Sample Category Title

ECB’s Lane signals confidence in inflation control with slower wage growth ahead

ECB Chief Economist Philip Lane noted at a conference today that while the second half of this year will still witness "plenty of wage increases," the momentum is expected to taper off significantly.

Lane emphasized that “the catch-up is peaking now,” suggesting that the pace of wage hikes will slow substantially over the next two years.

Lane highlighted the "lot of progress" made in reducing underlying price pressures, pointing out the rising optimism surrounding the anticipated deceleration in wage growth. "This is where the confidence in returning to target comes from," he added.

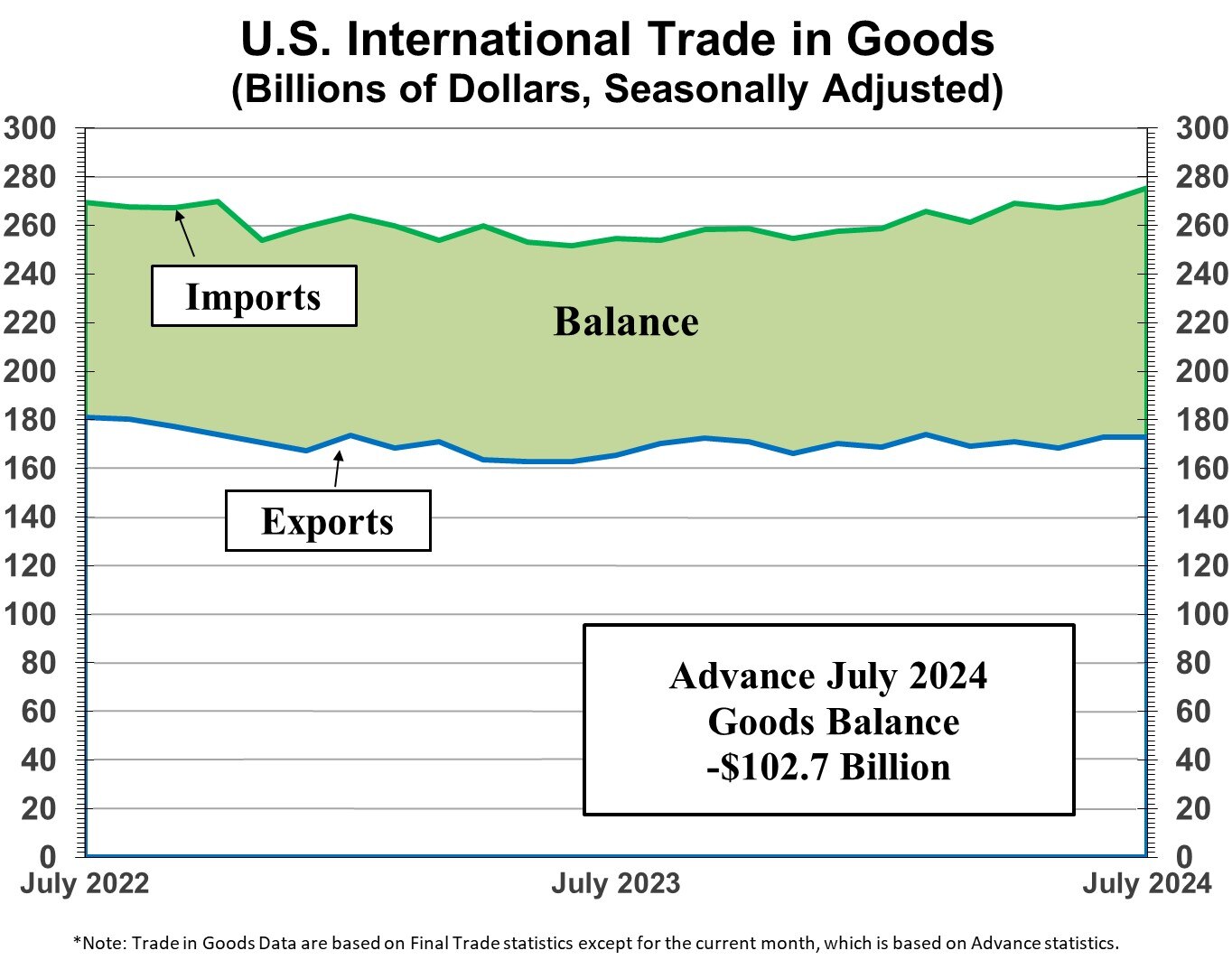

US goods trade deficit at USD -102.7B in Jul

US goods exports fell -0.0% mom to USD 172.9B in July. Goods imports fell -3.2% mom to USD 275.6B. Trade balance reported USD -102.7B deficit, larger than expectation of USD -97.1B.

