Sample Category Title

EUR/USD Daily Outlook

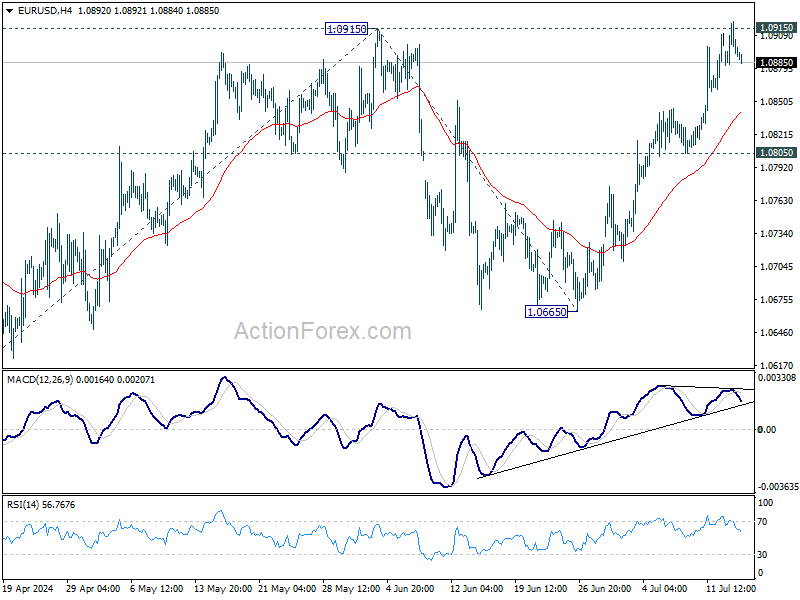

Daily Pivots: (S1) 1.0877; (P) 1.0900; (R1) 1.0916; More....

EUR/USD breached 1.0915 briefly but retreated since then. With 4H MACD crossed below signal line, intraday is turned neutral first. Some consolidations would be seen but further rally is expected as long as 1.0805 support holds. Firm break of 1.0915 will resume whole rise from 1.0601 to 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, break of 1.0805 will turn bias back to the downside for deeper pullback.

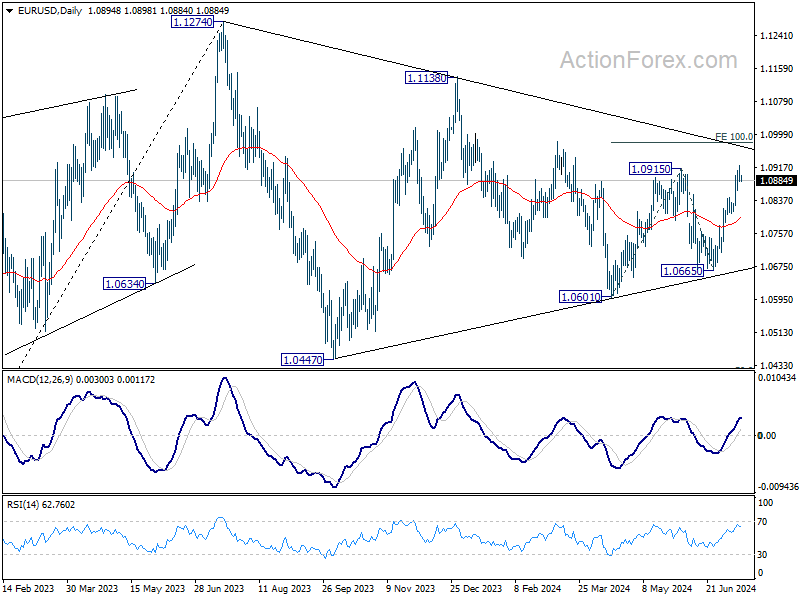

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

GBP/USD Daily Outlook

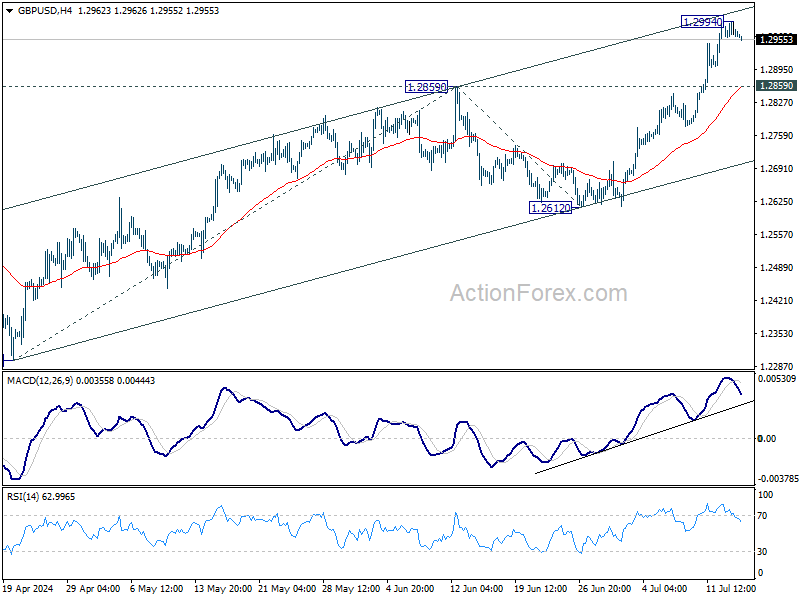

Daily Pivots: (S1) 1.2955; (P) 1.2975; (R1) 1.2988; More...

