approach to cutting policy rates. So far, the BoE only sliced rates once by 25 bps in August (5-4 vote) and kept them stable in September (8-1 vote). UK money markets discount a second 25 bps rate cut at the November meeting, when the BoE publishes its quarterly Monetary Policy Report, but only attach a 50% probability to more action in December. The bottom of the expected rate path in the UK next year (>3.5%) is also significantly higher still than for example in Europe (1.5%-1.75%) or the US (<3%). That leaves quite some room for repositioning should the BoE effectively start a more aggressive normalization campaign and makes sterling vulnerable in the process. EUR/GBP rises in Asian trading from 0.8325 to 0.8370 in a move which we expect to continue. Regaining EUR/GBP 0.84 would turn the short term picture neutral again for the currency pair. GBP/USD failed to move above 1.34 earlier this week as USD profited from some safe haven flows. GBP weakness now takes over with cable losing a big figure from 1.3275 to 1.3175 this morning.

News & Views

The IMF in concluding its annual (Article IV) review said Australia’s “last mile” in taming inflation back to target is proving particularly difficult. Keeping the policy rate at 4.35% even when the rest of the advanced world started easing was therefore appropriate. The IMF said the central bank may even need to raise them again if inflation – still almost 4% in Q2 - stopped falling. Washington urged for the government to play their part with tighter fiscal policy as well. It welcomed two consecutive federal government surpluses (A$15.8 in 2023-2024) but Australia’s Treasury back in May forecasted the budget would return to deficit over the forecast horizon out to 2027-2028. This (fiscal) year’s deficit is projected at A$28.3bn, which the IMF said is delivering a “positive fiscal impulse” at a time where inflation is still hovering above the central bank’s 2-3% target. The Reserve Bank of Australia’s next policy meeting is on November 5. Money markets expect virtually nothing though. A first 25 bps cut isn’t fully priced in before February of next year. The Australian dollar meanwhile hovers near YtD highs of AUD/USD 0.69.

OPEC+ is sticking with plans to gradually scale back oil production curbs. In yesterday’s meeting, the Saudi led oil cartel reaffirmed its intention to revive output with 180k barrels a day starting from December. That was already two months later than originally scheduled due to a steep drop in oil prices in recent weeks/months over global demand concerns. After briefly dropping below $70 (Brent) for the first time since end 2021 early September, prices have rebounded a bit. Partly in response to the series of Chinese stimulus measures announced over the last two weeks but mostly on fears for a disruption in supply as the conflict in the Middle East escalated. After trading as high as $76, prices yesterday pulled back intraday after the US unexpectedly posted a weekly inventory build-up. One barrel is currently changing hands for $74.8.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) makes a follow-up move less evident in October, but very weak PMI’s and soft Lagarde comments hang in the balance. Disappointing US and unconvincing-to-outright-weak EMU activity data dragged the long end of the curve down with the 2023 low at 1.89% as key support.

US 10y yield

The Fed kicked off its easing cycle with a 50 bps move. It is headed towards a neutral stance now that inflation and employment risks are in balance. Conservative SEP unemployment forecasts risk being caught up by reality and with it the dot plot (50 bps more cuts in 2024). We hold our call for two more 50 bps cuts this year. Pressure on the front of the curve and weakening eco data keeps the long end in the defensive for now as well.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) only briefly offset some of the general USD weakness. EUR/USD’s dollar-driven bumped into 1.12 resistance.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. But the economic picture is increasingly diverging to the benefit of sterling, pulling EUR/GBP below 0.84 support. Dovish comments by BoE Bailey ended by default GBP-strength.

Oil Struggles to Break Above Key Medium-Term Resistance

The geopolitical situation in the Middle East gets tenser, and the Federal Reserve (Fed) doves get worried with the sight of better-than-expected jolts and ADP report announced earlier in the week.

Yesterday’s ADP report showed that the US economy added around 142K new private jobs last month, comfortably higher than the 124K pencilled in by analysts. Last month’s figure was revised higher. The numbers are not near 200-300K job additions of the post-pandemic months – far from that – but we are not seeing the kind of numbers that would keep the expectation of another jumbo rate cut from the Fed in November either. The US 2-year yield is pushing gently above the 3.60% level, having bottomed near the 3.50% last week when the 50bp cut expectations for November have surfaced, the 10-year yield recovered to 3.80% and the US dollar broke above its negative trend top building since summer and is preparing to test the 50-DMA. The last test for the US dollar bulls is tomorrow’s official jobs data. If the data continues to show that the US jobs market is slowing but not collapsing, we shall see the US dollar recover further.

