Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6390; (P) 0.6455; (R1) 0.6562; More...

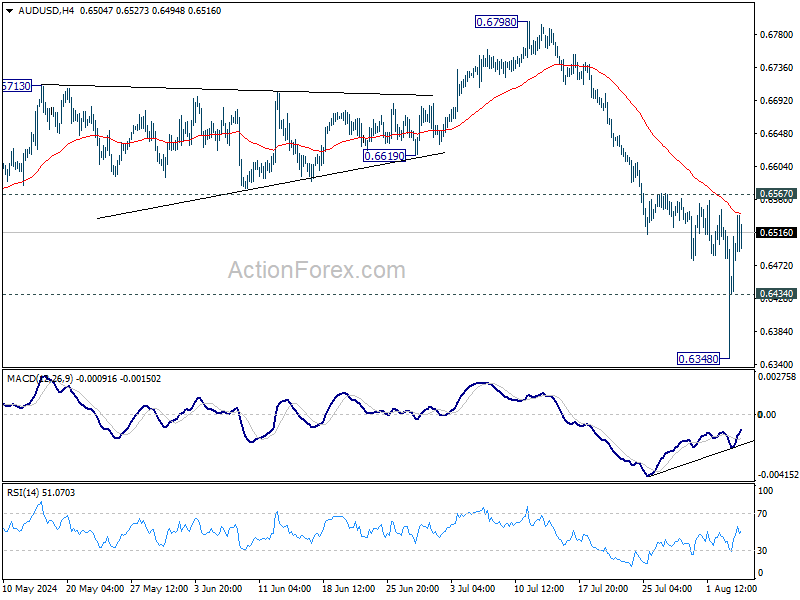

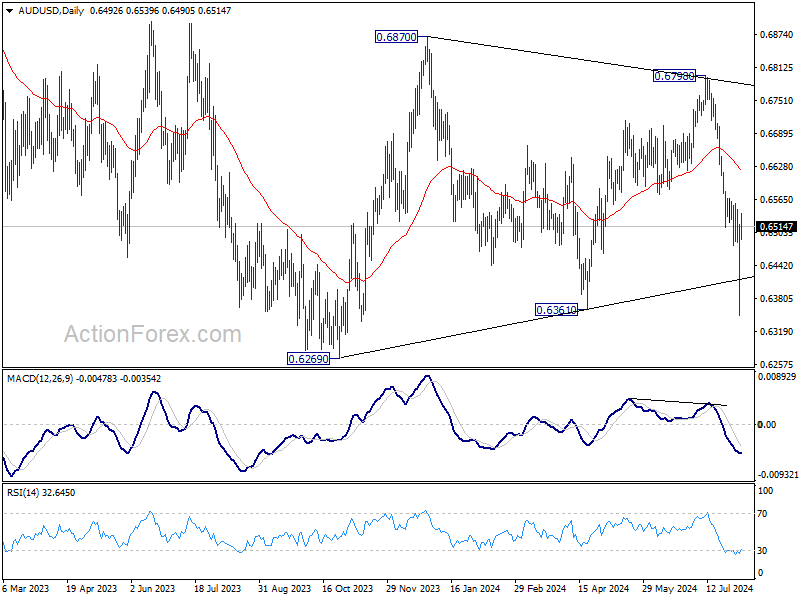

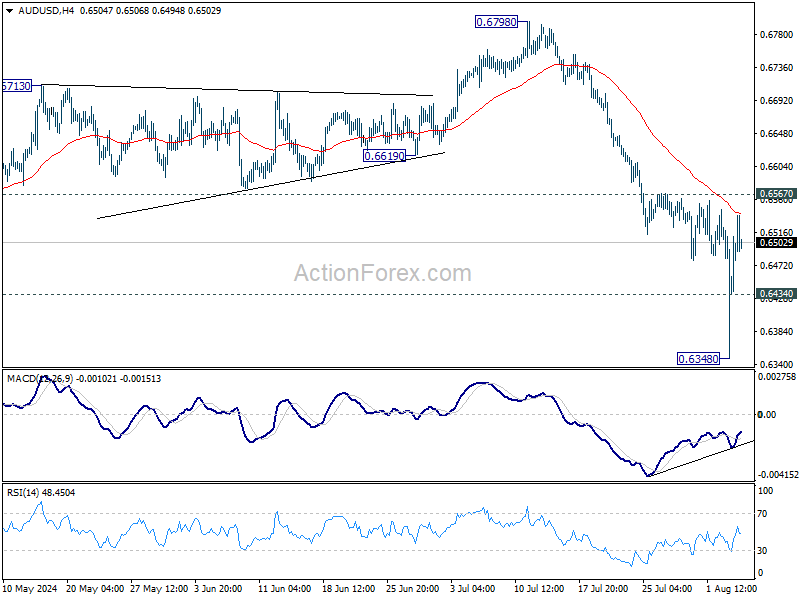

AUD?USD rebounded strongly after diving to 0.6348 but upside is capped below 0.6567 resistance so far. Intraday bias is turned neutral first, and further fall is in favor. Below 0.6434 minor support will bring retest of 0.6348 low. Firm break there will resume the decline from 0.6798 to 0.6269 support next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 55 D EMA (now at 0.6619) holds, in case of rebound.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3775; (P) 1.3861; (R1) 1.3913; More...

