Sample Category Title

JP 225 Index Tries to Find Footing After 20% Crash

- JP 225 index plummets to 10-month low amid global stock meltdown

- Oversold signals detected; but bulls could show up above 33,585

Japan’s 225 stock index (cash) started the month on the wrong foot, sinking by a massive 21% to a 10-month low of 30,361 in the wake of recession fears in the US and as the bruised yen finally entered a bullish cycle.

Technically, the index suffered its sharpest correction below its 200-day simple moving average (SMA) since the pandemic, reaching the lows from October 2023 before closing the day around 33,336. The latter overlaps with the 161.8% Fibonacci extension of the April-July upleg, which is currently buffering downside pressures.

However, for the index to run towards the 35,470 barrier, the price might first need to overcome the nearby resistance line at 33,585. Even higher, April’s low of 36,692 and the 200-day SMA could block the way towards the 38,000 psychological mark.

According to the RSI and the stochastic oscillator, the market is hovering near oversold levels. Hence, the bears could soon get exhausted. Nevertheless, a close below the 33,130 region could postpone any recovering attempts, shifting the spotlight towards the ascending trendline which connects the 2020 and 2023 lows at 31,400, although the line was unable to stop Monday’s freefall. If selling forces persist, the price might revisit the October double bottom area of 30,300. The 29,300 region could be the next pivot point.

In brief, Japan’s 225 index erased all its progress from late 2023 in short-period of time and some recovery could be justified given the oversold signals. Still, selling interest may not evaporate in the coming sessions, unless the price manages to step above 33,585.

Gold (XAU/USD) Steadies After Volatile Monday; DXY Bounces Back

- Gold prices rebounded above $2,400/oz after a dip to $2,364/oz, showing resilience despite a strengthening US Dollar.

- Gold benefits from expectations of more aggressive rate cuts and its safe-haven status.

- Geopolitical and economic risks in the second half of 2024, along with anticipated rate cuts, should theoretically support the gold rally, but a Middle East peace agreement could complicate the outlook.