Wholesale inventories rose 0.3% mom to USD 904.9B. Retail inventories rose 0.8% mom to USD 811.4B.

US initial jobless claims fall to 231k, vs exp 234k

US initial jobless claims fell -2k to 231k in the week ending August 24, slightly below expectation of 234k. Four-week moving average of initial claims fell -5k to 232k.

Continuing claims rose 13k to 1868k in the week ending August 17. Four-week moving average of continuing claims fell -250 to 1863k.

EUR/USD – ECB Keeping Close Tabs on German, Eurozone CPI

The euro has extended its decline on Thursday. In the European session, EUR/USD is trading at 1.1095 at the time of writing, down 0.22% on the day. The US dollar has rebounded against the euro this week, climbing 0.89%.

German and eurozone inflation expected to ease in August

Inflation is expected to ease in Germany and the eurozone, which could have significant impact on the European Central Bank rate announcement on Sept. 12. Inflation declined in German states and the national harmonized inflation rate is expected to fall to 2.1% y/y in August, down from 2.3% in July.

The eurozone releases CPI on Friday. The market estimate for CPI stands at 2.2%, compared to 2.6% in July. The core inflation rate is expected to creep lower to 2.8%, down from 2.9% in July. A drop in inflation in Germany and the eurozone would support the case for another rate reduction next month. The weak eurozone economy and the fact that the Federal Reserve is also poised to lower rates have strengthened the case to cut rates. At the same time, concern about wage increases is a reason for the ECB to hold off on cutting rates.

The Federal Reserve is poised to cut rates next month, which would mark the US central bank joining in the global trend of central banks lowering rates now that the threat of inflation has largely abated. Most FOMC members have come out in favor of a September cut but Atlanta Fed President Raphael Bostic said on Wednesday that the Fed should wait for additional data before lowering rates as it would be a mistake to cut and then have to hike again.

EUR/USD Technical

- EUR/USD is testing support at 1.1087. Below, there is support at 1.1055

- There is resistance at 1.1138 and 1.1170

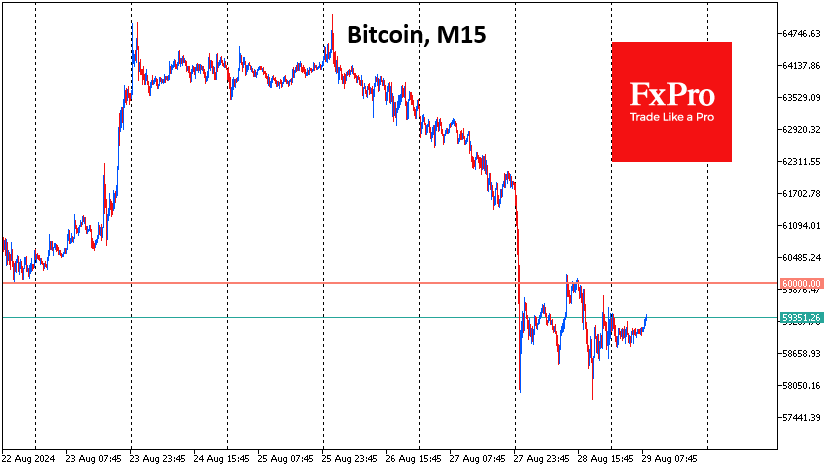

Bitcoin Price Analysis: Key Support Levels and Market Trends Amidst Major Transactions

- Bitcoin find support following profit taking induced selloff.

