Sample Category Title

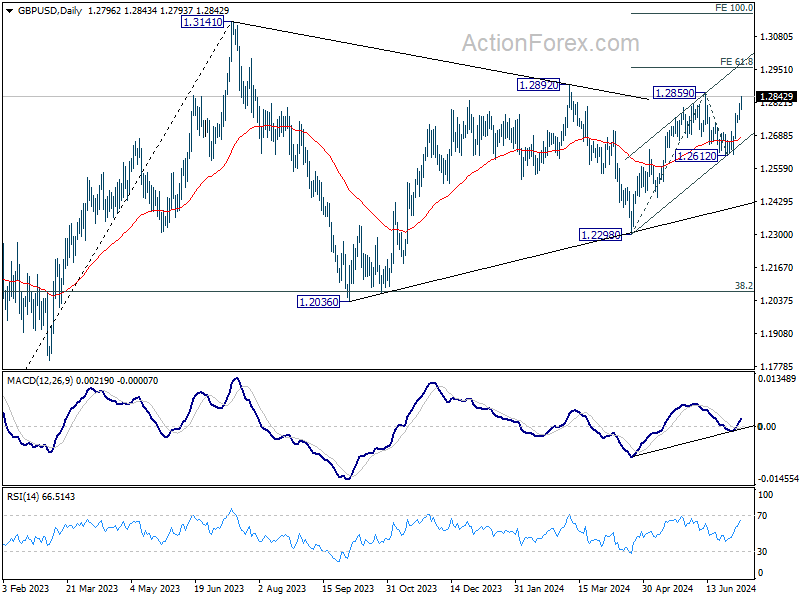

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2773; (P) 1.2796; (R1) 1.2837; More...

Intraday bias in GBP/USD remains on the upside as rally from 1.2612 is in progress for retesting 1.2859 resistance. Firm break there will resume the rally from 1.2298 and target 61.8% projection of 1.2298 to 1.2859 from 1.2612 at 1.2959. Decisive break there would prompt upside acceleration through 1.3141 to 100% projection at 1.3173. On the downside, below 1.2793 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern which might still extend. Break of 1.2612 support will bring another fall to 1.2298 support and possibly below. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351 might be ready to resume through 1.3141.

Pound Gains on Hawkish BoE Remarks; Euro Regains Lost Ground

Sterling strengthened broadly today, support by comments from Jonathan Haskel, a known hawk on BoE's MPC. Haskel indicated his preference to maintain interest rates until there is clear evidence that inflationary pressures have subsided sustainably. This stance has introduced some uncertainty regarding the widely anticipated BoE rate cut in August. While many economists still expect a rate reduction, upcoming economic data—such as this week's UK GDP report and next week's CPI figures—could still shift these expectations.

Meanwhile, Canadian dollar ranks as the second strongest currency, closely followed by Euro. The common currency has recovered from earlier losses caused by the French parliamentary elections, which resulted in a hung parliament. The left-wing coalition secured the most seats, while the far-right group garnered the least among major coalitions. In contrast, Kiwi is the weakest performer, followed by Swiss franc, which is feeling the pressure from Euro's rebound. Dollar, Aussie, and Yen are mixed, with markets keenly awaiting key events such as Fed Chair Jerome Powell's testimony and the release of US CPI data later this week.

