Sample Category Title

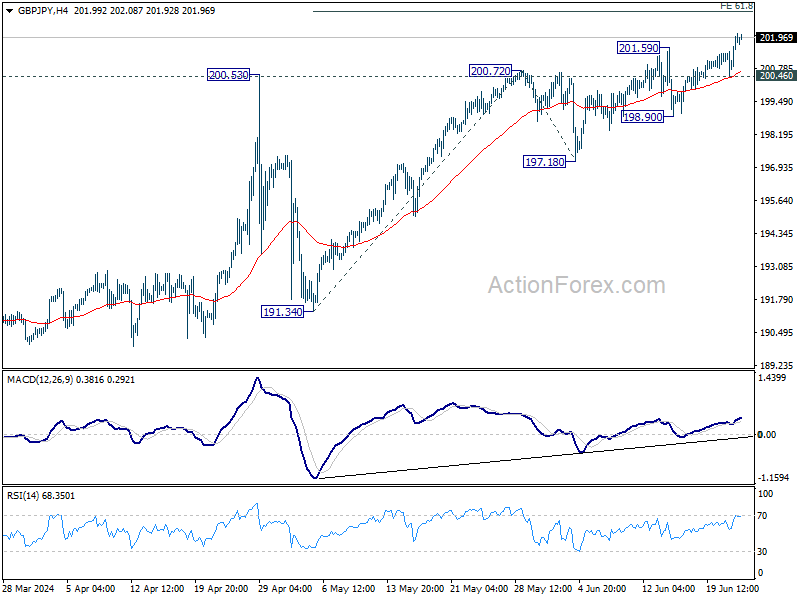

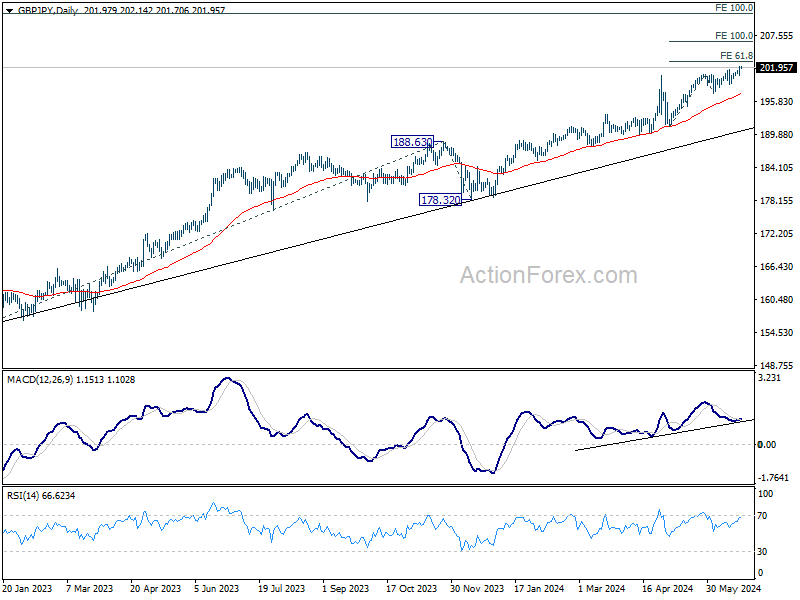

GBP/JPY Daily Outlook

Daily Pivots: (S1) 200.96; (P) 201.56; (R1) 202.63; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current up trend should target 61.8% projection of 191.34 to 200.72 from 197.18 at 202.97. Firm break there will pave the way to 100% projection at 206.56 next. on the downside, below 200.46 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 198.90 support holds, in case of retreat.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 191.34 support holds, even in case of deep pullback.