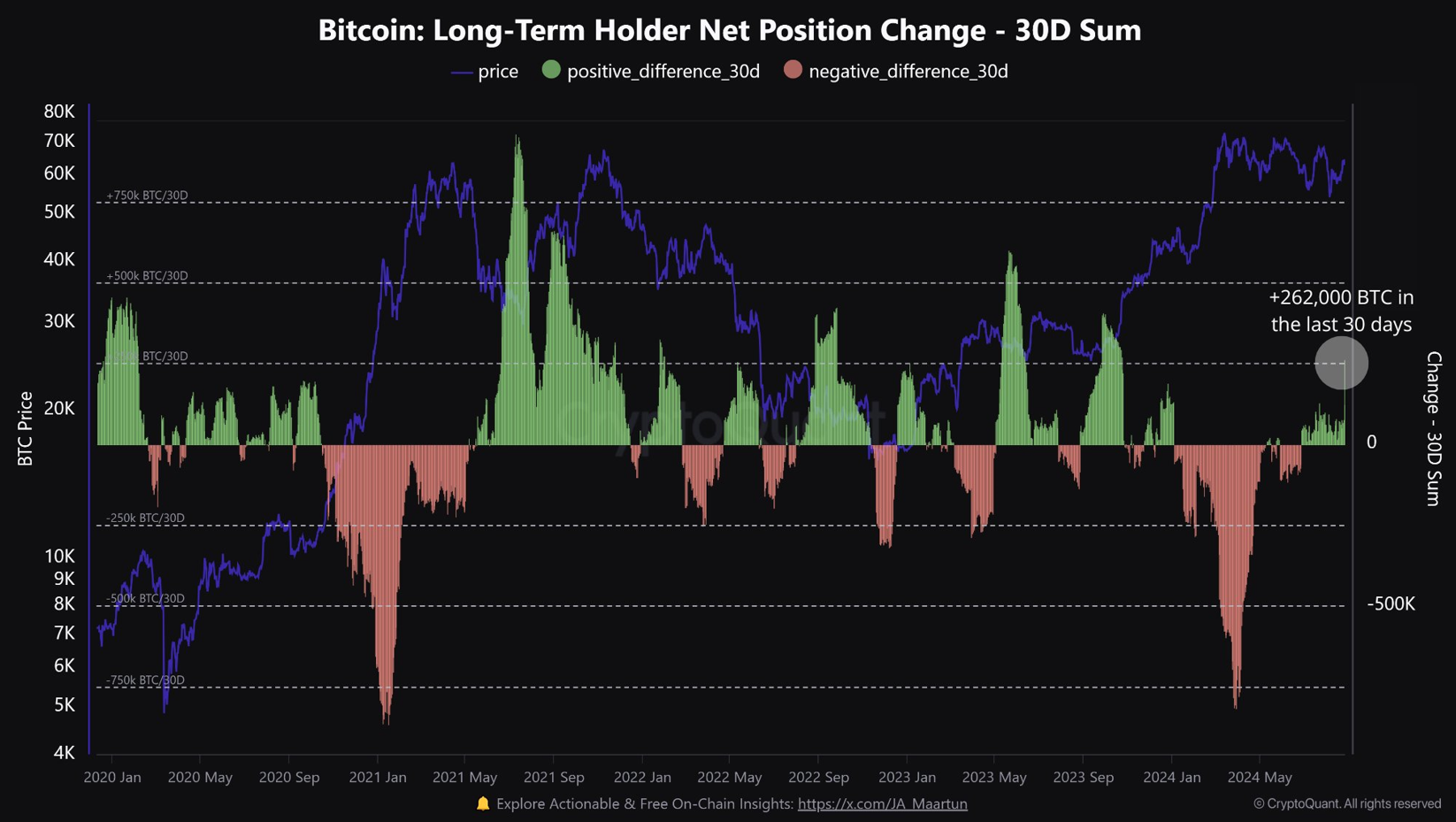

- ‘Hodlers’ continue to accumulate Bitcoin at pace, adding 262k Bitcoin over the last 30 days.

- Bitcoin’s current price stabilization above the critical 58,500 support level, a new leg to the upside?

Bitcoin prices have stabilized at a key area of support above the 58500 handle following a sharp selloff. Following a rally that took the world’s largest cryptocurrency to within a whisker of the 65000 psychological handle, the sharp selloff took many by surprise.

A massive transfer of around $1.88 billion worth of Bitcoin on Monday added further uncertainty as prices began to drop. A transfer of that size generally spooks markets as it is seen as a massive increase in supply which may be put up for sale and thus having a downward impact on Bitcoin prices.

Data from Arkham Intelligence provided some form of clarity. It shows that both the Bitcoin address that sent the initial amount and the one that received 30,000 BTC are owned by Binance. This suggests it was some form internal transfer and that should have eased the concerns of market participants.