The broadly stronger US dollar, combined with a slide in the euro area inflation below the European Central Bank’s (ECB) 2% inflation target justifies a further selloff in the EURUSD. The pair took out the 50-DMA support and is now preparing to test the next, and the important psychological support of $1.10 level. Below that, at 1.0980, stands the major 38.2% Fibonacci retracement on June to September rebound, and should distinguish between the positive trend building since summer and a medium-term bearish reversal.

And of course, the sharp yen selloff in the Japanese yen is giving an additional support to the US dollar following the new PM Ishiba’s comments that the Japanese economy is ‘not ready yet for further rate hikes’ and hopes that the ‘economy will make progress n a sustainable manner toward the end of deflation with monetary easing trend in place’. The USDJPY was sent immediately above the 146 level. We can forget a sustainable fall to and below the 140 mark. There is a greater chance that we see the pair return and stabilize near the 148/150 level.

Now, a better-than-expected set of US jobs data is positive for the US dollar bulls and negative for the US treasuries, but it is not outright positive or negative for sentiment in the stock markets. Yes, the Fed cuts are supportive of valuations and the 50bp cut has provided a lot of joy to stock investors, but a collapsing jobs market is fundamentally bad news for the economy. So the impact of a possibly stronger-than-expected jobs data on Friday is difficult to tell. In one hand, a good set of data would confirm that the US economy is doing well enough to keep the S&P500’s profit expectations strong and give a further support to stock valuations near ATH levels. On the other hand, a too strong set of data would crash the expectations of further and aggressive rate cuts from the Fed and that’s mathematically unfavourable for the stock valuations. Investors’ opinions diverge. Many think that the 6000 for the S&P500 is not only within reach but is too easy to reach, while a few others – like Apollo’s CEO - think that the Fed has no reason to keep cutting rates and that its aggressive U-turn could backfire. After all, the US ports went on a strike this week, oil bulls give signs of life as a result of a widening war in the Middle East and the Fed may have declared victory on inflation earlier than ideal, and probably louder than reasonable.

Oil topside remain limited at key technical resistance

Oil prices rose yesterday as Israel promised to retaliate against Iran and the G7 leaders announced that they are preparing to impose fresh sanctions on Iran. But the topside in US crude rally remained capped near the $72.85pb level, the major Fibonacci retracement on July to September retreat, and that should, in theory, distinguish between the actual bearish trend and a medium-term bullish reversal. I know I insist but I find the US crude’s inability to clear this technical resistance interesting and informing. It tells me that the geopolitical tensions do attract tactical longs, but the conviction for reversing a medium-term trend is still not strong enough. Look, we saw yesterday’s gains rapidly given back after the EIA data showed a 3.9-mio barrel build in US oil inventories last week.

Now, note that some bullish voices are emerging, putting the $100 per barrel target back on the table. But I believe that we will hardly see the barrel of US crude go past the $88-90pb range in case of badly deteriorating situation in the Middle East, because OPEC is preparing to call the end of its production restrictions by the end of the year as Saudi is moving toward a strategy where it will try to increase its market share rather than supporting oil prices. And second, around half to two-thirds of the Iranian oil goes mainly to China – which is not concerned by the sanctions. The only thing that could materially extend crude oil’s topside is if the US-backed Israel attacked the Iranian oil facilities. That’s the biggest risk to the global oil supply and that’s – to me – the only scenario which would justify a rise in crude prices to $100pb or more. And even then, imagine what would happen to the Fed – and other major central banks’ – inflation expectations and loosening policies. A significant rally in energy costs would simply stop and reverse them – which in return would boost the global recession expectations and limit oil’s upside potential. What I am trying to say is that, the geopolitical tensions could be interesting tactical opportunities for the oil bulls, but the medium-term picture remains comfortably bearish.

US ISM and Swiss Inflation on Today’s Menu

In focus today

In the afternoon, US ISM Services index is due for release. While the index has been volatile over the past years, flash PMIs released earlier signalled still solid growth in services sector activity in September.

In Switzerland, we get inflation data for September. Consensus expects a drop to 1.0% in headline inflation (from 1.1%) and core to remain steady at 1.1%. This should leave inflation in line with the SNBs Q3 forecast at 1.1%. In line with the SNB, we expect inflation to continue to edge lower into the lower end of the inflation target range of 0-2%.

