Sample Category Title

Focus Turns to June PMIs After Central Bank Bonanza

In focus today

After yesterday's hawkish surprise from Norges Bank, we revise our call for the first rate cut to come in March 2025 rather than September this year, see more below.

This morning at 8.00 CET we get UK retail sales for May and later in the day June PMIs where consensus is for status quo (comp. PMI consensus: +0.01).

In the euro area, we get the data highlight of the week with the June PMIs. The composite PMI has now been above 50 for three months in a row and we expect this to be the case also in June as the economy has gathered momentum. The service sector is holding up growth and we expect the services index to be broadly unchanged at a still strong level. We expect the recovery in the manufacturing sector to continue as most of the cyclical factors explaining the recent weakness have turned the corner. We will also follow the service sector price index closely to see if the recent declines continue in June as an indicator for inflation.

In the US, we expect the June flash PMIs to signal positive but still modest growth. May data showed an unexpected pick-up in business activity especially in the services sector, while price indicators remain close to pre-pandemic average levels.

Economic and market news

What happened overnight

Japanese May core CPI printed at 2.5% y/y, slightly lower than expected (cons.: 2.6%) while core CPI excl. energy declined to 2.1% y/y from previously 2.4%. Hence no new evidence for the BoJ that demand-driven price pressure is strong, which could cloud the outlook for monetary policy. The yen initially slid against the dollar but recovered losses during the session.

What happened yesterday

A hawkish surprise from Norges Bank, who shifted guidance on the most likely timing for the first rate cut from September this year to March next year. Markets expected a shift to December and reacted by flattening the forward rate curve and strengthening the NOK (EUR/NOK -0.7%) though still pricing in a roughly 50/50 chance of a December cut. We change our forecast to be in line with the path set by NB and now see the first cut in March 2025.

The SNB cut rates by 25bp to 1.25%. The cut today is likely due to the recent CHF strengthening as was also the focus of the press conference, where Chairman Jordan noted that the exchange rate is very important for monetary conditions. EUR/CHF tracked some 0.5% higher during the day. We stick to our call of an end-of-year rate at 1.00% with today's meeting not proving a gamechanger but highlighting the more frontloaded nature of the SNB.

Slightly dovish tilt from the BoE, who kept the bank rate unchanged at 5.25 as expected but comments from the "unchanged" voting camp downplaying the recent topside surprises in services inflation. EUR/GBP ticked slightly higher during the day and yields posted a modest decrease.

Market movements

Equities: Global equities were flat yesterday with notably mixed regional and sector performance. Europe emerged as the significant gainer, boosted by a catch-up in both France and Italy. Most sectors in Europe saw gains. The US, however, presented a more mixed picture. Tech stocks in a sizeable sell-off for a change, with the Dow outperforming the Nasdaq by 1.5%. Industrial value began to somewhat recover from its massive underperformance against tech growth recently. From a value and investment cycle perspective, this development makes a great deal of sense. However, it's too early to determine whether this signifies the beginning of a trend shift. In the US, the Dow rose by +0.8%, while the S&P 500 fell by -0.3%. The Nasdaq and Russell 2000 also dipped, with decreases of -0.8% and -0.4%, respectively. Asian markets are quite varied this morning, with South Korea and China standing out on the negative side. Meanwhile, futures in the US and Europe are trending higher.

FI: EGB rates rose marginally in yesterda'’s session with limited volatility throughout the day. 10Y Bund yields rose 3bp, while long-end yields for peripheral and OATs were close to unchanged. The Bund ASW-spread was close to unchanged at 36-37bp, while implied volatility continued to fade.

FX: CHF was the poorest performer in G10 during yesterday's session as the SNB delivered its second 25bp cut this year. While the BoE kept the Bank Rate unchanged as widely expected, a slight dovish tilt in communication provided headwind for GBP. Among the top performs was NOK, where Norges Bank delivered a hawkish surprise by postponing the signal for the timing of the first rate cut one additional quarter compared to market expectations (September 2024 to March 2025).