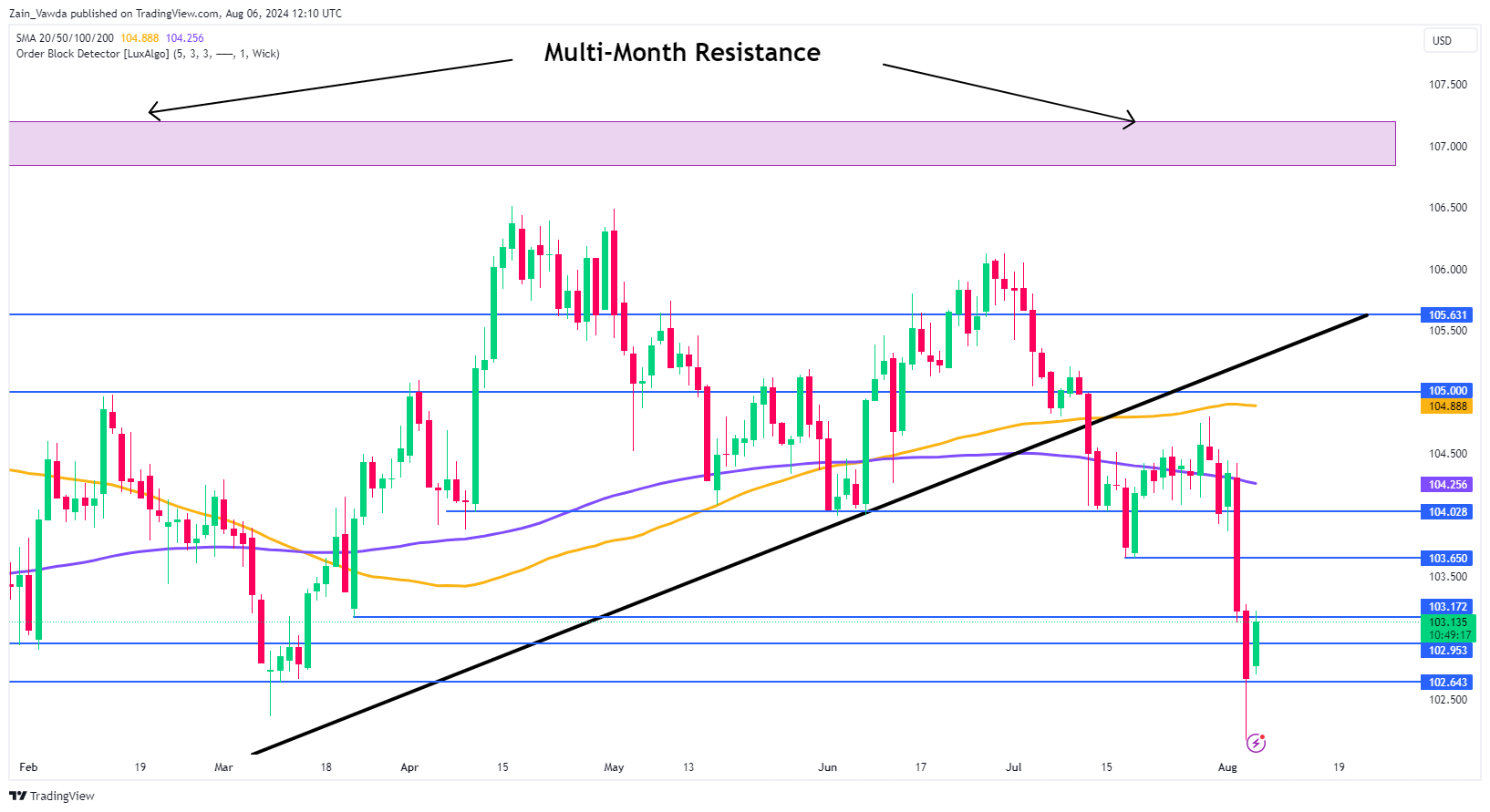

Gold prices bounced back robustly yesterday following a selloff that saw the precious metal dip to around $2,364/oz. Since then, gold has rallied back above the $2,400/oz mark and continues to consolidate above this level.

The resilience of gold and sustained buying interest are evident, even with the US Dollar strengthening significantly in European trade this morning. Despite the rise in the DXY, gold prices have remained largely unaffected.

The notion of the Dollar’s demise as a safe-haven asset might be premature, given the increasing geopolitical risks. Today’s bounce in the Dollar comes amid heightened tensions in the Middle East, suggesting that the US Dollar may still retain some of its haven appeal despite ongoing recessionary concerns.

On the chart, the DXY found support around the key 102.00 level yesterday.

A rally has since followed, but the DXY is now encountering its first resistance at approximately 103.200, with further resistance ahead at 103.60. Conversely, a push to the downside from this point could lead Gold to revisit recent lows, but this would require a daily candle close below 102.60 for it to materialize.

US Dollar Index Daily Chat, July 25, 2024

Source:TradingView.com

Support

- 2400

- 2392

- 2364

Resistance

- 2420

- 2450

- 2470

Gold is benefitting from expectations of more aggressive rate cuts, along with its safe-haven appeal. Moving forward, gold could return to the rangebound behavior observed frequently in 2024.

The second half of the year presents numerous risks, both geopolitical and economic. These, coupled with anticipated interest rate cuts, should theoretically sustain the gold rally. However, a peace agreement in the Middle East could complicate the outlook, necessitating a reassessment of gold’s medium-term direction at the very least.

Economic Data, US Earnings and Geopolitics to Drive Sentiment

Data is sparse for the US this week and thus the geopolitics and US earnings may be the driving force of sentiment as well.

Among the big names on the earnings front this week, we have Occidental Petroleum and Disney reporting tomorrow among a host of other names.

Source: Earnings Hub

Technical Analysis Gold (XAU/USD)

