Sample Category Title

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3637; (P) 1.3672; (R1) 1.3695; More...

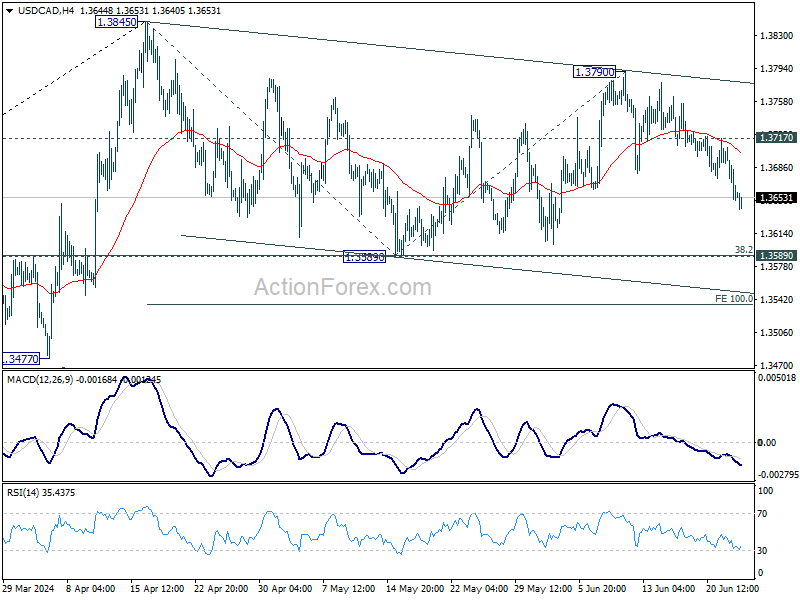

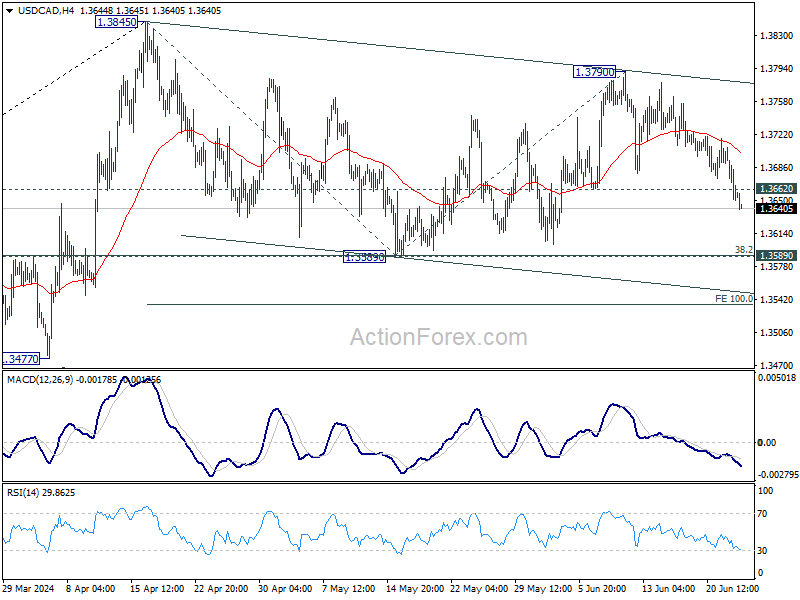

USD/CAD's extended fall from 1.3790 suggests that rebound form 1.3589 has completed. Corrective pattern from 1.3845 is now in the third leg. Intraday bias is back on the downside for 1.3589 support. Break there will target 100% projection of 1.3845 to 1.3589 from 1.3790 at 1.3534. On the upside, above 1.3717 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6633; (P) 0.6650; (R1) 0.6675; More...

