Sample Category Title

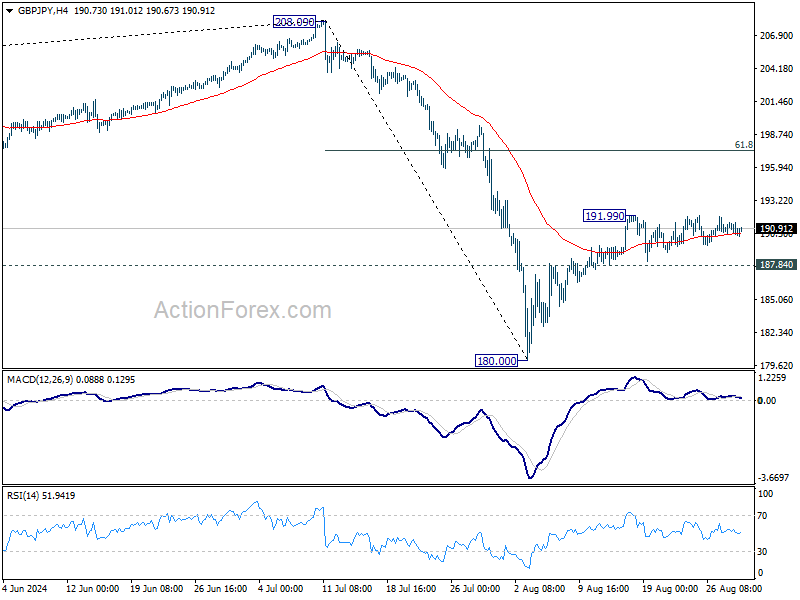

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.24; (P) 190.85; (R1) 191.33; More...

GBP/JPY is still bounded in consolidation below 191.99 and intraday bias remains neutral for the moment. On the upside, above 191.99 will target 61.8% retracement of 208.09 to 180.00 at 197.35, as the second leg of the corrective pattern from 208.09. On the downside, however, firm break of 187.84 support will argue that rebound from 180.00 has completed, and turn bias back to the downside for retesting 180.00 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). Current development suggests that the first leg has completed and the range of medium term consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09.