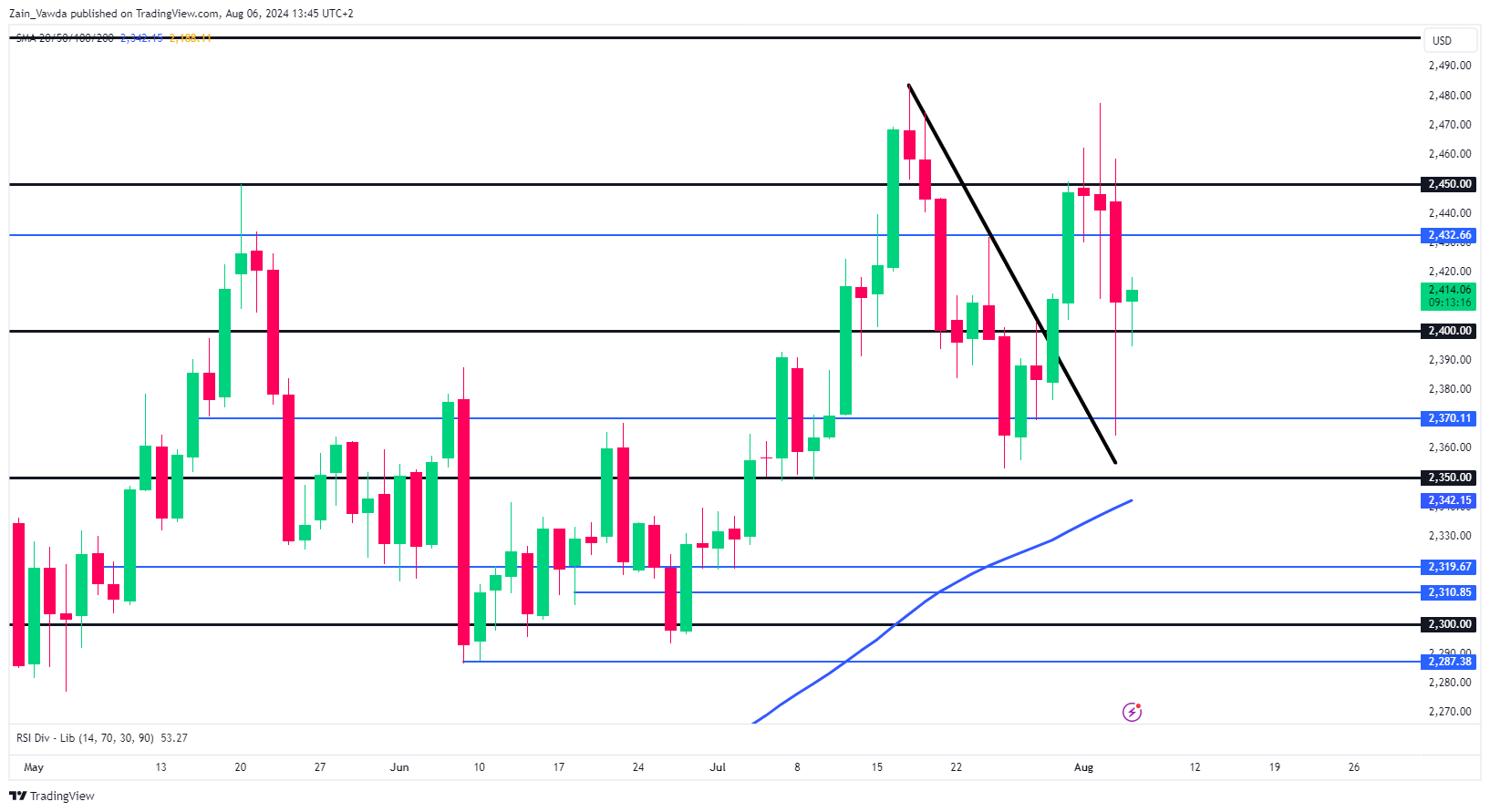

From a technical standpoint, gold made an impressive recovery during the US session yesterday, leaving markets puzzled by its earlier selloff.

This rebound positions the precious metal for potential further gains. Immediate support at $2,400 is crucial; a daily candle close below this level could signal sustained downside pressure. The key question remains whether this will be counterbalanced by gold’s safe-haven appeal.

GOLD (XAU/USD) Chart, August 6, 2024

Source: TradingView (click to enlarge)

Support

- 2400

- 2392

- 2370

Resistance

- 2420

- 2450

- 2470

Canada’s Trade Position Swings to a Surplus in June

Canada’s merchandise trade balance moved sharply into surplus territory in June after three months in deficit. June's surplus registered at $638 million, with last month's deficit being revised slightly lower to $1.6 billion.

Merchandise exports increased by a hefty 5.5% in June, pulling the value of goods exported to the highest level since January 2023. Increases were broad-based, with shipments up in 9 of 11 sectors. Leading the charge was a 13.3% month-on-month (m/m) increase in crude oil shipments helped by the recently completed Trans Mountain pipeline. Exports of metal and non-metallic products also advanced at a healthy 11.8% m/m pace.

Merchandise imports also increase in June, but by a smaller amount (1.9% m/m). Gains were also broad based as 9 of 11 sectors posted increases, with outsized contributions from a 5.1% m/m increase in passenger cars and light truck imports. Elsewhere, consumer goods imports rose by 3.7% m/m and imports of pharmaceutical goods advanced by 16.9%.

In volume terms, merchandise exports and imports rose by 4.57% and 1.16% m/m, respectively.

Canada's merchandise trade surplus with the United States widened for a third straight month, up to $9.4 billion in June from $8.8 billion the month prior.

Key Implications

Despite robust export activity in June, trade will likely act as a headwind to second quarter GDP growth, as April and May data came in on the weaker end. That being said, the hand-off into next quarter could prove to be significant. The effects of the Trans Mountain pipeline expansion are now flowing through the data, with strong crude oil exports expected in the coming months.

In the Bank of Canada's recently released Monetary Policy Report (MPR), they expect GDP in the third quarter to grow by a sizeable 2.8%, higher than most forecasters expect. While we still have minimal data on how the entire economy is tracking, Q3 trade could add up to 1.0 percentage points (ppts) to headline GDP growth.

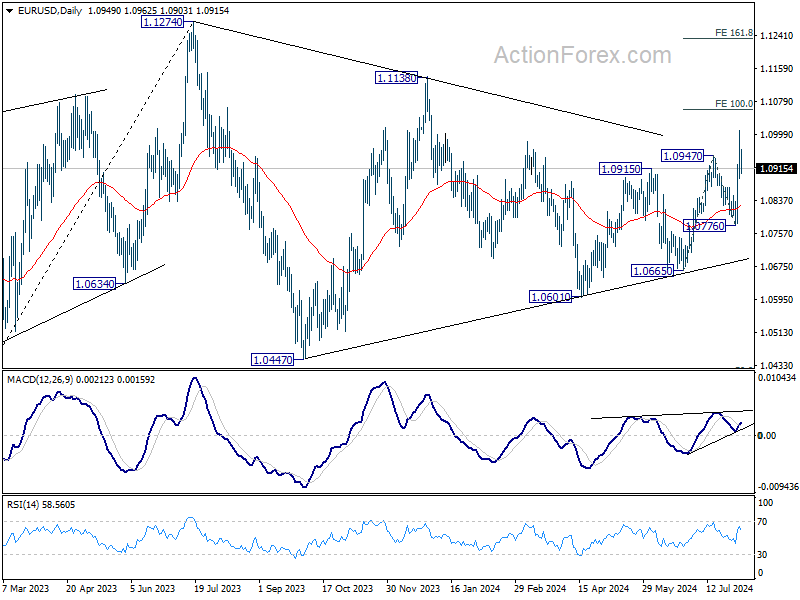

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0893; (P) 1.0951; (R1) 1.1009; More.....