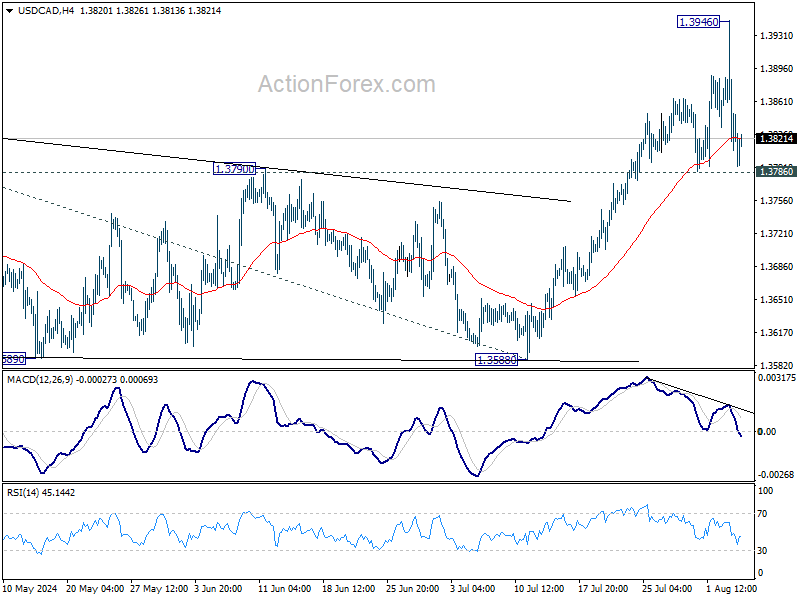

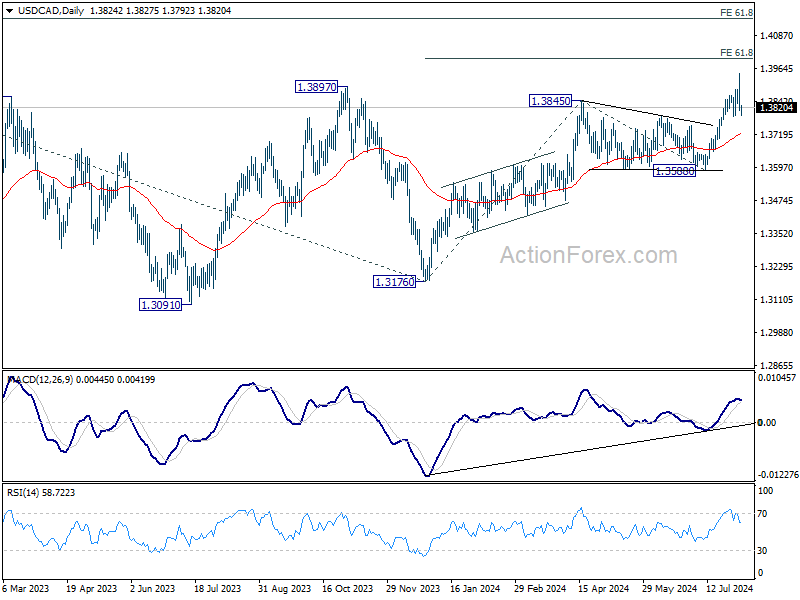

Intraday bias in USD/CAD turned neutral with the current retreat. But further rise is expected as long as 1.3786 support holds. Break of 1.3946 will target 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025 next. Nevertheless, firm break of 1.3786 will turn bias back to the downside for deeper pullback instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

