Sample Category Title

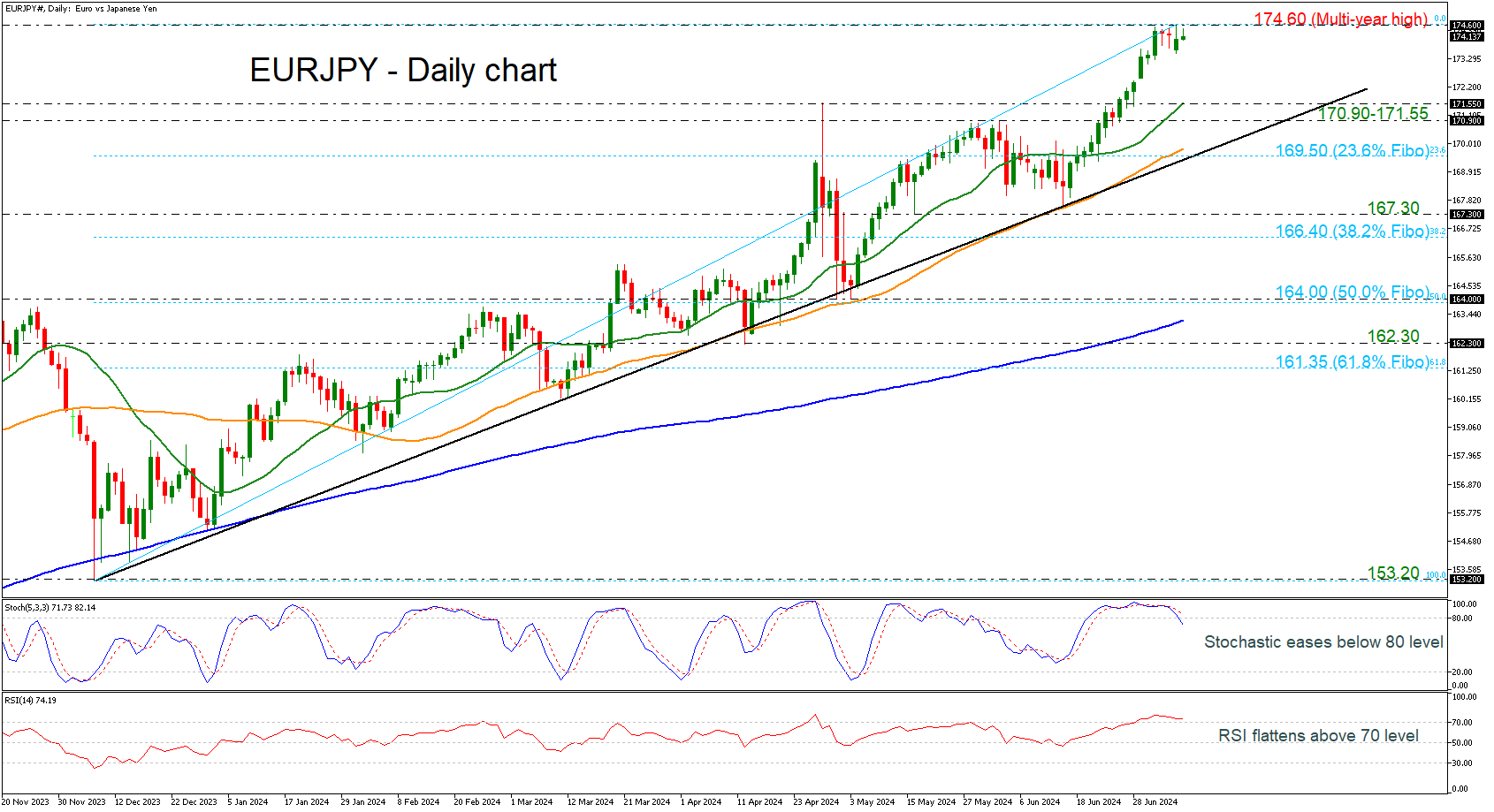

EURJPY Moves Beneath Its Lifetime High of 174.60

- EURJPY struggles to jump above its recent high

- Momentum oscillators look overstretched

EURJPY skyrocketed to a fresh multi-year high of 174.60 in the previous week but is currently hovering slightly below this level, with the technical oscillators suggesting an overstretched market. The RSI is trying to cross the 70 level to the downside, while the MACD is weakening its positive momentum above its trigger and zero lines.

