Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6494; (P) 0.6535; (R1) 0.6559; More...

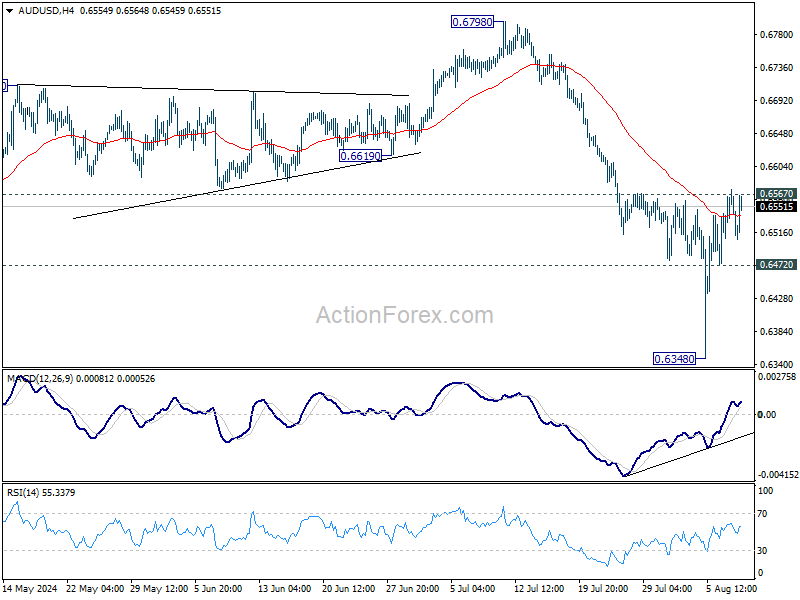

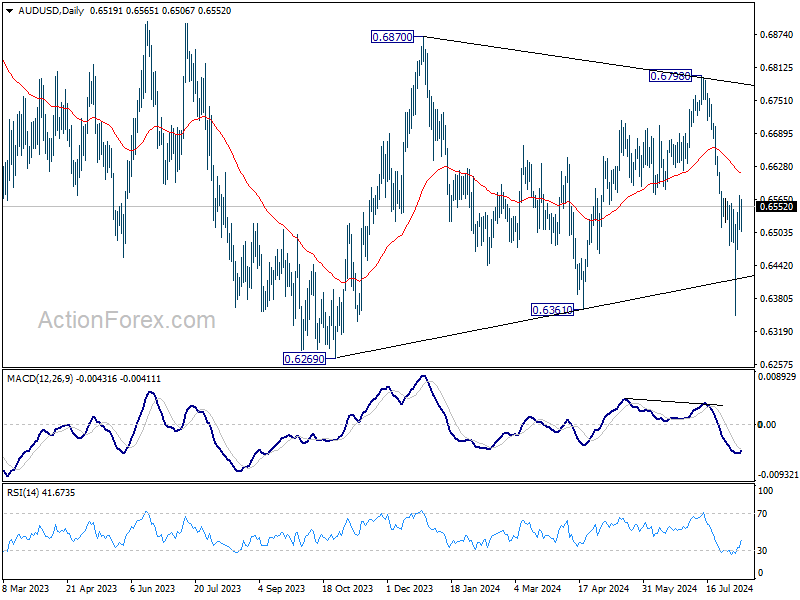

Intraday bias in AUD/USD remains neutral as rebound from 0.6348 is still struggling to extend through 0.6567 resistance decisively. On the downside, break of 0.6472 minor support will retain near term bearishness and bring retest of 0.6348 low first. However, strong break of 0.6567 will bring stronger rally to 55 D EMA (now at 0.6616) and possibly above.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 55 D EMA (now at 0.6617) holds, in case of rebound.