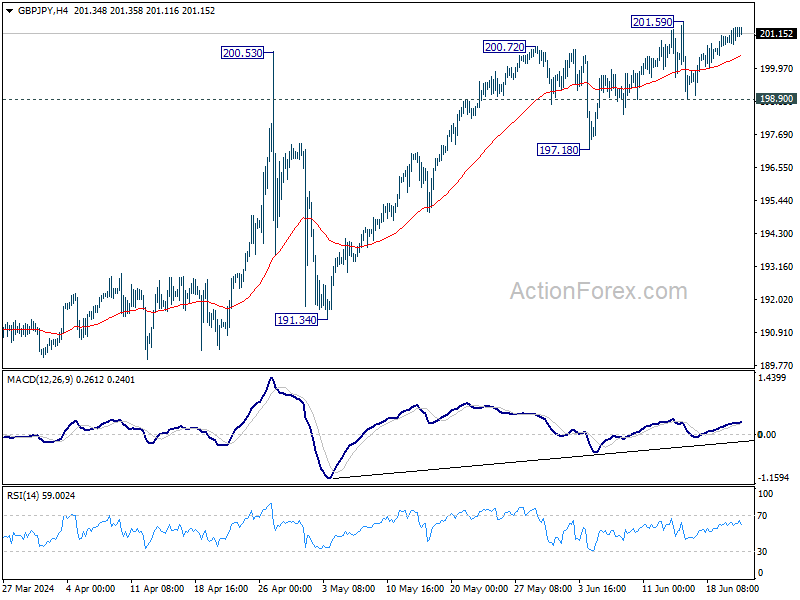

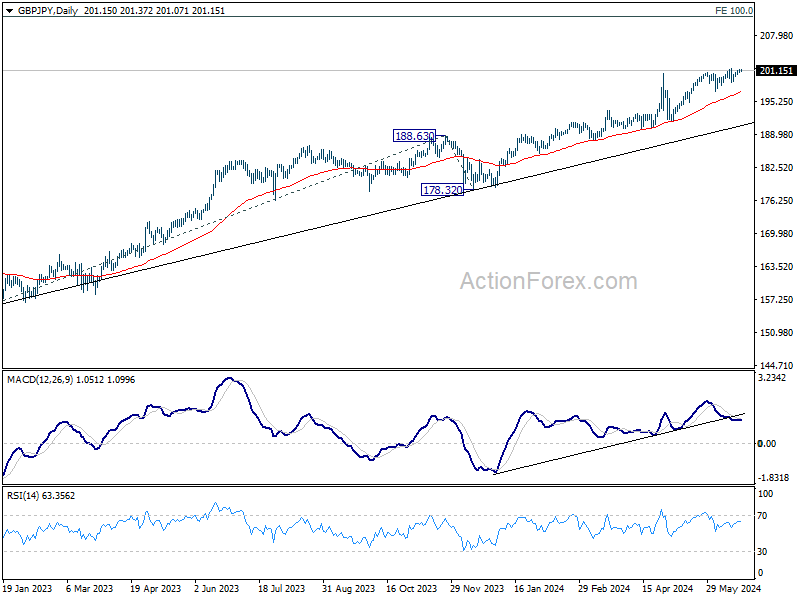

GBP/JPY Daily Outlook

Daily Pivots: (S1) 200.82; (P) 201.10; (R1) 201.45; More...

GBP/JPY is staying below 201.59 resistance for now and intraday bias stays neutral first. Further rally is expected as long as 198.90 support holds. Firm break of 201.59 will resume larger up trend. However, on the downside, break of 198.90 will turn bias back to the downside for deeper pullback to 197.18 support instead.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