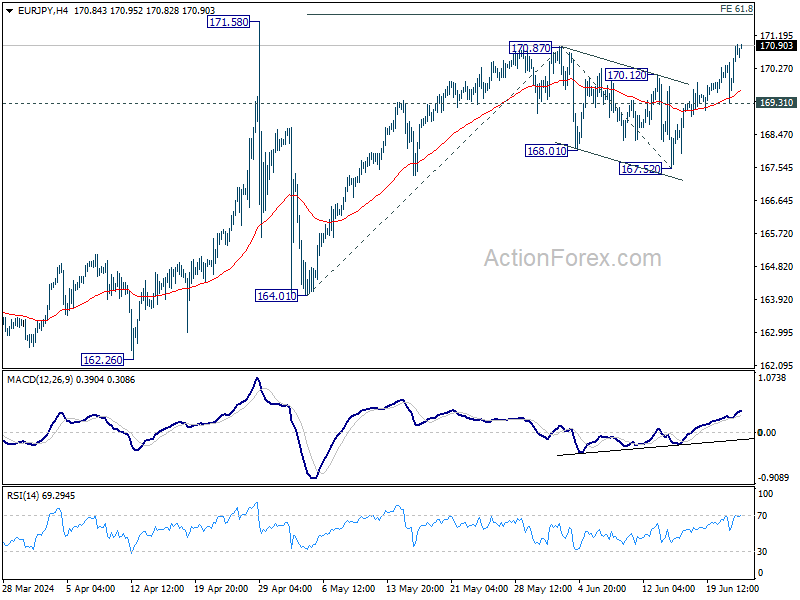

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.79; (P) 170.36; (R1) 171.38; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Rise from 164.01 is resuming and should target 61.8% projection of 164.01 to 170.87 from 167.52 at 171.75. On the downside, below 169.31 minor support will dampen this bullish case and turn intraday bias neutral gain first.

In the bigger picture, strong support from 55 D EMA indicates that the long term up trend is still in progress. Decisive break of 171.58 will confirm resumption and target 100% projection of 139.05 to 164.29 from 153.15 at 178.38. For now outlook will stay bullish as long as 164.01 support holds, even in case of deep pullback.