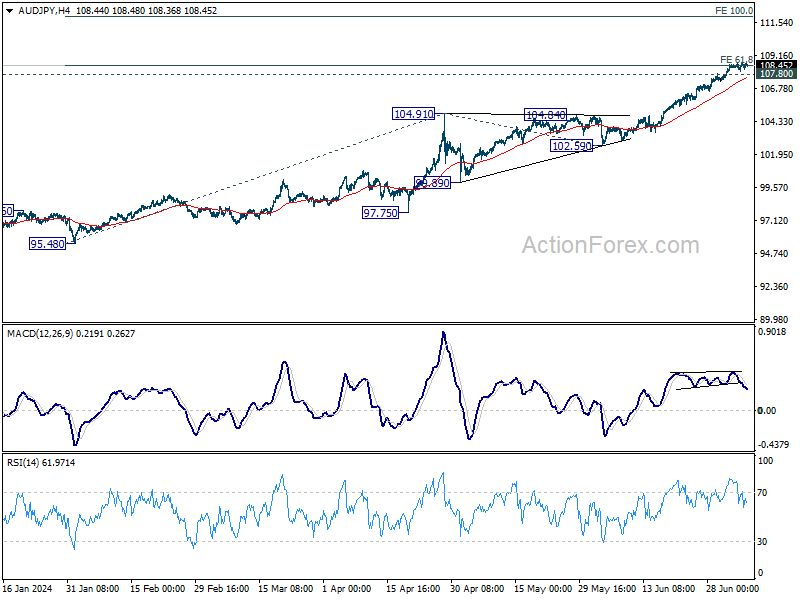

In the upcoming Asian session, AUD/JPY will be one to watch, with Australia's Westpac Consumer Sentiment and NAB Business Confidence reports due to be released. Technically, recent uptrend stalled after hitting 61.8% projection of 95.48 to 104.91 from 102.59 at 108.41. But there is no sign of a deep pullback yet. As long as 107.80 minor support holds. Further rally is in favor. Sustained break of 108.41 will pave the way to 100% projection at 112.02 next.

In Europe, at the time of writing, FTSE is up 0.28%. DAX is up 0.40%. CAC is up 0.10%. UK 10-year yield is down -0.013 at 4.115. Germany 10-year yield is up 0.009 at 2.545. Earlier in Asia, Nikkei fell -0.32%. Hong Kong HSI fell -1.55%. China Shanghai SSE fell -0.93%. Singapore Strait Times fell -0.19%. Japan 10-year JGB yield rose 0.0209 to 1.091.

BoE's Haskel advocates holding rates amid tight labor market

BoE MPC member Jonathan Haskel highlighted in a speech that assuming no further shocks, inflation will depend on the "interaction of a tight labour market and second-round effects as previous inflation works its way through the wage-price system."

Haskel emphasized that the MPC is closely monitoring labor market conditions and underlying inflationary indicators, particularly services inflation.

He expressed concerns about the current state of the labor market, stating, "The labour market continues to be tight, and I worry it is still impaired. I would rather hold rates until there is more certainty that underlying inflationary pressures have subsided sustainably."

ECB's Knot rules out July rate cut

ECB Governing Council member Klaas Knot has indicated there is no case for another rate cut in July. In an interview with Handelsblatt, Knot stated, "I don't see a case for another rate cut in July." He emphasized that the next ECB meeting that will consider rate adjustments will be in September.

Knot expressed satisfaction with ECB's progress in reducing inflation, projecting that 2% target will be achieved by late 2025. However, he warned against tolerating further delays, noting that inflation will have exceeded ECB's target for four and a half years by that time.

Market expectations suggest between one and two rate cuts this year and just over four cuts over the next 18 months. This implies that the deposit rate would remain above 3% into the second half of next year. K

not commented on this outlook, saying, "As long as we are above 3%, we are still restrictive. And that will be the case for the foreseeable future, beyond which I cannot make meaningful statements."

Eurozone Sentix drops sharply to -7.3 on rising political and economic uncertainties

Eurozone Sentix Investor Confidence dropped sharply in July, falling from 0.3 to -7.3, significantly worse than the expected 0.0. This decline ends a series of eight consecutive rises and marks a severe setback. Current Situation Index also declined from -9.0 to -15.8, while Expectations Index fell from 10.0 to 1.5.

Sentix highlighted that investors are increasingly concerned not just about the French elections but also about upcoming state elections in Germany. Moreover, growing worries about the health of the incumbent US president and the uncertainty surrounding who will run against Donald Trump in the next presidential election are adding to the overall anxiety. This uncertainty is creating a vacuum, compounded by the slowdown in the US economy, which is beginning to affect the rest of the world.

Given this "first mover" trend in the Eurozone, ECB is likely to consider further interest rate cuts. Investors anticipate that ECB will shift its focus more towards addressing economic weaknesses, particularly as the Sentix thematic barometer on "Inflation" signals an easing of inflationary pressures.

BoJ highlights spread of big firm wage hikes to smaller companies

In the Regional Economic Report, BoJ maintained its economic assessment for five out of Japan's nine regions, while upgrading two and downgrading two. Eight regions, with the exception of Hokuriku, indicated that their economies had been recovering moderately, picking up, or picking up moderately, although some weakness was noted in certain areas.

