Sample Category Title

USD/CHF Weekly Outlook

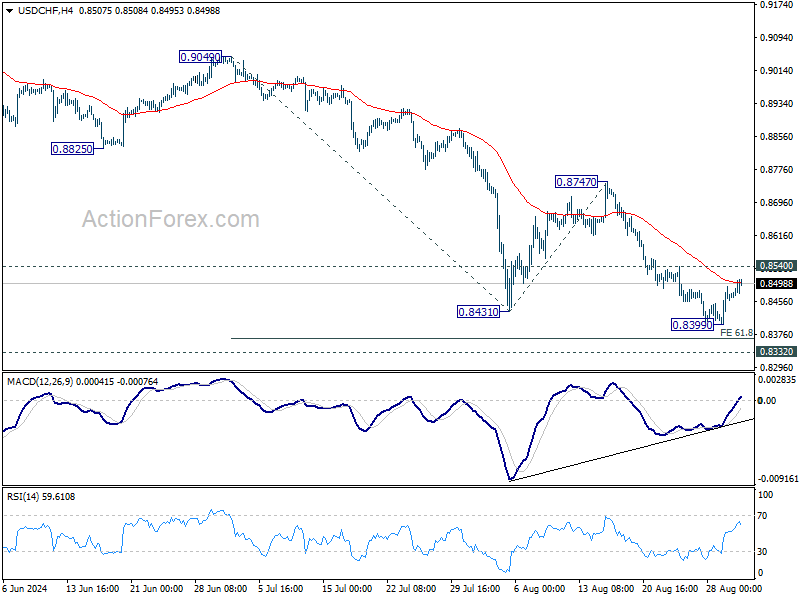

USD/CHF's fall from 0.9223 resumed by breaking through 0.8431 support, but quickly recovered after hitting 0.8399. Initial bias remains neutral this week first. Further fall is expected as long as 0.8540 resistance holds. Break of 0.8339 will target 61.8% projection of 0.9049 to 0.8431 from 0.8747 at 0.8365, and then 0.8332 low. However, firm break of 0.8540 will turn bias back to the upside for 0.8747 resistance instead.

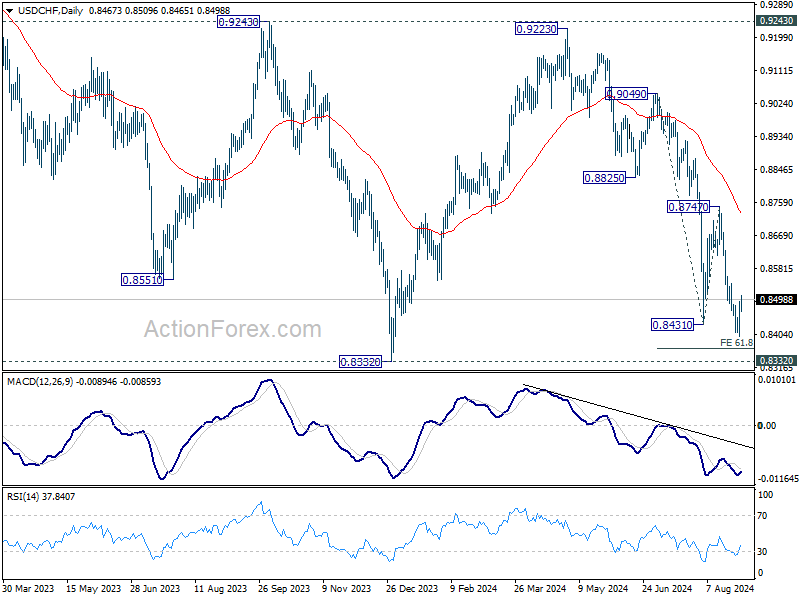

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

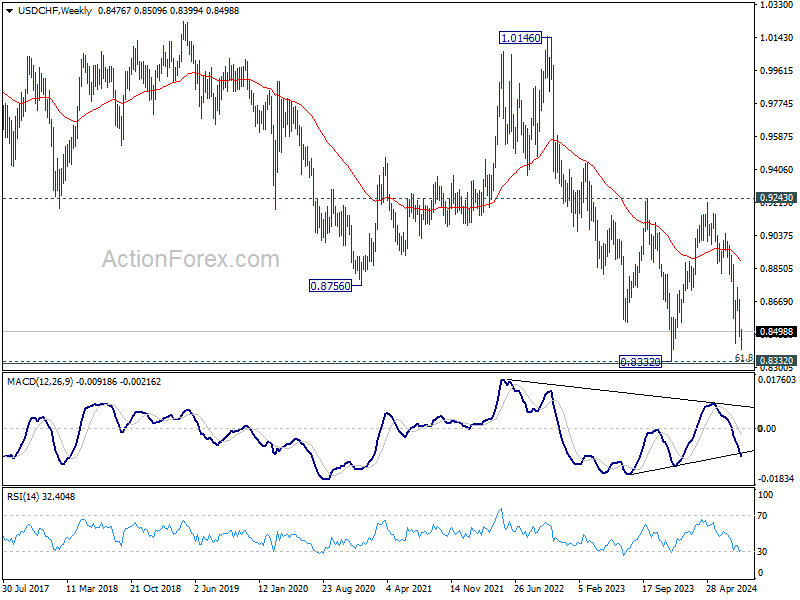

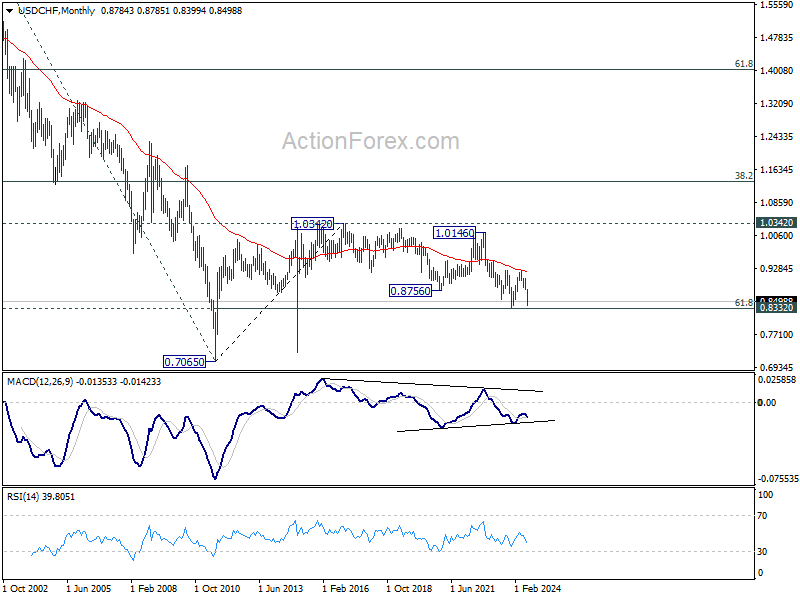

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Rejection by 55 M EMA suggest that this fall is in progress. Break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.

