Sample Category Title

Summary 6/24 – 6/28

Monday, Jun 24, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 155M | 91M |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 08:00 | EUR | Germany IFO Business Climate Jun | 89.7 | 89.3 |

| 08:00 | EUR | Germany IFO Current Assessment Jun | 88.4 | 88.3 |

| 08:00 | EUR | Germany IFO Expectations Jun | 91.0 | 90.4 |

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | |

| Forecast: 155M | Previous: 91M | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 08:00 | EUR | Germany IFO Business Climate Jun | |

| Forecast: 89.7 | Previous: 89.3 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jun | |

| Forecast: 88.4 | Previous: 88.3 | ||

| 08:00 | EUR | Germany IFO Expectations Jun | |

| Forecast: 91.0 | Previous: 90.4 | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y May | |

| Forecast: | Previous: 2.80% | ||

Tuesday, Jun 25, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jun | -0.30% | |

| 12:30 | CAD | CPI M/M May | 0.30% | 0.50% |

| 12:30 | CAD | CPI Y/Y May | 2.70% | |

| 12:30 | CAD | CPI Core M/M May | 0.20% | 0.20% |

| 12:30 | CAD | CPI Media Y/Y May | 2.60% | 2.60% |

| 12:30 | CAD | CPI Trimmed Y/Y May | 2.80% | 2.90% |

| 12:30 | CAD | CPI Common Y/Y May | 2.60% | 2.60% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | 7.00% | 7.40% |

| 13:00 | USD | Housing Price Index M/M Apr | 0.50% | 0.10% |

| 14:00 | USD | Consumer Confidence Jun | 100.2 | 102 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jun | |

| Forecast: | Previous: -0.30% | ||

| 12:30 | CAD | CPI M/M May | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 12:30 | CAD | CPI Y/Y May | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | CAD | CPI Core M/M May | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | CAD | CPI Media Y/Y May | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 12:30 | CAD | CPI Trimmed Y/Y May | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y May | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | |

| Forecast: 7.00% | Previous: 7.40% | ||

| 13:00 | USD | Housing Price Index M/M Apr | |

| Forecast: 0.50% | Previous: 0.10% | ||

| 14:00 | USD | Consumer Confidence Jun | |

| Forecast: 100.2 | Previous: 102 | ||

Wednesday, Jun 26, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M May | 0.00% | |

| 01:30 | AUD | Monthly CPI Y/Y May | 3.50% | 3.60% |

| 06:00 | EUR | Germany GfK Consumer Confidence Jul | -20 | -20.9 |

| 08:00 | CHF | UBS Economic Expectations Jun | 18.2 | |

| 14:00 | USD | New Home Sales M/M May | 650K | 634K |

| 14:30 | USD | Inventories | -2.5M | |

| 23:50 | JPY | Retail Trade Y/Y May | 2.00% | 2.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M May | |

| Forecast: | Previous: 0.00% | ||

| 01:30 | AUD | Monthly CPI Y/Y May | |

| Forecast: 3.50% | Previous: 3.60% | ||

| 06:00 | EUR | Germany GfK Consumer Confidence Jul | |

| Forecast: -20 | Previous: -20.9 | ||

| 08:00 | CHF | UBS Economic Expectations Jun | |

| Forecast: | Previous: 18.2 | ||

| 14:00 | USD | New Home Sales M/M May | |

| Forecast: 650K | Previous: 634K | ||

| 14:30 | USD | Inventories | |

| Forecast: | Previous: -2.5M | ||

| 23:50 | JPY | Retail Trade Y/Y May | |

| Forecast: 2.00% | Previous: 2.40% | ||

Thursday, Jun 27, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Jun | 4.10% | |

| 01:00 | NZD | ANZ Business Confidence Jun | 11.2 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 1.60% | 1.30% |

| 09:00 | EUR | Eurozone Economic Sentiment Jun | 96.3 | 96 |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | -9.9 | |

| 09:00 | EUR | Eurozone Services Sentiment Jun | 6.5 | |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -14 | -14 |

| 12:30 | USD | Initial Jobless Claims (Jun 21) | 230K | 238K |

| 12:30 | USD | Durable Goods Orders May | -0.10% | 0.60% |

| 12:30 | USD | Durable Goods Orders ex Transport May | 0.10% | 0.40% |

| 12:30 | USD | Goods Trade Balance (USD) May P | -96.0B | -99.4B |

| 12:30 | USD | Wholesale Inventories May P | 0.20% | 0.10% |

| 12:30 | USD | GDP Annualized Q1 F | 1.30% | 1.30% |

| 12:30 | USD | GDP Price Index Q1 F | 3.00% | 3.00% |

| 14:00 | USD | Pending Home Sales M/M May | -7.70% | |

| 14:30 | USD | Natural Gas Storage | 71B | |

| 23:30 | JPY | Tokyo CPI Y/Y Jun | 2.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | 2.00% | 1.90% |

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Jun | 2.20% | |

| 23:30 | JPY | Unemployment Rate May | 2.60% | 2.60% |

| 23:50 | JPY | Industrial Production M/M May P | 2.00% | -0.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Jun | |

| Forecast: | Previous: 4.10% | ||

| 01:00 | NZD | ANZ Business Confidence Jun | |

| Forecast: | Previous: 11.2 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | |

| Forecast: 1.60% | Previous: 1.30% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Jun | |

| Forecast: 96.3 | Previous: 96 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jun | |

| Forecast: | Previous: -9.9 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jun | |

| Forecast: | Previous: 6.5 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | |

| Forecast: -14 | Previous: -14 | ||

| 12:30 | USD | Initial Jobless Claims (Jun 21) | |

| Forecast: 230K | Previous: 238K | ||

| 12:30 | USD | Durable Goods Orders May | |

| Forecast: -0.10% | Previous: 0.60% | ||

| 12:30 | USD | Durable Goods Orders ex Transport May | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 12:30 | USD | Goods Trade Balance (USD) May P | |

| Forecast: -96.0B | Previous: -99.4B | ||

| 12:30 | USD | Wholesale Inventories May P | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 12:30 | USD | GDP Annualized Q1 F | |

| Forecast: 1.30% | Previous: 1.30% | ||

| 12:30 | USD | GDP Price Index Q1 F | |

| Forecast: 3.00% | Previous: 3.00% | ||

| 14:00 | USD | Pending Home Sales M/M May | |

| Forecast: | Previous: -7.70% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 71B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Jun | |

| Forecast: | Previous: 2.20% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Jun | |

| Forecast: 2.00% | Previous: 1.90% | ||

| 23:30 | JPY | Tokyo CPI ex Food & Energy Y/Y Jun | |

| Forecast: | Previous: 2.20% | ||

| 23:30 | JPY | Unemployment Rate May | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 23:50 | JPY | Industrial Production M/M May P | |

| Forecast: 2.00% | Previous: -0.90% | ||

Friday, Jun 28, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.50% |

| 05:00 | JPY | Housing Starts Y/Y May | -6.00% | 13.90% |

| 06:00 | EUR | Germany Import Price Index M/M May | 0.20% | 0.70% |

| 06:00 | GBP | GDP Q/Q Q1 F | 0.60% | 0.60% |

| 06:00 | GBP | Current Account (GBP) Q1 | -17.7B | -21.2B |

| 06:45 | EUR | France Consumer Spending M/M May | 0.20% | -0.80% |

| 07:00 | CHF | KOF Economic Barometer Jun | 100.5 | 100.3 |

| 07:55 | EUR | Germany Unemployment Change Jun | 15K | 25K |

| 07:55 | EUR | Germany Unemployment Rate Jun | 5.90% | 5.90% |

| 12:30 | CAD | GDP M/M Apr | 0.30% | 0.00% |

| 12:30 | USD | Personal Income M/M May | 0.40% | 0.30% |

| 12:30 | USD | Personal Spending M/M May | 0.30% | 0.20% |

| 12:30 | USD | PCE Price Index M/M May | 0.30% | |

| 12:30 | USD | PCE Price Index Y/Y May | 2.70% | |

| 12:30 | USD | Core PCE Price Index M/M May | 0.10% | 0.20% |

| 12:30 | USD | Core PCE Price Index Y/Y May | 2.80% | |

| 13:45 | USD | Chicago PMI Jun | 40 | 35.4 |

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | 65.6 | 65.6 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Private Sector Credit M/M May | |