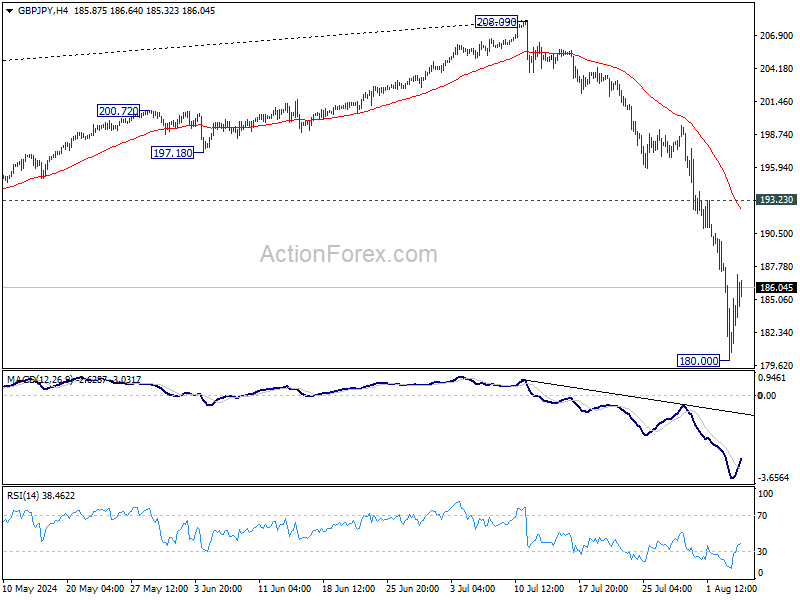

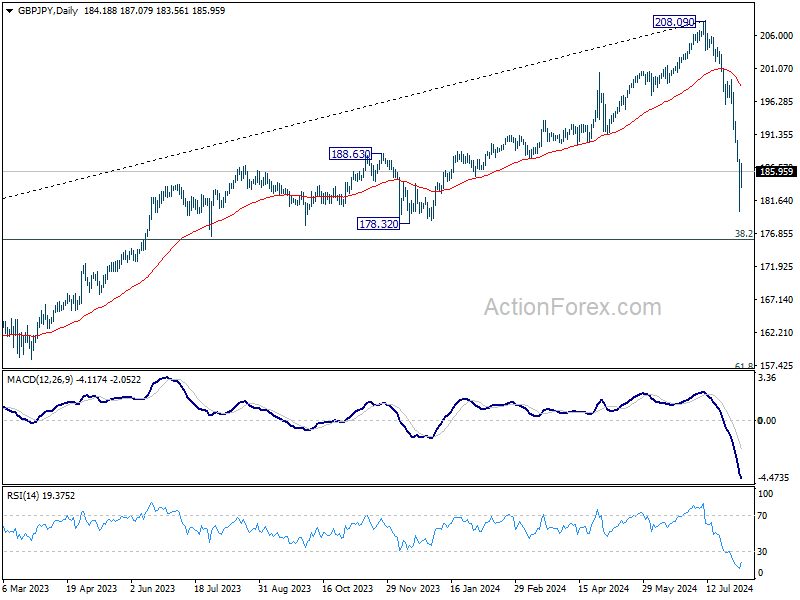

GBP/JPY Daily Outlook

Daily Pivots: (S1) 180.22; (P) 184.11; (R1) 188.11; More...

GBP/JPY recovered after diving to 180.00 and intraday bias is turned neutral first. Some consolidations would be seen but upside should be limited by 193.23 resistance to bring another fall. Break of 180.00 will resume the decline from 208.09 to 178.32 support next.

In the bigger picture, fall from 208.09 medium term top is seen as correcting the up trend from 123.94 (2020 low). Deeper decline is in favor as long as 55 W EMA (now at 189.31) holds. But strong support could emerge between 178.32 and 38.2% retracement of 123.94 to 208.09 at 175.94 to bring rebound. Meanwhile, sustained trading above 55 W EMA will suggest that the range for the medium term corrective pattern is already set.

