Sample Category Title

Crypto Fails to Bounce Off the Bottom

Market Picture

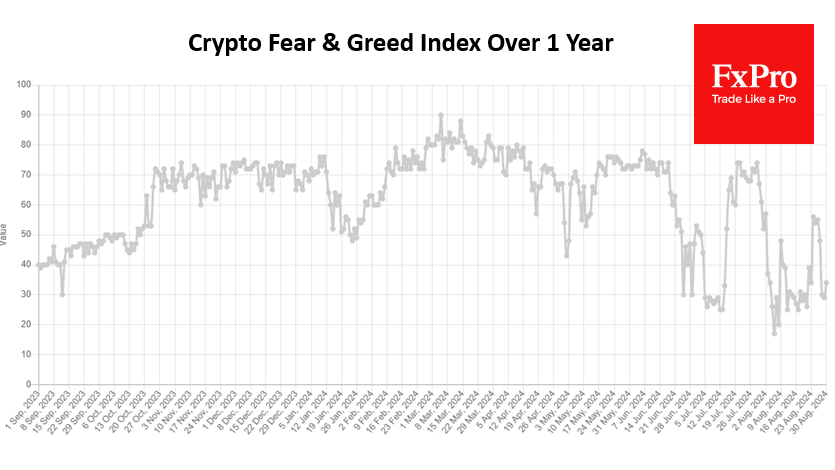

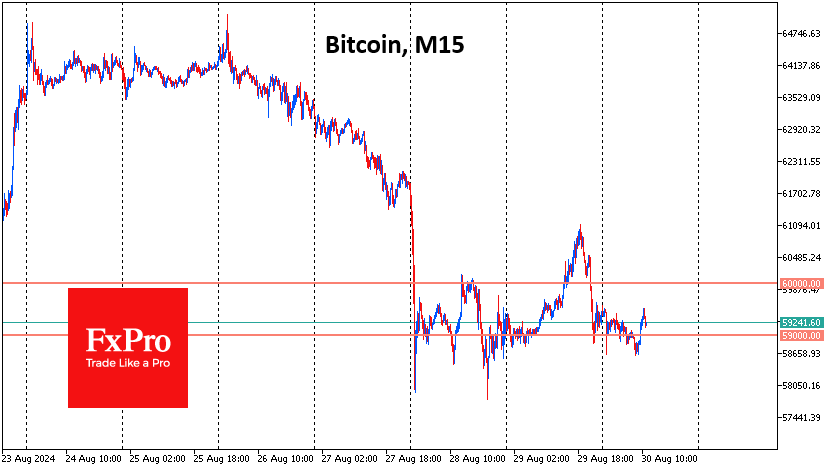

The cryptocurrency market failed to move significantly from the previous day’s levels, losing 0.5% to $2.07 trillion. Crypto followed the stock market but was noticeably weaker. Smooth growth during the day was wiped out by a late sell-off, taking capitalisation back to the local lows of recent days. Sentiment in the crypto market remains in the fear zone, with the index at 34 (+5 for the day).

Bitcoin approached $61K on Thursday, buoyed by hopes that the equity market would be able to digest the fall in Nvidia shares. However, a sell-off in the second half of the session showed that the bears were in control and the breakout was false. In early trading on Friday, BTC rolled back to $58.8K, an area of lows since August 28th.

The technical picture didn’t change much during the day: the ability to consolidate above $60K will open the way for sustained buying, while a sustained dip below $59K will accelerate selling. There could be many false signals between these levels.

News Background

Another recalculation showed that the first cryptocurrency’s mining difficulty increased by 2.99% to 89.47 T. The average Hash Rate reached a maximum value of 718.28 EH/s, indicating the continued connection of high-performance equipment.

OpenSea, one of the largest NFT trading platforms, received a warning from the US SEC about possible legal action for securities trading.

The team behind an L2 solution for Bitcoin called Stacks announced the start of the Nakamoto upgrade process. This process decouples the block production schedule from the cryptocurrency’s network. The activation will increase transaction speeds and provide a foundation for smart contracts using the BTC network as a base layer.