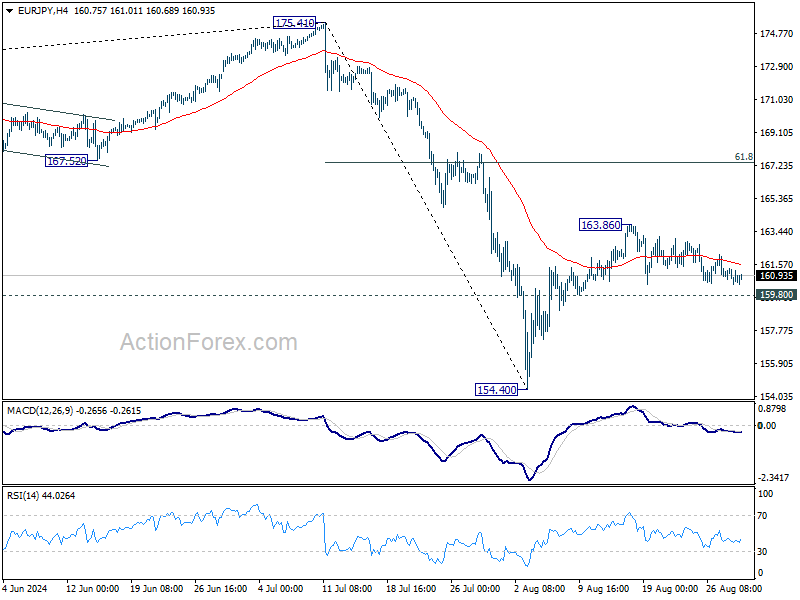

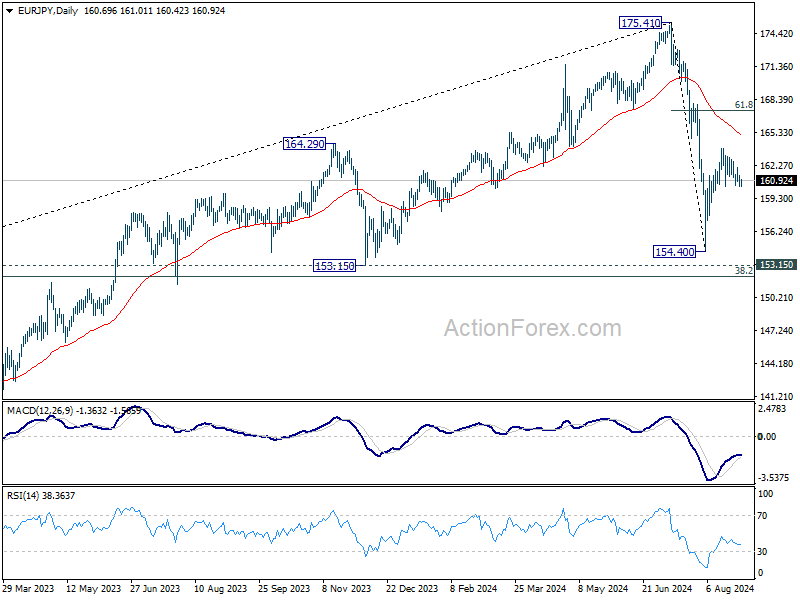

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.36; (P) 160.87; (R1) 161.29; More....

EUR/JPY is still bounded in consolidations below 163.86 and intraday bias stays neutral. On the upside, break of 163.86 will target 61.8% retracement of 175.41 to 154.40 at 167.38, as the second leg of the corrective pattern from 175.41. On the downside, however, firm break of 159.80 support will suggest that the rebound from 154.40 has completed, and turn bias back to the downside for 154.40 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Current development suggests that the first leg has completed. The range of consolidation should be seen between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high.