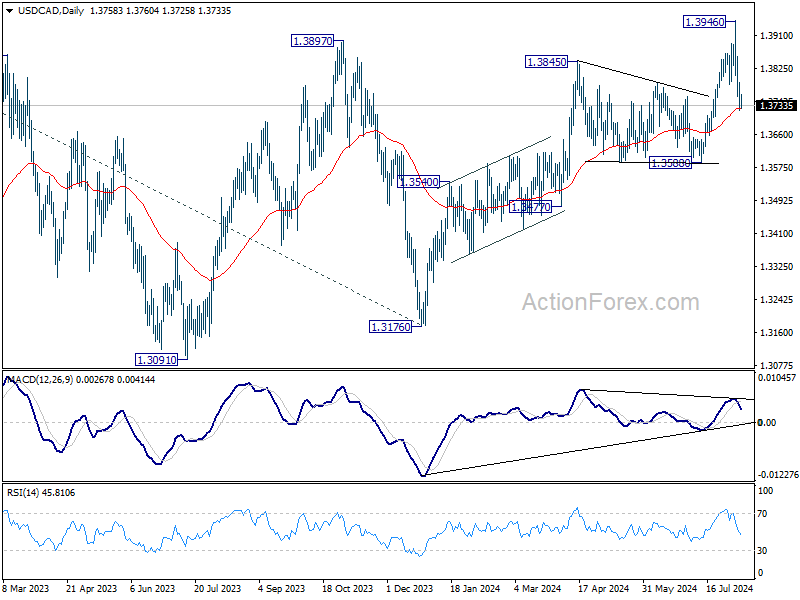

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3722; (P) 1.3756; (R1) 1.3792; More...

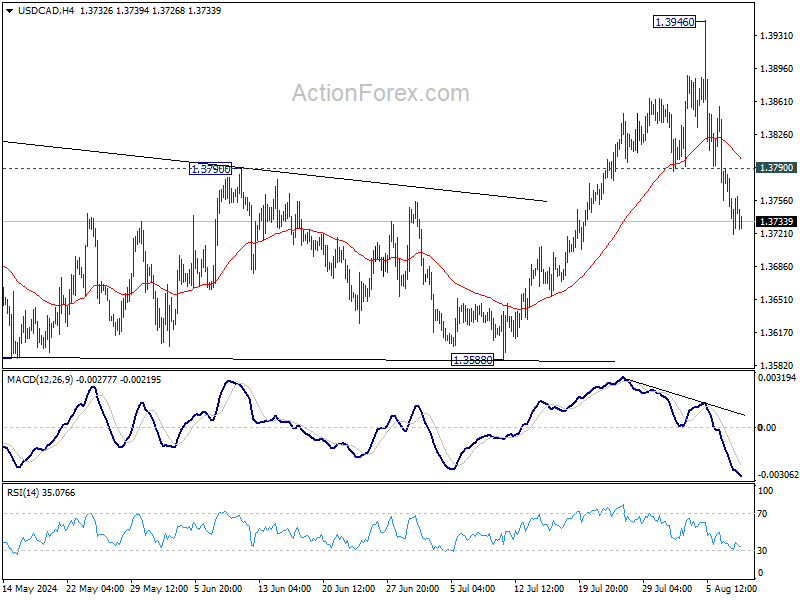

Intraday bias in USD/CAD remains on the downside as pullback from 1.3946 short term top extends. Sustained break of 55 D EMA (now at 1.3726) would dampen the original bullish outlook and bring deeper fall. On the upside, above 1.3790 minor resistance will bring retest of 1.3946.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

