Sample Category Title

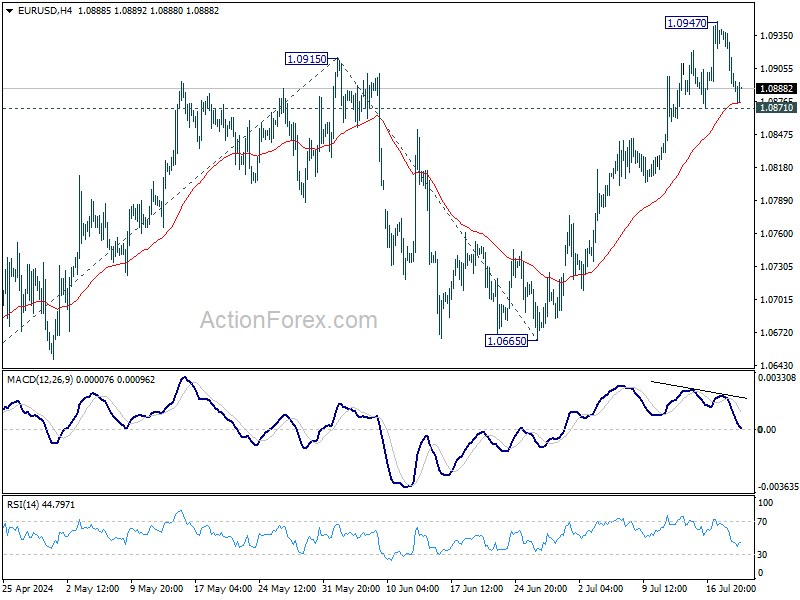

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0879; (P) 1.0911; (R1) 1.0928; More....

EUR/USD is still holding above 1.0871 support and intraday bias stays neutral. Further remains mildly in favor. Break of 1.0947 will resume the rise from 1.0601 and target target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, considering bearish divergence condition in 4H MACD, firm break of 1.0871 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 1.0804).

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

Dollar Gains on Risk Aversion Amid Quiet Trading

Risk aversion continues to support Dollar in relatively quiet trading today. Both Sterling and Canadian Dollar weakened mildly after worse-than-expected retail sales data. Euro shrugged off dovish comments from some ECB officials. Meanwhile, Yen softened slightly following lower-than-expected CPI core reading.

However, overall movements in the currency markets remain limited as traders hold their bets, awaiting further developments to determine if yesterday's steep selloff in US stocks will continue or if risk sentiment will improve as the week comes to a close.

For the week, Swiss Franc remains the strongest, followed by Yen and then Dollar. The greenback, however, has the potential to overtake both of their positions. Kiwi remains the worst performer, followed by Aussie and Loonie, which is typical in risk-off markets. Euro and Sterling are stuck in the middle, with the common currency having a slight upper hand.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.54%. CAC is down -0.44%. UK 10-year yield is up 0.0467 at 3.252. Germany 10-year yield is up 0.0463 at 2.473. Earlier in Asia, Nikkei fell -0.16%. Hong Kong HSI fell -2.03%. China Shanghai SSE rose 0.17%. Singapore Strait Times fell -0.68%. Japan 10-year JGB yield closed flat at 1.047.

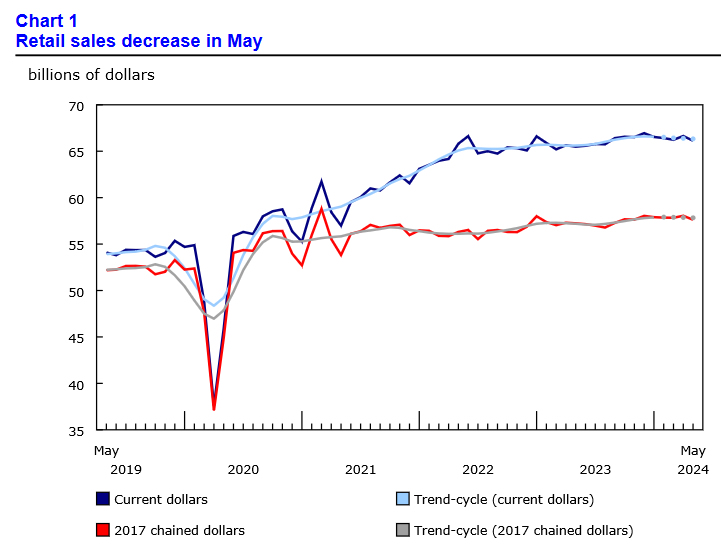

Canada retail sales falls -0.8% mom in May, down further -0.3% mom in Jun

Canada's retail sales fell -0.8% mom to CAD 66.1B in May, worse than expectation of -0.5% mom. Sales were down in eight of nine subsectors, led by decreases at food and beverage retailers. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -1.4% mom in May.