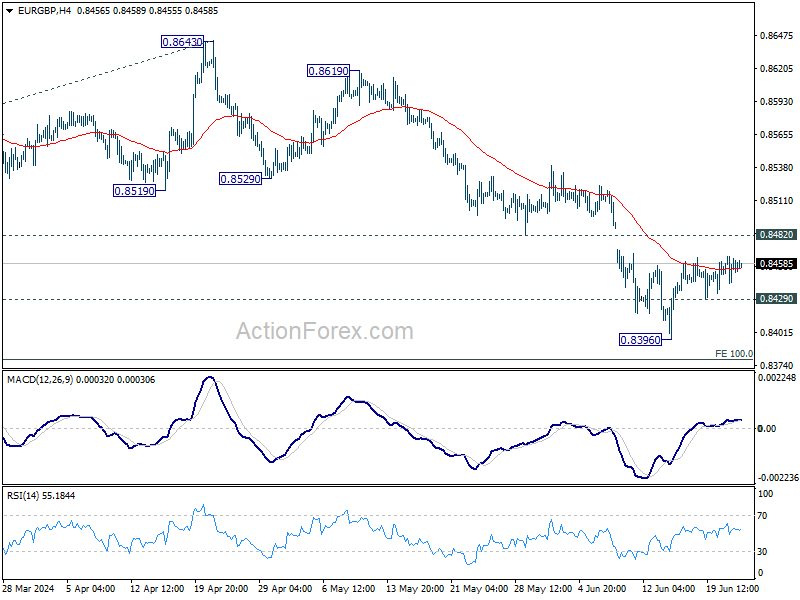

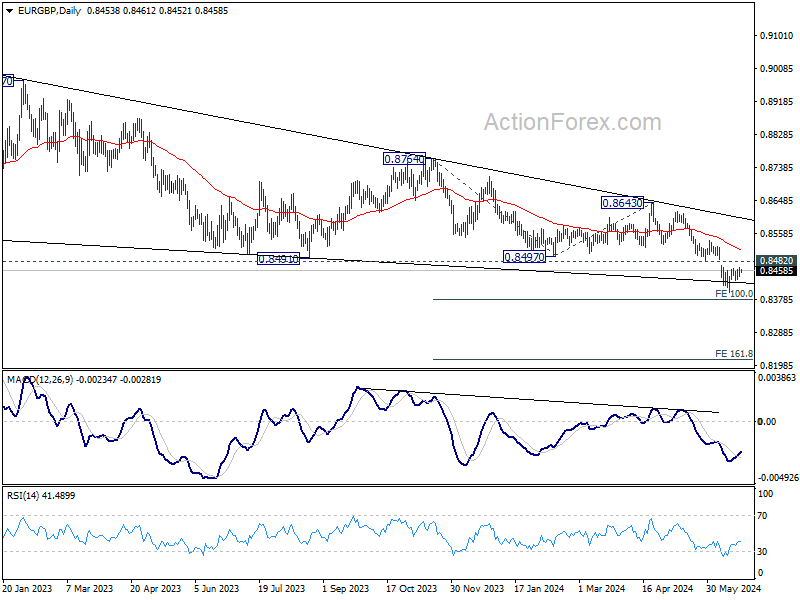

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8444; (P) 0.8455; (R1) 0.8467; More...

Intraday bias in EUR/GBP remains neutral and consolidation from 0.8396 could extend further. But outlook will stay bearish as long as 0.8482 support turned resistance holds. On the downside, below 0.8429 minor support will bring retest of 0.8396 low first. Further break there will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

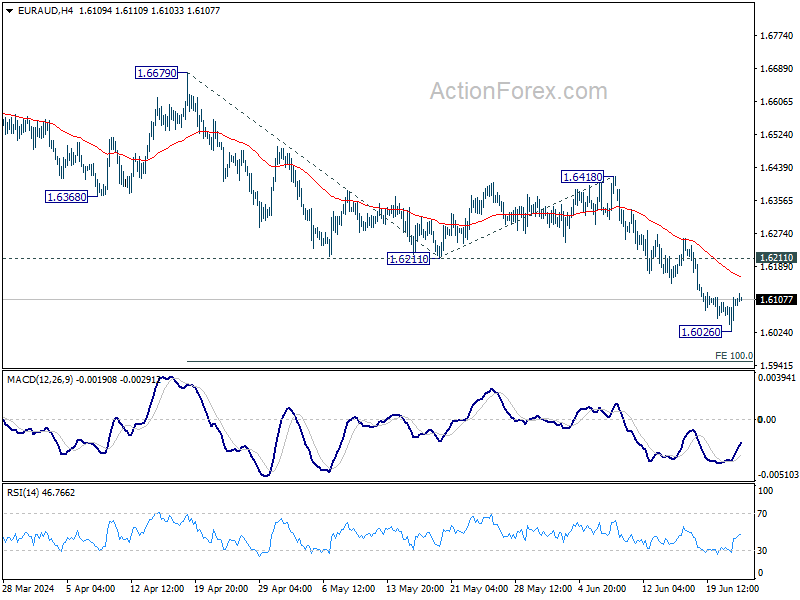

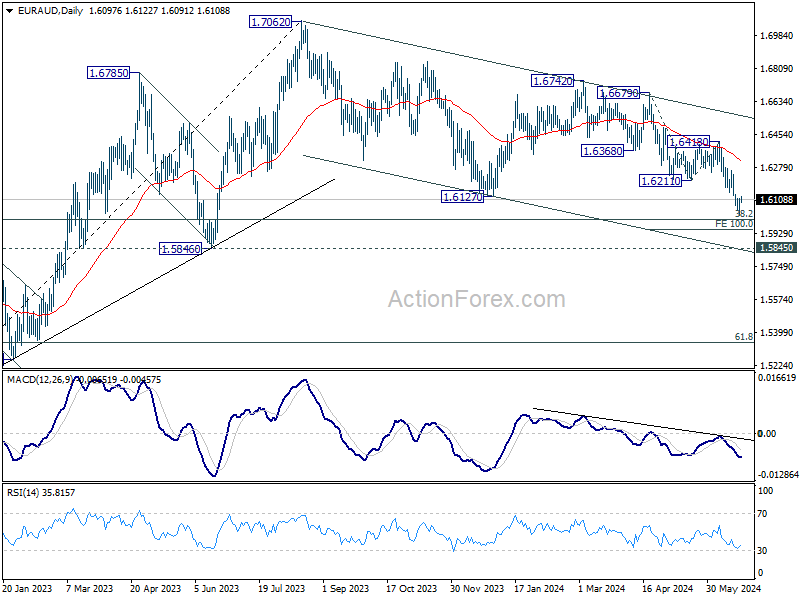

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6048; (P) 1.6081; (R1) 1.6134; More...

