Sample Category Title

Bitcoin and Ethereum Test 50-Day MAs

Market Picture

The crypto market has rallied nearly 2% over the past 24 hours to a $2.34 trillion cap, with the slippage at the start of the day pushing the figure to $2.38 trillion, a level last seen on June 20th.

Bitcoin and Ethereum are testing their 50-day moving averages on Tuesday after retreating from the more important 200-day MA. A major correction and upside reversal has already finished earlier this month, so the $63K per BTC and $3500 per ETH levels now look like a temporary shakeout of positions but not impenetrable resistance.

According to data from CoinShares, crypto fund investments rose by $1.439 billion last week, following inflows of $441 million the previous week; the figure marked the second week of growth and was the fifth-largest weekly inflow on record. Investments in Bitcoin rose by $1.347 billion, Ethereum by $72 million, and Solana by $4 million, with Ethereum seeing the largest inflows since March, likely in anticipation of the imminent approval of spot ETH ETFs in the US.

News Background

However, weekly trading volume remained low at $8.9 billion, compared to this year’s average of $21 billion, CoinShares noted.

BlackRock CEO Larry Fink said Bitcoin is a legitimate financial instrument to invest in during times of heightened fear. BTC offers a way to invest “in something outside the control of any country.”

IntoTheBlock calculates that Bitcoin miners added $71K BTC to their wallets last week against a backdrop of falling prices. CryptoQuant noted that the 30-day coin accumulation rate was the highest since April 2023. Santiment cited a reduction in long positions by retail traders, which should support the long-term bullish trend.

At the same time, Whale Alert recorded the activation of a wallet that had been dormant for almost 12 years, moving 1,000 BTC worth ~$60 million.

Retail investors are underestimating Ethereum, which could reach a new high faster than other assets due to institutional demand, according to Michael van de Poppe. He expects spot Ethereum ETFs to be approved in the US this week.

Bernstein advises buying shares in companies in this segment because the “Trump factor” is creating an ideal economic growth scenario for Bitcoin miners.

September 25 bps Fed Rate Cut Fully Discounted

Markets

Fed Chair Powell in an interview at the Economic Club of Washington DC didn’t want to commit to any timing of a first Fed rate cut. By doing so, he effectively closed the door on the (tail) risk of a surprise move at the next, July 31, FOMC meeting. With inflation coming down and the labor market cooling off, it’s time look at both mandates (price stability & maximum employment), Powell said. “They’re in much better balance.” An unexpected weakening of the no longer overheated labour market could be a reason for the Fed to pull the trigger on interest rates. The Fed chair also referred to last week’s benign CPI print: “We didn’t gain additional confidence (that inflation is sustainably heading towards the 2% target) in Q1, but the three readings in Q2 do add somewhat to confidence.” This month’s eco release already triggered a significant repositioning on US (money) markets. A September 25 bps rate cut is fully discounted with some starting to contemplate the possibility of the Fed starting with a bigger 50 bps move. A cumulative 75 bps of rate cuts are nearly discounted by the end of the year, compared to June Fed guidance of just one 25 bps move. The combination of market positioning and Powell’s balanced comments left little room to push the front end of the US yield curve further down. US 2-yr and 3-yr yields closed almost unchanged. The long end of the US curve underperformed with 10-yr and 30-yr yields rising by 4.7 bps and 6.2 bps respectively. The US 2/30-yr yield spread is now flat after a period of almost two years being nearly constantly inverted. We believe US politics are responsible for this curve move. US president-candidate Trump got a boost in ratings after surviving an assassination attempt at a weekend rally. His decision to nominate JD Vance as vice-president running mate is an expression of Trump feeling bullish on the November outcome. He’s doubling down on his MAGA agenda, implying more protectionism (especially against China) and the promise of tax cuts. EUR/USD holds close to 1.0916 resistance, but avoids a break higher, at least for now. Today’s eco calendar contains German ZEW investor confidence (July), the ECB’s Bank Lending Survey and US retail sales (June). In the run-up to Thursday’s ECB meeting, the BLS could get some more attention. The central bank will hold rates steady, but could hint at a September policy rate cut which isn’t completely discounted yet. Headline June retail sales are forecast to fall by 0.3% M/M. This low threshold on the back of weak readings in April (-0.1%) and May (+0.1%) might limit downside risks. The market reaction could still be asymmetric though, ignoring better or in-line figures and moving on a miss.