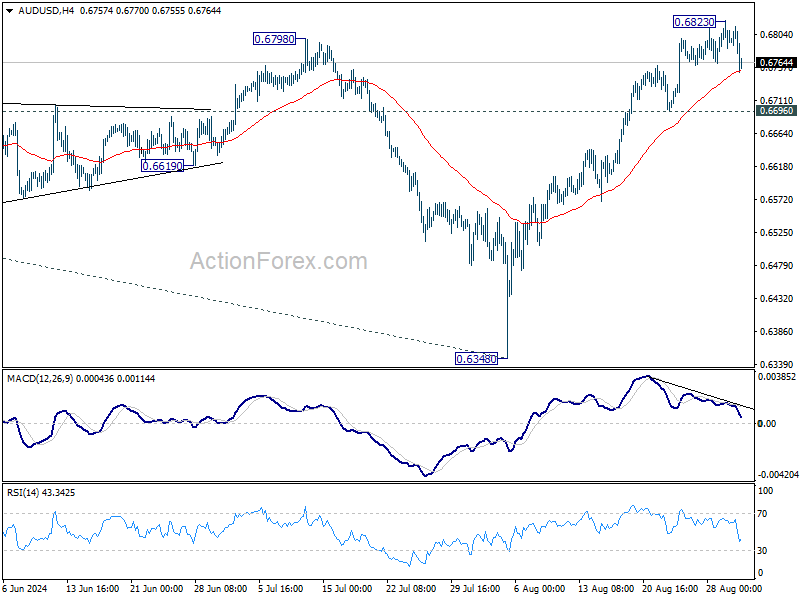

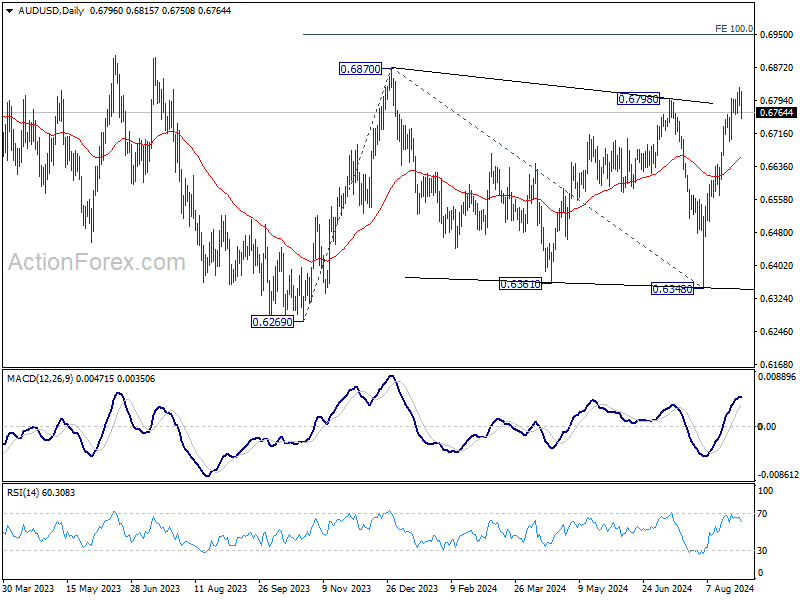

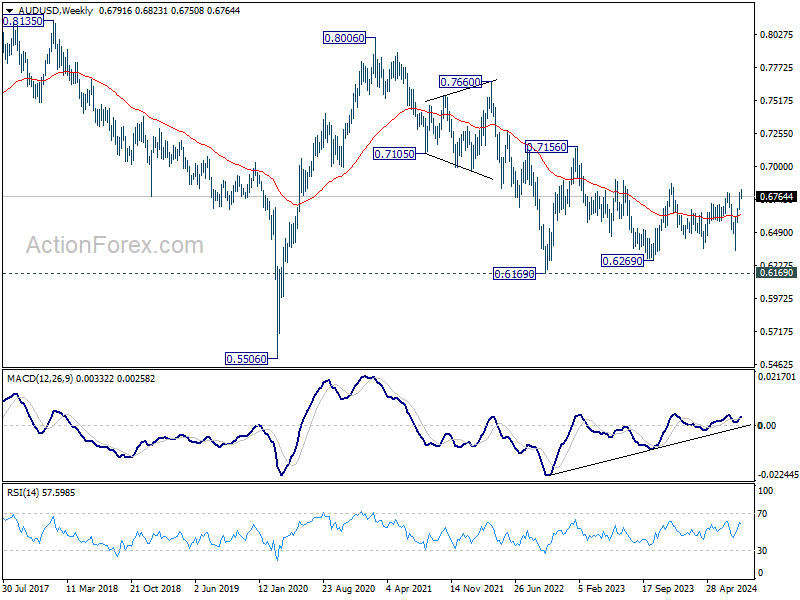

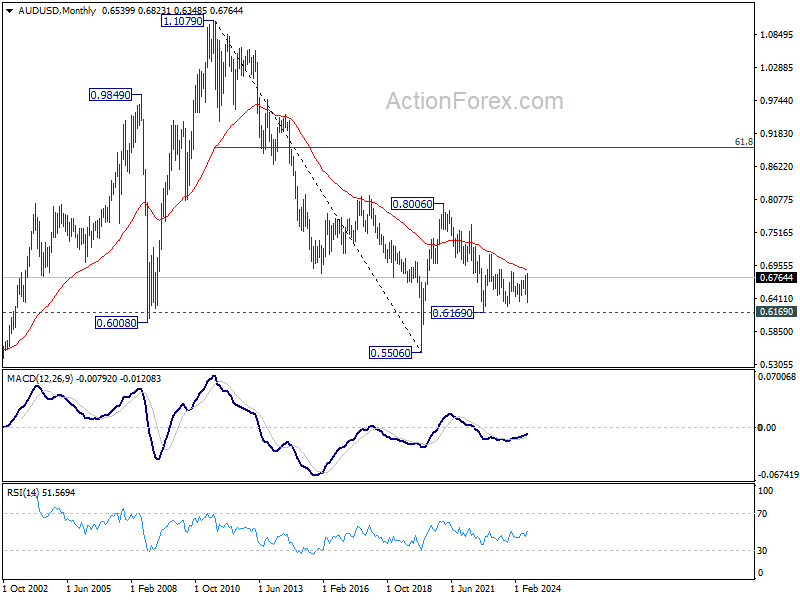

AUD/USD Weekly Report

AUD/USD edged higher to 0.6823 last week but lost momentum and retreated. Initial bias is turned neutral this week for consolidations. Break of 0.6823 will target 0.6870 resistance. Firm break there will target 100% projection of 0.6269 to 0.6870 from 0.6348 at 0.6949. However, break of 0.6696 support will indicate short term topping, on bearish divergence condition in 4H MACD, and turn bias back to the downside for deeper pullback.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

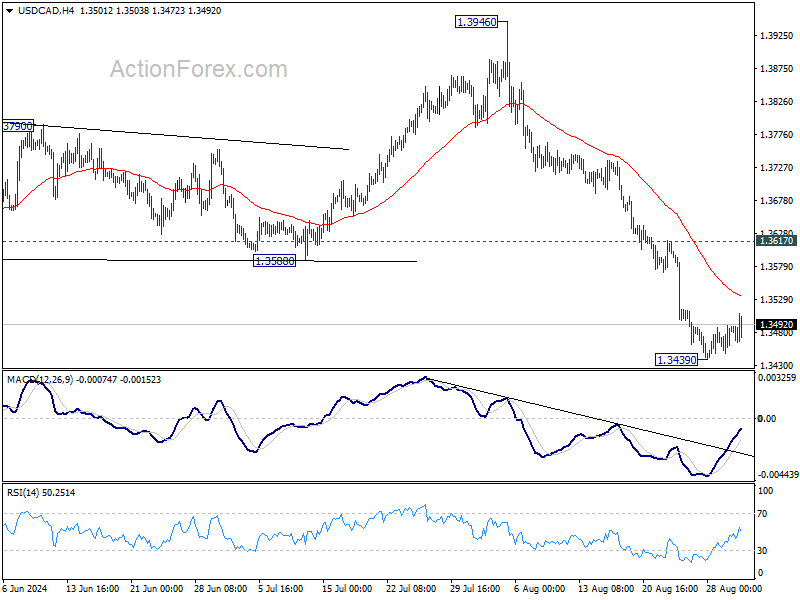

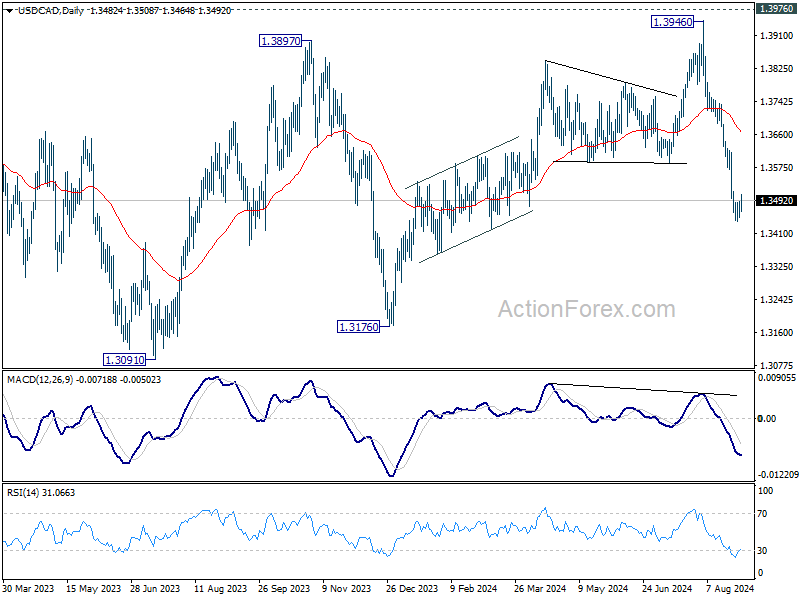

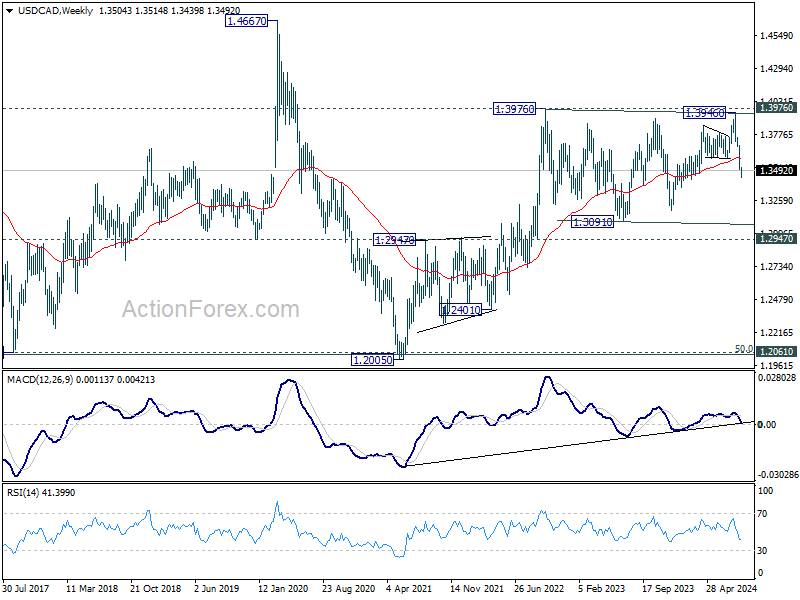

USD/CAD Weekly Outlook

USD/CAD's fall from 1.3946 continued last week and extended to as low as 1.3439. But as a temporary low was formed there, initial bias remains neutral this week for more consolidations. Outlook will stay bearish as long as 1.3617 resistance holds. Below 1.3439 will target 1.3176 support next.