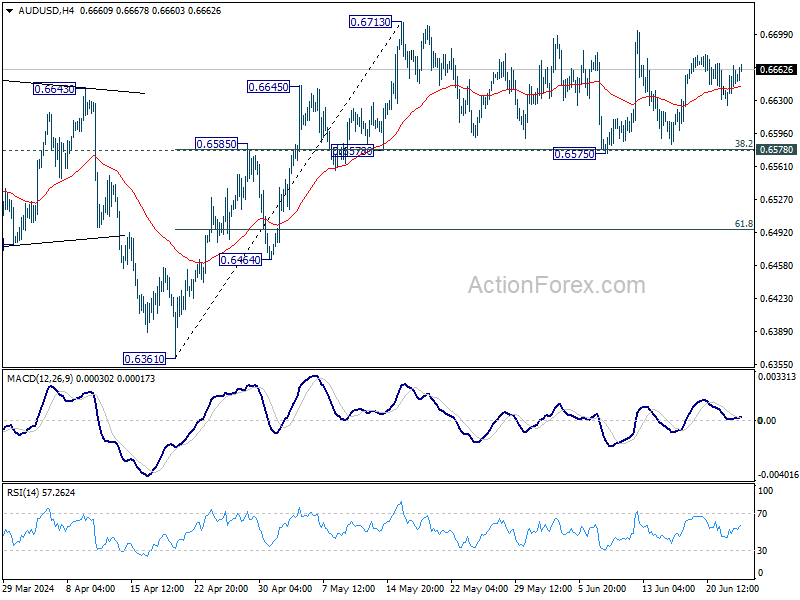

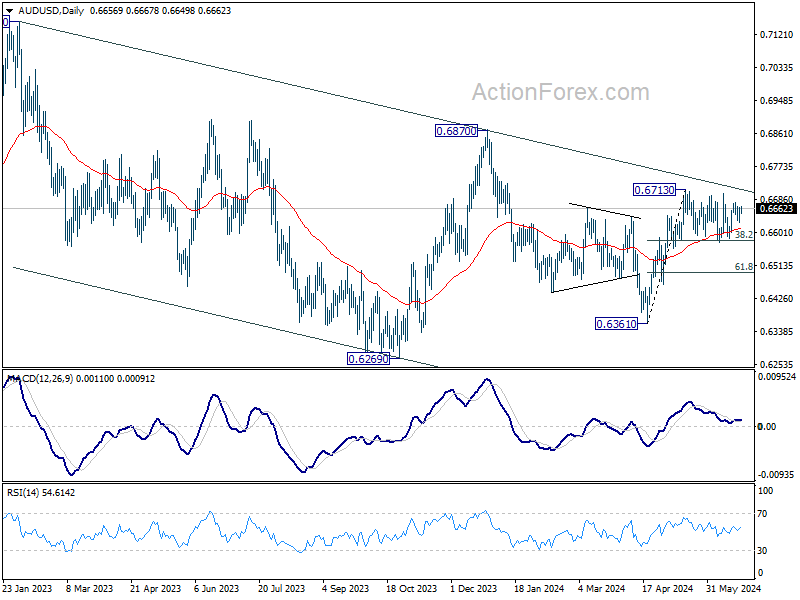

AUD/USD is still bounded in consolidation from 0.6713 and intraday bias stays neutral. Further rally is in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

