Sample Category Title

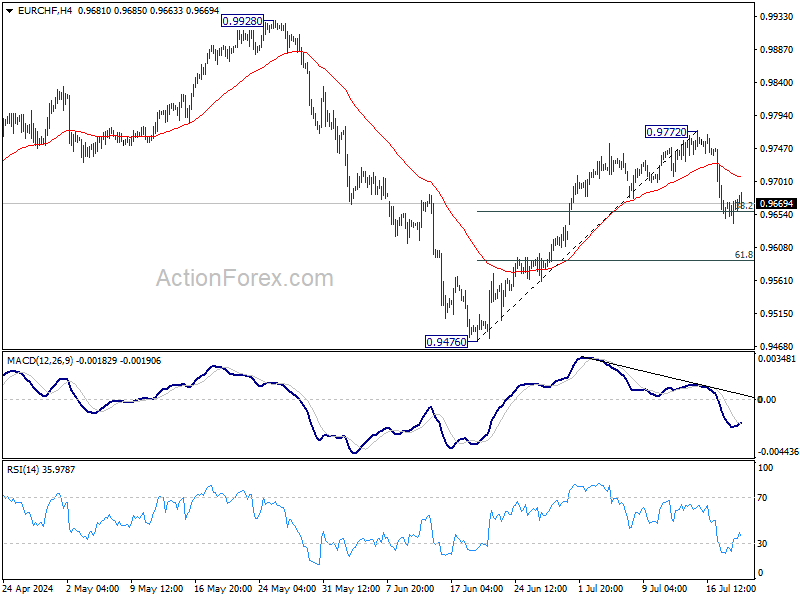

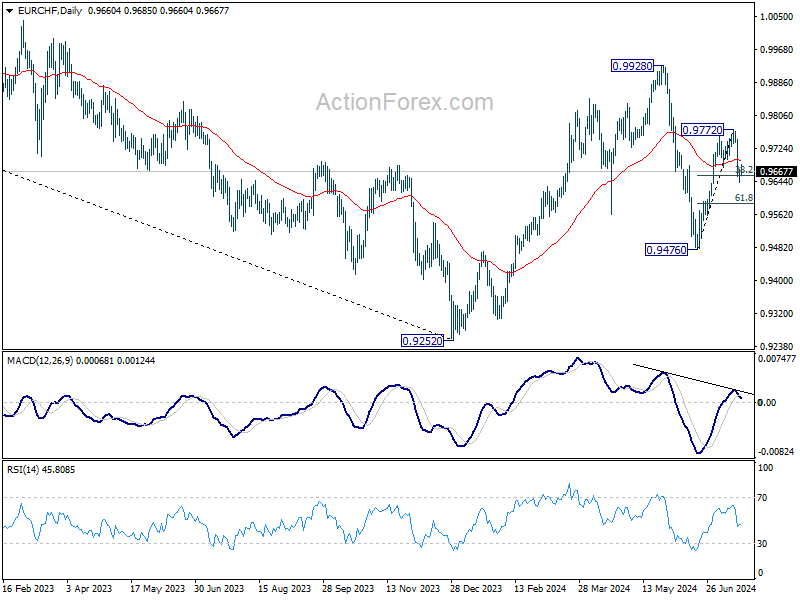

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9654; (P) 0.9664; (R1) 0.9686; More....

Intraday bias in EUR/CHF remains on the downside at this point. Break of 38.2% retracement of 0.9476 to 0.9772 at 0.9659 will extend the fall from 0.9772 to 61.8% retracement at 0.9589 and possibly below. On the upside, above 0.9772 will resume the rally from 0.9476 towards 0.9928 high instead.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.

ECB Meeting Non-Event from Market Point of View

Markets

The ECB kept its policy rates unchanged yesterday with President Lagarde saying that the outcome of the September meeting is “wide open”. The only sure thing is that they’ll lower the spread between the deposit rate and the main refinancing rate from currently 50 bps to 15 bps, as announced in March. Apart from that, it is data dependency to the fullest unlike the ECB’s strategy in April-June. A strong precommitment (in April) to cut interest rates a first time in June led to the awkward situation of eventually having to lower interest rates while simultaneously having to upwardly revise the headline and core inflation outlook and growth prospects. Markets don’t read too much into the ECB’s new tactics and stick to the view that a September policy rate cut is a near done deal. We see some reason for caution though with the central bank being worried about sticky and even strengthening underlying core and services inflation while the hoped-for wage moderation could take longer to unfold. Bloomberg yesterday evening also ran an article suggesting that ECB officials are increasingly wondering if they may only be able to cut interest rates once more this year. ECB Muller is the first official to hit the wires this morning. He said that he needs more confidence that inflation is going to 2% to cut policy rates again. He doesn’t pre-commit to a September move and doesn’t want to put a figure on the total amount of rate cuts we’ll get this year.