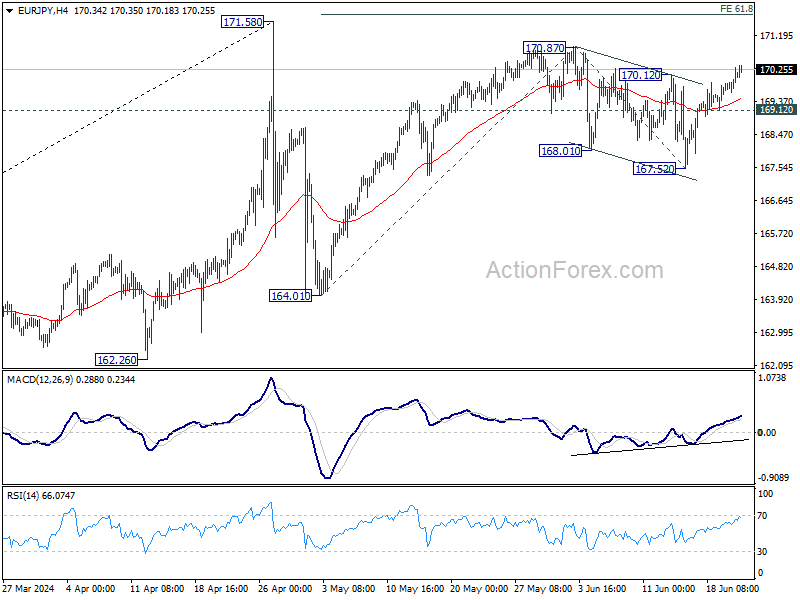

EUR/JPY Daily Outlook

Daily Pivots: (S1) 169.70; (P) 170.01; (R1) 170.40; More...

EUR/JPY's break of 170.12 resistance suggests that corrective fall from 170.87 has completed with three waves down to 167.52. Rise from 164.01 might be ready to resume. Intraday bias is back on the upside for 170.87 first. Firm break there will target 61.8% projection of 164.01 to 170.87 from 167.52 at 171.75. On the downside, break of 169.12 minor support will dampen this bullish case and turn intraday bias neutral gain first.

In the bigger picture, as long as 55 W EMA (now at 159.83) holds, price actions from 171.58 medium term top are seen as as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue as a later stage. Firm break of 171.58 will target 100% projection of 139.05 to 164.29 from 153.15 at 178.38. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