"Many regions reported that big firms' big pay hikes in this year's wage negotiations were spreading to small and medium-sized companies," BoJ noted. This suggests a positive spillover effect from large corporations to smaller businesses.

BOJ also noted that consumption was "firm as a whole," driven by robust spending from inbound tourists. This strong tourist spending is helping to offset softer consumption among households affected by rising living costs.

Japan's nominal wages rises 1.9% yoy, highest in 11months

Japan's nominal labor cash earnings increased by 1.9% yoy in May, up from April's 1.6% growth. Despite this being the 29th consecutive month of growth and the most substantial increase in 11 months, it fell short of the expected 2.1% yoy.

Regular pay saw a notable rise of 2.5% yoy, marking the best pace since January 1993, while overtime pay rebounded by 2.3% yoy, its first increase in six months.

However, these gains in nominal wages are overshadowed by the continued decline in real wages, which fell by -1.4% yoy, marking the 26th consecutive month of decline. This is also a deterioration from the -1.2% yoy drop recorded in April.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2773; (P) 1.2796; (R1) 1.2837; More...

Intraday bias in GBP/USD remains on the upside as rally from 1.2612 is in progress for retesting 1.2859 resistance. Firm break there will resume the rally from 1.2298 and target 61.8% projection of 1.2298 to 1.2859 from 1.2612 at 1.2959. Decisive break there would prompt upside acceleration through 1.3141 to 100% projection at 1.3173. On the downside, below 1.2793 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern which might still extend. Break of 1.2612 support will bring another fall to 1.2298 support and possibly below. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351 might be ready to resume through 1.3141.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y May | 1.90% | 2.10% | 1.60% | |

| 23:50 | JPY | Bank Lending Y/Y Jun | 3.20% | 3.10% | 3.00% | |

| 23:50 | JPY | Current Account (JPY) May | 2.41T | 2.13T | 2.52T | |

| 05:00 | JPY | Eco Watchers Survey: Current Jun | 47 | 46.3 | 45.7 | |

| 06:00 | EUR | Germany Trade Balance (EUR) May | 24.9B | 19.9B | 22.1B | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | -7.3 | 0 | 0.3 |

USD/JPY: Soft US Data Offers a Potential Relief Rally for JPY

- Lacklustre US non-farm payrolls & ISM Services PMI for June has led to a further drop in US Treasury yields.

- Both the 2-year and 10-year US Treasuries/JGBs yield premiums have shrunk to a 5-month low.

- A lower positive carry using JPY as a funded currency and elevated net short positioning in JPY futures may put a temporary halt to JPY’s persistent weakness.

- Watch the 162.40 intermediate resistance on the USD/JPY.

Weak ISM US Services PMI & a softer US jobs market have increased the odds of two Fed funds rate cuts before 2024 ends

Even though the latest US non-farm farm payrolls data for June released last Friday, 5 July has managed to beat expectations of +190K jobs as it came in at +206K, the prior two months of jobs data has been revised downwards to +218K in May from +272K and +108K in April from +165K.

The unemployment rate has also ticked slightly higher from 4% in May to 4.1% in June, the highest level since November 2021 coupled with a contractionary reading of 48.8 on the latest ISM Services PMI for June which indicates that the current high interest rate environment in the US has started to trickle down an adverse effect into the US jobs market, and services sector; a key economic growth contributor in the US.

Hence, the data-dependent US Federal Reserve now has more data points to support an imminent interest rate cut after seven consecutive monetary policy meetings that kept the Fed funds rate unchanged at 5.25% to 5.50%.

The latest data obtained from the CME FedWatch tool at this time of the writing based on the pricing of the Fed funds futures contracts has painted significantly high odds of two 25 basis points cut to the Fed funds rate before 2024 ends; a 78% chance of a cut in the September FOMC meeting, and 94% chance of another cut in December after the US Presidential Election in November.

Further narrowing of the yield spread between US Treasuries & JGBs

Fig 2: 2-YR & 10-YR US Treasuries/JGBs spreads as of 8 Jul 2024 (Source: TradingView, click to enlarge chart)

Given an increase in expectations of a more dovish Fed in the near -term, both the 2-year and 10-year US Treasury yields have headed south in the past week which in turn saw a reduction in their respective yield premiums against the Japanese Government Bonds (JGBs).