Donald Trump has promised to make the US the ‘crypto capital of the planet’. He announced a plan to help the US strengthen its leadership position in cryptocurrencies. Sales of Donald Trump’s fourth NFT collection exceeded $2 million. He earned ~$7.16 million in royalties from the previous three collections.

The TON team fixed the second blockchain outage in 24 hours. The outage was apparently caused by the heavy load associated with the DOGS meme token issue.

ECB’s Schnabel: Rate cuts can’t be mechanical amid stubborn domestic inflation

In a speech today, ECB Executive Board member Isabel Schnabel addressed the recent declines in inflation across parts of the Eurozone, describing them as "welcome developments." However, she cautioned that the "current level of headline inflation understates the challenges monetary policy is still facing."

Schnabel highlighted that domestic inflation remains elevated at 4.4%, driven largely by "persistent price pressures in the services sector," where disinflation has stalled since last November. She pointed out that the continued high inflation momentum, particularly the annualized three-month-on-three-month change, indicates that services prices are still rising at a significant pace of almost 5%.

Schnabel noted that while incoming data broadly supports ECB's baseline outlook, caution is needed as policy rates approach the upper band of the neutral rate, "the less certain we are how restrictive our policy is"

The pace of policy easing, she emphasized, "cannot be mechanical" and must be guided by data and analysis to ensure that monetary policy does not itself become a factor hindering disinflation.

Swiss KOF rises to 101.6, signaling hesitant economic recovery

Swiss KOF Economic Barometer edged up to 101.6 in August, slightly above expectations of 100.6, signaling a modest improvement in economic activity. The indicator remains just above its medium-term average, suggesting that Swiss economy is on what KOF describes as a "hesitant recovery path."

The upward movement in the Barometer was driven primarily by gains in the other services sector, consumer demand, and construction industry. Additionally, the manufacturing and hospitality sectors saw modest improvements.

Meanwhile, the indicators for foreign demand remained nearly stable, while the financial and insurance services sector faced a slight decline.

