Sample Category Title

Sunset Market Commentary

Markets

It was a slow but constructive start of the week. The economic calendar had little to offer with the exception of the German Ifo indicator. Confidence fell in June from May with the headline series easing from 89.3 to 88.6. Both the current assessment (88.3) and the expectations (89.0) component fell short of expectations. More or less confirming last week’s (skewed) PMI’s, markets quickly set the downside surprise aside. A mildly constructive atmosphere dominated instead, lifting European equities about 0.80% higher. There’s a noteworthy outperformance of the car sector (> 2%). It followed news over the weekend that the EU and China have agreed to start talks over the bloc’s recently announced EV tariffs. It eases concerns for Chinese retaliatory measures against European carmakers. Core bond yields trade more or less flat, Bunds marginally underperforming Treasuries. German yields rise <2 bps across the curve. Both peripheral and the French spread vs Germany’s 10-yr yield ease a few basis points ahead of the June 30 snap elections (first round). Treasury yields change less than 1 bp in a daily perspective.

The Japanese yen drew most attention on currency markets. Ongoing JPY weakness triggered FX interventions around USD/JPY 160 end April and the beginning of May. Less than two months later, the pair is again closing in on these levels, with the latest acceleration coming on the back of dollar strength. Japan’s finance (vice-)minister this morning reiterated readiness to act again. USD/JPY today suddenly dropped from around 159.8 to 158.8 for no particular reason. We do recall a move out of thin air happening on Friday, April 26 as well (though it was a larger one back then). On Monday, April 29, the first round of interventions took place. The difference, for now, is that USD/JPY is slightly down for the day, as are most other dollar cross rates. EUR/USD rises from just south of 1.07 to 1.0738. The trade-weighted index eases towards 105.47. EUR/GBP continues to bottom out with the Bank of England having protected the pair’s downside better. The combination is currently changing hands around 0.8467, up from a daily low of 0.845.

News & Views

The June industrial trends survey released by the Confederation of British Industry (CBI) showed export orders deteriorating in June, falling from -27% to -39%, the weakest performance since February 2021 and significantly falling below the long-run average of -18%. Total orders on the other hand improved from -33% to -18% but also remain below average. Output volumes were broadly unchanged in the three months to June (+3%) following an increase in the quarter to May (+14%). Notably, only four out of 17 sub-sectors saw output growth. Growth was noted in the food, drink, and tobacco, motor vehicle and transport, and plastics and furniture and upholstery sub-sectors. Looking at the next three months, the outlook suggested a modest rise in output of +13%. Stocks of finished goods (+14%) are sufficient to meet expected demand. CBI lead economist Jones said that it’s encouraging to see that manufacturing remain confident the economy is heading in the right direction with the survey suggesting a broadening out over summer. Soft orders are a note of caution. Expectations for average selling prices accelerated from 15% to 20%.

Belgian business confidence stabilized in June (-11.1 from -11). This stability masks contrasting developments in the sectors surveyed, with a strong improvement observed in business-related services (1.4 from -2.1; mainly more favorable activity expectations) but a fall in confidence in trade (-21.5 from -17.4; more negative employment expectations and intentions of placing orders with suppliers), building (-11.4 from -10.3) and manufacturing (-13.1 from -12.7; worse demand expectations and a more negative assessment of total order books and stock levels). Last week, Belgian consumer confidence improved from -7 to -1, the second best level since February 2020.

Graphs

USD/JPY nears 160, triggering a new series of verbal (for now) interventions from Japanese finance officials

EuroStox50: carmakers among the best performers as China and EU agreed to start tariff talks

EUR/GBP extends its recent bottoming out process and has the BoE to thank for it

EUR/CZK eases after touching highest level in a month last Friday as it goes into the CNB’s (hawkish) cut on Thursday

Australian Dollar Calm Ahead of Consumer Confidence

The Australian dollar has started the week quietly. AUD/USD is trading at 0.6648 early in the North American session, up 0.11% on the day.

Australia releases Westpac Consumer Sentiment early on Tuesday. Consumer confidence has been weak and fell 0.3% in May to 82.4, following a 2.4% decline in April. Consumers have been pessimistic about the weak economy and concerns that sticky inflation could prod the Reserve Bank of Australia to hike interest rates.