The 2-year and 10-year spread between the US Treasury note and JGB has narrowed to 4.28% and 3.23% respectively, their lowest levels since early February 2024 (see Fig 2).

Therefore, a further US Treasury yield premium shrinkage over JGB may reduce the positive carry of using the Japanese yen as a funded currency, in turn putting a temporary halt to the persistent bearish trend of the JPY that has slipped to a 38-year low against the US dollar last week.

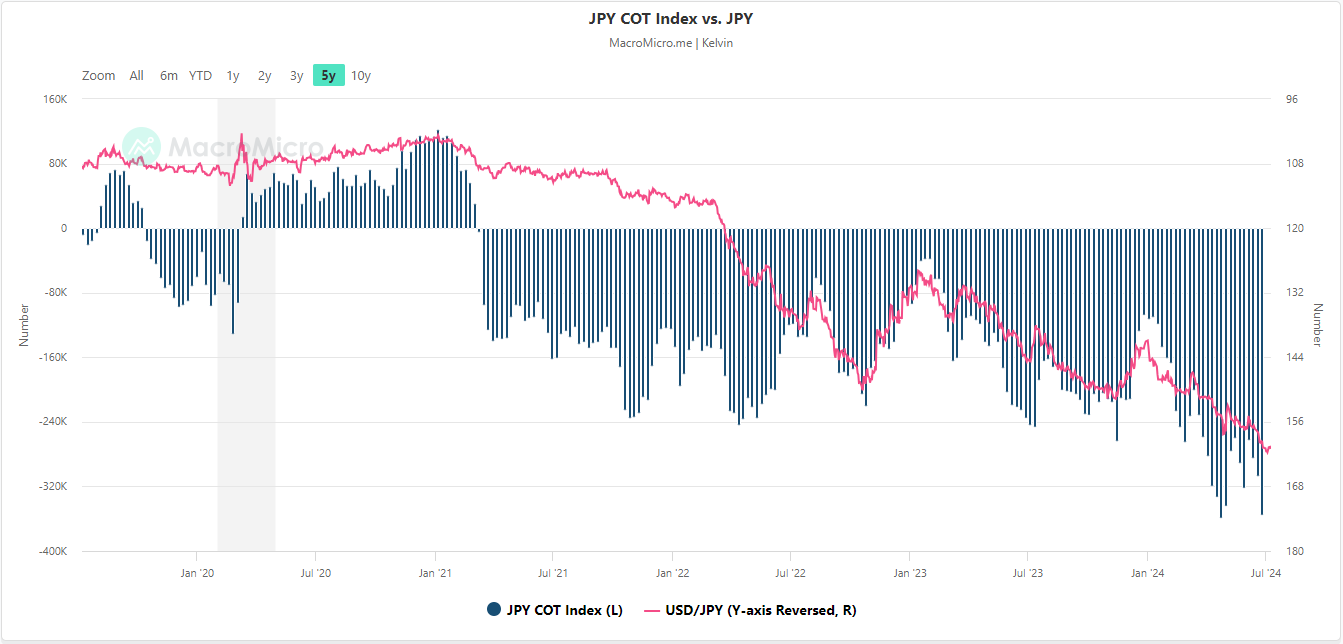

Large speculative players’ net bearish positioning on JPY remained at an elevated level

Fig 3: Commitments of Trader large speculators’ net positioning in JPY futures as of 24 Jun 2024 (Source: Macro Micro, click to enlarge chart)

Based on the latest data Commitments of Traders data as of 24 June 2024 (compiled by Macro Micro), the aggregate net bearish open positions of large speculators in the JPY futures market in the US (after offsetting the aggregate positions of large commercial hedgers) have inched lower since late May to-355,758 contracts, a revisit to its almost 17-year low of -359,063 contracts printed on 22 April.

Since large speculators have committed a relatively high amount of net bearish open positioning on JPY via the futures market, a further push down in the USD/JPY may trigger a spurt of short covering activities on such elevated leveraged short positions on the JPY which in turn might cascade into an abrupt liquidity squeeze and negative feedback loop movement into the USD/JPY at least in the short-term horizon.