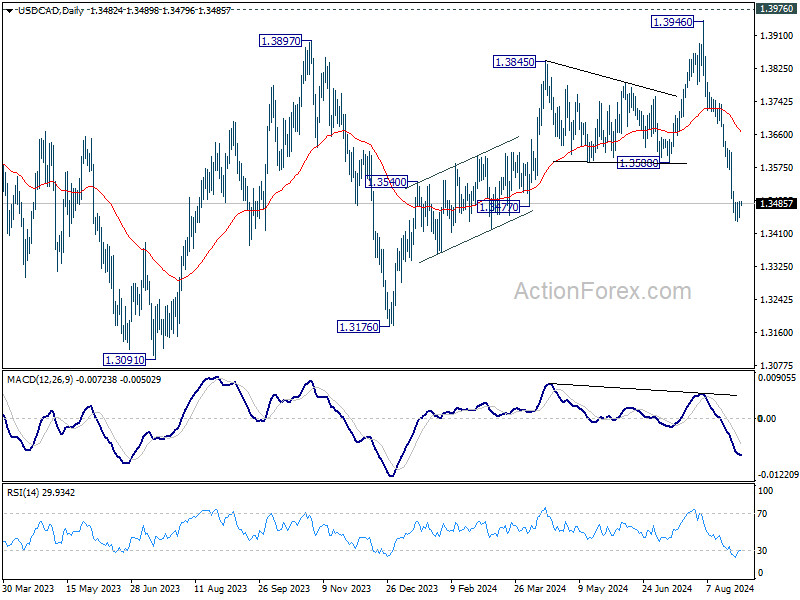

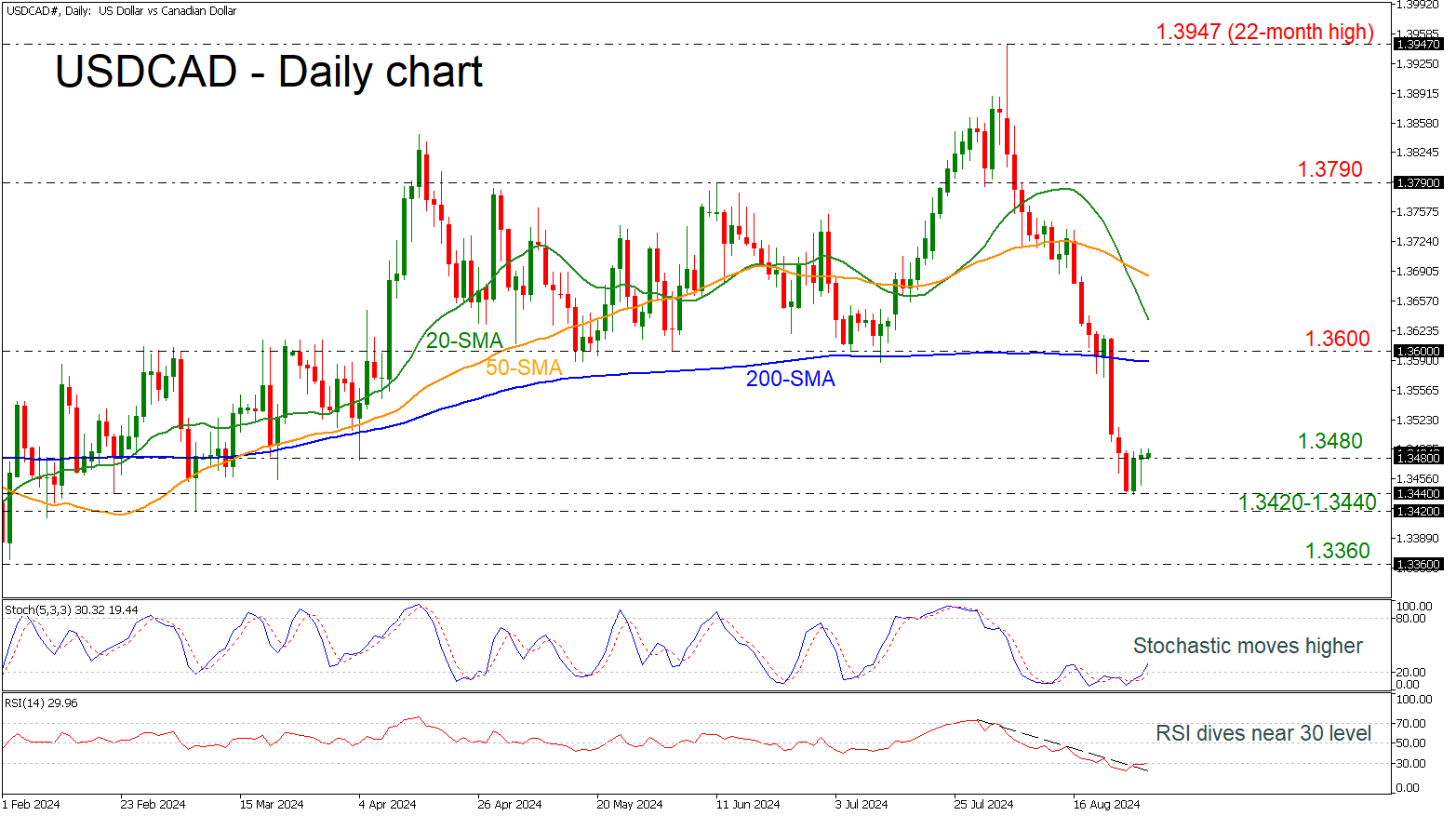

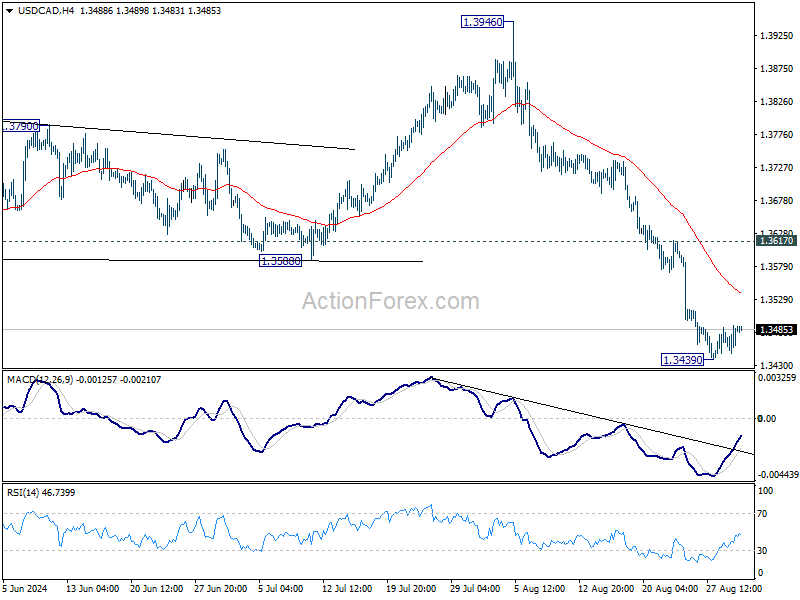

USDCAD Rises From Almost 6-Month Low

- USDCAD changes the outlook to bearish after the fall below 1.3600

- Stochastic ticks up but RSI still holds near 30 zone

USDCAD is recouping some losses after the strong selling interest that started from the penetration of the 1.3600 round number and the 200-day simple moving average (SMA). The pair found support near the 1.3440 level, which is an almost six-month low.

Currently the market is trying to remain above the 1.3480 barricade with the technical oscillators suggesting more buying interest. The stochastic is pointing upwards following a bullish crossover within its %K and %D lines, while the RSI is flattening near the 30 level after it bottomed in the oversold region.