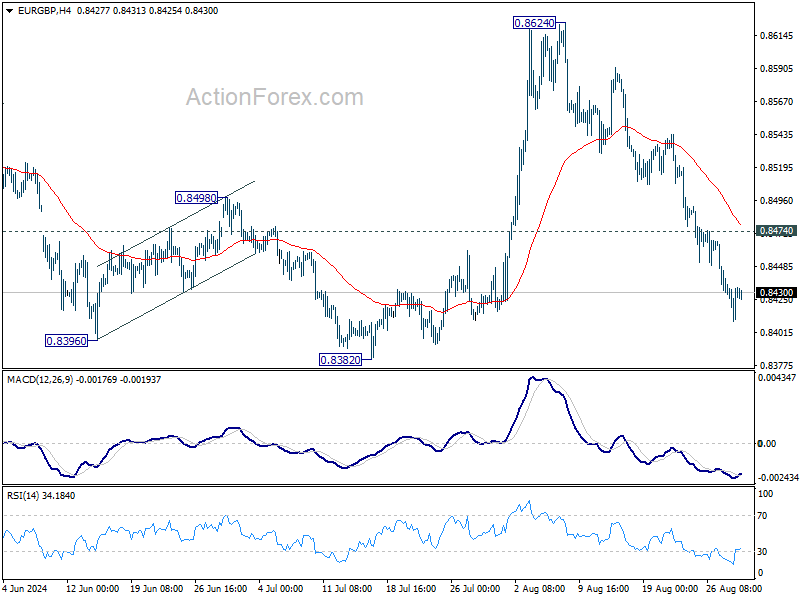

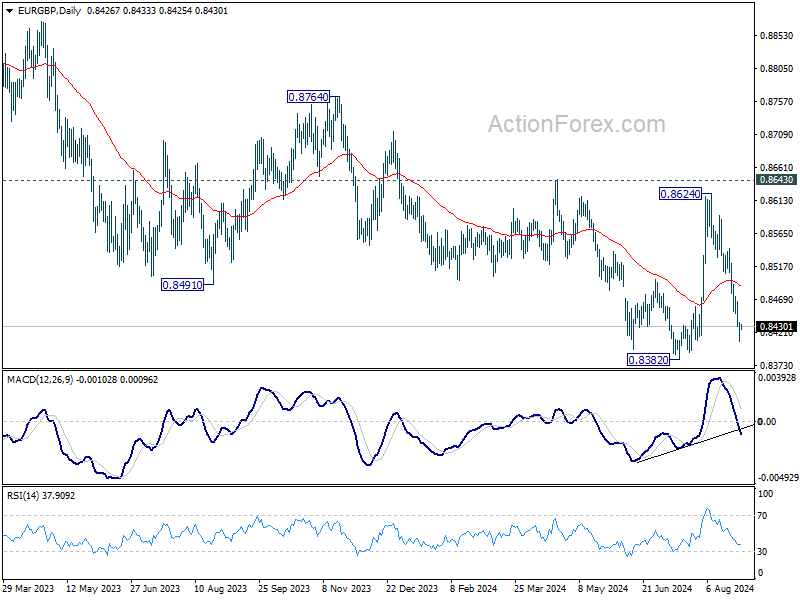

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8413; (P) 0.8427; (R1) 0.8445; More....

Intraday bias in EUR/GBP remains on the downside as fall from 0.8624 is in progress for retesting 0.8382 low. Strong support could be seen from there to bring rebound on first attempt. Above 0.8474 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 55 D EMA (now at 0.8492) holds. Firm break of 0.8382 will confirm larger down trend resumption.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage towards 0.8201 (2022 low). However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

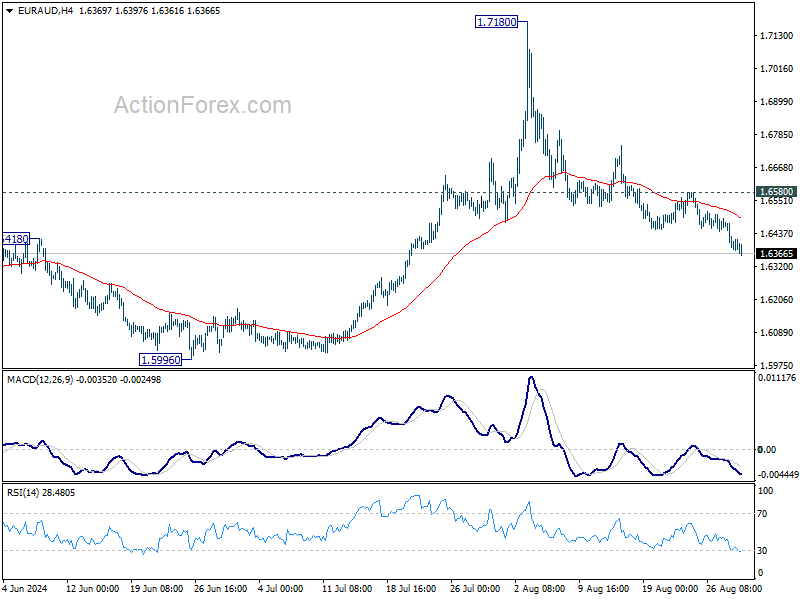

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6352; (P) 1.6417; (R1) 1.6454; More...

Intraday bias in EUR/AUD remains on the downside as fall from 1.7180 is extending. Rise from 1.5996 could have completed at 1.7180 already, and deeper fall would be seen back towards this support. On the upside, though, above 1.6580 resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

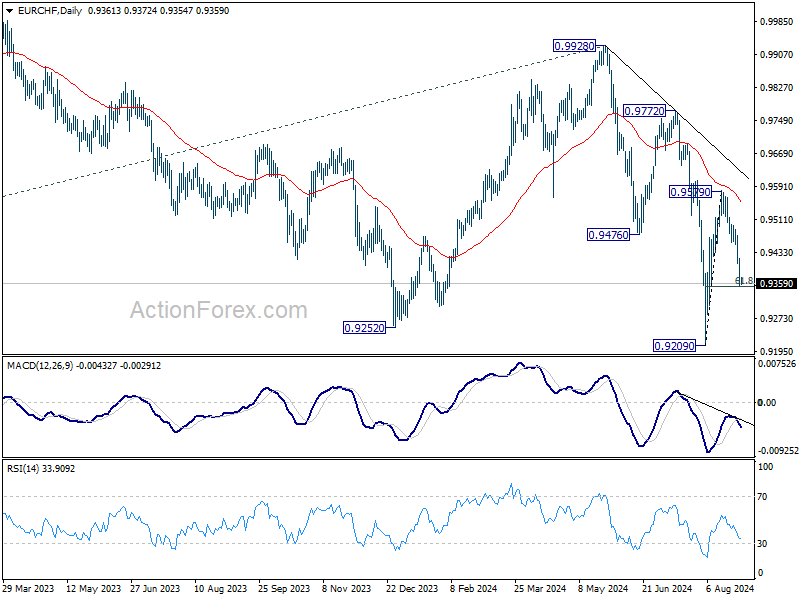

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9339; (P) 0.9379; (R1) 0.9406; More....