Should the pair stretch south, the previous peak of 171.55 could provide immediate support near the 20-day simple moving average (SMA), as well as ahead of the 170.80 level. A significant step lower could bring bearish sentiment into play, sending the price probably towards the 50-day SMA at 169.70 and the 23.6% Fibonacci retracement level of the up leg from 153.20 to 174.60 at 169.50, which stands near the uptrend line.

On the flip side, another upturn may require the pair to retest the 174.60 barricade before opening the way to fresh uncharted levels such as 175.00 and 176.00.

To summarize, EURJPY has climbed to new levels since the euro’s inception, indicating a strongly positive outlook in the long term. A decline beneath the uptrend line and, more importantly, below the 200-day SMA at 163.23, could switch the outlook to bearish.

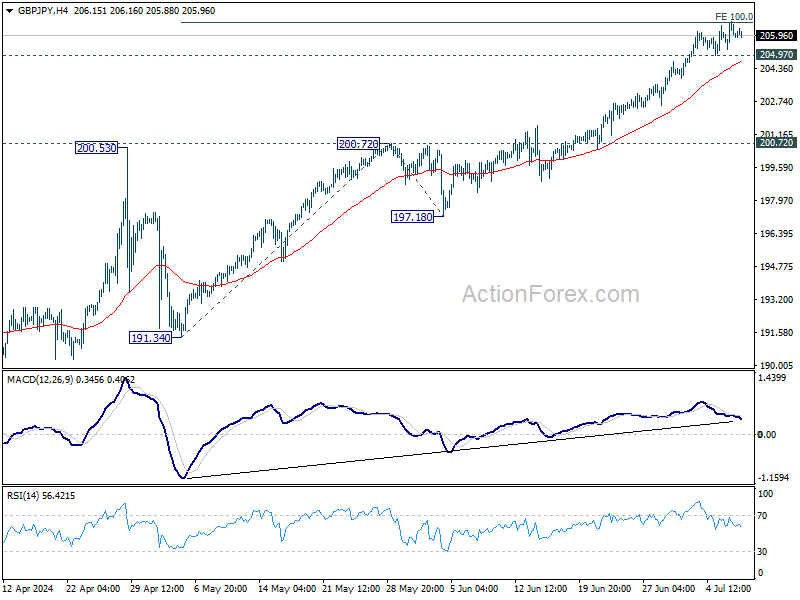

GBP/JPY Daily Outlook

Daily Pivots: (S1) 205.28; (P) 205.98; (R1) 206.66; More...

Intraday bias in GBP/JPY is turned neutral with loss of momentum as seen in 4H MACD. On the upside, sustained break of 100% projection of 191.34 to 200.72 from 197.18 at 206.56 will target 138.2% projection at 210.17. On the downside, below 204.97 minor support will turn bias to the downside for deeper pull back.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 197.18 support holds, even in case of deep pullback.