In the bigger picture, current development suggests that corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

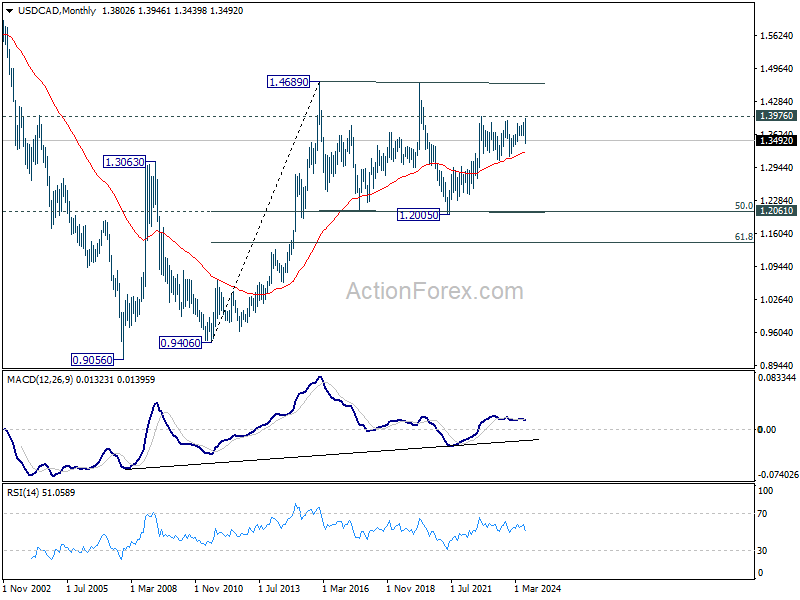

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

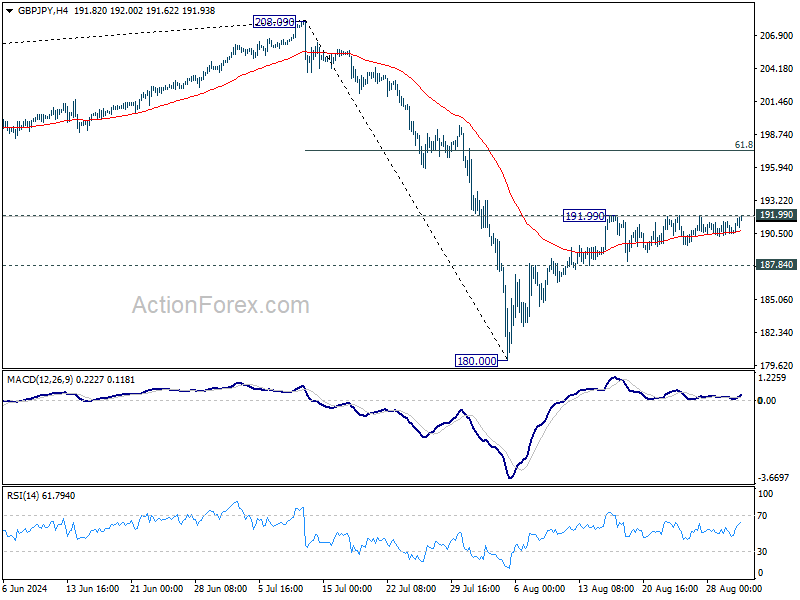

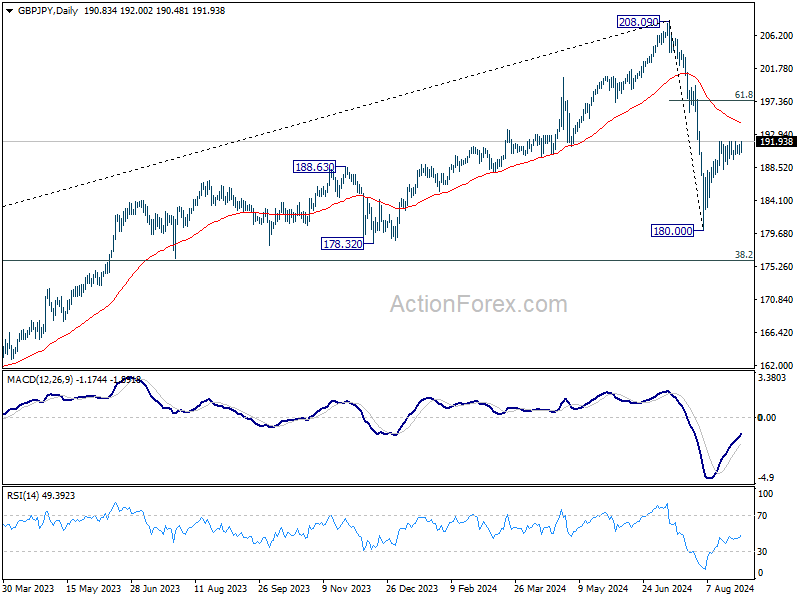

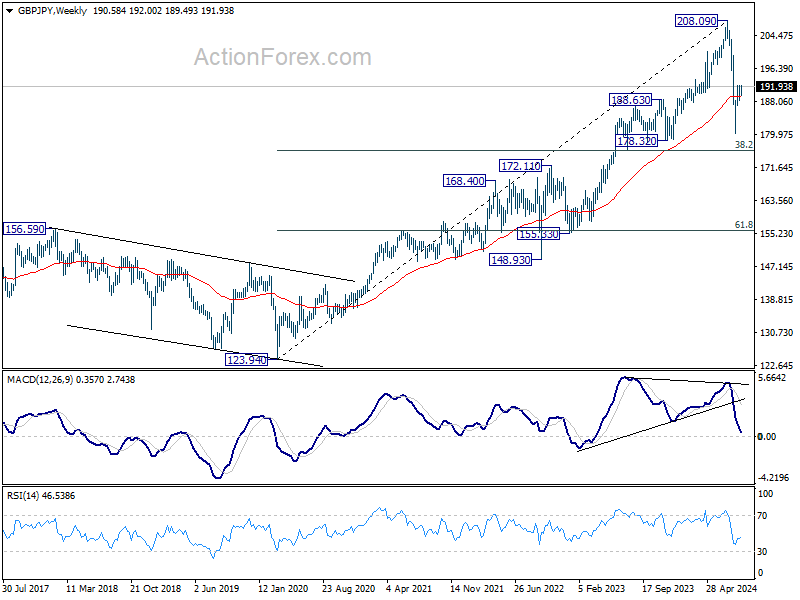

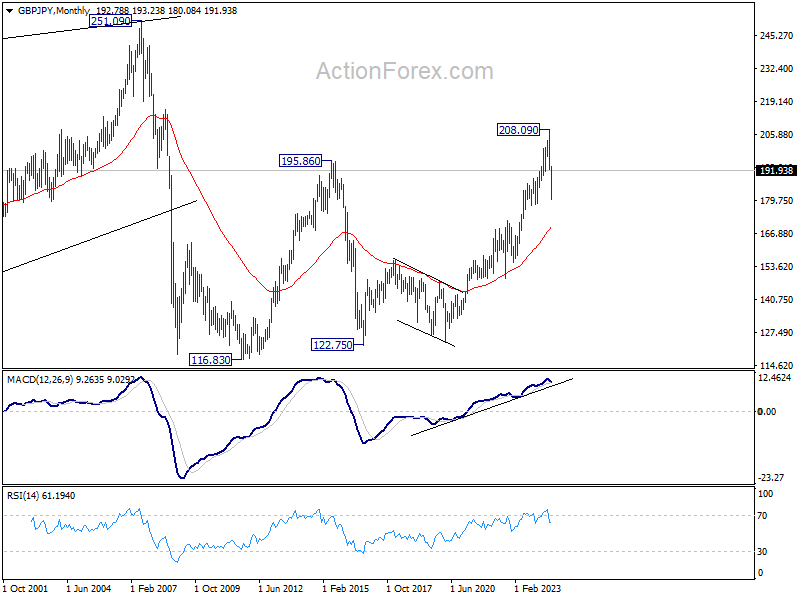

GBP/JPY Weekly Outlook

No change in GBP/JPY's outlook as sideway trading continued below 191.99 last week. Initial bias stays neutral this week first. On the upside, above 191.99 will target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will argue that rebound from 180.00 has completed, and turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

In the longer term picture, considering bearish divergence condition in W MACD, 208.09 is at least a medium term top. It's still early to conclude that the up trend from 122.75 (2016 low) has completed. But it's at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 169.35).