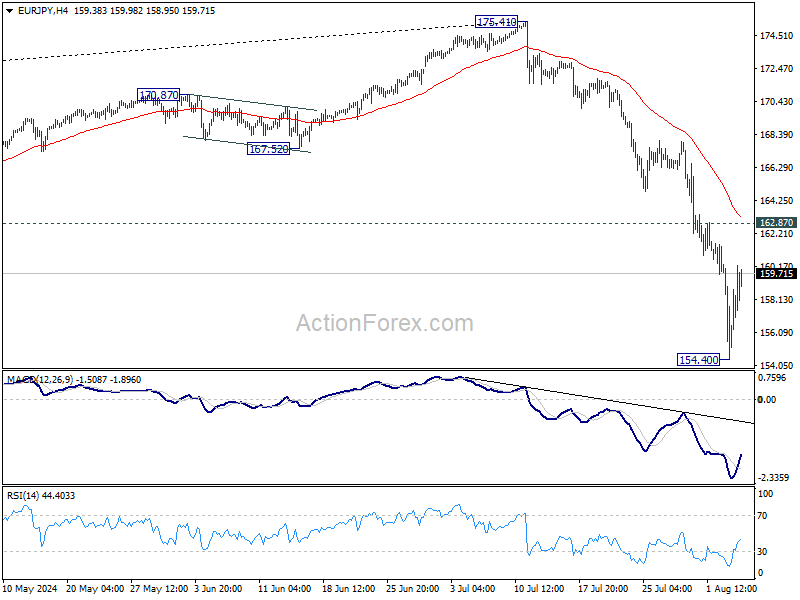

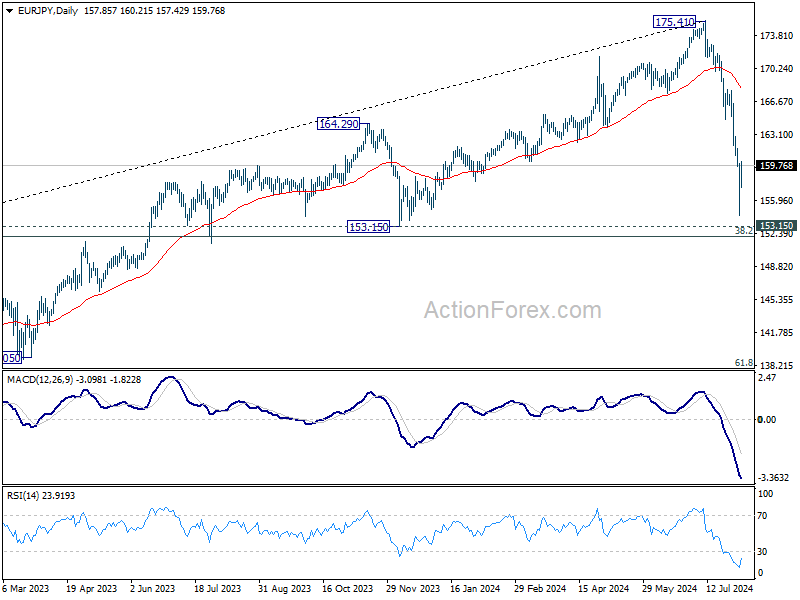

EUR/JPY Daily Outlook

Daily Pivots: (S1) 154.80; (P) 157.51; (R1) 160.60; More...

EUR/JPY recovered after diving to 154.40 and intraday bias is turned neutral first. Some consolidations would be seen but upside should be limited by 162.87 resistance to bring another fall. Break of 154.40 will resume the decline from 175.41 to 153.15 support next.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper fall could be seen as long as 55 W EMA (now at 161.79) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound (at least on first attempt). Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

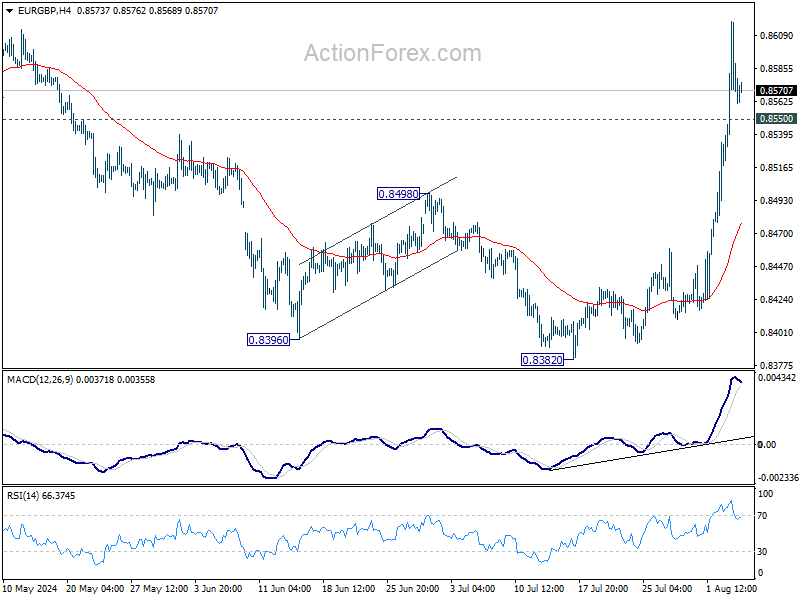

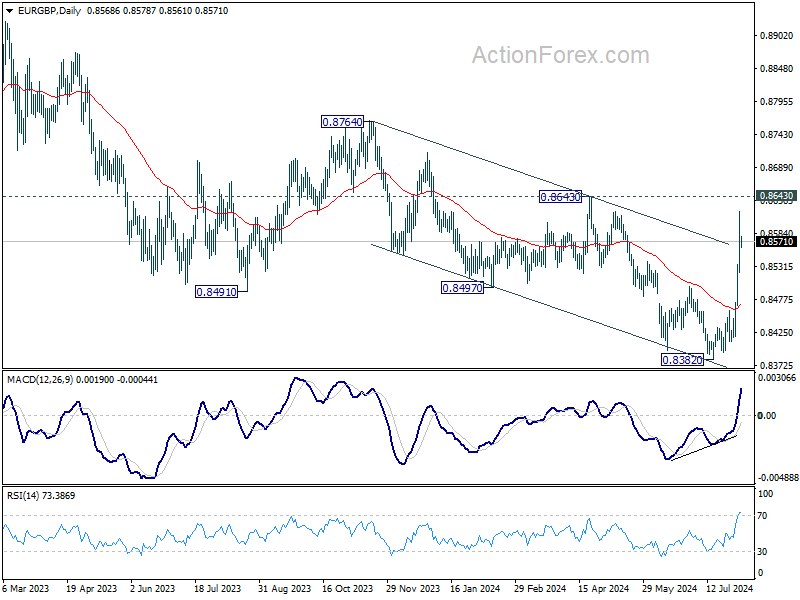

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8521; (P) 0.8571; (R1) 0.8619; More....

Intraday bias in EUR/GBP remains on the upside at this point. Further rise should be seen to 0.8643 resistance. Decisive break there will strengthen the case of larger bullish reversal and target 0.8764 key resistance next. On the downside, though, below 0.8550 minor support will turn intraday bias neutral first.