The ECB meeting was a non-event from a market point of view. Yesterday’s moves mainly occurred during US dealings. Both stocks and bonds were sold, giving a lifeline to the dollar who’s testing key support levels. On a trade-weighted basis, we look out whether the 104 neckline of a double top formation survives in the weekly close. A continuation of the risk-off/sell-all market setting could help the greenback further. Today’s eco calendar is empty apart from central bank speeches. Disappointing UK retail sales (-1.2% M/M & -0.2% Y/Y) add to lingering uncertainty on whether or not the BoE will be in a position to cut policy rates at its August 1st policy meeting. EUR/GBP moves somewhat further away from the 0.84 support area, changing hands at 0.8420.

News & Views

Japan’s consumer prices excluding volatile fresh food prices rose by 0.4% M/M, raising the Y/Y measure from 2.5% in May to 2.6% in June. It now trades at or above the BoJ’s 2% target since April 2022. Amongst others, the rise in Y/Y inflation was driven by the government reducing subsidies for energy/utility bills. Also important from a BoJ point of view, services inflation accelerated (0.2% M/M and 1.7% Y/Y). This might be an indication that higher wages are gradually filtering through into the overall price level. Headline inflation was unchanged at 2.8%. Still, both measures printed slightly below expectations. The core measure excluding fresh food and energy rose from 2.1% to 2.2%. Markets remain divided whether this gradual rise in inflation combined with mediocre growth will be enough for the BoJ to raise rates further already at the July 31 policy meeting (about 50% chance of a 0.1% rate hike). The Japanese government today lowered its growth forecast for the fiscal year ending April 2025 to 0.9% from 1.3% in January. Rising prices for imported consumer goods weigh on consumption. The government still expects the economy to grow 1.2% in the fiscal year 2025. After rebounding on broad USD-weakness and suspected yen-interventions last week and early this week, the yen now again trades in the defensive with USD/JPY at 157.65.

In its July monthly Bulletin, the Reserve Bank of India made an update of its estimate for the (real) natural interest rate. The new estimate was raised to a range of 1.4-1.9% and compares to a previous estimate of 0.8%/1% during the pandemic (estimate for Q4 2021). It is driven by a further increase in the potential growth rate of the economy. The RBI assesses that "when the policy rate is set below the natural rate, the stance is regarded as accommodative, and the converse signifies a restrictive stance. The policy stance is neutral when the real policy rate is at the level of the natural rate". June inflation printed at 5.08% Y/Y and the RBI policy rate currently stands at 6.5%. The RBI has an inflation target of 4%. In a separate article, the RBI indicated that it is prudent to stay on the straight and narrow path of aligning inflation to 4% rather than supporting economic growth via an easing of policy short-term.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on (at least) two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