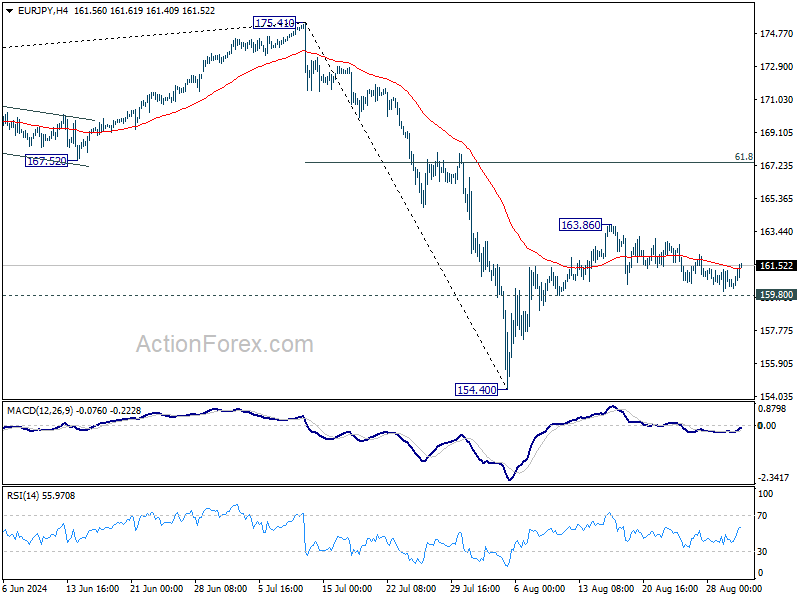

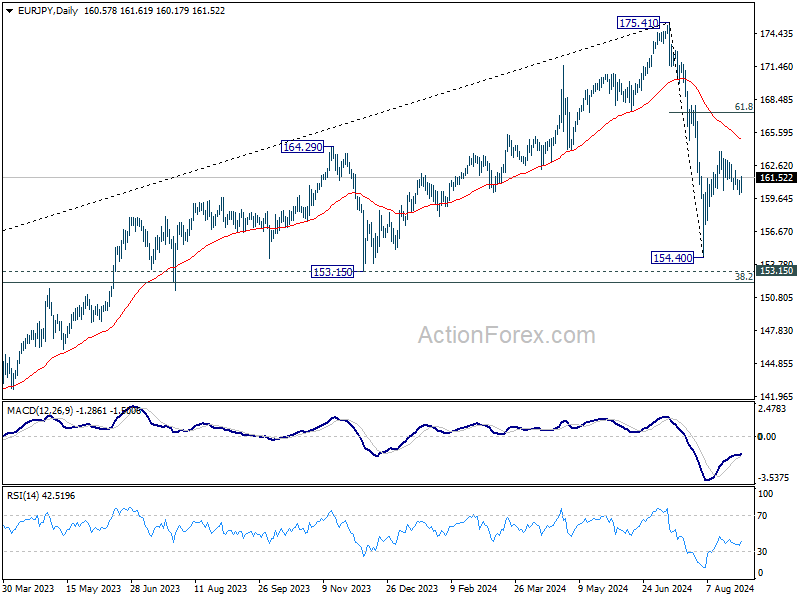

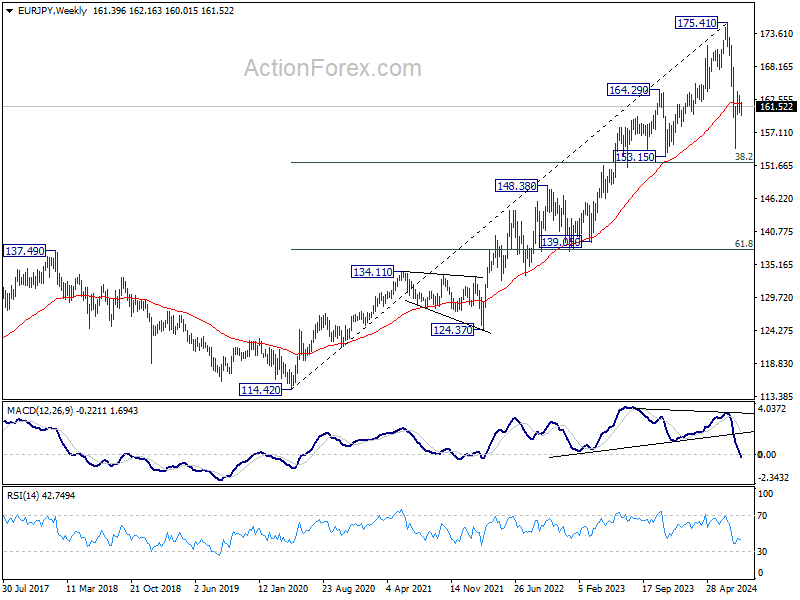

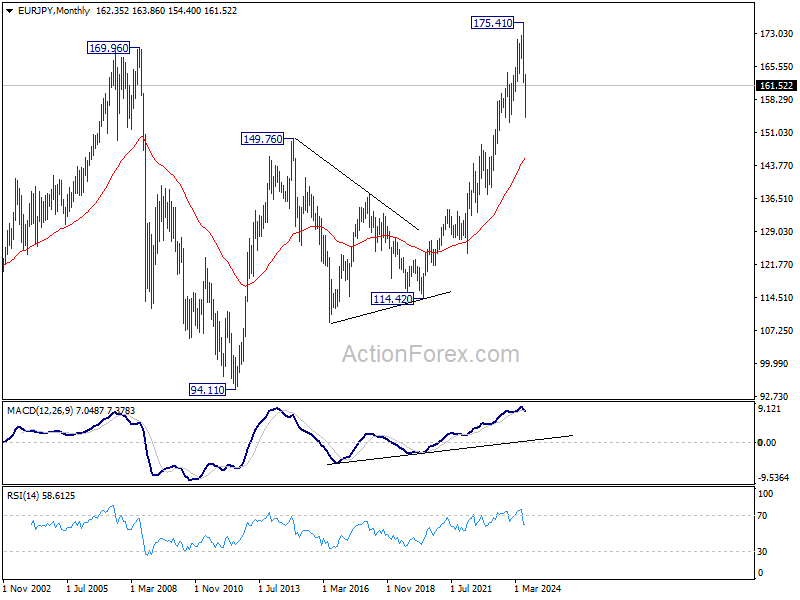

EUR/JPY Weekly Outlook

No change in EUR/JPY's outlook as sideway trading continued below 163.86 last week. Initial bias remains neutral this week first. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 159.80 support will suggest that the rebound from 154.40 has completed, and turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

In the long term picture, considering bearish divergence condition in W MACD, 175.41 is at least a medium term top. It's still early to conclude that up trend from 94.11 (2012 low) has completed. But a medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 145.56).

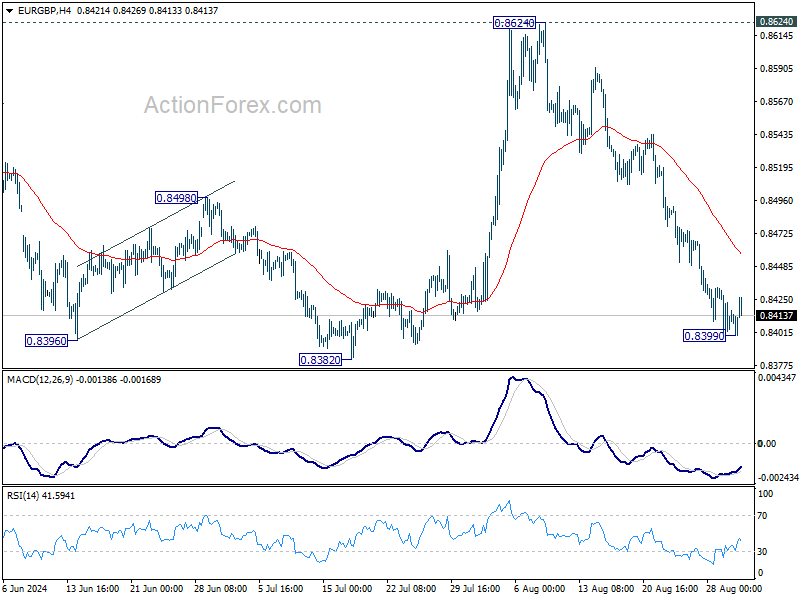

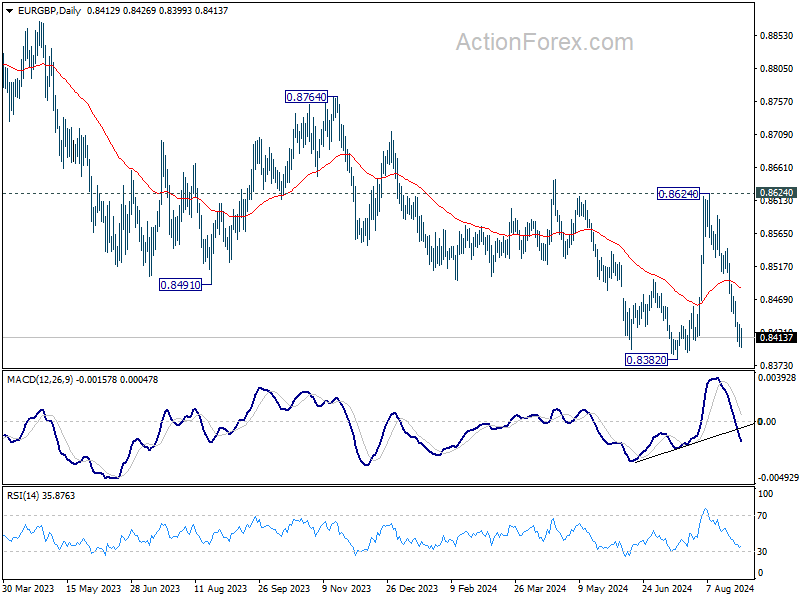

EUR/GBP Weekly Outlook

EUR/GBP's fall from 0.8624 extended to as low as 0.8399 last week but recovered since then. Initial bias is turned neutral this week for some consolidations. Risk will stay on the downside as long as 55 4H EMA (now at 0.8457) holds. Below 0.8399 will target 0.8382 support. Firm break there will resume larger down trend.