In the bigger picture, while the rebound from 0.8382 is strong, there is no confirmation of trend reversal yet. As long as 0.8643 resistance holds, down trend from 0.9267 could still resume through 0.8382 at a later stage. However, firm break of 0.8643 will indicate that such down trend has completed, and turn outlook bullish.

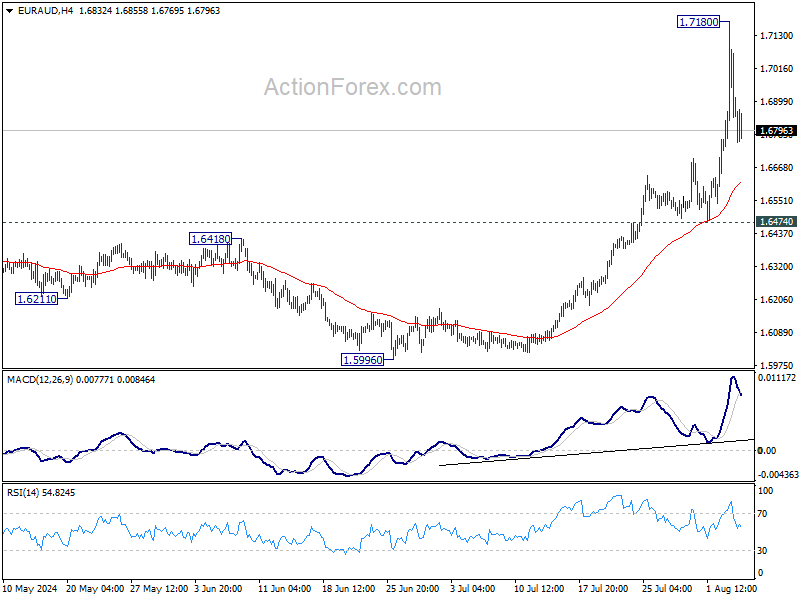

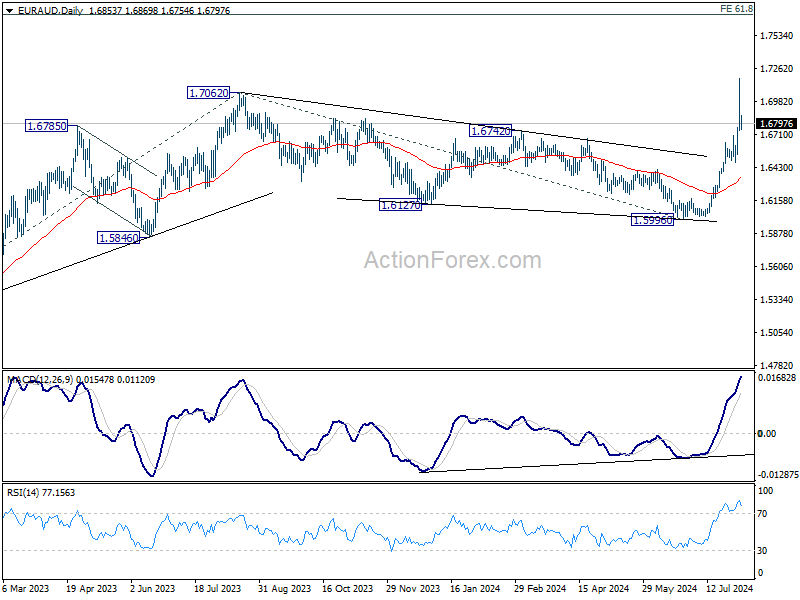

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6665; (P) 1.6926; (R1) 1.7118; More...

Intraday bias in EUR/AUD is turned neutral first as it retreated after hitting 1.7180. Some consolidations would be seen but downside should be contained above 1.6474 support to bring another rally. On the upside, break of 1.7180 will resume larger up trend to 1.7715 fibonacci projection level next.

In the bigger picture, decisive break of 1.7062 resistance will confirm resumption of whole up trend from 1. 1.4281 (2022 low). Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. For now, further rally is expected as long as 55 D EMA (now at 1.6355) support holds, even in case of deep retreat.

FOMC to Act Decisively, But With Confidence

We have added additional rate cuts at the November and January FOMC meetings to our profile. Our unrevised terminal rate of 3.375% is now seen at end-2025 instead of mid-2026.

July’s US employment report unnerved global markets. Growth in nonfarm payrolls slowed to less than half the average of the prior twelve months (including revisions) and the unemployment rate rose by 0.2ppts in the month to 4.3%.

The unemployment rate’s rise held particular significance for many in the market. Firstly, it triggered the Sahm Rule (an indicator that states that a recession has started once the three-month moving average of the unemployment rate is 0.5ppts above the lowest three-month average of the past 12 months). In addition, the July print was 0.1ppt above the peak rate the FOMC foresaw through 2024–2026 at the time of their June meeting.

