Sample Category Title

Weak German Inflation vs Healthy US Data

Germany data

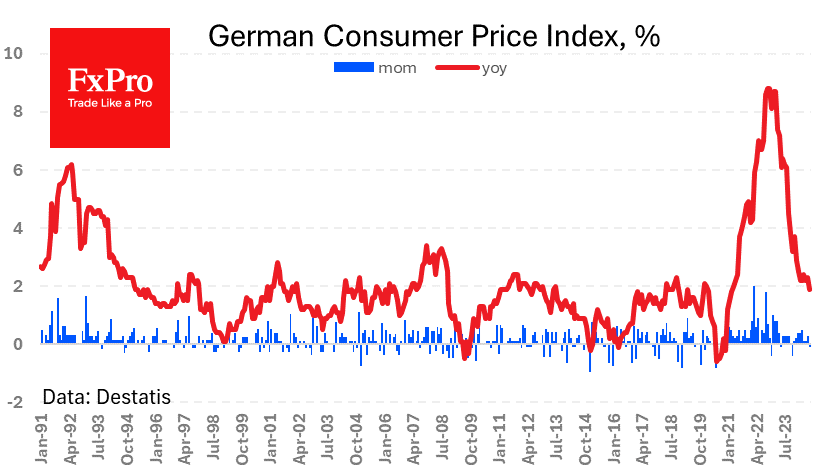

German inflation is slowing more than expected. According to a preliminary estimate from Destatis, the consumer price index fell 0.1% in August, and annual inflation slowed to 1.9%, compared to 2.3% in the previous month and the 2.1% expected.

Germany released state-specific data later in the day, and the weak readings put pressure on the Euro. The weakness in inflation is further evidence of a limping economy. The data will also weigh on Friday’s Euro-zone CPI estimates. At the start of the week, the average forecast was for a decline from 2.6% to 2.2%, but after the German data, a slowdown to 2.0% would not be too surprising.

The EUR/USD pair fell back to 1.1070 on the news. Since the beginning of the week, we have seen negative surprises in other macroeconomic data from the European economy’s locomotive.

US data

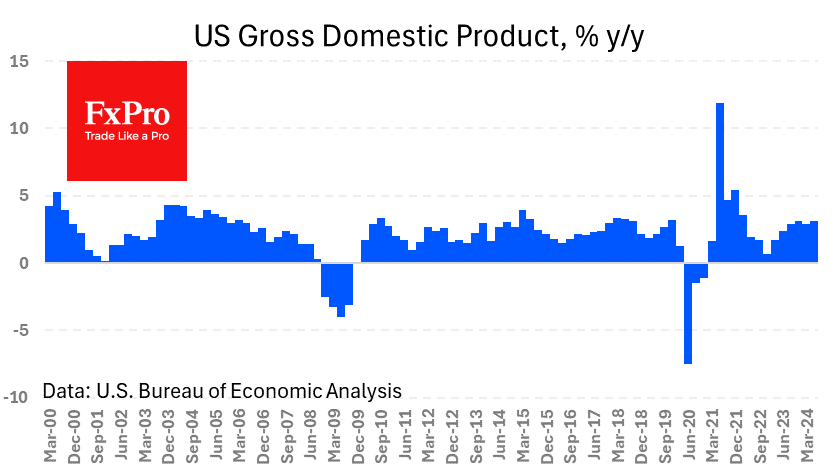

At the same time, macro data from the US continues to be strong. A revised estimate of Q2 GDP growth is 3.0% from 2.8%, and there is a drop in weekly jobless claims from 233K to 231K. Continuing claims rose from 1855K to 1868K. In both cases, these are stronger than expected readings (short-term positive) at historically low levels (long-term positive).

This solid data makes us question the appropriateness of a 50-point cut in the Fed Funds rate in September. However, the futures market is pricing in a 33% chance of such an outcome (67% in favour of a 25-point cut), leaving the potential for dollar strength on a reassessment of expectations. The Fed and the markets are unlikely to make a final decision until after the employment data in early September and the inflation data in the middle of next month.