In case of more bullish movements the next battle would come again with the 1.3600 psychological mark ahead of the 20- and 50-day SMAs at 1.3635 and 1.3685 respectively.

On the other hand, a slide beneath the 1.3420-1.3440 support area could open the way for a new low in the short-term, meeting the 1.3360 barricade, taken from the trough on January 31.

All in all, USDCAD has decreased around 4% from the 22-month high of 1.3947 and switched the near-term outlook to bearish.

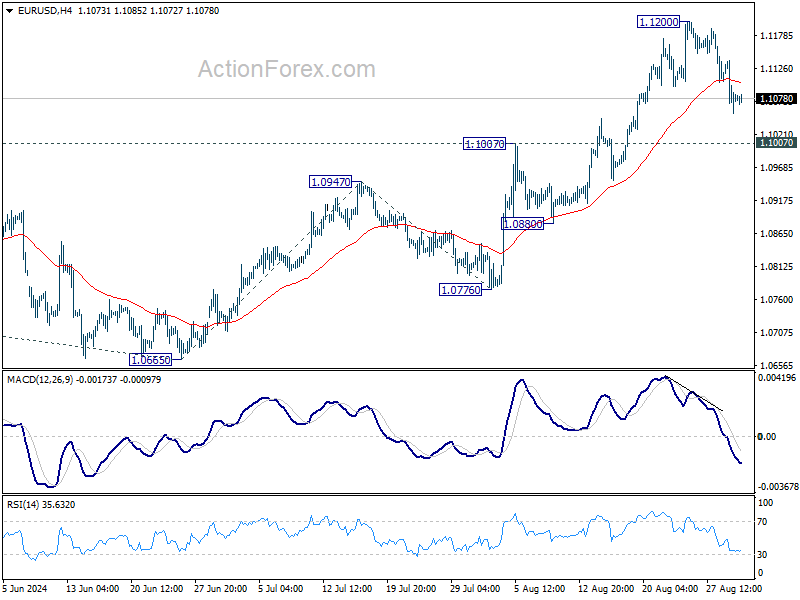

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1043; (P) 1.1091; (R1) 1.1127; More....

While EUR/USD's retreat from 1.1200 extended lower, downside is contained above 1.1007 resistance turned support. Intraday bias remains neutral and larger rally is still expected to continue. On the upside, break of 1.1200 will resume recent rally to 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