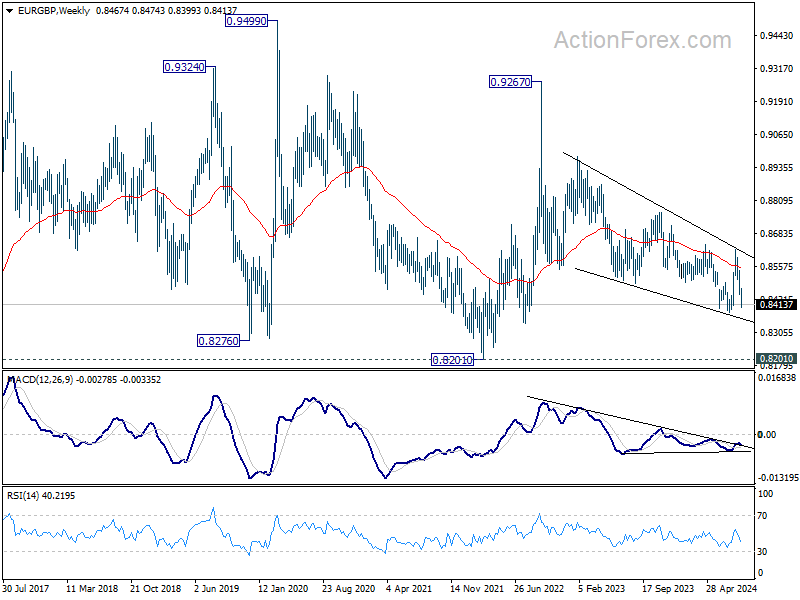

In the bigger picture, as long as 0.8624 resistance holds, down trend from 0.9267 is expected to continue. Firm break of 0.8382 will target 0.8201 (2022 low). However, decisive break of 0.8624 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

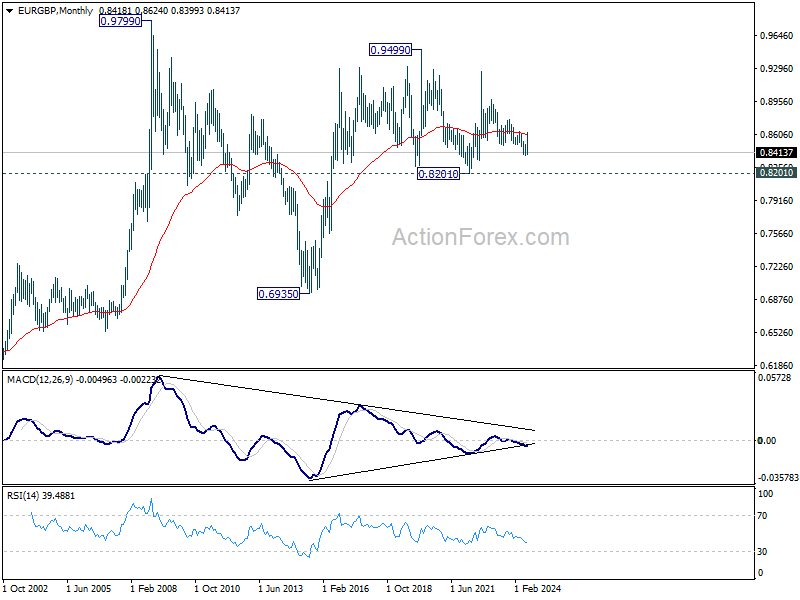

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

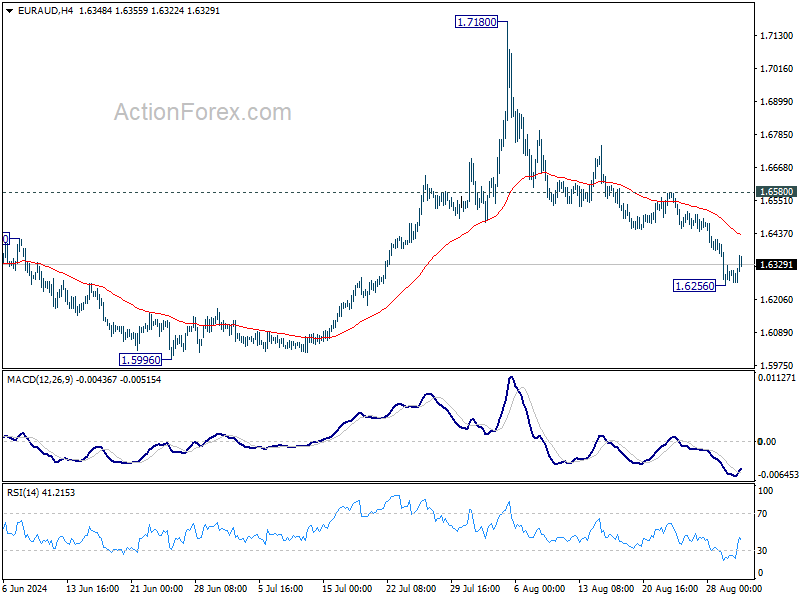

EUR/AUD Weekly Outlook

EUR/AUD's decline from 1.7180 extended to as low as 1.6256 last week but recovered since then. Initial bias is turned neutral this week for some consolidations. Further decline would remain in favor as long as 1.6580 resistance holds. Below 1.6256 will target 1.5996 key support level next.

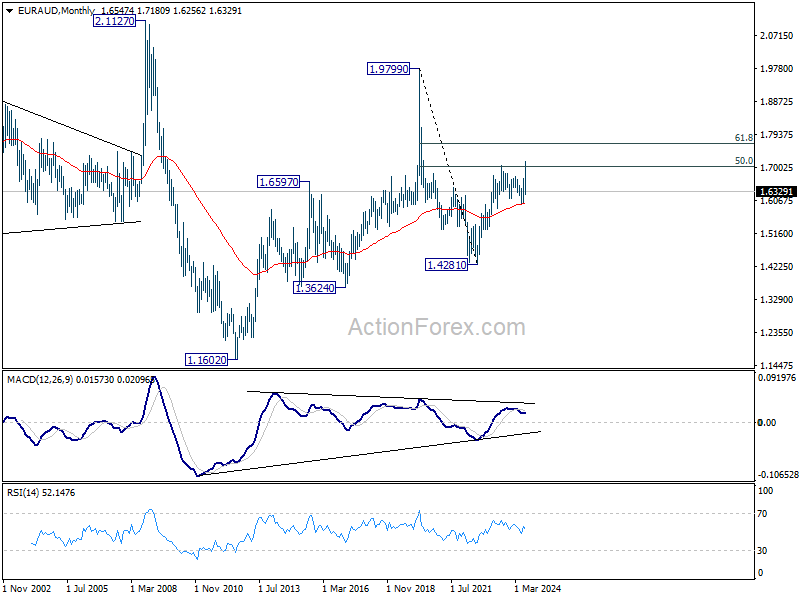

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5987) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