News & Views

The Bank of Canada’s Q2 Business Outlook Survey showed firms’ sales outlooks being mostly unchanged from Q1 and remaining more pessimistic than average. Especially business tied to discretionary spending reported weak sales expectations. Investment spending plans are also below average and investment spending has become increasingly concentrated on upkeep and repair rather than expansion ore improvements in productivity. The share of firms reporting labour shortages is near survey lows, but for now few firms are planning to reduce headcounts. Businesses expect growth of their input prices and selling prices to slow, suggesting that inflation will continue to decline over the coming year. Most firms that made abnormally large price increases in the past 12 months do not plan to do so again in the coming year. The BoC concludes that firms’ expectations for inflation fell in June and are now in the Bank of Canada’s inflation-control range. That might support the case of another BoC policy rate cut next week. In a separate survey on consumer expectations, perceptions of inflation expectations were unchanged from Q1, but expectations for inflation over the next year declined significantly. June CPI data are out later today.

MNB vice-governor Virag kept a cautious approach on additional policy easing yesterday, but didn’t rule out further gradual steps. The MNB made a big step forward towards low inflation, but can’t declare victory yet. He expects inflation to stay within the MNB 3% +/- 1% tolerance band in coming months. Inflation and core inflation might rise later in the year, but he expects December inflation still to be closer to 4% than 5%. He indicated that the latest, better-than-expected, inflation data and improving global risk sentiment don’t change the monetary policy assessment but they do make it possible to deliver rate cuts earlier. In this respect, a 25 bps rate cut might be on the table at the July 23 meeting. He sees two to three 25 bps rate cuts as still possible by year-end even after the MNB at the June meeting indicated that it entered a new phase in monetary policy with less room for further rate cuts. The Hungarian 2-y swap rate fell by 6 bps. Still the forint closed with a marginal gain (EUR/HUF 391.4).

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on (at least) two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

EUR/USD

EUR/USD is testing the topside of the 1.06-1.09 range as the dollar loses interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. Risks of a topside break are high, bringing the psychologic 1.10 and the December 2023 top at 1.1139 on the radar.