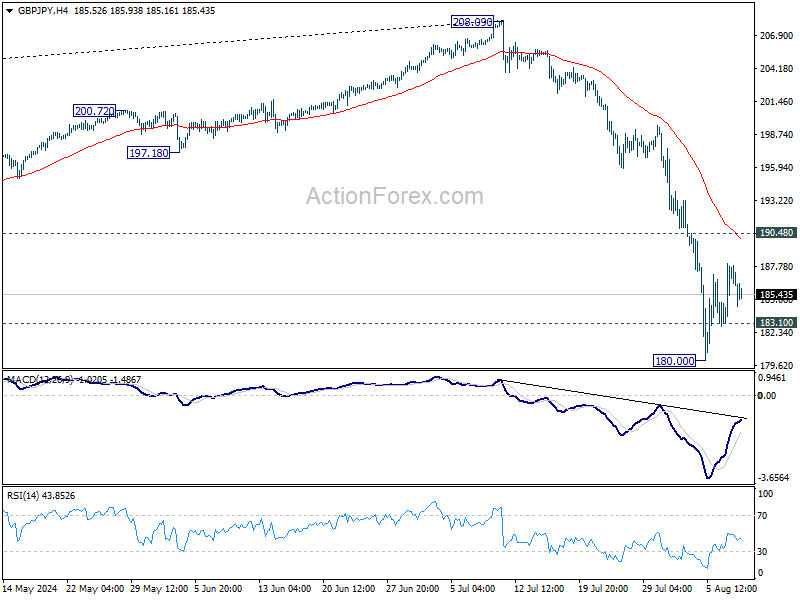

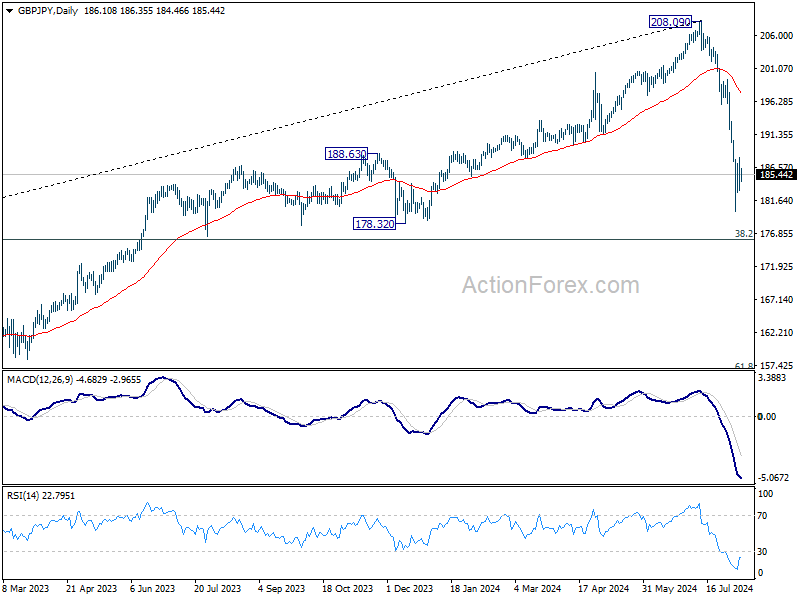

GBP/JPY Daily Outlook

Daily Pivots: (S1) 183.47; (P) 185.78; (R1) 188.55; More...

Intraday bias in GBP/JPY remains neutral for the moment. Outlook stays bearish as long as 190.48 resistance holds. On the downside, below 183.10 minor support will bring retest of 180.00 first. Break there will resume the fall from 208.09 to 178.32 support next. Nevertheless, firm break of 190.48 will confirm short term bottoming and bring stronger rebound.

In the bigger picture, fall from 208.09 medium term top is seen as correcting the up trend from 123.94 (2020 low). Deeper decline is in favor as long as 55 W EMA (now at 189.31) holds. But strong support could emerge between 178.32 and 38.2% retracement of 123.94 to 208.09 at 175.94 to bring rebound. Meanwhile, sustained trading above 55 W EMA will suggest that the range for the medium term corrective pattern is already set.