Advance estimate indicates that sales decreased further by -0.3% mom in June.

ECB's Villeroy: Market rate cut expectations "rather reasonable"

ECB Governing Council member Francois Villeroy de Galhau spoke on French radio BFM Business today, expressing that current market expectations for interest rate cuts seem "rather reasonable."

Markets are currently pricing in nearly two ECB rate cuts for the remainder of the year, likely occurring in September and December, with around five cuts anticipated by the end of next year.

Villeroy de Galhau affirmed ECB's stance on inflation, stating, "Overall, we are 'on track' with our inflation target and forecast of 2% next year." He further emphasized the commitment to this target, noting, "Barring any shocks, this is more than a forecast, it's a commitment."

ECB's Simkus: Interest rates are getting lower, quite significantly

ECB Governing Council member Gediminas Simkus shared his views with reporters today, indicating that his outlook aligns with current market expectations, which anticipate two rate cuts this year.

Simkus commented, "Interest rates are getting lower and, I think, will keep getting lower, and quite significantly."

UK retail sales falls -1.2% mom in Jun, down -0.2% yoy in Q2

UK retail sales volume fell -1.2% mom in June, worse than expectation of -0.6% mom. Sales volumes fell across most sectors, with department stores and clothing retailers broadly returning to their Q1 levels. It's -1.3% below their pre-pandemic levels in February 2020.

Looking at the quarter, sales volumes fell by -0.1% qoq and -0.2% yoy in Q2.

Japan's CPI core rises to 2.6%, above target for 27th month

Japan's core CPI, which excludes food prices, rose from 2.5% yoy to 2.6% yoy in June, slightly missing expectations of 2.7% yoy. This nonetheless marks the 27th consecutive month that inflation has been at or above BoJ's 2% target. Core-core CPI, which excludes both food and energy, increased from 2.1% yoy to 2.2% yoy, while headline CPI as unchanged at 2.8% yoy.

Services inflation saw a modest increase from 1.6% yoy to 1.7% yoy. A reduction in government subsidies aimed at curbing utility bills resulted in a 7.7% yoy rise in energy costs, up from 7.2% increase seen in May.

Attention is now shifting to BoJ's upcoming meeting on July 30-31. There is divided opinion on whether BoJ will decide to hike the policy rate from the current 0.00-0.10% range to 0.15-0.25%. The central bank is also expected to unveil a roadmap for reducing its bond purchases and release its economic outlook report, which will publish new economic forecasts.

Japan downgrades fiscal 2024 growth forecast amid consumption struggles

Japan's government has downgraded its growth forecast for the current fiscal year 2024 from 1.3% to 0.9%.

This adjustment comes as inflation continues to impact private consumption, which accounts for over half of the economy. Private consumption growth is now expected to be just 0.5%, a significant drop from the January forecast of 1.2%.

Various one-off factors, including safety test scandals in the auto industry, have also contributed to this downgrade.

However, the economy is expected to rebound in fiscal 2025 with a growth rate of 1.2%.

Consumer prices are now forecast to rise by 2.8% in fiscal 2024, an increase from the earlier expectation of 2.5%.

The government has also adjusted its assumption for Yen, now expecting it to remain around 158.8 per Dollar for the current fiscal year, weaker than the previous estimate of 149.8 Yen.