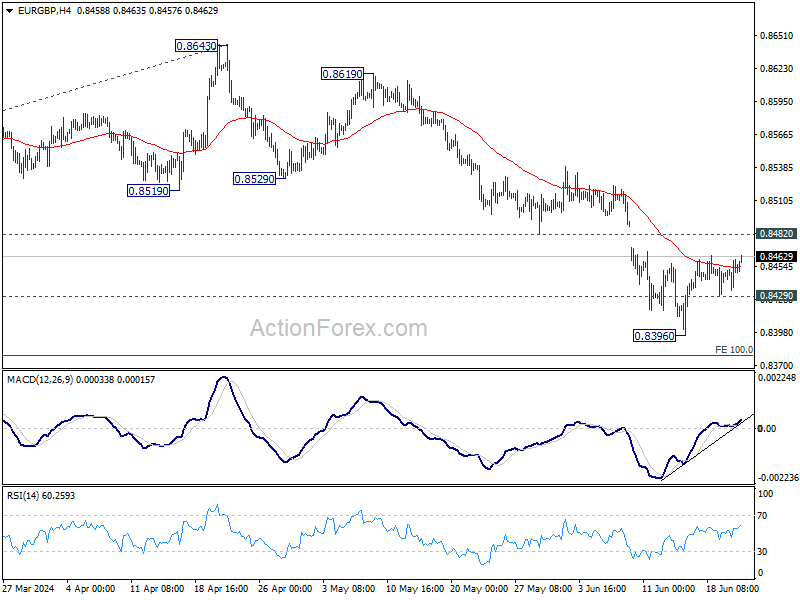

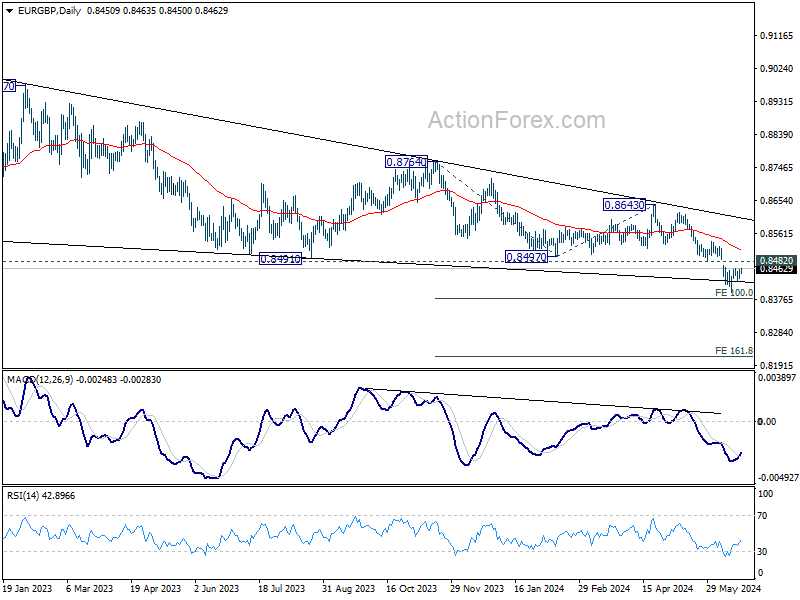

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8440; (P) 0.8451; (R1) 0.8466; More...

Intraday bias in EUR/GBP remains neutral for the moment. Consolidations form 0.8396 could continue with stronger recovery. But outlook will stay bearish as long as 0.8482 support turned resistance holds. On the downside, below 0.8429 minor support will bring retest of 0.8396 low first. Further break there will resume larger down trend to 0.8376 projection level next.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

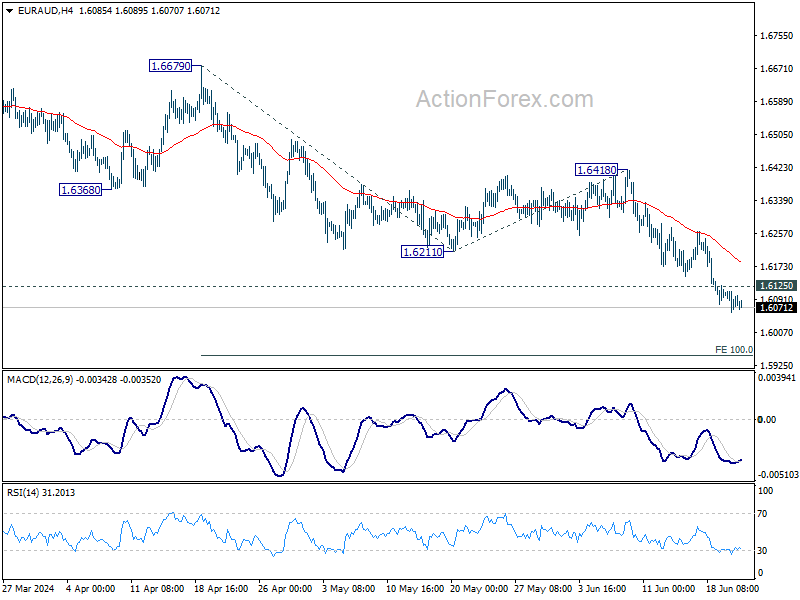

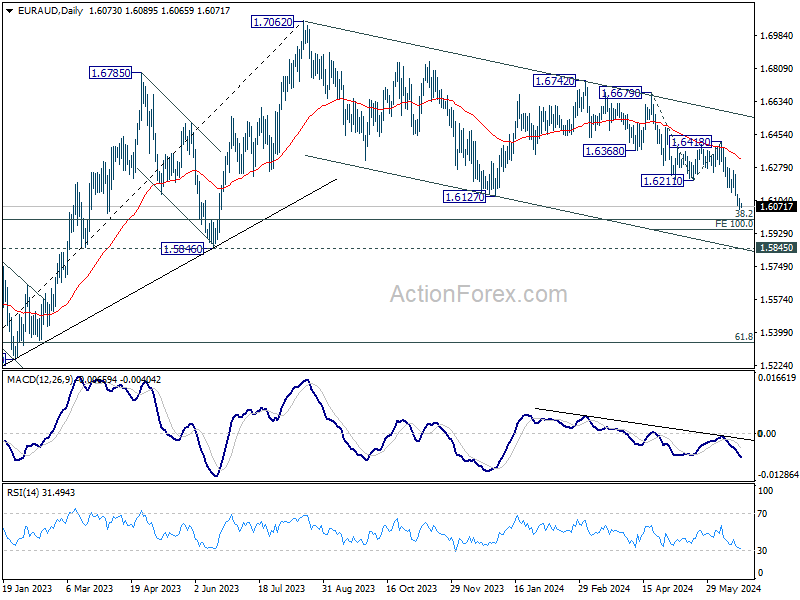

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6054; (P) 1.6085; (R1) 1.6110; More...