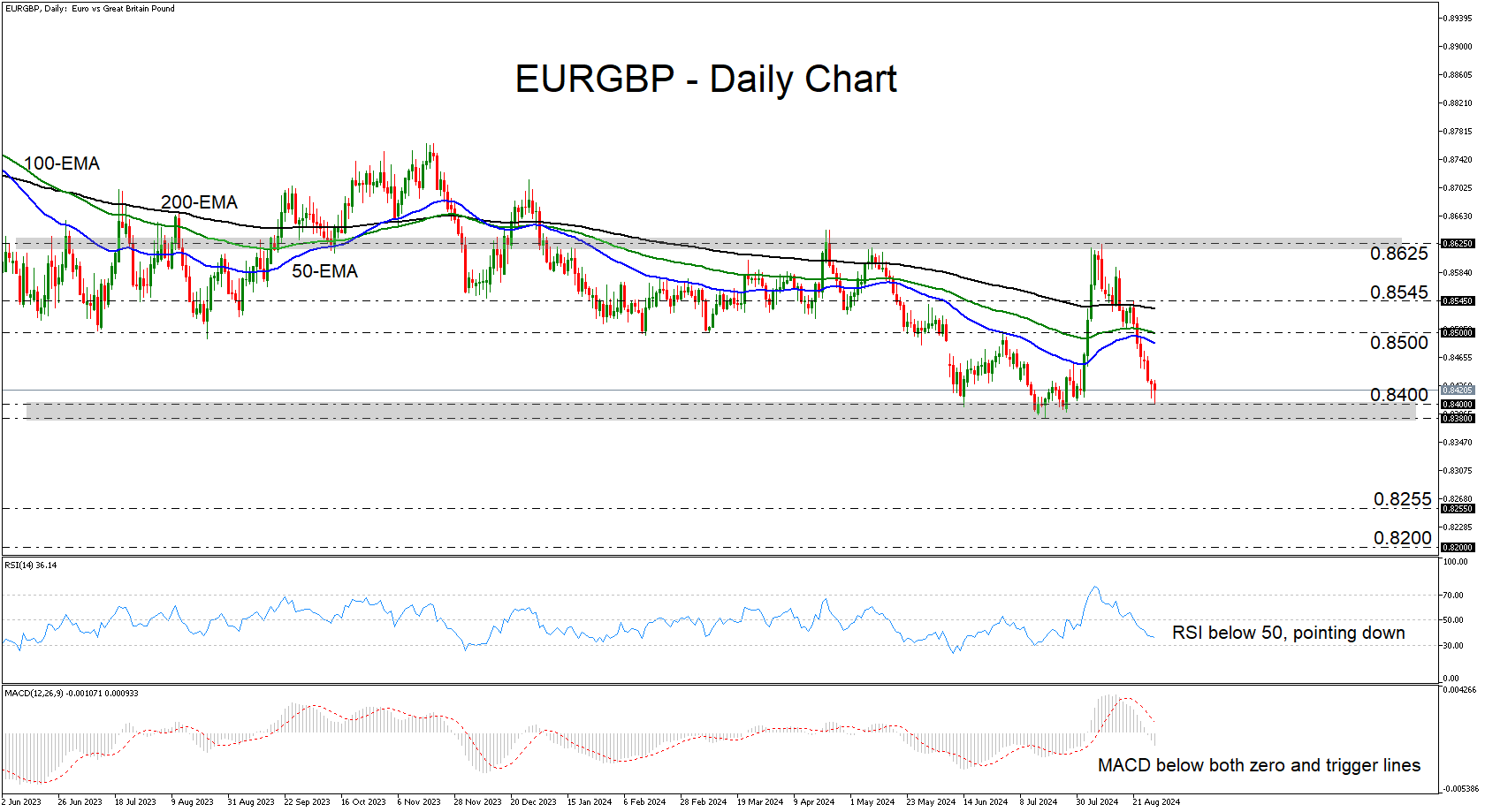

EURGBP Flirts With Key Support Territory

- EURGBP tumbles, but finds support near 0.8400

- RSI and MACD detect bearish momentum

- But a break below 0.8380 is needed for further declines

- A move above 0.8500 could keep the picture neutral

EURGBP has been in a steady slide since August 8, when it hit the key resistance zone of 0.8625. That said, the pair is currently flirting with the all-important support area of 0.8380-0.8400, a break below which may be needed for the near-term outlook to clearly be considered bearish.

The RSI is lying below 50 and looks to be headed towards its 30 line, while the MACD is running below both its zero and trigger lines. Both oscillators are detecting bearish momentum and suggest that there is a decent chance for the pair to break below the aforementioned key support area.

If so, the bears will find themselves exploring territories last seen two years ago, with the next line of defense for the bulls resting at 0.8255, marked by the low of April 14, 2022. If there is no buying interest there, the slide may extend towards the low of March 7 of that year, at around 0.8200.

On the upside, a rebound from around 0.8400 could take the action towards the 0.8500 barrier, where a break could aim for the 0.8545 hurdle. If the bulls remain in charge, the next stop may be the key 0.8625 ceiling.