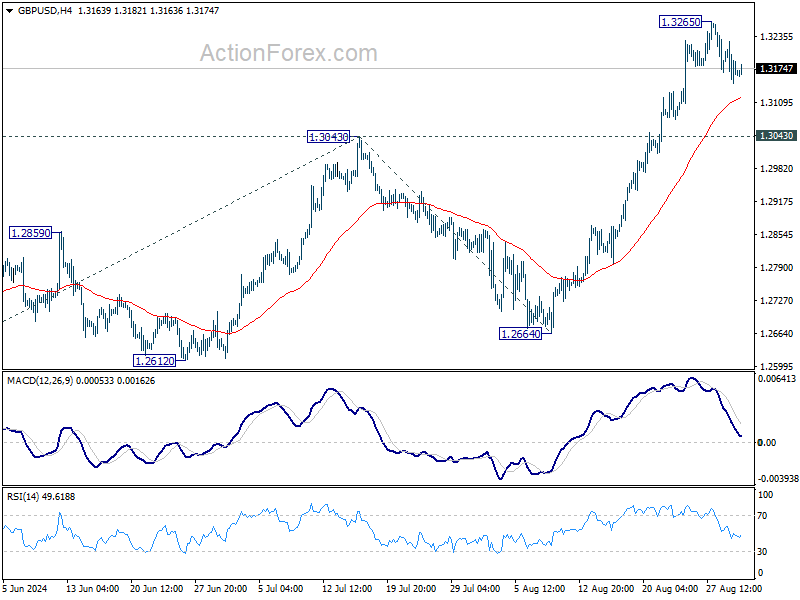

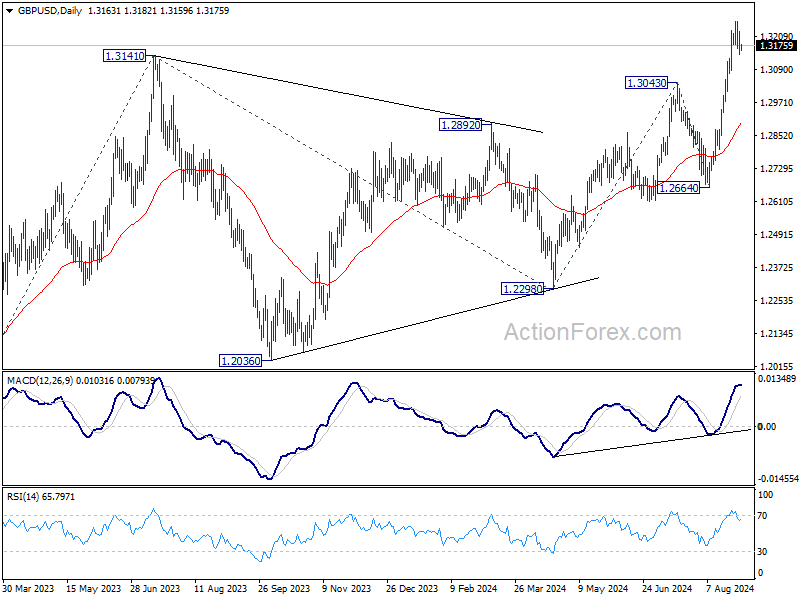

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3133; (P) 1.3180; (R1) 1.3215; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3265 is still expected. Downside of retreat should be contained well above 1.3043 resistance turned support to bring rebound. On the upside, above 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