Fearing the FOMC may have missed their opportunity to produce a soft landing, participants quickly jumped to price in a near 100% chance of a 50bp cut in September and a 60% chance of a follow-up 50bp move in November. Around 110bps of easing is currently expected by end-2024, to be followed by a string of additional cuts in 2025 towards the FOMC’s 2.8% ‘longer run’ estimate.

Westpac has warned throughout 2024 of a coming deterioration in the US labour market, so July’s outcomes are not a big surprise. However, we remain confident in the underlying health of the US economy and believe the FOMC will as well, resulting in a more muted easing cycle than the market currently expects.

In gauging the underlying health of the US economy, firstly it is important to recognise that US employment estimates are, at worst, pointing to a stalling out of job growth, not an outright contraction, with household employment, the weaker of the two key measures, having averaged +19k the past six months.

While the ISM surveys have, over the past six months, signalled the possibility of a dramatic reduction in labour demand, the NFIB small business survey’s employment measure has held modestly above average and the Federal Reserve’s Beige Book is in keeping with the household survey’s signal of ‘only’ a stalling out of employment growth. Hours worked from the establishment survey also continues to track nonfarm payrolls, so there is no evidence of hours being reduced disproportionately either.

Current momentum in US economic activity is also healthy, with domestic final demand growth around average in the first half of 2024, circa 2.5% annualised. Households’ decision to lock in historically low rates before and during the pandemic continues to provide benefit, while consumer wealth and debt levels remain constructive for spending and confidence.

For the FOMC then, as inflation continues to come down and with the labour market weaker today than expected over the forecast period, there is cause to cut decisively into year end and through early-2025. But, given the economy’s resilience and the absence of evidence that inflation will soon undershoot the FOMC’s 2% target, there is no need to rush to neutral or below.

As before, we look for the FOMC to begin the cutting cycle in September with a 25bp cut. In view of the greater downside risks becoming evident in the labour market data, we now also forecast 25bp cuts at the November 2024 and January 2025 meetings in addition to those already expected in December 2024 and March 2025. A cut per quarter from the June quarter will see our unrevised terminal rate of 3.375% reached at end-2025 instead of mid-2026.

We will have more to say on the implications for term interest rates and the Australian dollar in our forthcoming August Market Outlook. But, broadly speaking, while we expect the 10-year to hold near its current level over the remainder of the year as rate cuts commence, it is then anticipated to drift back up to around 4.00% in mid-2025, putting in place a sizeable spread to the fed funds rate.

This will be a consequence of the US economy’s underlying health, but also the established trend for the Federal deficit and evidence of inflation pressures related to capacity constraints and trade policy. While these uncertainties remain, it will prove difficult for the Australian dollar to stage a strong rally, although the recovery in Australian growth in 2025 and improving global sentiment should allow for a slow uptrend through USD0.70 from late-2025.

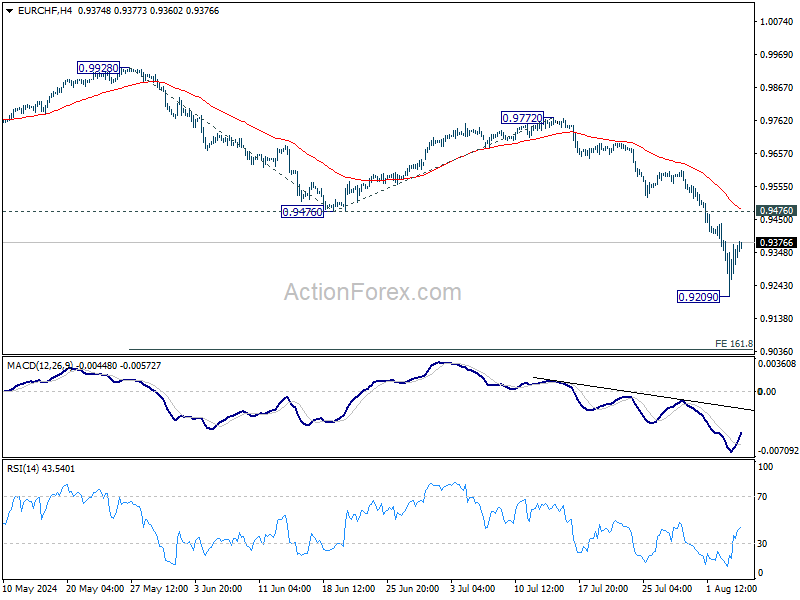

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9235; (P) 0.9310; (R1) 0.9408; More....

EUR/CHF recovered after hitting 0.9029 and intraday bias is turned neutral for consolidations first. But near term outlook will stay bearish as long as 0.9476 support turned resistance holds. Below 0.9209 will target 161.8% projection of 0.9928 to 0.94767 from 0.9772 at 0.9041 next.

In the bigger picture, current downside acceleration argues that medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Market Volatility Persists, Aussie Steady with RBA’s Intricate Inflation Forecast

The financial markets continued to see extreme volatility. DOW dropped by over -1000 points overnight, but the global rout seems to have paused for now. Nikkei staged a dramatic 10% rebound in early trading after yesterday's history plunge of -12.4%. However, this recovery was not mirrored by other Asian markets. Investor sentiment remains fragile, with worries over US recession dominating the headlines.

