Sample Category Title

Fed’s Schmid needs to see a bit more data before acting on rate cut

In a Bloomberg TV interview recorded on Wednesday and aired Thursday, Kansas City Fed Bank President Jeff Schmid emphasized the importance of waiting for additional economic data before making any decisions on rate cuts.

“It makes sense for me to really look at some of the data that comes in the next few weeks,” Schmid stated.“ Before we act — at least before I act, or recommend acting — I think we need to see a little bit more.”

Schmid also downplayed concerns arising from a recent Bureau of Labor Statistics report that suggested payroll growth over the past year may have been overstated by 818k jobs.

Despite the significance of the number, Schmid remarked, “While it’s a big number, it doesn’t really change the path of the way I think of things when I think about monetary policy.”

ECB minutes highlight September as ideal time for policy re-evaluation

ECB's July meeting accounts revealed that the upcoming September meeting is "widely seen as a good time to re-evaluate the level of monetary policy restriction," with members emphasizing the importance of approaching that meeting with an "open mind."

The data-dependent approach was reiterated, but with a clear message that this does not mean overemphasizing specific, single data points. Instead, the policy decisions should be guided by established elements of the reaction function.

As inflation is coming down "only gradually," the Governing Council opted for a cautious stance during the July meeting, supporting a pause in rate cuts. This cautious approach was deemed necessary due to the "prevailing uncertainties" surrounding key economic factors such as wages, profits, productivity, and services inflation. These elements require further monitoring and assessment as new data becomes available to gain greater confidence in the inflation outlook.

By the September meeting, ECB will have access to extensive new data, including July and August inflation figures, second-quarter national account information covering compensation per employee, profits, and productivity, as well as updated monetary data and a new set of staff projections.

(ECB) Monetary policy accounts

Account of the monetary policy meeting of the Governing Council of the European Central Bank held in Frankfurt am Main on Wednesday and Thursday, 17-18 July 2024

22 August 2024

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Ms Schnabel noted that since the Governing Council’s previous monetary policy meeting on 5-6 June 2024, financial markets had moved in response to political news, which had caused some volatility, and in response to weaker than expected US inflation data. The announcement of snap elections in France had dented investors’ risk appetite and the rally in euro area risk asset markets. However, the resulting rise in volatility in some market segments had remained contained and short-lived, without signs of systemic stress or fragmentation. Risk premia had risen only modestly, and the euro exchange rate had recovered quickly. Macroeconomic news had been muted, with small negative macroeconomic surprises in both the euro area and the United States. Expectations regarding ECB policy rates had remained broadly unchanged amid some volatility following the elections for the European Parliament, but had edged lower after the release of US consumer price index (CPI) data. Euro area financial conditions had also remained broadly unchanged, with continued benign market conditions. The absorption of the net issuance of government bonds had continued to proceed smoothly as investor demand remained strong.

Political uncertainty had affected financial markets, as reflected in a spike in implied volatility in the euro area stock market. However, implied volatility had remained contained from a longer-term perspective and had retreated swiftly to previous lows. By contrast, option-implied volatility in euro area bond markets had hardly moved and stood close to the lowest level seen since 2021. Moreover, investor risk appetite in the euro area had recovered quickly after a temporary slump and currently stood well above the levels seen at the start of the year, pointing to continued strong investor risk sentiment.

The resilience of financial markets and a high degree of investor differentiation had also been visible in sovereign bond markets. The increase in sovereign spreads over the German Bund had been small from a historical perspective. Spreads had narrowed again after the initial spike in volatility and currently stood below the levels prevailing before the European parliamentary elections, with the exception of French sovereign bond spreads, which stood slightly higher.

Investor differentiation had also extended to euro area equity markets and corporate bond markets. Overall, however, the impact on euro area stock market valuations had been muted and short-lived. Developments in euro area corporate bond markets had mirrored those in equity markets, with spreads of investment-grade financial corporate bonds and non-financial corporate bonds in the euro area, excluding France, having narrowed overall. The EUR/USD exchange rate had initially depreciated somewhat, but had quickly recovered its losses, and was broadly unchanged from the levels prevailing at the time of the Governing Council’s previous monetary policy meeting.

As regards expectations about US monetary policy, following the June meeting of the Federal Open Market Committee the probability of a cut in US interest rates in September had initially declined slightly. However, this had been counterbalanced subsequently by the somewhat weaker than expected US macroeconomic data and, in particular, the June release of US CPI data, which had pushed the US fed funds futures curve substantially lower than it had been at the time of the June Governing Council meeting.

US developments had also spilled over to some extent to expectations regarding ECB interest rates. Rate expectations had remained broadly unaffected by the political uncertainty after the European elections, but had edged lower in July after the weaker than expected US CPI data release. However, the current market pricing of the expected policy rate path remained relatively close to the peak forward curve in late May and substantially above the trough in rate expectations reached at the start of the year. Moreover, as regards the speed and extent of the rate-cutting cycle, participants in the Survey of Monetary Analysts (SMA) had not changed their views since the previous survey round and, on average, continued to expect 25 basis point rate cuts at every quarterly meeting at which new staff projections were available until December 2025. This was broadly in line with expectations in financial markets and with other surveys, with some differences regarding the expected level of the terminal rate.

The more moderate downward shift of the euro area forward curve relative to the United States could partly reflect the fact that euro area core inflation – as measured by the Harmonised Index of Consumer Prices (HICP) excluding energy and food – had continued to surprise to the upside, in contrast to the latest US inflation data release. Euro area near-term “inflation fixings” (swap contracts linked to specific monthly releases in euro area year-on-year HICP inflation excluding tobacco) had edged up since the Governing Council’s previous monetary policy meeting, but they remained below the level foreseen in the June 2024 Eurosystem staff macroeconomic projections. Moreover, according to market participants, risks to the longer-term inflation outlook remained tilted to the upside, as evidenced by option-implied probabilities for five-year forward inflation-linked swap rates five years ahead. Under the assumption of risk neutrality – meaning that investors assessed an overshooting of the inflation target to be as costly as an undershooting – investors were pricing in a substantially higher probability of inflation overshooting a level of 2.5% than of it undershooting a level of 1.5%. This could reflect the anticipation of more frequent adverse supply shocks, as signalled by positive inflation risk premia.

At the same time, developments in euro area real interest rates had been mixed recently. While ten-year real rates had remained broadly unchanged amid high volatility, two-year and five-year real rates had dropped since the Governing Council’s previous monetary policy meeting.

The absorption of government securities had continued to proceed smoothly, including for France. Recent auctions had continued to see strong investor demand, with auction results being in line with past regularities. Over the past year net issuance had found strong demand among foreign investors, with foreign hedge funds emerging as important players in European sovereign bond markets.