| Forecast: 0.40% | Previous: 0.50% | ||

| 05:00 | JPY | Housing Starts Y/Y May | |

| Forecast: -6.00% | Previous: 13.90% | ||

| 06:00 | EUR | Germany Import Price Index M/M May | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 06:00 | GBP | GDP Q/Q Q1 F | |

| Forecast: 0.60% | Previous: 0.60% | ||

| 06:00 | GBP | Current Account (GBP) Q1 | |

| Forecast: -17.7B | Previous: -21.2B | ||

| 06:45 | EUR | France Consumer Spending M/M May | |

| Forecast: 0.20% | Previous: -0.80% | ||

| 07:00 | CHF | KOF Economic Barometer Jun | |

| Forecast: 100.5 | Previous: 100.3 | ||

| 07:55 | EUR | Germany Unemployment Change Jun | |

| Forecast: 15K | Previous: 25K | ||

| 07:55 | EUR | Germany Unemployment Rate Jun | |

| Forecast: 5.90% | Previous: 5.90% | ||

| 12:30 | CAD | GDP M/M Apr | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 12:30 | USD | Personal Income M/M May | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 12:30 | USD | Personal Spending M/M May | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 12:30 | USD | PCE Price Index M/M May | |

| Forecast: | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y May | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | USD | Core PCE Price Index M/M May | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y May | |

| Forecast: | Previous: 2.80% | ||

| 13:45 | USD | Chicago PMI Jun | |

| Forecast: 40 | Previous: 35.4 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun F | |

| Forecast: 65.6 | Previous: 65.6 | ||

S&P 500 & Nasdaq 100 Week Ahead: Is It Time for a Deeper Retracement as US Investors Shed Equity...

- Over the past two weeks, US investors have shed nearly $30 billion dollars of US equity funds (net selling) according to data from LSEG.

- A bullish week for the S&P 500 but the Nasdaq 100 looks less convincing.

- A pullback in Nvidia stock and the psychological 20000 barrier have halted the Nasdaq’s impressive early week rally.

- Technicals are delicately poised as we await the final GDP and PCE (the Fed’s preferred inflation gauge) data next week.

Fundamental Overview

A big week for US indices as both the S&P and Nasdaq 100 crossed key psychological levels in 5500 and 20000 respectively. The relatively brief time each index managed to sustain above these levels highlights the fact that acceptance above such barriers take time, The selloff came in part thanks to a drop off in Nvidia with the chip maker continuing its slide, posting losses of 1.4% in pre-market trade on Friday. The ongoing debate around Nvidia and whether or not the current valuations around the chip maker continues to rumble on.

Mixed data from the US continued in the early part of the week as a string of weak economic data and commentary from Federal Reserve policymakers that rates could remain higher for longer sent conflicting messages. Inflationary concerns remain in play despite producer price inflation numbers showing positive signs. Rising geopolitical tensions are seen as the major bump in the road which could prove detrimental to the fight against inflation.

Friday saw a further slide for US equities which was a slight surprise given the PMI data for manufacturing and services beat estimates. This disconnect between data and US stocks has been a growing trend for quite some time now and seems set to continue.

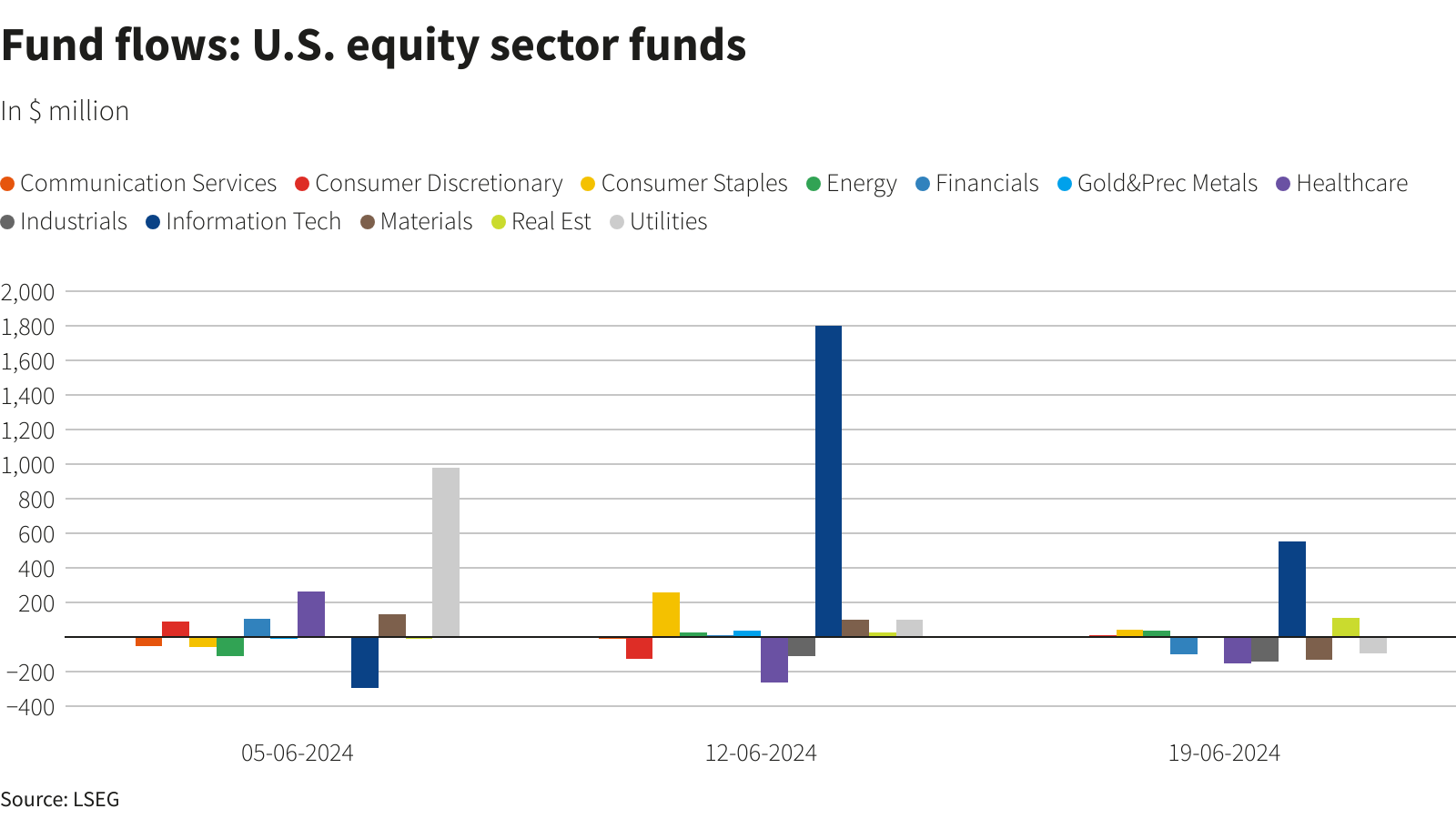

There are signs however that point to the possibility of a deeper correction and could be behind the slump in US Indices as the week progressed. US investors shed equity funds for a second successive week in the seven days ending June 19. This means over the past two weeks, US investors have shed nearly $30 billion dollars of US equity funds (net selling) according to data from LSEG. If you break it down by segment, US large cap and multi-cap funds led the outflows with the healthcare and industrial sectors leading the way. Surprisingly and despite valuation concerns the tech sector experienced a second week of inflows, attracting around $554 million (net).