To recap, EURGBP has fallen sharply lately, but for the near-term technical outlook to be considered overly bearish, a decisive dip below 0.8380 may be necessary.

Sunset Market Commentary

Markets

Spanish and German consumer prices rose less than expected in August. Spanish prices were flat in M/M terms with headline CPI falling more than forecast, from 2.9% to 2.4%. German prices even fell by 0.2% M/M to be up 2% Y/Y (from 2.6% vs 2.2% expected). It was the first time since March 2021 that they hit the ECB 2% price goal. The drop is mainly the result of lower energy prices and favorable base effects for goods. Looking at core inflation, the disinflationary trends was much more modest both in Spain (2.7% from 2.8%) and Germany (2.8% from 2.9%). Markets nevertheless welcomed the outcome. The front end of the European yield curve outperforms with the German 2-yr yield currently 2.1 bps lower. Losses were bigger intraday. 25 bps rate cuts at all three remaining ECB meetings still aren’t fully discounted yet. Tenors from 7-yr and longer are 1 to 2.5 bps higher in line with the US move. US yields add 2.5 bps to 4 bps across the curve. The move started after an upward revision to Q2 GDP numbers (3% Q/Qa from 2.8%). Personal consumption increased by 2.9% Q/Qa from an earlier reported 2.3% (and vs 2.2% expected). Weekly jobless claims stabilized for a fourth week running around 230k after their increase to the 250k area in the month of July. Data help putting to bed recent US recession fears. The loss of interest rate support weighs on the single current with EUR/USD slipping from levels around 1.1140 ahead of first regional German CPI’s to 1.1090 currently. EUR/GBP tried to test the 0.84 handle, but without success. European stock markets rallied up to 0.8% for the likes of the EuroStoxx50 which took out the August recovery high in the process and is on his way back to the 5k mark. US stock markets open up to 1% higher for Nasdaq, recovering from the overnight scare (up to -2.5% for futures) in the wake of yesterday’s Nvidia results (-2% from -6%).

News & Views

Swedish GDP growth decreased by 0.3% Q/Q in Q2. Activity was 0.5% higher compared to the same period last year. The decline was less than an initial flash estimate published end July (-0.8% Q/Q). According to Statistics Sweden the setback in the economy was wide, but offset by a positive contrition from net exports (0.9 ppts contribution) as exports increased (1.0%) and imports declined (0.6%). Household consumption fell 0.2% Q/Q. General government consumption increased a small 0.1%. Gross fixed capital formation fell 1.7% Q/Q, mainly due to investments in machinery and equipment and weapon systems. Investments in intellectual property products increased for the second consecutive quarter. Changes in inventories also were an important drag on overall growth (negative contribution of 0.6 ppts). The number of employed persons decreased by 0.2 percent. The number of hours worked decreased by 0.5% in the whole economy and by 0.9% in the business sector. Labour productivity in the business sector increased 0.4%. Household real disposable income increased by 2.0% Y/Y. Poor domestic demand supports the case for further Riksbank easing. The RB last week cut its policy rate from 3.75% to 3.50% and indicated that it could accelerate the pace of rate cuts compared to earlier guidance. A 25 bps rate cut at each of the 3 remaining meetings this year is possible. After a rebound of the krone since the early August sell-off, the Swedish currency today trades little changed EUR/SEK (11.345).

Belgian CPI consumer prices were unchanged from July in August. Y/Y inflation declined from 3.64% to 2.86%. Core inflation (excluding energy products and unprocessed food) stood at 2.73% Y/Y, compared to 3.04% in July and 2.97% in June. In a monthly perspective, the most significant price increases were registered for tobacco (5.4%), private rents (0.6%), non-alcoholic beverages (1.7%), hotel rooms ,(2.1%) clothing (0.5%) and restaurants and cafés (0.3%). However, motor fuels (-3.9%), household appliances(-6.9%), flowers and plants (-4.7%), vegetables (-1.2%) and natural gas (1.6%) had a decreasing effect on the index. The first inflation estimate according to the European harmonized index of consumer prices (HICP flash estimate) for Belgium amounts to 4.5% for August 2024.

Graphs

EU 2y swap rate ticks lower on stronger headline disinflationary trends in Spain and Germany in August

EUR/SEK: tough environment for more SEK-gains despite some euro weakness today

EUR/USD: stronger US data also help the pair away from 1.12 area

EuroStoxx50: (more?) rate cuts are coming!