Intraday bias in EUR/AUD stays neutral and consolidation from 1.6026 could extend. But upside should be limited by

EUR/AUD's down trend continued last week but it recovered after hitting 1.6026. Initial bias is neutral this week for some consolidations first. Upside should be limited by 1.6211 support turned resistance to bring another fall. Below 1.6026 will turn bias back to the downside for 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

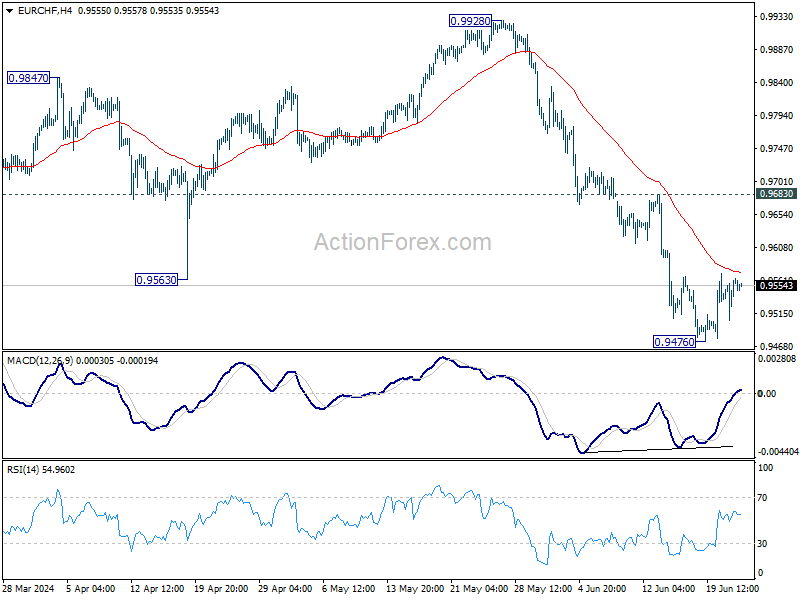

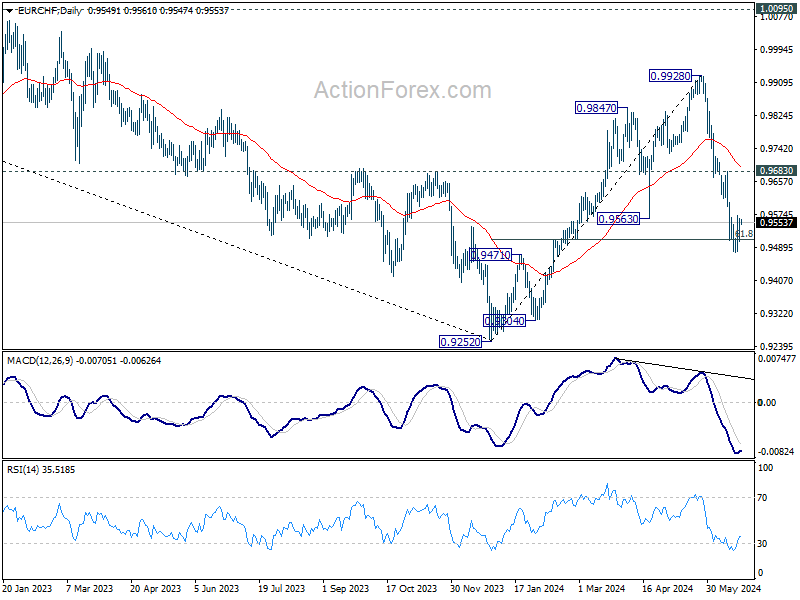

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9524; (P) 0.9545; (R1) 0.9583; More....

EUR/CHF is staying inc consolidation above 0.9476 and intraday bias remains neutral. While stronger recovery cannot be ruled out, outlook will remain bearish as long as 0.9683 resistance holds. On the downside, break of 0.9476, and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will bring retest of 0.9252 low next.