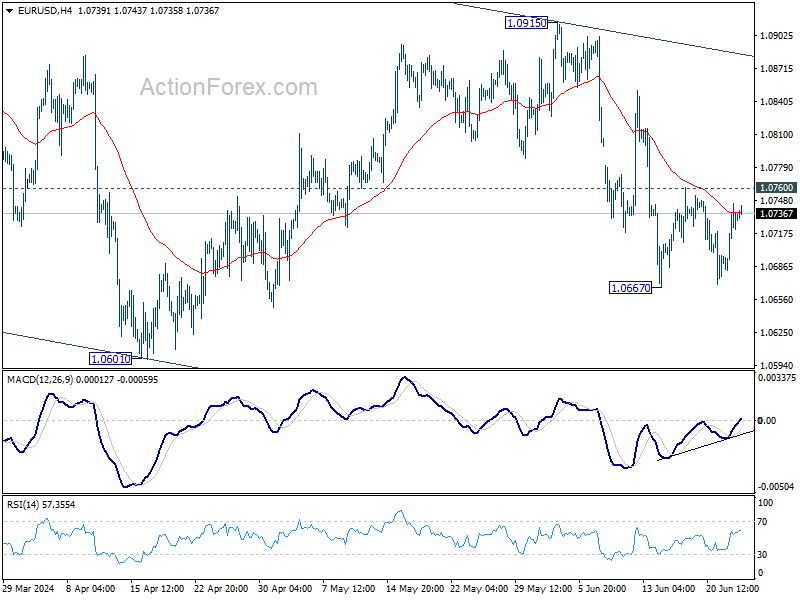

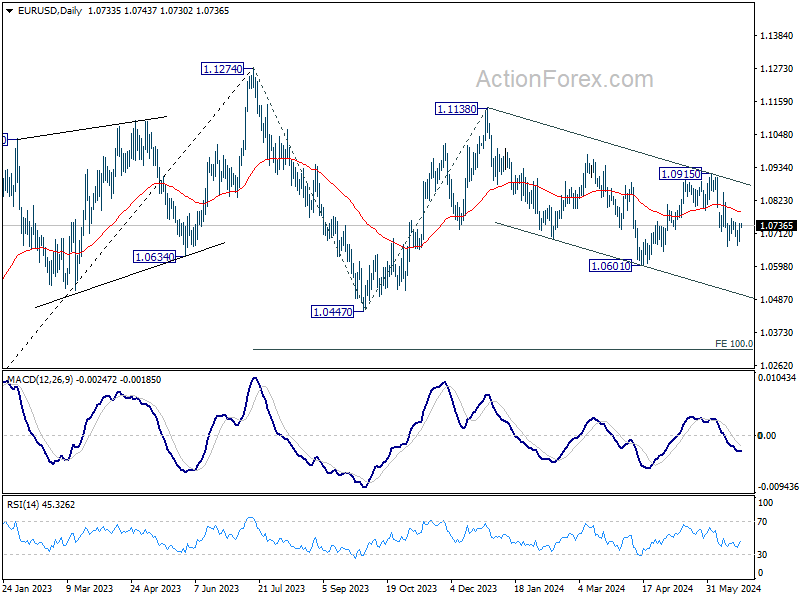

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0696; (P) 1.0721; (R1) 1.0760; More....

EUR/USD is extending the consolidations from 1.0667 and intraday bias stays neutral. Further fall is expected with 1.0760 resistance intact. Decline from 1.0915 is seen as another leg in the larger corrective pattern. Break of 1.0667 will target 1.0601 and below. However, firm break of 1.0760 will turn intraday bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

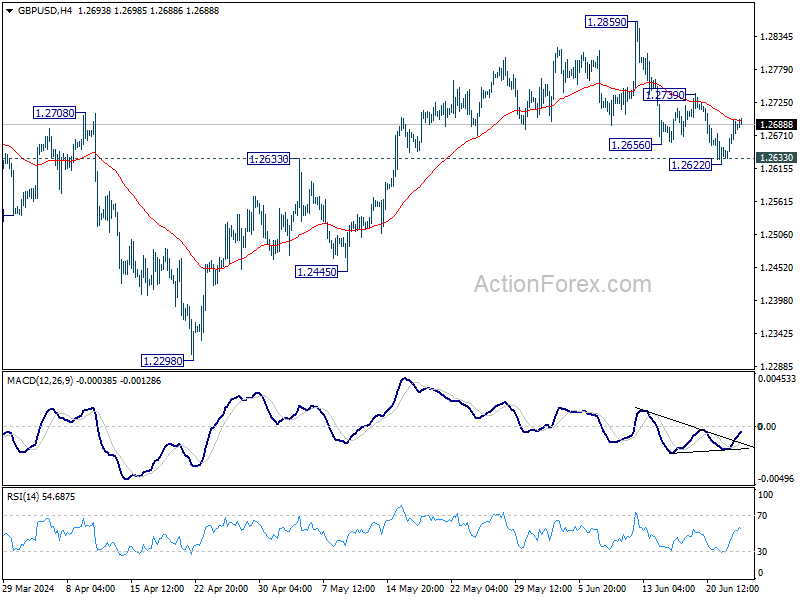

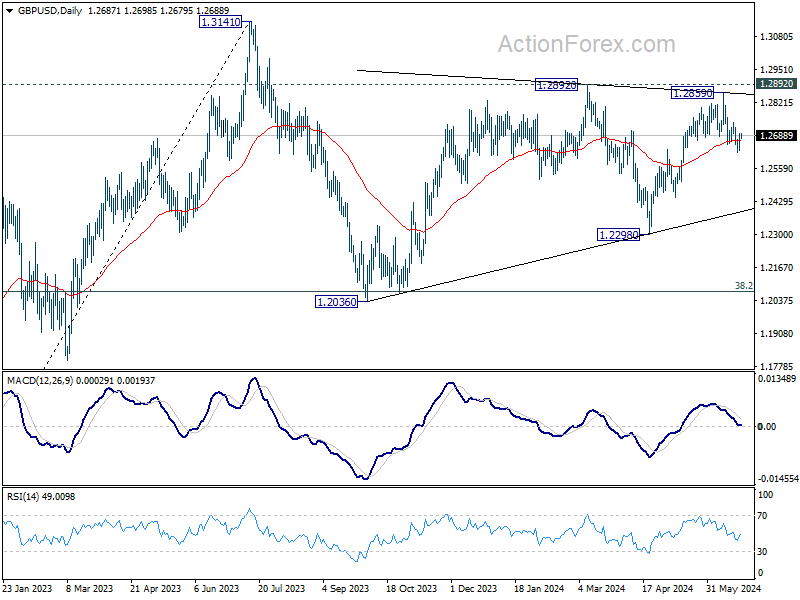

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2672; (R1) 1.2712; More...