EUR/CHF's fall from 0.9579 is in progress and intraday bias stays on the downside. Sustained break of 61.8% retracement of 0.9209 to 0.9579 at 0.9350 will pave the way to retest 0.9209 low. On the upside, above 0.9418 minor resistance will turn intraday bias neutral first. But rise will stay on the downside as long as 0.9579 resistance holds.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Kiwi Rallies on Strong Confidence Data, Nvidia’s Underwhelming Forecast Weighs on NASDAQ

New Zealand Dollar made significant gains in Asian session today, boosted by unexpectedly strong business confidence data from New Zealand. In retrospect, RBNZ's unexpected rate cut just two weeks ago now appears to be a timely and strategic move, welcomed by Kiwi traders. By initiating the policy easing cycle earlier than anticipated, RBNZ may have provided the sluggish economy with a crucial boost, which could lead to a shorter and shallower easing cycle than initially feared. If future economic data continues to show resilience, the RBNZ might find itself needing to implement only one more rate cut this year, as originally projected, rather than the two cuts that some market analysts had been predicting.

Despite this strong showing from Kiwi, Swiss Franc remains the top performer of the week at this point, although New Zealand Dollar has overtaken Canadian Dollar for the second spot. On the other end of the spectrum, Euro continues to be the weakest performer, followed by Yen and British Pound. The Dollar and Australian Dollar are holding their positions in the middle of the currency performance chart.

Investor sentiment appears to be cooling after Nvidia's fiscal second-quarter earnings report, which, despite beating expectations, left investors underwhelmed. The fiscal Q3 forecast, in particular, did not impress, with concerns over gross margins missing market estimates and revenue projections that were just largely in line with expectations. Consequently, NASDAQ futures are trading lower in the Asian session, after the index declined by -1.12% overnight.

Technically, NASDAQ's retreat from 18171.67 is set to extend lower towards 38.2% retracement of 15708.53 to 18171.68 at 17135.59. Strong rebound from there would keep the rise from 15708.53 intact for another rally to 18671.06 high. However, firm break of 17135.59 will argue that the corrective pattern from 18671.06 has already started the third leg, and deeper fall could be seen to 61.8% retracement at 16590.63 and below. If this bearish scenario unfolds, it could provide a much-needed boost to Dollar, aiding its rebound.

In Asia, at the time of writing, Nikkei is down -0.39%. Hong Kong HSI is down -0.71%. China Shanghai SSE is down -0.43%. Singapore Strait Times is up 0.28%. Japan 10-year JGB yield is up 0.0059 at 0.901. Overnight, DOW fell -0.39%. S&P 500 fell -0.60%. NASDAQ fell -1.12%. 10-year yield rose 0.0008 to 3.841.

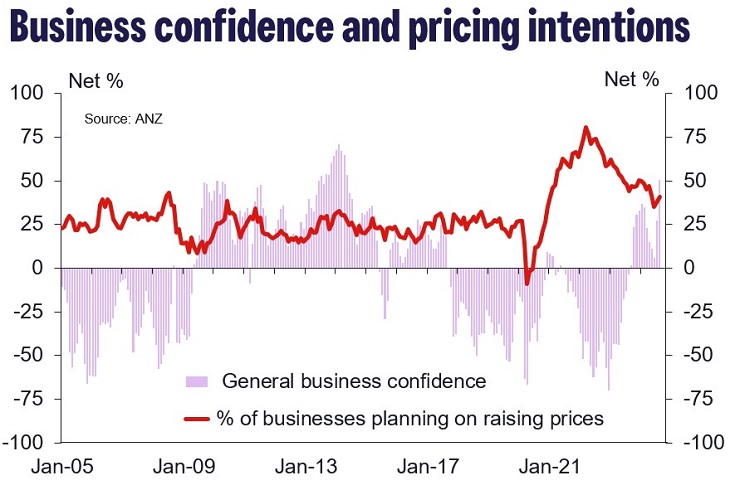

NZ ANZ business confidence hits decade high, activity outlook at 7-yr peak

New Zealand's ANZ Business Confidence surged in August, reaching 50.6, the highest level in a decade, up from 27.1 in July. This sharp increase was accompanied by a notable rise in the own activity outlook, which jumped from 16.3 to a seven-year high of 37.1.