The global environment and economic and monetary developments in the euro area

Starting with inflation in the euro area, Mr Lane noted that headline HICP inflation had declined slightly to 2.5% in June, after rising to 2.6% in May. Energy inflation had edged down to 0.2%, from 0.3% in May, despite upward base effects; food inflation had fallen to 2.4% from 2.6% in May. Goods price inflation and services price inflation had been 0.7% and 4.1% respectively in both May and June.

While some measures of underlying inflation had ticked up in May, owing to one-off factors, most measures of underlying inflation had either been stable or edged down in June compared with May. On average over the second quarter of 2024, all measures of underlying inflation had declined compared with the previous quarter.

In relation to current wage developments, compensation per employee had increased to 5.0% in the first quarter of 2024, in line with the June staff projections. Negotiated wages remained an important driver of total compensation. After decreasing slightly in the fourth quarter of 2023 to 4.5%, negotiated wage growth including one-off payments had increased to 4.7% in the first quarter of 2024. The forward-looking wage trackers had continued to signal elevated wage pressures this year, largely driven by catch-up dynamics. Wage agreements in the euro area’s largest economy accounted for the bulk of the latest tracker information, as agreements had been reached in the wholesale, retail, chemical and construction sectors, which tended to have long contract durations and therefore a more pronounced catch-up component during this phase. The Indeed tracker, which reflected wages for new hires, had picked up to 3.7% in June, from 3.5% in May.

However, beyond the near term the responses from firms participating in the ECB’s Corporate Telephone Survey (CTS) and the Survey on the Access to Finance of Enterprises (SAFE) had pointed to materially lower wage growth in 2025. This picture was also reflected in the year-by-year profile of recently agreed multi-year wage contracts. The participants in the ECB’s Survey of Professional Forecasters (SPF) also expected a marked deceleration in wage growth in 2025. According to the SPF, the expected deceleration in wage growth next year was attributable to the catch-up to past inflation playing a much smaller role and to the decline in expected inflation.

For domestic price pressures to moderate in the period ahead, profits also needed to play their part. In the first quarter the annual growth rate of the GDP deflator had declined more than expected, falling to 3.6%, from 5.1% in the fourth quarter of 2023. The largest contribution to this decline had come from unit profits, with the contribution of the annual growth rate of unit profits turning negative in the first quarter of 2024.

Headline inflation was expected to fluctuate around current levels for the remainder of 2024. It should then resume its downward path and decline to the ECB’s target of 2% in the second half of 2025 owing to the fading impact of the past inflation surge, weaker growth in labour costs and the unfolding effects of restrictive monetary policy. Medium and longer-term inflation expectations had remained broadly stable, with most standing at around 2%.

Turning to the global economy, growth momentum was increasing, with the global composite Purchasing Managers’ Index (PMI) excluding the euro area rising to 53.2 in the second quarter, from 52.6 in the first quarter, and other survey-based indicators also signalling a further improvement in global activity. Global trade continued to strengthen, driven by a frontloading of demand, as firms rebuilt inventories after a long phase of destocking. This was also confirmed by the July 2024 update of the IMF World Economic Outlook (WEO), which projected global real GDP growth to be 3.2% in 2024 and 3.3% in 2025, and global trade growth to be 3.1% in 2024 and 3.4% in 2025. Compared with the April WEO, there was basically no change in the outlook for global growth and trade.

The euro exchange rate had remained broadly stable, both against the US dollar and in nominal effective terms, since the last Governing Council meeting, while oil prices had increased by 15% to USD 88 per barrel of Brent crude oil. The increase in the oil price since the last meeting reflected tighter supply conditions and rising geopolitical concerns. European natural gas prices had decreased by 7% since the last Governing Council meeting, to stand at around €31 per megawatt-hour, as demand remained subdued and gas storage levels were high.

The incoming information indicated that the euro area economy had continued to expand in the second quarter of 2024. The services sector continued to lead the recovery, although the services component of the PMI had softened somewhat in June. Construction output, which had been boosted by favourable weather in Germany and fiscal incentives in Italy in the first quarter, had fallen in April. Non-construction investment had risen moderately in the first quarter but was likely to remain muted for the rest of the year. Manufacturing activity had shown renewed signs of weakness, with the PMI indicators for output and new orders dropping further into contractionary territory, at 46.1 and 44.4 respectively in June. Goods exports had been weak.

The overall narrative remained that of a consumption-led recovery with rising real incomes translating into rising consumption. The latest data for the first quarter supported the view that consumption was growing overall. Consumer confidence had slowly increased in the second quarter, but remained subdued compared with its pre-pandemic average level.

Employment had expanded by 0.3% in the first quarter, in line with economic activity and supported by a further expansion of 0.3% in the labour force. The unemployment rate had remained unchanged at 6.4% in May. Survey indicators suggested that positive, but moderating, employment growth would continue. The PMI for employment had averaged 51.7 in the second quarter, suggesting employment growth of around 0.2%, compared with 0.1% in the June staff projections. At the same time, labour demand seemed to be gradually moderating. The ECB’s labour hoarding indicator – which measured the share of firms holding on to workers despite a deteriorating outlook – had declined further in the second quarter, and the Indeed job postings had declined by 1.8% from May to June, following the deceleration in the job vacancy rate in the first quarter of the year.

Turning to fiscal policies, the level of fiscal support in the euro area remained sizeable and was likely to be somewhat stronger than assumed in the June Eurosystem staff projections. While concrete fiscal news since the June projections had been relatively limited, the uncertainty surrounding the fiscal outlook had increased.

The policy rate cut in June had been transmitted smoothly to money market interest rates, while broader financial conditions had been somewhat volatile. Financing conditions for firms and households remained at restrictive levels, as the effects of past policy rate increases continued to work their way through the transmission chain. The average interest rate on new business loans had declined slightly to 5.1% in May, while interest rates on new mortgage loans had remained constant at 3.8% for the third consecutive month. Growth in loans to firms and households had remained broadly stable at very subdued rates over the past several months. The annual growth in broad money – as measured by M3 – had continued to recover, reaching 1.6% in May, driven by strong net foreign inflows.

Taken together, the information from the euro area bank lending survey (BLS) and the SAFE suggested that credit supply conditions for loans to firms were stabilising but still tight, with demand persistently weak. While respondents to the July BLS had reported a slight tightening in credit standards for loans to firms, participants in the SAFE had seen a small net improvement in bank loan availability. According to both surveys, demand for corporate loans had declined further in the second quarter of 2024. On the household side, the BLS had signalled an easing in standards for mortgages but a moderate tightening for consumer credit. Net demand for housing loans and consumer credit had increased for the first time since mid-2022.