Intraday bias in GBP/USD remains neutral for the moment. Further decline is expected as long as 1.2739 resistance holds. Break of 1.2622, and sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below. However, firm break of 1.2739 will argue that pull back from 1.2859 has completed, and bring retest of this high instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8919; (P) 0.8932; (R1) 0.8943; More….

USD/CHF is still bounded in consolidation from 0.8825 and intraday bias stays neutral at this point. Near term outlook remains bearish with 0.8992 resistance intact. Break of 0.8825 will resume the fall from 0.9223 to 61.8% retracement of 0.8332 to 0.9223 at 0.8672.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside break out is mildly in favor at a later stage.

Tech Down, Energy Up

The selloff in Nvidia deepened yesterday and sent the shares into the correction territory following a 10% selloff. Nvidia shares erased around $430 bn in market cap over the past three sessions. The selloff hit suddenly, right after the company stole the status of the world’s most valuable company from Microsoft last week. There has been no bad news regarding the company’s fundamentals on the newswire, no analyst downgrades, no soft forecasts, no rumours of slowing sales. It’s just that the end of last quarter and the first half may have brought some investors to take some profit and go to the sidelines.

One question that everyone asks is, whether last week’s good news marked the finale of the Nvidia’s surge to the top, and if the past three-day selloff is the beginning of a sharper downside correction. I don’t have the answer to that question, the time will tell. Yes, there has certainly been strong speculation in Nvidia’s exponential surge since the beginning of last year. And yes, strong rallies were often followed by sharp selloffs. In this context, Nvidia probably has ways to correct before finding a more reasonable valuation.

From a technical perspective, the first support is seen near $110 a share, the minor 23.6% Fibonacci retracement on the AI rally that started at the beginning of last year with the launch of OpenAI’s ChatGTP. The 50-DMA, just above the $100 psychological support presently, could act as another support and finally, the major support to the AI rally is the $92 per share level, the major 38.2% Fibonacci retracement should, in theory, distinguish between the actual AI rally and a medium term bearish reversal.

The other question in minds is if the price pullback a good opportunity to strengthe long position at a better price before Nvidia announces its Q2 earnings, where it’s expected to reveal a monstruous $28bn sales, which is more than the double of money is made the same time last year.

In all cases, it’s too early to call the end of the Nvidia-mania, but given the high amount of speculation around the stock, we shall see the price action gets worse before it gets better.

Elsewhere, fortunes for Apple are improving as the company – who have lagged its peers in the AI rally – found an opportunity window to bring investors back on board and that opportunity window is offering the AI tools developed by others on their iPhones – with free partnerships – to see if people would buy the latest AI-boosted models. In this context, Apple announced that it would integrate Meta’s Llama 3 AI to its products, after it announced earlier that it would also offer OpenAI’s ChatGPT on iPhones. It’s a genius move, let’s see if it could make the AI rally change hands!

Energy smiles

Yesterday’s 6.68% plunge in Nvidia shares didn’t do good to mood in Nasdaq 100. The index dropped more than 1% whereas losses in the S&P500 remained limited to 0.31%, as the financials gained 0.63% while energy sector rallied 1.70% on the back of a rebound in crude oil to retest the $82pb level resistance, the major 61.8% level on the latest selloff. If this level is cleared, oil bulls will have a higher conviction on the sustainability of the rally and the gains could extend toward the $85pb level. The question is, do the soft economic data around the world justify a further rise in oil prices? Chinese growth is still not as strong as it should be, German business expectations unexpectedly declined for the first time in five months and the latest data from the US hinted at a faster-than-anticipated slowdown in the US economy. On the other hand, the central banks expectations aren’t easing enough to compensate for the slowing Western economies. So I’m wondering if we could see enough conviction above the $82pb level to carry this rally higher. And also, I’m wondering whether higher oil prices wouldn’t boost inflation expectations and jeopardize soft central bank expectations and limit the upside.

In the FX

The US dollar index eased yesterday, as the weekend euro bears scaled back their positions after the weekend. The EURUSD rebounded to near 1.0750. We could see the euro recover against the greenback in the first half of the year but I would expect the bears to come back in charge before the weekend, as the first round of the French legislative elections are due this weekend and political risks remain high as Marine Le Pen’s National Rally is seen getting more than a third of the votes. Elsewhere, the USDJPY trades a touch below the critical 160 level as the yen bears are testing the nerves of the Japanese officials to see what level will trigger an FX intervention. In Canada, the Loonie benefits from a rise in oil prices. Due today, data is expected to show a further slowdown in Canadian inflation and could fuel the expectation that the Bank of Canada (BoC) could continue pulling its rates lower. But we could see oil prices weigh heavier in the balance than rate cut expectations if crude prices break above a key resistance.