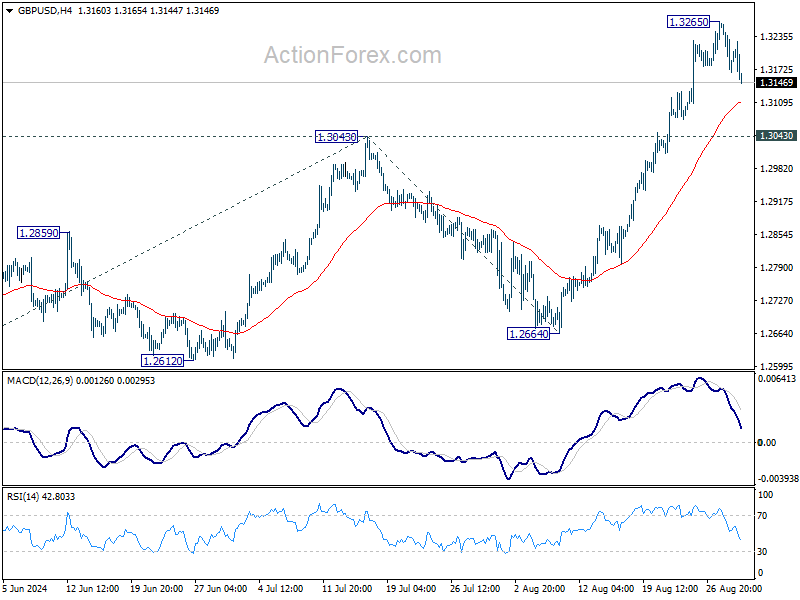

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3151; (P) 1.3208; (R1) 1.3249; More...

GBP/USD is staying in consolidation below 1.3265 and intraday bias stays neutral. Downside of retreat should be contained well above 1.3043 resistance turned support to bring rebound. On the upside, above 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

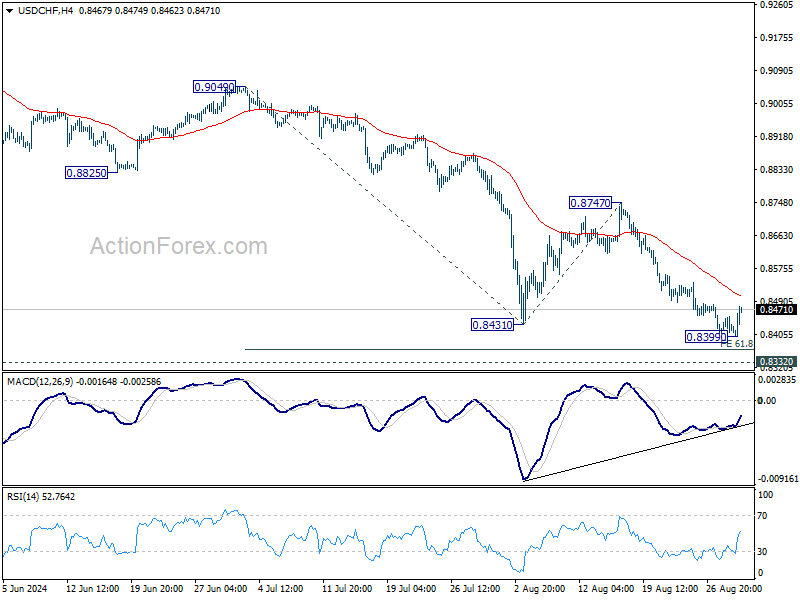

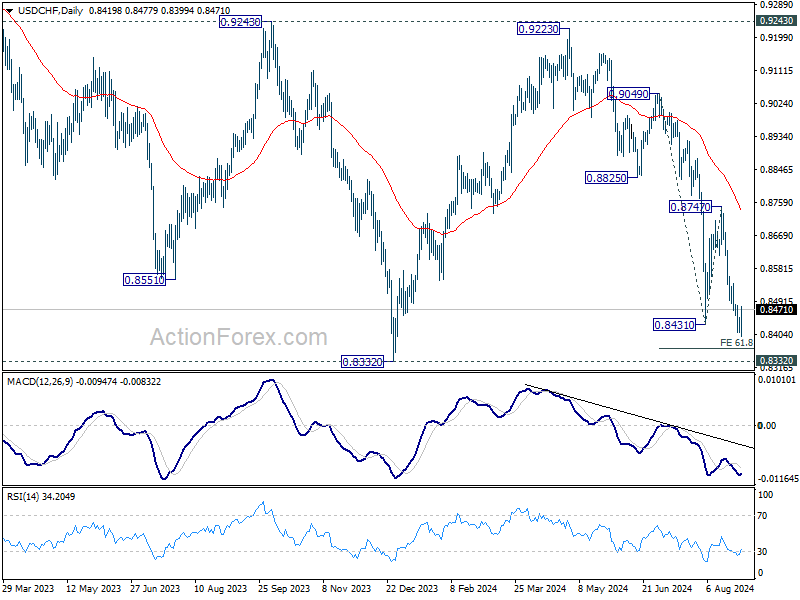

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8401; (P) 0.8431; (R1) 0.8452; More…..