Monetary policy considerations and policy options

In the aggregate, Mr Lane concluded that the incoming information broadly supported the previous assessment of the medium-term inflation outlook. The overall quarterly profile of measures of underlying inflation remained in line with the picture of gradually diminishing price pressures. The weakening in the economic data also helped to contain upside inflation risks. The elevated wage growth was in line with expectations, and firms had seen their profits decline, buffering the inflationary impact of higher labour costs. Monetary policy was keeping financing conditions restrictive. At the same time, domestic price pressures were still high, services inflation was elevated and headline inflation was likely to remain above the target well into next year.

Against this background, Mr Lane proposed keeping the three key ECB policy rates unchanged. The information available at the Governing Council’s next monetary policy meeting in September would incorporate a wealth of fresh data and the new staff macroeconomic projections for the euro area. Data for the second quarter would also be available – including GDP growth, compensation per employee, profit margins and productivity – alongside two more HICP releases, as well as monetary indicators and more timely soft indicators for activity and consumer confidence.

2. Governing Council’s discussion and monetary policy decisions

Economic, monetary and financial analyses

Looking at the external environment, members took note of the outlook for global growth presented by Mr Lane. The July 2024 update of the IMF’s April WEO entailed broadly unchanged expectations for real GDP growth in 2024 and 2025, which were somewhat above those embedded in the June Eurosystem staff projections. This was positive news, as solid growth in global activity and trade was an important element in the anticipated euro area recovery. At the same time, attention was drawn to the latest, softer data on economic activity for both the United States and China. It was argued that the external environment had recently become more clearly disinflationary, mitigating concerns over “higher for longer” inflation. Of late, inflation had declined in the United States, and the issue of a possible divergence of US and euro area monetary policy – much discussed in the spring – was abating.

With regard to the euro area economy, members widely noted that the medium-term outlook discussed during the previous Governing Council meeting and entailed in the June 2024 Eurosystem staff projections had not changed overall. The most recent data revealed that inflation was more persistent than previously anticipated, while activity indicators had disappointed on the downside. It was argued that the short-term outlook had thus become somewhat more “stagflationary”. At the same time, it was contended that weaker activity was likely to dampen inflation over time.

On economic activity, members concurred with Mr Lane that the incoming information indicated that the euro area economy had grown in the second quarter, but likely at a slower pace than in the first quarter. Services continued to lead the recovery, while industrial production and goods exports had been weak. Indicators pointed to muted investment growth in 2024, amid heightened uncertainty. The recovery was expected to be supported by consumption, driven by stronger real incomes resulting from lower inflation and higher nominal wages. Moreover, exports should pick up with a rise in global demand. Finally, monetary policy should exert less of a drag on demand over time.

In their discussion, members acknowledged that the short-term outlook for growth had deteriorated. This was visible in both soft and hard data, most notably in weak PMI indicators for manufacturing. The prospect of somewhat lower short-term growth than embedded in the staff projections was also corroborated by the latest surveys, such as the SPF and the SMA. Concerns were expressed that muted activity might not only be of a temporary or cyclical nature. This inference was supported notably by the fact that there were few signs of a recovery in manufacturing and industrial production, even though the adverse impact of earlier energy and terms-of-trade shocks had largely faded. Reference was made to the share of energy costs in GDP, which had fallen back to close to its longer-term average. It was doubtful that short-term cyclical phenomena could fully explain the weak performance of manufacturing. Rather, this was consistent with the observed subdued developments in exports and might well reflect a more lasting or structural loss of competitiveness, casting doubt on the capacity of the euro area to recover on the back of growth in world trade.

It was stressed that the economy remained lopsided, as the recovery continued to be driven, in essence, by activity in services. This was confirmed by positive incoming information on the services PMI and services production. Tourism had been playing an important role in recent services activity, but it was questionable whether this type of spending could support the economy sustainably in the second half of the year. It was also observed that the moderate recovery in consumer confidence was still from low levels and that the saving ratio was increasing. The point was made that the increase in the saving ratio reflected, to a large extent, increases in the non-labour income of high-income households that were likely to save rather than consume out of additional income. Moreover, greater saving was seen as a natural reaction to the higher interest rates on deposits offered in the context of past monetary policy tightening. However, the strong increase in savings observed in the first quarter of the year was raising questions about the consumption-based narrative embedded in the projections. Overall, despite all these layers of uncertainty, it was felt that the euro area economy remained on track for a consumption-led recovery, in line with rising real income growth. Survey results entailed some positive signs for future household spending and, according to the latest BLS, households’ demand for loans had risen.

Turning to the labour market, incoming data confirmed continued resilience. The unemployment rate was unchanged at 6.4% in May, its lowest level since the start of the euro. Employment had grown by 0.3% in the first quarter, supported by a further increase in the labour force, which had expanded at the same rate. More jobs were likely to have been created in the second quarter, mainly in the services sector. At the same time, firms were gradually reducing their job postings, albeit from high levels.

Members widely pointed to continued tightness in the labour market. It was noted that this tightness had persisted despite immigration and rising labour force participation. Participants in the ECB’s CTS continued to report difficulties in recruiting, which highlighted continued labour shortages. At the same time, the CTS findings suggested that firms were responding to these shortages by investing in labour-saving technology such as automation and digitalisation. It was noted that employment growth continued to be driven mainly by the services sector. However, a note of caution was expressed that the observed state of the labour market had two interpretations. On the one hand, its persistent resilience was reinforcing the prediction that a soft landing of the economy was indeed achievable. On the other, the lack of sustained growth dynamics raised concerns about the durability of what appeared to be the most inclusive and vibrant labour market in the history of the euro area.

With respect to national fiscal and structural policies, members reiterated that these policies should aim to make the economy more productive and competitive, which would help raise potential growth and reduce price pressures in the medium term. An effective, speedy and full implementation of the Next Generation EU (NGEU) programme, progress towards capital markets union and the completion of banking union, and a strengthening of the Single Market were key factors that would help foster innovation and increase investment in the green and digital transitions. The European Commission’s recent guidance calling for EU Member States to strengthen fiscal sustainability and the Eurogroup’s statement on the fiscal stance for the euro area in 2025 were welcome. Implementing the EU’s revised economic governance framework fully and without delay would help governments bring down budget deficits and debt ratios on a sustained basis.

The course of fiscal policy was seen as posing challenges in the coming months. Concerns were expressed that, in a period of political uncertainty and changing governments, there might be less fiscal consolidation than expected thus far. A combination of fiscal slippage in some countries and fiscal discipline in others was leading to a divergence in fiscal positions and greater vulnerability. In September euro area countries would have to present their multi-year budgetary plans. Markets would then start analysing how compliant these plans were with the fiscal rules, the credibility of which depended on early and serious compliance efforts. Promotion of a sound fiscal regime called for being vocal about the need for structural reforms as well, since weak economic growth implied a higher risk of slippages in complying with the fiscal rules. In this context, it was also suggested that in the implementation of the NGEU programme the emphasis should be more on effectiveness than on speediness, given the risk of inefficiencies associated with limited administrative capacity on the part of the implementation authorities.