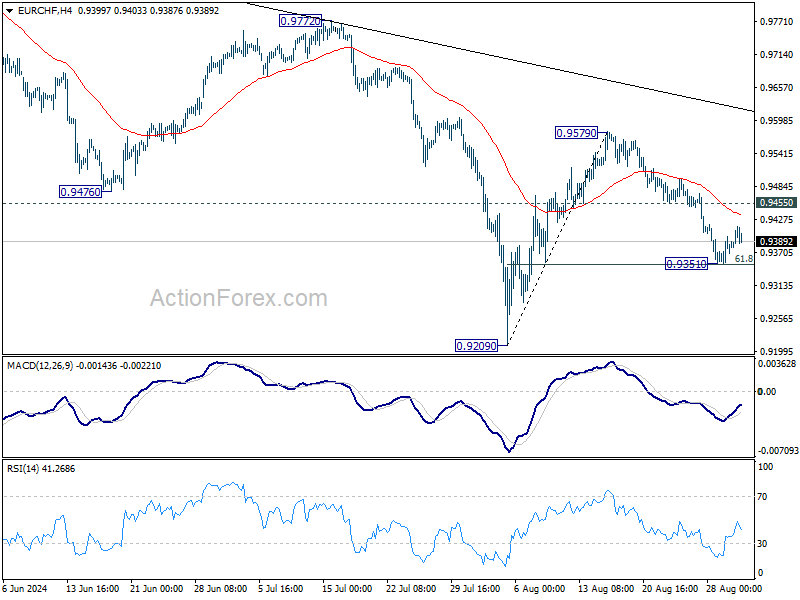

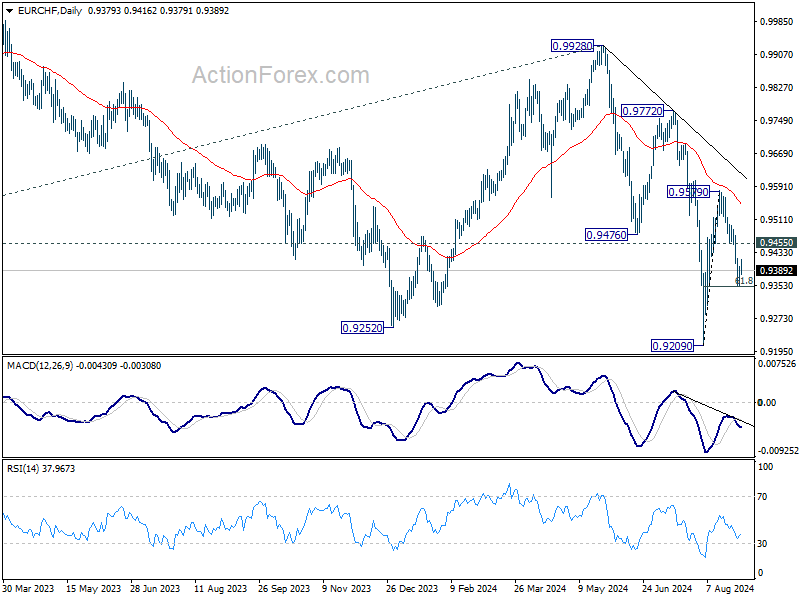

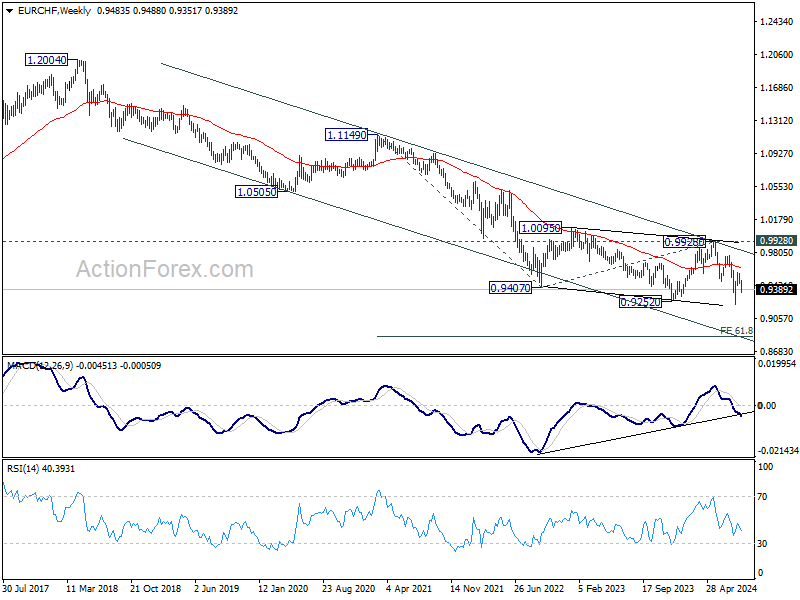

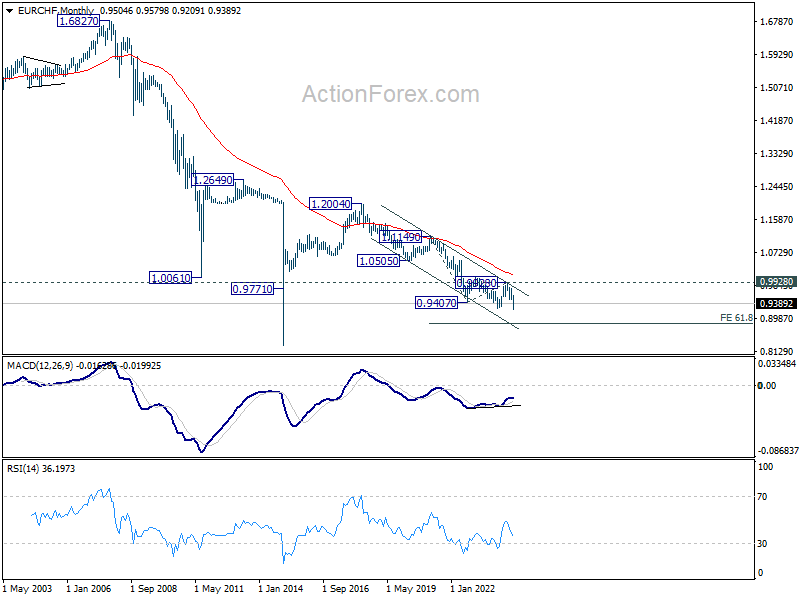

EUR/CHF Weekly Outlook

EUR/CHF's deep decline last week confirmed that rebound form 0.9209 has completed at 0.9579, ahead of 55 D EMA. But as a temporary low was formed at 0.9351, just ahead of 61.8% retracement of 0.9209 to 0.9579 at 0.9350, initial bias stays neutral first. Break of 0.9351 will target 0.9209 low next. However, break of 0.9497 will turn bias back to the upside for 0.9579 resistance instead.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 9/2 – 9/6

Monday, Sep 2, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q2 | 9.90% | 6.80% |

| 00:30 | JPY | Manufacturing PMI Aug F | 49.5 | 49.5 |

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q2 | -0.40% | -2.50% |

| 01:30 | AUD | Building Permits M/M Jul | 2.40% | -6.50% |

| 01:45 | CNY | Caixin Manufacturing PMI Aug | 50 | 49.8 |

| 06:30 | CHF | Retail Sales Y/Y Jul | -0.20% | -2.20% |

| 07:30 | CHF | Manufacturing PMI Aug | 43.7 | 43.5 |

| 07:50 | EUR | France Manufacturing PMI Aug F | 42.1 | 42.1 |

| 07:55 | EUR | Germany Manufacturing PMI Aug F | 42.1 | 42.1 |

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | 45.6 | 45.6 |

| 08:30 | GBP | Manufacturing PMI Aug F | 52.5 | 52.5 |

| 22:45 | NZD | Terms of Trade Index Q2 | 2.80% | 5.10% |

| 23:50 | JPY | Monetary Base Y/Y Aug | 0.60% | 1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:50 | JPY | Capital Spending Q2 | |

| Forecast: 9.90% | Previous: 6.80% | ||

| 00:30 | JPY | Manufacturing PMI Aug F | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q2 | |

| Forecast: -0.40% | Previous: -2.50% | ||

| 01:30 | AUD | Building Permits M/M Jul | |

| Forecast: 2.40% | Previous: -6.50% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Aug | |

| Forecast: 50 | Previous: 49.8 | ||

| 06:30 | CHF | Retail Sales Y/Y Jul | |

| Forecast: -0.20% | Previous: -2.20% | ||

| 07:30 | CHF | Manufacturing PMI Aug | |

| Forecast: 43.7 | Previous: 43.5 | ||

| 07:50 | EUR | France Manufacturing PMI Aug F | |

| Forecast: 42.1 | Previous: 42.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI Aug F | |

| Forecast: 42.1 | Previous: 42.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | |

| Forecast: 45.6 | Previous: 45.6 | ||

| 08:30 | GBP | Manufacturing PMI Aug F | |

| Forecast: 52.5 | Previous: 52.5 | ||

| 22:45 | NZD | Terms of Trade Index Q2 | |

| Forecast: 2.80% | Previous: 5.10% | ||

| 23:50 | JPY | Monetary Base Y/Y Aug | |

| Forecast: 0.60% | Previous: 1.00% | ||

Tuesday, Sep 3, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Current Account (AUD) Q2 | -5.5B | -4.9B |

| 06:30 | CHF | CPI M/M Aug | 0.10% | -0.20% |

| 06:30 | CHF | CPI Y/Y Aug | 1.20% | 1.30% |

| 07:00 | CHF | GDP Q/Q Q2 | 0.60% | 0.50% |

| 13:30 | CAD | Manufacturing PMI Aug | 47.8 | |

| 13:45 | USD | Manufacturing PMI Aug F | 48 | 48 |

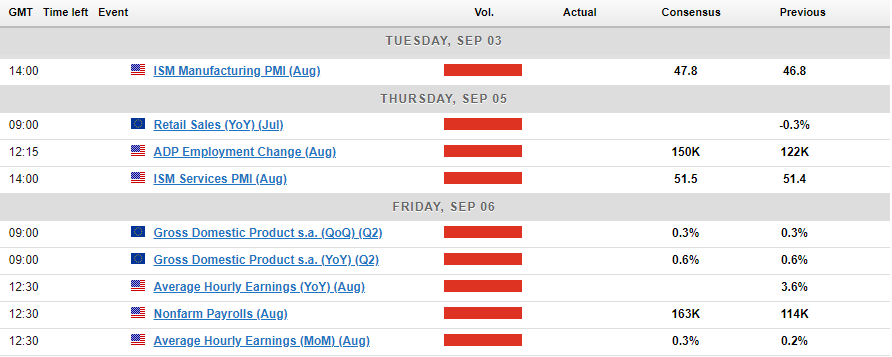

| 14:00 | USD | ISM Manufacturing PMI Aug | 47.8 | 46.8 |

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | 52.5 | 52.9 |

| 14:00 | USD | ISM Manufacturing Employment Index Aug | 43.4 | |

| 14:00 | USD | Construction Spending M/M Jul | 0.10% | -0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Current Account (AUD) Q2 | |