Intraday bias in EUR/USD is turned neutral with break of 1.0932 minor support. Some consolidations would be seen below 1.1007 first. While deeper retreat cannot be ruled out, downside should be contained well above 1.0776 support. On the upside, break of 1.1007 will resume recent rally from 1.0665 to 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1056 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

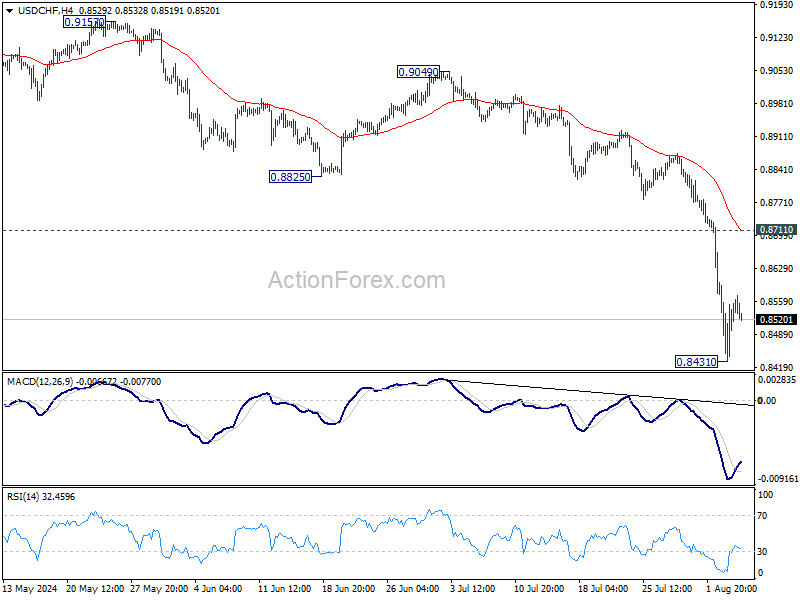

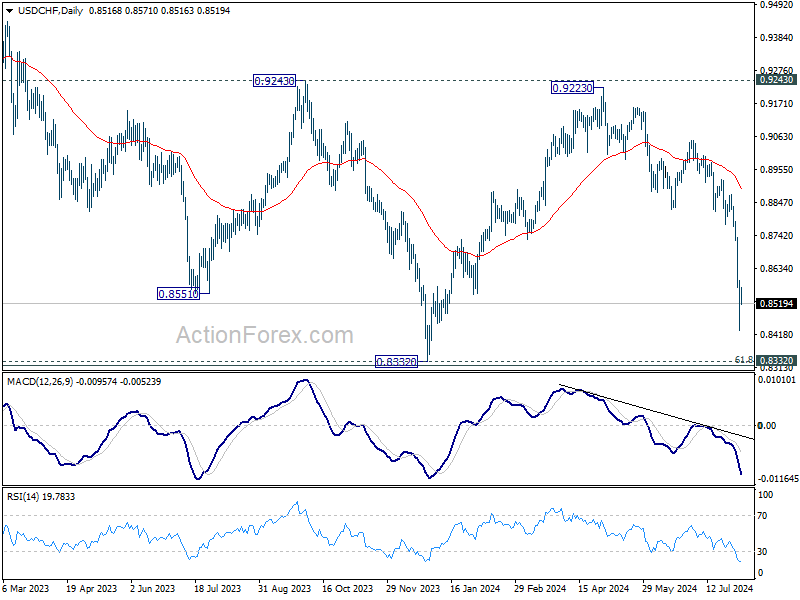

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8437; (P) 0.8520; (R1) 0.8606; More…

Intraday bias in USD/CHF remains neutral for consolidations above 0.8431. Upside of recovery should be limited by 0.8711 resistance to bring another fall. On the downside, below 0.8431 will resume the decline from 0.9223 to retest 0.8332 low.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