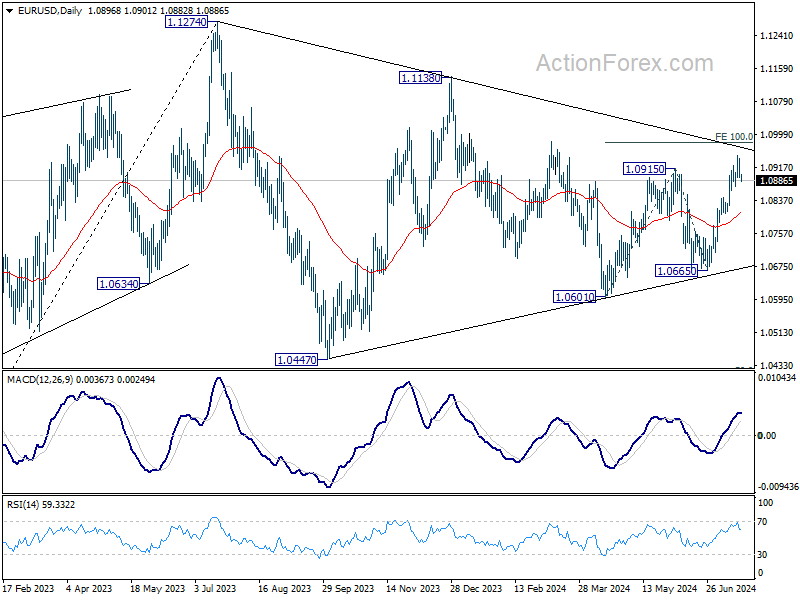

EUR/USD

EUR/USD is testing the topside of the 1.06-1.09 range as the dollar loses interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. Risks of a topside break are high, bringing the psychologic 1.10 and the December 2023 top at 1.1139 on the radar.

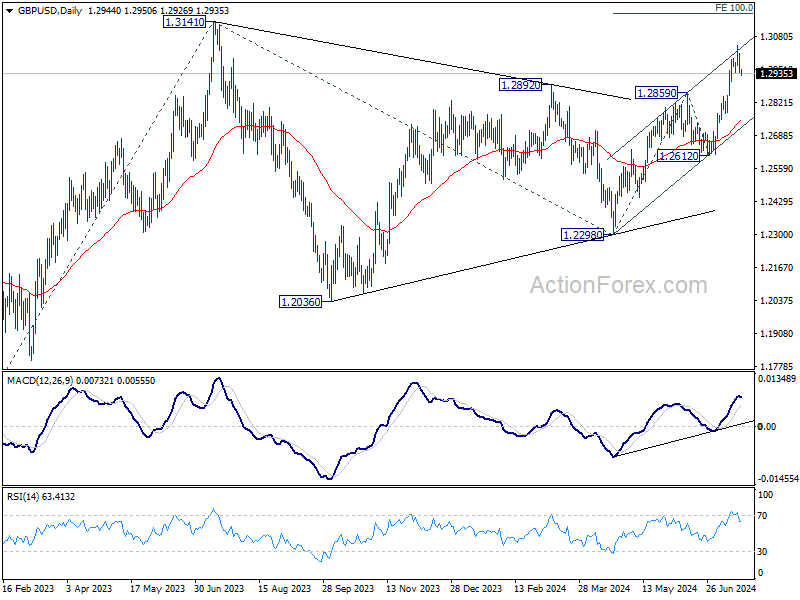

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 is support is being tested.

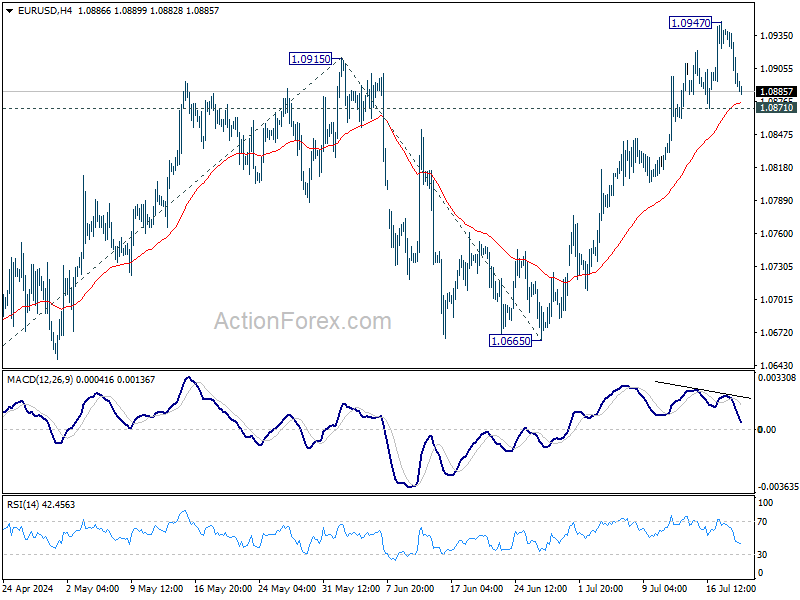

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0879; (P) 1.0911; (R1) 1.0928; More....