Members assessed that the risks to economic growth were tilted to the downside. A weaker world economy or an escalation in trade tensions between major economies would weigh on euro area growth. Russia’s unjustified war against Ukraine and the tragic conflict in the Middle East were major sources of geopolitical risk. This might result in firms and households becoming less confident about the future and global trade being disrupted. Growth could also be lower if the effects of monetary policy turned out stronger than expected. Growth could be higher if inflation came down more quickly than expected and rising confidence and real incomes meant that spending increased by more than anticipated, or if the world economy grew more strongly than expected. The point was made that the continuous presence of macro risks, such as geopolitical fragmentation and a lack of fiscal discipline, might fuel uncertainty and hamper planning, although it appeared that, thus far, the economy had shown resilience to this type of uncertainty.

With regard to price developments, members concurred with the assessment provided by Mr Lane that the incoming information broadly confirmed the medium-term inflation outlook. Annual inflation had eased slightly to 2.5% in June, with both goods price inflation and services price inflation unchanged, at 0.7% and 4.1% respectively. While some measures of underlying inflation had ticked up in May owing to one-off factors, most measures had either been stable or edged down in June. Inflation was expected to fluctuate around current levels for the rest of the year, partly owing to energy-related base effects. It was then expected to decline towards target over the second half of next year, owing to weaker growth in labour costs, the effects of restrictive monetary policy and the fading impact of the past inflation surge.

Members considered that the short-term inflation outlook had remained broadly in line with the June projections, although pointing to somewhat higher profiles for services inflation and core inflation, partly associated with increases in tourism-related prices. It was also emphasised that the disinflationary process in headline HICP inflation over the shorter-term horizon was more evident when adjusting for the impact of energy-related base effects that were causing some volatility in the latter part of this year. It was noted that surveys and markets were somewhat more optimistic about inflation over the short term than the June projections, while they were somewhat more pessimistic about economic growth.

The persistence in services inflation remained the central element shaping the inflation outlook. A remark was made that the risk of seeing high services inflation for a longer period had not been mitigated by the tepid recovery. This was not just an issue for the euro area but seemed to hold true more broadly. For the euro area, in June services inflation had been higher than expected and a string of consecutive upward surprises had been observed. Services inflation had dropped fairly quickly from its peak in mid-2023 to 4% in November 2023, but since then it had hovered around that level. In contrast to goods price inflation, where the decline had proceeded very quickly, progress in reducing services inflation appeared to have stalled. At current levels, services inflation was almost twice as high as its average before the global financial crisis. Moreover, the persistence of services inflation was broad-based across euro area countries and components rather than being driven by individual categories, and momentum remained high despite its recent decline. As disinflation in non-energy industrial goods was flattening out and high freight costs and rising protectionism might put upward pressure on goods price inflation in the future, a further decline in core inflation would need to rely on disinflation in services.

At the same time, the point was made that services inflation was a sluggish and lagging element in the inflation process. For some items, in particular, the latest observations may have reflected “laggards” – delayed backward-looking repricing in some specific subsectors – rather than a generalised forward-looking price resetting.

Members agreed that the triangular relationship between wages, productivity and profits remained central to assessing domestic price pressures and the inflation outlook more generally. It was argued that the expected disinflationary trend was based on dynamics in these three variables, which were quite aligned with historical patterns. However, it was cautioned that the evolution of these variables remained surrounded by a high level of uncertainty. Developments thus warranted close monitoring and the data for the second quarter would be important inputs for the Governing Council’s next monetary policy meeting in September.

Concerning wages specifically, in the first quarter of this year all available measures had pointed to continued elevated growth, but this had been largely anticipated in the June projections. While the latest data showed that wages in the euro area were still rising at an elevated pace, it was maintained that the most recent aggregate developments to a large extent reflected developments in specific sectors and countries rather than a broad-based trend. The profile for wage growth embedded in the latest projections was downward-sloping for 2025 and 2026, and this expectation was supported by results from a number of surveys. While survey indications of lower wage growth were favourable news for the inflation outlook, caution was expressed that this decline still needed to appear in the data, which, so far, had remained exceptionally high by historical standards.

In this context, it was considered useful to look at decompositions of wage growth into its main drivers, such as the catch-up component, forward-looking inflation expectations, labour market tightness and compensation for higher productivity. Reference was made to evidence from the CTS, where more than half of respondents had indicated that recruiting had become harder at prevailing wages. In case labour scarcity turned out to be a structural phenomenon caused, for example, by demographic factors or changes in preferences for leisure, it was important to assess how far wage increases reflected the increased negotiation power of workers, whether individual or collective, and how far they merely reflected real wage catch-up in the wake of the inflation surge.

The staggered process of collective wage bargaining implied a deferred impact of inflation on real wage catch-up. Real wages of a very large share of workers in some countries still fell short of their pre-pandemic levels. Looking ahead, this provided for some protractedness in wage dynamics. While from an inflation perspective it was desirable for the catch-up to proceed in a contained manner, it was also a healthy element underpinning real income growth and benefiting the euro area economy. At the same time, concerns were expressed that wages might continue to grow more strongly than would be consistent with the inflation target – even after the catch-up process had been completed. However, the more real wages caught up, the lower the incentives for workers to claim higher wage increases and for firms to pass on those wage increases in the current environment of weak demand.

As regards longer-term inflation expectations, members took note of the latest developments in market-based measures of inflation compensation and survey-based indicators. Measures of longer-term inflation expectations had remained broadly stable, with most standing at around 2%. Current inflation expectations were well anchored, but suggested that inflation was unlikely to undershoot the target as distributions were still skewed to the upside. This was generally valid for expectations derived from the Consumer Expectations Survey, the SAFE, the SPF and the SMA. The option-implied probabilities for five-year forward inflation-linked swap rates five years ahead were higher for outcomes above 2.5% than for outcomes below 1.5%. However, analysts’ longer-term inflation expectations as reported in the SMA did not show the same asymmetry. It was suggested that, in principle, larger upside than downside risks could be reconciled with expectations of more frequent adverse supply shocks in the future.

Regarding risks, members assessed that inflation could turn out higher than anticipated if wages or profits increased by more than expected. Upside risks to inflation also stemmed from the heightened geopolitical tensions, which could push energy prices and freight costs higher in the near term and disrupt global trade. Moreover, extreme weather events, and the unfolding climate crisis more broadly, could drive up food prices. By contrast, inflation might surprise on the downside if monetary policy dampened demand more than expected, or if the economic environment in the rest of the world worsened unexpectedly.