Fund Flows: US Equity Sector Funds Through Jun 19, 2024

Source: LSEG Eikon (click to enlarge)

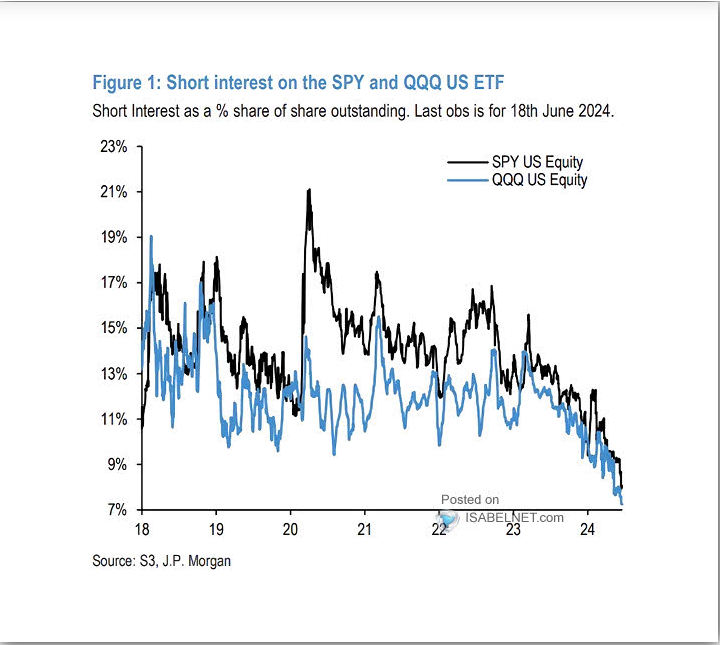

On the other end of the spectrum, short interest on SPY and QQQ US ETFS is low, showing little speculation on price declines. Low short interest indicates that relatively few investors are betting against the ETF. This suggests a general lack of pessimism about the future performance of the underlying indices (S&P 500 for SPY and Nasdaq-100 for QQQ). This could mean that the current pullback may be viewed as an opportunity by institutions to get in at better prices and capitalize on another bullish run to the upside. Looking at the two data points discussed above, they provide mixed signals in a similar vein to US economic data. Definitely a lot to consider for market participants moving forward.

S&P 500 – Short Interest on the SPY and QQQ US ETFs

Source: S3, JP Morgan, Isabelnet (click to enlarge)

The Week Ahead: US GDP AND PCE Data

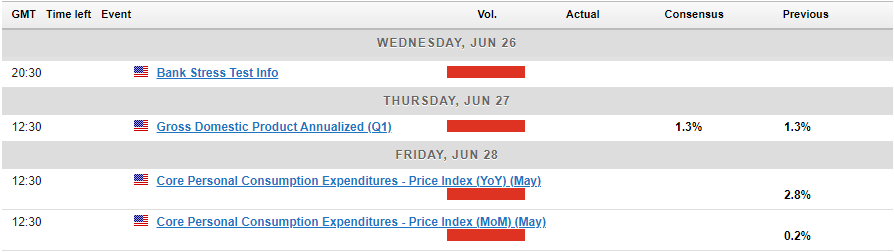

Looking ahead to next week, market participants will monitor the Fed’s preferred inflation gauge, the PCE index due for release on Friday June 28, 2024. The data will likely add another layer to what is an already complex equation as the Fed grapples with the home stretch on the inflation front.

Other key events from the US include CB consumer confidence data, Bank stress test results, durable goods orders and more comments from Federal Reserve policymakers. It will be an intriguing week as both the S&P and Nasdaq are hovering around key levels of support.

S&P 500 and NASDAQ 100 Technical Outlook

S&P 500

Looking at the S&P from a technical perspective, and the weekly chart did show a rejection of the psychological 5500 mark. Thursdays daily candle closing as an imperfect shooting star but is struggling to achieve follow through on Friday (at the time of writing). The RSI on a daily timeframe is also threatening to cross back below the 70 handle from overbought territory which is usually a sign that momentum may be shifting.

Looking at the H4 chart below and the S&P has been trading in a channel since the end of May. On Friday price threatened to break down below this channel which could open up a deeper selloff toward support at 5420. Any push below that and the 100-day MA comes into focus currently resting at 5374 with the 200 day MA the next area of interest at 5321.

S&P 500 Four-Hour Chart, June 21, 2024

Source: TradingView.com (click to enlarge)

NASDAQ 100

Looking at the Nasdaq 100 weekly chart and the rejection of the 20000 has left the weekly candle battling to close in the green. A bearish close will require the Nasdaq to close below the 19670 mark, and should it happen will no doubt stoke the interest of potential shorts. The daily is almost a mirror image of the S&P chart as a key support level may keep a bearish weekly close at bay.

The H$ chart below shows price testing the support handle around the 19650 mark with a break below opening up a retest of support at 19500. Beyond that we have support provided by the 100-day MA at 19253 and then the psychological 19000 level which coincides with the 200-day MA.

Alternatively a push higher from here needs to navigate the 20000 psychological barrier and post a daily close above. this would be the first sign of acceptance by market participants before resistance at 20500 comes into play.

NASDAQ 100 Four-Hour Chart, June 21, 2024

Source: TradingView.com (click to enlarge)

The Weekly Bottom Line: A Grand Slam of Economic Data

U.S. Highlights

- U.S. retail sales grew marginally in May, however the downward revision in April points to waning momentum among U.S. consumers.

- Housing starts and building permits both declined in May as higher interest rates weigh on builder confidence.

- U.S. existing home sales dipped for a third consecutive month as record home prices stretch buyers’ affordability limit.

Canadian Highlights

- The housing market showed mixed signals in May, with an increase in housing starts and contraction in home sales. The overall trend suggests the housing market will weigh on economic activity in the short term.

- Consumer spending also appears tepid, with a strong retail sales print in April overshadowed by weak performance in the prior two months, and an anticipated decline in May.

- The Summary of the Bank of Canada’s Governing Council deliberations showed that policymakers contemplated waiting until July to cut rates. The Bank will remain cautious, focusing on both inflation risks and economic performance, rather than foreign exchange divergence, when making the next move.

U.S. – Housing Market Strains Under the Weight of Higher Rates and Prices

Data out this week was largely tilted to the housing market, providing an update on where things stand in the usually busy spring season. Thus far, the situation appears largely unimpressive as market activity continues to be impacted by the dowsing effect of higher interest rates and prices. Another look at the health of the U.S. consumer via the retail spending report was also in the lineup. Despite news on the economic front, activity is the stock market was largely driven by the ups and downs of Nvidia, which managed to dethrone Microsoft this week as the most valuable public company in the world. Bond prices also continued to rise, driving yields lower. At the time of writing, the 10-year Treasury yield was down 0.5 basis points relative to where they started the week.

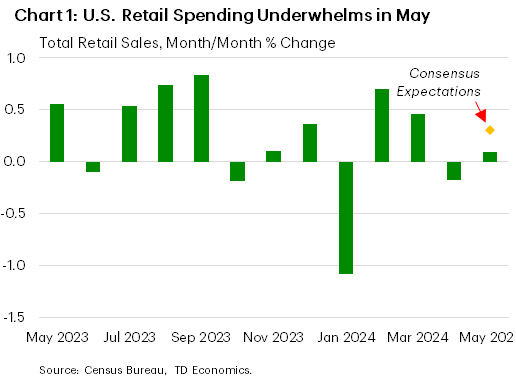

Consumer spending continued to show signs of fading as retail sales barely grew in May (0.1% m/m), following a decline of -0.2% in April. The outturn was weaker than analysts expected (Chart 1). Overall, weak retail sales are consistent with a U.S. economy that is losing momentum. The main takeaway is that consumers may finally be starting to yield to the pressures of elevated prices and higher borrowing costs.