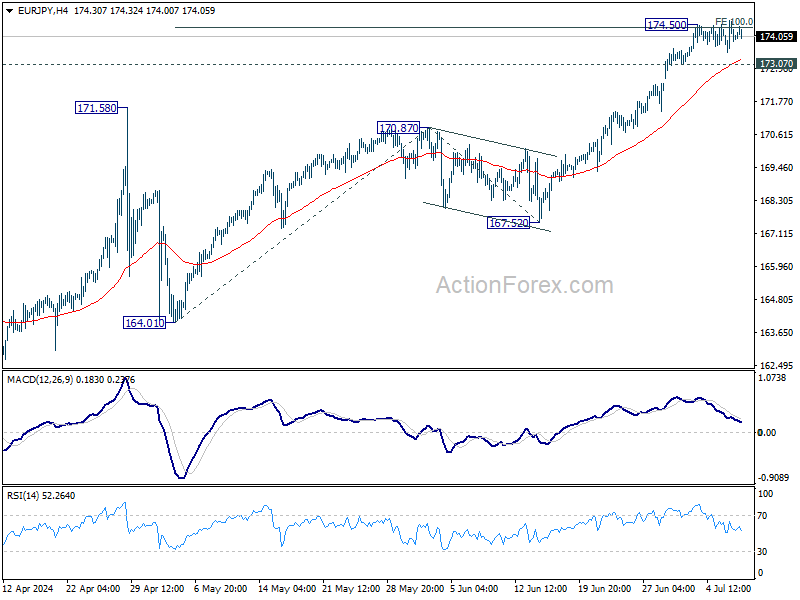

EUR/JPY Daily Outlook

Daily Pivots: (S1) 173.54; (P) 174.08; (R1) 174.65; More...

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, firm break of 174.50 will resume the larger up trend and target 138.2% projection of 164.01 to 170.87 from 167.52 at 177.00. On the downside, however, break of 173.07 will turn bias to the downside for deeper pullback.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 139.05 to 164.29 from 153.15 at 178.38. For now outlook will stay bullish as long as 170.7 resistance turned support holds, even in case of deep pullback.

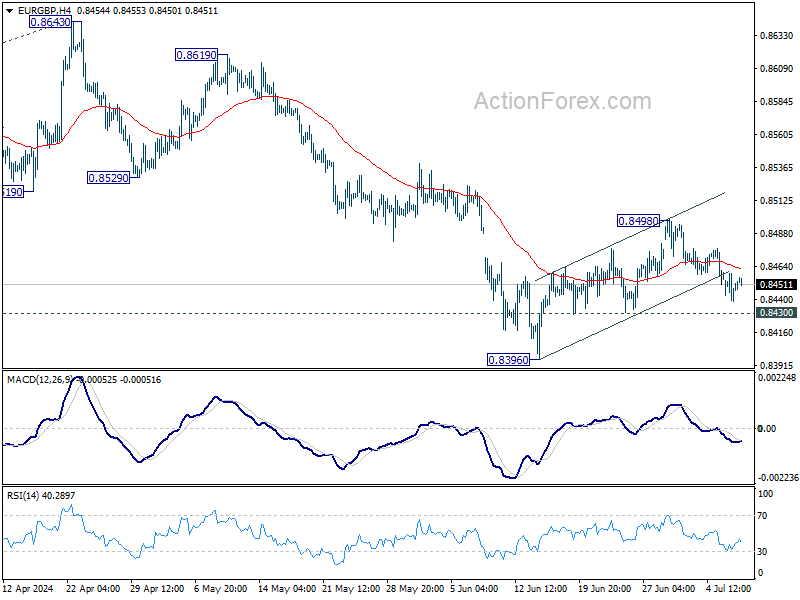

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8441; (P) 0.8450; (R1) 0.8462; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, sustained trading above 55 D EMA (now at 0.8501) will extend the rise from 0.8396 short term bottom to 0.8529 support turned resistance. Nevertheless, On the downside, break of 0.8493 support will suggest that the corrective recovery has completed. Intraday bias will be back on the downside for retesting of 0.8396 low. Firm break there will resume larger down trend.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