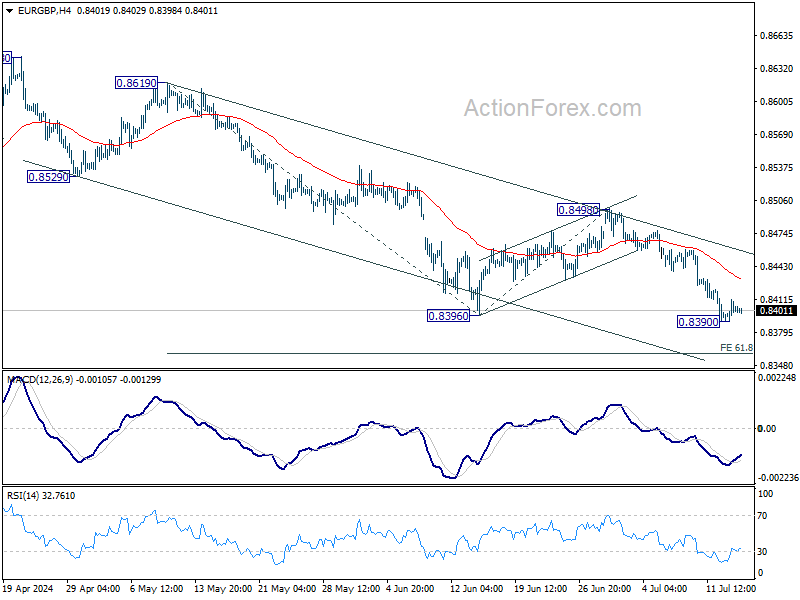

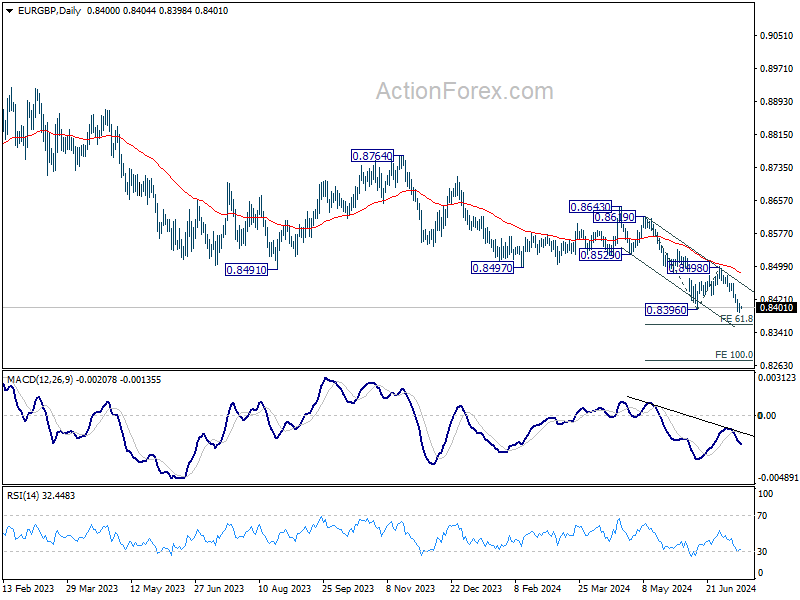

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 is support is being tested.

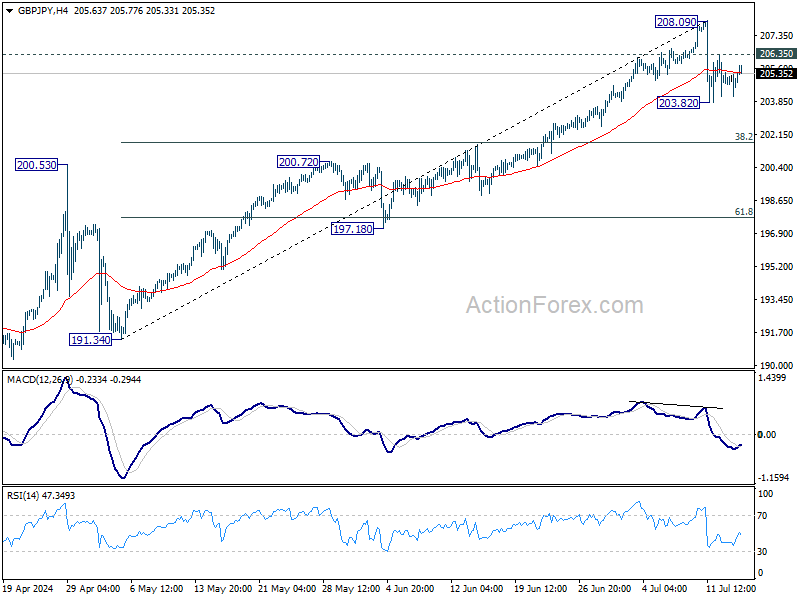

GBP/JPY Daily Outlook

Daily Pivots: (S1) 204.32; (P) 204.86; (R1) 205.57; More...

Intraday bias in GBP/JPY is turned neutral first. Corrective fall from 208.09 short term top could still extend lower. Break of 203.82 would target 38.2% retracement of 191.34 to 208.09 at 201.69. Strong support is expected there to bring rebound. On the upside, above 206.35 minor resistance will turn intraday bias will turn bias back to the upside for retesting 208.09. However, sustained break of 201.69 will argue that larger correction is already underway.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 200.72 resistance turned support holds, even in case of deep pullback.