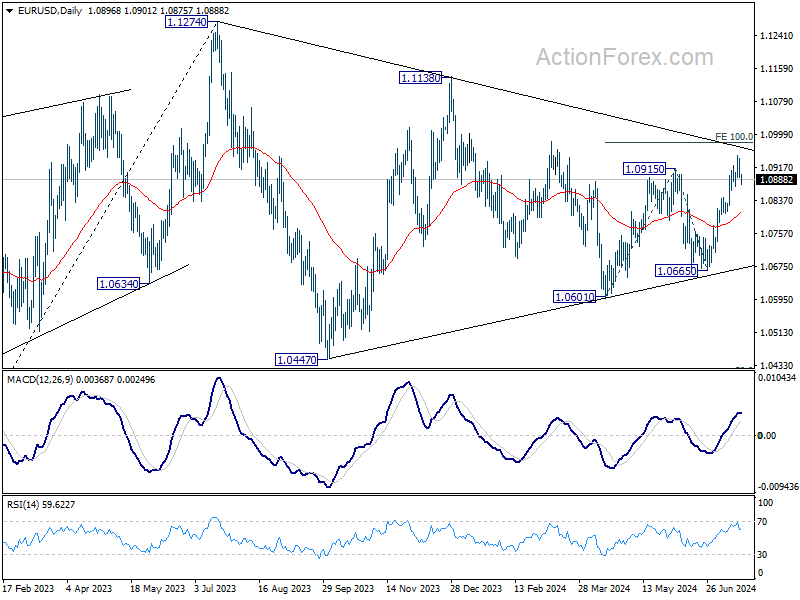

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0879; (P) 1.0911; (R1) 1.0928; More....

EUR/USD is still holding above 1.0871 support and intraday bias stays neutral. Further remains mildly in favor. Break of 1.0947 will resume the rise from 1.0601 and target target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, considering bearish divergence condition in 4H MACD, firm break of 1.0871 will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 1.0804).

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Jul | -13 | -11 | -14 | |

| 23:30 | JPY | National CPI Y/Y Jun | 2.80% | 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.60% | 2.70% | 2.50% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 2.20% | 2.10% | ||

| 06:00 | EUR | Germany PPI M/M Jun | 0.20% | 0.10% | 0.00% | |

| 06:00 | EUR | Germany PPI Y/Y Jun | -1.60% | -1.60% | -2.20% | |

| 06:00 | GBP | Retail Sales M/M Jun | -1.20% | -0.60% | 2.90% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 13.6B | 12.0B | 14.1B | 15.6B |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 37B | 34.6B | 38.6B | |

| 12:30 | CAD | Industrial Product Price M/M Jun | 0.00% | 0.20% | 0.00% | 0.20% |

| 12:30 | CAD | Raw Material Price Index Jun | -1.40% | -0.70% | -1.00% | -1.50% |

| 12:30 | CAD | Retail Sales M/M May | -0.80% | -0.50% | 0.70% | 0.60% |

| 12:30 | CAD | Retail Sales ex Autos M/M May | -1.30% | -0.50% | 1.80% | 1.70% |

Canada retail sales falls -0.8% mom in May, down further -0.3% mom in Jun

Canada's retail sales fell -0.8% mom to CAD 66.1B in May, worse than expectation of -0.5% mom. Sales were down in eight of nine subsectors, led by decreases at food and beverage retailers. Core retail sales—which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers—were down -1.4% mom in May.

Advance estimate indicates that sales decreased further by -0.3% mom in June.

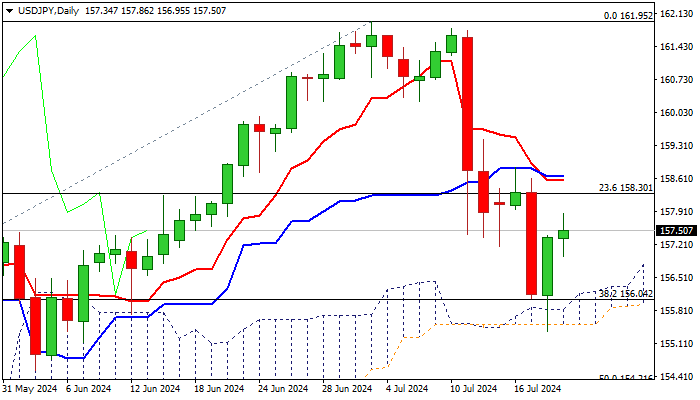

USD/JPY Outlook: Bear-Trap Underpins But Recovery Still Faces Headwinds

USDJPY remains constructive on Friday and attempts to further extend Thursday’s strong bounce, with recovery being supported by signals of a double bear-trap, following a false break below pivotal Fibo support at 156.04 and thin daily cloud (spanned between 155.83 and 155.50).