Spotlight on US Consumer Sentiment

In focus today

- Today's schedule is light in terms of data releases.

- In the US we get the Conference Board Consumer Confidence numbers for June at 16.00 CEST. A Reuters poll has consensus expecting 100.0, slightly down from 102.0 in May.

- In Sweden, May PPI is released at 08.00 CEST. Its development has been normalized over many months now. However, frontloaded import inflation has begun to moderately pick up pace and is now slightly above its historical mean. Thus, Sweden is no longer importing a deflationary pressure.

- FOMC members Bowman and Cook (both voting members) give speeches today. Bowman speaks at both 13.00 and 20.10 CEST and Cook at 18.00 CEST.

Economic and market news

What happened overnight

In Japan, the Chief Cabinet Secretary Yoshimasa Hayashi said that authorities would respond appropriately to excess FX volatility. The top governmental spokesperson emphasised that currency volatility was negatively affecting both households and businesses, as such following the lines of Japanese Finance Minister Shunichi Suzuki, who had said earlier that currency rates 'need to be stable', and that authorities would respond 'appropriately to excessive currency moves'. The Japanese yen has been nearing 160 against the US dollar (USDJPY), and trades around 159.4 as of this morning. When the USDJPY hit a 34-year trough of 160.245 earlier this year it triggered interventions by authorities in late April and early May of USD61.33bn.

In the US, president of the San Fransisco Fed, Mary Daly, said the Fed need not only worry about inflation as rising unemployment was increasingly becoming a risk. Daly said inflation still posed a risk, and the Fed would hence need to keep monetary policy strict to dampen demand. However, she said in doing so, it would need to exhibit care so as not to risk it translating into too high unemployment.

What happened yesterday

In Germany, the Ifo declined in line with Friday's composite PMIs. Ifo dropped solely due to its expectations component which fell to 89.0 (consensus: 90.7, prior: 90.3), whereas the assessment of the current business situation stood unchanged at 88.3 (consensus: 90.7, prior: 90.3). The June decline in both the Ifo and PMI follows several months of strengthening. Although one should caution against overinterpreting a single month's data, the weak sentiment signals in June clearly questions the strength of the growth rebound seen in the first half of 2024.

In Sweden, finance minister Elisabeth Svantesson declared victory over inflation, and stated that fiscal policy would no longer try to beat inflation. The finance minister however reiterated that what matters going forward is not the amount spent, but rather the type of fiscal measures that are implemented, as long-term fiscal stability remains a core objective. As such, the finance minister warned that fiscal policy will not necessarily turn expansionary just because inflation has come under control.

In the US, President of the Chicago Fed, Austan Goolsbee, said policy makers were still looking for further cooling of inflation before considering initiating their first rate cut. Goolsbee described himself as a 'closet optimist' that improvements in terms of inflation would soon show themselves in data releases.

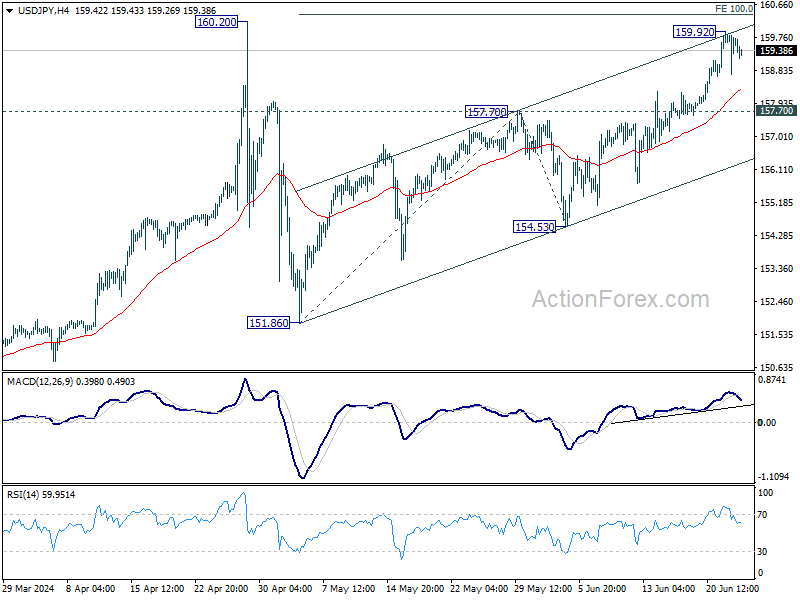

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.95; (P) 159.43; (R1) 160.11; More...