Intraday bias in USD/CHF is turned neutral with current recovery and some consolidations could be seen. But outlook will remain bearish as long as 0.8747 resistance holds. Break of 0.8339 will resume the decline from 0.9223 and target 61.8% projection of 0.9049 to 0.8431 from 0.8747 at 0.8365, and then 0.8332 low.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

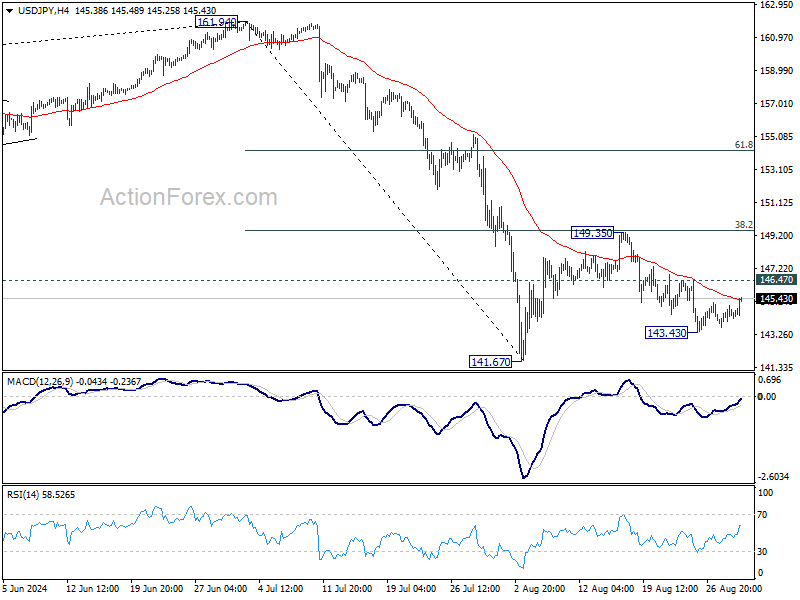

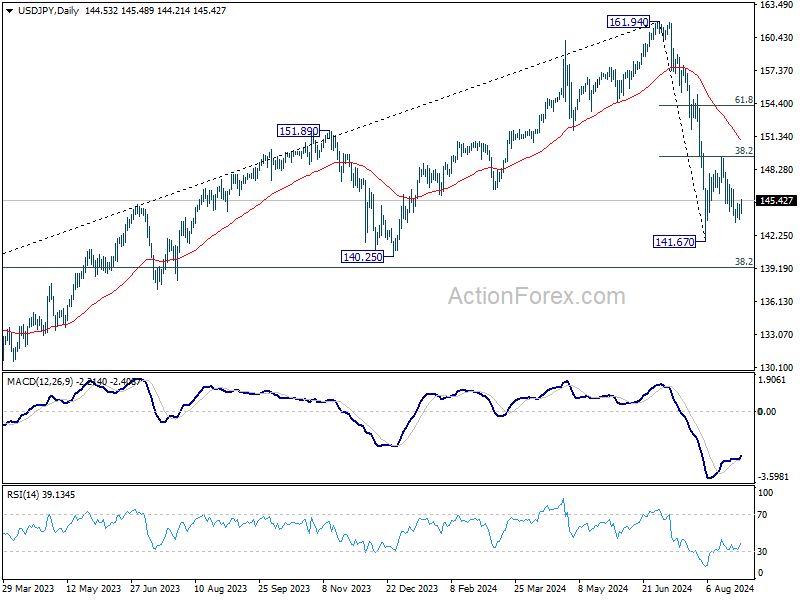

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.84; (P) 144.44; (R1) 145.19; More...

Intraday bias in USD/JPY is turned neutral as recovery from 143.43 extends. With 146.47 minor resistance intact, further decline is in favor. Break of 143.43 will bring retest of 141.67 low. Firm break there will resume the whole fall from 161.94 to 140.25 support next. On the upside, above 146.47 will turn intraday bias back to the upside for 149.35 resistance instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.38) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

U.S. Economic Resilience on Display in the Second Quarter

The second estimate of second quarter real GDP growth was revised up 0.2 percentage points (pp) to 3.0% quarter-over-quarter annualized (q/q) – slightly above the consensus forecast.