In the bigger picture, rebound from 0.9252 should have completed at 0.9228. Medium term outlook remains bearish with 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

Nvidia Selloff Raises Worries

The week kicks off on a weak note following a moody trading session across Europe and the US on Friday. One of the most significant moves of last two trading days of the US was a 10% selloff in Nvidia sales for … no reason other than the fact that it was the end of the month, the end of the quarter and the end of H1, and investors preferred taking profits while they repositioned for the new half than buying more Nvidia shares at peak levels, and at a very high valuation with little certainty regarding how to value a stock that’s price-to-projected sales hit the highest of the S&P500. But still, Nvidia is expected to deliver around $28bn in the Q2, more than double the same time last year, while Microsoft is expected to announce 15% sales and Apple just 3%. It’s just that, no one really knows at this point, if Nvidia deserves a higher price tag.

And the problem with that is, because the US Big Tech stocks led by Nvidia were responsible for most of this year’s rally in major US indices – because the S&P500’s equal weight index remained far behind the normal weighted index since at least a month, any weakness in the US tech rally could mean the end of the party for the major US indices.

This week, the US will reveal its latest GDP update on Thursday. US growth is expected to be revised slightly higher from 1.3% to 1.4% down, but that’s down from 3.4% printed a quarter earlier. And on Friday, investors will focus on core PCE data – the Federal Reserve’s (Fed) favourite gauge of inflation. The latter better be soft enough to prevent a broader selloff in US indices. On the individual front, FedEx and Micron Technology are due to release earnings.

Elsewhere, appetite is limited. The Stoxx 600 in Europe was toppish last week as the French political uncertainties occupied the headlines. The EURUSD sold off to 1.0670 on Friday and is trading a touch below 1.07 at the start of the week. Le Pen’s National Rally increased its lead in the polls for the upcoming legislative elections to 36%, while Emmanuel Macron’s centrists stand near 20% support. French risks will likely remain a shadow over the single currency at least until the election.

In Japan, the USDJPY is dangerously flirting with the 160 level – a level which had brought the Japanese policymakers to intervene to stop the bleeding back in April. The Japanese Vice Finance Minister Kanda told reporters that they are ready to intervene 24 hours a day if necessary. The net speculative short positions against the yen remain relatively high despite the rising risk of a currency intervention. The latter means that the USDJPY could post a rapid fall in case a BoJ-triggered price action clears a part of these short positions, but currency intervention alone will hardly send the USDJPY into a sustainable bearish trend; the Bank of Japan (BoJ) must change its rate policy that leads to such a strong yen selloff in the first place.

In energy, US crude is lower this Monday morning after having tested and failed to clear the $82pb resistance last Friday. Trend and momentum indicators remain in favour of a further rise while the RSI index is not yet pointing at extensively bought market conditions. Clearing the $82pb level, the major 61.8% Fibonacci retracement on April to May selloff, should act as a strong signal about the viability of the latest rebound and could throw the foundation of a further rise toward $85pb. But clearing the $82pb could be difficult with sputtering China.

Chinese equities begin the week on continued downside pressure. The CSI 300 fell to an almost 4-month low on the back of insufficient rebound in economic activity, copper futures remain also under the pressure of a slow Chinese rebound.