A temporary top should be formed at 159.92 in USD/JPY and intraday bias is turned neutral first. Further rise will remain in favor as long as 157.70 resistance turned support holds. Sustained break of 106.20 and 100% projection of 151.86 to 157.70 from 154.53 at 160.37 will confirm long term up trend resumption, and pave the way to 161.8% projection at 163.97. Nevertheless, firm break of 157.70 will turn bias back to the downside for channel support (now at 156.23) first.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Canadian CPI Takes Center Stage; Yen Stabilizes in Quiet Trading

Trading in the Asian session has been quiet today and is expected to remain so during the European session, given the empty economic calendar. However, Yen continues to be a significant focus among market participants. Discussions are emerging about the possibility of USD/JPY surging through the 160 level, which is currently perceived as the intervention threshold for Japanese authorities, reaching 170 in a rapid manner.

The primary driver behind this speculation is the substantial interest rate gap between the US and Japan, which is unlikely to narrow significantly anytime soon. Today's data from Japan, showing a further slowdown in business-to-business service inflation in May, does not bolster the case for BoJ to hike rates again in July. Additionally, intervention alone, without substantial market participation in buying Yen, is considered insufficient to reverse the currency's course.

Attention will also turn to Canadian Dollar later in the day with the release of Canadian CPI data. BoC Governor Tiff Macklem has stated that he does not want to ease monetary policy "too quickly," aligning with the expectation that BoC will not deliver back-to-back rate cuts in July. Stronger-than-expected inflation readings today would likely prompt BoC to maintain its current stance for longer before considering the second rate cut in this cycle.

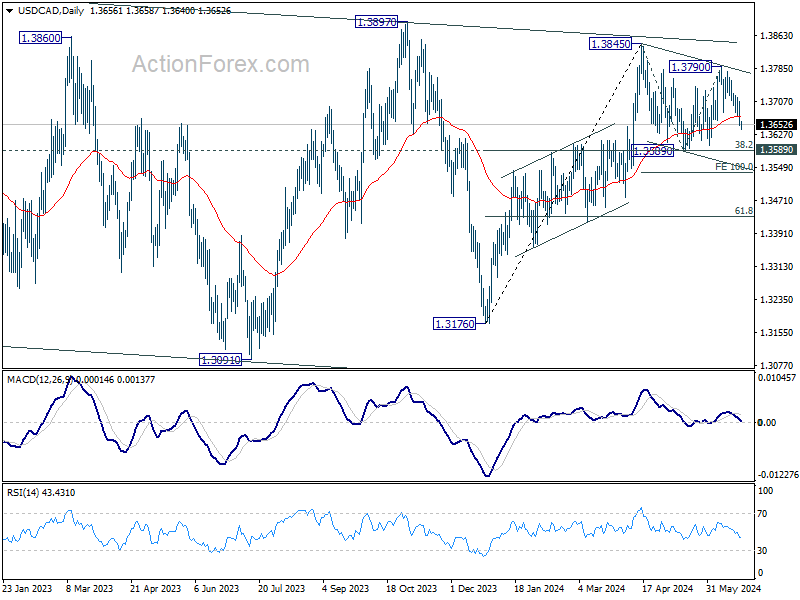

Technically, USD/CAD's extended fall from 1.3790 suggests that rebound from 1.3589 has completed. Corrective pattern from 1.3845 is now extending with the third leg. Deeper fall would be seen to 1.3589 support, or even further to 100% projection of 1.3845 to 1.3589 from 1.3790 at 1.3534.

In Asia, at the time of writing, Nikkei is up 0.72%. Hong Kong HSI is up 0.41%. China Shanghai SSE is down -0.10%. Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is up 0.0099 at 1.001. Overnight, DOW rose 0.67%. S&P 500 fell -0.31%. NASDAQ fell -1.09%. 10-year yield fell -0.009 to 4.248.

Fed's Daly: We have two goals, one tool, and a lot of uncertainty

San Francisco Fed President Mary Daly, in a speech last night, discussed the ongoing challenges with inflation and the labor market. Daly remarked that the inconsistent inflation data this year has not built confidence. While recent figures are promising, it remains uncertain if the path to sustainable price stability is secure.