Intraday bias in GBP/USD is turned neutral first with current retreat. Some consolidations would be seen below 1.2994 temporary top first. But further rally is expected as long as 1.2859 resistance turned support holds. Above 1.2994 will resume the rally from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, break of 1.2859 will turn bias to the downside for deeper pullback.

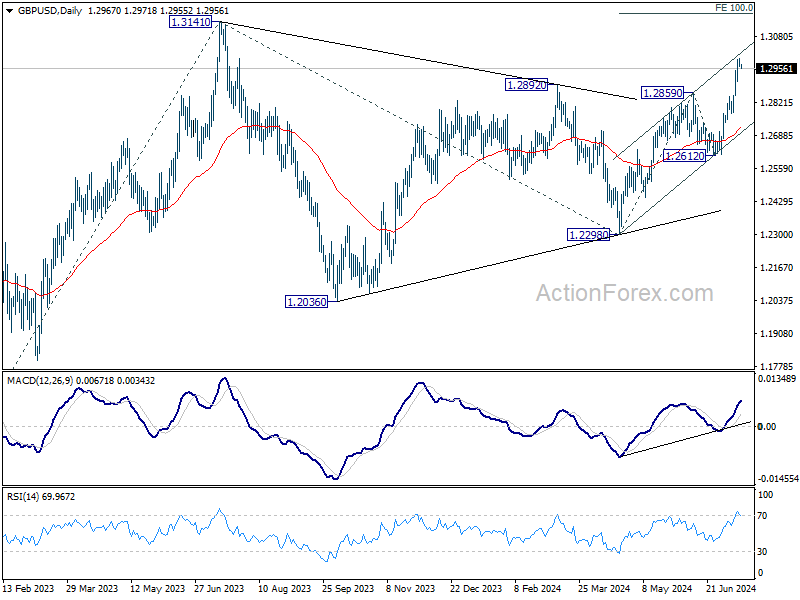

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

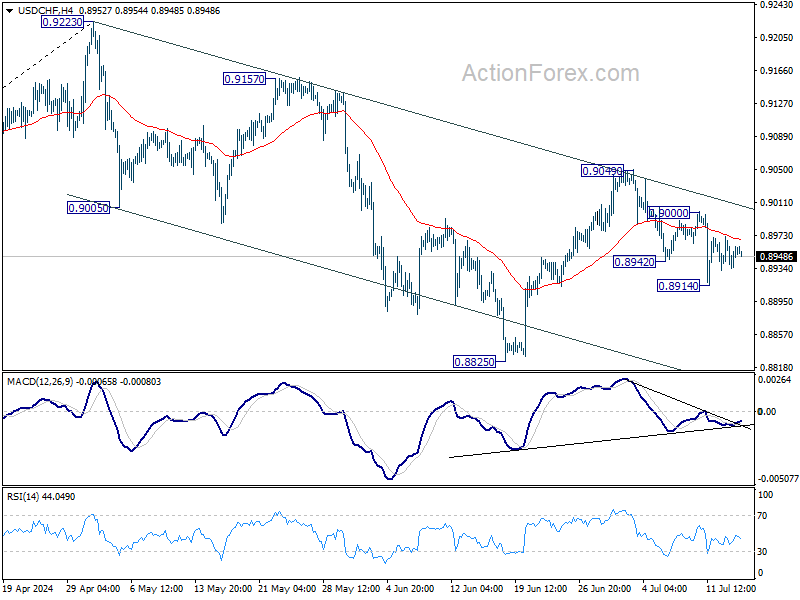

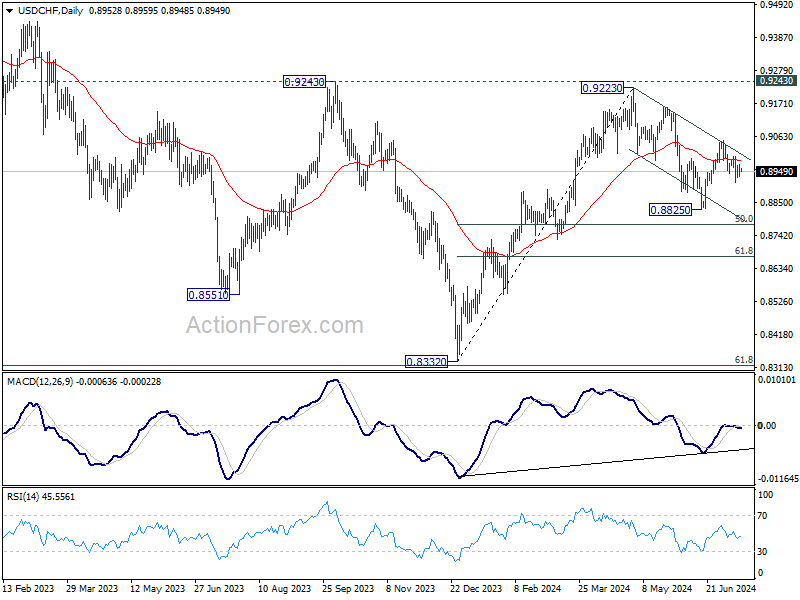