The RBA has maintained its stance of “higher for longer”, holding rates at 4.35% for the past five meetings. The central bank hasn’t shied away from warning that it could raise rates if inflationary pressures don’t ease. The April CPI report surprised on the upside, rising from 3.5% to 3.6%, above the market estimate of 3.5%. The May CPI report will be released on Wednesday, with a market estimate of 3.8%. If inflation does rise again, we will no doubt hear the RBA express its concern and reiterate that rate hikes remain on the table.

The economy is barely treading above water and posted a weak 0.1% gain in the first quarter, but the labor market, which is surprisingly tight, continues to confound the RBA and has dampened any hope of a rate cut in the near term.

There are no US releases on Monday but we’ll hear from two FOMC members, Christopher Waller and Mary Daly. Investors will be hoping for some insights about the Fed’s rate path. The Federal Reserve has been hawkish as inflation has been stickier than anticipated. The markets have priced in a rate cut in September at around 60%, according to CME’s FedWatch.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6655. Above, there is resistance at 0.6685

- 0.6591 and 0.6541 are the next support levels

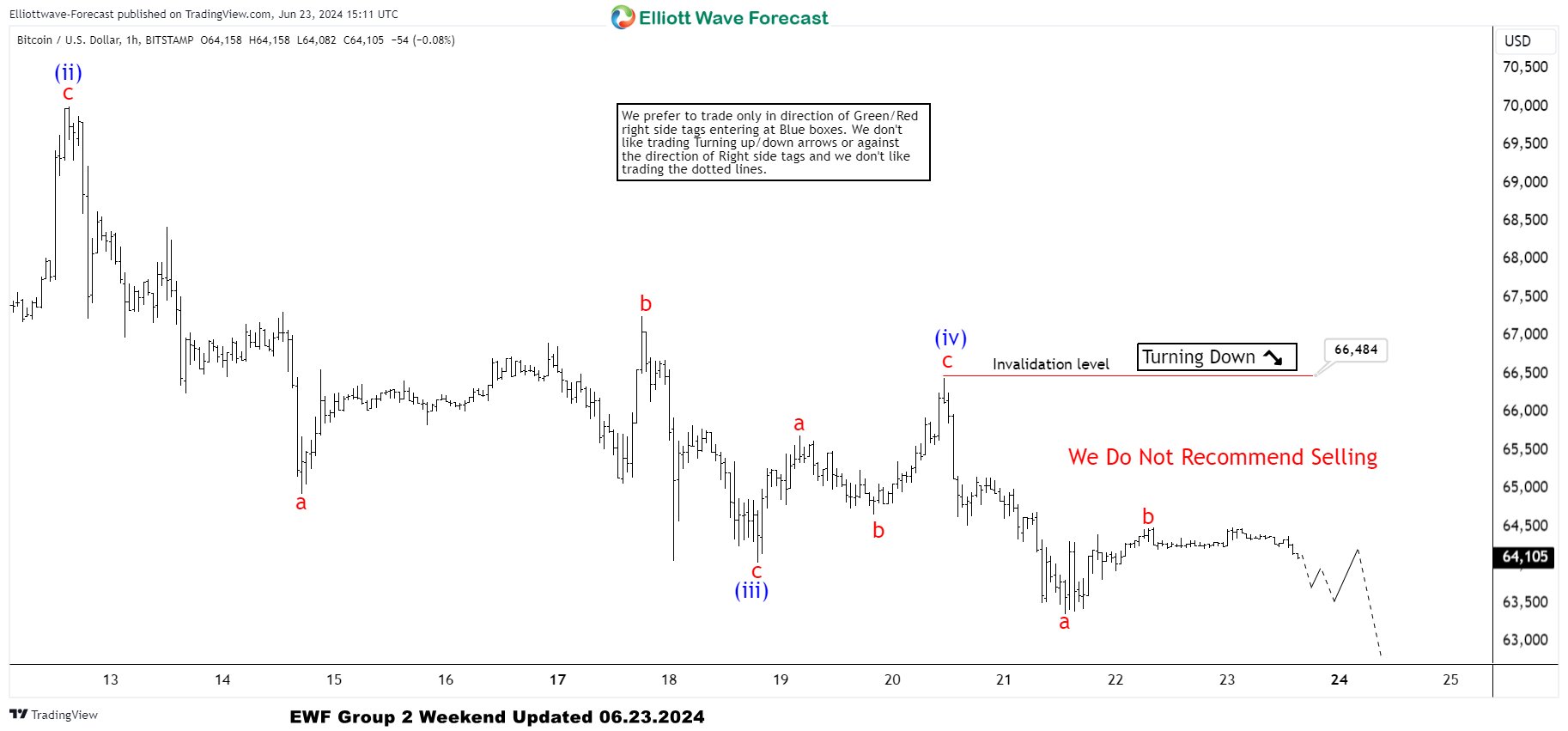

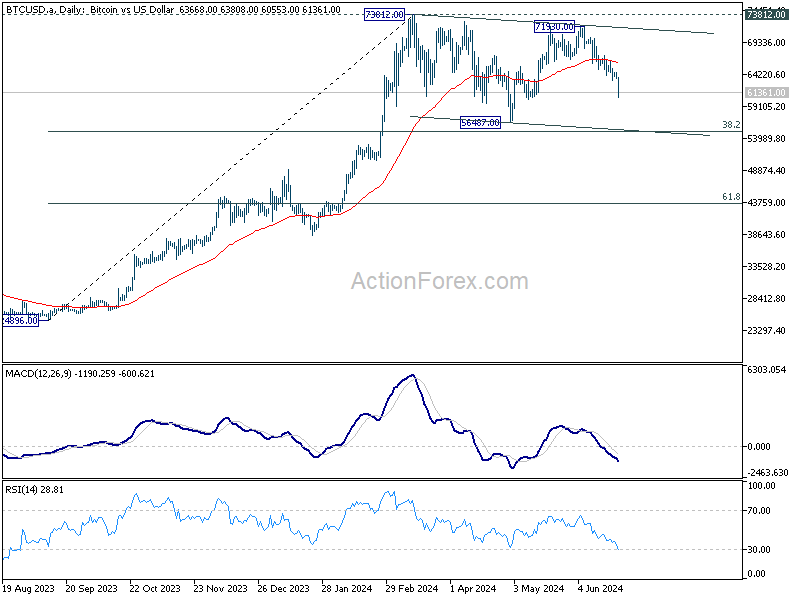

BTCUSD Elliott Wave : Forecasting the Decline Toward New Lows