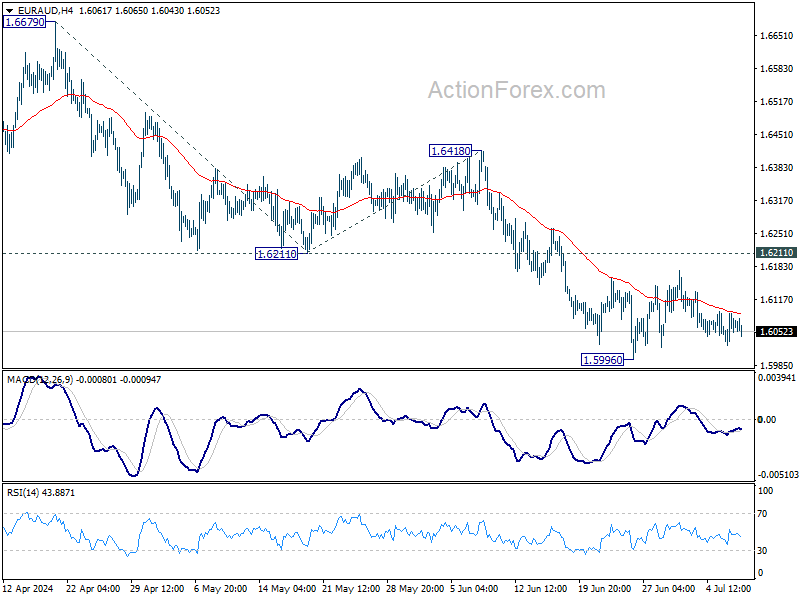

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6032; (P) 1.6061; (R1) 1.6096; More...

EUR/AUD is still bounded in consolidation from 1.5996 an intraday bias remains neutral. Outlook will remain bearish as long as 1.6211 support turned resistance holds. On the downside, break of 1.5996 will target 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. Firm break there will target 1.5846 key support next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6148 resistance will argue that the correction has completed.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9689; (P) 0.9705; (R1) 0.9732; More....

Intraday bias in EUR/CHF remains neutral for the moment, and some more consolidations could be seen below 0.9754 temporary top. Further rally is expected with 0.9639 support intact. On the upside, above 0.9754 will resume the rebound from 0.9476 to retest 0.9928 high. Nevertheless, break of 0.9639 will turn bias back to the downside for 0.9476 low instead.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.

We Expect Fed Chair to Hold a Mildly Dovish Tone

Markets

A surprise but inconclusive outcome of the French parliamentary election after some initial jitters also resulted in an inconclusive market (European) reaction yesterday. As the left group Nouveau Front Populair gained most seats in Parliament (180) they might try to take the initiative, but reaching the support of a 289-majority to execute their own (or a compromise) program with support of other center groups is far from evident. The French 10-y spread (vs Germany) yesterday eased 3 bps (66 bps), but stays well above the levels recorded before the European elections (< 50 bps). Even as an outright tax-and-spend scenario can be avoided due to the political stalemate, it is unlikely for the political risk premium of France (but also of other EMU countries) to again reverse anytime soon. The ‘relief’ after the outcome of the election early in the session triggered a limited underperformance of Bunds, but the rise in yields was undone later in US dealings as US yields maintained a tentative downward bias after Friday’s softer than expected payrolls. German yields in the end changed between +1.7 bps (2-y) and -2.0 bps (30-y). US yields showed a very similar picture (2-y +2.5 bps, 30-y minus 1.2 bps). EUR/USD whipsawed intraday. In the end the pair at 1.0824 still closed marginally lower compared to Friday’s close. The EuroStoxx50 ceded 0.2%. The S&P 500 (+0.1%) and the Nasdaq (+0.28%) still closed at record levels.

Asian equities mostly traded in positive territory with Japan outperforming (Nikkei 225 +2.35% at new record high). US Treasuries and the dollar trade little changed as investors are counting down to Fed Chair Powell’s testimony before the Senate Banking Committee. Aside from Powell’s testimony, the US NFIB small business confidence is the only data release worth mentioning. The Fed Chair probably will applaud the slowing in the monthly price rise in May. Friday’s (mildly) softer than expected payrolls (including unemployment uptick to 4.1%) also might cause the Fed Chair to reconfirm that its policy is guided by the double mandate of price stability and at same time maximal employment. We expect the Fed Chair to hold a mildly dovish tone, but still looking for further confirmation that inflation is cooling further with Thursday’s US June CPI the next high profile data reference. We expect US yields to maintain a cautious downside bias. Two Fed rate cuts by December are fully discounted. Some more anticipation on faster Fed easing has to become visible in the 2025 (+) sector of the curve. The US 2-y yield post payrolls dropped below the 4.70/65% support area, with 4.55% (end March low) next reference on the technical charts. In a steepening move, the US 10-y yield (currently 4.28%) still as some room ahead of the 4.19% mid-June correction low. The combination of a soft tone of Fed Chair Powell and European risk moving a bit to the background might help EUR/USD to move closer to the 1.0916 early June ST range top.