The point was made that downside risks to aggregate demand would come with downside risks to inflation over the medium term. At the same time, it was argued that there were still good reasons to remain watchful of upside risks to inflation. First, incoming data, particularly for services inflation, had been above earlier expectations. Second, key building blocks of the disinflation narrative, such as the expected pick-up in productivity and moderation in wage growth, had yet to appear in the actual data. At present, unit labour costs were still growing fast.

Turning to the monetary and financial analysis, members underlined that the policy rate cut in June had been transmitted smoothly to money market interest rates. Market interest rates had edged down since the Governing Council’s previous monetary policy meeting in June, although they had been fluctuating to some extent since then in response to data releases. On average market participants were currently pricing in almost two additional 25 basis point cuts by the end of the year, but had attached almost no probability to a cut at the July monetary policy meeting.

Overall, broader financial conditions had changed little since the Governing Council’s previous monetary policy meeting in June, but they had been somewhat volatile in the meantime. Financial markets had been affected by political uncertainty in the euro area, although the overall effects and increase in volatility had remained muted and had largely been reversed. Financing costs had remained broadly stable at restrictive levels, as previous policy rate increases continued to work their way through the transmission chain. The average interest rate on new loans to firms had edged down in May, while mortgage rates had remained unchanged.

Lending conditions had remained tight. According to the latest BLS, credit standards for lending to firms had tightened slightly in the second quarter, while standards for mortgages had eased moderately. The BLS also highlighted continued sluggish demand from firms for loans and credit lines, though expected growth in loan demand had turned positive. Moreover, households’ demand for mortgages and consumer loans had risen. The view was expressed that, overall, the BLS results suggested that the transmission of monetary policy restriction was likely to have passed its peak.

Credit growth also remained subdued. Growth of bank lending to firms and households had remained at low levels in May and had only marginally increased from the previous month. The annual growth rate of M3 had continued its gradual recovery while remaining relatively subdued. It was largely being driven by inflows of funds from outside the euro area.

Monetary policy stance and policy considerations

Turning to the monetary policy stance, members assessed the data that had become available since the last monetary policy meeting in accordance with the three main elements that the Governing Council had communicated in 2023 as shaping its reaction function.

Starting with the inflation outlook, members broadly concurred with the assessment that had been presented by Mr Lane in his introduction. The incoming information and forward-looking indicators had generally supported the Governing Council’s previous assessment of the medium-term inflation outlook. Recent developments and the latest data were still broadly consistent with the June staff projections. Headline inflation was expected to fluctuate around current levels for the rest of the year, partly owing to energy-related base effects. But inflation was expected to decline towards the target over the second half of next year and then stabilise around the target in 2026. It was also important to note that inflation expectations had remained firmly anchored, with most measures of longer-term inflation expectations standing at around 2%. At the same time, the current distribution of inflation expectations was still skewed to the upside. In addition, services inflation had continued to be more persistent than expected.

With regard to underlying inflation, members noted that while some measures of underlying inflation had ticked up in May owing to one-off factors, most measures had either been stable or edged down in June. Still, the signals from the different measures of underlying inflation remained mixed. Domestic inflation continued to be elevated, at the top of the range of these measures, and appeared to be stickier than expected. Core inflation also remained relatively high. It had been higher than expected, showing some persistence, and was still subject to upside risks given the repeated upside surprises in services inflation. More generally, many measures of underlying inflation were likely to be fairly flat for the remainder of the year. Interpreting these data had become trickier because, as inflation approached the target, these measures would naturally adjust more slowly. It was therefore becoming harder to determine whether or not the slower decline signalled a genuine stalling of the disinflation process. Labour cost dynamics would continue to be a key concern, with the interaction between wages, productivity and profits likely to be particularly important for the evolution of domestic inflation, as captured by the GDP deflator. In this respect, it was comforting to see that domestic cost pressures from high wage growth, including in the services sector, had been increasingly buffered by unit profits.

Finally, members generally agreed that monetary policy transmission was unfolding according to expectations. Monetary policy was keeping financing conditions restrictive and the transmission of past policy rate hikes remained strong. Tight financing conditions partly explained the sluggishness in domestic demand and would continue to weigh on activity in the coming months. The view was taken that the ongoing contraction of the Eurosystem balance sheet added to that restrictiveness. At the same time, the continued growth of profits in the services sector, albeit at lower rates, and the strength of services demand suggested a weaker transmission of monetary policy to the part of the economy that was exerting the strongest inflationary pressures. That said, monetary policy would probably take longer to be transmitted to the services sector. And even if transmission to services inflation was relatively weaker, this should not be seen in isolation from the relatively low goods price inflation.

Monetary policy decisions and communication

Against this background, all members agreed with Mr Lane’s proposal to maintain the three key ECB interest rates at their current levels. Members concurred that the incoming information broadly supported the Governing Council’s previous assessment of the medium-term inflation outlook. While some measures of underlying inflation had ticked up in May owing to one-off factors, most measures had either been stable or edged down in June. In line with expectations, the inflationary impact of high wage growth had been buffered by profits. Monetary policy was keeping financing conditions restrictive. At the same time, domestic price pressures were still high, services inflation was elevated and headline inflation was likely to remain above the target well into 2025. It was remarked that these developments suggested that the last mile of disinflation was more challenging and that the task of bringing inflation down sustainably to the 2% target was not yet assured, despite the significant progress made.

With inflation coming down only gradually, it was seen as natural that the Governing Council’s policy response should be cautious. This supported a pause at the current meeting. Such a cautious approach was particularly warranted given the prevailing uncertainties about the evolution of wages, profits, productivity and services inflation. All of these would need further monitoring and assessment as new data arrived in order to gain further confidence in the inflation outlook. By the time of the September meeting extensive new data would be available, such as the July and August inflation data; national account information on the second quarter, including compensation per employee, profits and productivity; an update on monetary data; and a new set of staff projections.

In terms of timing, it was argued that the Governing Council could afford to be patient and wait for more data to confirm that disinflation was indeed on track. A cautious approach would also allow the Governing Council to respond by following a more gradual path of reducing policy rates if inflation was more persistent than currently foreseen. The importance of bringing inflation down sustainably to the target in a timely manner was reiterated. It mattered both for credibility and because a further delay could entail high costs, with inflation expectations being more fragile than usual owing to inflation having been above target for so long. At the same time, it was underlined that a gradual attenuation of policy restriction was a balancing act, as it was also important not to unduly harm the economy by keeping rates at a restrictive level for too long.

Members emphasised that they remained determined to ensure inflation would return to the 2% medium-term target in a timely manner and that they would keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. It was also seen as important to maintain a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. There should be no pre-commitment to a particular rate path, since the exact pace at which inflation would return to target remained uncertain. It was nonetheless also important to keep an eye on the real economy. The September meeting was widely seen as a good time to re-evaluate the level of monetary policy restriction. That meeting should be approached with an open mind, which also implied that data dependence was not equivalent to being overly focused on specific, single data points. Finally, policy should continue to be based on the established elements of the reaction function.