Breaking down the data, investment intentions climbed from -1.4 to 6.9, while employment intentions improved from -3.6 to 11.9. Profit expectations also saw a positive shift, moving from -3.6 to 8.0.

Cost expectations remained elevated, ticking up slightly from 68.2 to 68.3, and pricing intentions rose from 37.6 to 41.0. On a positive note, inflation expectations fell from 3.20% to 2.92%, finally falling within the RBNZ's target band.

ANZ highlighted that the significant increases in confidence and activity expectations were already evident at the beginning of August. The responses collected after RBNZ's Official Cash Rate cut did not significantly alter the overall results.

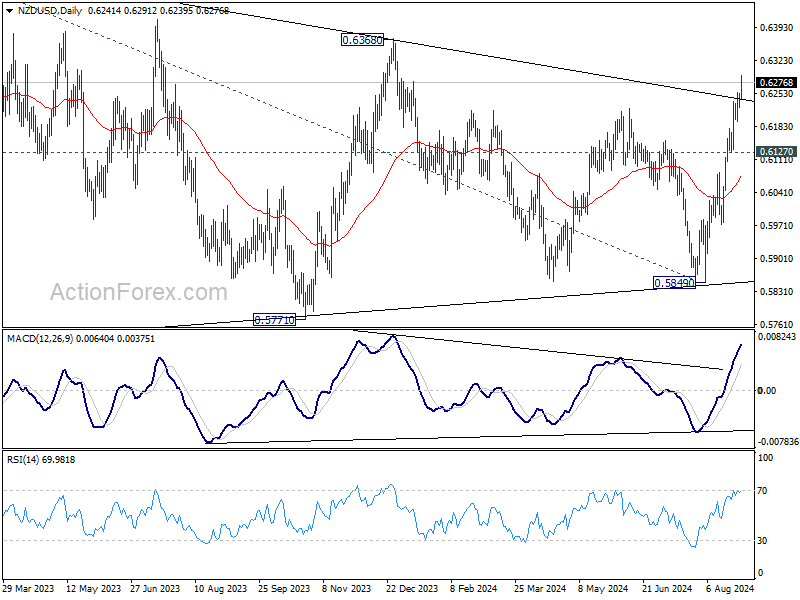

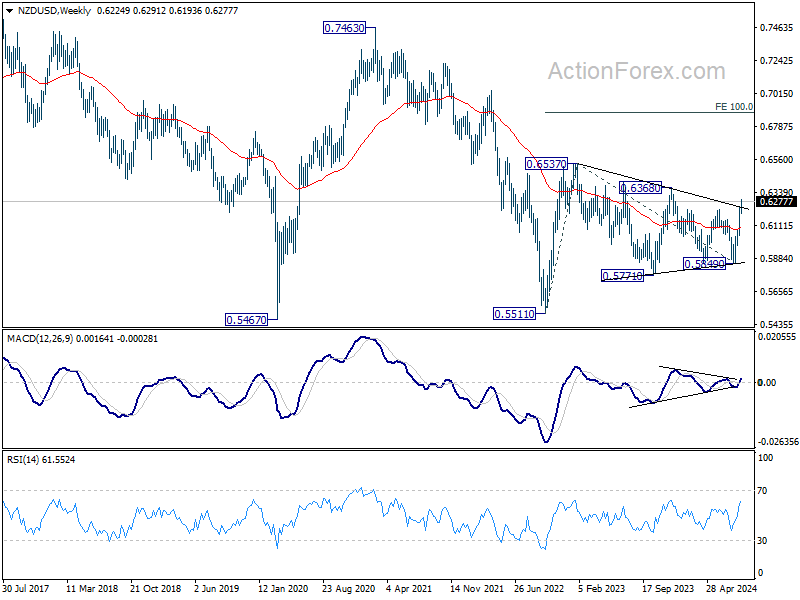

NZD/USD breaks key trend line, sets bullish path towards 0.6537 and beyond

NZD/USD surges notably today in response to strong business confidence data in New Zealand. The solid break of medium term falling trend line strengthens that case that corrective pattern from 0.6537 has completed at 0.5849. Near term outlook will now stay bullish as long as 0.6127 support holds. Next target is 0.6368 resistance.