News & Views

The British Retail Consortium said that total sales in June fell by 0.2% y/y after the 0.7% uptick in May. It’s only the second negative reading in almost two years (the other one being a sharp –4% y/y in April). Surveying the same stores, showed retail sales dropping 0.5% y/y. The decline was concentrated in the non-food department, whose three-month moving average was negative (-2.9%) for 11 months straight now. Food still rose a 1.1%. BRC blamed the cold spell in June for the poor reading with consumers reining in spending on clothing particularly. An unusually wet month of April was also the culprit for the dire reading back then. BRC’s chief executive ended on a positive note though, saying that “Retailers remain hopeful that as the summer social season gets into full swing and the weather improves, sales will follow suit”.

The NY Fed June’s consumer inflation survey revealed their expectations declining at the short- and longer-term horizons while increasing slightly at the medium term. The one-year-ahead and five-year-ahead median gauges fell to 3.0% and 2.8% respectively. The three-year-ahead one increased to 2.9% (+0.1 ppt). Expectations about home price growth decreased to 3.0% from 3.3% and one-year-ahead expected earnings growth increased by 0.3 ppts point to a 3.0%. The latter is above than the 12-month moving average (2.8%) as well as the highest reading since September 2023. Expected growth in government debt one year from now remained unchanged at 9.3%.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed needs more evidence than just one slower-than-expected (May) CPI provided. June dots suggest one move in 2024 and four next year. The long end of the curve was also supported by increased odds of a Trump presidency after the debate with Biden. At the same time, softer US labour market data are fuelling the debate on the September Fed rate cut, steepening the curve.

EUR/USD

EUR/USD is stuck in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB taking the lead and a swing to the right in European elections pulled the pair to the 1.0665 area. However, the dollar also lost some momentum as the Fed is turning its focus to a potential softening of the labour market, potentially opening the way for policy easing in September.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. This might cap further sterling gains. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 is solid support.

S&P 500 (SPX) Bullish Elliott Wave Sequence Remains in Play

Short Term Elliott Wave View in S&P 500 (SPX) suggests that cycle from 4.20.2024 low is in progress as a 5 waves impulse. Up from 4.20.2024 low, wave 1 ended at 5325.49 and pullback in wave 2 ended in a zigzag structure. Down from wave 1, wave ((a)) ended at 5256.93 and wave ((b)) ended at 5311.65. Wave ((c)) lower ended at 5191.68 which completed wave 2 in higher degree. The Index has resumed higher in wave 3. Up from wave 2, wave (i) ended at 5292.25 and pullback in wave (ii) ended at 5234.32. The Index extends higher again from there with wave i ended at 5375.08 and wave ii ended at 5340.51. Wave iii higher ended at 5447.25 and wave iv ended at 5402.51. Final wave v ended at 5499.51 which completed wave (iii) in higher degree.

Down from there, wave a ended at 5446.56, and wave b ended at 5521.4. Wave c lower ended at 5447.47 which completed wave (iv) in higher degree. Index is now in the last wave (v) higher to complete wave ((i)) of 3. Up from wave (iv), expect wave i to complete soon. Then it should pullback in wave ii to correct cycle from 7.1.2024 low before it resumes higher again. Near term, as far as pullback stays above 5447.47 low, expect dips to find support in 3, 7, or 11 swing for further upside.