Looking under the hood, an upward revision to consumer spending (2.9% q/q vs. prior 2.3% q/q) was largely responsible for last quarter's upgrade. Spending on both goods (3.0% q/q vs. prior 2.5% q/q) and services (2.2% q/q vs prior 2.8% q/q) were revised higher. Meanwhile, non-residential investment saw a modest downward revision to 4.6% q/q, thanks to downgrades in both equipment spending (10.6% q/q vs. prior 11.6% q/q) and intellectual property products (2.6% q/q vs. prior 4.5% q/q).

Government spending was reported to have expanded by 2.7% q/q, with healthy gains from both the federal (+3.3% q/q) and state & local (2.3% q/q) level.

Net exports shaved 0.8 pp from Q2 growth (unchanged from the prior estimate), though this was entirely offset by an equal gain in inventory investment.

Real Gross Domestic Income (GDI) rose by 1.3% q/q in the second quarter, matching Q1's gain. Corporate profits were up 7.0% (annualized) or $57.6 billion after accounting for inventory valuation and capital consumption adjustments. The ratio of corporate profits to nominal GDP ticked up 0.1 pp to 12.0%.

- The average of GDP and GDI, a supplemental estimate of domestic production, rose 2.1% q/q in the second quarter or slightly weaker than the pace of growth suggested by the expenditure GDP data.

Key Implications

The Bureau of Economic Analysis' second estimate of Q2 GDP saw a very modest upward revision relative to the preliminary reading. Overall, the economy continued to show ongoing resilience through the second quarter, as evidenced by the breadth of gains across domestic drivers. Final domestic demand (i.e., the sum of consumer spending, fixed investment, and government outlays) rose by a healthy 2.9% in Q2 and averaged 2.8% through the first half of the year – largely unchanged from H2-2023's 3.1%.

That said, there was at least some evidence in this morning's report to suggest that the economy's resilience will soon start to wane. For starters, the uptick in Q2 PCE was driven by a rebound in goods spending, which we do not expect to continue, particularly given the recent softening in labor market fundamentals. Second, the sharp acceleration in equipment outlays can largely be traced back to a surge in aircraft purchases last quarter and is unlikely to be repeated in Q3. Lastly, the gain in federal spending was the result of a notable bump in national defense outlays, which is also likely to mean revert over the coming quarters. All that to say, we appear to be in a goldilocks scenario where growth is likely to gradually edge lower through the second half of the year, allowing inflation to drift closer to the Fed's 2% target. This should enable the FOMC to cut its policy rate by at least 75 basis points by year-end.

Aussie Rises to 8-Month High, Retail Sales Next

The Australian dollar has posted considerable gains on Thursday. AUD/USD is trading at 0.6816 in the European session, up 0.47% on the day at the time of writing. The US dollar continues to struggle against the major currencies and the Aussie has taken full advantage with an impressive 4.1% gain in August.

Australian retail sales projected to ease

Australia’s retail sales are expected to fall to 0.3% m/m in July, compared to 0.5% in June. The retail sector has been limping as consumers are being squeezed by high interest rates and the high cost of living. The weak economy and a cooling labor market are making consumers even more cautious about discretionary spending.

The Reserve Bank of Australia continues to sound hawkish and Governor Bullock has said that interest rate cuts remain unlikely in the next six months. The markets aren’t buying it and have priced in a rate cut in November with more cuts in early 2025. The RBA discussed a rate hike at the meeting earlier this month but the markets are betting that the RBA won’t become an outlier with the Federal Reserve set to cut rates next month.

The RBA is showing some frustration at the slow pace of disinflation. CPI rose 3.5% on July, down from 3.8% a month earlier but higher than the market estimate of 3.6%. Core CPI eased to 3.7%, the lowest level since January 2022. Inflation remains above the RBA’s target range of 2-3% and the Bank is wary about cutting rates until inflation falls further.

Fed’s Bostic urges caution on rate cut

The Federal Reserve is poised to cut rates next month after Jerome Powell stated last week that it was time to loosen policy. Most FOMC members have come out in favor of a September cut but Atlanta Fed President Raphael Bostic urged the Fed to wait for additional data before lowering rates as it would be a mistake to cut and then have to hike again.