While, the labor market has been slow to adjust, with only a slight increase in the unemployment rate, Daly warned that "we are getting nearer to a point where that benign outcome could be less likely. "

Emphasizing Fed's situation with "two goals, one tool, and a lot of uncertainty," and Daly stressed that "policy has to be conditional" and policymakers have to "think in scenarios."

Daly outlined the possible policy responses to different economic scenarios. "If inflation turns out to fall more slowly than projected, then holding the federal funds rate higher for longer would be appropriate."

Conversely, "If inflation falls rapidly, or the labor market softens more than expected, then lowering the policy rate would be necessary."

Daly also addressed a middle-ground scenario, saying, "If we continue to see gradual declines in inflation and a slow rebalancing in the labor market, then we can normalize policy over time, as many expect."

BoC's Macklem monitoring wage growth for further moderation

BoC Governor Tiff Macklem emphasized overnight that the central bank doesn't want monetary to be "more restrictive than it has to be,". Yet he also cautioned against lowering borrowing costs "too quickly" as it could undermine progress on controlling inflation.

Macklem pointed out that although wage growth remains above pre-pandemic levels, there are signs that the labor market is rebalancing and inflation is moderating, which could reduce compensation pressures.

"Wages tend to lag adjustments in employment," he explained, adding, "Going forward, we will be looking for wage growth to moderate further."

Australia's Westpac consumer sentiment ticks up but still deeply pessimistic

Australia's Westpac Consumer Sentiment rose 1.7% mom to 83.6 in June. However, the index remains deeply pessimistic, well below neutral level of 100. Although assessments of personal finances and buyer sentiment have become less negative, concerns about inflation, interest rates, and economic growth continue to weigh heavily on consumers.

The sub-index tracking the 'economic outlook for the next 12 months' fell -5.7% mom to 78.5, marking its lowest level since last October. In contrast, the 'economic outlook for the next 5 years' sub-index saw a slight improvement, rising 2.1% mom to 94.1.

Regarding RBA monetary policy, Westpac noted that the upcoming Q2 CPI data, due on July 31, will be crucial. Westpac expects the update to confirm that weak demand is still exerting disinflationary pressure. This should provide RBA with sufficient confidence that upside risks are not materializing, reducing the likelihood of a rate hike.

Looking ahead

The economic calendar is empty in Europen session. Canada CPI is the main focus later in the day. US will relase house price index and consumer confidence.

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.95; (P) 159.43; (R1) 160.11; More...

A temporary top should be formed at 159.92 in USD/JPY and intraday bias is turned neutral first. Further rise will remain in favor as long as 157.70 resistance turned support holds. Sustained break of 106.20 and 100% projection of 151.86 to 157.70 from 154.53 at 160.37 will confirm long term up trend resumption, and pave the way to 161.8% projection at 163.97. Nevertheless, firm break of 157.70 will turn bias back to the downside for channel support (now at 156.23) first.

In the bigger picture, there is no sign of long term trend reversal yet. Further rally is expected as long as 150.87 resistance turned support holds. Decisive break of 160.02 will target 100% projection of 127.20 to 151.89 from 140.25 at 164.94.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 2.50% | 2.80% | 2.70% | |

| 00:30 | AUD | Westpac Consumer Confidence Jun | 1.70% | -0.30% | ||

| 12:30 | CAD | CPI M/M May | 0.30% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y May | 2.60% | 2.70% | ||

| 12:30 | CAD | CPI Core M/M May | 0.20% | 0.20% | ||

| 12:30 | CAD | CPI Media Y/Y May | 2.60% | 2.60% | ||

| 12:30 | CAD | CPI Trimmed Y/Y May | 2.80% | 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y May | 2.60% | 2.60% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | 7.00% | 7.40% | ||