| Forecast: -5.5B | Previous: -4.9B | ||

| 06:30 | CHF | CPI M/M Aug | |

| Forecast: 0.10% | Previous: -0.20% | ||

| 06:30 | CHF | CPI Y/Y Aug | |

| Forecast: 1.20% | Previous: 1.30% | ||

| 07:00 | CHF | GDP Q/Q Q2 | |

| Forecast: 0.60% | Previous: 0.50% | ||

| 13:30 | CAD | Manufacturing PMI Aug | |

| Forecast: | Previous: 47.8 | ||

| 13:45 | USD | Manufacturing PMI Aug F | |

| Forecast: 48 | Previous: 48 | ||

| 14:00 | USD | ISM Manufacturing PMI Aug | |

| Forecast: 47.8 | Previous: 46.8 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | |

| Forecast: 52.5 | Previous: 52.9 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Aug | |

| Forecast: | Previous: 43.4 | ||

| 14:00 | USD | Construction Spending M/M Jul | |

| Forecast: 0.10% | Previous: -0.30% | ||

Wednesday, Sep 4, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q2 | 0.20% | 0.10% |

| 01:45 | CNY | Caixin Services PMI Aug | 52.2 | 52.1 |

| 07:50 | EUR | France Services PMI Aug F | 55 | 55 |

| 07:55 | EUR | Germany Services PMI Aug F | 51.4 | 51.4 |

| 08:00 | EUR | EurozoneServices PMI Aug F | 53.3 | 53.3 |

| 08:30 | GBP | Services PMI Aug F | 53.3 | 53.3 |

| 09:00 | EUR | Eurozone PPI M/M Jul | 0.30% | 0.50% |

| 09:00 | EUR | EurozonePPI Y/Y Jul | -3.20% | |

| 12:30 | USD | Trade Balance (USD) Jul | -76.4B | -73.1B |

| 12:30 | CAD | Trade Balance (CAD) Jul | -0.3B | 0.6B |

| 13:45 | CAD | BoC Interest Rate Decision | 4.25% | 4.50% |

| 14:30 | CAD | BOC Press Conference | ||

| 18:00 | USD | Fed's Beige Book | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jul | 3.10% | 4.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | GDP Q/Q Q2 | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 01:45 | CNY | Caixin Services PMI Aug | |

| Forecast: 52.2 | Previous: 52.1 | ||

| 07:50 | EUR | France Services PMI Aug F | |

| Forecast: 55 | Previous: 55 | ||

| 07:55 | EUR | Germany Services PMI Aug F | |

| Forecast: 51.4 | Previous: 51.4 | ||

| 08:00 | EUR | EurozoneServices PMI Aug F | |

| Forecast: 53.3 | Previous: 53.3 | ||

| 08:30 | GBP | Services PMI Aug F | |

| Forecast: 53.3 | Previous: 53.3 | ||

| 09:00 | EUR | Eurozone PPI M/M Jul | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 09:00 | EUR | EurozonePPI Y/Y Jul | |

| Forecast: | Previous: -3.20% | ||

| 12:30 | USD | Trade Balance (USD) Jul | |

| Forecast: -76.4B | Previous: -73.1B | ||

| 12:30 | CAD | Trade Balance (CAD) Jul | |

| Forecast: -0.3B | Previous: 0.6B | ||

| 13:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 4.25% | Previous: 4.50% | ||

| 14:30 | CAD | BOC Press Conference | |

| Forecast: | Previous: | ||

| 18:00 | USD | Fed's Beige Book | |

| Forecast: | Previous: | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jul | |

| Forecast: 3.10% | Previous: 4.50% | ||

Thursday, Sep 5, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jul | 4.95B | 5.59B |

| 05:45 | CHF | Unemployment Rate Aug | 2.50% | 2.50% |

| 06:00 | EUR | Germany Factory Orders M/M Jul | -1.50% | 3.90% |

| 08:30 | GBP | Construction PMI Aug | 54.4 | 55.3 |

| 09:00 | EUR | EurozoneRetail Sales M/M Jul | 0.10% | -0.30% |

| 11:30 | USD | Challenger Job Cuts Y/Y Aug | 9.20% | |

| 12:15 | USD | ADP Employment Change Aug | 150K | 122K |

| 12:30 | USD | Initial Jobless Claims (Aug 30) | 233K | 231K |

| 12:30 | USD | Nonfarm Productivity Q2 | 2.30% | 2.30% |

| 12:30 | USD | Unit Labor Costs Q2 | 0.90% | 0.90% |

| 13:45 | USD | Services PMI Aug F | 55.2 | 55.2 |

| 14:00 | USD | ISM Services PMI Aug | 51.5 | 51.4 |

| 14:00 | USD | ISM Services New Orders Index Aug | 52.4 | |

| 14:30 | USD | Natural Gas Storage | 35B | |

| 15:00 | USD | Crude Oil Inventories | -0.8M | |

| 23:30 | JPY | Overall Household Spending Y/Y Jul | 1.20% | -1.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jul | |

| Forecast: 4.95B | Previous: 5.59B | ||

| 05:45 | CHF | Unemployment Rate Aug | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 06:00 | EUR | Germany Factory Orders M/M Jul | |

| Forecast: -1.50% | Previous: 3.90% | ||

| 08:30 | GBP | Construction PMI Aug | |

| Forecast: 54.4 | Previous: 55.3 | ||

| 09:00 | EUR | EurozoneRetail Sales M/M Jul | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Aug | |

| Forecast: | Previous: 9.20% | ||

| 12:15 | USD | ADP Employment Change Aug | |

| Forecast: 150K | Previous: 122K | ||

| 12:30 | USD | Initial Jobless Claims (Aug 30) | |

| Forecast: 233K | Previous: 231K | ||

| 12:30 | USD | Nonfarm Productivity Q2 | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 12:30 | USD | Unit Labor Costs Q2 | |

| Forecast: 0.90% | Previous: 0.90% | ||

| 13:45 | USD | Services PMI Aug F | |

| Forecast: 55.2 | Previous: 55.2 | ||

| 14:00 | USD | ISM Services PMI Aug | |

| Forecast: 51.5 | Previous: 51.4 | ||

| 14:00 | USD | ISM Services New Orders Index Aug | |

| Forecast: | Previous: 52.4 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 35B | ||

| 15:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -0.8M | ||

| 23:30 | JPY | Overall Household Spending Y/Y Jul | |

| Forecast: 1.20% | Previous: -1.40% | ||

Friday, Sep 6, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Jul P | 109.4 | 109 |

| 06:00 | EUR | Germany Industrial Production sM/M Jul | -0.20% | 1.40% |

| 06:00 | EUR | Germany Trade Balance (EUR) Jul | 21.2B | 20.4B |

| 06:45 | EUR | France Trade Balance (EUR) Jul | -5.7B | -6.1B |

| 06:45 | EUR | France Industrial Output M/M Jul | -0.20% | 0.80% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | 704B | |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | 0.30% | 0.30% |

| 12:30 | USD | Nonfarm Payrolls Aug | 163K | 114K |

| 12:30 | USD | Unemployment Rate Aug | 4.20% | 4.30% |

| 12:30 | USD | Average Hourly Earnings M/M Aug | 0.30% | 0.20% |

| 12:30 | CAD | Net Change in Employment Aug | 25.0K | -2.8K |

| 12:30 | CAD | Unemployment Rate Aug | 6.50% | 6.40% |

| 14:00 | CAD | Ivey PMI Aug | 55.3 | 57.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Jul P | |

| Forecast: 109.4 | Previous: 109 | ||

| 06:00 | EUR | Germany Industrial Production sM/M Jul | |

| Forecast: -0.20% | Previous: 1.40% | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Jul | |

| Forecast: 21.2B | Previous: 20.4B | ||

| 06:45 | EUR | France Trade Balance (EUR) Jul | |

| Forecast: -5.7B | Previous: -6.1B | ||

| 06:45 | EUR | France Industrial Output M/M Jul | |

| Forecast: -0.20% | Previous: 0.80% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Aug | |

| Forecast: | Previous: 704B | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls Aug | |

| Forecast: 163K | Previous: 114K | ||

| 12:30 | USD | Unemployment Rate Aug | |

| Forecast: 4.20% | Previous: 4.30% | ||

| 12:30 | USD | Average Hourly Earnings M/M Aug | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | CAD | Net Change in Employment Aug | |

| Forecast: 25.0K | Previous: -2.8K | ||

| 12:30 | CAD | Unemployment Rate Aug | |

| Forecast: 6.50% | Previous: 6.40% | ||

| 14:00 | CAD | Ivey PMI Aug | |

| Forecast: 55.3 | Previous: 57.6 | ||

Markets Weekly Outlook – NFP Jobs Data to Rule Out 50 bps Fed Rate Cut?

- US PCE data keeps Fed rate cut hopes alive as inflation moves towards 2% target.

- Commodity prices fluctuate on geopolitical fears and OPEC+ production plans.

- US jobs data release is key market-moving event in the week ahead, with potential to impact Fed rate cut decisions.

Week in Review: Rate Cut Hopes Alive Post PCE Data

As the week draws to a close, US PCE data has kept Fed rate cut hopes on track as inflation continues on its way to its 2% target. Consumer spending remains strong and this has kept pricing for a 50 bps cut steady. However with a massive Jobs report next week, we could be having a very different conversation this time next week should the US economy deliver a soft jobs print.