Rising and thickening daily cloud also underpins near-term action, however, headwinds are still to be expected, as structure on daily chart is still bearish.

Recovery needs to clear initial pivots at 157.73/88 (55DMA / Fibo 38.2% of 161.95/155.36) to reduce downside risk and open way for fresh acceleration towards next targets at 158.65/78 (falling 10DMA/50% retracement).

Caution on repeated daily close under 55DMA.

Res: 157.73; 158.30; 158.86; 159.52.

Sup: 156.91; 156.04; 155.36; 155.18.

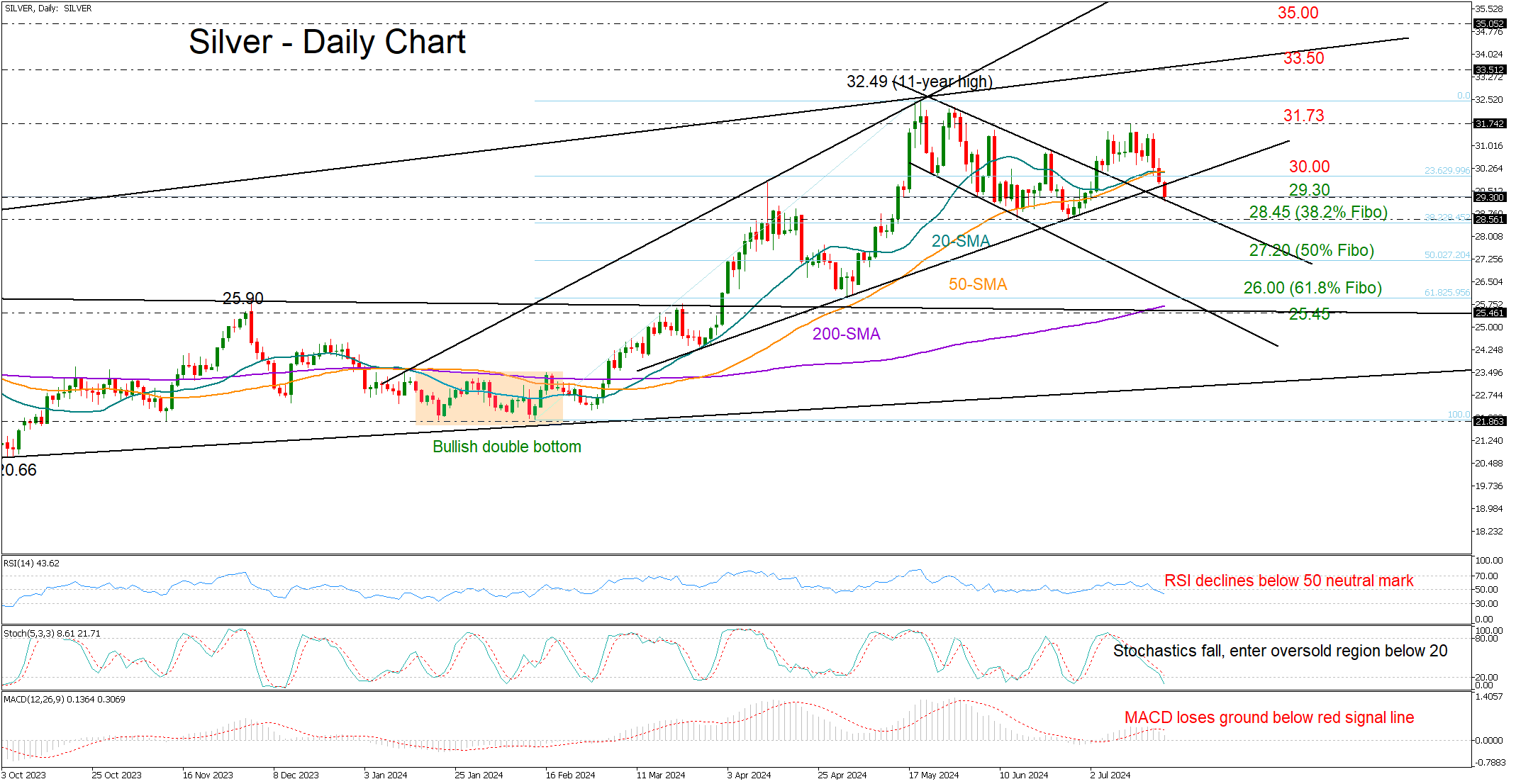

Silver Sinks Below 30

- Silver erases June’s gains; eyes on 28.50

- Technical signals favor the bears

Silver’s performance took a hit, marking its worst week in 2024 as the US dollar switched to recovery mode and investors questioned China’s economic outlook. As a result, the metal swiftly reversed a substantial part of its June upswing in just three days and is currently trading near 29.24, correcting by around 10% from May’s 11-year high of 32.49.

The former resistance trendline drawn from May’s peak is currently under examination at 29.30 and a break below it could immediately squeeze the price towards June’s base of 28.55. The inclusion of the 38.2% Fibonacci retracement of the February-May upleg at 28.45 strengthens the region’s significance. Hence, failure to pivot there could prompt a faster decline towards the 50% Fibonacci mark of 27.20. Should the 27.00 round-level prove fragile too, the next stop could be around the 61.8% Fibonacci of 26.00.

With the 20- and 50-day SMAs posting a negative cross and technical indicators falling, a substantial rebound seems unlikely at the moment. Nonetheless, with the stochastic oscillator dipping below 20 into the oversold territory, downward pressures might not endure for long.

For the outlook to improve, the price must reclaim the 30.00 mark, where the 20-day SMA and the 23.6% Fibonacci number are placed. If bullish efforts prove successful, the recovery phase could expand towards July’s high of 31.73, and then up to the top of 32.49. Even higher, the bulls might peak around the ascending trendline drawn from December 2022 at 33.50 or near 35.00.

To summarize, silver may face a negative situation in the near future, but bulls will have start to worry more if the price drops below 28.45.