Members also agreed with the Executive Board proposal to continue applying flexibility in the partial reinvestment of redemptions falling due in the pandemic emergency purchase programme portfolio.

Taking into account the foregoing discussion among the members, upon a proposal by the President, the Governing Council took the monetary policy decisions as set out in the monetary policy press release. The members of the Governing Council subsequently finalised the monetary policy statement, which the President and the Vice-President would, as usual, deliver at the press conference following the Governing Council meeting.

Monetary policy statement

Monetary policy statement for the press conference of 18 July 2024

Press release

Meeting of the ECB’s Governing Council, 17-18 July 2024

Members

- Ms Lagarde President

- Mr de Guindos Vice-President

- Mr Centeno

- Mr Cipollone

- Ms Delgado

- Mr Elderson

- Mr Kazāks*

- Mr Kažimír

- Mr Knot

- Mr Lane

- Mr Makhlouf

- Mr Müller

- Mr Nagel*

- Mr Panetta

- Mr Patsalides*

- Mr Rehn

- Mr Reinesch*

- Ms Schnabel

- Mr Scicluna

- Mr Šimkus*

- Mr Stournaras

- Mr Vasle

- Mr Villeroy de Galhau

- Mr Vujčić

- Mr Wunsch

* Members not holding a voting right in July 2024 under Article 10.2 of the ESCB Statute.

Other attendees

- Ms Senkovic, Secretary, Director General Secretariat

- Mr Rostagno, Secretary for monetary policy, Director General Monetary Policy

- Mr Winkler, Deputy Secretary for monetary policy, Senior Adviser, DG Economics

Accompanying persons

- Mr Arpa

- Ms Bénassy-Quéré

- Mr Dabušinskas

- Mr Demarco

- Mr Gavilán

- Mr Gilbert

- Mr Haber Alternate to Mr Holzmann

- Mr Kaasik

- Mr Koukoularides

- Mr Lünnemann

- Mr Madouros

- Mr Martin

- Ms Mauderer

- Mr Nicoletti Altimari

- Mr Novo

- Mr Rutkaste

- Mr Šošić

- Mr Tavlas

- Mr Välimäki

- Mr Vanackere

- Ms Žumer Šujica

Other ECB staff

- Mr Proissl, Director General Communications

- Mr Straub, Counsellor to the President

- Ms Rahmouni-Rousseau, Director General Market Operations

- Mr Arce, Director General Economics

- Mr Sousa, Deputy Director General Economics

Release of the next monetary policy account foreseen on 10 October 2024.

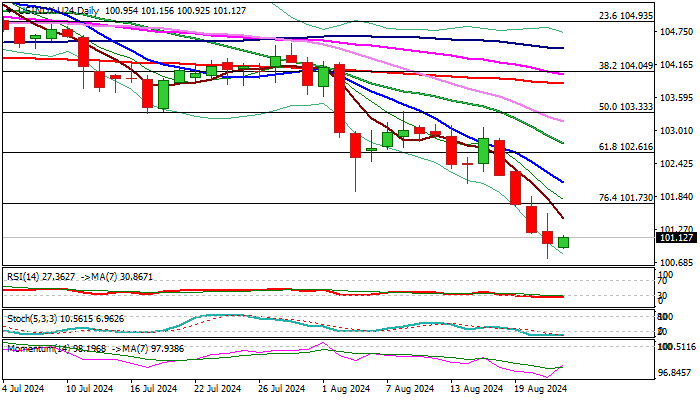

Dollar Index Ooutlook: Bears Take a Breather Ahead of Speech of Fed Chair Powell

The Dollar Index ticks higher in early European trading on Thursday, from new lowest level since Dec 23, hit after release of FOMC July policy meeting.

Minutes showed that the US policymakers remain on track for rate cut in September, as inflation eased and significant signs of weakness in the labor market, further support the anticipated scenario.

The dollar was in steep bear-leg in past four days (part of broader downtrend) in expectations that Fed will confirm its dovish stance, suggesting FOMC decisions have been already priced in and ‘sell the rumors-buy the facts’ scenario likely to follow.

Deeply oversold daily studies contribute to signals that it is a time for partial profit taking, as markets expect next key event of the week – the speech of Fed Chair Powell in Jackson Hole on Friday, which is expected to provide more details about the depth and the pace of Fed policy easing and generate fresh direction signal.

Powell is unlikely to diverge from Fed’s general direction, therefore expected to maintain dovish stance, that will contribute to expectations for limited correction before bears regain control.

Solid resistances at 102.00 zone (former low of Aug 5 at 101.94 and falling 10DMA at 102.08) should ideally cap and provide better selling opportunities (on anticipated dovish comments from Fed Powell) for push towards targets at 102.29/18 (Dec 28 low / 200WMA) and psychological 100.00 support.

Conversely, stronger acceleration higher and violation of pivotal 102.80/103.00 resistance zone, would question larger bears.

Res: 101.54; 101.73; 102.00; 102.61.

Sup: 100.75; 100.29; 100.18; 100.00.

Euro Edges Lower on Mixed Eurozone PMI

The euro is steady on Thursday. In the European session, EUR/USD is trading at 1.1136 at the time of writing, down 0.11% on the day.

Eurozone services accelerates, manufacturing dips down

There was mixed news from the eurozone PMIs, which provide a monthly report card for the services and manufacturing sectors. The services PMI climbed to 53.3 in August, up from 51.9 and above the market estimate of 51.9. This was the highest level of expansion since April and was largely boosted by the Olympic Games in Paris which took place in August. Notably, inflation fell to its lowest level since April 2021.

Manufacturing remained mired in contraction and dipped to 45.6, down from 45.8 in July and shy of the market estimate of 45.8. This was an eight-month low. Manufacturing hasn’t posted a month of growth in over two years and a weak global market means demand isn’t likely to improve anytime soon.

Germany, the largest economy in the eurozone, continues to struggle. The services PMI dropped to 51.4 in August, down from 52.5 in July and below the market estimate of 52.3. This was the weakest pace of expansion since March and services have weakened for the third straight month.

The Fed has signaled that a milestone interest rate cut is coming next month, likely as a quarter-point reduction. The Fed minutes on Wednesday noted concern over the deterioration in the labor market and most FOMC members at the meeting viewed a September rate cut as appropriate. Federal Chair Jerome Powell will address the Jackson Hole Symposium on Friday and the markets will be all ears.

.

EUR/USD Technical

- EUR/USD is testing support at 1.1141. Below, there is support at 1.1108

- 1.1183 and 1.1216 are the next resistance lines

JP 225 Index: Is There More Upside on the Horizon?

- JP 225 index reclaims August’s loss

- Short-term risk is on the positive side

- Will the bulls breach the 38,600-39,950 area too?