In this technical article we’re going to take a quick look at the Elliott Wave charts of Bitcoin BTCUSD , published in members area of the website. As our members know, Bitcoin is doing a correction against the 56510 low, which is unfolding as a Flat pattern. Now, the crypto is showing impulsive sequences in the cycle from the June 7th peak, which can be the last leg of the proposed Flat pattern. Consequently, we expect more short-term weakness in the near term. In the further text, we are going to explain the wave count.

BTCUSD H1 Weekend Update 06.23.2024

BTCUSD has broken the previous low, confirming more downside in the near term against the 66484 pivot. The current view suggests that the intraday recovery completed at the 64482 high as b red. While below that high, we believe the c red leg is in progress toward new lows, targeting the 61592-59793 area. We expect Bitcoin to keep finding intraday sellers in 3, 7, and 11 swings.

BTCUSD H1 London Update 06.24.2024

Bitcoin made a further decline as expected, reaching our first target zone at 61592-59793. From there, we can see an intraday bounce. The count has been adjusted, now suggesting we are potentially still within wave (iii), which is part of the last leg of the proposed Flat pullback. We don’t recommend forcing trades in BTCUSD at this stage.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0669; (P) 1.0695; (R1) 1.0719; More....

Intraday bias in EUR/USD remains neutral as range trading continues above 1.0667. Further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