USD/JPY at risk of a short-term corrective pull-back

Fig 4: USD/JPY medium-term & major trends as of 8 Jul 2024 (Source: TradingView, click to enlarge chart)

The daily RSI momentum indicator has just exited from its overbought region which suggested that the recent impulsive upmove sequence from the 4 June 2024 low of 154.55 has reached an overstretched condition that in turn increases the odds of a minor corrective pull-back scenario (see Fig 4).

If the intermediate resistance of 162.40 is not surpassed to the upside, the USD/JPY may stage a minor corrective pull-back within its medium-term and major uptrend phases to expose the 158.35/156.50 support zone (also confluences with the rising 50-day moving average).

On the flip side, a clearance above 162.40 sees the continuation of the impulsive upmove sequence for the next medium-term resistances to come in at 164.20/164.90 and 167.10 next.

Oil Price Update – Oil Prices Fall as Gaza Talks and Hurricane Beryl Take Center Stage

- Geopolitical events and weather disruptions are currently the main drivers of oil price fluctuations.

- OPEC+ production cuts have contributed to tighter oil markets, supporting prices. Can it continue?

- Technical analysis suggests key support and resistance levels to watch for future price movements.

Oil prices have retreated sharply since printing a fresh high on Friday. Gaza ceasefire talks and Hurricane Beryl touching down in Texas, are the major talking points at the start of the week.

Talks for a ceasefire in the Gaza strip have started up once more as a potential escalation in Northern Israel threatens to spillover. Any positive developments in talks will likely have an impact on the geopolitical premium currently priced into oil markets.

Hurricane Beryl has touched down in Texas with market participants concerned about the potential impact on US refineries just as summer demand reaches its peak. The drop off in crude inventories last week reinforced recent hopes that declining inventories could help keep oil prices supported over the medium term.

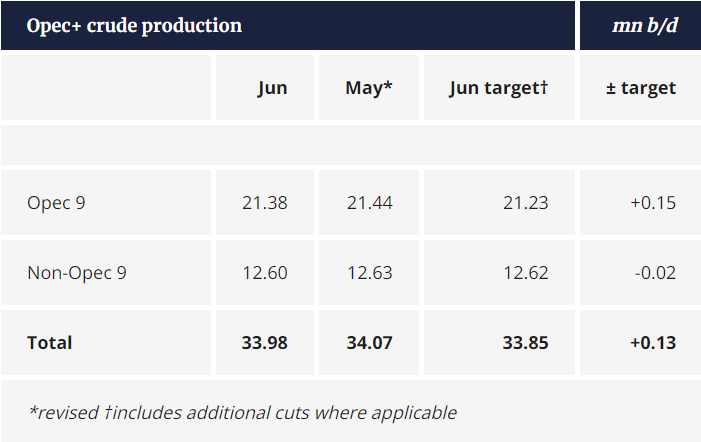

OPEC + Crude Production Falls in June

OPEC+ crude output from members under production cuts declined for the third consecutive month in June, as reduced Russian production offset increases from some consistent overproducers.

Output fell by 90,000 b/d to 33.98mn b/d in June, according to Argus estimates, the lowest in three years. But it could have been lower, with the alliance overshooting its target for the month by 130,000 b/d.

Reduced OPEC+ production has significantly contributed to tightening oil markets in recent weeks. The $7-8 per barrel increase in oil prices over the past month is likely a relief to OPEC+, which initially witnessed price declines after key members indicated plans to begin unwinding some of their production cuts starting in October.

OPEC + Crude Production

Source: Argus

Oil Inventories Remain Key

Oil inventory data is very important as the US and Europe are currently in the middle of summer. This period is typically the peak driving season in the US, leading to high demand for petroleum and other oil-related products.

Due to the busy summer season in the US, there is a good chance that weekly oil inventories will decrease more than expected. This could help keep oil prices strong and prevent any significant long-term price drops.

Technical Analysis

Oil prices have been on a terrific run of late, posting four consecutive weeks of gains. Brent reached a high around 88.55 on Friday before a pullback began. This has extended into the new week with oil prices retesting resistance turned support at the 86.21 handle.

This level could prove to be key for bullish momentum to continue. A bounce here could put oil back on course for the $90 a barrel mark.There is a possibility that price might dip below here and look to the 100 or 200-day MA as better areas of support. These two levels are currently resting at 85.13 and 83.60 respectively.