Economic and market news

What happened overnight

In Japan, the newly appointed Prime Minister, Shigeru Ishiba, stated it is too early for additional rate hikes after meeting with Bank of Japan (BoJ) Governor Kazuo Ueda. Ueda echoed this, saying the BoJ will move cautiously on rate hikes, and board member Noguchi stressed the need to maintain a loose monetary policy. As of this morning, USD/JPY is trading around 146.85 after the dovish remarks.

What happened yesterday

In the US, ADP private sector employment growth for September exceeded expectations at 143k (cons: 120k), with the August figure being revised up to 103k (prior: 99k). Gains were broad-based occurring in leisure and hospitality (34k), construction (26k) and education and health services (24k). While on a cooling trend the past months, the reading suggest that labour market conditions remain solid. The print also points to a potentially decent labour market report on Friday, where we forecast NFP at 160k, slightly above consensus.

In the euro area, the unemployment rate remained at 6.4% in August as expected, with the number of unemployed persons declining by 94k. This indicates that the labour market remains historically strong. The decline was driven by a reduction in Spain, Italy and Greece, while the number of unemployed increased somewhat in Germany and France. Despite the low unemployment rate, more timely indicators show that recent employment growth has cooled or turned negative, reflecting an overall stagnant private labour market. Germany and France face the weakest labour markets, and largest risks of employment declines, while growth is expected to continue in Spain, Portugal and Greece.

ECB board member Isabel Schnabel noted that euro area inflation is increasingly likely to approach the 2% target amid signs of softening labour demand and further progress in disinflation. On the other hand, the Portuguese central bank chief Mario Centeno warned of the risk of undershooting its target, which could hinder economic growth.

In France, President Emmanuel Macron backed a temporary tax on the country's largest firms to support his new government's strategy. The French government unveiled plans for an EUR 60bn budget squeeze via spending cuts and tax hikes next year to curb the spiralling budget deficit and stabilise the country's financial outlook.

In Poland, as widely expected, the Monetary Policy Council kept its key policy rate steady at 5.75%.

In commodities space, the oil price remained bid amid concerns of supply disruptions from potential Israeli retaliation against Iran. Albeit OPEC+ is still weighing a December output increase, supported by recent price rises. Rising supply should help balance sentiment in the oil market amid escalation of the ongoing conflict in the Middle East.

Equities: Global equities were flat yesterday, with China being the regional exception, experiencing a sharp rise in Hong Kong. It is somewhat intriguing to observe both European and US equity markets being flat amidst substantial uncertainty across various parameters, including politics, geopolitics, macroeconomics, and monetary policy. In other words, all the elements are present that could potentially drive volatility higher as well as trigger significant movements in either direction for equities. The US job market data is a major catalyst in this context, and we will gain more insights on this front both today and tomorrow. In the US yesterday, the Dow closed up 0.1%, the S&P 500 slightly up by 0.01%, the Nasdaq increased by 0.1%, and the Russell 2000 decreased by 0.1%. The Chinese market's honeymoon appears to be over this morning, with markets down approximately 3% in Hong Kong. Conversely, in Japan, stocks are up more than 2% following dovish monetary statements, which have led to a renewed weakening of the yen. Futures in Europe and the US are lower this morning.

FI: There was a decent rebound in global bond yields and interest rates yesterday as 10Y US Treasury yields rose some 5bp and the curve steepened between 2Y and 10Y as well as 2Y and 30Y on the back of better-than-expected US labour market data and rising oil prices. We have seen a similar move in European government bond yields where yields rose, and the curves steepened from the long end. Furthermore, the Bund ASW-spread tightened once again.

FX: Risky assets saw some stabilisation despite continued geopolitical stress. Oil prices remained bid, although Brent closed some 2% below the intraday high. NOK/SEK pushed above 0.97 once more and the yen had a rough session following dovish remarks from new PM Ishiba, with USD/JPY rising 2% on the day. NBP left rates unchanged amid accelerating inflation with EUR/PLN trading close to our 1-3M target of 4.30.