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8937; (P) 0.8955; (R1) 0.8975; More…

Intraday bias in USD/CHF remains neutral and further decline is expected with 0.9000 resistance intact. Below 0.8914 will target 0.8825 low. Break of 0.8825 will target 50% retracement of 0.8332 to 0.9223 at 0.8778 next. However, break of 0.9000 will turn bias back to the upside for 0.9049 resistance instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

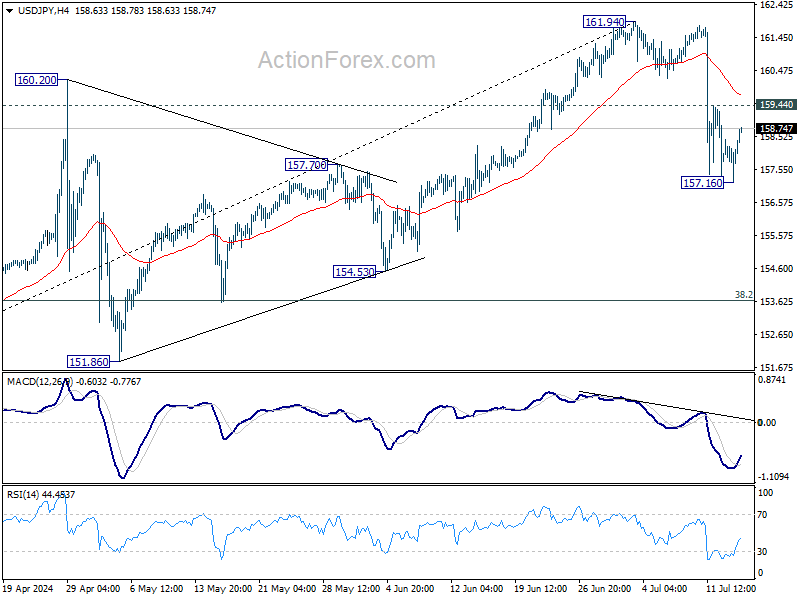

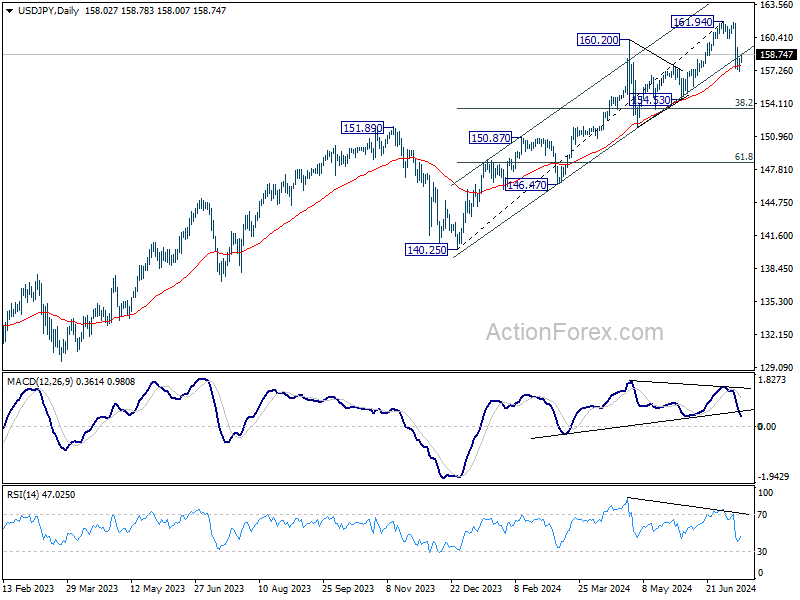

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.32; (P) 157.88; (R1) 158.57; More...