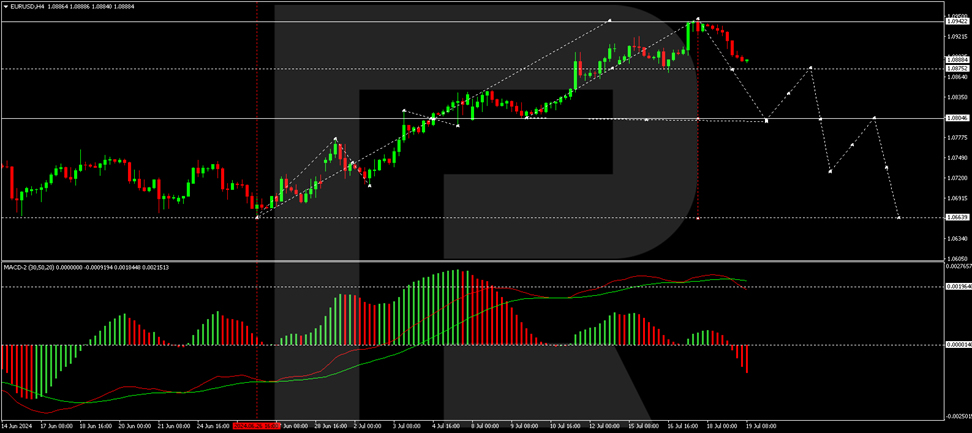

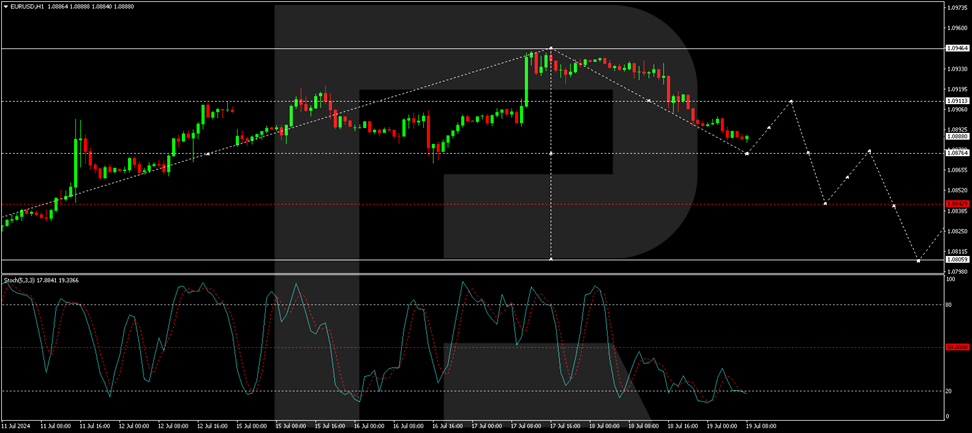

EUR/USD Experiences Sharp Decline: Risk Appetite Heightens

The EUR/USD pair fell sharply to 1.0888, with investors speculating on the future of US interest rates and the potential implications of the upcoming presidential election, particularly as Donald Trump's chances appear to be improving. These factors contribute to a heightened risk appetite, leading to a retreat in the USD.

As the Federal Reserve approaches its meeting at the end of the month, a quiet period will begin this Saturday, during which the Fed will make no further comments.

Concurrently, the European Central Bank (ECB) recently held its meeting, maintaining the current interest rates as anticipated. This decision aligns with recent economic indicators corroborating the ECB's inflation forecasts, prompting a cautious approach. The ECB emphasised that the prevailing high rates are instrumental in managing the consumer price index and reiterated the necessity to maintain these rates, given the expected inflation to remain above the 2% target into 2025.

This perspective is reinforced by sustained price pressures, particularly in the services sector, highlighting ongoing inflationary concerns.

EUR/USD technical analysis

The market has developed a consolidation range around the 1.0806 level, with a breakout leading to achieving the target at 1.0946. A correction towards 1.0806 is currently anticipated, with the initial correction wave targeting 1.0880. Subsequently, a potential rebound to 1.0910 may occur before another decline to 1.0840. The MACD indicator supports this bearish outlook, indicating a downward trajectory from above zero.

The pair is forming a downward wave to 1.0880. Upon reaching this level, a rise to 1.0910 may be considered. This analysis is corroborated by the Stochastic oscillator, positioned below 20 and poised for an upward movement, suggesting a short-term recovery in the pair.