Support

- 86.21

- 85.00

- 83.60 (200-day MA)

Resistance

- 87.90

- 89.00

- 90.00

Brent Crude Oil Daily Chart, July 8, 2024

Source: TradingView.com (click to enlarge)

EUR/USD Gains Ground Despite French Election Shocker

The euro has started the week with gains and is trading at 1.0836 in the European session, up 0.33% on the day. EUR/USD is coming off its best week of the year, gaining 1.19%.

France veers to the left in Round 2

France has been on a political roller over the past two weeks and the wild ride isn’t over yet. President Macron called a snap election in June after European parliamentary elections saw the far-right make strong gains. Macron gambled that frightened French voters would support his centrist coalition, but things didn’t quite work out that way. France went to the polls twice in two weeks and each round of voting brought a stunning result.

In the first round, Mary Le Pen’s far-right National Rally party won the most votes and seemed well on its way to becoming the largest party in parliament and perhaps even winning a majority. The second round brought its own surprise, as the left-wing alliance won the most seats, followed by Macron’s centrist alliance, with National Rally placing third.

As the dust settles from Sunday’s vote, the political system is in gridlock, with no clear winner. The left-wing alliance fell short of a majority and Macron must now pick a prime minister who will be tasked with forming a government. This could mean a minority government or an unwieldy coalition, either which could usher in a period of instability.

Despite the political uncertainty, the financial markets are steady, likely in a sign of relief that fears of a Le Pen majority did not materialize. The French stock market is steady on Monday and the euro has posted gains. It has been a good start to the week, but investors will be keeping close tabs on the fallout from France’s remarkable election.

.