From a medium term point of view, break of 0.6368 resistance will further solidify the bullish case that rise from 0.5511 (2022 low) is resuming. Further break of 0.6537 resistance would pave the way to 100% projection of 0.5511 to 0.6537 from 0.5849 at 0.6875.

Fed's Bostic signals readiness for rate cuts, but urges caution before September decision

Atlanta Fed President Raphael Bostic signaled that it "may be time to move" towards lowering interest rates, though he remains cautious about committing to a cut in September.

Speaking at an event overnight, Bostic emphasized the need for more data before making a definitive decision.

"I don't want us to be in a situation where we cut and then we have to raise rates again," he noted. "So, if I'm going to err on one side, it's going to be waiting longer just to make sure that we don't have that up and down."

Looking ahead

Eurozone economic sentiment and Germany CPI flash will be released in European session. Later in the day, US will publish Q2 GDP revision, jobless claims, goods trade balance and pending home sales.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9339; (P) 0.9379; (R1) 0.9406; More....

EUR/CHF's fall from 0.9579 is in progress and intraday bias stays on the downside. Sustained break of 61.8% retracement of 0.9209 to 0.9579 at 0.9350 will pave the way to retest 0.9209 low. On the upside, above 0.9418 minor resistance will turn intraday bias neutral first. But rise will stay on the downside as long as 0.9579 resistance holds.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Aug | 50.6 | 27.1 | ||

| 01:30 | AUD | Private Capital Expenditure Q2 | -2.20% | 1.10% | 1.00% | 1.90% |

| 05:00 | JPY | Consumer Confidence Index Aug | 37.1 | 36.7 | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Aug | 95.9 | 95.8 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Aug | -10.6 | -10.5 | ||

| 09:00 | EUR | Eurozone Services Sentiment Aug | 5.1 | 4.8 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Aug F | -13.4 | -13.4 | ||

| 12:00 | EUR | Germany CPI M/M Aug P | 0.00% | 0.30% | ||

| 12:00 | EUR | Germany CPI Y/Y Aug P | 2.10% | 2.30% | ||

| 12:30 | CAD | Current Account (CAD) Q2 | -6.0B | -5.4B | ||

| 12:30 | USD | Initial Jobless Claims (Aug 23) | 234K | 232K | ||

| 12:30 | USD | GDP Annualized Q2 P | 2.80% | 2.80% | ||

| 12:30 | USD | GDP Price Index Q2 P | 2.30% | 2.30% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jul P | -97.1B | -96.6B | ||