Intraday bias in EUR/AUD remains on the downside for now, despite some loss of momentum as seen in 4H MACD. Current down trend should target 100% projection of 1.6679 to 1.6211 from 1.6418 at 1.5950. On the upside, above 1.6125 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another decline.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

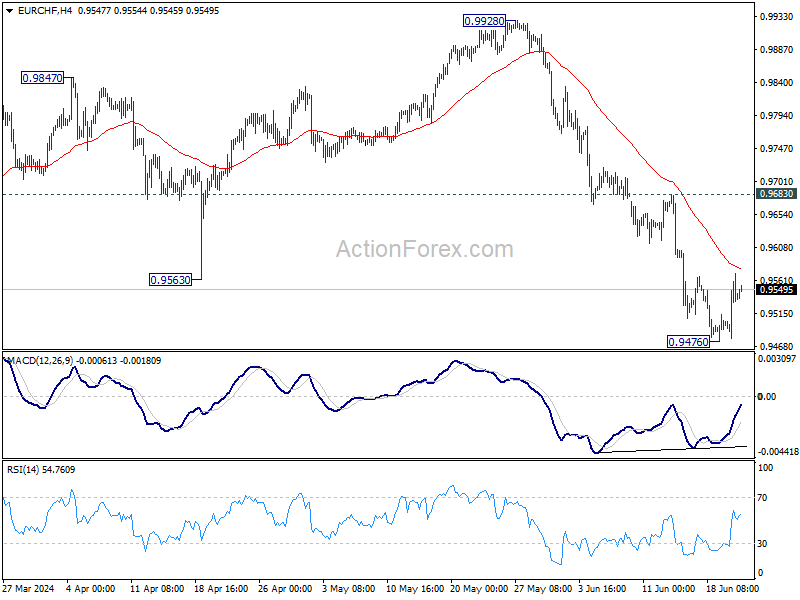

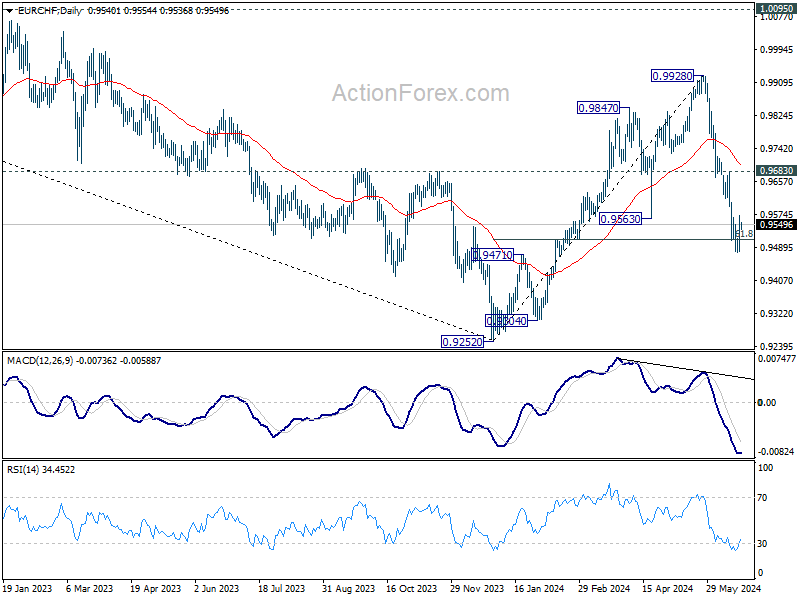

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9490; (P) 0.9531; (R1) 0.9582; More....

Intraday bias in EUR/CHF remains neutral for consolidation above 0.9476. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 0.9683 resistance holds, and fall from 0.9928 is expected to resume later. Below 0.9476 and sustained trading below 61.8% retracement of 0.9252 to 0.9928 at 0.9510 will raise the chance of long term down trend resumption, and target 0.9252 low next.