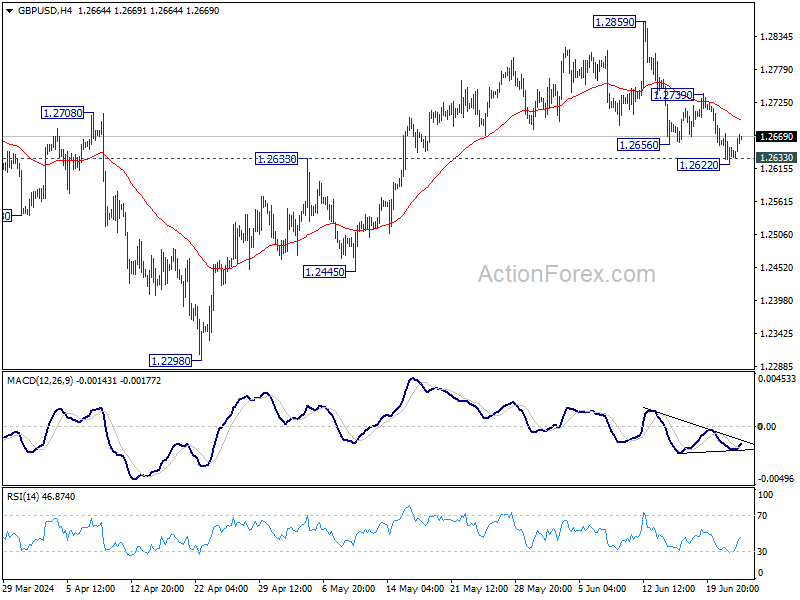

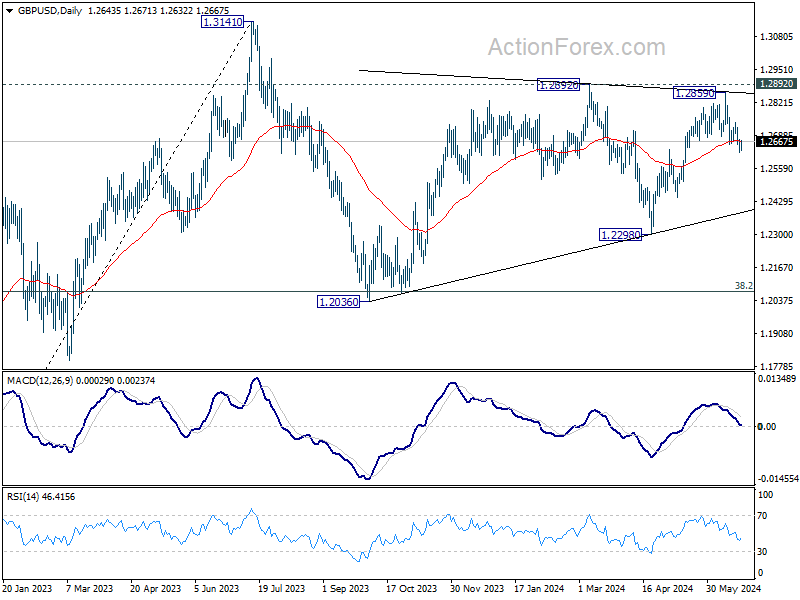

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2619; (P) 1.2646; (R1) 1.2671; More...

Intraday bias in GBP/USD is turned neutral first with current recovery. Further decline is expected as long as 1.2739 resistance holds. Break of 1.2622, and sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. However, firm break of 1.2739 will argue that pull back from 1.2859 has completed, and bring retest of this high instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