Intraday bias in EUR/USD remains neutral for consolidations below 1.0947 temporary top. Downside of retreat should be contained by 1.0871 support to bring another rally. On the upside, break of 1.0947 will resume the rise from 1.0601 and target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, firm break of 1.0871 will turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2915; (P) 1.2968; (R1) 1.2997; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.3043 temporary top. Downside of retreat should be contained by 1.2859 resistance turned support to bring another rally. Above 1.3043 will resume the rise from 1.2298 to 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

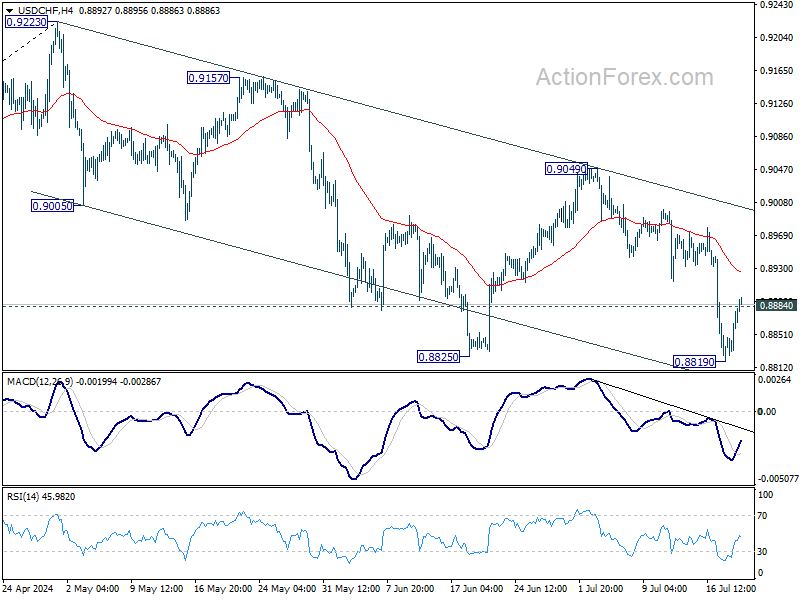

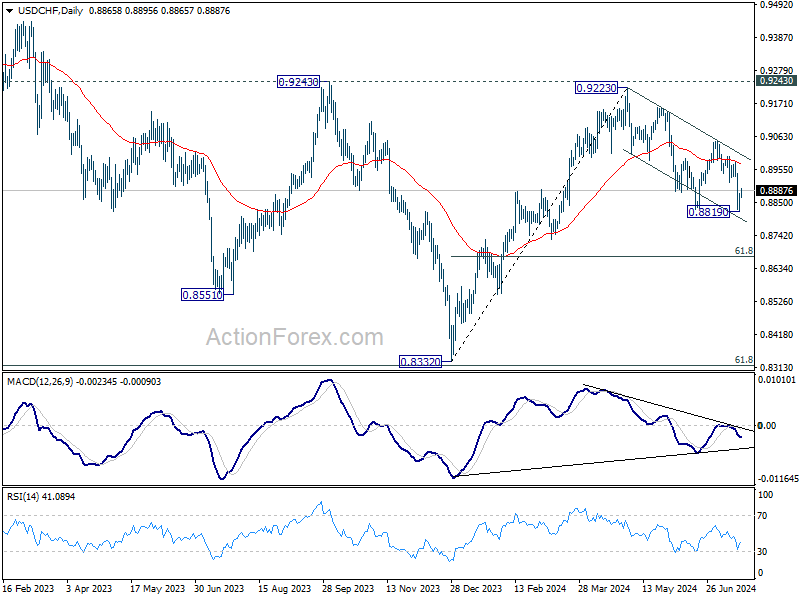

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8839; (P) 0.8859; (R1) 0.8898; More…

Intraday bias in USD/CHF is turned neutral first with current recovery and break of 0.8884 minor resistance. Some consolidations would be seen above 0.8819 temporary low. But further decline is expected as long as 0.9049 resistance holds. Break of 0.8819 will resume the fall from 0.9223 to 60% retracement of 0.8332 to 0.9223 at 0.8672 next.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