In the bigger picture, the break of 0.9563 support, as well as 55 W EMA (now at 0.9672) argues that rebound from 0.9252 has completed at 0.9928. Medium term bearish is maintained with both 1.0095 resistance intact. Firm break of 0.9252 will resume the down trend from 1.2004 (2018 high).

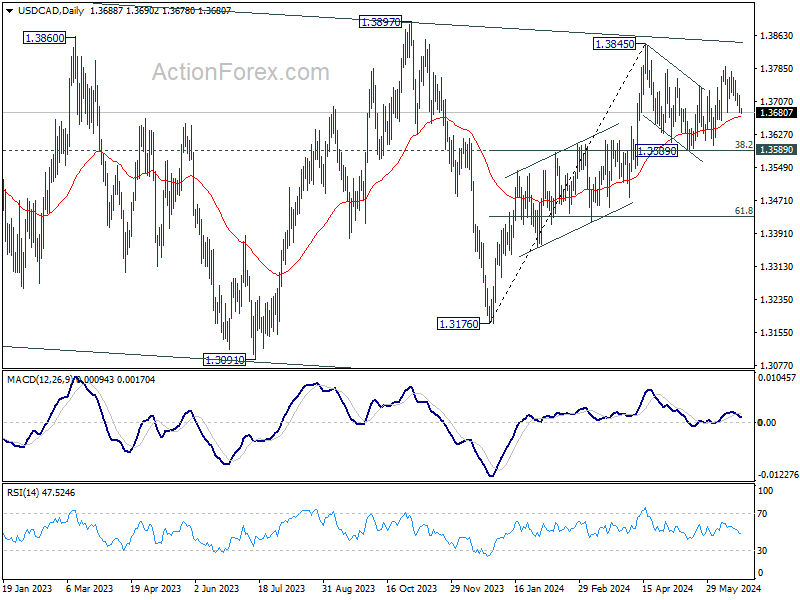

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3674; (P) 1.3697; (R1) 1.3713; More...

No change in USD/CAD's outlook as range trading continues below 1.3790. Corrective fall from 1.3845 should have completed already. Further rally is expected as long as 1.3662 support holds. Break of 1.3790 will target a retest on 1.3845 first. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