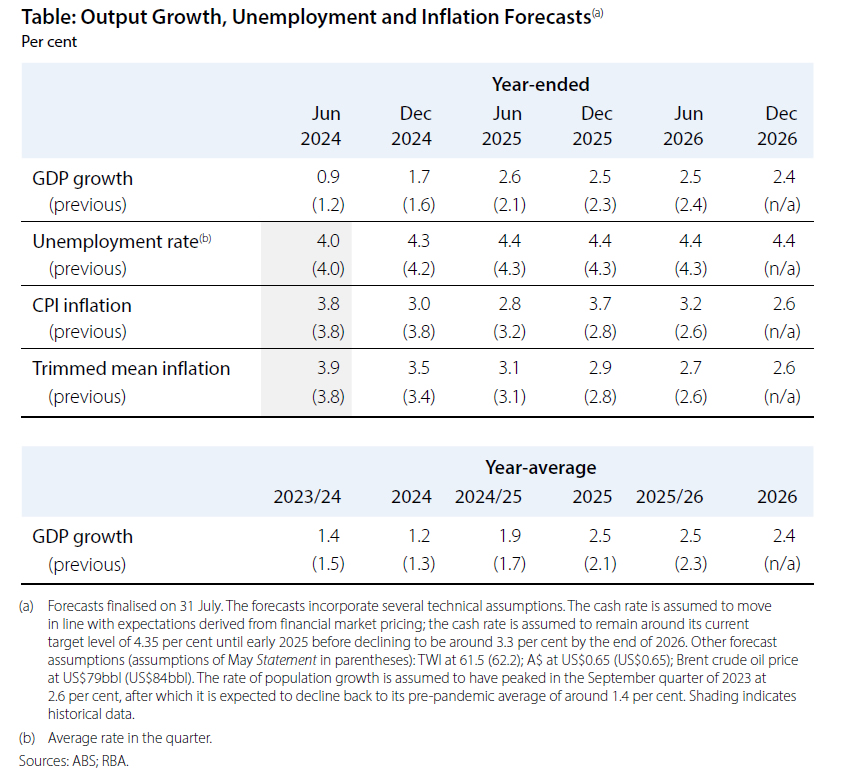

In the currency markets, Australian Dollar is holding steady following RBA's decision to keep interest rates unchanged, as anticipated. The new economic projections present a complicated outlook. Inflation is expected to dip to the target rate by mid-2025, rise again in subsequent quarters, and then return to the target range by mid-2026. It's still uncertain whether RBA would need to raise interest rates again. However, given the risk of inflation resurgence highlighted in the projections, RBA is likely to remain cautious and avoid premature policy easing.

For the week so far, Yen remains the strongest performer. Canadian Dollar has overtaken Swiss Franc for the second spot, with Euro following as the third strongest. New Zealand Dollar is currently the weakest performer, followed by Sterling and then Australian Dollar. Dollar and Swiss Franc are positioned in the middle.

Technically, while AUD/USD staged a strong rebound after diving to 0.6348, there is no follow through momentum so far. Further decline will remain in favor as long as 0.6567 resistance holds. Below 0.6434 minor support will bring retest of 0.6348 first. Firm break there will resume the decline form 0.6798 towards 0.6269 (2023 low). Nevertheless, strong break of 0.6567 will suggest near term reversal and bring stronger rally.

In Asia, at the time of writing, Nikkei is up 7.85%. Hong Kong HSI is down -0.01%. China Shanghai SSE is down -0.09%. Singapore Strait Times is down -0.60%. Japan 10-year JGB yield is up 0.01542 at 0.908. Overnight, DOW fell -2.60%. S&P 500 fell -3.00%. NASDAQ fell -3.43%. 10-year yield fell -0.007 to 3.785.

RBA maintains cash rate, anticipates inflation resurgence post-mid-2025

RBA kept its cash rate target unchanged at 4.35%, as widely expected. Maintaining its stance of "not ruling anything in or out," the highlighted that underlying inflation "remains too high" and stated it will be "some time yet" before inflation sustainably returns to the target range. The central bank emphasized that monetary policy will need to be "sufficiently restrictive" until the Board is confident that inflation is moving sustainably towards the target range.

In its new economic projections, RBA forecasts headline inflation to briefly dip to 2.8% in June 2025, back in the target range, but expects it to surge above the target in subsequent quarters before falling back to 2.6% by the end of 2026. Meanwhile, growth projections have been generally upgraded.

Details of the new economic projections include:

CPI at:

- 3.0% by the end of 2024, downgraded from the prior 3.8%.

- 3.7% by the end of 2025, upgraded from the previous 2.8%.

- 2.6% by the end of 2026 (new projection).

Trimmed mean CPI at:

- 3.5% by the end of 2024, up from 3.4%.

- 2.9% by the end of 2025, up from 2.8%.

- 2.6% by the end of 2026 (new projection).