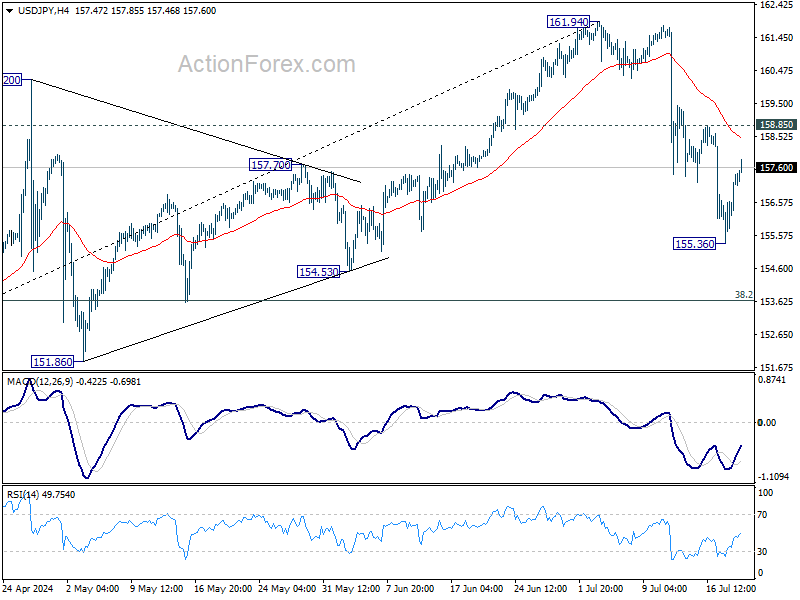

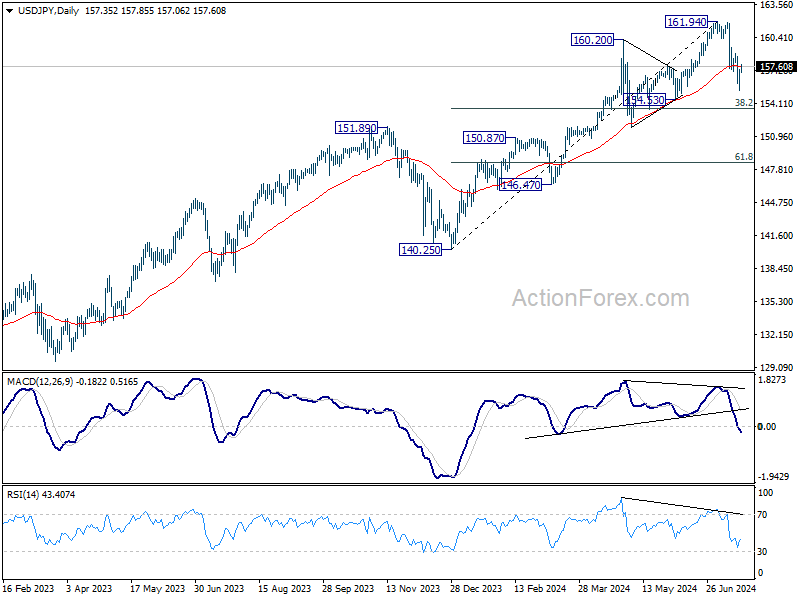

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.29; (P) 156.95; (R1) 157.84; More...

USD/JPY rebounded after dipping to 155.36 and intraday bias is turned neutral first. Deeper decline is still expected as long as 158.85 resistance holds. Below 155.36 will extend the fall from 161.94, as a correction to rally from 140.25, to 38.2% retracement of 140.25 to 161.94 at 163.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