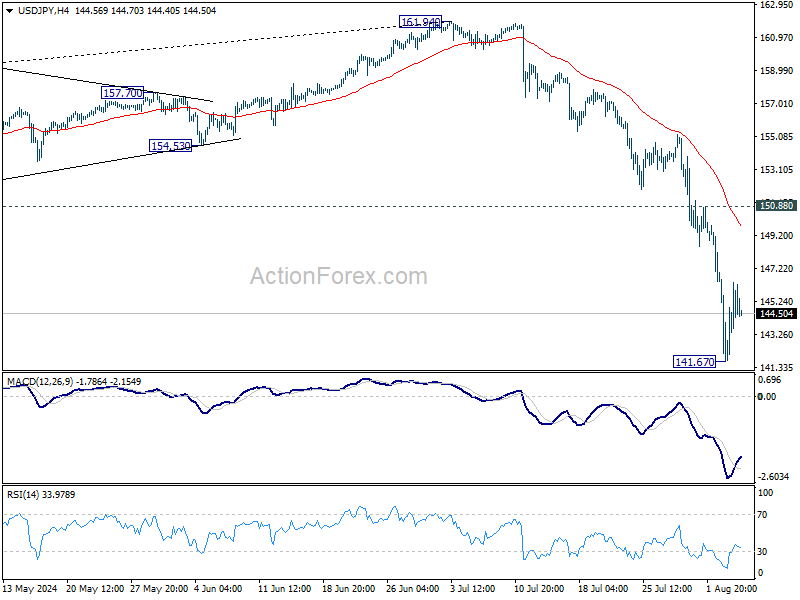

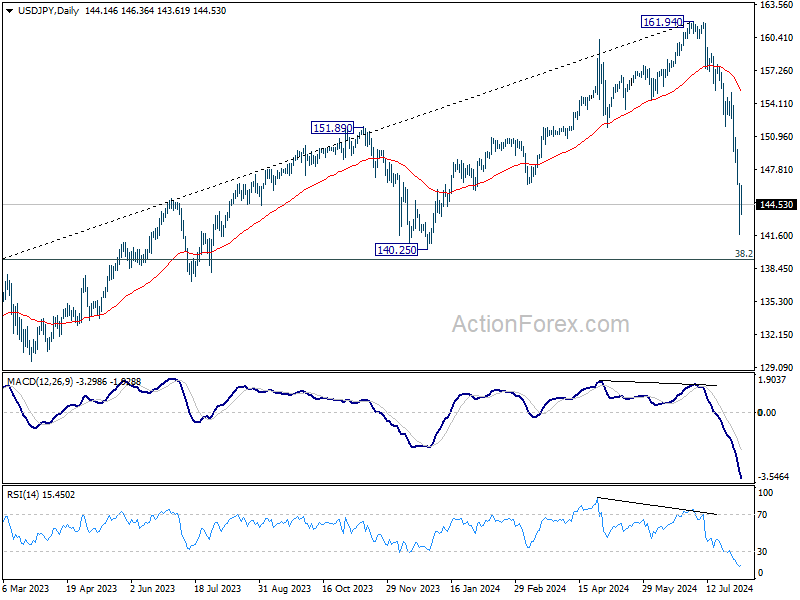

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.68; (P) 144.17; (R1) 146.64; More...

Intraday bias in USD/JPY remains neutral for consolidation above 141.67. Upside of recovery should be limited by 150.88 resistance to bring another fall. On the downside, break of 141.67 will resume the decline from 161.94 to 140.25 support next.

In the bigger picture, the strong break of 55 W EMA (now at 149.98) argue that fall from 161.94 medium term is correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.83) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2719; (P) 1.2769; (R1) 1.2829; More...

GBP/USD's fall from 1.3043 resumed by breaking 1.2706 temporary low and intraday bias is back on the downside for 1.2612 support. Decisive break there should confirm that rise from 1.2298 has completed, and target this support next. For now, risk will remain on the downside as long as 1.2839 resistance holds, in case of recovery.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone even in case of deep decline. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

Dollar Strengthens Mildly Amid Market Calm, Sterling Weakens

Dollar is showing broad but mild strength today as global financial markets stabilize after recent turmoil. The stock market rebound, including a notable 10% surge in the Nikkei, appears to be driven by short covering rather than a sustained recovery. Despite the temporary calm, the risk of another round of sell-offs remains, but with some consolidation likely first in the near term. Canadian Dollar follows as the second strongest performer of the day, with Swiss Franc in third place.

On the other hand, Sterling has emerged as the worst performer, breaking to new lows against greenback despite robust UK PMI construction data. Yen is the second weakest, digesting its recent gains, while Euro is the third weakest. Australian and New Zealand Dollars are positioned in the middle of the performance spectrum.

In particular, Aussie saw no special support from the hawkish rate hold by RBA today. Governor Michele Bullock ruled out a rate cut in the near term, asserting that it "doesn't align with the board's current thinking." This cautious stance is justified by RBA's new economic projections, which anticipate headline inflation rising again after mid-2025. Additionally, underlying inflation is expected to return to the 2-3% target range by late 2025 and approach the midpoint in 2026, reflecting a slower return to target than forecasted in May.

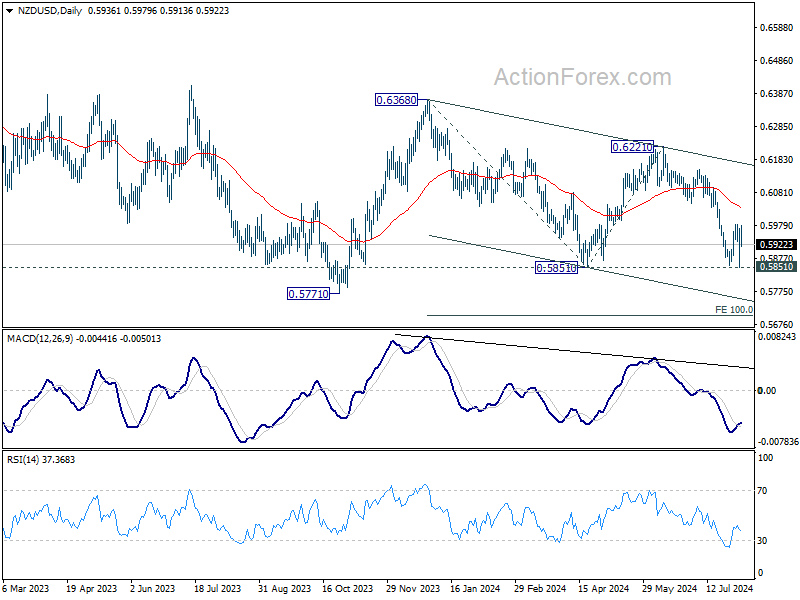

Looking ahead, NZD/USD will be in focus during the upcoming Asian session with the release of New Zealand's employment data. Some economists are predicting that RBNZ might consider lowering interest rates next week, given recent economic indicators pointing to a significant downturn. Activity in the manufacturing and services sectors has slumped further into contraction, and inflation slowed more than expected in Q2. The Q2 job and wage data will be crucial for the policy decision.