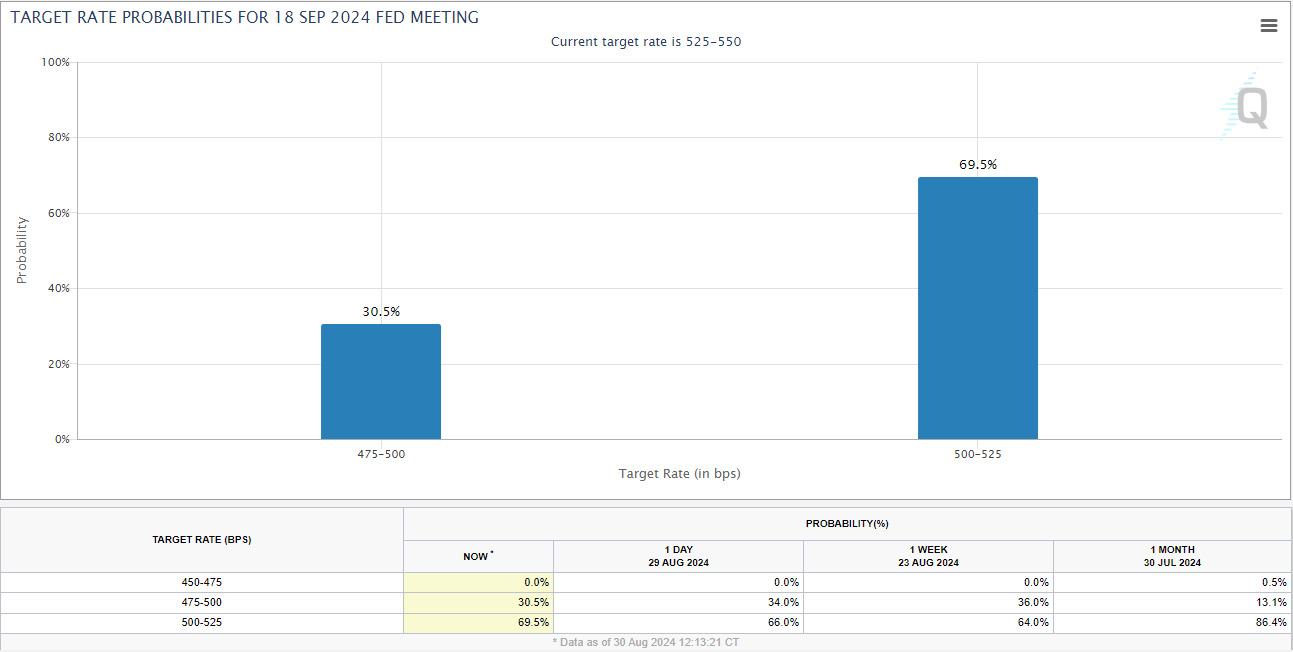

Heading into the Labour day weekend, the rate hike odds for the September 18 meeting has adjusted once more. The theme of the week has seen the probability of a 50 bps cut continue to diminish as robust US data gave market participants something to think about it. As you can see from the CME chart below, the probability of a 50 bps cut declined from 36% to 30% during the course of the week.

Source: CME FedWatch Tool

The strong GDP and PCE data prints at the back end of the week rescued the US Dollar Index (DXY) which appeared to be on the ropes. The early part of the week saw the greenback lose ground to its G7 counterparts with Cable holding near 30 month highs against the greenback. USD/JPY finally made a break of the 145.00 handle as the greenback recovered some of its early week losses.

Commodity prices went through a rollercoaster week with Brent Crude Oil rising on geopolitical fears and Libyan production going offline. However, news at the back end of the week regarding OPEC + and its proposed output hike saw Oil surrender some early week gains. According to sources, OPEC + are planning to increase output as planned with uncertainty around Libya production and some member states pledging cuts to overcompensate for potential overproduction. This sets up Oil prices for an interesting week.

Gold prices struggled within a tight range for the majority of the week. The $2530 handle in particular has proved a sticking point and a lot of this has to do with how much of the expected rate cuts by the Federal Reserve are already priced in. If we do not see a significant miss next week with the jobs data release this could facilitate a break of the range, if not expect more of the same in the week ahead.

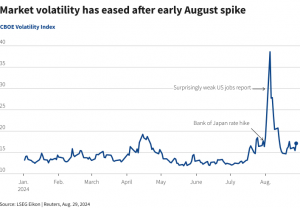

Wall Street indexes are ending August in a completely different light to the start of the month. We all can remember the early August selloff and concern by many market participants, all of which seems to have eased as the summer period draws to a close.

The Nasdaq 100 was trading down 0.03% with the S&P 500 up around 1.5% for the month. Another indication of the change in market sentiment can be seen from the CBOE Volatility Index chart below which shows the change in volatility through the month of August.

Source: LSEG Workspace

Despite the positive end to the month of August for the S&P 500 I am cautious moving forward. This lies in my views on seasonality and with the US election around the corner the data speaks for itself. During US election years dating back to 1928, the S&P 500 usually experiences a lull and some small losses in September and October ahead of the election before a rally post election and into the Christmas period. Will history repeat itself?

The Week Ahead: US Jobs Data to Rule Out 50 Bps Cut?

The week ahead is actually shaping up to be a massive one for both the US Federal Reserve and Global Central Banks. The debate around rate cuts from the US has shifted toward the size of an initial cut expected on September 18, 2024.

At present the 25 bps cut is winning the race, however a softer jobs report on Friday could throw a spanner in the works. A soft jobs number could weigh on the US Dollar once more and lead to rallies in some risk assets such as US indices. The question that still remains though is how much of the rate cuts have already been priced in?

Let’s break down the key market moving events by region for the week starting Monday September 2.

Asia Pacific Markets

In Asia, the upcoming week is a busy one with a spate of inflation release from the smaller economies. The main areas of interest however will likely be Australian, Chinese and Japanese data.

Following the moderation in Australian inflation this week, GDP data will now be the focus. Unlike many of its counterparts the Reserve Bank of Australia has actually been grappling with concerts around further rate hikes as opposed to rate cuts. Thus a GDP print that shows a cooling economy is sorely needed by the RBA and thus could alleviate concerns of further rate hikes.

China’s official PMI numbers are scheduled for release by the National Bureau of Statistics on Saturday. The August PMI will likely stay mostly steady, dropping just a bit from 49.4 to 49.3. Manufacturing has slowed a little lately because car production has decreased. The Caixin PMI will also be released next Wednesday and should provide further insight into the performance of the Chinese economy and potential demand for raw material in Q4.

Japanese data continues to improve, setting the stage for continued rate hikes by the Bank of Japan (BoJ). The week ahead sees Japan sharing data on capital spending, labor earnings, and household spending, all expected to point to an economic recovery. Capital spending is expected to grow by 10% in the second quarter of 2024, up from 6.8% in the first quarter, thanks to more investments in transport and IT. There is also a strong possibility that labor earnings and household spending will get better in July, with real cash earnings rising for the second month in a row. This should help boost household spending and support the Bank of Japan’s efforts to adjust its policies.

Europe + UK + US

In Europe and the US, it’s another data-heavy week. The US is celebrating Labor day weekend with US markets closed on Monday. This should see a slow start to the week with thin liquidity on Monday..

The Uk will finally get some respite on the data front with the major economic data release coming early in the week. The BRC like-for-like retail sales YoY print will be released on Monday with no other high impact releases scheduled.

The Euro Area as well is expected to enjoy a much quieter week on the data front with composite PMI, PPi and retail sales data the main releases. Following a week in which inflation data put pressure on the Euro as market participants ramped up their rate cut bets it will be interesting to gauge the reaction the data releases.

All eyes are on the US next week as the NFP and jobs report takes center stage. This has become a major release after the largest downward revision in Jobs numbers since the Global Financial Crisis. However, the past week’s GDP and PCE data restored some confidence but the labor data remains the kingmaker ahead of the September 18 Fed meeting.

A softer jobs print on Friday could increase expectation of a 50 bps cut and scupper the DXY’s attempt at a recovery from 13 month-lows.

Chart of the Week

This week’s highlighted chart brings us back to the US Dollar Index (DXY) chart which should be no surprise. The importance of the US Dollar and US data in the week ahead makes this a no-brainer, while the technical picture throws up some interesting takeaways as well.

The DXY hit a 13-month low this week, trading at levels last seen in July 2023. The Greenback enjoyed a late week renaissance of sorts, bouncing aggressively out of a key area of support at the 100.50 level and avoiding a retest of the psychological 100.00 handle.

There is a lot of resistance up ahead though and with the US jobs data potentially serving as a catalyst on Friday, Dollar bulls will be hoping the recovery continues in the early part of the week.

The daily chart below does show that we have had a change of structure (from a price action standpoint) from bearish to bullish as Friday’s daily candle is set to close above the swing high at 101.53.

This would mean that the DXY is now on track to either push on or if there is a pullback it will likely be to print a higher low above the 100.50. WIll the NFP data facilitate a break below the 100.50 handle? This is a possibility but it would require a significant downside miss in my opinion for such a move to occur.

Immediate resistance rests at 102.16 and 102.64. Beyond that there is further resistance available 103.00, 103.65 and 104.00 which houses the 200-day MA as well.

US Dollar Index (DXY) Daily Chart – August 30, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 101.50

- 100.50

- 100.00

Resistance:

- 102.16

- 103.00

- 104.00 (200-day MA)