| 12:30 | USD | Wholesale Inventories Jul P | 0.20% | 0.20% | ||

| 14:00 | USD | Pending Home Sales M/M Jul | 0.20% | 4.80% | ||

| 14:30 | USD | Natural Gas Storage | 33B | 35B |

Gold Holds Steady: Will It Rise Again? US GDP Next

Key Highlights

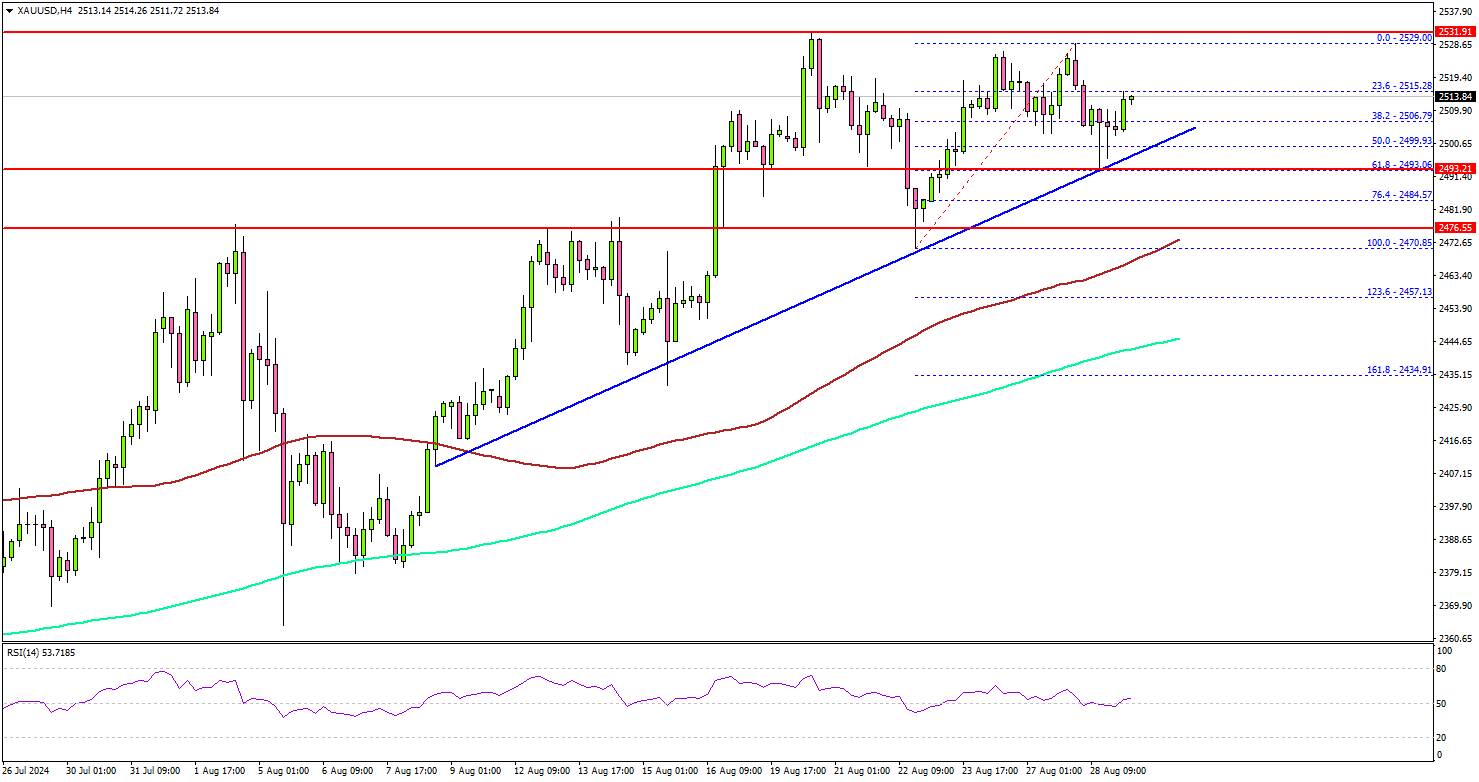

- Gold gained pace and traded above the $2,500 resistance.

- A connecting bullish trend line is forming with support at $2,495 on the 4-hour chart.

- Oil prices faced resistance near $78.40 and trimmed some gains.

- The US Gross Domestic Product could grow by 2.8% in Q2 2024 (Preliminary).

Gold Price Technical Analysis

Gold prices started a steady increase above $2,450 against the US Dollar. The price even cleared the $2,480 and $2,500 resistance levels.

The 4-hour chart of XAU/USD indicates that the price settled above the $2,485 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours). It even surpassed the $2,520 resistance zone.

Finally, the bears appeared near the $2,530 zone. The price is now consolidating above a connecting bullish trend line with support at $2,495 on the same chart.

The main support is now near $2,475. A downside break below the $2,475 support might call for more downsides. The next major support is near the $2,445 level and the 200 Simple Moving Average (green, 4 hours).

Any more losses might send gold prices toward $2,400. On the upside, immediate resistance is near the $2,515 level. The first major resistance sits near the $2,530 level.

A clear move above the $2,530 resistance could open the doors for more upsides. The next major resistance could be near $2,550, above which the price could accelerate higher toward the $2,565 level. Any more gains might send Gold toward the $2,580 resistance.

Looking at Oil, the price struggled to clear the $78.40 resistance zone and recently corrected some gains to trade below $76.00.