USD/JPY quickly recovered after dipping to 157.16. With 4H MACD crossed above signal line, intraday bias is turned neutral first. On the downside, break of 157.16 and sustained trading below 55 D EMA (now at 157.72) will bring deeper correction to 38.2% retracement of 140.25 to 161.94 at 163.65. But strong support should be seen there to bring rebound. Meanwhile, break of 159.44 minor resistance will turn bias back to the upside for stronger rebound towards 161.94 high.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

Yen Softens as Rebound Fades; Loonie Looks to Canadian CPI

Yen weakened broadly during Asian session today, giving back some of last week's strong gains that were reportedly driven by Japan's market intervention. Japan's Chief Cabinet Secretary Yoshimasa Hayashi repeated in a press conference that it is crucial for currency rates to move "stably" and reflect economic fundamentals. He reiterated the government's commitment to taking necessary measures against speculative moves in Yen's exchange rate.

Despite these warnings, it appears Japan might be comfortable with Yen at its current levels and is unlikely to take further action to push it higher against Dollar. If this view is correct, the range is probably set for USD/JPY to consolidate in the near term.

Meanwhile, Canadian dollar is in the spotlight today with the release of Canada's CPI data. In May, core inflation measures unexpectedly jumped just after BoC became the first G7 central bank to cut interest rates on June 5. However, subsequent job data revealed minimal growth and a rise in unemployment rate. If today's CPI data show that disinflation is back on track, BoC could be in a position to cut interest rates again next week.

Elsewhere, Swiss franc and Dollar are currently the strongest performers of the day, followed by Loonie. Yen is the weakest, followed by Kiwi and Aussie, both of which are weighed down by disappointing GDP data from China this week. Euro and Sterling are positioned in the middle.

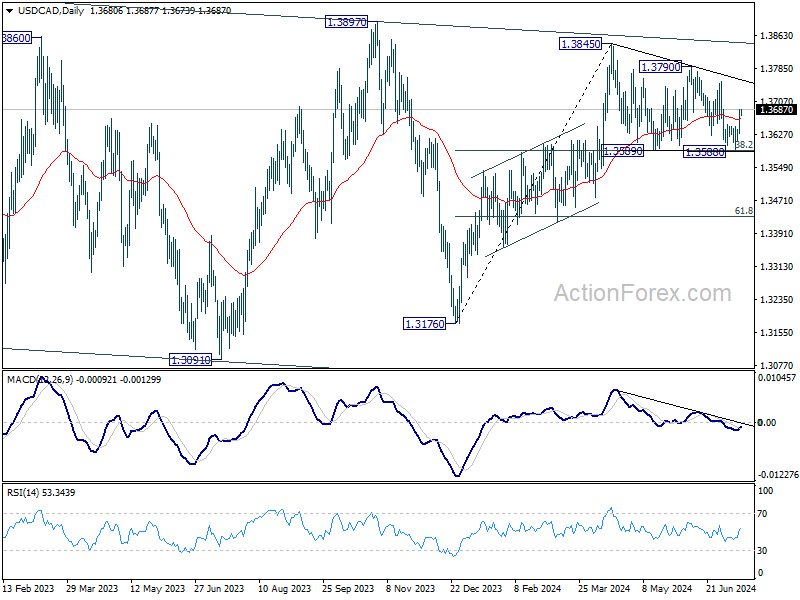

Technically, USD/CAD's strong rebound this week and break of 55 D EMA raises the chance that corrective pattern from 1.3845 has completed with three waves to 1.3588. That came after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Near term focus is back on 1.3790 resistance. Decisive break there will argue that rise from 1.3716 is ready to resume through 1.3845.

In Asia, at the time of writing, Nikkei is up 0.28%. Hong Kong HSI is down -1.35%. China Shanghai SSE is down -0.31%. Singapore Strait Times is down -0.43%. Japan 10-year JGB yield is down -0.0204 at 1.030. Overnight, DOW rose 0.53%. S&P 500 rose 0.28%. NASDAQ rose 0.40%. 10-year yield rose 0.040 to 4.229.

Fed's Powell: Q2 inflation data do add somewhat to confidence

Fed Chair Jerome Powell, speaking at an event overnight, highlighted that in Q2, the economy made "some more progress" on taming inflation. He noted that there have been "three better readings" on inflation, averaging them places Fed in a "pretty good place."

Powell reiterated that it wouldn't be appropriate to start loosening policy until there is greater confidence that inflation is sustainably returning to 2% target. However, he also acknowledged that Q2's data "do add somewhat to confidence".

Fed's Daly sees growing confidence in inflation control

San Francisco Fed President Mary Daly, speaking at a conference overnight, expressed optimism about the Fed's progress in controlling inflation. "Confidence is growing that we are getting nearer a sustainable pace of getting inflation back down to 2%," Daly noted.

However, she refrained from providing specific timelines or numbers for potential rate cuts. "I'm not going to give time-based guidance. I'm not going to tell you when the rate cut is, how many rate cuts might come," Daly stated.