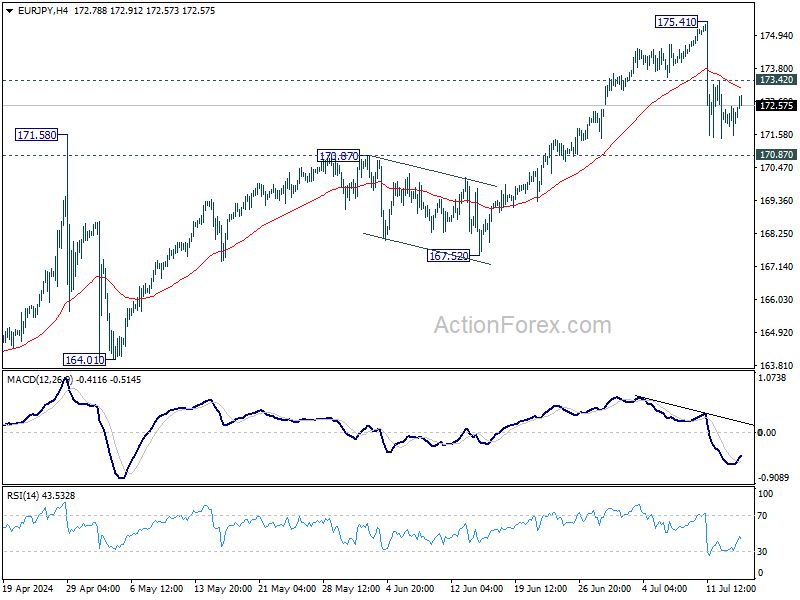

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.61; (P) 172.08; (R1) 172.61; More...

Intraday bias in EUR/JPY is turned neutral with current recovery. Corrective fall from 175.41 could still extend lower. But downside should be contained by 170.87 and bring rebound. On the upside, above 173.42 will turn bias back to the upside for retesting 175.41. However, firm break of 170.87 will argue that larger correction is already underway and target 167.52 and possibly below.

In the bigger picture, as long as 170.87 resistance turned support holds, the long term up trend is still expected to continue. Next target is 100% projection of 139.05 to 164.29 from 153.15 at 178.38. However, firm break of 170.87 will bring deeper fall to 167.52 support. Decisive break there will confirm that larger correction in in progress for 153.15/164.29 support zone.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8389; (P) 0.8401; (R1) 0.8412; More....

Intraday bias in EUR/GBP is turned neutral with current recovery. Some consolidations would be seen first but outlook will stay bearish as long as 0.8498 resistance holds. Break of 0.8390 will resume larger down trend to 61.8% projection of 0.8619 to 0.8396 from 0.8498 at 0.8360.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

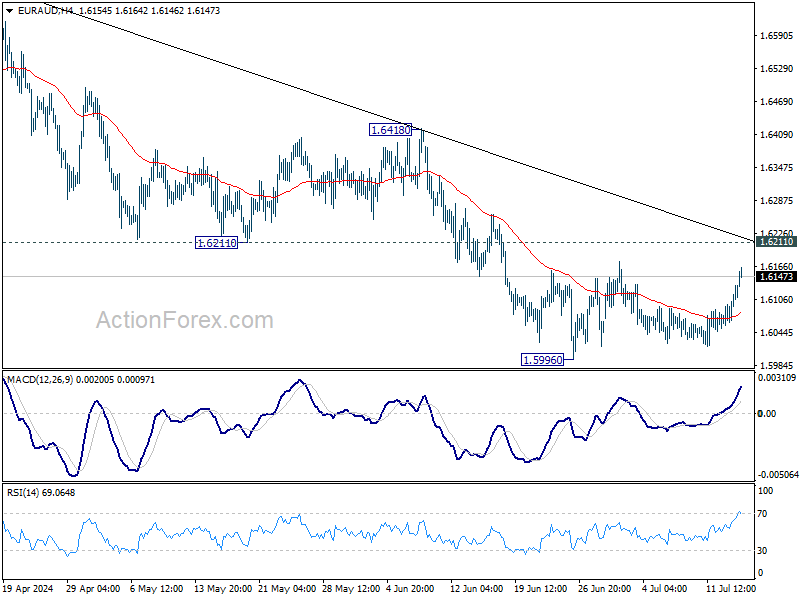

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6071; (P) 1.6102; (R1) 1.6148; More...

EUR/AUD rebounded strongly as consolidation from 1.5996 extends. But outlook is unchanged with 1.6211 support turned resistance intact. Intraday bias stays neutral and further decline is expected. On the downside, break of 1.5996 will resume larger fall to 1.5846 support next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6148 resistance will argue that the correction has completed.