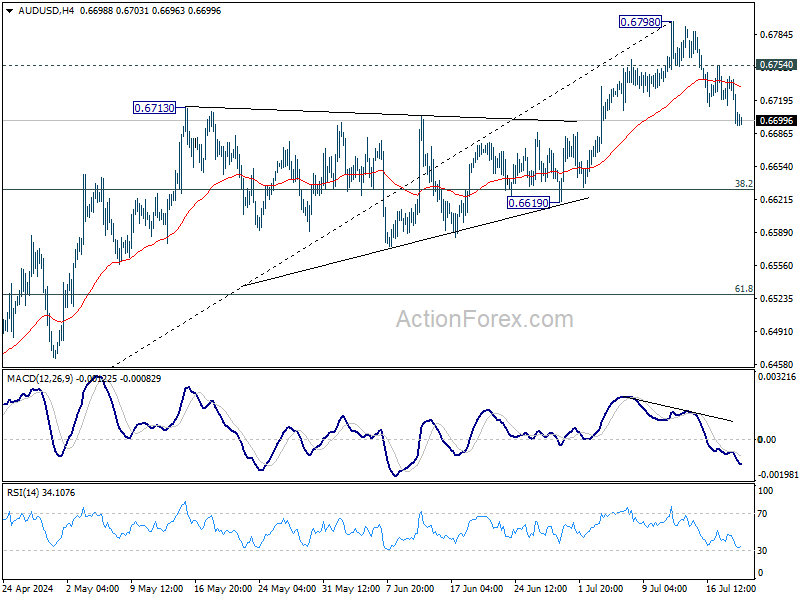

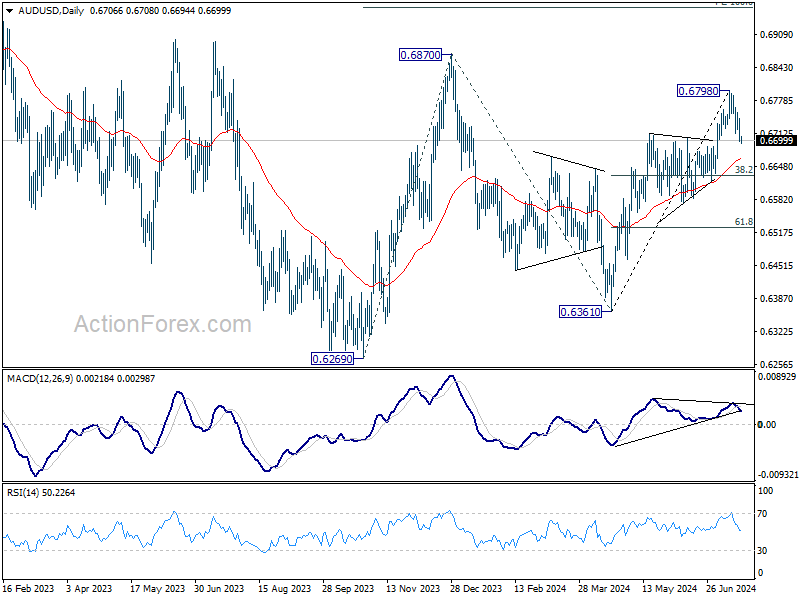

AUD/USD Daily Report

Daily Pivots: (S1) 0.6688; (P) 0.6716; (R1) 0.6734; More...

Break of 0.6713 resistance turned support indicates short term topping at 0.6798, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 38.2% retracement of 0.6361 to 0.6798 at 0.6631. Strong rebound would be seen there to bring rebound. On the upside, above 0.6754 minor resistance will turn bias back to the upside for retesting 0.6798.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

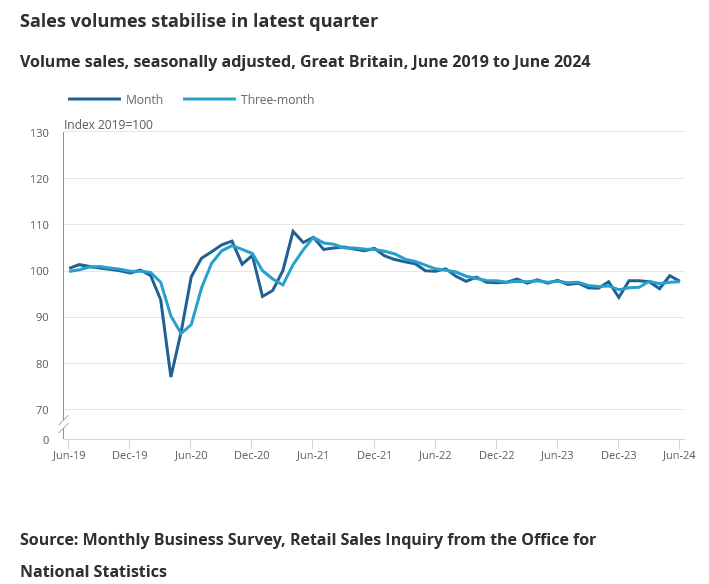

UK retail sales falls -1.2% mom in Jun, down -0.2% yoy in Q2

UK retail sales volume fell -1.2% mom in June, worse than expectation of -0.6% mom. Sales volumes fell across most sectors, with department stores and clothing retailers broadly returning to their Q1 levels. It's -1.3% below their pre-pandemic levels in February 2020.

Looking at the quarter, sales volumes fell by -0.1% qoq and -0.2% yoy in Q2.