| 13:00 | USD | Housing Price Index M/M Apr | 0.50% | 0.10% | ||

| 14:00 | USD | Consumer Confidence Jun | 100.2 | 102 |

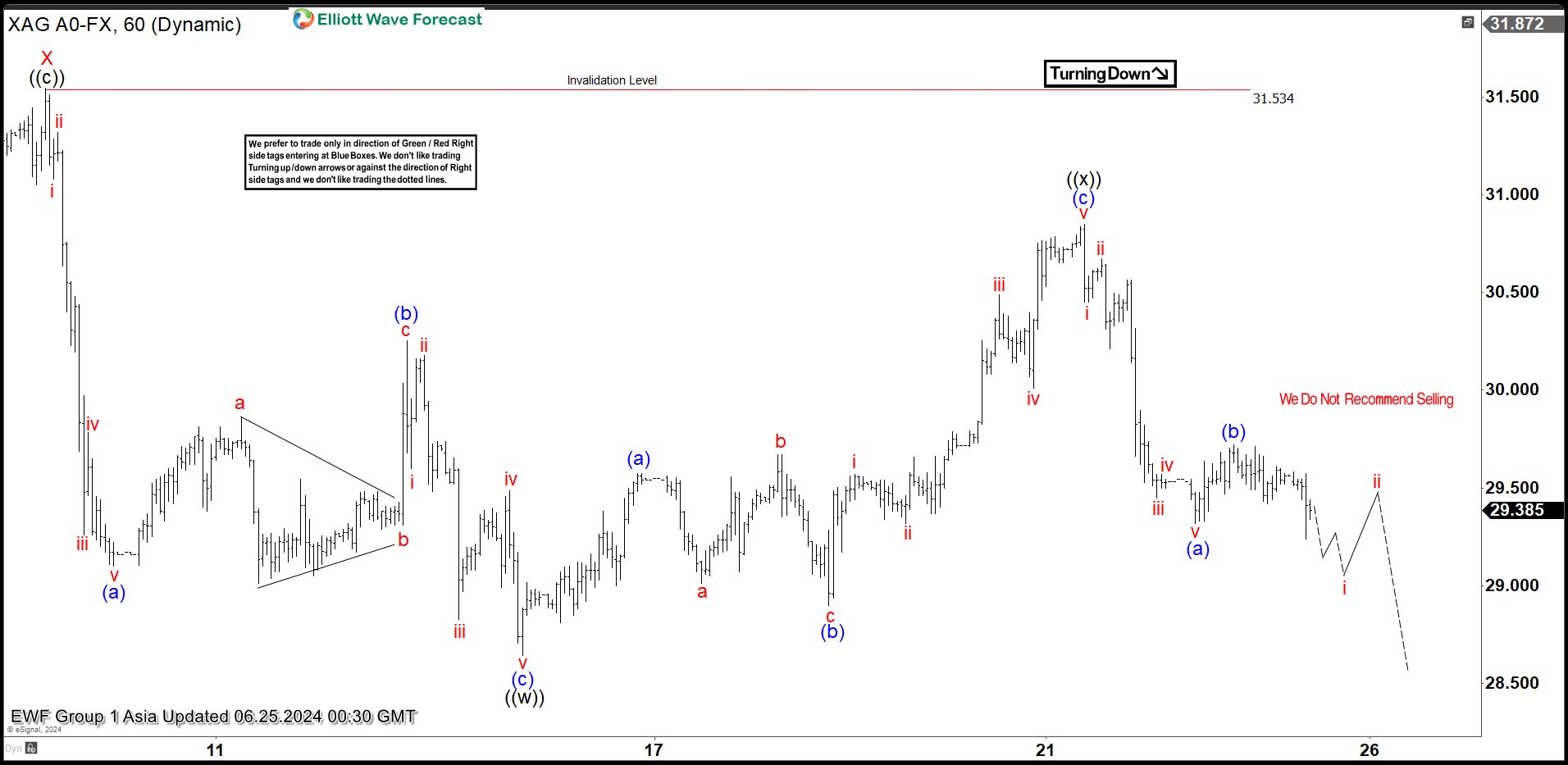

Elliott Wave Analysis on Silver (XAGUSD) Expects Further Correction Lower

Short Term Elliott Wave in XAGUSD (Silver) suggests cycle from 5.20.2024 high remains in progress as a double three structure. Down from 5.20.2024 high, wave ((a)) ended at 30.03 and wave ((b)) rally ended at 32.29. Wave ((c)) lower ended at 29.36 which completed wave W. Rally in wave X has ended at 31.53 as the 1 hour chart below shows. Wave Y lower is now in progress as another double three in lower degree.

Down from wave X, wave (a) ended at 29.1 and rally in wave (b) ended at 30.25. Wave (c) lower ended at 28.64 which completed wave ((w)) in higher degree. Rally in wave ((x)) unfolded as a zigzag structure. Up from wave ((w)), wave (a) ended at 29.57 and pullback in wave (b) ended at 28.90. Wave (c) higher ended at 30.84 which completed wave ((x)) in higher degree. The metal has turned lower in wave ((y)). Down from wave ((x)), wave (a) ended at 29.32 and rally in wave (b) ended at 29.72. The metal has extended lower in wave (c). Near term, as far as pivot at 31.53 high stays intact, expect rally to fail in 3, 7, 11 swing for further downside.

XAGUSD 60 Minutes Elliott Wave Chart

Silver (XAGUSD) Elliott Wave Video

https://www.youtube.com/watch?v=HclRLq-spKY