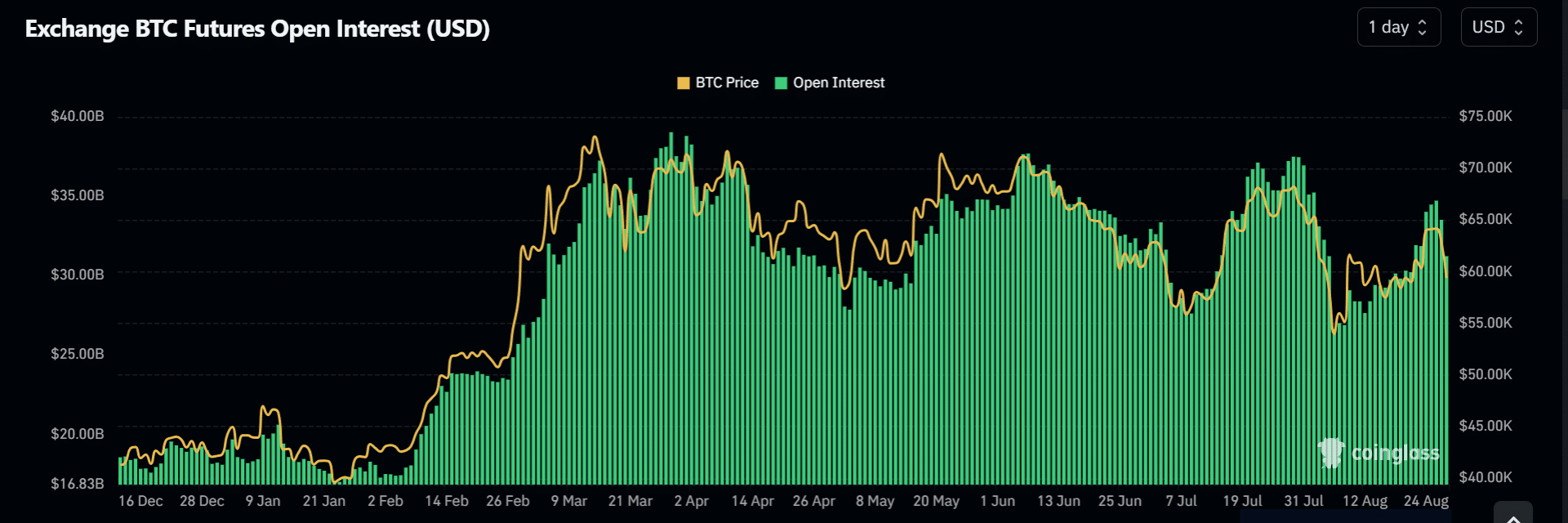

Interesting data out from AMBCrypto of late suggests that many market participants have been cashing in on short-term Bitcoin rallies. This could explain the sharp selloffs Bitcoin has been experiencing when approaching key resistance levels.

The data used by AMBCrypto is the Bitcoin Futures Open Interest chart which showed that when price reached key resistance levels of late closed positions increased, signaling potential profit taking.

Source: Coinglass (click to enlarge)

AMBCrypto also noted that there seems to be an increase in USDT outflows from exchanges just after significant rallies in the price of Bitcoin. This would suggest that market participants may be cashing out their gains from shorter-term positions.

Despite this however, long-term Bitcoin holders have ramped up their accumulation of late which is a sign that many of them are taking advantage of the dips in price.

Long-Term ‘Hodlers’ Step Up Accumulation

Recent CryptoQuant data showed that long-term Bitcoin holders continue to snap up Bitcoin at an impressive rate. Over the last 30 days, long-term Bitcoin investors have added a massive 262,000 BTC to their stash.

This increase has pushed their total holdings to an impressive 14.82 million Bitcoin, which now makes up 75% of all Bitcoin available. This surge in accumulation highlights their confidence in the cryptocurrency’s future.

Source: CryptoQuant (click to enlarge)

Technical Analysis BTC/USD

Bitcoin is sitting at a crucial support level around 58,500, which it has touched before. Today’s closing price is important because it could signal a recovery with a strong upward pattern or a drop below this key level, potentially leading to more declines.

There’s a bearish sign where the 100-day moving average has crossed below the 200-day moving average, usually indicating downward momentum. However, since this indicator reacts to past data, it’s not always a reliable predictor.

The overall trend still looks positive, but if Bitcoin closes below 58,500, it might indicate a change. If prices go up, they could face challenges at the psychological 60,000 level and then around 61,750.

On the other hand, if Bitcoin breaks below 58,500, it might test lower levels like 56,561 and possibly 55,000.