AUD/USD Technical

- AUD/USD pushed above resistance at 0.6788 and is testing resistance at 0.6710. Above, there is resistance at 0.6836

- 0.6762 and 0.6740 are the next support levels

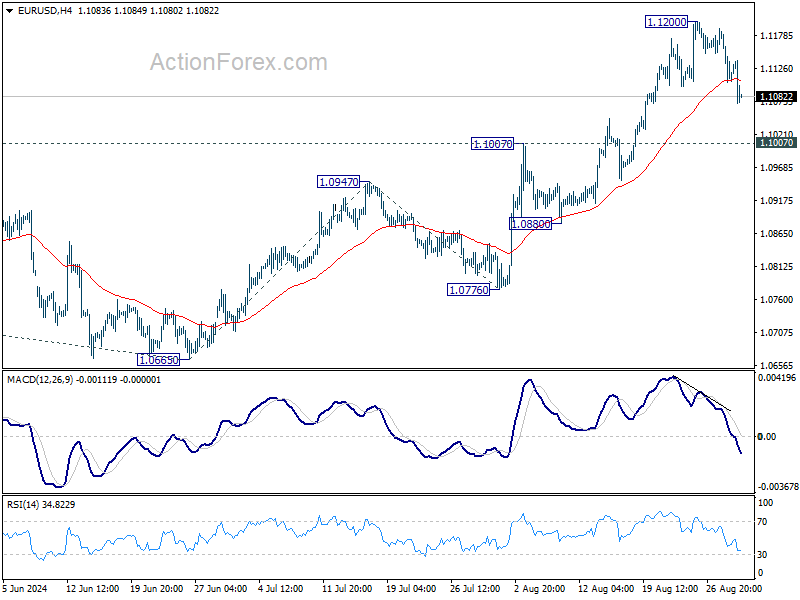

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1087; (P) 1.1138; (R1) 1.1170; More....

EUR/USD's retreat from 1.1200 extends lower today, but stays well above 1.1007 resistance turned support. Intraday bias remains neutral and larger rally is still expected to continue. On the upside, break of 1.1200 will resume recent rally to 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Euro Sinks as Weak Inflation Data Bolsters Case for Faster ECB Rate Cuts

Euro fell notably in European session today, as inflation data from both Germany and Spain significantly underperformed expectations. The rapid deceleration in price pressures strengthens the argument for a September rate cut by ECB. With inflation slowing faster than anticipated, there is growing speculation that ECB could have the flexibility to implement two additional rate cuts this year, totaling 100 basis points, to provide much-needed support to the faltering economies of major Eurozone nations like Germany and France.

Despite Euro's struggles, Swiss Franc has emerged as the day's weakest performer for the day so far, followed by the Yen, while the common currency is just the third worst. Australian Dollar, on the other hand, has reversed earlier losses against New Zealand Dollar to become the strongest performer of the day. Kiwi also remains buoyant, bolstered by robust business confidence data, making it the second-best performer, with Canadian Dollar trailing in third place. Meanwhile, US Dollar and British Pound are holding steady in middle positions.

In the broader market, US risk sentiment appears to be recovering, with stock futures pointing to a positive market open. The initial jitters caused by Nvidia's earnings report and its cautious forecast have subsided. Focus is now back on whether DOW can break to new record highs and power through 41376 resistance cleanly. Or, if momentum fades, the index might reverse and test the 40584.47 support to confirm short-term topping by the end of the week.

In Europe, at the time of writing, FTSE is up 0.44%. DAX is up 0.64%. CAC is up 0.75%. UK 10-year yield is up 0.0053 at 3.990. Germany 10-year yield is up 0.016 at 2.277. Earlier in Asia, Nikkei fell -0.02%. Hong Kong HSI rose 0.53%. China Shanghai SSE fell -0.50%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield fell -0.0047 to 0.890.

US goods trade deficit at USD -102.7B in Jul

US goods exports fell -0.0% mom to USD 172.9B in July. Goods imports fell -3.2% mom to USD 275.6B. Trade balance reported USD -102.7B deficit, larger than expectation of USD -97.1B.

Wholesale inventories rose 0.3% mom to USD 904.9B. Retail inventories rose 0.8% mom to USD 811.4B.

US initial jobless claims fall to 231k, vs exp 234k

US initial jobless claims fell -2k to 231k in the week ending August 24, slightly below expectation of 234k. Four-week moving average of initial claims fell -5k to 232k.

Continuing claims rose 13k to 1868k in the week ending August 17. Four-week moving average of continuing claims fell -250 to 1863k.

ECB's Lane signals confidence in inflation control with slower wage growth ahead

ECB Chief Economist Philip Lane noted at a conference today that while the second half of this year will still witness "plenty of wage increases," the momentum is expected to taper off significantly.