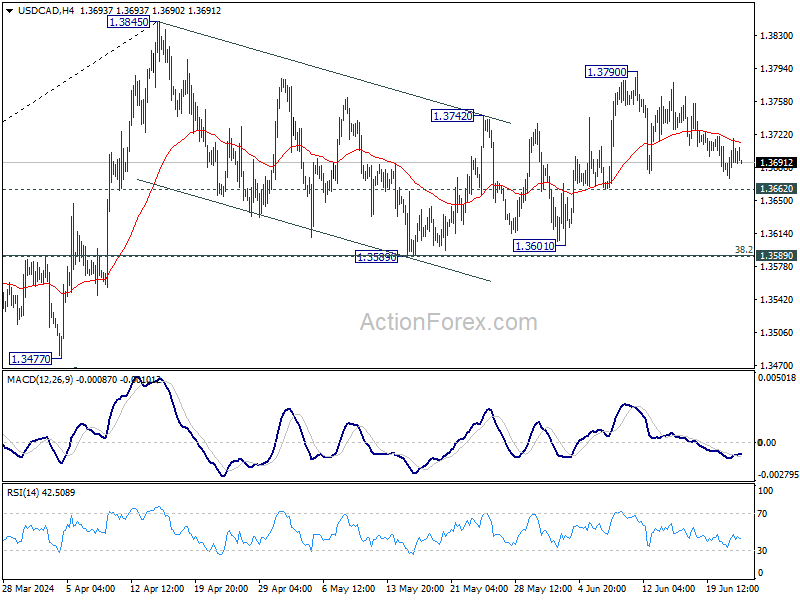

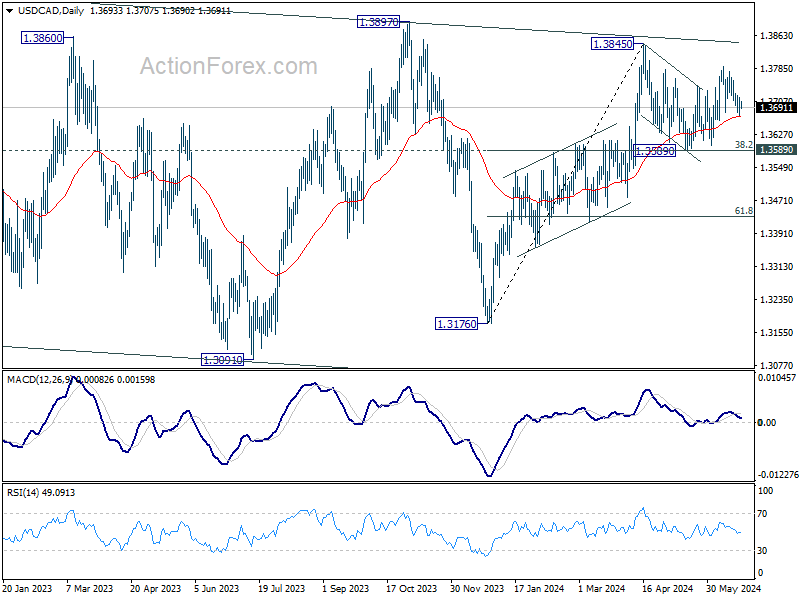

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3671; (P) 1.3698; (R1) 1.3721; More...

Intraday bias in USD/CAD remains neutral and outlook is unchanged. Further rally is expected as long as 1.3662 support holds. Above 1.3790 will bring retest of 1.3845 high first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