Investors and traders should monitor these developments closely, particularly any shifts in market sentiment influenced by macroeconomic data and central bank activities, which are crucial in shaping the currency dynamics in the near term.

Canadian Dollar Eyes Retail Sales Ahead of Rate Meeting

The Canadian dollar is calm on Friday. In the European session, USD/CAD is trading at 1.3717, up 0.08% on the day at the time of writing. We could see stronger movement in the North American session, with the release of Canadian retail sales.

Will retail sales suffer a reversal?

Canada’s retail sales is expected to regress in June after a strong reading a month earlier. The market estimate stands at -0.6% m/m, after a gain of 0.7% in May. Annually, retail sales sparkled with a gain of 1.8%.

Today’s retail sales report is the final key release ahead of the Bank of Canada’s meeting on July 24. The BoC is widely expected to cut interest rates for a second straight month after last week’s positive inflation report. Inflation fell from 2.9% to 2.7% y/y in June and CPI declined by 0.1% on a monthly basis, the first decline since December 2023. Core CPI also decreased slightly.

The BoC has already demonstrated that it is ready, willing and able to cut rates as both headline and core inflation are within the 1% to 3% target range. Households and businesses are looking for more relief from high interest rates and the central bank will need to continue lowering rates in order to avoid a recession.

In the US, unemployment claims jumped to 243 thousand last week, up from a revised 223,000 in the previous release and higher than expectations. The increase is another indication that the labor market has been softening, which supports the case for a rate cut. The markets have priced in a 95% probability a rate cut in September, according to CME’s FedWatch.

.