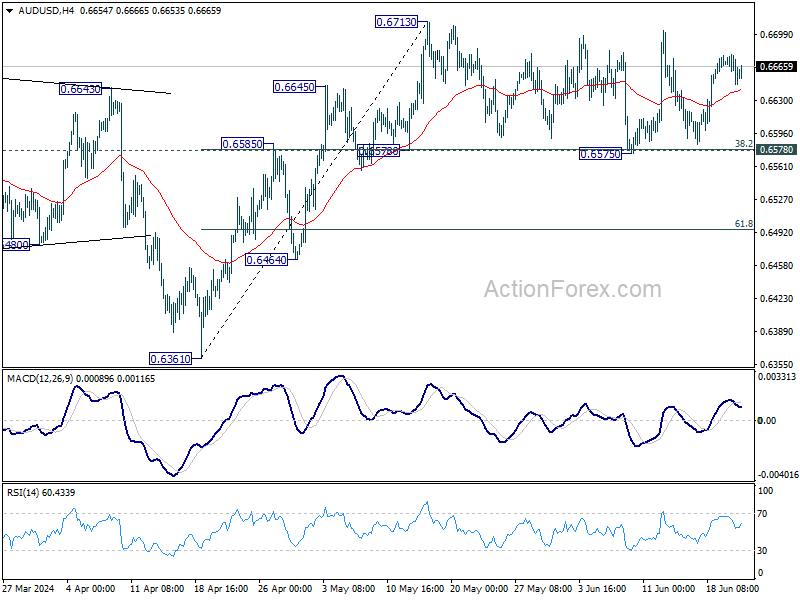

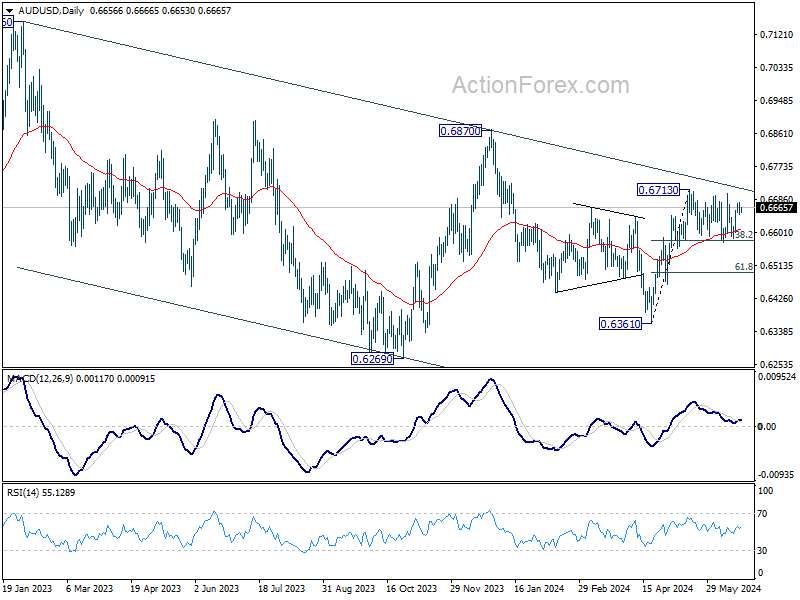

AUD/USD Daily Report

Daily Pivots: (S1) 0.6643; (P) 0.6661; (R1) 0.6674; More...

No change in AUD/USD's outlook as range trading continues below 0.6713. Intraday bias remains neutral for the moment. Further rally remains in favor with 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) intact. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

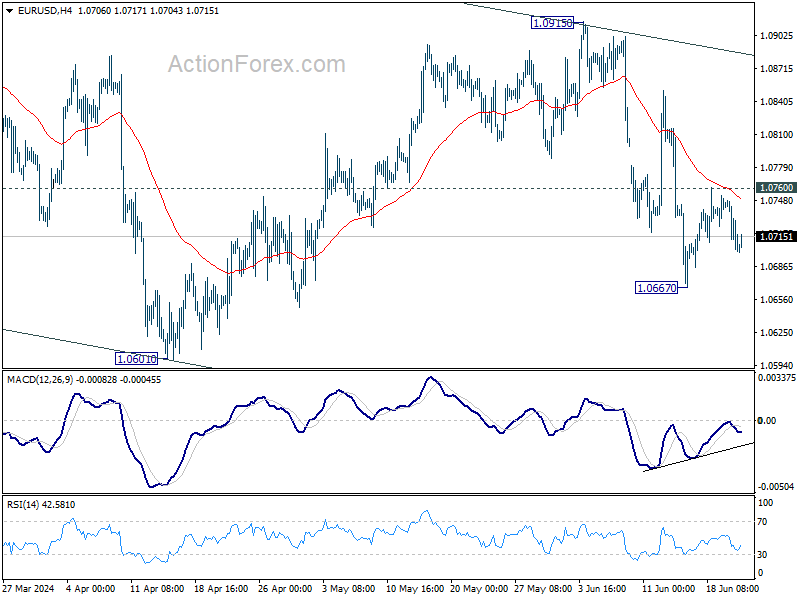

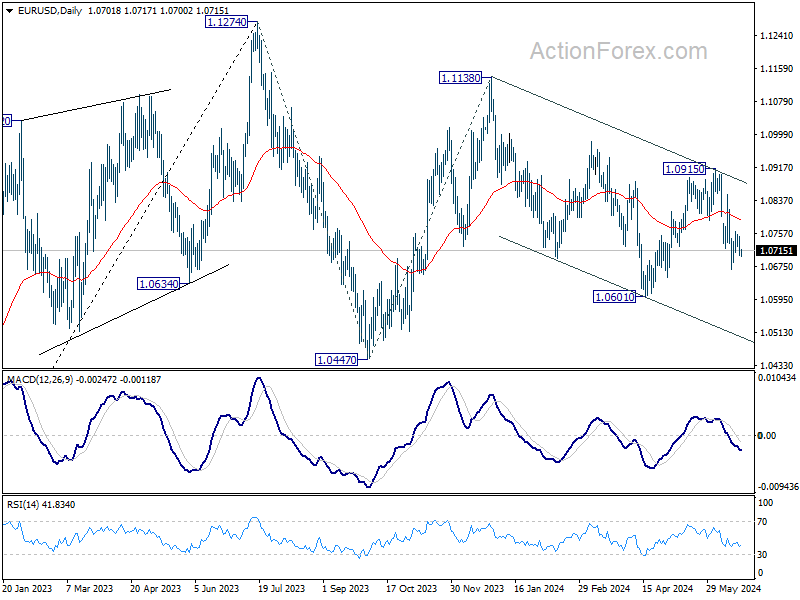

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0686; (P) 1.0719; (R1) 1.0735; More....