Nonetheless, most Fed speakers throughout the week were key to emphasize that there is still more ground to be gained on the inflation front with the current restrictive policy before normalization becomes appropriate. In a recent interview, Fed Governor Barkin suggested that consumer spending is “fine” despite the weak retail sales print. In his view, “consumer spending is solid, not frothy and not weak” and the Fed is well positioned to respond to any path the economy may take. Other speakers, including New York Fed President John Williams and Boston Fed President Susan Collins, stressed the Fed’s data dependent approach. Williams noted that he expects “interest rates to come down gradually over the next couple of years” but declined to give specific timing, while Collins stressed the need for patience and time to assess the “constellation of available data.”

On the housing front, homebuilding activity retreated last month with a decline in both housing starts and building permits. A consistent pullback in permitting activity over the past few months, has resulted in a decline in the number of units under construction. Evidently, elevated interest rates are weighing not only on buyers, who have pulled back on new home purchases resulting in higher inventory, but also on builders as it increases the cost of construction financing.

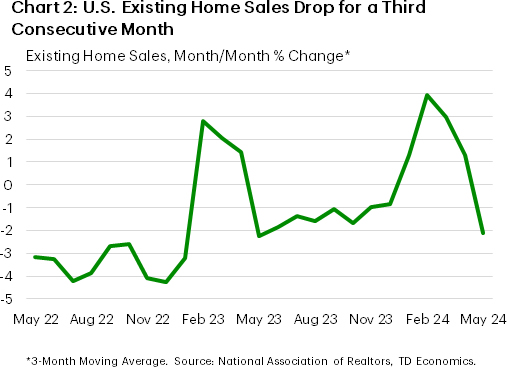

Despite a decline in the average 30-year fixed mortgage rate from a recent peak of 7.22% in early May to 6.87% this week, the housing market remains under pressure. Existing home sales slipped again for the third month in a row as home prices hit a record high (Chart 2). Buyers continue to be weighed down by high prices and rates, with little prospect of relief in the near term as the Fed continues to exercise patience with respect to rate cuts.

Looking ahead, the central bank’s preferred inflation gauge is out next week. Fed governors and market participants alike will be eager to see how much of the recent easing in the Consumer Price Index will flow through to the Personal Consumption Expenditure measure. Perhaps the Fed will find more of that “consistent data” they require to support a less restrictive policy stance.

Canada – A Grand Slam of Economic Data

Just as sports enthusiasts reveled in the array of top-tier events like the Euro Cup, Stanley Cup playoffs, and Copa America, economic news aficionados had a wealth of data to absorb this week. The economic arena was further energized by updates from forecasters, including yours truly – TD Economics - releasing our own view on the outlook for national and provincial economic growth.

The week kicked off with updates on the state of the housing market. Housing starts surprised to the upside, posting a robust 10% month-on-month increase. This performance boosted the three-month average, though it fell short of reaching the explosive growth seen during the pandemic-induced ‘race for space’.

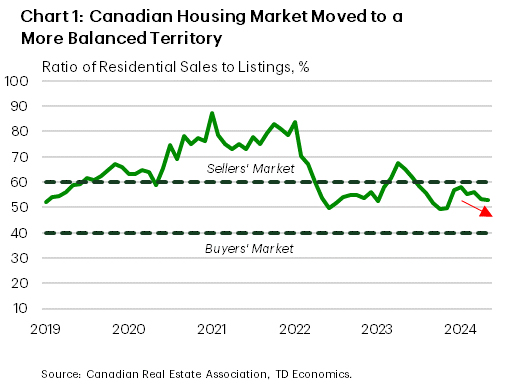

Conversely, the spring home selling season failed to gain momentum in May, with residential home sales posting another monthly decline. This was not entirely unexpected, as many potential buyers remained cautious, awaiting signals from the Bank of Canada. Luckily, both short- and long-term interest rates moved lower after the BoC cut rates on June 5th. This will help make home borrowing more affordable. An increase to new listings also contributed to improved affordability. This combined with lower sales activity, the sales-to-listings ratio pushed further into balanced territory (Chart 1). With that, the benchmark home price index declined by 0.2% month-on-month, primarily due to weakness in the condo market. Despite these adjustments, the softer sales trend is expected to persist, leading to an anticipated 3% contraction in the second quarter. We forecast that housing will weigh on economic activity in the short term, with a rebound expected in the latter half of the year as interest rate uncertainty subsides.

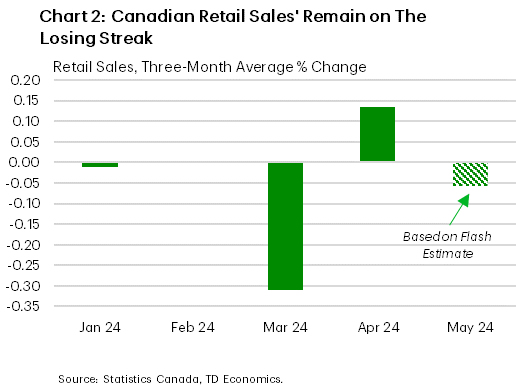

Similarly, the consumer is not likely to be pulling the freight. The strong retail sales print for April is preceded by two months of weakness and is expected to be followed by a weak print in May (Chart 2). This hardly signals strength. Notably, auto sales declined sharply, erasing the marginal gains of the previous two months. Recent industry data points to sluggish demand in auto sales in May as consumers grapple with high borrowing cost and prices roughly 20% higher than three years ago. This weakness offsets some of the strength observed in services spending, weighing on our projections for personal consumer spending of 0.7% quarter-on-quarter annualized (down from 3.0% in the first quarter).

As a result, this week’s data doesn’t provide a strong case for a more hawkish stance from the BoC. The Summary of the Governing Council’s deliberations showed that members considered waiting until July to cut the policy rate, as they placed similar weight on the downside risks to inflation stemming from weaker consumer spending and on the upside risks associated with persistence in wage growth and the potential for a housing market rebound. Ultimately, the Council decided that there was sufficient progress on inflation to cut in June, but this doesn’t guarantee a cut in July. Policymakers also discussed market expectations for policy divergence between Canada and the U.S.. They agreed that while there are limits to how far policy can diverge, the limits are not close to being reached. Therefore, the domestic economic performance will remain the major driver of the BoC’s decisions this year.

Weekly Economic & Financial Commentary: Global Central Bank Decisions Galore

Summary

United States: Economic Data More Rice & Beans than Steak & Eggs

- Markets chewed on an array of economic data this week, and what was served was mostly gristle. A weak retail sales print suggests that consumers may finally be feeling some spending fatigue. Markets also received a three-course housing market update which painted the picture of a sector that remains rocked by higher interest rates. Much of the week's disappointing data were concentrated in interest-rate sensitive sectors, and the wider economy remains healthy on balance even as softening becomes increasingly evident.

- Next week: New Home Sales (Wed.), Durable Goods Orders (Thu.), Personal Income & Spending (Fri.)

International: Global Central Bank Decisions Galore

- It was a busy week for global central banks. The Reserve Bank of Australia (RBA) held its policy rate at 4.35% and offered hawkish commentary; we have pushed out our forecast for an initial RBA rate cut to February 2025. The Bank of England held rates steady and communicated a more dovish-leaning tone, affirming our outlook for an August rate cut. The Swiss National Bank cut its policy rate by 25 bps, Norway's central bank delivered a hawkish hold, while in emerging markets the Chilean Central Bank opted for a 25 bps rate cut while Brazil's central bank held steady.