USD/CAD Technical

- USD/CAD is testing resistance at 1.3727. Close by, there is resistance at 1.3747

- There is support at 1.3698 and 1.3678

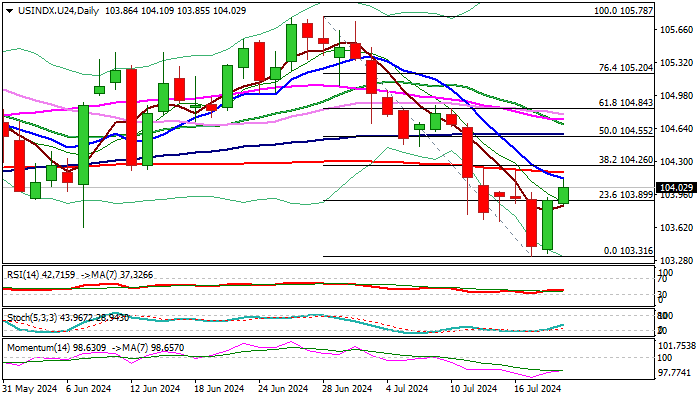

US Dollar Index Outlook: Risk Aversion Lifts the Dollar

The dollar index extends recovery into second straight day, with strong bounce from new four-month low (103.31) on Thursday, being fueled by fresh risk aversion on global cyber outage, which hit financial centers, banks, airlines and many others, prompting investors into safer assets.

Technical picture on daily chart is overall still negative, as 14-d momentum remains deeply in the negative zone and MA’s are in bearish configuration, warning that recovery may struggle to sustain gains.

Bulls face headwinds on approach to falling 10DMA (104.12), which recently formed a death cross with 200DMA (104.18), guarding pivotal Fibo barrier at 104.26 (38.2% of 105.78/103.31 bear-leg)., with sustained break through this zone needed to improve near-term outlook for further recovery.

Otherwise, the downside is expected to remain vulnerable, with limited recovery to offer better levels to re-enter larger downtrend.

Res: 104.18; 104.26; 104.55; 104.67.

Sup: 103.85; 103.67; 103.31; 103.00.

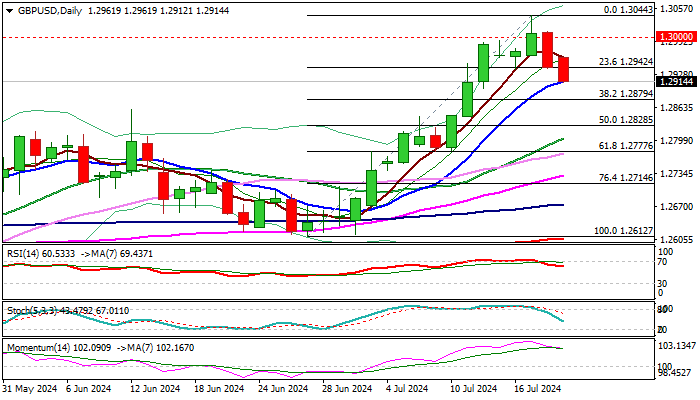

GBP/USD: Cable Dips Further After Downbeat UK Retail Sales

Cable remains in red for the second consecutive day and extends pullback from new one-year high (1.3044).

Weaker than expected UK retail sales increase pressure on sterling and add to bets for BoE rate cut in August (currently at 44%).

Fresh bears broke below the floor of recent consolidation (around Fibo 23.6% of 1.2615/1.3044 upleg), generating initial bearish signal, with extension below cracked rising 10DMA (1.2914) to validate the signal and close below 1.2879 (Fibo 38.2%) to generate initial reversal signal.

Also, formation of bull-trap above 1.30 barrier on weekly chart, may add to downside risk.

On the other hand, daily studies are still predominantly bullish (MA’s in bullish setup / strong positive momentum), suggesting that current pullback could be seen as correction of larger uptrend, if dips find firm ground above 1.2830 zone.

Res: 1.2942; 1.3000; 1.3044; 1.3100.

Sup: 1.2879; 1.2860; 1.2828; 1.2777.