EUR/USD Technical

- There is support at 1.0797 and 1.0752

- 1.0884 and 1.0929 are the next resistance lines

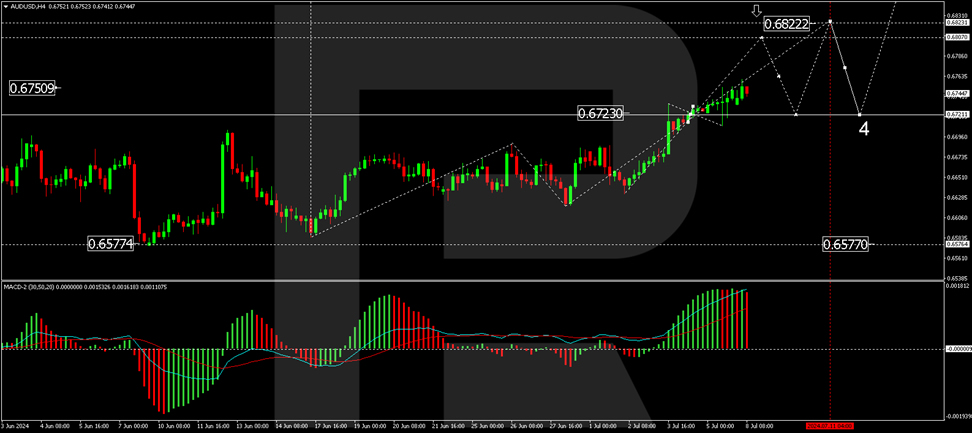

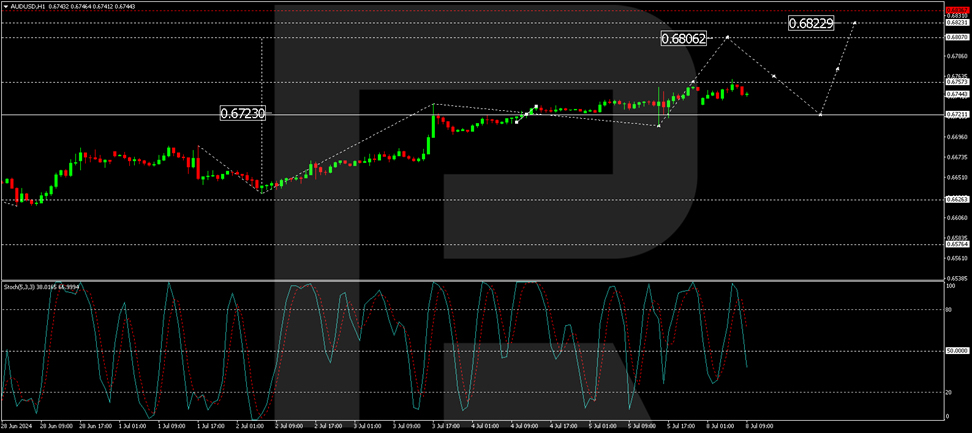

AUD/USD Hits Six-Month High Amid RBA Rate Hike Speculations

The AUD/USD pair reached a six-month high of 0.6752, marking its fifth consecutive day of gains. The currency's strength is largely driven by market expectations that the Reserve Bank of Australia (RBA) might diverge from the global trend of lowering interest rates, raising them in response to escalating inflation pressures. May's CPI figures have intensified discussions around monetary tightening.

Market sentiment is split between expectations for a rate hike and maintaining the current rates at the RBA's next meeting in August. High domestic yields draw international capital, boost the Australian dollar, and provide a haven from the political uncertainties in the US and Europe.

Moreover, a weaker US dollar, underscored by unimpressive economic data released on Friday, has also bolstered the AUD. This data reinforced the Federal Reserve's dovish stance on monetary policy.

Technical analysis of AUD/USD

The market has established a broad consolidation pattern centred around 0.6723. Moving forward, there is a potential for an upward movement to 0.6822. Once this level is reached, a retraction to 0.6750 for a retest might occur, followed by a continuation of the upward trajectory towards 0.6858. This bullish outlook is supported by the MACD indicator, with its signal line positioned above zero and trending upwards.

The AUD/USD pair is currently challenging the 0.6757 level, with the potential to extend the rally towards 0.6806. Following this target, a pullback to 0.6757 could occur, setting the stage for another rise to 0.6822. The stochastic oscillator, situated above the 50 mark, suggests an imminent climb to 80, reinforcing the bullish momentum forecasted.

Traders and investors are closely monitoring developments, especially the upcoming RBA meeting, which could significantly influence the direction of the AUD/USD pair.

BoE’s Haskel advocates holding rates amid tight labor market

BoE MPC member Jonathan Haskel highlighted in a speech that assuming no further shocks, inflation will depend on the "interaction of a tight labour market and second-round effects as previous inflation works its way through the wage-price system."

Haskel emphasized that the MPC is closely monitoring labor market conditions and underlying inflationary indicators, particularly services inflation.

He expressed concerns about the current state of the labor market, stating, "The labour market continues to be tight, and I worry it is still impaired. I would rather hold rates until there is more certainty that underlying inflationary pressures have subsided sustainably."

ECB’s Knot rules out July rate cut

ECB Governing Council member Klaas Knot has indicated there is no case for another rate cut in July. In an interview with Handelsblatt, Knot stated, "I don't see a case for another rate cut in July." He emphasized that the next ECB meeting that will consider rate adjustments will be in September.

Knot expressed satisfaction with ECB's progress in reducing inflation, projecting that 2% target will be achieved by late 2025. However, he warned against tolerating further delays, noting that inflation will have exceeded ECB's target for four and a half years by that time.

Market expectations suggest between one and two rate cuts this year and just over four cuts over the next 18 months. This implies that the deposit rate would remain above 3% into the second half of next year. K

not commented on this outlook, saying, "As long as we are above 3%, we are still restrictive. And that will be the case for the foreseeable future, beyond which I cannot make meaningful statements."

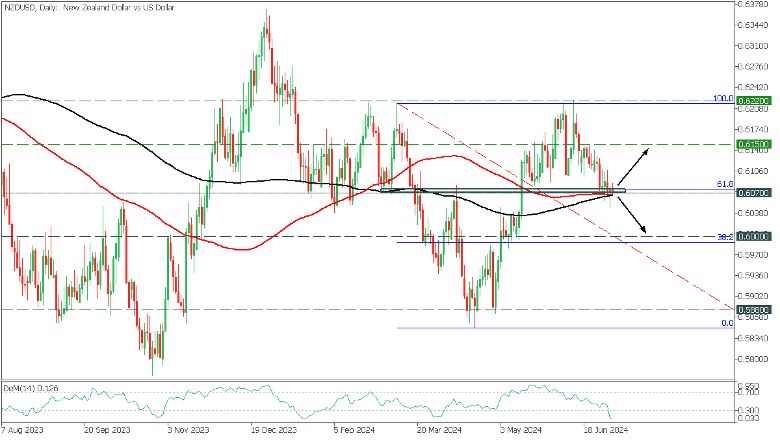

News of the Week (July 8—12): NZDUSD Detailed Analysis!