"Over time, as inflation comes down and the labor market slows, we have to make sure that we're holding rates high enough that we don't lose that inflation fight, but not hold them too long and risk worsening the labor market to a point where it's challenging for people to get jobs," Daly added.

Looking ahead

Eurozone will release trade balance while Germany will publish ZEW economic sentiment in European session. Later in the day, Canada CPI will take center stage. US retail sales, import prices, business inventories and NAHB housing index will also be featured.

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.32; (P) 157.88; (R1) 158.57; More...

USD/JPY quickly recovered after dipping to 157.16. With 4H MACD crossed above signal line, intraday bias is turned neutral first. On the downside, break of 157.16 and sustained trading below 55 D EMA (now at 157.72) will bring deeper correction to 38.2% retracement of 140.25 to 161.94 at 163.65. But strong support should be seen there to bring rebound. Meanwhile, break of 159.44 minor resistance will turn bias back to the upside for stronger rebound towards 161.94 high.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M May | -0.4% | 0.20% | 1.90% | 2.20% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 20.3B | 19.4B | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | 44.3 | 47.5 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jul | -73 | -73.8 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | 50.2 | 51.3 | ||

| 12:15 | CAD | Housing Starts Y/Y Jun | 259K | 265K | ||

| 12:30 | CAD | CPI M/M Jun | 0.10% | 0.60% | ||

| 12:30 | CAD | CPI Y/Y Jun | 2.90% | |||

| 12:30 | CAD | CPI Median Y/Y Jun | 2.70% | 2.80% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jun | 2.80% | 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y Jun | 2.40% | 2.40% | ||

| 12:30 | USD | Retail Sales M/M Jun | -0.20% | 0.10% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Jun | 0.10% | -0.10% | ||

| 12:30 | USD | Import Price Index M/M Jun | 0.20% | -0.40% | ||

| 14:00 | USD | Business Inventories May | 0.30% | 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Jul | 44 | 43 |

Fed’s Daly sees growing confidence in inflation control

San Francisco Fed President Mary Daly, speaking at a conference overnight, expressed optimism about the Fed's progress in controlling inflation. "Confidence is growing that we are getting nearer a sustainable pace of getting inflation back down to 2%," Daly noted.

However, she refrained from providing specific timelines or numbers for potential rate cuts. "I'm not going to give time-based guidance. I'm not going to tell you when the rate cut is, how many rate cuts might come," Daly stated.

"Over time, as inflation comes down and the labor market slows, we have to make sure that we're holding rates high enough that we don't lose that inflation fight, but not hold them too long and risk worsening the labor market to a point where it's challenging for people to get jobs," Daly added.

Fed’s Powell: Q2 inflation data do add somewhat to confidence

Fed Chair Jerome Powell, speaking at an event overnight, highlighted that in Q2, the economy made "some more progress" on taming inflation. He noted that there have been "three better readings" on inflation, averaging them places Fed in a "pretty good place."

Powell reiterated that it wouldn't be appropriate to start loosening policy until there is greater confidence that inflation is sustainably returning to 2% target. However, he also acknowledged that Q2's data "do add somewhat to confidence".

Gold Regains Strength: Poised for Continued Gains?