Cliff Notes: The Emergence of Slack

Key insights from the week that was.

It was a relatively quiet week in Australia, with the June Labour Force Survey the only market sensitive date release. The main surprise in the report was labour supply’s strength, evinced by the participation rate printing its second-highest read for the cycle at 66.9%. The level of employment also rose at a solid clip in June, up +50.2k for a cumulative gain of a quarter-million over H1 2024, the same pace as H1 2023 when the labour market was much ‘tighter’. It is worth noting that employment is behaving as expected given the trend in participation – the percentage increase in both measures over the last three months is well within the historical range. While both were robust, labour supply slightly outstripped demand in the month, resulting in the unemployment rate just rounding up to 4.1%.

These results are unlikely to drive any material change in the RBA’s view of the labour market, which is currently assessed as “tight relative to full employment”. Employment has transitioned from outpacing population growth to now tracking broadly in line, pointing to balance between labour demand and supply. The unemployment rate gradually ticking higher, as a consequence of labour supply outstripping still-resilient labour demand, is consistent with the RBA achieving a ‘soft’ landing. Looking ahead, the Q2 CPI (due July 31) will prove critical to assessing the near-term outlook for policy. In this week’s essay, Chief Economist Luci Ellis discusses recent international developments with disinflation and the similarity of Australia’s experience.

Across in New Zealand, this week’s Q2 CPI shifted the debate around the policy outlook. The below expectations Q2 print of 0.4% resulted in annual inflation moderating from 4.0%yr in Q1 to 3.3%yr in Q2. Our New Zealand team now expects annual inflation to fall below 3.0%yr in Q3 and to then continue to decelerate towards 2.0%yr into 2025. This trend will allow the RBNZ to place a greater weight on activity data, which has been recessionary for a few months, and to bring forward their first cut to November. Westpac NZ economics sees an earlier cut in October as around a 30% chance.

Further afield, the European Central Bank kept rates steady at their July meeting and made clear policy would be decided meeting by meeting. At this stage, September is regarded as “wide open”. President Lagarde also emphasised the ECB is looking at a range of data not one particular variable. The Governing Council view policy as restrictive. The Bank Lending Survey, released earlier in the week, support this perspective, highlighting that credit conditions are tight and loan demand sluggish, particularly among corporates. Going ahead, the ECB will be mindful of underlying strength in the labour market and an expected acceleration in activity growth into 2025; but inflation trending sustainably to target should instil confidence in a succession of rate cuts towards neutral.

In the UK meanwhile, key data ahead of the August meeting made clear the complexity of the task before the Bank of England. The headline CPI rose 2.0%yr in June, consistent with the May print and their medium-term policy target. However, both core inflation and services inflation remained unchanged at an elevated level, 3.5%yr and 5.7%yr respectively. Wages also rose 5.7%yr in May, continuing their downtrend but still elevated versus history. Significant further progress with wages is necessary to quell services inflation. In this light, while annual headline inflation is at target, the Bank of England may choose to hold in August and wait to September to cut. The August decision is likely to be finely balanced; the market views it as such, with a cut seen as a roughly 50/50 proposition.

US retail sales were flat in June after an upward revision in May from 0.1% to 0.3%. The sales control group, which feeds into GDP calculations, was robust at 0.9% in June, up from 0.4% in May. Though, year-to-date, growth in control group sales remains weak, having averaged a gain of around 0.2% per month, less than half of 2023's pace. While decelerating inflation and the promise of rate cuts are supportive of spending, growing uncertainty over the labour market should restrict consumption to a modest pace through the remainder of 2024.

Taking a broader view, the FOMC's Beige Book for July signalled the economy is softening and price conditions are consistent with a return to target inflation. Respondents noted that activity was maintaining "a slight to modest pace" in aggregate, but five districts reported "flat or declining activity". On employment, "Most districts reported employment was flat or up slightly" and wages grew at a "modest to moderate pace", in part because of improved labour availability. Price increases were "modest" overall, with a "couple" of districts noting only "slight increases".

Finally to China, where the economy expanded 0.7%qtr in Q2 and 5.0% year-to-date. This puts the economy on track to achieve the 5.0% growth target set for 2024 overall, even without active government support. Growth is being fuelled by capacity expansion and a drive to increase value add, principally to meet foreign demand. Fixed asset investment growth of 8.5%ytd (excluding property) against a 10% decline in property investment and retail sales growth of just 3.7%ytd highlights that the consumer has, to date, missed out on the dividends from trade. As we discuss in our note, this situation has to change if downside risks are to be extinguished and the government’s medium-term objectives for the whole economy met.