Economic Releases to Watch Today

- US Gross Domestic Product for Q2 2024 (Preliminary) – Forecast 2.8% versus previous 2.8%.

- US Initial Jobless Claims - Forecast 232K, versus 232K previous.

NZ First Impressions: ANZ business confidence, August 2024

Businesses sentiment rose strongly in August, as the prospect and then delivery of an OCR cut was brought forward.

Key results (August 2024)

- Business confidence: 50.6 (Prev: 27.1)

- Expectations for own trading activity: 37.1 (Prev: 16.3)

- Activity vs same month one year ago: -23.1 (Prev: -24.3)

- Inflation expectations: 2.92% (Prev: 3.20%)

- Pricing intentions: 41.0 (Prev: 37.6)

Business confidence has lifted sharply in the wake of the Reserve Bank’s turnaround on monetary policy. The ANZ survey of business opinion saw general confidence rise from 27.1 to 50.6 in August, the highest reading in a decade. Firms’ expectations for their own activity, which tends to correspond more closely with GDP growth, rose from 16.3 to 37.1, the highest since 2017.

Firms’ confidence was up across a range of measures, including hiring and investment intentions and expected profits. And to remove any doubt about the source of this newfound optimism, expectations about the availability of credit rose to their second-highest since this question was added to the survey in 2009.

Many of the survey responses will have been received before the RBNZ cut the OCR at its 14 August Monetary Policy Statement. However, the change of tone in its July policy review laid the groundwork for this move.

We wouldn’t suggest that a single OCR cut could make this degree of difference to the economic outlook. Rather, we think this shows how downbeat firms had become earlier in the year. We had noticed a distinct souring in the mood amongst businesses at the prospect that interest rate cuts might be another year or so away, as the RBNZ had been signalling in its February and May forecasts. With the economy having already been effectively flat for the last year and a half, the prospect of having to “survive until ‘25” would have been daunting for many.

While the outlook may be looking brighter, businesses are still doing it tough right now. A net 23% said that their output was down on a year ago, only slightly better than the net 24% in July. A net 15% said that their staff levels were down on a year ago, compared to a net 20% last month.

The improvement in confidence also came with a note of caution on the inflation front. Firm’s expectations of general inflation fell further from 3.2% to 2.9%, the lowest reading since July 2021. However, their own pricing intentions ticked up slightly for a second month, and their expectations for wages and other costs held steady.

The RBNZ emphasised the recent weakness of high-frequency activity indicators in its decision to cut the OCR in August. And indeed there was a marked deterioration across a range of measures for the June month. However, the updates for July and beyond have generally improved since then. We don’t think this will derail further OCR cuts in the months ahead, but the lift in business confidence along with other measures should see the market scale back the odds of larger 50bp moves.

NZD/USD breaks key trend line, sets bullish path towards 0.6537 and beyond

NZD/USD surges notably today in response to strong business confidence data in New Zealand. The solid break of medium term falling trend line strengthens that case that corrective pattern from 0.6537 has completed at 0.5849. Near term outlook will now stay bullish as long as 0.6127 support holds. Next target is 0.6368 resistance.

From a medium term point of view, break of 0.6368 resistance will further solidify the bullish case that rise from 0.5511 (2022 low) is resuming. Further break of 0.6537 resistance would pave the way to 100% projection of 0.5511 to 0.6537 from 0.5849 at 0.6875.

NZ ANZ business confidence hits decade high, activity outlook at 7-yr peak

New Zealand's ANZ Business Confidence surged in August, reaching 50.6, the highest level in a decade, up from 27.1 in July. This sharp increase was accompanied by a notable rise in the own activity outlook, which jumped from 16.3 to a seven-year high of 37.1.

Breaking down the data, investment intentions climbed from -1.4 to 6.9, while employment intentions improved from -3.6 to 11.9. Profit expectations also saw a positive shift, moving from -3.6 to 8.0.

Cost expectations remained elevated, ticking up slightly from 68.2 to 68.3, and pricing intentions rose from 37.6 to 41.0. On a positive note, inflation expectations fell from 3.20% to 2.92%, finally falling within the RBNZ's target band.

ANZ highlighted that the significant increases in confidence and activity expectations were already evident at the beginning of August. The responses collected after RBNZ's Official Cash Rate cut did not significantly alter the overall results.