Support

- 58500

- 56561

- 55000

Resistance

- 60000

- 61750

- 62917

Bitcoin (BTC/USD) Daily Chart, August 29, 2024

Source: TradingView.com (click to enlarge)

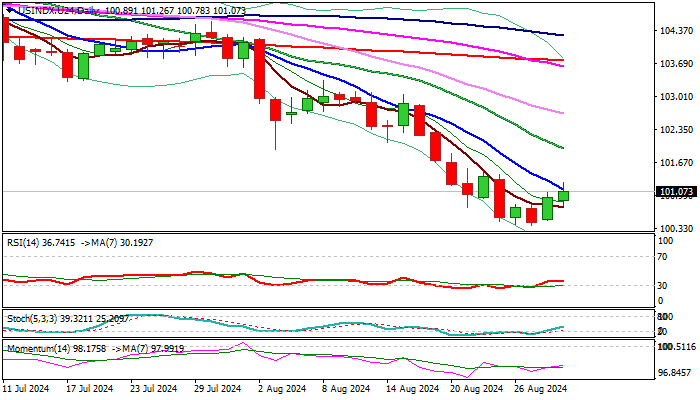

US Dollar Index Outlook: Bears Take a Breather for Limited Correction Ahead of Key US Data

The Dollar Index extends recovery into second straight day, lifted by short covering ahead of key supports at 100.29/21 zone (Dec 2023 low / 200WMA).

Oversold daily studies contributed to fresh rise, as stochastic and RSI emerged from oversold zone and bearish divergence of stochastic indicator signaled rebound in advance.

Bounce is likely to be a positioning for fresh push lower, as the dollar remains pressured by expectations for the first Fed rate cut in September, which was strongly signaled by the latest dovish comments from Fed’s Chair Powell.

Markets have fully priced in a 25 basis points cut, with rising bets for more aggressive action for 50 basis points cut, weighing on current recovery.

Key US economic data due today (Q2 GDP / Jobless claims) and on Friday (PCE price index, Fed’s preferred inflation measure) are expected to provide more information and contribute to Fed’s decisions in size and the pace of rate cuts.

The dollar index remains in a larger downtrend and is on track for the biggest monthly loss since November 2023, adding to likely scenario of limited correction, which should provide better levels to re-enter broader downtrend.

Technical picture remains bearish on daily chart (negative momentum / MA’s in bearish configuration), with cracked falling 10DMA (101.13) producing so far significant headwinds to recovery attempts and should ideally cap.

Stronger upticks, on the other hand should be limited under pivotal 101.95 barriers (falling 20DMA / former low of Aug 5) to keep larger bears intact for final attack at key supports at 100.29/00.

Res: 101.26; 101.50; 101.73; 101.95.

Sup: 100.78; 100.29; 100.00; 99.20.

Eurozone economic sentiment rises to 96.6, EU up to 96.9

Eurozone Economic Sentiment Indicator rose from 96.0 to 96.6 in August. Employment Expectations Indicator rose from 97.9 to 99.2. Economic Uncertainty Indicator fell from 17.9 to 17.2.

Eurozone industry confidence rose from -10.4 to -9.7. Services confidence rose from 5.0 to 6.3. Consumer confidence fell from -13.0 to -13.5. Retail trade confidence rose from -9.1 to -8.1. Construction confidence rose from -9.1 to -8.1.

EU Economic Sentiment Indicator rose from 96.5 to 96.9. Employment Expectations Indicator rose form 98.7 to 99.6. Economic Uncertainty Indicator fell from 17.1 to 6.6.

For the largest EU economies, the ESI improved strikingly for France (+4.3). It also improved significantly for Spain (+1.3) and the Netherlands (+0.9), while for Poland the ESI recorded only a slight increase (+0.3). The ESI deteriorated for Germany (-1.7) and Italy (-1.2).

EUR/USD Stabilises Ahead of Core PCE Inflation Report

The EUR/USD pair is holding steady at around 1.1134 as markets consolidate USD positions during a lull in significant news. Investors are now keenly awaiting the release of the Core PCE inflation data, a critical metric that the Federal Reserve uses to gauge inflationary pressures and shape its interest rate policy.

The anticipation surrounding this week's Core PCE release is particularly high due to the lack of impactful data from both the US and the eurozone earlier in the week. While significant shifts in expectations regarding the Fed's monetary policy trajectory are unlikely, the upcoming report will still be crucial for fine-tuning investor forecasts.

The market has currently primarily priced in a rate cut by the Fed at its September meeting, with the baseline expectation being a 25 basis point reduction. However, a 34.5% probability of a more aggressive cut of 50 basis points remains. This possibility is bolstered by recent comments from Fed Chair Jerome Powell indicating that the timing for a rate adjustment is appropriate now, echoing sentiments within the monetary policy community.