Technically, NZD/USD turned into consolidation after failing to break through 0.5851 support. But subsequent rebound was capped well below 55 D EMA. Hence further decline remains in favor. Firm break of 0.5851 will resume the whole fall from 0.6368 to 0.5771 support first, and then 100% projection of 0.6368 to 0.5851 from 0.6221 at 0.5704.

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -0.51%. CAC is down -0.97%. UK 10-year yield is down -0.0003 at 3.867. Germany 10-year yield is down -0.0034 at 2.154. Earlier in Asia, Nikkei rose 10.23%. Hong Kong HSI fell -0.31%. China Shanghai SSE rose 0.23%. Singapore Strait Times fell -1.39%. Japan 10-year JGB yield rose 0.140 to 0.894.

Eurozone retail sales falls -0.3% mom in June, EU down -0.1% mom

Eurozone retail sales volume fell -0.3% mom in June, worse than expectation of -0.2% mom. Retail trade decreased for food, drinks, tobacco by -0.7%, and for non-food products (except automotive fuel) by - 0.1%. Retail trade increased increased for automotive fuel in specialised stores by 0.5%.

EU retail sales volume fell -0.1% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were recorded in Croatia (-2.7%), Austria (-2.3%), Latvia and Lithuania (both -1.7%). The highest increases were observed in Romania (+1.8%), Bulgaria (+1.4%) and Denmark (+1.0%).

UK PMI construction jumps to 55.3, paused projects released

UK PMI Construction rose from 52.2 to 55.3 in June, highest reading since May 2022. S&P Global noted that activity rose amid much faster increase in new orders. Employment increased for the third month running. Emerging pressure on supply chains signaled.

Andrew Harker, Economics Director at S&P Global Market Intelligence, said: "The election-related slowdown in growth seen in June proved to be temporary, with the pace of expansion roaring ahead in July. Firms saw the strongest increases in new orders and activity since 2022 as paused projects were released amid reports of improved customer confidence."

RBA maintains cash rate, anticipates inflation resurgence post-mid-2025

RBA kept its cash rate target unchanged at 4.35%, as widely expected. Maintaining its stance of "not ruling anything in or out," the highlighted that underlying inflation "remains too high" and stated it will be "some time yet" before inflation sustainably returns to the target range. The central bank emphasized that monetary policy will need to be "sufficiently restrictive" until the Board is confident that inflation is moving sustainably towards the target range.

In its new economic projections, RBA forecasts headline inflation to briefly dip to 2.8% in June 2025, back in the target range, but expects it to surge above the target in subsequent quarters before falling back to 2.6% by the end of 2026. Meanwhile, growth projections have been generally upgraded.

Details of the new economic projections include:

CPI at:

- 3.0% by the end of 2024, downgraded from the prior 3.8%.

- 3.7% by the end of 2025, upgraded from the previous 2.8%.

- 2.6% by the end of 2026 (new projection).

Trimmed mean CPI at:

- 3.5% by the end of 2024, up from 3.4%.

- 2.9% by the end of 2025, up from 2.8%.

- 2.6% by the end of 2026 (new projection).

Year-average GDP growth in:

- 2024 downgraded from 1.3% to 1.2%.

- 2025 upgraded from 2.1% to 2.5%.

- 2026 projected to be 2.4% (new).

Unemployment rate at:

- 4.3% by the end of 2024, up from the prior 4.2%.

- 4.4% by the end of 2025, up from 4.3%.

- be 4.4% by the end of 2026 (new projection).

Japan's nominal wages surge 4.5% yoy in Jun, outpacing inflation for first time in 27 months

Japan's nominal wages, or average monthly cash earnings, rose by 4.5% yoy in June, significantly exceeding expectations of a 2.3% yoy increase. This marks the 30th consecutive month of wage growth. More importantly, with CPI rising 3.3% yoy in the same month, real wages increased by 1.1% yoy, marking the first gain in 27 months as wage growth finally outpaced inflation.

A Ministry of Health, Labor and Welfare official commented, "We will monitor incoming data closely to see if the trend has really changed as there is a possibility that those firms that paid bonuses in July might have just moved up the timing this year."

Excluding bonuses and non-scheduled payments, average wages climbed 2.3% yoy, while overtime and other allowances rose by 1.3% yoy.

Also released, household spending in June fell by -1.4% yoy, worse than the expected -0.9% yoy decline, marking the second consecutive month of decline following a -1.8% drop yoy in May.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2719; (P) 1.2769; (R1) 1.2829; More...