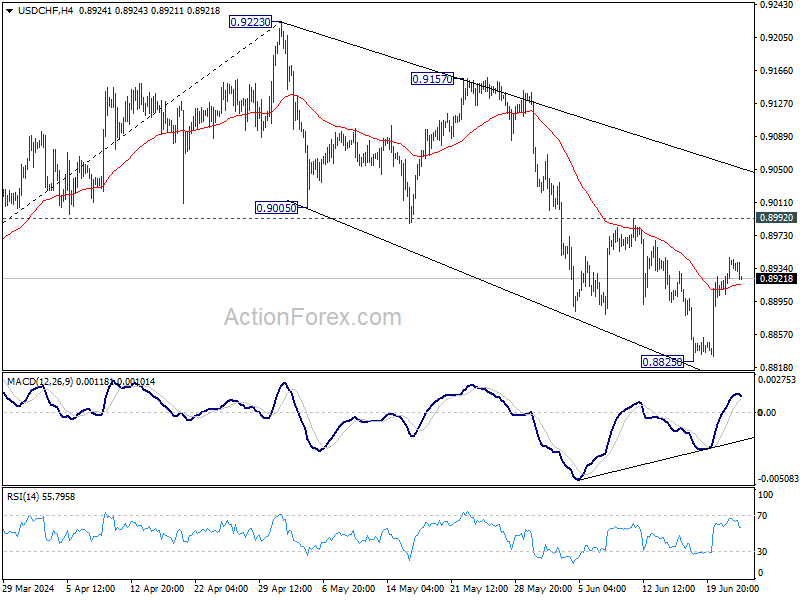

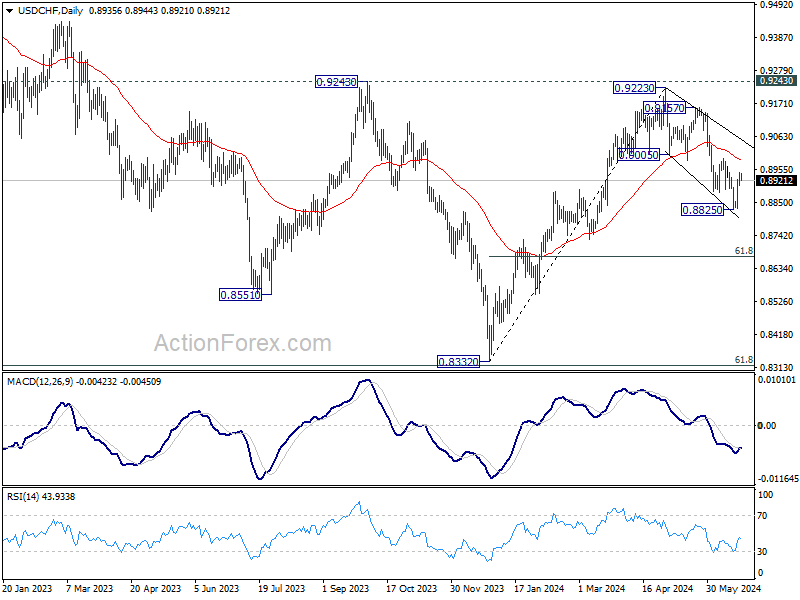

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8917; (P) 0.8931; (R1) 0.8958; More….

USD/CHF is extending the consolidation above 0.8825 and intraday bias remains neutral first. Still, near term outlook remains bearish with 0.8992 resistance intact. Break of 0.8825 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

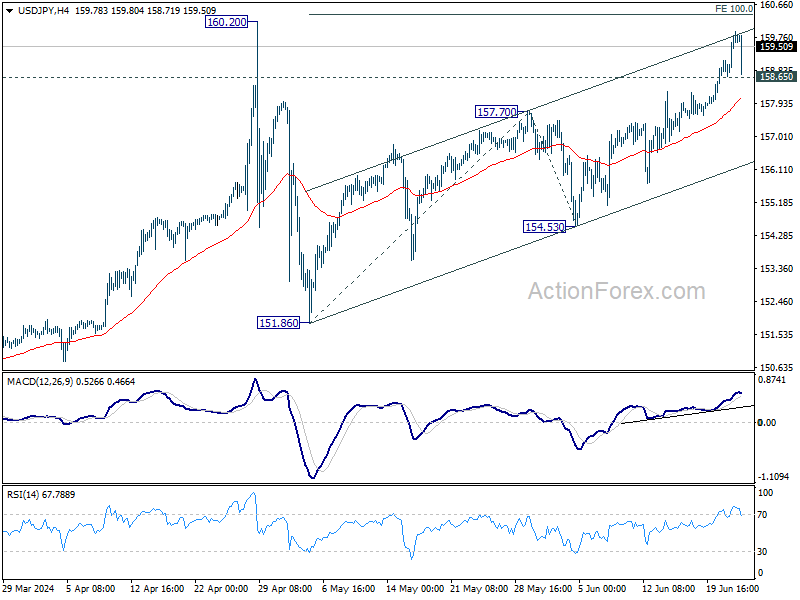

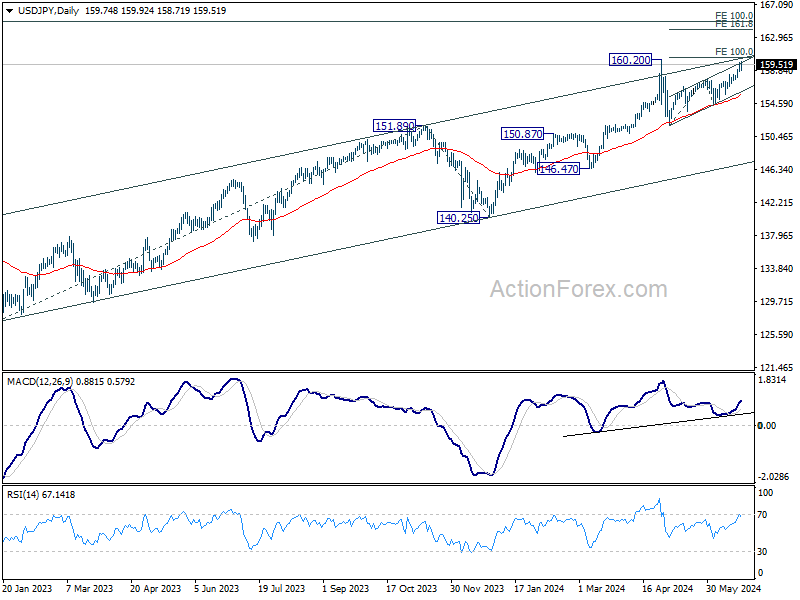

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.02; (P) 159.44; (R1) 160.22; More...