EUR/USD technical analysis

On the H4 chart of EUR/USD, the pair is forming a structure indicating an initial decline towards 1.1090. Following this decline, a corrective movement to 1.1150 is anticipated. Once this correction concludes, a further decline to 1.1030 is expected, potentially continuing to 1.0960. This bearish outlook is supported by the MACD indicator, with its signal line positioned above zero but trending sharply downwards.

On the H1 chart, EUR/USD has already declined to 1.1104. A corrective phase towards 1.1150 may follow, testing it from below before resuming the downward trajectory towards 1.1090. The Stochastic oscillator, currently above 80, suggests an impending drop to 20, reinforcing the likelihood of continued downward movement.

Ethereum: Rebound on the Long Road to Sunset

Market picture

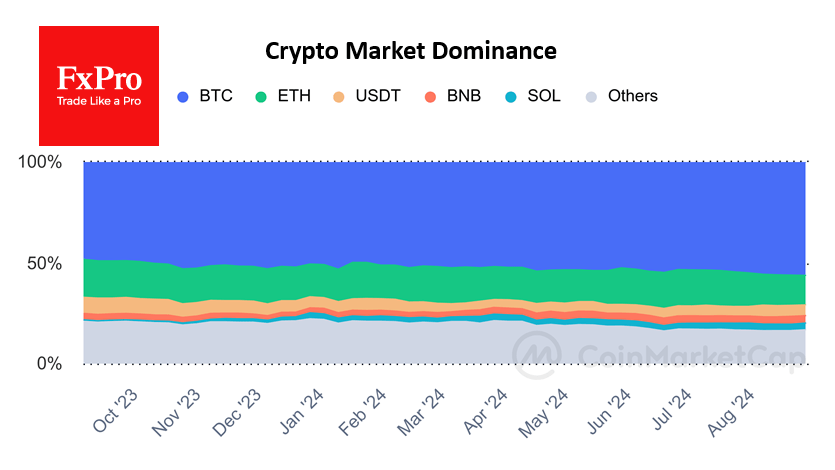

The cryptocurrency market remained in the same position as the day before, with a capitalisation of $2.09 trillion (+0.07% in 24 hours). Bitcoin’s price stabilised after the crash, with Solana losing 3% and Ethereum recovering 2% over the same period.

Bitcoin buyers beat back several waves of selling on Wednesday, preventing the price from consolidating below $58K. This dynamic increases the chances of a rebound during the day on Thursday. A rise above $60K will allow us to talk about a more significant growth than just a technical rebound.

In the absence of a meaningful cryptocurrency rally, which is often the case in a half year, bitcoin has been consolidating its dominance, reinforced by the launch of ETFs at the start of the year. However, this story doesn’t apply to Ethereum, whose crypto market share has shrunk to 14.6% from 18.8% a year earlier. The ‘other’ category lost roughly the same market share over the course of the year but has been trending upward for the past month. Ethereum is in danger of fading into the sunset, as is Litecoin, whose capitalisation is now close to the cyclical market lows of two years ago.

News background

Experts believe that the collapse of TON due to the arrest of Telegram founder Pavel Durov could have been a catalyst for the deterioration of sentiment in the crypto market. The situation may have been exacerbated by technical problems with the blockchain caused by the crash. The network overload was caused by ‘garbage’ operations with the DOGS meme token.

Glassnode warned that Bitcoin’s relative calm last week will be replaced by a period of increased volatility. Both on-chain indicators and perpetual contracts have reached equilibrium. Such signs indicate a reduction in speculation and usually precede a significant increase in volatility.

CoinGecko notes that the political coin category (PolitiFi) has significantly outperformed the entire meme coin segment in terms of capitalisation growth in 2024 – 782.4% vs. 90.2%. Most of these assets are satirical and not officially linked to any politician.

Telegram founder Pavel Durov was released on €5 million bail on Wednesday and is banned from leaving the country. Durov is charged with six offences for which he faces up to 10 years in prison. In recent days, prosecutors in Germany and India have also announced investigations into Telegram and its founder for a similar range of offences.