The NZDUSD pair, often called the "Kiwi," refers to the exchange rate between the New Zealand dollar and the US dollar and is an important indicator for understanding the economic relationship between New Zealand and the United States. The New Zealand dollar is strongly influenced by fluctuations in commodity exports, especially dairy products, which are sensitive to world market demand and price changes. Other local factors, such as tourism and export volumes, also play a significant role. At the same time, the US dollar reacts to a wide range of domestic economic indicators, including inflation rates, employment reports and GDP growth, Federal Reserve decisions, and international trade policy.

US Fed Chair Powell Testifies, July 9, 16:00 (GMT+2)

The testimony of US Federal Reserve Chair Jerome Powell is highly anticipated as an indication of future US monetary policy. Should Powell present an optimistic view of the US economy, suggesting robust growth or a hawkish stance towards interest rate hikes, the US Dollar would likely strengthen against the New Zealand Dollar, causing a downward movement in the NZDUSD pair. Conversely, if Powell expresses concerns about the US economy or signals a more dovish stance on interest rate adjustments, indicating potential delays or reductions in rate hikes, the US Dollar could weaken, potentially elevating the NZDUSD rate. It's also worth remembering that the US CPI comes out on July 12, which will also be very important for this pair!

During Fed Chair Powell's testimony on March 7, 2024, he emphasized a cautious approach to the US economic outlook, which weakened the US Dollar. As a result, the NZDUSD pair experienced an uptick, benefiting from the decreased strength of the USD as investors adjusted their expectations for US interest rate hikes.

New Zealand Interest Rate Decision, July 10, 4:30 (GMT+2)

The decision on interest rates by the Reserve Bank of New Zealand is crucial for the NZDUSD pair. If the RBNZ unexpectedly raises the interest rate above the forecasted 5.50%, it would signal a proactive stance against inflation or an unexpectedly strong economic outlook, likely boosting the NZD and causing the NZDUSD rate to rise. Alternatively, if the RBNZ decides to maintain the rate at 5.50% or cuts it, it could indicate satisfaction with the current economic path or a defensive response to perceived external or internal economic risks, respectively. Holding the rate steady might stabilize the NZD, while a rate cut would likely weaken it, resulting in a decline in the NZDUSD rate. However, given the current level of inflation in New Zealand, it is very likely that the rate will be kept at the current level.

In the Daily timeframe, NZDUSD corrected to the 61.8 support area after a short-term rise. The price tests the critical levels of MA100 and MA200, while DeMarker indicates exceptionally oversold.

- If the price overcomes the support at 0.6070, falling below the moving averages, we can expect a decline to 0.6000;

- However, if the price bounces off the support, NZDUSD will recover to 0.6150;

Ethereum (ETHUSD) Incomplete Sequences Calling the Decline

Hello fellow traders. In this technical blog we’re going to take a quick look at the Elliott Wave charts of Ethereum (ETHUSD). As our members know, ETHUSD is showing incomplete sequences in the cycle from the 3977 peak. We have been predicting a price decline. Recently, we got a bounce against the 3650 peak , after which the price dropped toward new lows as we expected. In the following text, we will explain the Elliott Wave Pattern and the forecast.

ETHUSD H1 Elliott Wave Analysis 07.01.2024

ETHUSD current view suggests cycle from the 3650 is still in progress as 5 waves structure. We believe wave (iv) blue ended at 3515 high, as labeled on the chart. As far as the price stays below that peak and more importantly below 3650 peak, we expect further weakness in the cryptocurrency to occur. Although overall view is bullish, we don’t recommend buying the cryptocurrency at this stage and expect to see a decline toward new lows ideally.

ETHUSD H1 Elliott Wave Analysis 07.01.2024

The cryptocurrency hold previous peak at 3515 and found sellers as expected. As a result we got a decline toward new lows. Current view suggests cycle from the 3622.7 peak is still in progress as impulsive structure. ETHUSD is now doing (iv) blue recovery. Once wave (iv) blue recovery completes, we should ideally get another low to complete the structure.