Despite the deep but brief retreat, intraday bias in USD/JPY stays mildly on the upside with 158.65 minor support intact. Current rally should target 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. Upside could be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first. However, decisive break of 160.37 will pave the way to 161.8% projection at 163.97.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Yen Rebounds from 160 Level, Euro Gains but Political Risks Remain

USD/JPY attempt to break through the critical 160 level was unsuccessful for, as Yen recovered during a relatively quiet European session today. Although Yen surged briefly, there was no sustained selloff below the 159 mark against the greenback. The scale of the movement makes it challenging to determine if Japan intervened in the market. This could be due to a cautious probe by the authorities, actions by institutional traders, or simply heightened market nerves. Yen will remain under close scrutiny, especially given the lack of significant economic data from the US until tomorrow's European session.

Euro is currently the best performer today, with notable bounce against Sterling. However, the rebound in the common currency isn't strong enough to signal a reversal of the recent downtrend yet. According to the latest Ipsos poll released over the weekend, the far-right National Rally continues to lead the first round of the parliamentary elections with 35.5% of the vote, followed by the left-wing New Popular Front with 29.5%. Should these poll results be reflected in the elections, Euro could face another wave of selling pressure.

Across the broader currency markets, Euro and Yen are the strongest performers today, followed by the Sterling. In contrast, New Zealand Dollar and Australian Dollar are the weakest, alongside Dollar, with Canadian Dollar also lagging. The Swiss Franc is positioned in the middle of the performance spectrum.

Technically, Bitcoin is now extending the corrective pattern from 73812, with fall from 71930 as the third leg. Deeper decline could be seen in the near term to 56487 support. Strong downside should be contained by 38.2% retracement of 24896 to 73812 at 55126 to bring rebound. Meanwhile, sustained break of 55 D EMA (now at 66019) will suggest that Bitcoin is ready for another test on 73812 again.

In Europe, at the time of writing, FTSE is up 0.43%. DAX is up 0.54%. CAC is up 0.83%. UK 10-year yield is up 0.001 at 4.089. Germany 10-year yield is up 0.015 at 2.427. Earlier in Asia, Nikkei rose 0.54%. Hong Kong HSI fell -0.00%. China Shanghai SSE fell -1.17%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.0138 to 0.991.

German Ifo falls to 88.6, struggling to overcome stagnation

German Ifo Business Climate fell from 89.3 to 88.6 in June, below expectation of 89.7. Current Assessment index was unchanged at 88.3, below expectation of 88.4. Expectations Index fell from 90.3 to 89.0, below expectation of 91.0.

Ifo said that the German economy is "having difficulty overcoming stagnation".

By sector, manufacturing fell from -6.5 to -9.2. Services rose from 1.8 to 4.2. Trade fell from -17. to -23.5. Construction ticked up from -25.6 to -25.0.

BoJ deliberates on rate hikes, Yen depreciation, and JGB purchase adjustments

During Monetary Policy Meeting on June 13-14, BoJ board discussed the need for adjustments in response to rising inflation risks. One key opinion indicated that if April Outlook Report's economic and inflation forecasts are realized, BoJ will raise the policy interest rate and adjust monetary accommodation.

Another member warned that prices could "deviate upward" from the baseline scenario if recent cost increases are passed on to consumers, suggesting a need for further policy adjustments from a "risk management" perspective. It's also highlighted the growing "upside risks" to prices, with one member stating these risks have affected consumer sentiment and that the policy interest rate should be raised "not too late" if appropriate.

The impact of Yen's depreciation was also discussed, with an opinion suggesting an "upward revision" to the inflation outlook, warranting a higher risk-neutral policy interest rate. Some members emphasized the importance of basing monetary policy on the "overall picture of developments in economic activity and prices," rather than short-term foreign exchange fluctuations. They stressed that policy should be informed by trends in prices and wage developments.

Regarding asset purchases, one opinion recommended reducing the purchase amount of Japanese government bonds to allow long-term interest rates to form more freely in financial markets. This reduction should be "sizeable" and "predictable," while ensuring flexibility to maintain stability in JGB market.

New Zealand's goods exports reach record high in may, trade surplus exceeds expectations

New Zealand's goods exports rose by 2.9% yoy to NZD 7.2B in May, marking the first time that monthly exports have surpassed the NZD 7B mark. Goods imports also saw a slight increase, rising by 0.6% yoy to NZD 7.0B. This resulted in a trade surplus of NZD 204m, exceeding the expected NZD 155m.