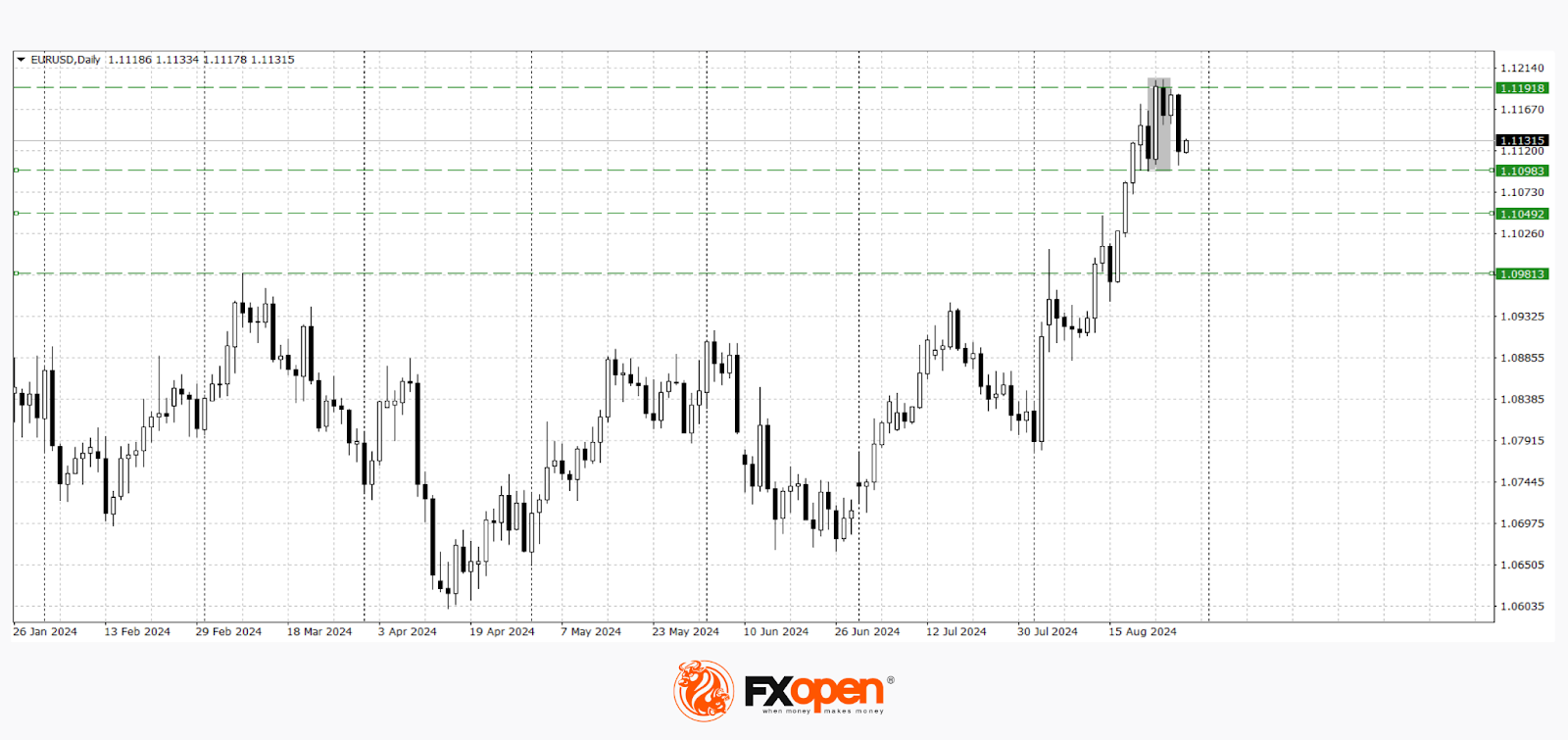

Euro Tests Key Levels Ahead of Inflation Data

EUR/USD

The euro has retreated from its previously reached highs. The 1.12000 level provided strong resistance to buyers, and after testing it twice, the price has corrected to 1.1100. This level has already offered support to the pair last week, so for now, we are seeing range-bound trading between 1.1200-1.1090.

What scenarios could unfold in the upcoming trading sessions?

- If the price breaks and holds below 1.1090, a full-fledged downward correction could develop, with a decline towards 1.1050-1.0980.

- If the price consolidates above 1.1200, the upward momentum could resume, with a rise towards 1.1400-1.1300.

Technical analysis of EUR/USD suggests the potential for a deeper downward retracement, as a “bearish harami” pattern has formed on the daily timeframe.

Key fundamental factors that could influence the pair’s price:

- Today at 10:15 (GMT +3:00): Speech by European Central Bank member Isabel Schnabel.

- Today at 12:00 (GMT +3:00): Eurozone Consumer Confidence Index release.

- Today at 15:30 (GMT +3:00): German Consumer Price Index (CPI) release.

- Today at 15:30 (GMT +3:00): US Q2 GDP data release.