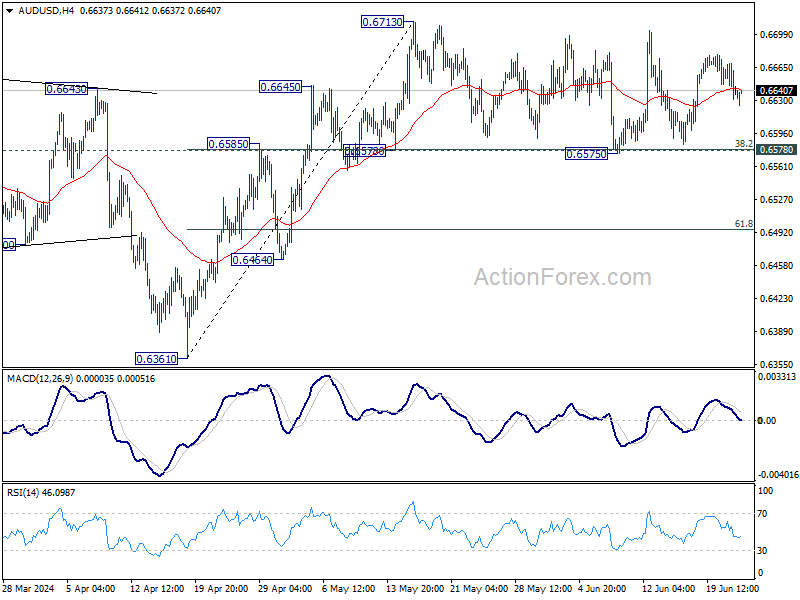

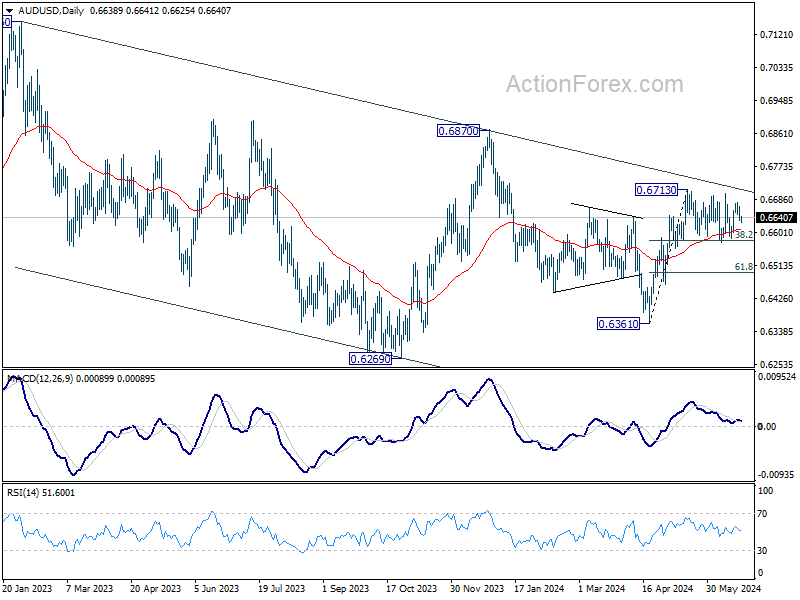

AUD/USD Daily Report

Daily Pivots: (S1) 0.6625; (P) 0.6648; (R1) 0.6663; More...

No change in AUD/USD's outlook as consolidation from 0.6713 is still extending. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