Lane emphasized that “the catch-up is peaking now,” suggesting that the pace of wage hikes will slow substantially over the next two years.

Lane highlighted the "lot of progress" made in reducing underlying price pressures, pointing out the rising optimism surrounding the anticipated deceleration in wage growth. "This is where the confidence in returning to target comes from," he added.

Eurozone economic sentiment rises to 96.6, EU up to 96.9

Eurozone Economic Sentiment Indicator rose from 96.0 to 96.6 in August. Employment Expectations Indicator rose from 97.9 to 99.2. Economic Uncertainty Indicator fell from 17.9 to 17.2.

Eurozone industry confidence rose from -10.4 to -9.7. Services confidence rose from 5.0 to 6.3. Consumer confidence fell from -13.0 to -13.5. Retail trade confidence rose from -9.1 to -8.1. Construction confidence rose from -9.1 to -8.1.

EU Economic Sentiment Indicator rose from 96.5 to 96.9. Employment Expectations Indicator rose form 98.7 to 99.6. Economic Uncertainty Indicator fell from 17.1 to 6.6.

For the largest EU economies, the ESI improved strikingly for France (+4.3). It also improved significantly for Spain (+1.3) and the Netherlands (+0.9), while for Poland the ESI recorded only a slight increase (+0.3). The ESI deteriorated for Germany (-1.7) and Italy (-1.2).

NZ ANZ business confidence hits decade high, activity outlook at 7-yr peak

New Zealand's ANZ Business Confidence surged in August, reaching 50.6, the highest level in a decade, up from 27.1 in July. This sharp increase was accompanied by a notable rise in the own activity outlook, which jumped from 16.3 to a seven-year high of 37.1.

Breaking down the data, investment intentions climbed from -1.4 to 6.9, while employment intentions improved from -3.6 to 11.9. Profit expectations also saw a positive shift, moving from -3.6 to 8.0.

Cost expectations remained elevated, ticking up slightly from 68.2 to 68.3, and pricing intentions rose from 37.6 to 41.0. On a positive note, inflation expectations fell from 3.20% to 2.92%, finally falling within the RBNZ's target band.

ANZ highlighted that the significant increases in confidence and activity expectations were already evident at the beginning of August. The responses collected after RBNZ's Official Cash Rate cut did not significantly alter the overall results.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1087; (P) 1.1138; (R1) 1.1170; More....

EUR/USD's retreat from 1.1200 extends lower today, but stays well above 1.1007 resistance turned support. Intraday bias remains neutral and larger rally is still expected to continue. On the upside, break of 1.1200 will resume recent rally to 161.8% projection of 1.0665 to 1.0947 from 1.0776 at 1.1232, and then 1.1274 high.

In the bigger picture, break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Aug | 50.6 | 27.1 | ||

| 01:30 | AUD | Private Capital Expenditure Q2 | -2.20% | 1.10% | 1.00% | 1.90% |

| 05:00 | JPY | Consumer Confidence Index Aug | 36.7 | 37.1 | 36.7 | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | 96.6 | 95.9 | 95.8 | 96 |

| 09:00 | EUR | Eurozone Industrial Confidence Aug | -9.7 | -10.6 | -10.5 | -10.4 |

| 09:00 | EUR | Eurozone Services Sentiment Aug | 6.3 | 5.1 | 4.8 | 5 |

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | -13.5 | -13.4 | -13.4 | |

| 12:00 | EUR | Germany CPI M/M Aug P | -0.10% | 0.00% | 0.30% | |

| 12:00 | EUR | Germany CPI Y/Y Aug P | 1.90% | 2.10% | 2.30% | |

| 12:30 | CAD | Current Account (CAD) Q2 | -8.5B | -6.0B | -5.4B | |

| 12:30 | USD | Initial Jobless Claims (Aug 23) | 231K | 234K | 232K | 233K |

| 12:30 | USD | GDP Annualized Q2 P | 3.00% | 2.80% | 2.80% | |

| 12:30 | USD | GDP Price Index Q2 P | 2.50% | 2.30% | 2.30% | |

| 12:30 | USD | Goods Trade Balance (USD) Jul P | -102.7B | -97.1B | -96.6B | -96.6B |

| 12:30 | USD | Wholesale Inventories Jul P | 0.30% | 0.20% | 0.20% | |

| 14:00 | USD | Pending Home Sales M/M Jul | 0.20% | 4.80% | ||

| 14:30 | USD | Natural Gas Storage | 33B | 35B |