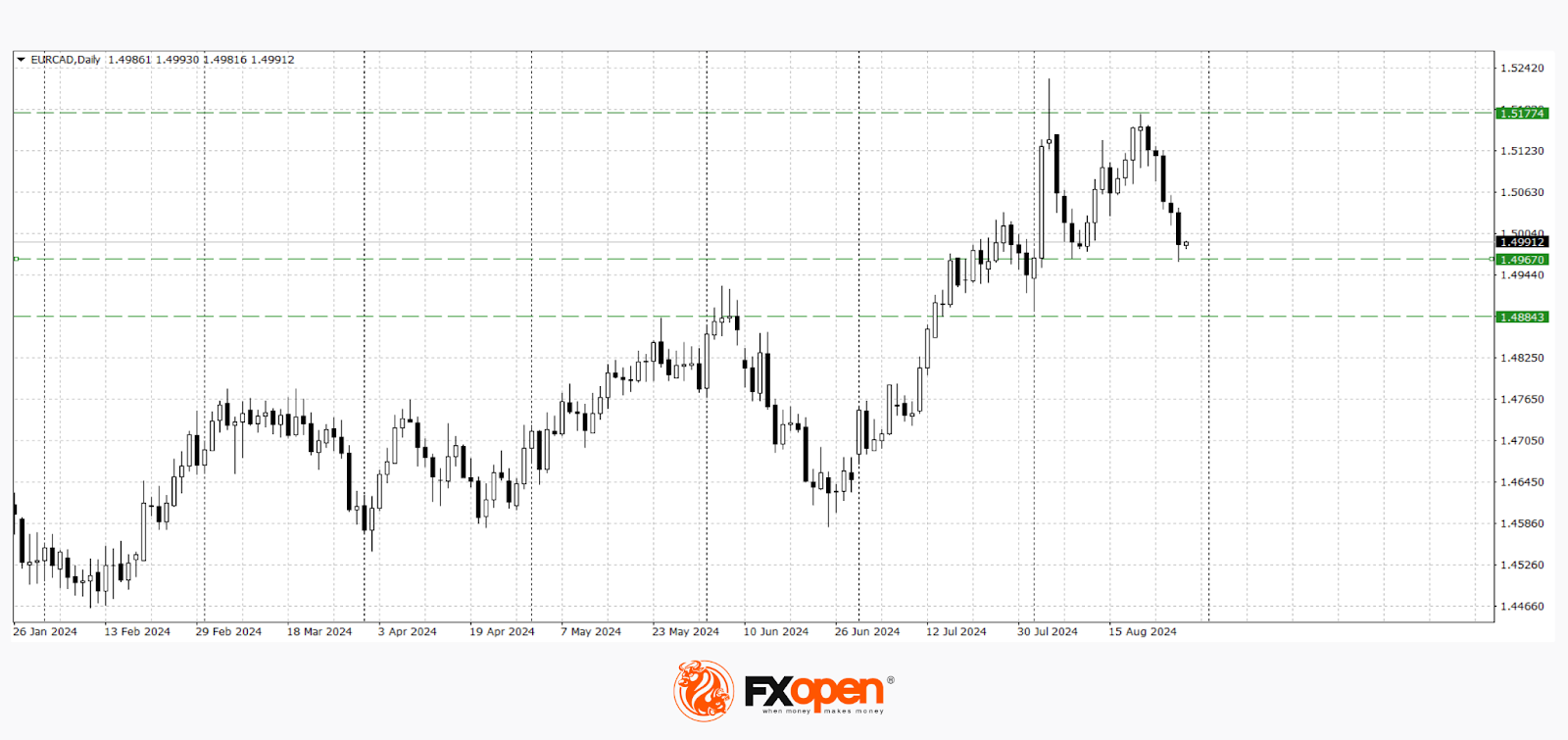

EUR/CAD

Technical analysis of the EUR/CAD pair also indicates range-bound trading, but within a wider corridor. Two weeks ago, the price surged and tested key resistance at 1.5200. It failed to consolidate above on the first attempt, and the pair dropped to 1.4970. Last week, buyers made another attempt to break through 1.5200, but again without success. Currently, the price is trading at the lower boundary of the four-week range between 1.5220-1.4970.

A move below 1.4970 could trigger a resumption of the downward movement and a test of 1.4880. Consolidation above 1.5200 could lead to a new upward impulse towards 1.5600-1.5400.

Key events for the pair tomorrow:

- Tomorrow at 10:55 (GMT +3:00): German Unemployment Rate release.

- Tomorrow at 15:30 (GMT +3:00): Canadian GDP release.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.