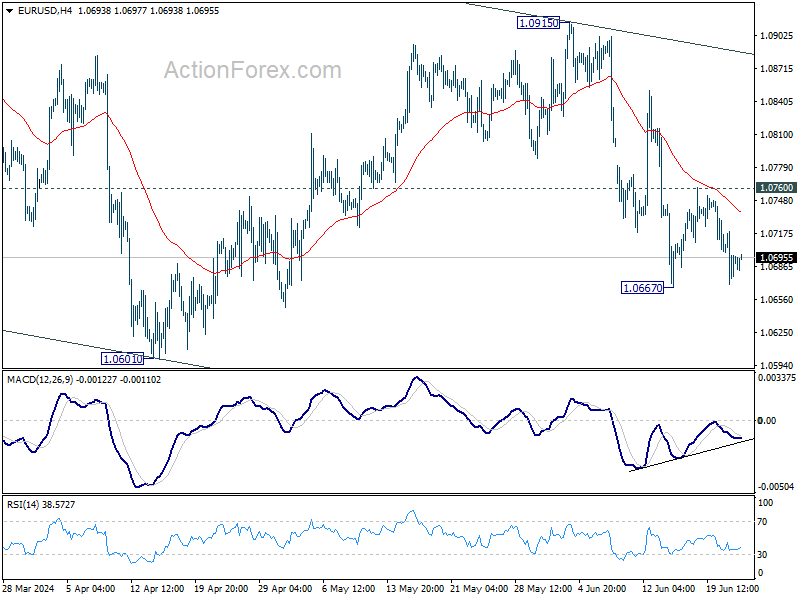

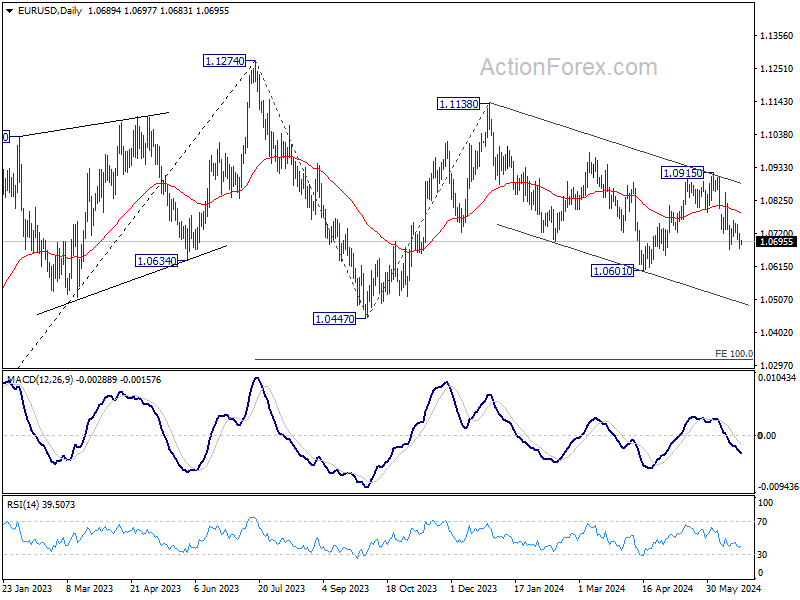

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0669; (P) 1.0695; (R1) 1.0719; More....

Intraday bias in EUR/USD remains neutral first and consolidation from 1.0667 could extend. But further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

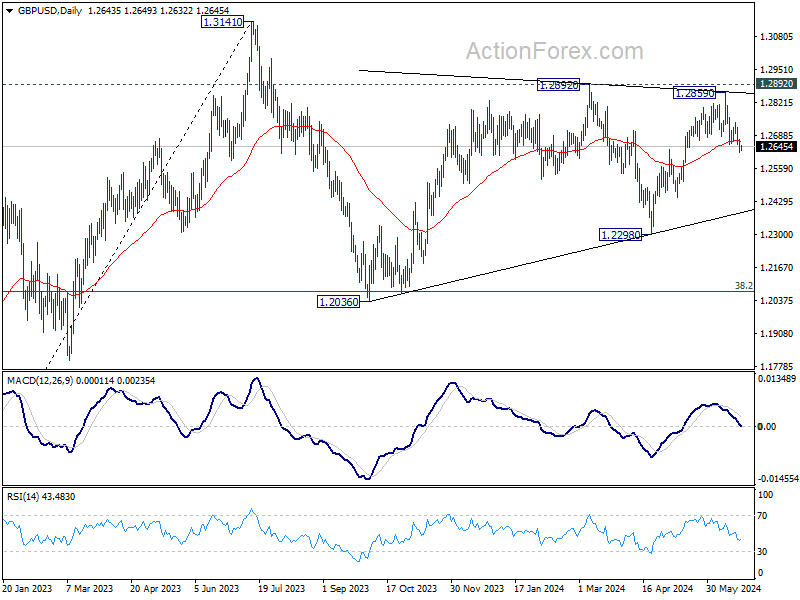

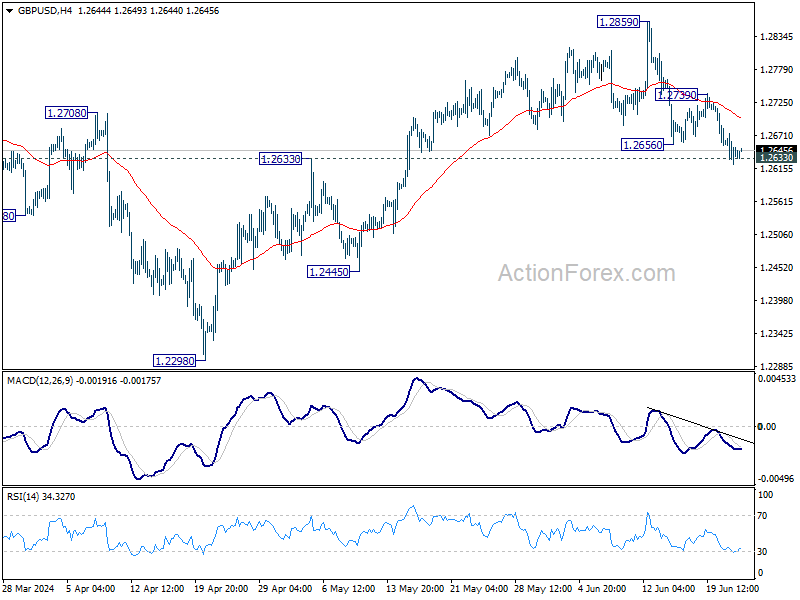

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2619; (P) 1.2646; (R1) 1.2671; More...

Intraday bias in GBP/USD remains mildly on the downside for the moment. Sustained break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. For now, risk will stay on the downside as long as 1.2739 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.