- Next week: Canada Inflation (Tue.), Riksbank Policy Rate (Thu.), Banxico Policy Rate (Thu.)

Credit Market Insights: Households Feeling Greater Squeeze

- Earlier this month, the New York Fed released May data for its Survey of Consumer Expectations (SCE). While perceptions of financial well-being improved, gauges of credit standards and availability saw no improvement over the month.

Topic of the Week: CBO Budget Projections Reaffirm Challenged Fiscal Outlook

- The Congressional Budget Office released an update to its 10-year budget projections this week, reaffirming an already challenged fiscal outlook. CBO boosted its fiscal year 2024 U.S. budget deficit estimate to $1.9 trillion, up from $1.5 trillion in previous projections from February.

May Data to Show Canadian Inflation on Downward Trajectory

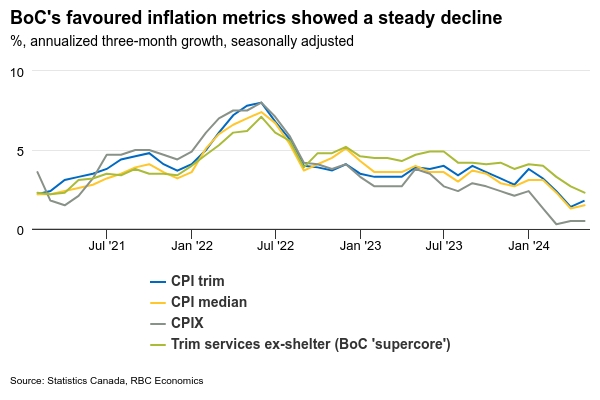

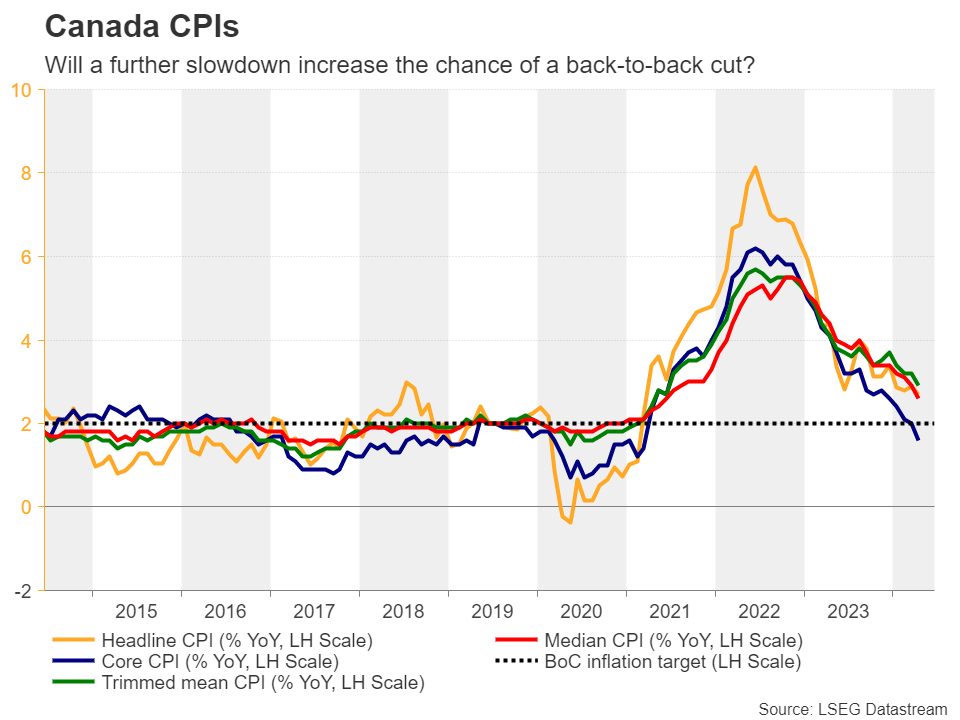

We expect Canadian inflation numbers on Tuesday will show further signs of gradual easing in price pressures. Consumer price index growth should edge down to 2.6% year-over-year from 2.7% in April. That would mark the fifth consecutive month that annual price growth is within the Bank of Canada’s 1% to 3% inflation target range.

Gasoline prices eased in May alongside lower global oil prices, and food price growth likely continued to move lower. But, the BoC will be focused on their preferred core measures for evidence that a broadly based slowdown in price growth in 2024 is continuing. The closely watched three-month rolling averages for the CPI-trim and CPI-median measures will likely tick higher but remain relatively low after unusually soft readings left both under the 2% inflation target over the last two months. The breadth of inflation pressures has continued to ease with the share of consumer products seeing inflation above a 3% annual rate back close to its historical rate in April.

A softening economic growth backdrop has made it more likely that Canadian inflation pressures will not reaccelerate the way they did in the United States earlier this year. We expect a 0.3% increase in next Friday’s April gross domestic product numbers—consistent with the preliminary Statistics Canada estimate. But two-thirds of that gain is expected to come from a rise in oil production and drilling activity ahead of the TMX pipeline expansion starting service this spring. Manufacturing output was likely little changed with a small increase in sale volumes (0.4%) pulled from inventories rather than new production. April retail sale volumes edged up 0.5% but preliminary estimates from Statistics Canada pointed to lower sales in May, consistent with signs of softening in our own tracking of card transactions. We expect May GDP growth to look softer. That would leave GDP for Q2 as a whole tracking close to our 1.4% annualized forecast, marking another decline in per-capita output.

Week ahead data watch

SEPH employment data for April will also be closely watched for further signs of softening in the labour market. Job openings (not counted in the timelier Labour Force Survey data) are expected to continue to drift lower as labour demand slows.

We expect U.S. personal consumption to edge higher from 0.2% to 0.3% in May, given retail sales were up 0.1% in May. Personal income likely drifted higher by 0.3% due to a slight rebound in wage growth (0.4%).

Week Ahead – US PCE Inflation the Highlight of a Relatively Light Agenda

- Core PCE inflation to test bets of two Fed rate cuts in 2024

- Yen awaits BoJ Summary of Opinions, Tokyo CPI

- Canadian CPI data also enters the spotlight

Will PCE data confirm Fed rate cut bets?

Although the Fed’s updated dot plot pointed to only one quarter-point reduction by the end of the year, the softer-than-expected CPI numbers a few hours ahead of last week’s decision did not convince market participants about officials’ intentions. The weaker-than-expected retail sales numbers this week corroborated that view.