Breaking down the top monthly export movements by country, New Zealand saw mixed results. Exports to China fell by -12% yoy, and exports to Australia dropped by -3.8% yoy. In contrast, exports to the US surged by 33% yoy, while exports to the EU and Japan rose by 2.8% yoy and 12% yoy, respectively.

On the import side, imports from China increased by 2.6% yoy, while imports from the EU decreased by -1.8% yoy. Imports from Australia -4.7% yoy, whereas imports from the US and South Korea rose by 1.6% yoy and 5.8% yoy, respectively.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.02; (P) 159.44; (R1) 160.22; More...

Despite the deep but brief retreat, intraday bias in USD/JPY stays mildly on the upside with 158.65 minor support intact. Current rally should target 160.20 high, or possibly to 100% projection of 151.86 to 157.70 from 154.53 at 160.37. Upside could be limited there, at least on first attempt. On the downside, below 158.24 minor support will turn intraday bias neutral first. However, decisive break of 160.37 will pave the way to 161.8% projection at 163.97.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 204M | 155M | 91M | -3M |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 08:00 | EUR | Germany IFO Business Climate Jun | 88.6 | 89.7 | 89.3 | |

| 08:00 | EUR | Germany IFO Current Assessment Jun | 88.3 | 88.4 | 88.3 | |

| 08:00 | EUR | Germany IFO Expectations Jun | 89 | 91 | 90.4 | 90.3 |

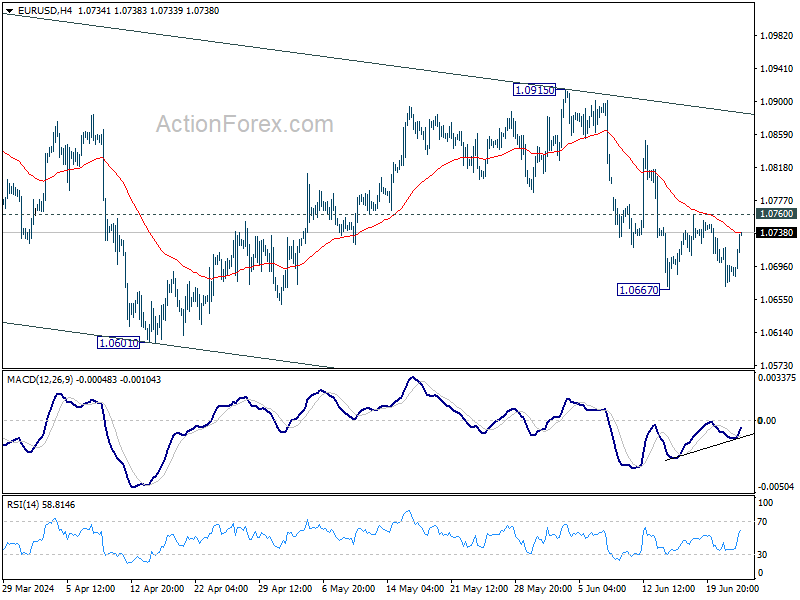

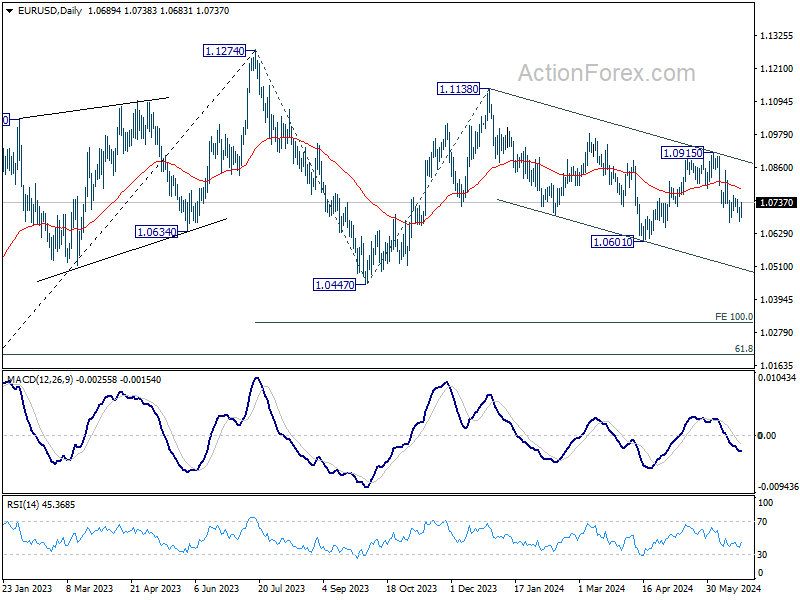

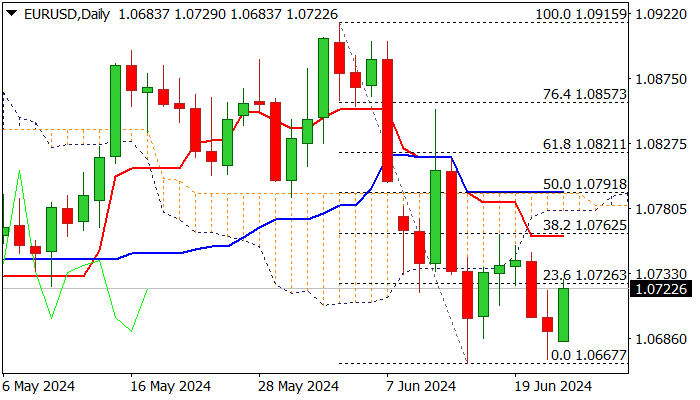

EUR/USD: Bounce Needs to Clear 1.0760 Barrier to Signal Stronger Correction

EURUSD bounces on Monday, as traders collect profits from Thu/Fri fall.

The single currency regained traction despite weaker than expected German Ifo data, as sentiment improves on growing expectations on ECB rate cut, following recent weak economic data.

Markets shift focus to US PCE data and French election, due this week and expected to generate fresh signals.