Year-average GDP growth in:

- 2024 downgraded from 1.3% to 1.2%.

- 2025 upgraded from 2.1% to 2.5%.

- 2026 projected to be 2.4% (new).

Unemployment rate at:

- 4.3% by the end of 2024, up from the prior 4.2%.

- 4.4% by the end of 2025, up from 4.3%.

- be 4.4% by the end of 2026 (new projection).

Japan's nominal wages surge 4.5% yoy in Jun, outpacing inflation for first time in 27 months

Japan's nominal wages, or average monthly cash earnings, rose by 4.5% yoy in June, significantly exceeding expectations of a 2.3% yoy increase. This marks the 30th consecutive month of wage growth. More importantly, with CPI rising 3.3% yoy in the same month, real wages increased by 1.1% yoy, marking the first gain in 27 months as wage growth finally outpaced inflation.

A Ministry of Health, Labor and Welfare official commented, "We will monitor incoming data closely to see if the trend has really changed as there is a possibility that those firms that paid bonuses in July might have just moved up the timing this year."

Excluding bonuses and non-scheduled payments, average wages climbed 2.3% yoy, while overtime and other allowances rose by 1.3% yoy.

Also released, household spending in June fell by -1.4% yoy, worse than the expected -0.9% yoy decline, marking the second consecutive month of decline following a -1.8% drop yoy in May.

Fed's Daly raises alarm over "real weakness" in slowing labor market

San Francisco Fed President Mary Daly commented in a forum overnight, stating that "we've now confirmed that the labor market is slowing". She emphasized the importance of ensuring that this slowdown does not turn into a downturn.

However, she expressed her concern that "it's too early to tell" whether the labor market is "slowing to a sustainable pace which allows the economy to continue to grow" or if it is approaching a point of "real weakness."

Daly also mentioned that she expects interest rates to eventually come down "to preserve the balance" of full employment and price stability. However, she cautioned that she is not prepared to specify when or by how much, as she plans to review more data before the next Fed policy meeting in September.

Looking ahead

Swiss unemployment rate and retail sales will be released in European session. Germany will release factory orders. Eurozone will release retail sales. UK will release PMI construction. Later in the day, both US and Canada will release trade balance.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9235; (P) 0.9310; (R1) 0.9408; More....

EUR/CHF recovered after hitting 0.9029 and intraday bias is turned neutral for consolidations first. But near term outlook will stay bearish as long as 0.9476 support turned resistance holds. Below 0.9209 will target 161.8% projection of 0.9928 to 0.94767 from 0.9772 at 0.9041 next.

In the bigger picture, current downside acceleration argues that medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Jun | 4.50% | 2.30% | 1.90% | 2.00% |

| 23:30 | JPY | Household Spending Y/Y Jun | -1.40% | -0.90% | -1.80% | |

| 04:30 | AUD | RBA Rate Decision | 4.35% | 4.35% | 4.35% | |

| 05:45 | CHF | Unemployment Rate M/M Jul | 2.50% | 2.40% | ||

| 06:00 | EUR | Germany Factory Orders M/M Jun | 0.80% | -1.60% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Jun | 0.50% | 0.40% | ||

| 08:30 | GBP | Construction PMI Jul | 51 | 52.2 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Jun | -0.20% | 0.10% | ||

| 12:30 | CAD | Trade Balance (CAD) Jun | -2.0B | -1.9B | ||

| 12:30 | USD | Trade Balance (USD) Jun | -72.5B | -75.1B |

RBA maintains cash rate, anticipates inflation resurgence post-mid-2025

RBA kept its cash rate target unchanged at 4.35%, as widely expected. Maintaining its stance of "not ruling anything in or out," the highlighted that underlying inflation "remains too high" and stated it will be "some time yet" before inflation sustainably returns to the target range. The central bank emphasized that monetary policy will need to be "sufficiently restrictive" until the Board is confident that inflation is moving sustainably towards the target range.

In its new economic projections, RBA forecasts headline inflation to briefly dip to 2.8% in June 2025, back in the target range, but expects it to surge above the target in subsequent quarters before falling back to 2.6% by the end of 2026. Meanwhile, growth projections have been generally upgraded.

Details of the new economic projections include:

CPI at:

- 3.0% by the end of 2024, downgraded from the prior 3.8%.

- 3.7% by the end of 2025, upgraded from the previous 2.8%.

- 2.6% by the end of 2026 (new projection).

Trimmed mean CPI at:

- 3.5% by the end of 2024, up from 3.4%.

- 2.9% by the end of 2025, up from 2.8%.

- 2.6% by the end of 2026 (new projection).

Year-average GDP growth in:

- 2024 downgraded from 1.3% to 1.2%.

- 2025 upgraded from 2.1% to 2.5%.

- 2026 projected to be 2.4% (new).

Unemployment rate at:

- 4.3% by the end of 2024, up from the prior 4.2%.

- 4.4% by the end of 2025, up from 4.3%.

- be 4.4% by the end of 2026 (new projection).