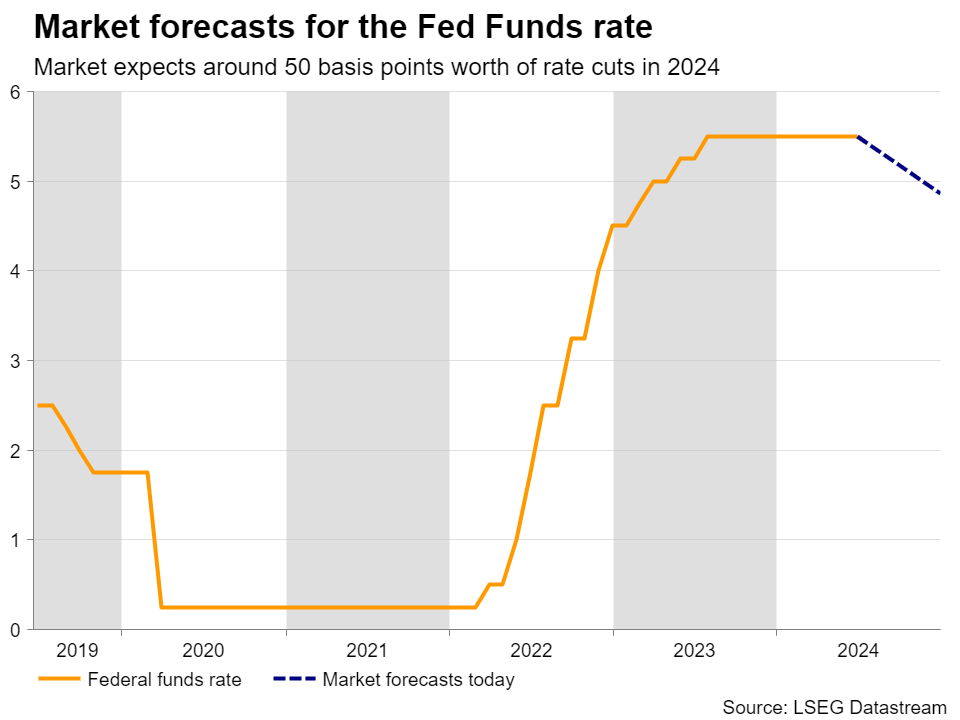

Indeed, according to Fed funds futures, investors are penciling in around 50bps worth of reductions by the end of the year, assigning around a 70% probability for the first cut to be delivered in September.

With all that in mind, the main item on dollar traders’ agenda next week may be the core PCE price index for May due out on Friday, which is accompanied by the personal income and spending data for the same month. The final GDP print for Q1 is also set to be released the day before, but given that Q2 is almost over, any minor deviations from the 2nd estimate are likely to pass unnoticed.

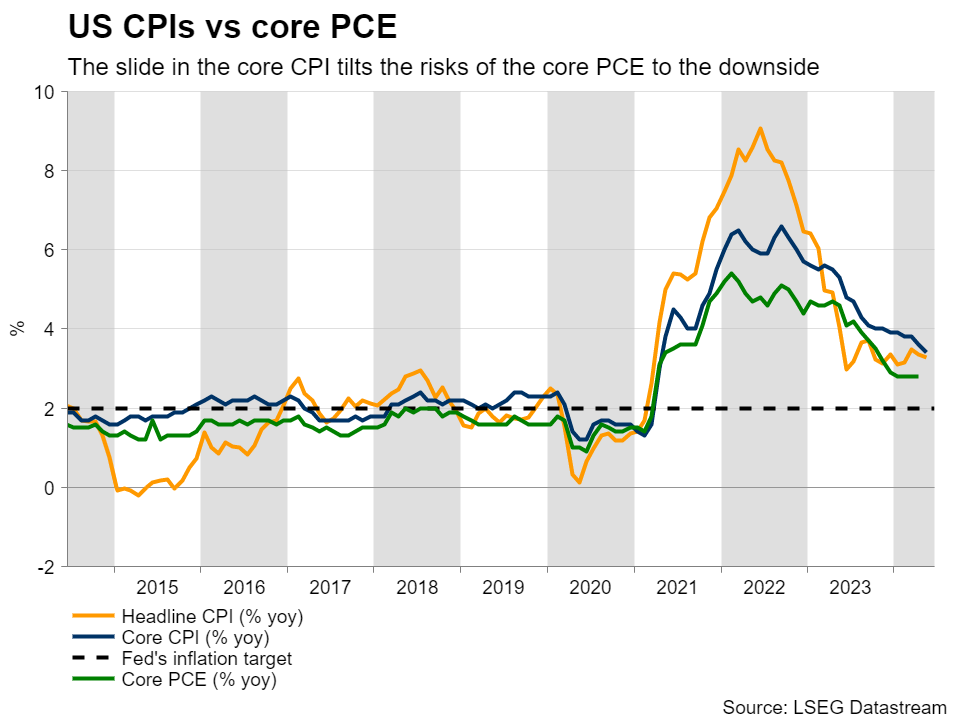

As for the core PCE index, the slide in the core CPI for the month poses some downside risks. There may be downside risks to spending as well, derived by the weakness in retail sales, although income may be poised to improve, something suggested by the better-than-expected average hourly earnings.

Overall, another set of economic data pointing to cooling consumer demand may further solidify expectations of two quarter-point cuts by the Fed, and perhaps increase the probability for initiating the process in September. This could prove negative for the US dollar, especially against its Australian counterpart. Remember that this week, the RBA maintained its neutral stance, while Governor Bullock revealed that they discussed the option of raising rates.

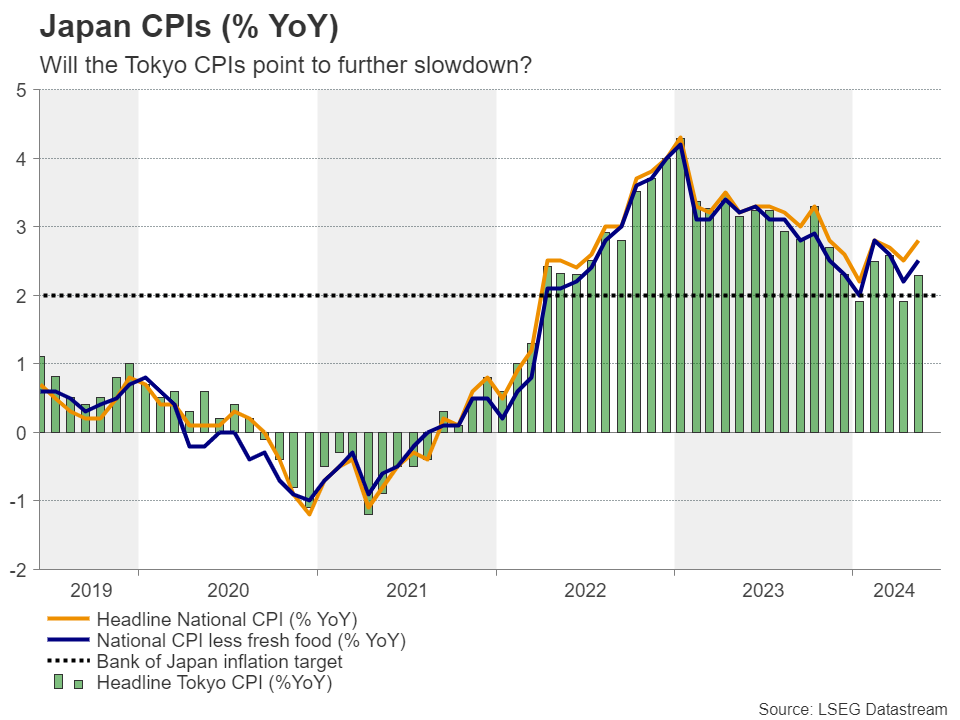

How likely is a July hike by the BoJ?

In Japan, the Summary of Opinions from last week’s BoJ decision will be released on Monday during the Asian session, while on Friday, the Tokyo CPIs for June are coming out.

At last week’s meeting, BoJ officials decided to keep interest rates unchanged and said that they would start trimming their bond purchases, but that they will announce a detailed plan next month. What’s more, Governor Ueda said that he is not ruling out interest rates rising in July.

Still, the yen fell, perhaps as some market participants were expecting more concrete signals about a July hike and a potential slowdown in bond purchases. This is also evident by market pricing, where the probability of a 10bps hike in July has dropped significantly, to around 27%. Ahead of the decision that chance was more than 65%.

All this suggests that yen traders will dig into the summary for clearer hints on how likely a July hike is. If they are left once again disappointed, the yen is likely to extend its slide and perhaps take another hit if the Tokyo CPIs pull back below the Bank’s 2% objective again. Having said all that though, with dollar/yen already trading near the 159.00 zone, further advances, closer to the round number of 160.00, may significantly increase the risk for another intervention episode by Japanese authorities, although officials have been silent until now.