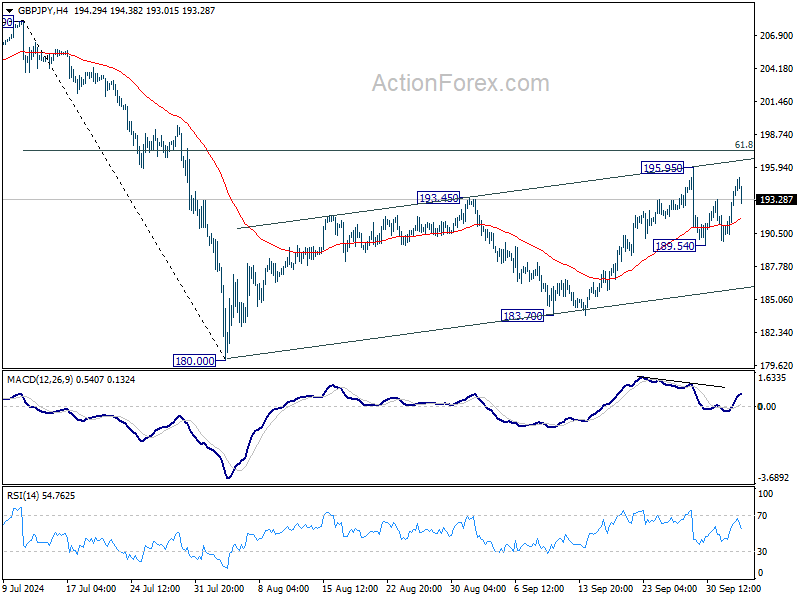

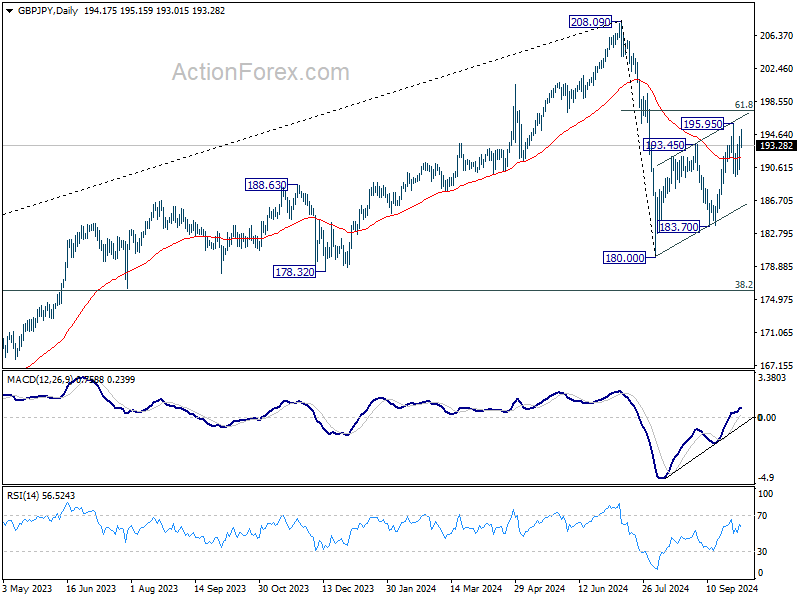

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.68; (P) 193.05; (R1) 195.69; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, below 189.54 will bring deeper fall to 183.70 support. On the upside, above 195.95 will resume the rise from 180.00 to 61.8% retracement of 208.09 to 180.00 at 197.35.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