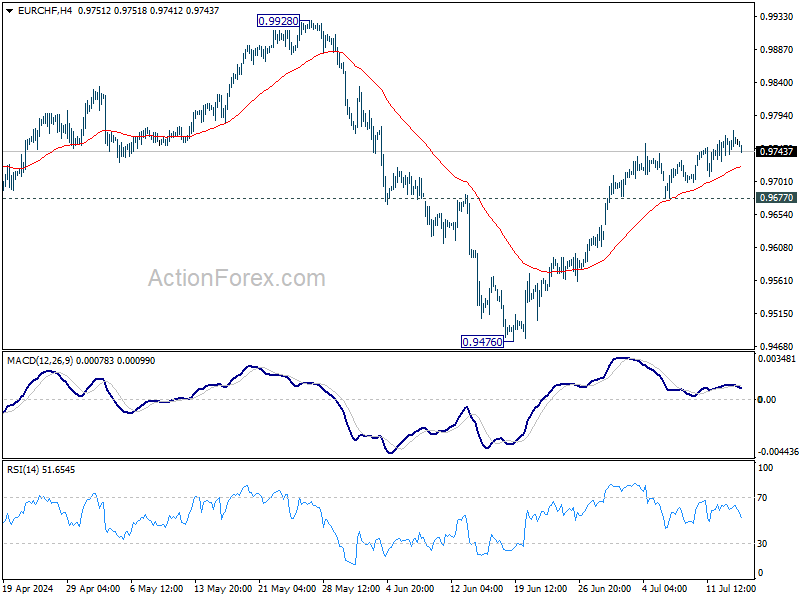

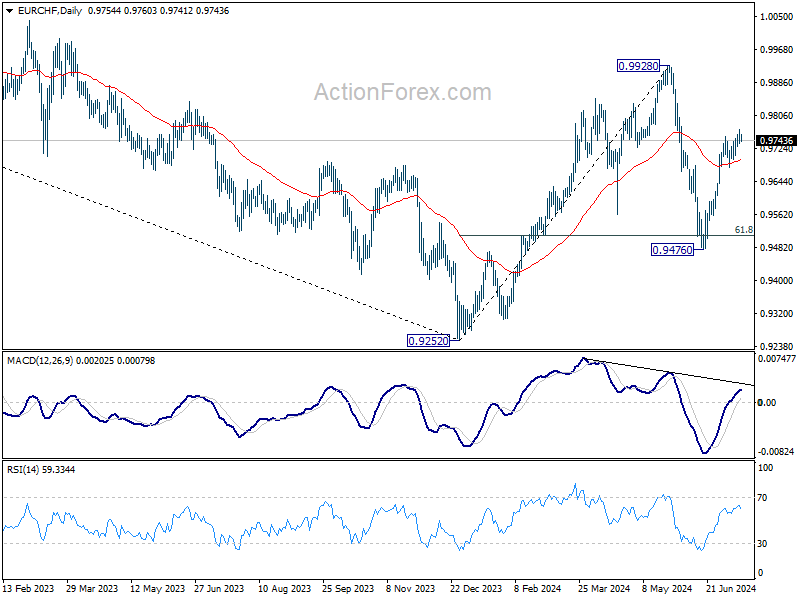

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9737; (P) 0.9756; (R1) 0.9777; More....

EUR/CHF's rise from 0.9476 is in progress and further rally is expected with 0.9677 support holds, to retest 0.9928 high. On the downside, however, break of 0.9677 will turn bias to the downside for deeper pullback.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.

Trump Trade, China Trade, Reflation Trade, AI Trade

There are a few stories developing at the same time:

The Trump trade consists of going long Bitcoin and equities (especially gunmakers, oil producers) and short the long term treasuries on expectation of exploding US debt with tax cuts, higher spending and growth supportive Trump policies. The yield on 30-year Treasuries yesterday surpassed the rate on two-year notes for the first time since January – the 30-year notes reflecting the exploding spending, while 2-year notes benefit from the rising Federal Reserve (Fed) rate cut bets as Powell reiterated on Monday that recent data boosted confidence that inflation is heading toward the Fed’s 2% goal. Other than that, Trump’s Media company jumped more than 30% yesterday following the murder attempt..

Nothing to do with Trump, but Apple’s 1.67% surge to a fresh high following news that its annual sales in India hit a record of $8bn – on path to potentially offsetting the Chinese weakness – and after being named a top pick at Morgan Stanley, also helped major US indices do well yesterday. While Goldman Sachs jumped more than 2.5% after announcing results. GS announced a much meagre investment banking revenue growth compared to JPM and Citi, but the trading unit and capital markets business did better than expected. And Trump trade is also positive for bank business. As a result, US kicked off the week on a positive note after the murder attempt on Trump, all major US indices – the S&P500, Nasdaq 100 and the Dow Jones eked out gains as the Russell 2000 jumped 1.80%.