Key Highlights

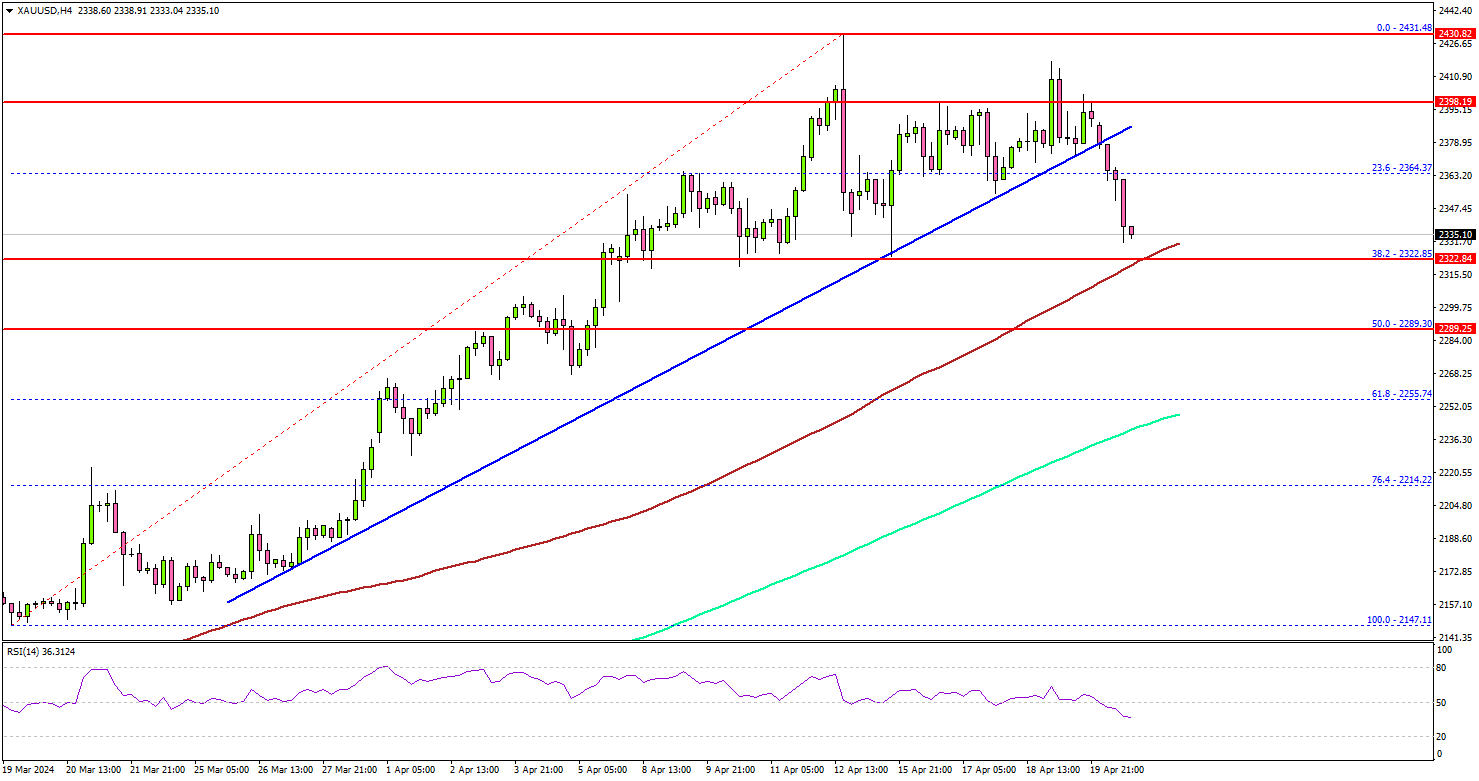

- Gold is gaining bullish momentum above the $2,400 support zone.

- A key bullish trend line is forming with support at $2,395 on the 4-hour chart.

- EUR/USD could continue to rise toward the 1.1000 resistance.