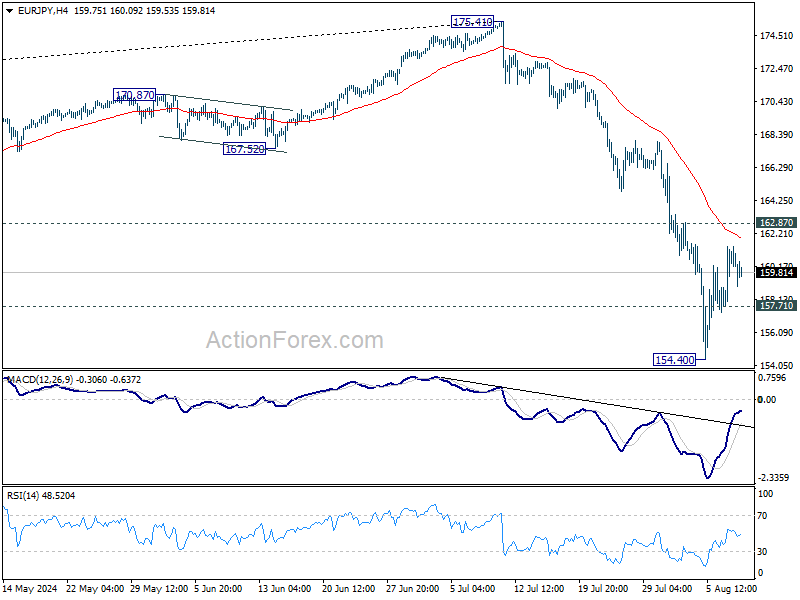

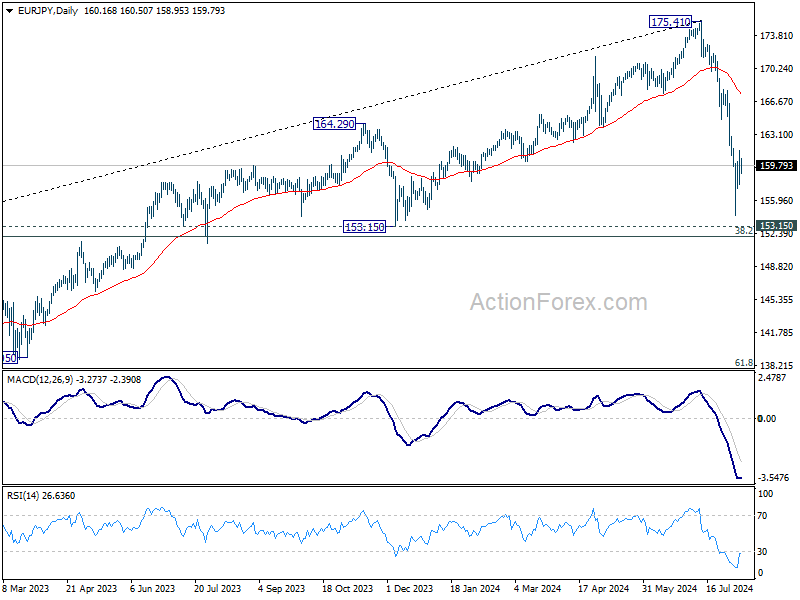

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.15; (P) 159.80; (R1) 161.91; More...

Intraday bias in EUR/JPY stays neutral at this point, and outlook remains bearish with 162.87 resistance intact. On the downside, below 157.71 minor support will turn bias back to the downside. Break of 154.40 will resume the fall from 175.41 to 153.15 support next. However, decisive break of 162.87 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper fall could be seen as long as 55 W EMA (now at 161.79) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound (at least on first attempt). Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8583; (P) 0.8600; (R1) 0.8623; More....

Intraday bias in EUR/GBP is mildly on the upside with breach of 0.8618 temporary top. Rise from 0.8382 is resuming for 0.8643 resistance. Decisive break there will strengthen the case of larger bullish reversal and target 0.8764 key resistance next. On the downside, however, break of 0.8561 support will turn bias to the downside for deeper pullback.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish.

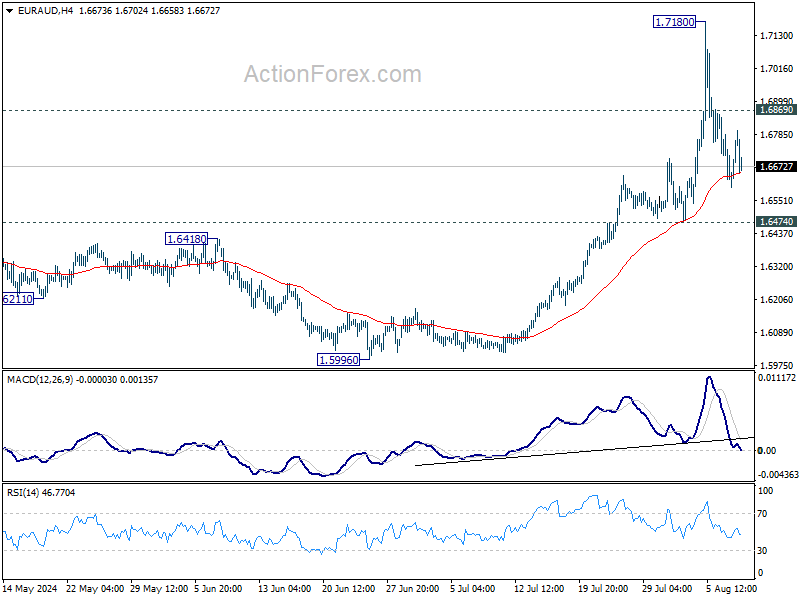

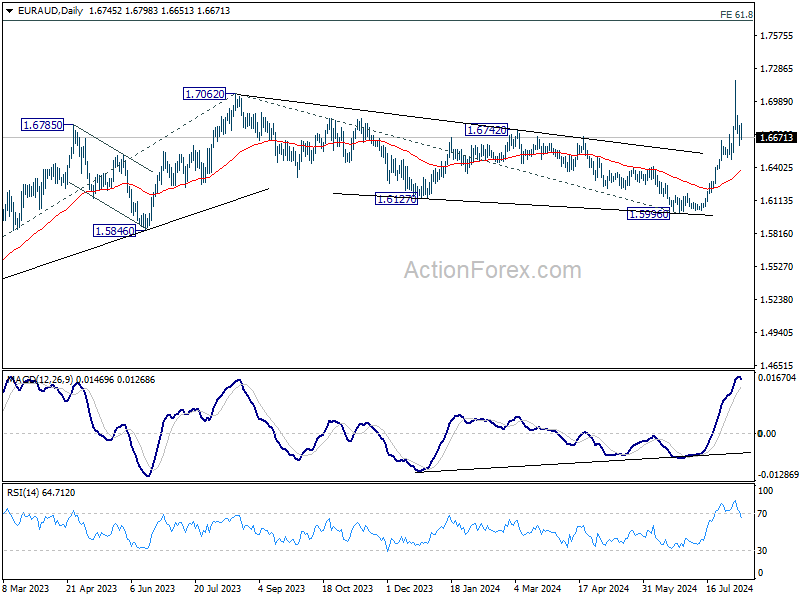

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6643; (P) 1.6714; (R1) 1.6826; More...

Intraday bias in EUR/AUD remains neutral for the moment. While deeper retreat cannot be ruled out, outlook will remain bullish as long as 1.6474 support holds. On the upside, above 1.6869 minor resistance will turn bias back to the upside for retesting 1.7180. Firm break there will resume larger up trend to 1.7715 fibonacci projection level next.

In the bigger picture, decisive break of 1.7062 resistance will confirm resumption of whole up trend from 1. 1.4281 (2022 low). Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. For now, further rally is expected as long as 55 D EMA (now at 1.6355) support holds, even in case of deep retreat.

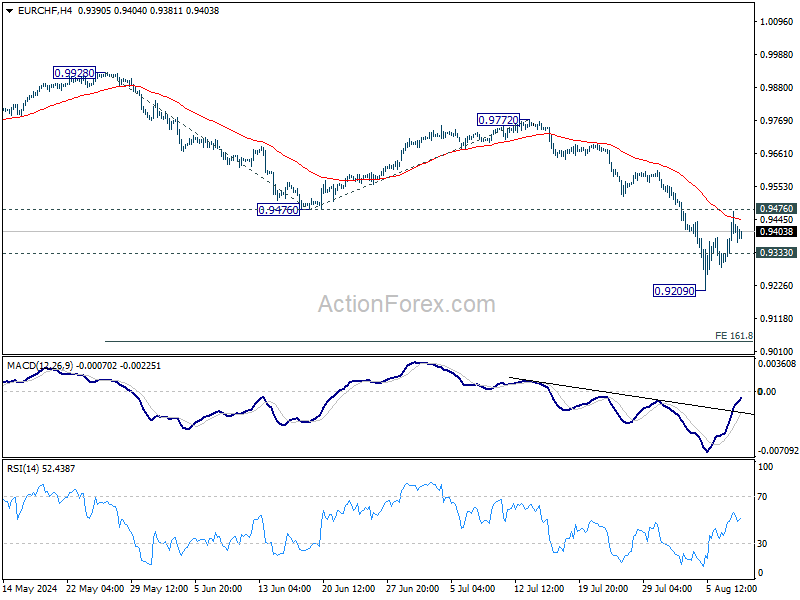

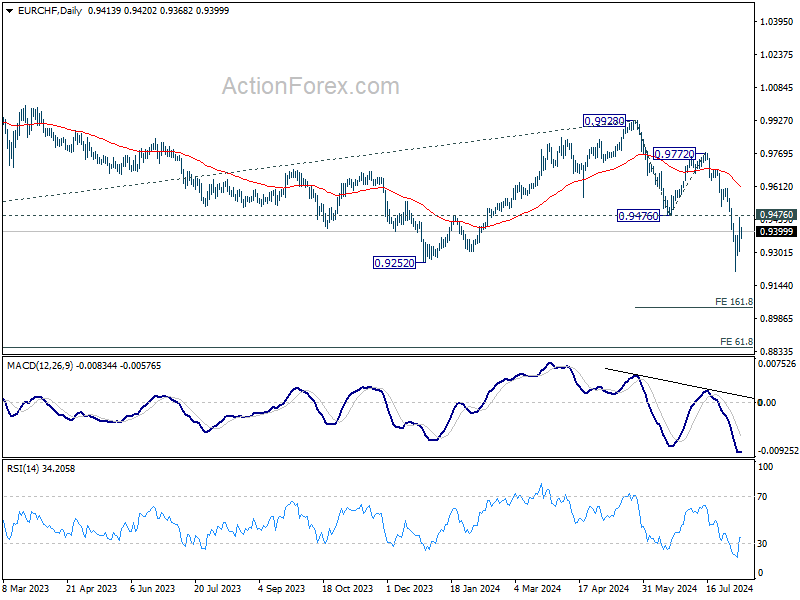

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9321; (P) 0.9395; (R1) 0.9488; More....

EUR/CHF's recovery from 0.9209 extended higher but upside is capped below 0.9476 support turned resistance. Intraday bias remains neutral and further decline is still expected. On the downside, below 0.9333 minor support will bring retest of 0.9209 first. Firm break there will resume larger fall from 0.9928 to 161.8% projection of 0.9928 to 0.94767 from 0.9772 at 0.9041 next. However, sustained break of 0.9476 will turn bias back to the upside for stronger rebound.

In the bigger picture, current downside acceleration argues that medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Central Bank Signals Ignored; Consolidation Continues in Currency Markets

The financial markets are relatively quiet in Asian session today, with major currency pairs and crosses trading within yesterday's range. BoC's summary of deliberations suggested that the central bank is on track for further policy loosening. Meanwhile, BoJ's summary of opinions indicated the board is preparing for more rate hikes. Comments from RBA's Governor reiterated that another rate hike remains possible, while rate cuts are not on the horizon. Additionally, RBNZ's survey showed a notable decline in inflation expectations, providing room for a rate cut this year. Despite these significant policy signals, the markets have largely ignored them.

Most currency pairs appear to be in consolidation following recent sharp moves, including Yen and Swiss Franc. Sentiment remains fragile, with risk-off behavior likely to resurface at any moment. For the week, Canadian Dollar is currently the strongest, followed by Kiwi and Aussie. Sterling is the weakest, followed by Swiss Franc and Dollar. Euro and Yen are positioned in the middle of the pack.

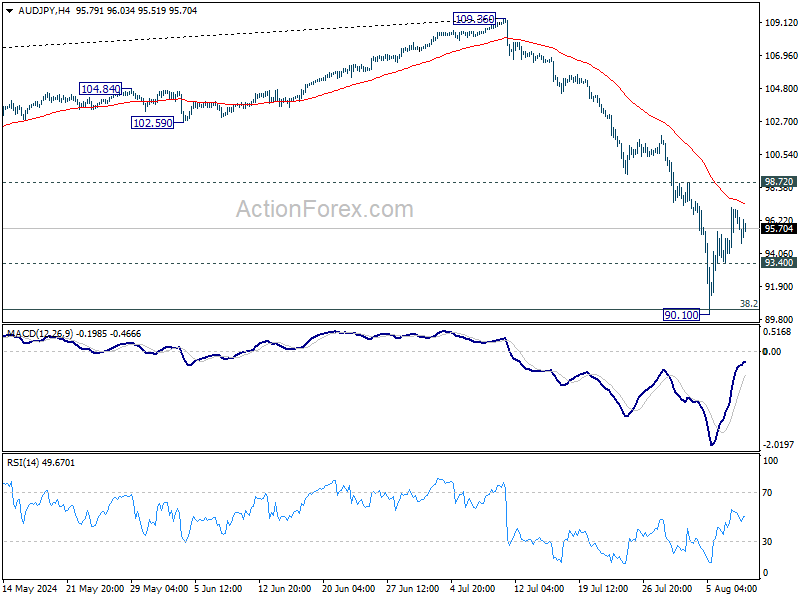

Technically, the recent rebound in Yen crosses is beginning to lose momentum. AUD/JPY is particularly worth watching, as it could be the first to fall on renewed risk-off sentiment. Break of 93.40 minor support will argue that the recovery from 90.10 has completed, and bring retest of this low. Further break there will resume the whole decline from 109.36. While another rise cannot be ruled out, outlook will stay bearish as long as 98.72 resistance holds, and eventual downside breakout is still in favor.

In Asia, Nikkei closed down -0.80%. Hong Kong HSI is up 0.22%. China Shanghai SSE is up 0.16%. Singapore Strait Times is up 0.13%. Japan 10-year JGB fell -0.0317 to 0.849. Overnight, DOW fell -0.60%. S&P 500 fell -0.77%. NASDAQ fell -1.05%. 10-year yield rose 0.080 to 3.968.

One BoJ member suggests gradual rate hike to above 1% neutral rate

BoJ's Summary of Opinions from the July 30-31 meeting reveals that board members discussed further rate hikes after implementing the second interest rate increase this year at the meeting.

One member's opinion stood out, suggesting that, assuming the price stability target is achieved in the second half of fiscal 2025, BoJ should raise the policy interest rate to the level of the "neutral interest rate." This neutral rate is estimated to be "at least around 1 percent." To avoid rapid hikes, BoJ should increase the policy interest rate in a "timely and gradual manner."

The consensus among members is that economic activity and prices have been developing generally "in line with the Bank's outlook." Consequently, it is deemed appropriate for to raise the policy interest rate and adjust the degree of monetary accommodation.

One opinion highlighted that raising interest rates at a "moderate pace" aligns the adjustment in monetary accommodation with underlying inflation. Such moves "will not have monetary tightening effects."

RBA's Bullock: Rate hikes still possible as inflation timeline extends

RBA Governor Michele Bullock revealed in a speech today that the board "explicitly considered" another rate hike during Tuesday's meeting. Although they decided to hold rates steady, Bullock stressed that RBA "will not hesitate" to hike if necessary.

Bullock highlighted two main points from the meeting. First, despite weak economic growth, the gap between aggregate demand and supply is "larger than previously thought," leading to "persistent inflation." Second, demand growth is expected to "pick up over the next year," though there is significant uncertainty about this outlook.

Due to these factors, the Board's inflation target timeline has been "pushed out". "We don't expect to be back in the 2–3 percent target range until the end of 2025 – over a year away," Bullock stated. This delay prompted the board to consider another rate hike to ensure inflation continues to decline.

Ultimately, RBA decided to keep interest rates unchanged, believing this would balance their inflation and employment objectives. However, Bullock emphasized that the Board remains vigilant regarding upside inflation risks and "will not hesitate to raise rates if it needs to."

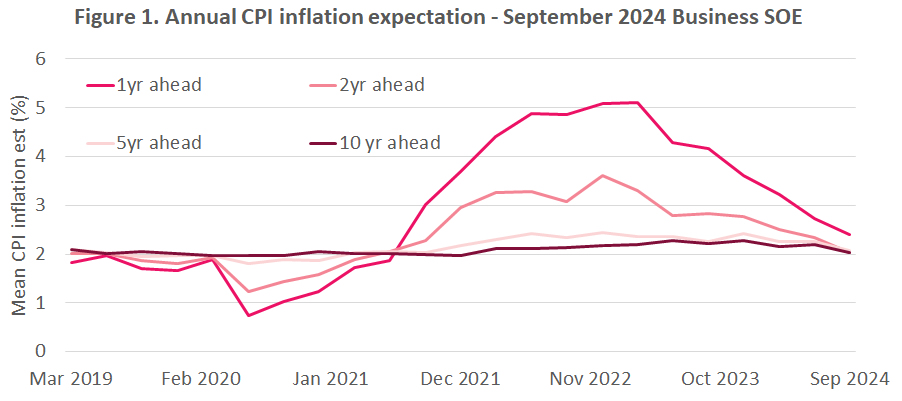

RBNZ inflation expectations drop across all horizons

RBNZ latest Survey of Expectations showed a notable decline in inflation expectations across all time horizons. One-year-ahead annual inflation expectations fell by 33 basis points, dropping from 2.73% to 2.40%. This marks the sixth consecutive quarterly decline since June 2023.

The two-year-ahead inflation expectations, a closely monitored indicator, also saw a decrease from 2.33% to 2.03%. These expectations are now below the average level observed since 2002, indicating a substantial shift in business outlook regarding future inflation.

Long-term expectations followed a similar trend. Five-year-ahead inflation expectations decreased to 2.07%, while ten-year-ahead expectations dropped to 2.03%.

Survey respondents also provided their outlook on the OCR. On average, they expect OCR to be 5.40% by the end of the September 2024 quarter, with a projected decrease to 4.24% by the end of June 2025. The current OCR stands at 5.50%.

BoC minutes reveal clear consensus for further rate cuts

BoC's Summary of Deliberations from its July meeting indicates a "clear consensus" on the need for more rate cuts if inflation continues to ease. With inflation "closer to target" and "downside risks" becoming "more prominent," members agreed that it would be appropriate to "lower the policy rate further" if inflation follows the projected path.