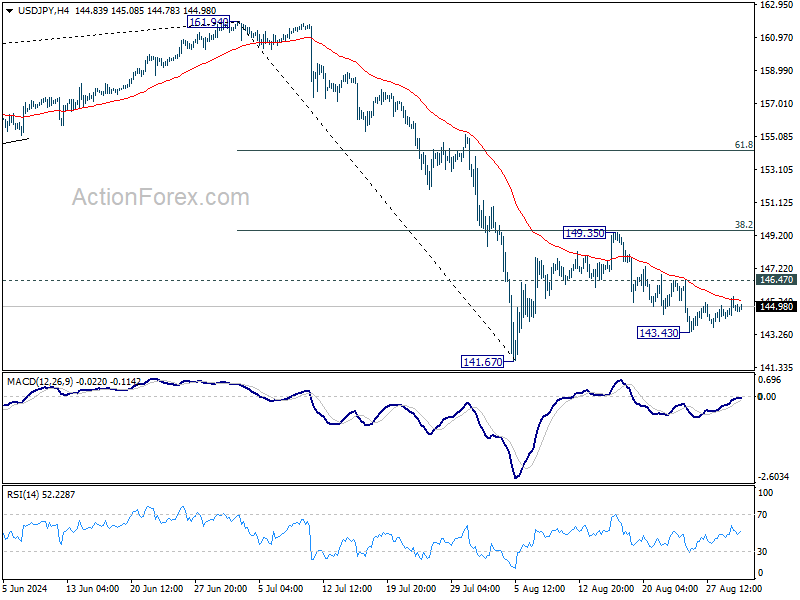

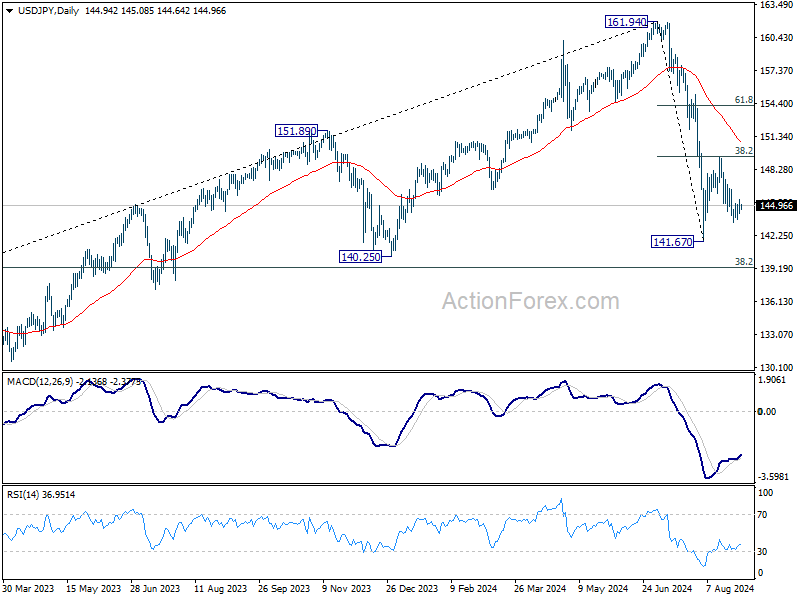

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.28; (P) 144.92; (R1) 145.61; More...

Intraday bias in USD/JPY stays neutral but further fall is in favor with 146.47 minor resistance intact. Break of 143.43 will bring retest of 141.67 low. Firm break there will resume the whole fall from 161.94 to 140.25 support next. On the upside, above 146.47 will turn intraday bias back to the upside for 149.35 resistance instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.38) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