S&P 500 (SPX) 60 Minutes Elliott Wave Chart

SPX Elliott Wave Video

https://www.youtube.com/watch?v=RL1eOvUr5Tg

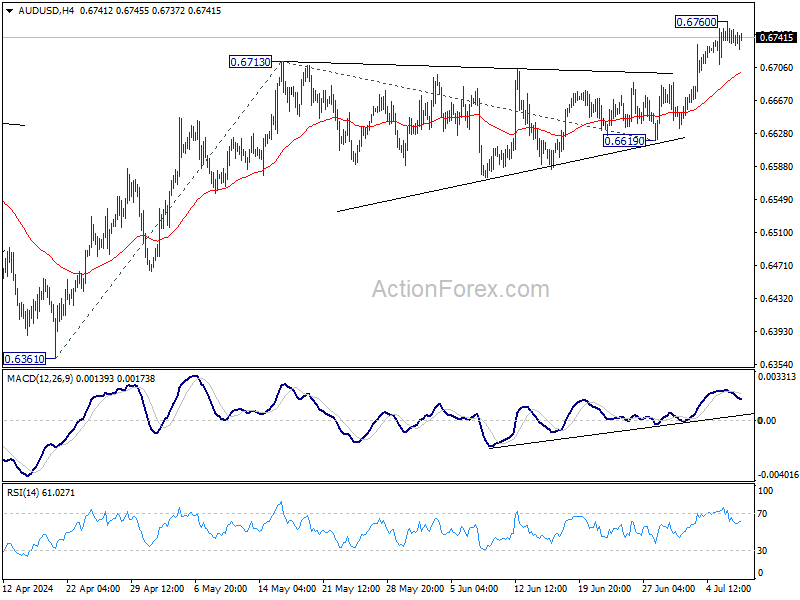

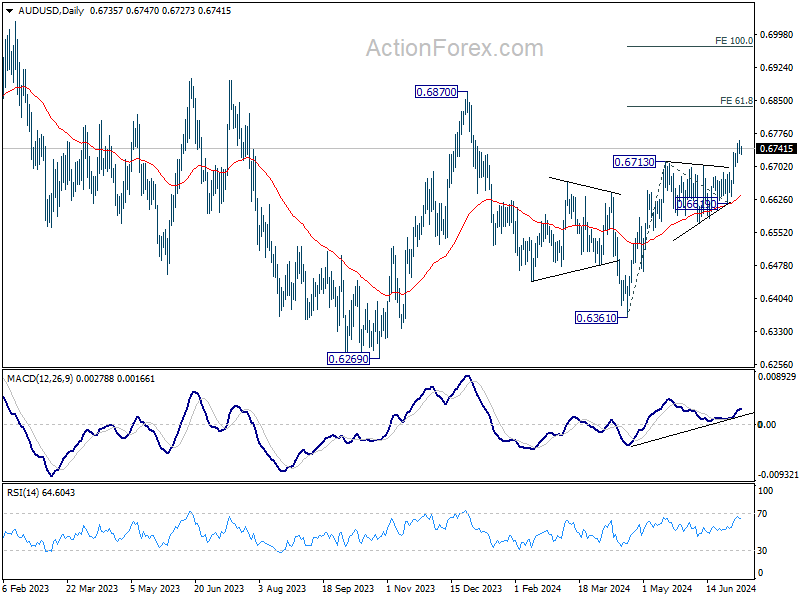

AUD/USD Daily Report

Daily Pivots: (S1) 0.6726; (P) 0.6744; (R1) 0.6755; More...

A temporary top is formed at 0.6760 in AUD/USD and intraday bias is turned neutral first. Outlook will stay bullish as long as 0.6619 support holds. On the upside, break of 0.6760 will resume the whole rally from 0.6361. Next target is 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3623; (P) 1.3635; (R1) 1.3647; More...

Intraday bias in USD/CAD stays neutral and outlook is unchanged. Corrective pattern from 1.3845 could still extend. Break of 1.3589 will target 100% projection of 1.3845 to 1.3589 from 1.3790 at 1.3534. Strong support would be seen there to bring rebound. On the upside, above 1.3686 minor resistance will turn bias back to the upside for 1.3790 resistance instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.