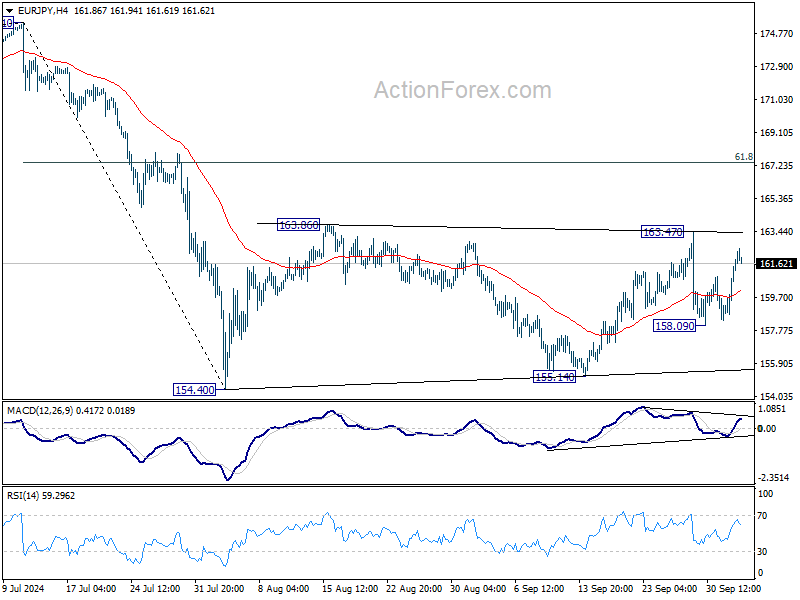

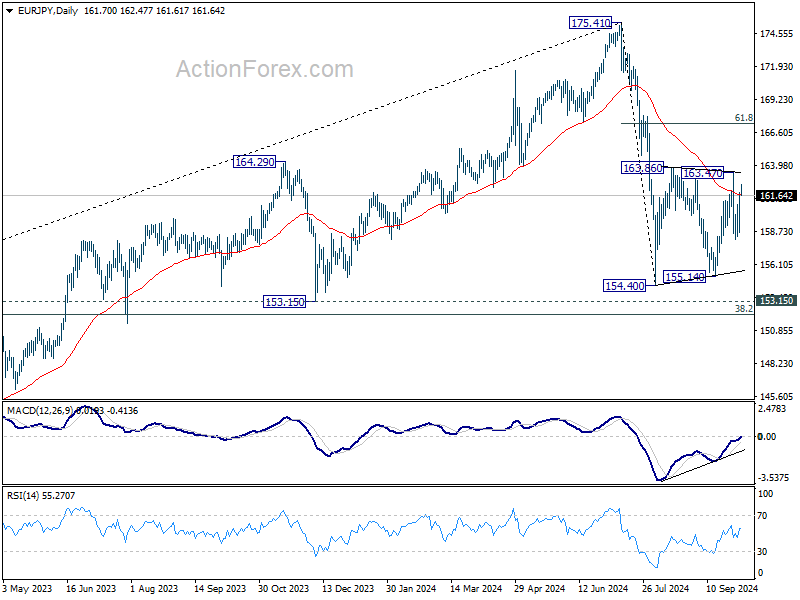

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.70; (P) 160.79; (R1) 162.88; More....

Intraday bias in EUR/JPY remains neutral for the moment. Risk is mildly on the downside as long as 163.47 resistance intact. Below 158.09 will bring deeper fall back to 154.40/155.14 support zone. ON the upside, though, break of 163.47 will resume the rise from 155.14 to 61.8% retracement of 175.41 to 154.40 at 167.38.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

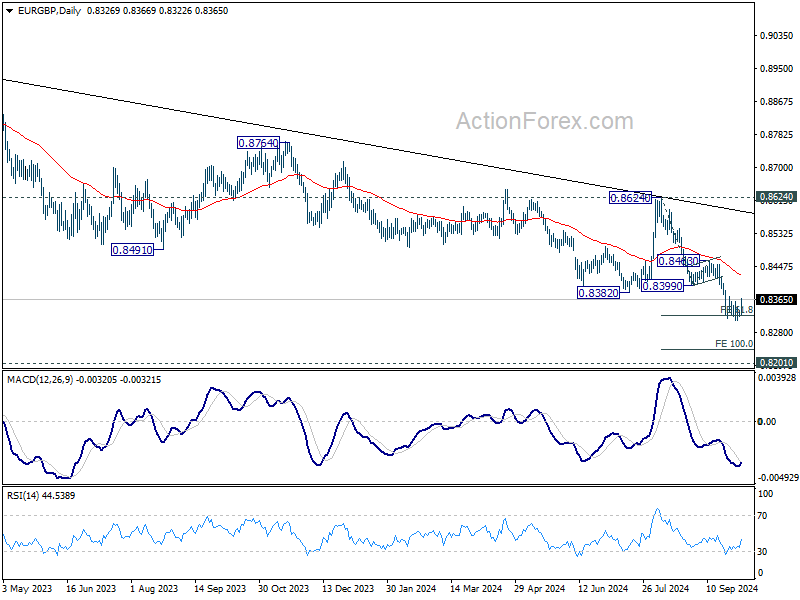

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8319; (P) 0.8329; (R1) 0.8335; More...

Intraday bias in EUR/GBP is turned neutral with current recovery. On the upside, firm break of 0.8370 resistance will indicate short term bottoming at 0.8309. Intraday bias will be turned back to the upside for 0.8399/8463 resistance zone. On the downside, firm break of 0.8309 will resume the fall from 0.8624 to 100% projection of 0.8624 to 0.8399 from 0.8463 at 0.8237 next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound.