Sample Category Title

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6699; (P) 1.6785; (R1) 1.6859; More...

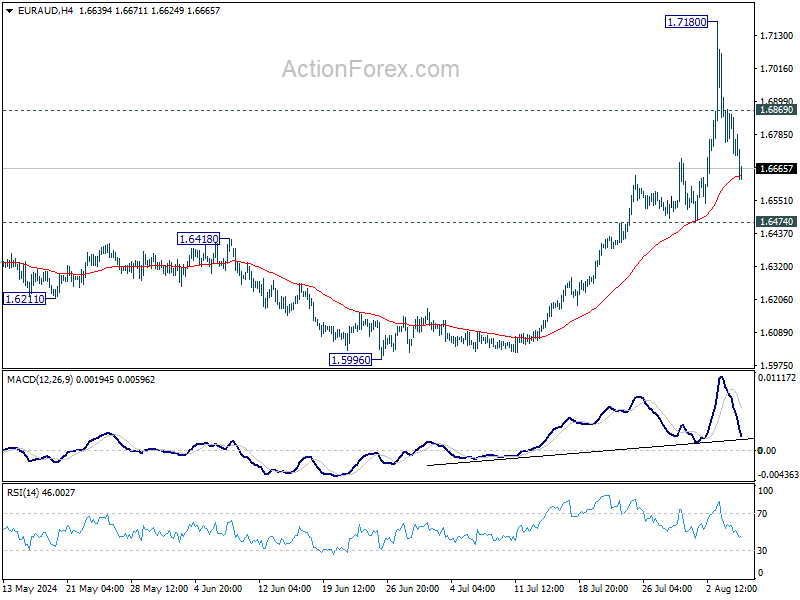

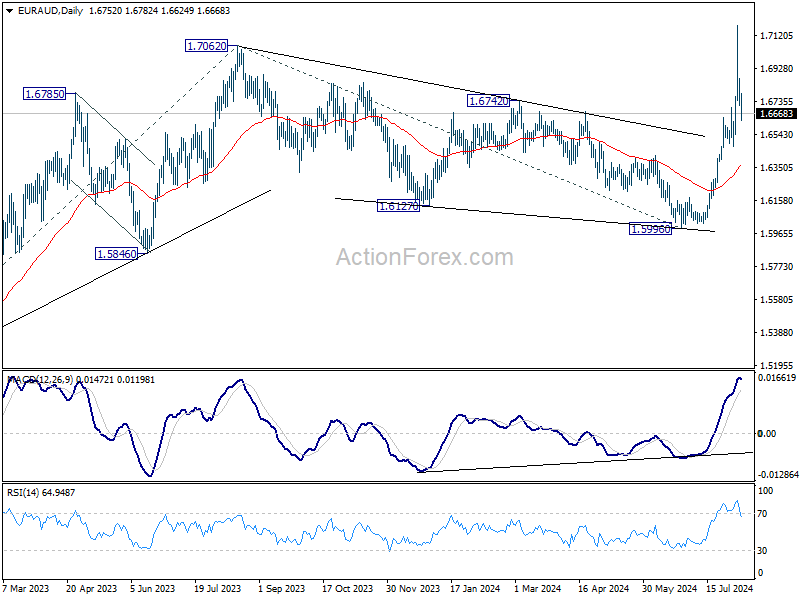

EUR/AUD's retreat from 1.7180 extends lower today but stays well above 1.6474 support. Intraday bias remains neutral first and further rally is still in favor. On the upside, above 1.6869 minor resistance will turn bias back to the upside for retesting 1.7180. Firm break there will resume larger up trend to 1.7715 fibonacci projection level next.

In the bigger picture, decisive break of 1.7062 resistance will confirm resumption of whole up trend from 1. 1.4281 (2022 low). Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. For now, further rally is expected as long as 55 D EMA (now at 1.6355) support holds, even in case of deep retreat.

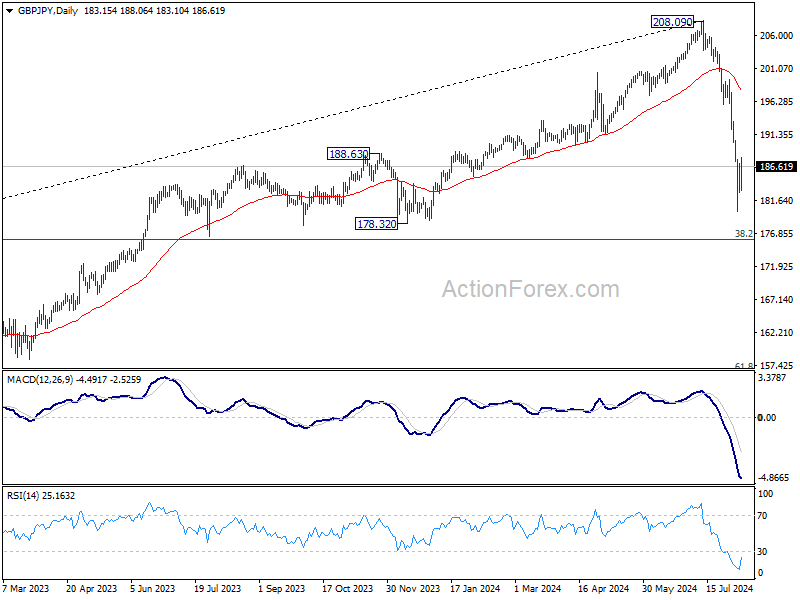

GBP/JPY Daily Outlook

Daily Pivots: (S1) 181.68; (P) 184.38; (R1) 185.95; More...

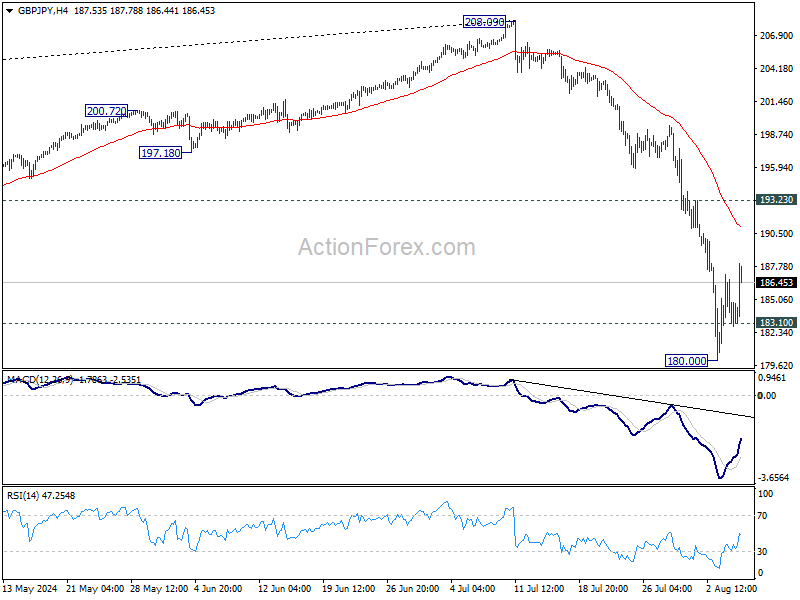

GBP/JPY's recovery from 180.00 extends higher today but stays well below 193.23 resistance. Intraday bias remains neutral first and further decline is in favor. On the downside, below 183.10 minor support will bring retest of 180.00 first. Break there will resume the fall from 208.09 to 178.32 support next.

In the bigger picture, fall from 208.09 medium term top is seen as correcting the up trend from 123.94 (2020 low). Deeper decline is in favor as long as 55 W EMA (now at 189.31) holds. But strong support could emerge between 178.32 and 38.2% retracement of 123.94 to 208.09 at 175.94 to bring rebound. Meanwhile, sustained trading above 55 W EMA will suggest that the range for the medium term corrective pattern is already set.

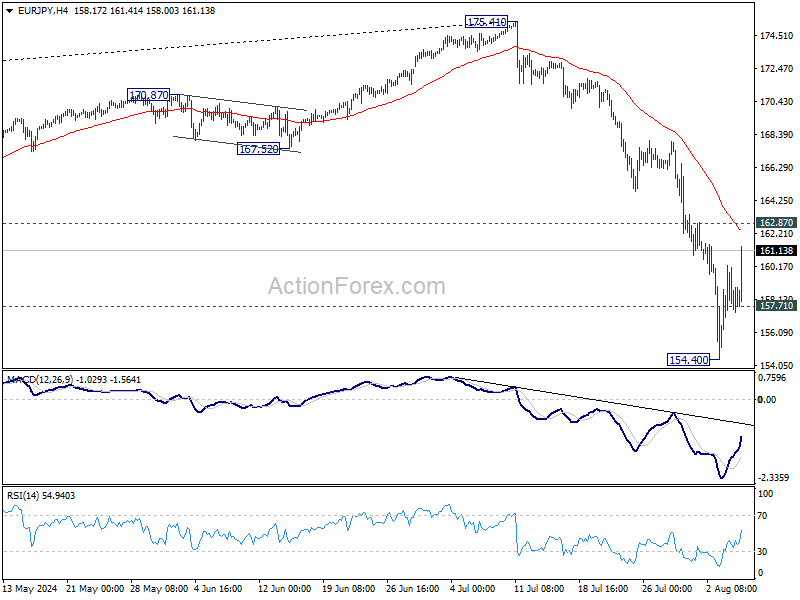

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.66; (P) 158.45; (R1) 159.60; More...

EUR/JPY's recovery from 154.40 extends higher today but stays below 162.87 resistance. Intraday bias remains neutral at this point, and further fall is expected. On the downside, below 157.71 minor support will turn bias back to the downside. Break of 154.40 will resume the fall from 175.41 to 153.15 support next. However, decisive break of 162.87 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper fall could be seen as long as 55 W EMA (now at 161.79) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound (at least on first attempt). Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

NZD Rallies on Strong Q2 Employment Data; JPY Sinks Amid BoJ Caution

New Zealand Dollar surged strongly today following much better than expected Q2 employment data.. Speculations of an early rate cut by RBNZ next week now seem exaggerated. Major banks still expect RBNZ to start easing monetary policy this year, with consensus pointing to the November meeting. However, there's still a possibility that RBNZ could signal a shift towards an easing bias in its upcoming meeting.

In contrast, Yen plummeted broadly after comments from BoJ Deputy Governor Shinichi Uchida. Uchida highlighted significant concerns over recent extreme volatility in global financial markets and acknowledged the strong rebound in Yen's exchange rate. These factors are affecting economic and price developments, leading Uchida to rule out another rate hike in the near term.

For today, Kiwi is the strongest performer, followed by Aussie and Sterling. Yen is the weakest, trailed by Swiss Franc and Euro. Dollar and Loonie are in the middle.

As for the week so far, Kiwi also leads as the strongest currency, followed by Loonie and Aussie. Sterling is the weakest, followed by Yen and Swiss Franc. Dollar and Euro position in the middle of the pack.

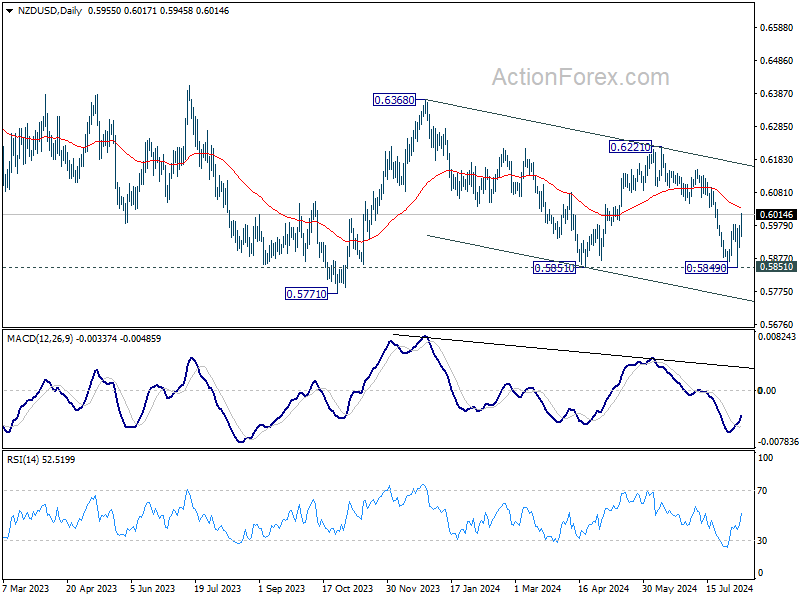

Technically, NZD/USD's extended rebound today confirms short term bottoming at 0.5849, after hitting 0.5851 support. Stronger rise could be seen to 55 D EMA (now at 0.6032) and possibly above. However, firm break of channel resistance (now at 0.6174) is needed to confirm completion of the decline from 0.6368. Otherwise, risk will stay on the downside for another fall through 0.5849/51 to 0.5771 at a later stage.

In Asia, at the time of writing, Nikkei is up 2.74%. Hong Kong HSI is up 1.31%. China Shanghai SSE is up 0.31%. Singapore Strait Times is up 1.26%. Japan 10-year JGB yield is down -0.0229 at 0.864. Overnight, DOW rose 0.76%. S&P 500 rose 1.04%. NASDAQ rose 1.03%. 10-year yield rose 0.103 to 3.888.

BoJ's Uchida: To keep interest rate for the time being due to extreme global market volatility

In a speech today, BoJ Deputy Governor Shinichi Uchida emphasized the necessity of maintaining monetary easing with the current policy interest rate "for the time being", citing "extremely volatile" recent developments in both Japanese and global financial and capital markets. Uchida assured that BoJ is monitoring these developments with "utmost vigilance" and will adjust monetary policy as appropriate.

Uchida reiterated that if the outlook for economic activity and prices is realized, BoJ would "continue to raise the policy interest rate." Howeer, he noted that "significant movements in stock prices and foreign exchange rates since last week" are particularly relevant in shaping this outlook.

Furthermore, Uchida pointed out that the recent correction in Yen's depreciation has reduced the "upside risk to prices arising from higher import prices." This adjustment in Yen's value "affects the conduct of monetary policy."

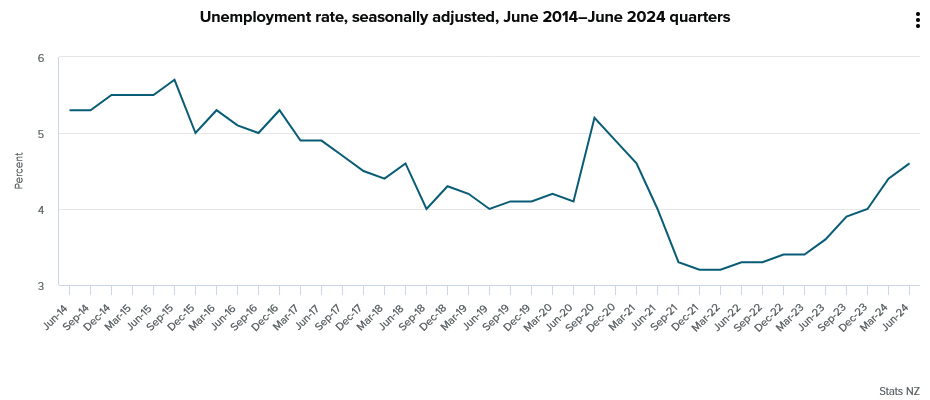

New Zealand employment grows 0.4% in Q2, above expectations

New Zealand's employment data for Q2 showed unexpected strength, with employment growing by 0.4%, defying expectations of a -0.3% contraction. However, the unemployment rate increased from 4.4% to 4.6%, which was still better than the anticipated 4.7%. The labor force participation rate also saw a modest rise of 0.2% to 71.7%, while the employment rate remained steady at 68.4%.

All sector wage inflation was recorded at 1.2% qoq and 4.3% yoy. Private sector wage inflation stood at 0.9% qoq and 3.6% yoy. The public sector saw higher wage inflation at 1.8% qoq and 6.9% yoy, with the annual rate hitting a series high.

China's exports grow 7.0% yoy in Jul, imports rises 7.2% yoy

China's export growth for July came in at 7.0% yoy, falling short of the expected 9.7% yoy increase. Exports to the US and EU each grew by about 8% yoy, while exports to ASEAN countries surged by 12% yoy.

Imports, on the other hand, rose by 7.2% yoy, exceeding the expected 3.5% growth. Notably, imports from the US surged by 24% yoy, imports from ASEAN countries increased by 11% yoy, and imports from the EU climbed by 7% yoy.

As a result, China's trade surplus narrowed from USD 99.1B to USD 84.6B, which was smaller than the expected USD 99.2B.

Looking ahead

Germany industiral production and trade balnace, France trade balance and Swiss foreign currency reserves will be released in European session. Later in the day, Canada will release Ivey PMI and BoC summery of deliberations.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.66; (P) 158.45; (R1) 159.60; More...

EUR/JPY's recovery from 154.40 extends higher today but stays below 162.87 resistance. Intraday bias remains neutral at this point, and further fall is expected. On the downside, below 157.71 minor support will turn bias back to the downside. Break of 154.40 will resume the fall from 175.41 to 153.15 support next. However, decisive break of 162.87 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper fall could be seen as long as 55 W EMA (now at 161.79) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound (at least on first attempt). Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Employment Change Q2 | 0.40% | -0.30% | -0.20% | -0.30% |

| 22:45 | NZD | Unemployment Rate Q2 | 4.60% | 4.70% | 4.30% | 4.40% |

| 22:45 | NZD | Labour Cost Index Q/Q Q2 | 0.90% | 0.80% | 0.80% | |

| 03:00 | CNY | Trade Balance (USD) Jul | 84.7B | 99.2B | 99.1B | |

| 05:00 | JPY | Leading Economic Index Jun P | 109.3 | 111.2 | ||

| 06:00 | EUR | Germany Industrial Production M/M Jun | 1.00% | -2.50% | ||

| 06:00 | EUR | Germany Trade Balance Jun | 21.5B | 24.9B | ||

| 06:45 | EUR | France Trade Balance (EUR) Jun | -7.5B | -8.0B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jul | 711B | |||

| 14:00 | CAD | Ivey PMI Jul | 62 | 62.5 | ||

| 14:30 | USD | Crude Oil Inventories | -1.6M | -3.4M | ||

| 17:30 | CAD | BoC Summary of Deliberations |

BoJ’s Uchida: To keep interest rate for the time being due to extreme global market volatility

In a speech today, BoJ Deputy Governor Shinichi Uchida emphasized the necessity of maintaining monetary easing with the current policy interest rate "for the time being", citing "extremely volatile" recent developments in both Japanese and global financial and capital markets. Uchida assured that BoJ is monitoring these developments with "utmost vigilance" and will adjust monetary policy as appropriate.

Uchida reiterated that if the outlook for economic activity and prices is realized, BoJ would "continue to raise the policy interest rate." Howeer, he noted that "significant movements in stock prices and foreign exchange rates since last week" are particularly relevant in shaping this outlook.

Furthermore, Uchida pointed out that the recent correction in Yen's depreciation has reduced the "upside risk to prices arising from higher import prices." This adjustment in Yen's value "affects the conduct of monetary policy."

China’s exports grow 7.0% yoy in Jul, imports rises 7.2% yoy

China's export growth for July came in at 7.0% yoy, falling short of the expected 9.7% yoy increase. Exports to the US and EU each grew by about 8% yoy, while exports to ASEAN countries surged by 12% yoy.

Imports, on the other hand, rose by 7.2% yoy, exceeding the expected 3.5% growth. Notably, imports from the US surged by 24% yoy, imports from ASEAN countries increased by 11% yoy, and imports from the EU climbed by 7% yoy.

As a result, China's trade surplus narrowed from USD 99.1B to USD 84.6B, which was smaller than the expected USD 99.2B.

New Zealand employment grows 0.4% in Q2, above expectations

New Zealand's employment data for Q2 showed unexpected strength, with employment growing by 0.4%, defying expectations of a -0.3% contraction. However, the unemployment rate increased from 4.4% to 4.6%, which was still better than the anticipated 4.7%. The labor force participation rate also saw a modest rise of 0.2% to 71.7%, while the employment rate remained steady at 68.4%.

All sector wage inflation was recorded at 1.2% qoq and 4.3% yoy. Private sector wage inflation stood at 0.9% qoq and 3.6% yoy. The public sector saw higher wage inflation at 1.8% qoq and 6.9% yoy, with the annual rate hitting a series high.

NZ First Impressions: Labour Market Surveys, Q2 2024

The New Zealand labour market is softening, but wage growth remains on the high side, partly supported by government pay agreements.

- Unemployment rate: 4.6% (prev: 4.4%, Westpac f/c: 4.7%, RBNZ f/c 4.6%)

- Employment change (quarterly): +0.4% (prev: -0.3%, Westpac f/c: -0.4%, RBNZ f/c +0.1%)

- Labour costs (private sector, quarterly): +0.9% (prev: +0.8%, Westpac f/c: +0.7%, RBNZ f/c +0.9%)

- Average hourly earnings (private sector, ordinary time quarterly): +1.4% (prev: +0.2%)

New Zealand’s labour market has continued to soften in broadly the manner that the Reserve Bank was expecting. Unemployment is steadily ticking higher, despite some volatility in the underlying figures. Less helpful for the RBNZ is that wage inflation remains uncomfortably high on the face of it, though this is more concentrated in sectors where government pay agreements are still taking effect.

The unemployment rate rose to 4.6% for the June quarter, slightly less than market predictions, but in line with the Reserve Bank’s most recent forecast. The March quarter was revised up slightly from 4.3% to 4.4% (as we noted in our preview, it was already extremely close to 4.4% before rounding). The unemployment rate is now at its highest level since March 2021.

As often happens with the Household Labour Force Survey (HLFS), there were some offsetting surprises in the details that don’t change our overall view. The number of people employed rose by 0.4% for the quarter, well above our estimate of a 0.4% decline. This was accompanied by a pickup in the labour force participation rate from 71.6% to 71.7%, the first increase in a year.

Our forecast was based on the Monthly Employment Indicator (MEI), which saw a steady decline in the number of filled jobs over the quarter. As we noted in our preview, the MEI is a comprehensive record drawn from income tax data, so to the extent that there is a divergence between this and the HLFS, it’s most likely to be due to sampling error in the latter. Indeed, the two had diverged in the opposite direction in the previous quarter, with the MEI recording a rise in jobs against a 0.3% decline in the HLFS. There was always a risk that we could see some payback in the June quarter, though it wasn’t our forecast (it hasn’t reliably behaved this way in the past).

We’re more inclined to believe the weak MEI jobs numbers, given that they are supported by other evidence. The Quarterly Employment Survey (QES) recorded a 0.5% fall in filled jobs and a 0.9% fall in hours paid, following gains in the previous quarter. And the HLFS itself recorded a whopping 1.2% fall in hours worked – consistent with our recent forecast that June quarter GDP will be particularly weak.

The Labour Cost Index (LCI) rose by 1.1% for all sectors in the June quarter, which actually lifted the annual growth rate up again from 4.1% to 4.2%. That included a whopping 1.9% rise in the public sector for the quarter; the private sector measure rose by 0.9%, albeit still above our forecast of 0.7%.

The wage figures were affected by pay increases in the health and education sectors, which had been previously agreed and were implemented in stages. We noted these in our preview, but we didn’t have a strong sense of how large an impact they would have – and it has clearly been on the higher side. These pay agreements boosted the public sector measure in particular, but also lifted the private sector measure to some degree (there are many providers that are privately owned but publicly funded). As a rough and ready guide, we estimate that labour costs excluding health and education rose by 3.5%yr, similar to the previous quarter.

The unadjusted analytical LCI rose by 1.2% for the private sector, with the annual growth rate slowing from 5.2% to 4.8%. This measure does not adjust for pay increases related to productivity improvements, and is perhaps a better gauge of what workers are actually receiving in hand. Overall it appears that wage inflation is slowing, but it remains above what would be consistent with the RBNZ’s 2% target midpoint.

Overall, there were no real surprises for the RBNZ in these surveys. That in itself is likely to be a disappointment for financial markets, which we suspect were looking for a result that would validate their pricing for an OCR cut at next week’s Monetary Policy Statement.

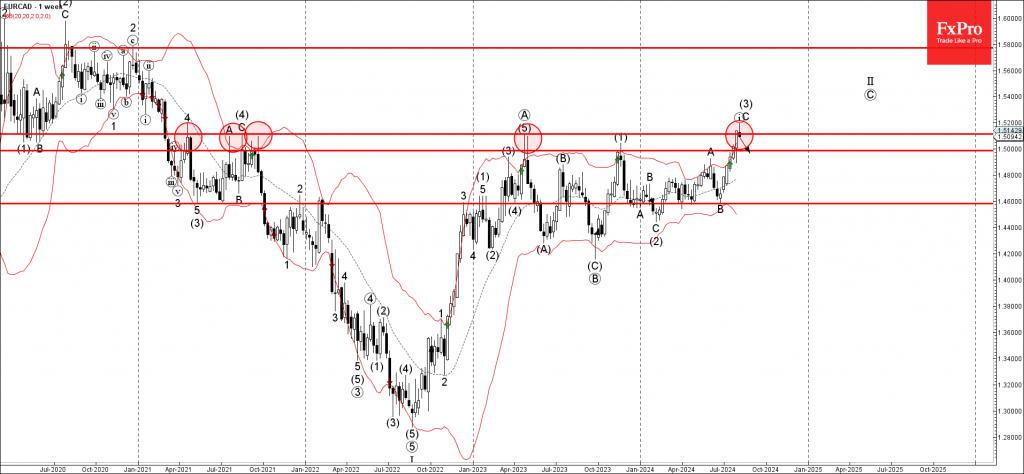

EURCAD Wave Analysis

- EURCAD reversed from resistance level 1.5110

- Likely to fall to support level 1.5000

EURCAD currency pair recently reversed down from the long-term resistance level 1.5110 (which has been reversing the price from the start of 2011), standing close to the upper weekly Bollinger Band.

The downward reversal from the resistance level 1.5110 created the weekly Japanese candlesticks reversal pattern Shooting Star.

Given the strength of the resistance level 1.5110 and the overbought daily Stochastic, EURCAD currency pair can be expected to fall further toward the next round support level 1.5000 (former resistance from the end of 2023).

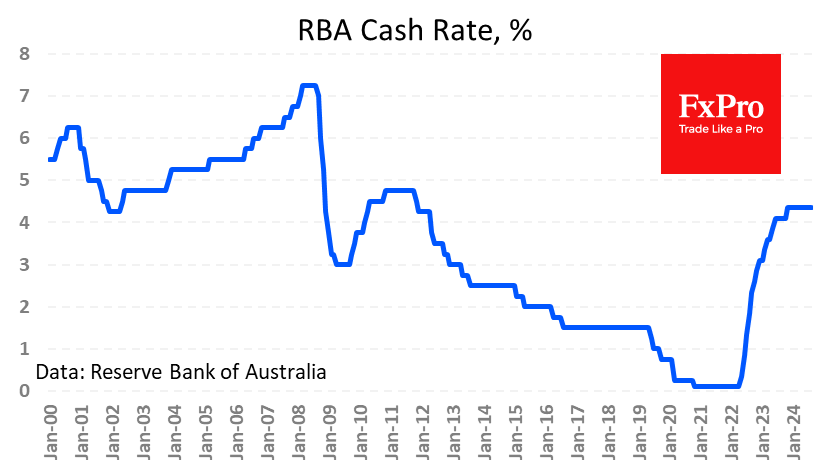

A Hawkish RBA Could be a Role Model for Other G10 Banks

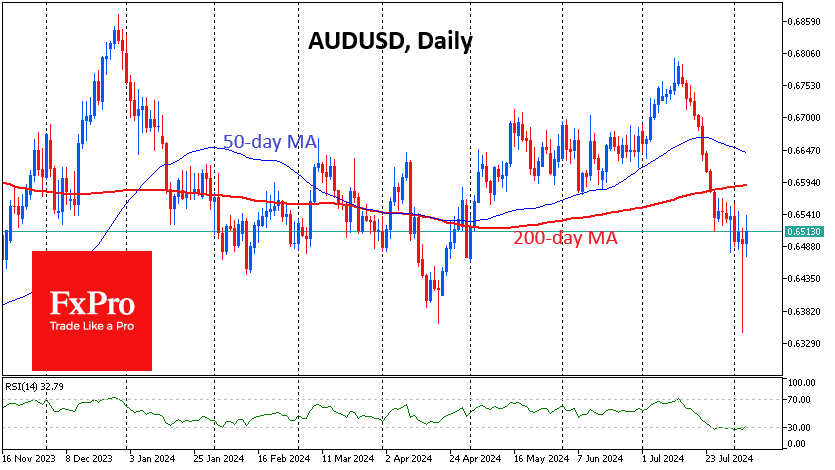

The Reserve Bank of Australia kept its cash rate on hold at a 12-year high of 4.35%, as widely expected by markets. In a statement along with the decision, the RBA noted that inflation is still well above its target range of 2-3%. Price growth has stabilised in the 3.5-4.0% range since December last year, most recently at 3.8%, with some acceleration in the second quarter. The latest producer price indices (+4.8% y/y) and a surprise in import prices (+1% q/q vs. -0.9% expected) pose upside risks to final prices.

The RBA remains focused on fighting inflation, a sentiment supported by an acceleration in consumer credit and relatively stable retail sales to push aside a slowdown in construction.

The RBA does not appear spooked by the recent sell-off and is not prepared to ease monetary conditions. This is positive news for the Aussie and is helping AUDUSD continue to fight for support at 0.6500, having overcome Monday’s more than 2% drop with a margin of safety. There is also a smooth RSI over-sold exit forming on the daily timeframe, signalling the potential for a bounce or reversal to the upside.

However, the pair is reluctant to gain strength without support from the global markets, where broad but multidirectional movements prevail.