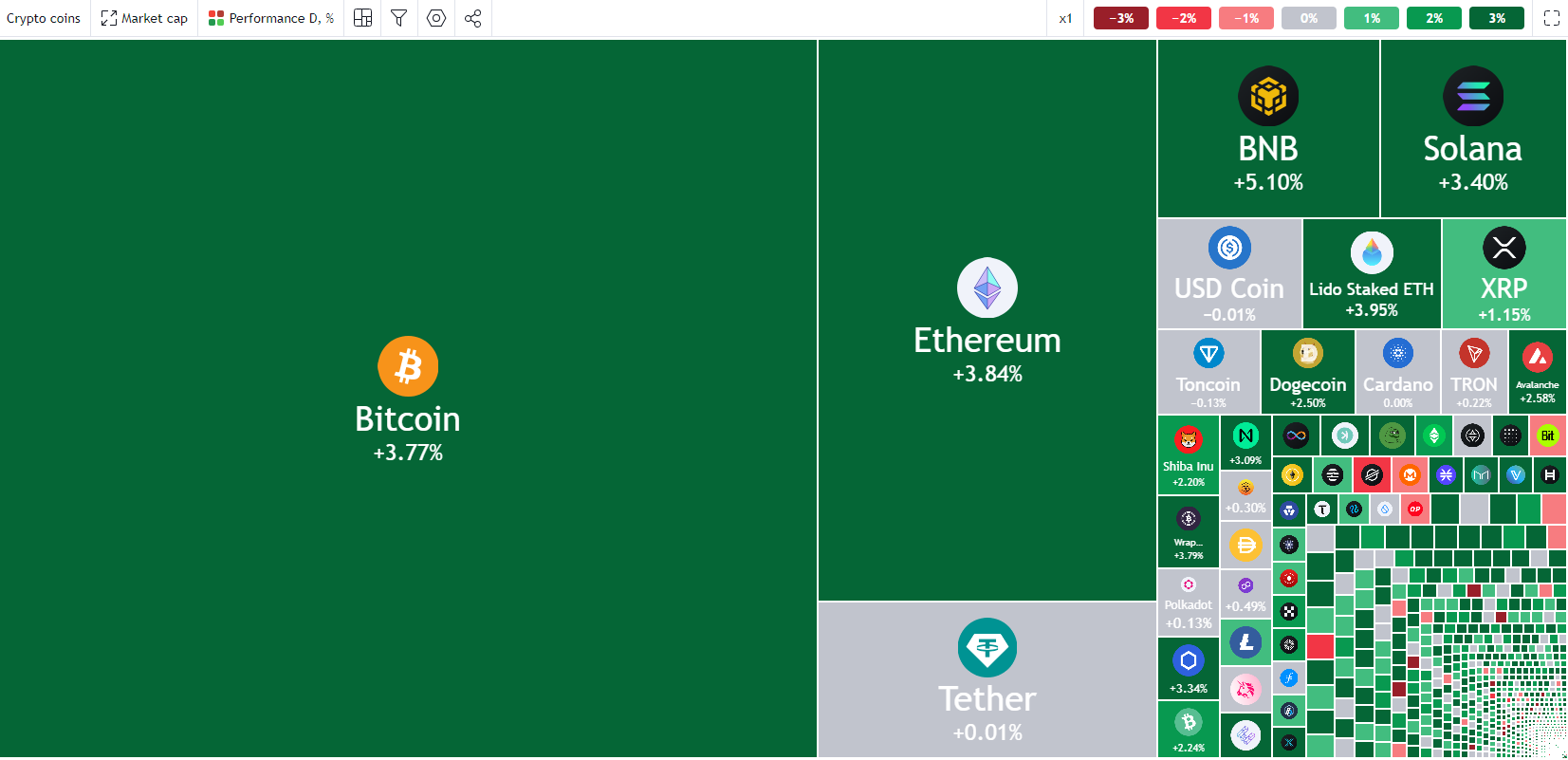

- Bitcoin recovered and broke the $64,000 resistance zone.

Gold Price Technical Analysis

Gold prices remained well-supported above the $2,350 zone against the US Dollar. The bulls were able to push the price above the $2,380 and $2,400 resistance levels.

The 4-hour chart of XAU/USD indicates that the price even cleared the $2,420 level and settled well above the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

The current price action suggests that the bulls could aim for a move toward the $2,440 level. The next major resistance sits near the $2,450 level.

A clear move above the $2,440 resistance could open the doors for more upsides. The next major resistance could be near $2,450, above which the price could accelerate higher toward the $2,465 level. Any more gains might send Gold toward the $2,500 resistance.

On the downside, there is a key support forming near the $2,400 level. There is also a major bullish trend line forming with support at $2,395 on the same chart.

A downside break below the $2,395 support might call for more downsides. The next major support is near the $2,380 level. Any more losses might send gold prices toward $2,365.

Looking at Bitcoin, the bulls took control, and they were able to push the price above the $64,000 resistance zone. The next major hurdle is at $65,000.

Economic Releases to Watch Today

- Eurozone ZEW Business Economic Sentiment Index for July 2024 – Forecast 48.1, versus 51.3 previous.

- US Retail Sales for June 2024 (MoM) – Forecast 0%, versus +0.1% previous.

China Q2 2024: Diverging Sectors and Risks

China’s Q2 activity data again highlighted disparate conditions across the economy. New industry continues to surge ahead, but the consumer is being left behind.

China GDP disappointed in Q2, gaining 0.7% after a 1.6% increase in Q1. Year-to-date at June, growth of 5.0% is down from 5.3% in March, but still consistent with authorities ambitions for 2024. This is despite support from the Government remaining passive.

Aggregate growth remains dependent on trade and business investment, particularly in high-tech sectors of the economy. While the trade surplus narrowed significantly through Q1, creating a headwind for growth in Q2, in May and June the surplus widened again, setting up support for Q3 GDP.

Strength and breadth in export growth continues to justify further investment in capacity across numerous sub-sectors of manufacturing and the infrastructure which supports industry and society more broadly. Year-to-date fixed asset investment at June was a sub-par 3.9%. However, excluding the 10.1%ytd contraction in property, investment was up a strong 8.5%ytd. Underlying this result is 10.1%ytd and 11.7%ytd gains for high-tech manufacturing and high-tech services respectively. Utilities investment (including power generation and transmission) is meanwhile up 24.2%ytd and other infrastructure 5.4%ytd.

The above outcomes speak to the private sector and state-owned enterprises putting the Government’s long-term plan to increase value add and efficiency across the economy into action, targeting capacity expansion in areas where China has a nascent global competitive advantage such as goods production tied to the green transition. It is certainly paying dividends for industry, but the extent and timing of gains for ordinary households remains an open question.

The PMI’s employment measures and other labour market data make clear that aggregate employment is yet to materially benefit from this capacity expansion, new jobs in the sector at best offsetting weakness in residential construction and manufacturing sub-sectors that have lost their advantage to developing Asia. Firms exposed to local consumer demand also find themselves unable to scale up hiring or investment with spending growth weak and the outlook highly uncertain.