Here in Europe, the Trump trade is not necessarily positive for the European stocks as who says Trump says higher tariffs and increased trade tensions. That’s one thing. Then there is the China trade where China’s inability to print sufficiently strong growth weighs on energy and commodities that are heavily represented in FTSE 100 and on the European luxury stocks. As such, Shell and Total Energies for example fell on the announcement of a weak growth number from China yesterday while their US peers gained on expectation that Trump will go slow on the climate-friendly policies and give support to the traditional energy businesses. In the luxury space, Burberry tanked 16% - yes 16% - yesterday after issuing a profit warnings and replacing its CEO. The Swiss Swatch Group lost almost 10% after slower spending in China in the first half led to a 70% decline in operating profit!

Happily for European stocks, the reflation trade is providing a boost, as rate cuts from major central banks are fostering better sentiment for European equities and supporting commodities weakened by China's economic slowdown. But alone, hope of lower rates may not suffice to keep the European Stoxx 600 near record, as Europe’s 12-month forward earnings revisions ratio, which is a gauge of analyst upgrades versus downgrades moved further into negative territory before companies started reporting their Q2 earnings. You could argue that softer earnings are easier to beat, of course, but do they really justify a rally to ATH levels, is another question.

Then there is the AI trade - which has been pushing the major US indices to record after record, but where, the high valuations start giving a foolish smell suggesting that a correction is certainly near. The expectations – here - are robust: the big tech earnings should slow but remain strong whereas the non-tech are expected to print positive earnings after quarters of struggle. That, combined with the rising odds of a September rate cut and heightened odds of a Trump victory keeps buyers in charge. But if the Big Tech starts falling, the other sectors will hardly make up for the drop because they have neither the potential nor a justification to do so.

All in all, uncertainties loom as equity markets on both sides of the Atlantic Ocean continue to flirt with record high levels. Due today, investors will focus on Canadian inflation print and the US retail sales. Retail sales in the US are expected to have fallen 0.2% in June. Such weakness would back the Fed’s easing inflation story and further reinforce the expectation of a September Fed cut. We could then see the US dollar index make a decisive move below a major Fibonacci support – the major 38.2% retracement that stands near 104.20 – and step into the medium-term bearish consolidation zone for the first time since the beginning of the year. If that happens, the price action would perfectly reflect the Fed rhetoric and give a further confidence regarding the weakening dollar outlook. The latter would inevitably boost the currency valuations elsewhere, and ease the dollar-led inflationary pressures elsewhere, as well. The EURUSD tested the 1.09 offers yesterday while Cable is flirting with the 1.30 psychological resistance amid a broad-based USD weakness, and ahead of the latest CPI update due tomorrow. UK’s headline inflation is expected to have eased below the 1.9% in some analyst surveys, but services inflation and jobs data will also play an important role in shaping the Bank of England (BoE) expectations for the August meeting. A sufficiently weak set of data will make the sterling bulls’ job harder near the 1.30 mark, while any strength in this week’s data could get the BoE doves to further scale back their rate cut expectations and pave the way for a further rally in Cable to above the 1.30 mark for the first time in a year.

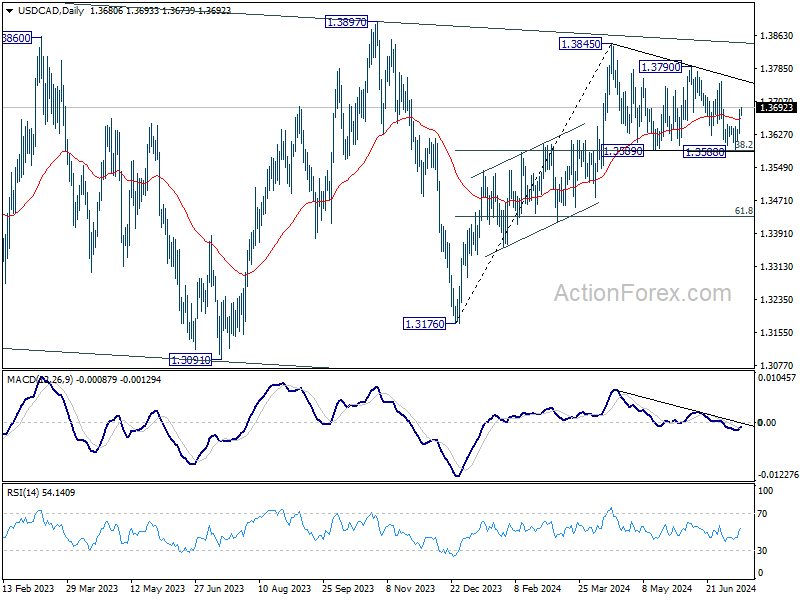

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3616; (P) 1.3630; (R1) 1.3649; More...