Intraday bias in EUR/USD remains neutral first and further decline is still expected. Break of 1.0667 will resume the fall from 1.0915, as another leg in the larger corrective pattern. Next target is 1.0601 low. However, break of 1.0760 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly further to 100% projection of 1.1274 to 1.0447 from 1.1138 at 1.0311. For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

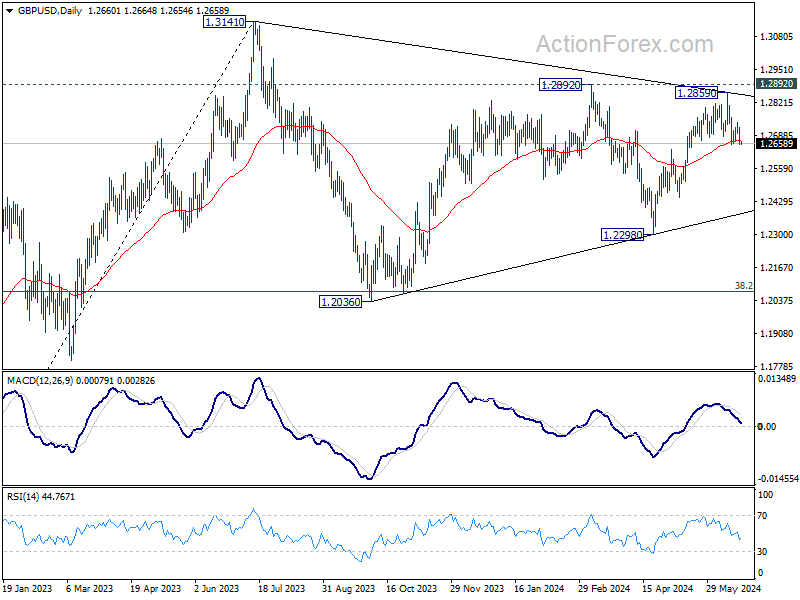

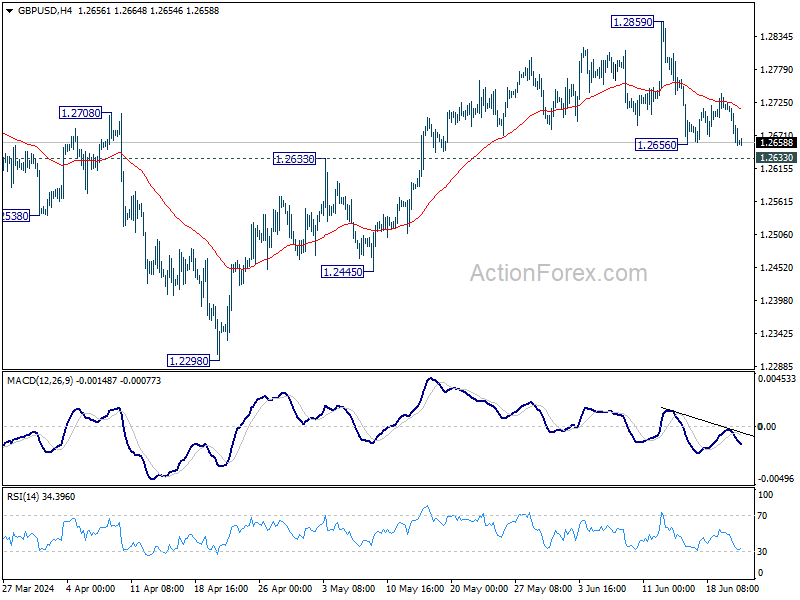

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2633; (P) 1.2679; (R1) 1.2704; More...

Intraday bias in GBP/USD remains neutral for the moment. While consolidation from 1.2656 could extend, risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.