Back-to-back rate cuts for the BoC?

Canada’s CPI numbers are also on next week’s agenda. They are due out on Tuesday. Earlier this month, the BoC became the second central bank in the G10 group to cut interest rates by 25bps, with Governor Macklem signaling that it would be “reasonable to expect further cuts” if inflation continues to cool.

Since then, the only data set worth mentioning was the employment report for May, which came in slightly better than expected. And that was not enough to deter investors from expecting another rate reduction in July. The probability of such a move currently rests at around 62% and should next week’s data reveal that inflation continued its downward trajectory, it could go higher. This could weigh on the Canadian dollar.

Australia releases its monthly CPI prints for May. Inflation in Australia has been proving stickier than other major economies, with RBA policymakers discussing the possibility of hiking rates at Tuesday’s gathering. Ergo, if the CPI confirms the stickiness in price pressures, traders will continue seeing the RBA as more hawkish than other major central banks, something that may keep the aussie supported.

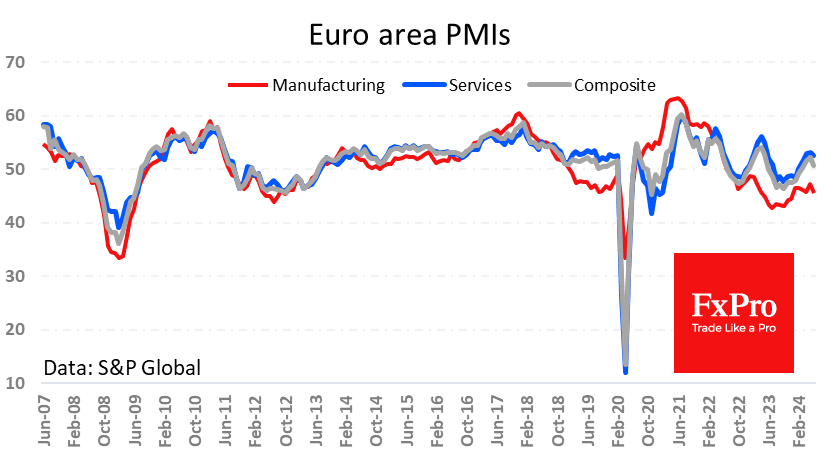

Weekly Focus – PMIs Question the Strength of Euro Area Recovery

In a fairly quiet week equities edged modestly higher, and a barrel of crude oil traded back above USD 85. Along a hawkish Norges Bank twist this supported NOK while more pricy oil weighs on JPY which continues to weaken. Japan's top currency diplomat stressed that there is no limit to FX intervention resources. We are probably just a small JPY sell-off away from the government stepping back in to prop up the JPY.

In bond markets, we have seen some intra-euro area spread tightening after the knee-jerk reaction last week when French president Macron called a snap election. On Friday, the French-German yield spread was still about 25bp wider than ahead of the EU parliament election, though. The EU Commission put France and Italy, among others, into Excessive Deficit Procedures, a disciplinary tool, which has, until now, been suspended since the pandemic. The respective governments will now need to come up with proposals on how to improve public finances.

We had several central bank meetings on the agenda this week. While Norges Bank adjusted their rate path higher on inflation worries, the SNB opted for another rate cut after they kicked off the global cutting cycle back in March. This leaves the policy rate at 1.25% and reflects the significant CHF strengthening through the recent month. With UK core inflation at 3.5% in May and particularly service prices continuing to move too fast, it was no surprise that the Bank of England kept the bank rate unchanged at 5.25%.

Euro area PMIs released Friday were weaker than expected, which drove 10-year Bund yields 5bp lower and weakened the euro a bit. The service sector recovery slowed, and the manufacturing recession accelerated after we had seen positive signs on that front for a while. Also worth noting, the index for output prices in the service sector took another leg lower. It has been a good indicator for core price pressures in the euro area. The German ZEW survey continues to signal a dire assessment of the current economic situation, whereas expectations are much more promising.

Also, Japanese PMIs were weak as the service sector cooled significantly. At the same time core inflation ticked back below 2% as price pressures remain very muted. This is not what the Bank of Japan wants to see before embarking on further rate hikes. Elsewhere in Asia, Chinese May data paint a picture of a still fragile economy with the housing crisis remaining a key drag on demand. After a strong start to the year, production seems to have lost some momentum.

Next week, we will zoom in not least on France as they release some of the first euro area inflation data for June on Friday along Spain and Italy. The first round of the French National Assembly elections kicks off the following Sunday. The most likely scenario is a "hung parliament", which would imply that the worst fears in markets of large spending increases should diminish. We will probably have to wait until the second round the following Sunday for the final results, though.

Sunset Market Commentary

Markets

PMI business confidence was on tap at the close of the week. The European June edition comes with an important disclaimer though. PMI owner S&P Global noted that the turmoil in the wake of the European elections and the French snap elections has likely stirred up a lot of uncertainty and that France’s poor outcome (unexpected decline to 48.2 on a composite level) “has significantly contributed to the deteriorating economic conditions in the Eurozone.” Indeed, economic activity unexpectedly eased on an aggregate level from 52.2 to 50.2. S&P Global estimates Q2 GDP growth at 0.2% q/q. Both services (52.6 from 53.2) and manufacturing (45.6 from 47.3) printed declines. A renewed fall in new orders was responsible, decreasing (slightly) for the first time in four months on sharply dropping manufacturing export orders. Aggregate net employment rose at the slowest pace since March as staffing levels were raised solidly in the services, while a similarly-sized fall was recorded in manufacturing. The combination of decreasing new orders but marginally rising employment resulted in a reduction of backlogs. Input prices, while easing for a second month, still rose at a pace slightly faster than the pre-pandemic average. The decline was driven by services (38-month low) but with manufacturing posting a renewed increase in their cost burdens for the first time in 16 months. Output price inflation equally eased again with an interesting divide as services inflation was the lowest in three years but manufacturers lowered prices at the slowest pace in 14 months. Confidence for the future waned, but more than anything of the above, should be taken with a pinch of salt given the timing of the survey (amidst European political turmoil). German rates nevertheless drop several bps with the front-end of the curve outperforming (-6.2 bps). The 10-yr eases 5.5 bps with support at 2.34% never really having been in danger. European stocks grind lower. The likes of the EuroStoxx50 loses >1%, capping this week’s recovery from the sell-off the week before to just a little over 1%. The euro neared the post-election low of 1.0668 before paring gains to 1.0692. Rates in the US ease between 3.7-4.6 bps ahead the US PMIs. Wall Street opened slightly lower.

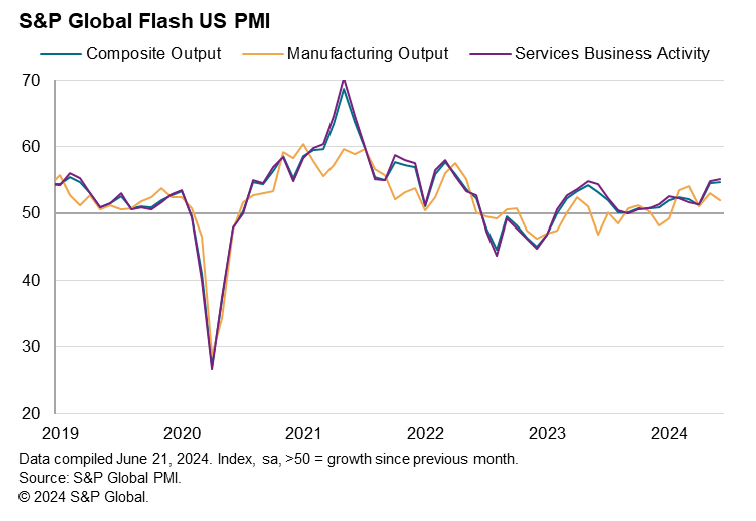

Contrasting with Japan, UK and the Euro area, US PMIs came in to the stronger side of expectations, catching markets probably a bit off guard. The composite reading unexpectedly grinded higher from 54.5 to 54.6 with both services (55.1) and manufacturing (51.7) suggesting a nice economic expansion overall. US yields cut back losses to less than 2 bps in a first reaction.