Japan’s 225 stock index (cash) is trading with soft positive momentum on Thursday for the second consecutive day, hitting a three-week high of 38,421.

The index has reversed more than half of its July-August freefall and there could be more bullish potential as the technical risk remains skewed to the upside.

Despite the downturn in the stochastic oscillator, the RSI is making a gradual upward progress above its neutral mark of 50 and is still far from its overbought level of 70. Likewise, the MACD remains positively charged above its red signal line, aiming to climb above its zero line. Adding to the positive signals is the price itself which has crossed above the middle Bollinger band and is some distance below the upper band.

The journey higher, however, could be challenging. The 50-day simple moving average (SMA) at 38,600 and then the 39,500-39,950 area could tease the bulls, delaying an advance towards the 41,147-41,500 resistance zone. If the latter gives way, it would be intriguing to see if fresh buying will push the price beyond the 42,950 bar.

In the bearish scenario that the price drops below the 200-day SMA at 37,435, the spotlight will fall on the 20-day SMA (Middle Bollinger band) at 36,600. The 35,300 region might draw greater attention as a violation there could press the price back into the 33,585-33,130 floor.

In summary, there is a possibility that Japan’s 225 index will maintain its recovery trend in the near future, though whether it will manage to surpass the 38,600-39,950 territory remains to be seen. Alternatively, a close below 37,435 might raise fresh selling interest.

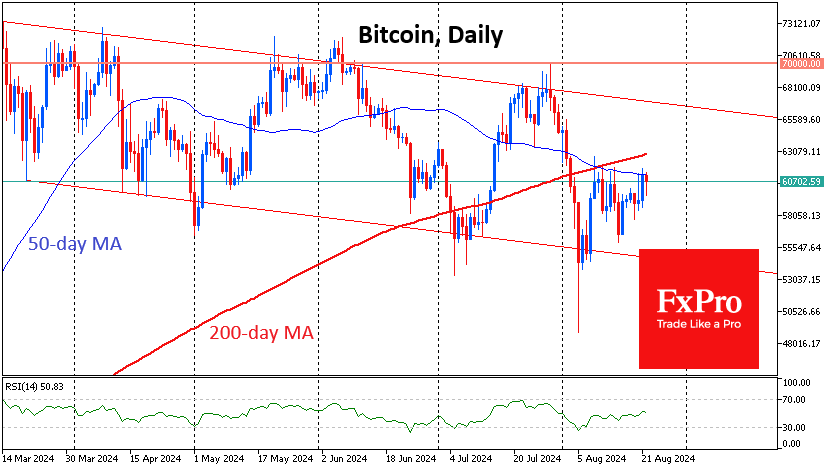

Crypto Tug of War

Market picture

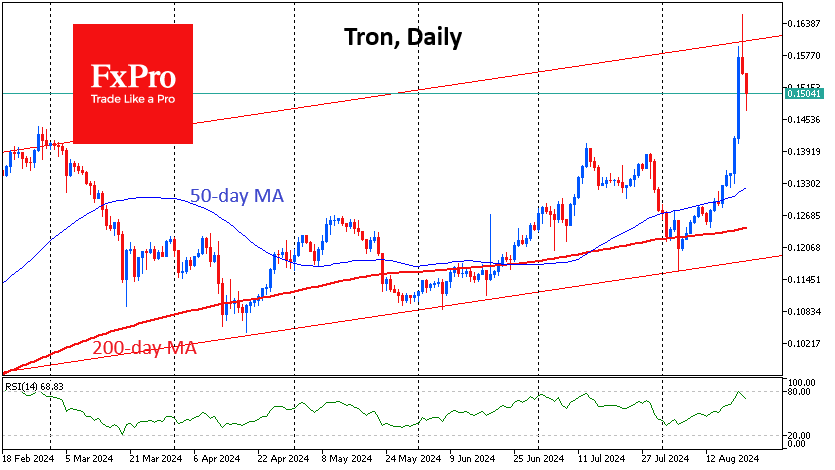

The crypto market gained 1.7% in the last 24 hours to reach $2.14 trillion, continuing to test August’s resistance. Bitcoin rose 2.6%, while Ethereum gained 1.2%. The battle for a 10th position in the CoinMarketCap has intensified: Tron’s 5.5% drop to a cap of $13.09 billion contrasted with Cardano’s 2.5% rise to $13.17 billion. Its closest rival, Dogecoin, added 1.3% to reach a total coin value of $15.36 billion, with 17% distance from Cardano.

Crypto market sentiment indices are approaching neutral territory thanks to a weaker dollar and growing confidence in an imminent interest rate cut. Bitcoin is trading around $60.8K, hesitant to grow but not far from its 50-day average. The dynamics of the last few days show a transfer of capital from cautious sellers (who may have received funds from Mt. Gox) to long-term buyers accumulating ETFs.

News background

According to CryptoQuant data, major bitcoin investors have slowed their monthly coin accumulation rate to 1%, compared to the 3% average typical of bull markets. Most demand metrics are showing weakness, which is not enough for a new all-time high. The alternative in the form of spot bitcoin ETFs is also unreliable, with daily net inflows into the instruments at a fraction of March’s levels.

According to Arkham, bankrupt cryptocurrency exchange Mt. Gox sent another 13,265 BTC ($784 million) to an unknown address. The last movements of Mt. Gox assets to external addresses were recorded at the end of July in the amounts of 33,964 BTC ($2.25 billion) and 858 BTC ($56.8 million).

A new class action lawsuit has been filed against the Binance exchange and former CEO Changpeng Zhao. According to the lawsuit, filed in federal court in Seattle, the three crypto investors have been unable to recover their stolen assets because the exchange failed to prevent money laundering.

The chances of the Solana ETF being registered in the US in 2024 are zero, as they will be in 2025. Bloomberg believes that only new SEC leadership can change the situation. Previously, the SEC rejected proposals from CBOE to register the SOL ETF, suggesting that Solana could be classified as a “security.”

Messari notes that only about 1.4% of the meme coins launched on Solana’s Pump.fun platform reach profitability levels. Amid frustration, investors have begun to pull out of the market, with trading volumes in the segment falling by 80% in the last two weeks.