Although employment growth is largely stagnant, the NBS reports that household disposable income rose more than 5% on both a nominal and real basis over the year to June. With retail sales only up 3.7% year-to-date in H1 2024 (and just 2.0% over the year to June), a lack of job creation is clearly not the only factor holding back consumption and housing investment; anxiety over wealth is also critical. The latter is unsurprising given new and existing home prices have been falling consistently for close to three years and property investment is now down more than 20% since mid-2022.

There are two key points to take from the above. (1) Despite the headwinds created by the property sector and wealth, and in the absence of active support from the Government, to date in 2024 China’s ‘new economy’ has achieved authorities’ aggregate growth ambitions. (2) But, increasingly risks are skewing to the downside – growth in the new economy inevitably will slow and consumer weakness increasingly looks entrenched. Beginning with this week’s Plenum, it is important that authorities show greater initiative and urgency with policy so as to begin to rebuild trust in the property sector and to make clear that the benefits of trade will, in time, flow to all of society. Unlikely this week, but also necessary in time, is confidence in the outlook for China’s equity markets. A greater use of equity capital by firms and increased ownership of equities by households is the surest way to transmit trade gains broadly and sustainably across the economy.

As a result of the weakness in consumption and with considerable trade risks into year end, we have edged down our growth forecasts for 2024 and 2025, from 5.2% and 5.0% to 5.0% and 4.9%, respectively. Achieving these outcomes will require a material near-term policy adjustment to strengthen consumer spending and stabilise both residential construction and household wealth. If achieved, downside risks will abate and may turn net positive in 2025. But, if policy makers continue to hold back, risks are likely to skew further to the downside and begin to crystalise.

Bitcoin (BTC/USD) Soars Amidst Surging ETF Inflows

- Increased investor confidence fueled by a $1.04 billion inflow into Bitcoin Spot ETFs.

- Bitcoin miners, particularly in the US, are accumulating Bitcoin in anticipation of another potential rally, with Marathon Digital Holdings aiming to significantly increase its hashrate.

- Technically, Bitcoin’s breakout above a long-term descending trendline suggests further upside potential.

Bitcoin prices enjoyed somewhat of a renaissance over the weekend bursting back above the 60k mark and taking out some key technical hurdles in the process.

Bitcoin Spot ETF Net Inflow (USD) data reveals an inflow of $1.04 billion last week, indicating rising investor confidence and potentially suggesting a short-term increase in Bitcoin’s price. Market participants are also hoping that an approval of the ETH ETF may lead to further inflows in the days and weeks ahead as market participants diversify their crypto holdings.

Source: TradingView.com (click to enlarge)

The conclusion of the German Government’s Bitcoin sales provided some relief, but ongoing uncertainty regarding Mt.Gox repayments might still pose challenges for bullish investors.

The attack on US Presidential Candidate Donald Trump further fueled the Bitcoin recovery. Trump has vowed to allow miners to remain active while also confirming that he will ensure every American has the right to self-custody of their digital assets and transact free from Government control. Given the probability of a Trump election rising it is no surprise that sentiment in the crypto space received a significant boost. Marathon holds 18,536 Bitcoin worth over $1 billion, up 48% from 2023’s total of 12,538.

Bitcoin miners are also in a race against time and their own competition when it comes to upping Bitcoin mining capacity. Companies such as Marathon and CleanSpark are looking to up their hashrate to improve their mining output.

Miners Opt to Accumulate Bitcoin

Bitcoin miners in the US are accumulating Bitcoin as market participants eye another rally. There are big names on the list like Marathon Digital Holdings whose CFO mentioned that Bitcoin is different from other asset classes when it comes down to what to consider. Marathon is targeting a hashrate of 50 (EH/s) by the end of 2024, up from a 31.5 (EH/s).

Bitcoin advocate and influencer Michael Saylor returned to the spotlight as Bitcoin began its latest move. The co-founder and the Executive Chairman of business intelligence giant MicroStrategy has taken to his account on the X platform to comment on the Bitcoin price increase that began on Sunday.

A simple message but clearly Saylor sees more upside ahead for BTC/USD.

Technical Analysis BTC/USD

From a technical standpoint, Bitcoin has surged above the long-term descending trendline, suggesting further upward potential. However, the rally faces strong resistance just below the crucial 65k level, where both the 50-day and 100-day moving averages (MAs) are positioned.

If the MAs reject the price, Bitcoin could retrace to the support levels at 61,750 or 59,300, aligning with the 200-day MA. This would also involve a retest of the trendline, which did not occur after the breakout.

Should Bitcoin surpass the 65,000 mark, the next key levels on the upside would be the 70,000 and 71,900 handles.

Support

- 61750

- 59311 (200-day MA)

- 56561

Resistance

- 64030

- 65000

- 70000 (psychological level)

- 71935

Bitcoin (BTC/USD) Daily Chart, July 15, 2024

Source: TradingView.com (click to enlarge)