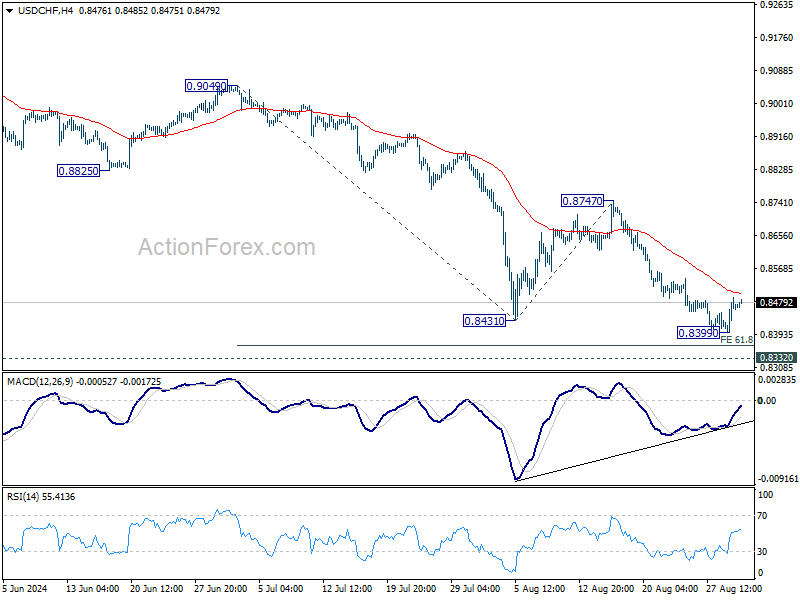

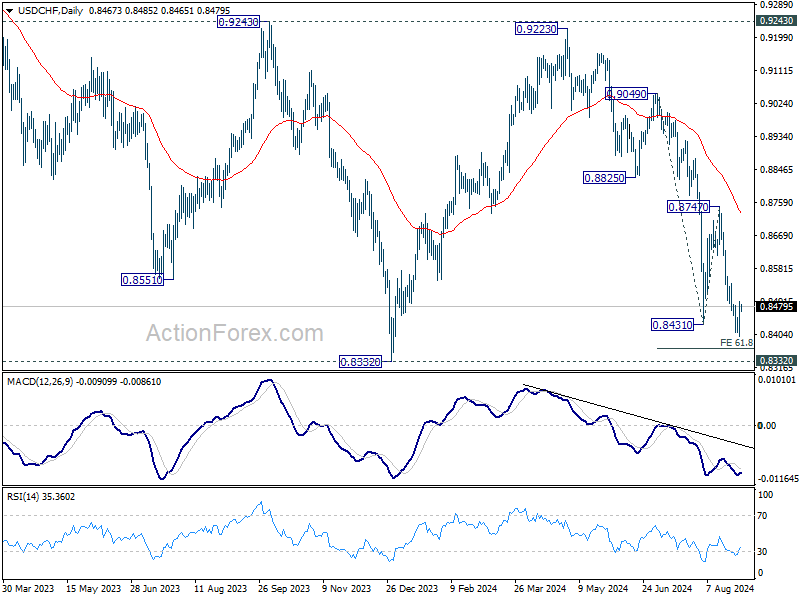

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8418; (P) 0.8456; (R1) 0.8512; More…..

Intraday bias in USD/CHF remains neutral as consolidation continues above 0.8399. Outlook will remain bearish as long as 0.8747 resistance holds. Break of 0.8339 will resume the decline from 0.9223 and target 61.8% projection of 0.9049 to 0.8431 from 0.8747 at 0.8365, and then 0.8332 low.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

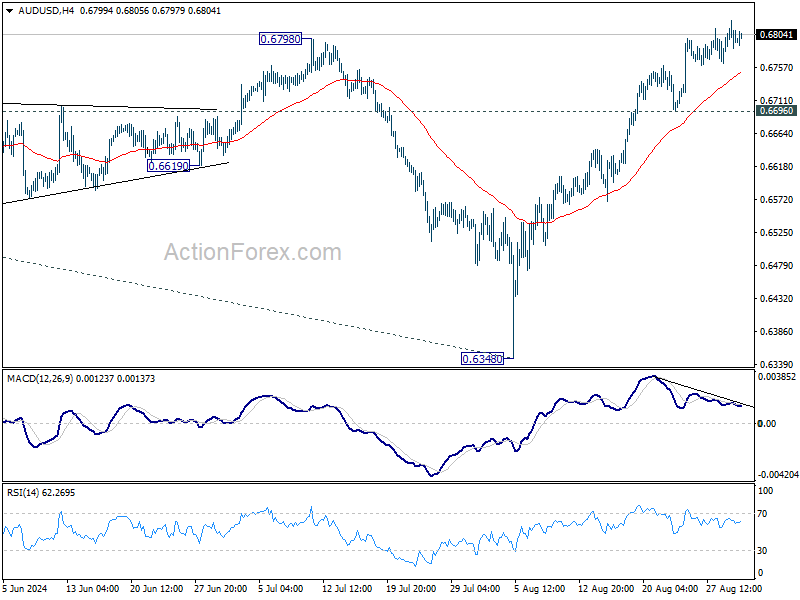

AUD/USD Daily Report

Daily Pivots: (S1) 0.6776; (P) 0.6800; (R1) 0.6822; More...

AUD//USD continues to lose upside moment as seen in 4H MACD, but there is no clear sign of topping yet. Further rally is expected as long as 06696 support holds. Current rally should target 0.6870 resistance. Firm break there will target 100% projection of 0.6269 to 0.6870 from 0.6348 at 0.6949. However, break of 0.6696 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3459; (P) 1.3475; (R1) 1.3500; More...

USD/CAD continues to consolidate above 1.3439 temporary low and intraday bias remains neutral. Upside of recovery should be limited below 1.3617 resistance to bring another fall. On the downside, below 1.3439 will resume the decline from 1.3946 and target 1.3176 support next.

In the bigger picture, current development suggests that corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.