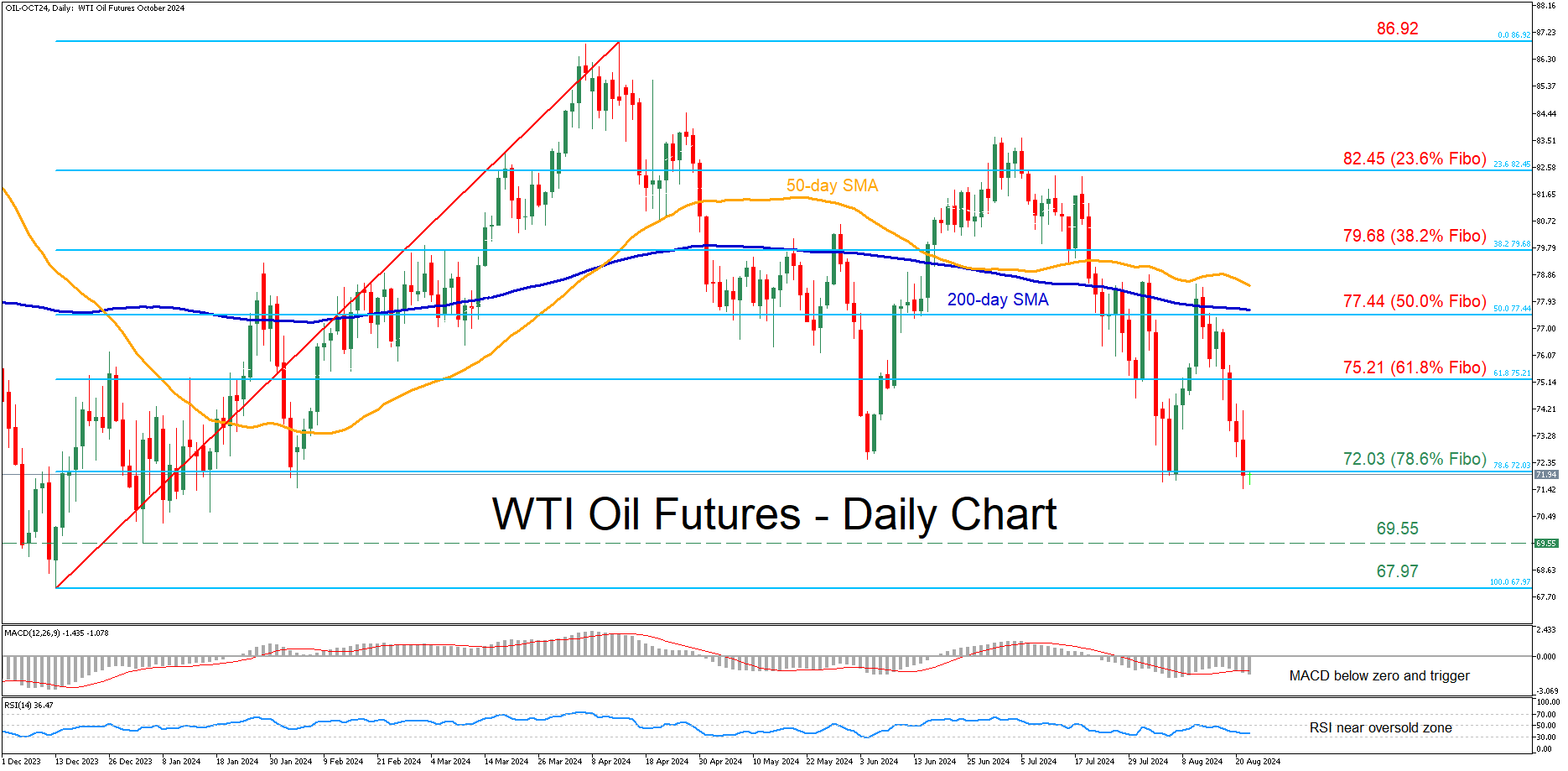

WTI Futures Fall to a 7-Month Low

- WTI futures drop to their lowest level since January 17

- Momentum indicators are heavily tilted to bearish side

WTI oil futures (October delivery) have been in a steady retreat following their rejection at the 200-day simple moving average (SMA) in mid-August. On Wednesday, the price fell to a fresh seven-month low before finding its feet a tad above the 70.00 psychological mark.

Should the bears attempt to push the price lower, they need to initially claim 72.03, which is the 78.6% Fibonacci retracement of the 67.97 – 86.92 upleg. A violation of that zone could pave the way for the 2024 low of 69.55. Further declines could then cease at the December 2023 bottom of 67.97.

On the flipside, bullish actions could propel the price towards the 61.8% fibo of 75.21. Surpassing that zone, the price may advance towards the 50.0% Fibo of 77.44, which coincides with the 200-day SMA. Even higher, the 38.2% Fibo of 79.68 could prevent further upside attempts.

Overall, WTI oil futures have been on a slippery slope in the past few sessions, dropping to a fresh seven-month low. However, their failure to extend the recent decline might lead to the formation of a double bottom, which is indicative of a reversal pattern.

UK PMI data shows robust growth, easing inflation opens door for BoE rate cuts

UK’s PMI data for August showed positive momentum across both the manufacturing and services sectors. PMI Manufacturing edged up from 52.1 to 52.5, surpassing expectations of 52.2 and marking a 26-month high. PMI Services also rose from 52.5 to 53.3, above the expected 52.8. This led to PMI Composite increase from 52.8 to 53.4.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, highlighted the significance of these figures, noting that "August is witnessing a welcome combination of stronger economic growth, improved job creation, and lower inflation." He emphasized that both manufacturing and service sectors are showing solid output growth and increased job gains, with business confidence remaining historically high.

However, Williamson tempered expectations by pointing out that while GDP growth is likely to slow in Q3 compared to the impressive gains seen earlier in the year, the PMI data still indicates the economy is expanding at a "reasonably solid quarterly rate of around 0.3%."

On the inflation front, pressures have continued to moderate, particularly in the service sector, which has been a key area of concern for BoE. Williamson suggested that the latest survey data could "lower the bar for further interest rate cuts," though he cautioned that the still-elevated nature of service sector inflation means that policymakers are likely to proceed with caution.

Eurozone PMI composite rises to 51.2, easing cost pressures strengthens case for ECB Sep cut

Eurozone PMI Manufacturing fell slightly from 45.8 to 45.6 in August, an 8-month low and below expectations of 46.1. In contrast, PMI Services showed a strong performance, rising from 51.9 to 53.3, surpassing the expected 52.2. This divergence led to a modest increase in PMI Composite, which climbed from 50.2 to 51.2, signaling faster expansion.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, offered a cautious interpretation of the data, noting that the underlying fundamentals might be "shakier than they appear." He highlighted that the boost in PMI Composite is largely driven by a surge in services activity in France, likely linked to the Olympic Games in Paris. However, de la Rubia expressed doubt that this momentum will persist in the coming months. Meanwhile, Germany’s services sector showed a slowdown in growth, and Eurozone’s manufacturing sector "remains in rapid decline."

On the inflation front, de la Rubia pointed out that input costs in the services sector, a key focus for ECB, rose at the slowest pace in 40 months. This easing of cost pressures, despite the faster climb in output prices compared to July, strengthens the case for an interest rate cut at ECB's upcoming September meeting.