Formation of a double-bottom at 1.0670 zone on daily chart and likely bullish engulfing, generate initial signal, along with magnetic daily cloud twist on Wednesday.

However, the downside is expected to remain vulnerable as long as current bounce stays below upper pivots at 1.0760 zone (daily Tenkan-sen / Fibo 38.2% of 1.0915/1.0667), as 14-d momentum is deeply in negative territory and adds to warning of limited correction of larger downtrend.

Firm break through 1.0760/80 zone is needed to ease downside risk, though a number of strong barriers lays above and would make recovery attempts more difficult.

Res: 1.0731; 1.0760; 1.0785; 1.0800.

Sup: 1.0700; 1.0667; 1.0649; 1.0624.

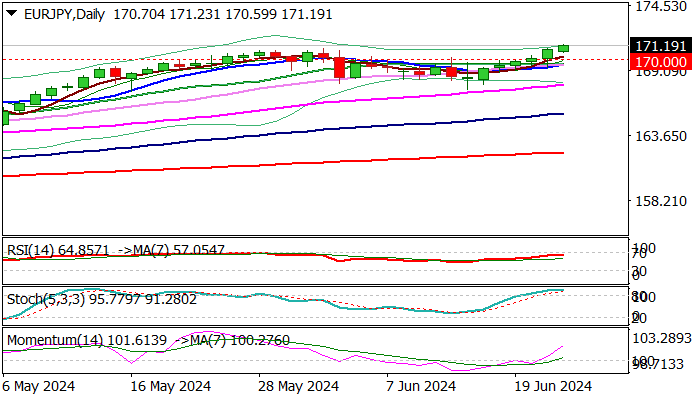

EUR/JPY Outlook: Hits New Record High

EURJPY continues to trend higher and extends steep upleg into sixth straight day, to hit new record high above 171 mark in early Monday trading.

Bulls firmly hold grip despite overbought conditions and signals from Japan’s authorities about the intervention to support falling yen, which came under increased pressure after dovish BoJ’s stance in the last meeting.

The pair is on track for the first monthly close above psychological 170 level, with last week’s significant gains and completion of bullish engulfing pattern on weekly chart, as well as long tail on last week’s candle, adding to positive signals.

However, initial warnings about rally’s stall cannot be ignored.

Technical studies are overbought on daily and monthly chart, where a loss of bullish momentum is evident, but any firmer signals are still to be seen.

Until then, we will hold in bullish mode, but with increased caution and tightened stops.

Broken 170 level and 2008 former record high (169.95) reverted to solid supports, reinforced by nearby converging 20/10 DMA’s (169.65/60), loss of which to generate stronger bearish signal and open way for deeper pullback.

Res: 171.50; 172.00; 172.20; 172.96.

Sup: 171.00; 170.60; 170.00; 169.60.