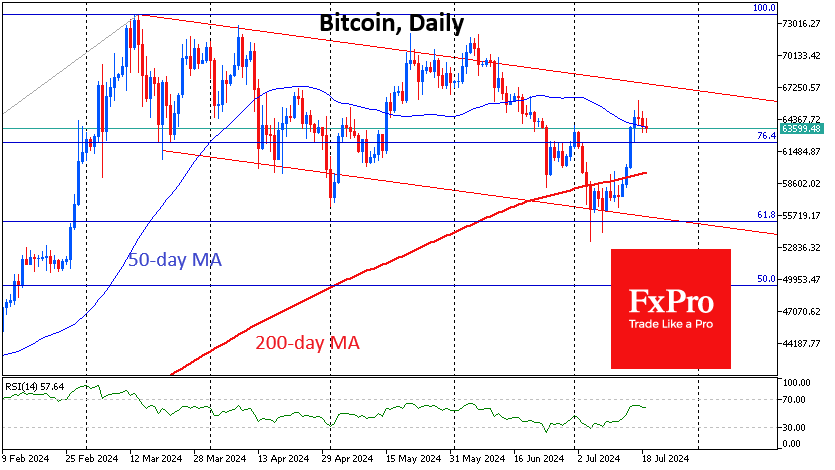

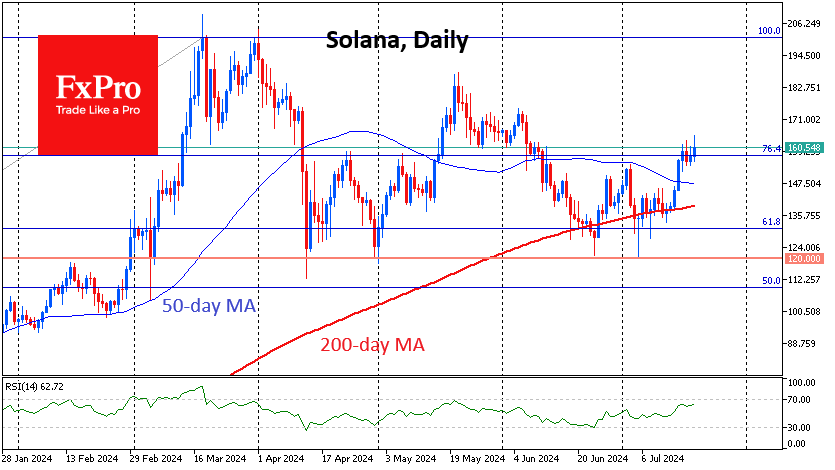

No Rush in Crypto

Market picture

The crypto market cap fell 1% in 24 hours to $2.36 trillion, in line with the US market’s losses during that time. The pullback in traditional finances explains why Bitcoin is dragging the overall crypto market down. Bitcoin is losing 1.3%, Ethereum 0.5%, and the top altcoins are changing between -4.7% (XRP) and 2.8% (Solana).

Bitcoin continues to tread around $64K, clinging to the area above its 50-day moving average. Consolidation after the rally in Bitcoin continues, with it technically far from overbought and sentiment far from euphoric, leaving room for gains.

Despite the unsightly external background, Solana set a new local peak at $164, the highest in six weeks. The coin withstood repeated attempts to sell the price below the 200-day average since the end of June. This support coincided with a 61.8% retracement of the rally from September to the March peak. The expansion pattern will activate if the price rises above $200, making the $320 area a potential target. It will take impressive FOMO and a successful Solana project effort to get the price there in the coming year.

News background

According to SoSoValue, spot bitcoin ETFs saw inflows of $53.35 million on 17 July. The positive trend continued for the ninth consecutive day with total inflows of $1.97 billion. In total, since the approval of BTC-ETFs in January, inflows have totalled $16.59 billion.

Billionaire investor Mark Cuban said Bitcoin could become a global safe haven amid geopolitical uncertainty and the dollar’s failure as a reserve currency. This would increase global demand for the first cryptocurrency as a means of saving.

Ripple executives expect the US SEC to drop further investigations and withdraw claims against the company after a series of unsuccessful lawsuits.

The SEC has approved applications to launch an Ethereum-based mini-ETF from Grayscale and an exchange-traded fund from ProShares. It is expected that trading in the instruments could begin on 23 July. The products do not involve staking, but this could change in the future.

According to CoinGecko, meme tokens were the most popular narrative in the cryptocurrency ecosystem at the end of Q2, with a 14.34% share. This was followed by real-world tokenised assets (RWAs) with 11.3% and artificial intelligence tokens with 10.09%. CoinGecko noted Ethereum inflation – the market supply of ETH for April-June increased by 120,000 coins.