During the meeting, members discussed various risks to the inflation outlook. The focus was on "downside risks" more than in previous meetings. Members acknowledged that weak consumer sentiment is likely to persist, posing a risk that consumer spending could be "significantly weaker" than expected in 2025 and 2026. Additionally, further labor market weakness could "delay the rebound" in consumption, exerting "downward pressure on growth and inflation."

Conversely, some members highlighted the "stickiness of services price inflation," which could keep inflation elevated. They noted that price pressures in services, which are "more closely affected by wages," are unlikely to be offset by the disinflation seen in goods and other services in recent months.

Looking ahead

The European economic calendar is empty. US will release jobless claims and wholesale inventories final.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9321; (P) 0.9395; (R1) 0.9488; More....

EUR/CHF's recovery from 0.9209 extended higher but upside is capped below 0.9476 support turned resistance. Intraday bias remains neutral and further decline is still expected. On the downside, below 0.9333 minor support will bring retest of 0.9209 first. Firm break there will resume larger fall from 0.9928 to 161.8% projection of 0.9928 to 0.94767 from 0.9772 at 0.9041 next. However, sustained break of 0.9476 will turn bias back to the upside for stronger rebound.

In the bigger picture, current downside acceleration argues that medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Bank Lending Y/Y Jul | 3.20% | 3.20% | 3.20% | |

| 23:50 | JPY | Current Account (JPY) Jun | 1.78T | 2.29T | 2.41T | |

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q3 | 2.03% | 2.33% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Jul | 47.5 | 47.8 | 47 | |

| 12:30 | USD | Initial Jobless Claims (Aug 2) | 245K | 249K | ||

| 14:00 | USD | Wholesale Inventories Jun F | 0.20% | 0.20% | ||

| 14:30 | USD | Natural Gas Storage | 22B | 18B |

Elliott Wave Intraday Analysis on Silver (XAGUSD) Looking to Find Buyers

Short Term Elliott Wave View in Silver (XAGUSD) suggests that pullback to 28.58 low ended a wave (A). The metal turned higher again in wave (B) ended at 31.75 high. The market resuming lower from wave (B) high breaking below 28.58 low to rule a larger correction. It means, Silver is developing a wave (C) of ((4)) as a zig zag Elliott Wave structure. Down from wave (B), wave ((i)) ended at 28.65 and wave ((ii)) ended at 29.45. Wave ((iii)) lower ended at 27.40, and pullback in wave ((iv)) ended at 28.19. Wave ((v)) ended at 27.29 which completed wave 1. Pullback in wave 2 ended at 29.22 high and the metal resumed lower in wave 3.

Down from wave 2, wave ((i)) ended at 27.93 and wave ((ii)) ended at 28.67. Wave ((iii)) lower ended at 26.49, and pullback in wave ((iv)) built a triangle structure ended at 27.16. Currently, silver is trading in wave ((v)) of 3. We are calling for one more low to end the cycle. The ideal place to end this wave comes in 26.32 – 26.06 area, where buyers should appear to start wave 4 pullback. Near term, as far as pivot at 29.22 high stays intact, expect pullback as wave 4 to fail in 3, 7 or 11 swing for further downside in wave 5 of (C).

Silver (XAGUSD) 60 Minutes Elliott Wave Chart

XAGUSD (Silver) Elliott Wave Video

https://www.youtube.com/watch?v=u7DW69XZtm0

RBNZ inflation expectations drop across all horizons

RBNZ latest Survey of Expectations showed a notable decline in inflation expectations across all time horizons. One-year-ahead annual inflation expectations fell by 33 basis points, dropping from 2.73% to 2.40%. This marks the sixth consecutive quarterly decline since June 2023.

The two-year-ahead inflation expectations, a closely monitored indicator, also saw a decrease from 2.33% to 2.03%. These expectations are now below the average level observed since 2002, indicating a substantial shift in business outlook regarding future inflation.

Long-term expectations followed a similar trend. Five-year-ahead inflation expectations decreased to 2.07%, while ten-year-ahead expectations dropped to 2.03%.

Survey respondents also provided their outlook on the OCR. On average, they expect OCR to be 5.40% by the end of the September 2024 quarter, with a projected decrease to 4.24% by the end of June 2025. The current OCR stands at 5.50%.