Intraday bias in USD/CAD remains on the upside for 1.3790 resistance. Corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589 twice. Break of 1.3790 will argue that larger rise from 1.3716 is ready to ready resume through 1.3845.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

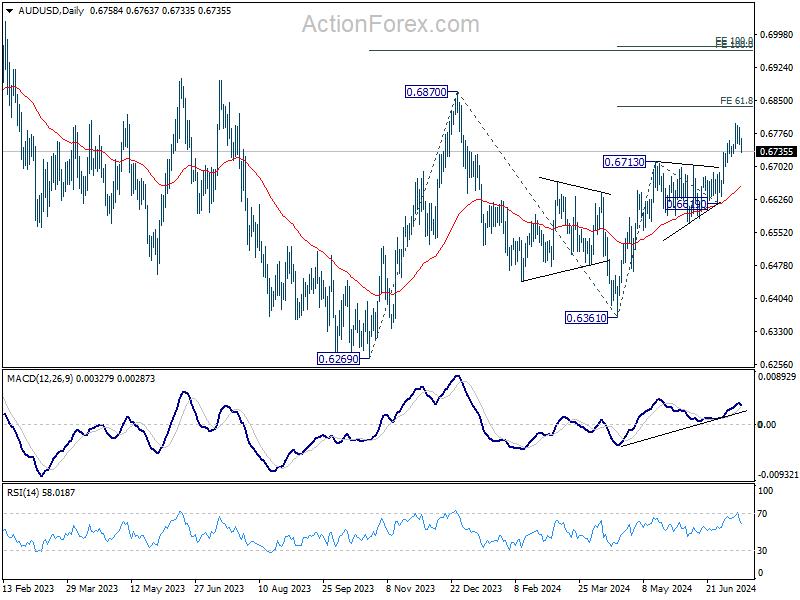

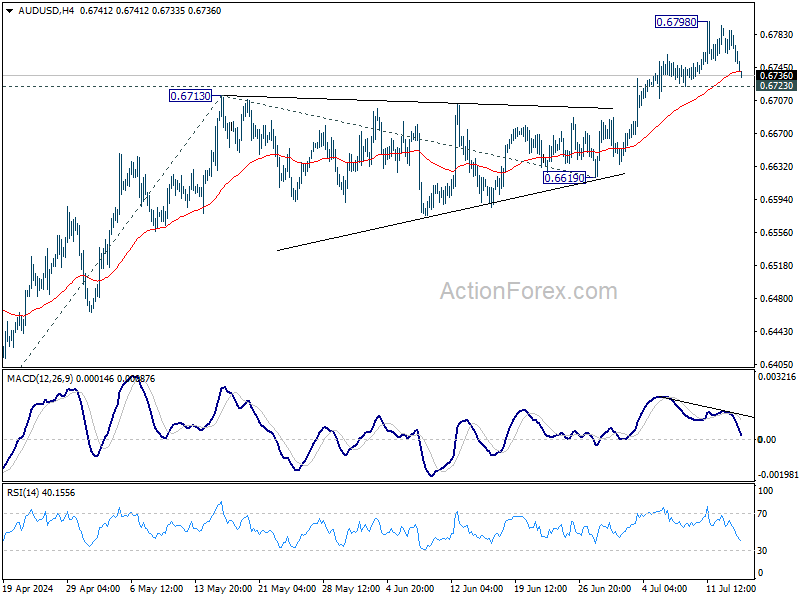

AUD/USD Daily Report

Daily Pivots: (S1) 0.6746; (P) 0.6767; (R1) 0.6782; More...

Intraday bias in AUD/USD remains neutral and more consolidations could be seen below 0.6798. Further rally is expected as long as 0.6723 minor support holds. On the upside, above 0.6798 will resume the rally from 0.6361 and target 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. On the downside, however, break of 0.6723 support will turn intraday bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.