GBP/USD's fall from 1.3043 resumed by breaking 1.2706 temporary low and intraday bias is back on the downside for 1.2612 support. Decisive break there should confirm that rise from 1.2298 has completed, and target this support next. For now, risk will remain on the downside as long as 1.2839 resistance holds, in case of recovery.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone even in case of deep decline. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | 4.50% | 2.30% | 1.90% | 2.00% |

| 23:30 | JPY | Household Spending Y/Y Jun | -1.40% | -0.90% | -1.80% | |

| 04:30 | AUD | RBA Rate Decision | 4.35% | 4.35% | 4.35% | |

| 05:45 | CHF | Unemployment Rate M/M Jul | 2.50% | 2.50% | 2.40% | |

| 06:00 | EUR | Germany Factory Orders M/M Jun | 3.90% | 0.80% | -1.60% | -1.70% |

| 06:30 | CHF | Real Retail Sales Y/Y Jun | -2.20% | 0.50% | 0.40% | -0.20% |

| 08:30 | GBP | Construction PMI Jul | 55.3 | 51 | 52.2 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Jun | -0.30% | -0.20% | 0.10% | |

| 12:30 | CAD | Trade Balance (CAD) Jun | 0.6B | -2.0B | -1.9B | -1.6B |

| 12:30 | USD | Trade Balance (USD) Jun | -73.1B | -72.5B | -75.1B | -75.0B |

Will BoJ Summary of Opinions Add More Fuel to Yen’s Engines?

- Yen rallies on cocktail of developments

- BoJ Summary could offer more policy clarity

- The report will be published on Wednesday at 23:50 GMT

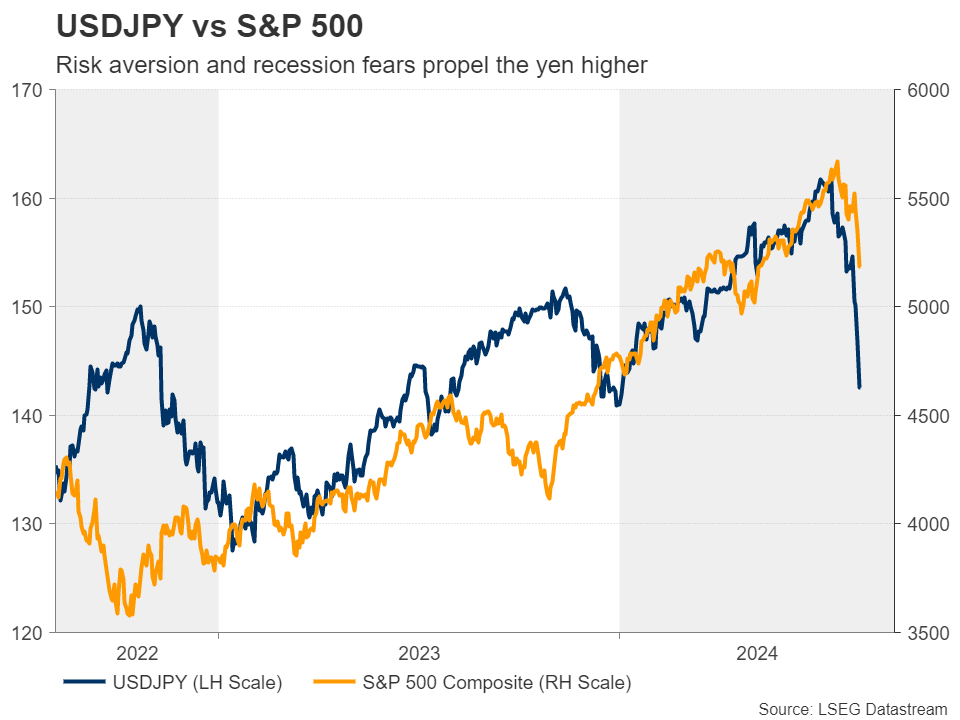

Yen skyrockets more than 12% after intervention

After hitting a 38-year low against its US counterpart on July 3, the Japanese yen entered a consolidative phase and then, on July 11, helped by an intervention episode, it staged an unprecedented recovery, with dollar/yen tumbling as much as 12.5%.

The intervention episode may have prompted market participants to start unwinding profitable carry trades, with the broader risk aversion adding extra fuel to the yen’s engines. The BoJ’s decision to raise interest rates by more than expected last week and the disappointing US employment report for July, which raised recession fears, may have given extra reasons for investors to keep buying the yen.

Traders await Summary of Opinions for hike clues

With all that in mind, attention for yen traders may now fall on the Summary of Opinions of last week’s gathering, due out late on Wednesday, during Thursday’s Asian session. Last week, policymakers decided to raise interest rates by 15bps at a time when market participants were penciling in a slightly more than 50% chance for a 10bps increase. Officials also agreed to taper the pace of their monthly bond purchases, aiming to take it down to around 3 trillion yen by April 2026.

Traders may dig into the summary for clues and hints on how willing policymakers are to continue raising interest rates and how soon they are planning to hit the hike button again.

On Monday, the minutes of the June gathering revealed that nine members called for a rate increase then, underlying the Bank’s policy shift and suggesting that the summary of the July meeting may also have a hawkish flavor, pointing to more rate increases this year.