News & Views

UK PMIs showed business activity in the country in June expanding at its slowed pace since November. The composite output index declined to 51.7 from 53.0 in May. Contrary to the EMU, a slowing pace in the services sector growth (activity index 51.2 from 52.9) offset a stronger performance in manufacturing (51.4 from 51.2). Output growth at goods producers even reached the strongest growth in 26 months (54.2), driven by improved order book intakes and strong business confidence. On the easing in services activity, S&P said that survey evidence indicated the slowdown was partly driven by a pause in spending decisions during the election period. Despite a mixed picture for activity, S&P UK firms are facing a quickening of input cost inflation as severe global shipping constraints led to higher transport costs. This resulted in quicker increases in output charges among both manufacturing and services companies, with producers notably raising their prices at the sharpest rate since May 2023. The combination of slower growth but at the same time signs of a new uptick in inflation only complicate the decision making of BoE members who are considering move toward an early rate cut.

Average gross earnings in the country in April were 13.5% higher than in the same period last year, data from the Hungarian Statistical Office showed today. Real earnings were 9.5% higher than in the same month last year. High real wage growth fueling domestic demand is an important factor in the decision making process of the Hungarian Central Bank (MNB) as it expects both headline and core inflation to return higher in the second half of the year. In this respect, the MNB this week slowed the pace of rate cuts to 25 bps (base rate 7.0%) and will shift to a guarded month-on-month approach going forward. The forint at EUR/HUF 397 is holding within reach of the weakest YTD levels.

Graphs

Germany’s 10-yr yield: support at 2.34% never really in danger despite weaker-than-expected PMIs

EuroStoxx50: this week’s recovery after the sell-off in the one before is all but disappointing

DXY: trade-weighted dollar looks set for a return towards the YtD high at 106.517

US 2-yr yield stabilizes around recent lows with strong PMIs capping daily losses

US PMI composite ticks up to 54.6, robust growth and cooling inflation

US PMI Manufacturing rose from 51.3 to 51.7 in June. PMI Services jumped from 54.8 to 55.1, a 26-month high. PMI Composite also ticked up from 54.5 to 54.6, a 26-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The early PMI data signal the fastest economic expansion for over two years in June, hinting at an encouragingly robust end to the second quarter while at the same time inflation pressures have cooled.

"The PMI is running at a level broadly consistent with the economy growing at an annualized rate of just under 2.5%. The upturn is broad-based, as rising demand continues to filter through the economy. Although led by the service sector, reflecting strong domestic spending, the expansion is being supported by an ongoing recovery in manufacturing, which so far this year is enjoying its best growth spell for two years.

"The survey also brings welcome news in terms of job gains, with a renewed appetite to hire being driven by improved business optimism about the outlook.

"Selling price inflation has meanwhile cooled again after ticking higher in May, down to one of the lowest levels seen over the past four years. Historical comparisons indicate that the latest decline brings the survey's price gauge into line with the Fed's 2% inflation target."

Downside PMI Surprise Brought the Euro Closer to the Critical Zone

The European session on Friday started with a new wave of euro selling, which was supported by weak preliminary PMIs.

According to June estimates, the strengthening of economic activity in the eurozone, which has been gaining momentum since October, is at risk of reversing. The composite index fell from 52.2 to 50.8, contrasting unpleasantly with the expected rise to 52.5. The services sector slipped for a second month, causing the index to fall from 53.2 to 52.6 instead of the expected rise to 53.5.

The jump in manufacturing activity last month also looks like a positive anomaly, as the index fell to 45.6 from 47.3 a month earlier, close to April’s reading of 45.6.

PMI values below 50 indicate a contraction in activity by last month, and the euro region’s industry has been below this waterline since July 2022. The services sector is more buoyant and only recorded a contraction between August 2023 and February 2024.

The downward trend reversal strengthens the case for monetary easing, and the ECB took the first step on this path earlier in June with a rate cut.

The Eurozone PMI has established itself as a reliable leading indicator of economic activity, and the latest data shows serious risks of a slowdown.

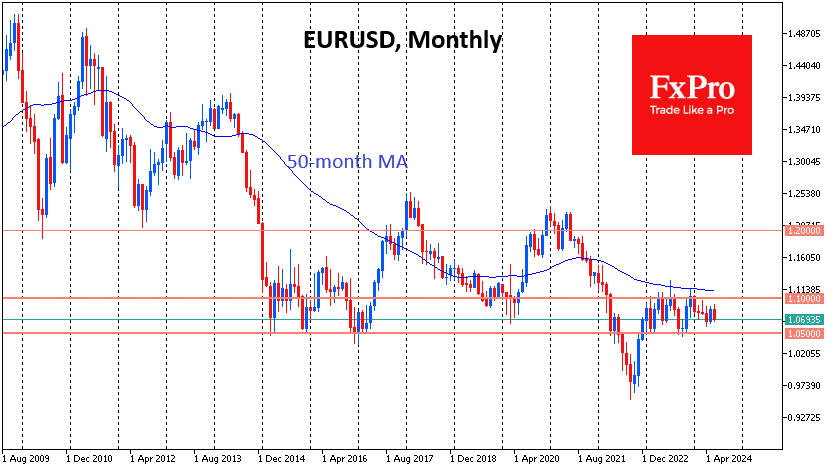

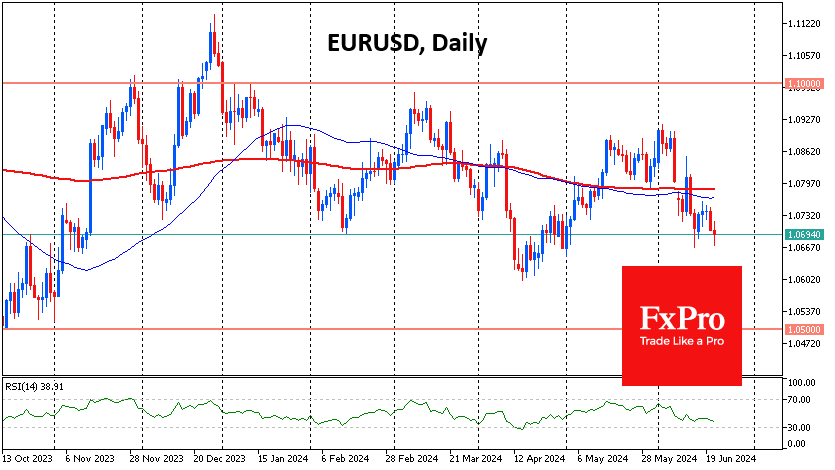

This is bad news for the European currency. EURUSD slipped below 1.0700, almost duplicating last Friday’s lows just below 1.0670.

If comparable data from the U.S. does not present similar unpleasant surprises, EURUSD may approach 1.06 without many obstacles, returning to the lows of April.

A pullback to 1.06 or even 1.05 would test the single currency’s support boundaries. A failure below would signal a fundamental change of attitude towards the euro, which would open the way below parity with a downside potential of 0.85.

This negative scenario is possible if Europe’s current economic cracks cannot be quickly mended by responding positively to monetary easing.

This is a possible scenario given the increased debt burden in the major economies, which reduces the effectiveness and space for stimulus. However, things could still unfold positively for Europe if we see a revival in the wake of the ECB’s key rate cut in June.