This week also saw the conclusion of China's latest Plenum. There was no change in the priorities of officials, with “high-quality development” remaining the focus and the property market receiving little attention. The reference to "actively expanding domestic demand" does not necessarily mean the consumer will receive immediate or significant support. Rather, it is more likely the central Government will focus on public and private investment, anticipating this activity will support employment and confidence and consequently stronger consumer demand. Further detail is likely to be provided in coming weeks, with a Politburo meeting scheduled for month end.

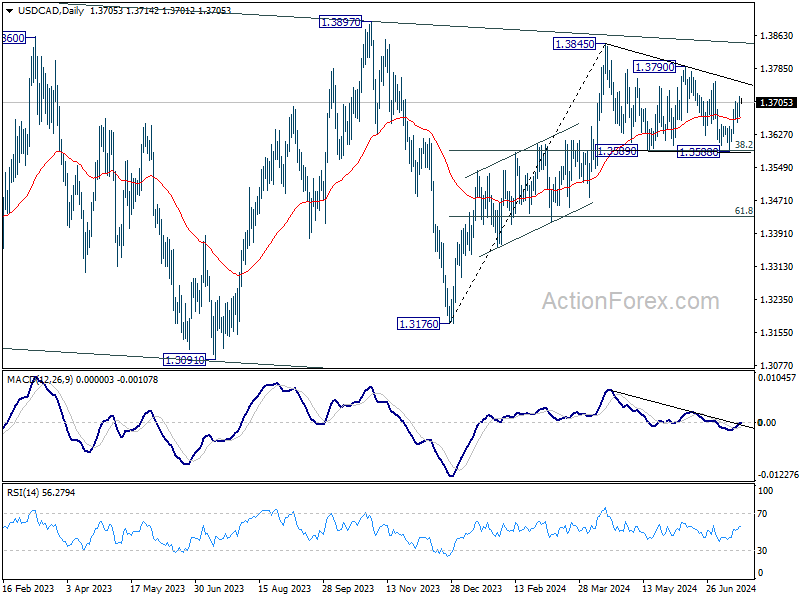

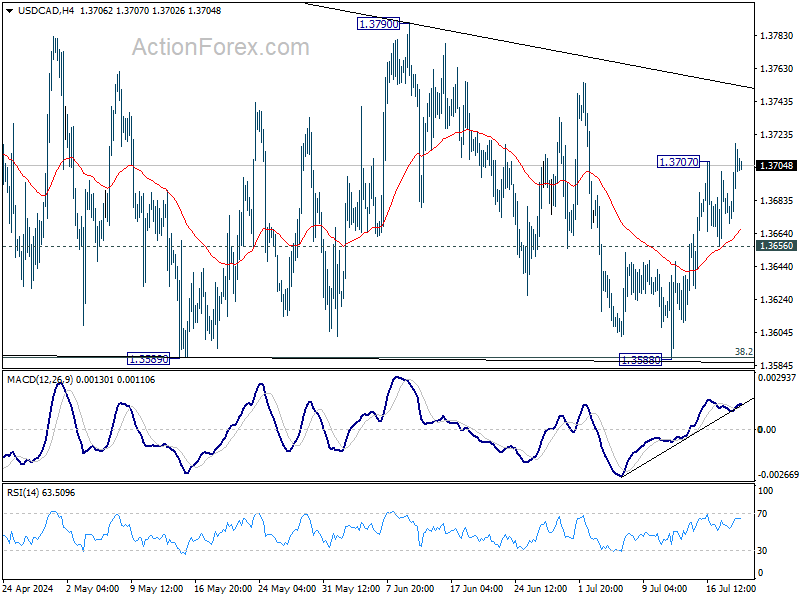

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3678; (P) 1.3698; (R1) 1.3727; More...

USD/CAD's rebound from 1.3588 resumed by breaking 1.3707 temporary top and intraday bias back on the upside. Outlook is unchanged that corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Further rise is expected to 1.3790 resistance first. Break there will larger rise from 1.3716 is ready to resume through 1.3845.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.