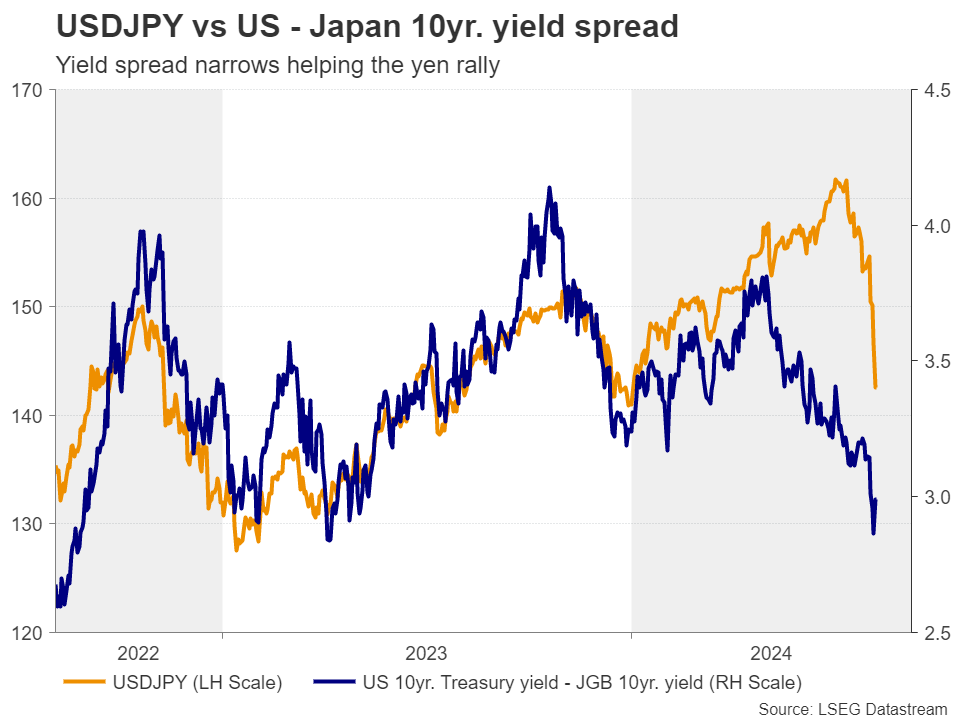

Currently, investors see around a 75% probability for another 10bps hike by the end of the year, though they anticipate no action at the upcoming meeting on September 20. If the Summary of Opinions reveals more-hawkish-than-expected language, with officials clearly favoring more increases, the yen may enjoy more gains as the yield spread between the US and Japanese yields continues to narrow.

Is the rally overstretched?

That said, the tumble in Treasury yields may be overstretched currently, considering that the market has gone as far as pricing in around 125bps worth of reductions this year following Friday’s nonfarm payrolls, which on its own can’t provide a complete picture of the state of the US economy.

The improving ISM non-manufacturing PMI confirmed the notion that any data point suggesting the world’s largest economy is not faring as badly as expected could make investors realize that the number of rate cuts they expect are probably unrealistic. After the PMI, the total number of bps worth of reductions for 2024 dropped to 110. This means that there is the chance of some recovery in dollar/yen before the next leg south.

Dollar/yen to remain bearish even if small rebound occurs

From a technical standpoint, dollar/yen entered a free-fall mode on July 11, but yesterday, it triggered some buy orders near the 141. 60 zone, from which it rebounded and tested the 146.40 area as resistance. The pair is well below its 200-day exponential moving average, which means that even if the recovery continues for a while longer, the bears could still take charge soon.

A drop below 141.60 could initially aim for the 140.20 barrier, the break of which could pave the way towards the low of July 14, 2023, at around 137.10. For the bearish outlook to come into question, the recovery may have to extend all the way above the crossroads of the 200-day EMA and the 152.00 zone.

AUD/USD Remains Under Pressure as RBA Holds Rates

The Australian dollar gained ground earlier but has reversed directions and has edged lower. In the European session, AUD/USD is trading at 0.6778, down 0.24% at the time of writing.

RBA maintains cash rate at 4.35%

The Reserve Bank of Australia held the cash rate at 4.35% for a seventh straight time today. The markets had fully priced in this move and the Australian dollar’s reaction has been muted.

At her press conference, RBA Governor Bullock said that policymakers had discussed the possibility of raising rates at today’s meeting. This has become a pattern for the RBA, which considered hiking rates in previous meetings but opted to hold rates each time. Bullock dropped a bombshell when she said that the central bank was unlikely to lower interest rates for at least six months due to inflation being too high.

Bullock said that the markets were “a little bit ahead of themselves” in pricing rate cuts, but the markets still expect the Bank to start lowering rates before the end of the year. The RBA is currently forecasting that inflation, which rose to 3.8% in Q2, will not drop to the midpoint of the 1-3% target band until mid-2026.

The RBA Governor noted the sudden meltdown in global stock markets, but said this development had not factored in to today’s rate decision. The rout stocks was a reaction to a soft US employment report on Friday, which has raised fears of a US recession. The Australian dollar wobbled on Monday, falling as much as 2.4% before recovering most of these losses. The S&P ASX 200 index, the country’s benchmark stock index, declined by 3.7% on Monday but has stabilized today.

AUD/USD Technical

- There is resistance at 0.6562 and 0.6627

- 0.6455 and 0.6390 are the next support levels